|

시장보고서

상품코드

1942450

미생물 검사 시장 예측(-2031년) : 제품(기기, 시약 및 키트, 소모품), 기술(기존형(수동 계수, 배양), 신속형(핵산, 생존성)), 최종사용자별(제약, 바이오테크놀러지, 식품, 물, 환경 검사)Microbiology Testing Market by Product (Instrument, Reagent & Kit, Consumable), Technology (Traditional (Manual Counting, Culture), Rapid (Nucleic Acid, Viability)), End User (Pharma, Biotech, Food, Water, Environmental Testing)-Global Forecast to 2031 |

||||||

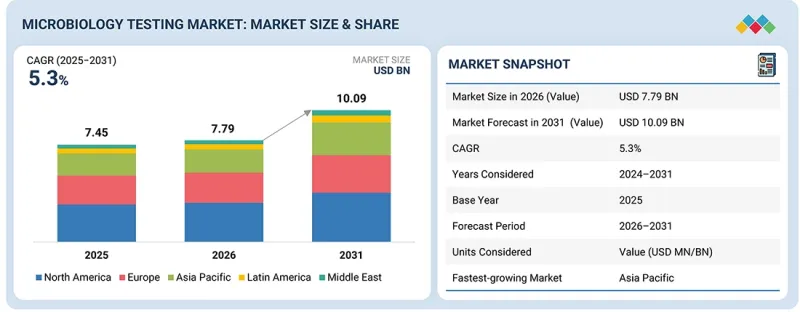

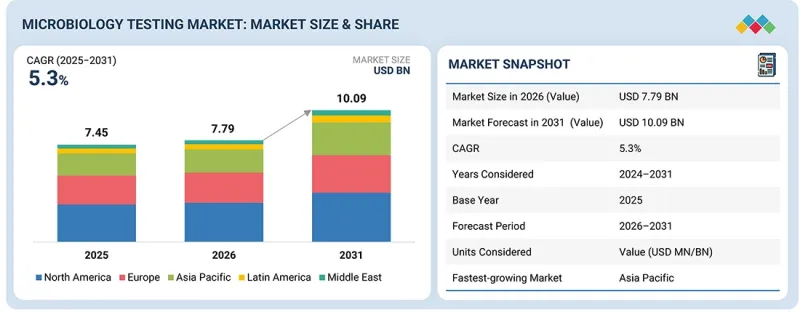

세계의 미생물 검사 시장 규모는 예측 기간 중 CAGR 5.3%로 성장하며, 2026년 77억 9,000만 달러에서 2031년에는 100억 9,000만 달러에 달할 것으로 전망되고 있습니다.

식품, 물, 환경 분야의 오염 위험 증가, 산업 생산 증가, 검사 기술의 발전으로 인해 시장은 빠르게 성장할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 기술, 병원체 유형, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

오염 관리, 규제 준수, 제품 안전에 대한 관심 증가와 더불어 신속 검사 및 자동화 기술의 혁신이 정확하고 신뢰할 수 있는 미생물 검사 솔루션에 대한 수요를 주도하고 있습니다. 고급 검사 시스템의 비용과 저비용 솔루션의 편차가 시장 성장을 저해할 수 있지만, 조사 방법의 지속적인 개선과 다양한 산업 분야에서의 채택 확대가 결합하여 시장 확대를 촉진할 것으로 예측됩니다.

"제약 및 생명공학 기업 부문이 예측 기간 중 가장 큰 시장 규모를 차지할 것으로 예측됩니다. "

최종사용자별로는 2025년 기준, 제약 및 생명공학 기업이 가장 큰 점유율을 차지했습니다. 의약품 제조 및 생명공학 연구에서의 오염 관리, 제품 안전 및 규제 준수에 대한 중요성 때문에 제약 및 생명공학 분야가 가장 큰 규모를 차지하고 있습니다. 이들 산업은 특히 생물제제, 백신, 치료제의 무균성, 품질, 안전성을 보장하기 위해 미생물 검사에 크게 의존하고 있습니다. FDA 및 EMA와 같은 엄격한 규제 요건에 따라 원자재 검증부터 최종 제품 출하까지 모든 생산 단계에서 엄격한 미생물 검사가 의무화되어 있습니다. 또한 질병의 확산과 새로운 치료법 및 요법에 대한 수요 증가로 인해 미생물 검사 솔루션에 대한 수요가 지속적으로 증가하고 있으며, 제약 및 생명공학 기업이 이러한 서비스의 가장 큰 수요처가 되고 있습니다.

"박테리아 제품 부문이 가장 큰 시장 점유율을 차지합니다. "

병원체 유형별로는 세균 오염이 다양한 산업에 광범위하게 존재하고 영향을 미치기 때문에 세균 부문이 가장 큰 규모를 차지하고 있습니다. 박테리아는 식품 및 음료, 수처리, 환경 모니터링 등의 분야에서 가장 흔한 오염 문제 중 하나입니다. 부패, 질병, 품질 문제를 일으키기 때문에 제품 안전, 규정 준수, 공중 보건을 보장하기 위해 세균 검사에 대한 수요가 높아지고 있습니다. 또한 세균성 병원체를 검출하고 식별하기 위해 확립된 신뢰할 수 있는 방법과 규제 요건이 결합되어 미생물 검사에서 세균 부문의 우위를 더욱 강화하고 있습니다.

"아시아태평양이 예측 기간 중 가장 빠른 성장세를 보일 것으로 예측됩니다. "

아시아태평양은 급속한 산업화, 의료 투자 증가, 산업 전반의 오염 관리에 대한 관심 증가로 인해 가장 빠르게 성장하는 시장입니다. 이 지역에서는 식품 및 음료, 수처리, 환경 모니터링 등의 분야에서 괄목할 만한 성장세를 보이고 있으며, 이들 분야는 모두 안전과 규제 준수를 보장하기 위해 광범위한 미생물 검사가 필요합니다. 또한 의료 인프라의 개선과 식품 안전 및 공중 보건에 대한 인식이 높아지면서 검사 솔루션에 대한 수요가 증가하고 있습니다. 중국, 인도, 동남아시아 국가 등의 정부 노력과 규제 개선은 시장 성장을 더욱 촉진하는 한편, 첨단 자동화 미생물 검사 기술의 채택은 업무의 효율성과 정확성을 향상시키는 데 기여하고 있습니다. 이러한 요인들이 복합적으로 작용하여 아시아태평양은 미생물 검사 분야에서 가장 빠르게 성장하는 시장으로 자리매김하고 있습니다.

또한 북미는 미생물 검사의 주요 시장으로, 제품 안전과 컴플라이언스 준수를 위한 검사 수요를 창출하는 강력한 규제 프레임워크에 의해 주도되고 있습니다. 이 지역은 효율성과 정확성을 향상시키는 첨단 자동화 검사 솔루션을 도입하는 데 있으며, 선도적인 위치에 있습니다. 또한 제약, 생명공학, 식품, 수처리 등 다양한 산업이 존재하는 북미에서는 신뢰할 수 있는 미생물 검사가 지속적으로 요구되고 있습니다. 잘 구축된 의료 및 산업 인프라와 연구개발에 대한 막대한 투자가 결합되어 이 지역 시장 리더로서의 입지를 더욱 공고히 하고 있습니다.

세계의 미생물 검사 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 미생물 검사 시장 : 제품별

제10장 미생물 검사 시장 : 수량 분석

제11장 미생물 검사 시장 : 기술별

제12장 미생물 검사 시장 : 병원체 유형별

제13장 미생물 검사 시장 : 최종사용자별

제14장 미생물 검사 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.03.09The global microbiology testing market is projected to reach USD 10.09 billion by 2031, up from USD 7.79 billion in 2026, at a CAGR of 5.3% during the forecast period. The market is expected to grow rapidly due to rising contamination risks in the food, water, and environmental sectors, increased industrial production, and advances in testing technologies.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Technology, Pathogen Type, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

A growing focus on contamination control, regulatory compliance, and product safety, along with innovations in rapid testing and automation, is driving demand for accurate and reliable microbiology testing solutions. However, concerns about the cost of advanced testing systems and variability in low-cost solutions may restrain market growth. Nonetheless, continuous improvements in testing methodologies, coupled with increasing adoption across various industries, are expected to fuel market expansion.

The pharmaceutical & biotech companies segment is expected to have the largest market during the forecast period.

By end user, the market is segmented into pharmaceutical & biotech companies, food & beverage companies, environmental & water testing, cosmetics & personal-care companies, and other end users. In 2025, pharmaceutical & biotech companies accounted for the largest share of the market. The pharmaceutical & biotech segment is the largest in the microbiology testing market due to the critical need for contamination control, product safety, and regulatory compliance across drug manufacturing and biotechnological research. These industries rely heavily on microbiological testing to ensure the sterility, quality, and safety of their products, particularly biologics, vaccines, and therapeutic compounds. Stringent regulatory requirements, such as those from the FDA and EMA, mandate rigorous microbial testing at every stage of production, from raw material validation to final product release. Furthermore, the growing prevalence of diseases and the need for new treatments and therapies continue to drive significant demand for microbiology testing solutions, making pharmaceutical & biotech companies the largest consumers of these services.

The bacterial products segment accounted for the largest market share in the microbiology testing market.

The microbiology testing market is segmented by pathogen type into bacterial, viral, fungal, and other pathogens. The bacterial segment is the largest within this category due to the widespread presence and impact of bacterial contamination across various industries. Bacteria are among the most common pathogens in contamination issues across sectors such as food and beverage, water treatment, and environmental monitoring. Their ability to cause spoilage, disease, and quality issues drives strong demand for bacterial testing to ensure product safety, regulatory compliance, and public health. Additionally, well-established, reliable methods for detecting and identifying bacterial pathogens, along with regulatory mandates, further strengthen the dominance of the bacterial segment in microbiology testing.

The Asia Pacific is expected to be the fastest-growing market for microbiology testing during the forecast period.

The global microbiology testing market is segmented into six regions: North America, Europe, the Asia Pacific, Latin America, the Middle East & Africa. The Asia Pacific is the fastest-growing market in the microbiology testing sector, driven by rapid industrialization, rising healthcare investments, and a growing focus on contamination control across industries. The region is seeing strong growth in sectors such as food and beverage, water treatment, and environmental monitoring, all of which require extensive microbiological testing to ensure safety and regulatory compliance. Additionally, improving healthcare infrastructure, coupled with rising awareness of food safety and public health, is driving demand for testing solutions. Government initiatives and regulatory developments in countries such as China, India, and across Southeast Asia further support market growth, while the adoption of advanced and automated microbiology testing technologies helps streamline operations and improve accuracy. These factors collectively position Asia-Pacific as the fastest-growing market for microbiology testing.

North America is the leading market for microbiology testing, driven by a strong regulatory framework that creates high demand for testing to ensure product safety and compliance. The region is a leader in adopting advanced, automated testing solutions that improve efficiency and accuracy. Additionally, North America's diverse industries, including pharmaceuticals, biotechnology, food, and water, continually require reliable microbiology testing. The region's well-established healthcare and industrial infrastructure, combined with significant investments in research and development, further solidifies its position as the market leader.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

- By Designation: C Level: 27%, Director Level: 18%, and Others: 55%

- By Region: North America: 51%, Europe: 21%, Asia Pacific: 18%, Latin America: 6%, and Middle East & Africa: 4%

- Note 1: Companies are classified into tiers based on their total revenue. As of 2024, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the microbiology testing market are bioMerieux (France), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Becton, Dickinson and Company (US), and Neogen Corporation (US).

Research Coverage

This report examines the microbiology testing market by product, technology, pathogen type, end user, and region. It also examines key factors (drivers, restraints, opportunities, and challenges) influencing market growth and provides an in-depth analysis of the competitive landscape among market leaders. Furthermore, the report analyzes micro-markets by their individual growth trends. It forecasts market segment revenue for five major regions (and the respective countries within each region).

Reasons to Buy the Report

The report will enable established firms and smaller entrants to gauge the market's pulse, which, in turn, will help them gain a larger market share. Firms purchasing the report could use one or more of the strategies listed below to strengthen their market presence.

This report provides insights into the following pointers:

- Analysis of key Drivers (Technological advancements in rapid microbiology testing, Increased funding for R&D, Rising food recalls due to non-compliant food products, Rising demand from cosmetics & personal care industry)

- Restraints (Complexity in testing techniques, High Capital investments, and low cost benefit ratio)

- Opportunities (Popularity of digital and automated testing platforms, Technological advancements in the testing industry)

- Challenges (Operational barriers, Increasing cost of procuring microbiology testing equipment)

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the microbiology testing market

Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product launches in the microbiology testing market

Market Development: Comprehensive information on lucrative emerging regions

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the microbiology testing market

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players, such as bioMerieux (France), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Becton, Dickinson and Company (US), and Neogen Corporation (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 FASTEST-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 MICROBIOLOGY TESTING MARKET OVERVIEW

- 3.2 MICROBIOLOGY TESTING MARKET, BY PRODUCT

- 3.3 MICROBIOLOGY TESTING MARKET, BY TECHNOLOGY

- 3.4 MICROBIOLOGY TESTING MARKET, BY PATHOGEN TYPE

- 3.5 MICROBIOLOGY TESTING MARKET, BY END USER

- 3.6 MICROBIOLOGY TESTING MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Technological advancements in rapid microbiology testing

- 4.2.1.2 Increased funding for R&D

- 4.2.1.3 Rising food recalls due to non-compliant food products

- 4.2.1.4 Rising demand from cosmetics & personal care industry

- 4.2.2 RESTRAINTS

- 4.2.2.1 Complexity in testing techniques

- 4.2.2.2 High Capital investments and low cost-benefit ratio

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Popularity of digital and automated testing platforms

- 4.2.3.2 Technological advancements in testing industry

- 4.2.4 CHALLENGES

- 4.2.4.1 Operational barriers

- 4.2.4.2 Increasing cost of procuring microbiology testing equipment

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MICROBIOLOGY TESTING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF MICROBIOLOGY TESTING, BY PRODUCT

- 5.6.2 AVERAGE SELLING PRICE TREND OF MICROBIOLOGY TESTING PRODUCTS, BY KEY PLAYER

- 5.6.3 AVERAGE SELLING PRICE TREND OF MICROBIOLOGY TESTING PRODUCTS, BY REGION

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 3822)

- 5.7.2 EXPORT SCENARIO (HS CODE 3822)

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 YOUNGS SEAFOOD ACCELERATED FOOD TESTING WITH VIDAS

- 5.11.2 RAPID MICROBIOLOGICAL METHOD CASE STUDY FOR ADVANCED THERAPY MEDICINAL PRODUCTS

- 5.11.3 RAPID DETECTION METHOD OF BACTERIAL PATHOGENS IN SURFACE WATERS AND NEW RISK INDICATOR FOR WATER PATHOGENIC POLLUTION

- 5.12 IMPACT OF 2025 US TARIFFS ON MICROBIOLOGY TESTING MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 KEY IMPACT ON COUNTRY/REGION

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Pharmaceutical & biotech companies

- 5.12.5.2 Food & beverage companies

- 5.12.5.3 Environmental & water testing

- 5.12.5.4 Cosmetics & personal care companies

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AUTOMATED MULTIPLEX PCR SYSTEMS

- 6.1.2 BIOSENSORS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 FOOD & WATER SAFETY MONITORING TOOLS

- 6.2.2 ANTIMICROBIAL RESISTANCE TESTING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATION

- 6.6 IMPACT OF AI/GENERATIVE AI ON MICROBIOLOGY TESTING MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 TOP USE CASES AND MARKET POTENTIAL

- 6.6.3 USE CASE

- 6.6.3.1 Adoption of Gen AI by CarbConnect to achieve accuracy and consistency in diagnostics

- 6.6.4 EVOLVING ADJACENT ECOSYSTEM THROUGH ADOPTION OF GEN AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ENVIRONMENTAL IMPACT AND ECO-FRIENDLY INITIATIVES IN MICROBIOLOGY TESTING

- 7.2.1.1 Eco-friendly initiatives

- 7.2.1 ENVIRONMENTAL IMPACT AND ECO-FRIENDLY INITIATIVES IN MICROBIOLOGY TESTING

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 MICROBIOLOGY TESTING MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 INSTRUMENTS

- 9.2.1 WIDESPREAD ADOPTION OF AUTOMATED AND HIGH-THROUGHPUT LABORATORY INSTRUMENTS TO SUPPORT MICROBIOLOGY TESTING DEMAND

- 9.2.2 INCUBATORS

- 9.2.2.1 Controlled environmental conditions to enable reliable microbial growth and detection

- 9.2.3 MICROSCOPES

- 9.2.3.1 Direct visualization and morphological analysis of microorganisms

- 9.2.4 COLONY COUNTERS

- 9.2.4.1 Accurate enumeration of microbial colonies to support quality assurance

- 9.2.5 MASS SPECTROMETERS

- 9.2.5.1 Rapid and accurate microbial identification through advanced mass spectrometry methods

- 9.2.6 AUTOMATED CULTURE SYSTEMS

- 9.2.6.1 High-throughput systems supporting standardized microbiology workflows

- 9.2.7 OTHER INSTRUMENTS

- 9.3 REAGENTS & KITS

- 9.3.1 HIGH RECURRING DEMAND FOR STANDARDIZED AND READY-TO-USE REAGENTS & KITS TO SUPPORT MARKET GROWTH

- 9.4 CONSUMABLES

- 9.4.1 CONSISTENT HIGH-VOLUME CONSUMPTION OF DISPOSABLE LABORATORY SUPPLIES TO FUEL ROUTINE MICROBIOLOGY TESTING MARKET

10 MICROBIOLOGY TESTING MARKET: VOLUME ANALYSIS

- 10.1 INTRODUCTION

- 10.2 US: VOLUME OF PHARMA INCUBATOR INSTALLED BASE

11 MICROBIOLOGY TESTING MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 TRADITIONAL MICROBIOLOGY METHODS (TMM)

- 11.2.1 WIDESPREAD REGULATORY ACCEPTANCE AND COST-EFFECTIVENESS TO SUPPORT CONTINUED ADOPTION

- 11.2.2 CULTURE METHODS

- 11.2.2.1 Continued reliance on culture-based techniques to support routine microbiology testing

- 11.2.3 MICROSCOPY METHODS

- 11.2.3.1 Rapid preliminary microbial screening to support contamination investigations

- 11.2.4 MANUAL COUNTING METHODS

- 11.2.4.1 Regulatory acceptance of plate count techniques to maintain widespread usage

- 11.2.5 STAINING TECHNIQUES

- 11.2.5.1 Low-cost and effective microbial differentiation methods to support quality control

- 11.2.6 OTHER TRADITIONAL MICROBIOLOGY METHODS

- 11.3 RAPID MICROBIOLOGY METHODS (RMM)

- 11.3.1 RAPID MICROBIOLOGY METHODS ENABLE FASTER CONTAMINATION DETECTION AND IMPROVED TESTING EFFICIENCY

- 11.3.2 GROWTH-BASED RAPID MICROBIOLOGY TESTING

- 11.3.2.1 Growing demand for growth-based rapid microbiology testing to drive market growth

- 11.3.3 CELLULAR COMPONENT-BASED RAPID MICROBIOLOGY TESTING

- 11.3.3.1 High level of sensitivity, accuracy, and specificity associated with this method to boost market

- 11.3.4 NUCLEIC ACID-BASED RAPID MICROBIOLOGY TESTING

- 11.3.4.1 High accuracy associated with nucleic acid-based methods to favor market growth

- 11.3.5 VIABILITY-BASED RAPID MICROBIOLOGY TESTING

- 11.3.5.1 Near real-time detection and improved accuracy to drive demand

12 MICROBIOLOGY TESTING MARKET, BY PATHOGEN TYPE

- 12.1 INTRODUCTION

- 12.2 BACTERIAL

- 12.2.1 WIDESPREAD OCCURRENCE OF BACTERIAL CONTAMINATION ACROSS INDUSTRIES TO SUPPORT MARKET DOMINANCE

- 12.3 VIRAL

- 12.3.1 INCREASING FOCUS ON VIRAL SAFETY AND ENVIRONMENTAL SURVEILLANCE TO DRIVE SEGMENT GROWTH

- 12.4 FUNGAL

- 12.4.1 RISING INCIDENCE OF YEAST AND MOLD CONTAMINATION TO FUEL TESTING DEMAND

- 12.5 OTHER PATHOGENS

13 MICROBIOLOGY TESTING MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 PHARMACEUTICAL & BIOTECH COMPANIES

- 13.2.1 STRINGENT GMP AND CONTAMINATION CONTROL REQUIREMENTS TO DRIVE TESTING DEMAND

- 13.3 FOOD & BEVERAGE COMPANIES

- 13.3.1 STRINGENT FOOD SAFETY REGULATIONS AND QUALITY CONTROL TO SUPPORT MARKET GROWTH

- 13.4 ENVIRONMENTAL & WATER TESTING

- 13.4.1 GROWING FOCUS ON WATER SAFETY AND ENVIRONMENTAL MONITORING TO DRIVE DEMAND

- 13.5 COSMETICS & PERSONAL CARE COMPANIES

- 13.5.1 MICROBIAL SAFETY AND PRODUCT STABILITY REQUIREMENTS TO SUPPORT MARKET GROWTH

- 13.6 OTHER END USERS

14 MICROBIOLOGY TESTING MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Increasing adoption of technologically advanced products in US to favor market growth

- 14.2.2 CANADA

- 14.2.2.1 Favorable environment for R&D to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Increase in investments and funding by government to fuel market growth

- 14.3.2 UK

- 14.3.2.1 High prevalence of contaminated food to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Rise in R&D expenditure to favor market growth

- 14.3.4 ITALY

- 14.3.4.1 Increased adoption of advanced diagnostic technologies and growing government healthcare investments to drive market

- 14.3.5 SPAIN

- 14.3.5.1 Water monitoring mandate to boost market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 High-profile contamination events and export standards to propel market

- 14.4.2 JAPAN

- 14.4.2.1 Stringent safety laws and foodborne outbreaks to accelerate market

- 14.4.3 INDIA

- 14.4.3.1 Growth in private and public investments in healthcare systems to drive adoption of microbiology testing products

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Increasing demand for infection control products to support market growth

- 14.4.5 AUSTRALIA

- 14.4.5.1 Increase in awareness about antimicrobial resistance to fuel market

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Need for manufacturers to comply with ANVISA's rules to drive demand

- 14.5.2 MEXICO

- 14.5.2.1 Expanding microbiology testing capacity through trade and food safety enforcement to drive market

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 15.3 REVENUE ANALYSIS, 2022-2024

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Regional footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Technology footprint

- 15.5.5.5 End user footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 List of startups/SMEs

- 15.6.5.2 Competitive benchmarking of startups/SMEs

- 15.6.5.2.1 Competitive benchmarking of startups/SMEs (1/2)

- 15.6.5.2.2 Competitive benchmarking of startups/SMEs (2/2)

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 BIOMERIEUX

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches and approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 THERMO FISHER SCIENTIFIC INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches & approvals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 MERCK KGAA

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 BECTON, DICKINSON AND COMPANY (BD)

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 NEOGEN CORPORATION

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product/Service launches and approvals

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 QIAGEN

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.7 BIO-RAD LABORATORIES, INC.

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.8 BRUKER

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.9 SHIMADZU CORPORATION

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product/Service launches and approvals

- 16.1.9.3.2 Expansions

- 16.1.10 CHARLES RIVER LABORATORIES

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product/Service launches and approvals

- 16.1.11 EUROFINS SCIENTIFIC

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.12 IDEXX

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product/Service launches and approvals

- 16.1.1 BIOMERIEUX

- 16.2 OTHER PLAYERS

- 16.2.1 HARDY DIAGNOSTICS

- 16.2.2 CHARM SCIENCES

- 16.2.3 MICROBIOLOGICS

- 16.2.4 LIOFILCHEM S.R.L.

- 16.2.5 R-BIOPHARM

- 16.2.6 ROMER LABS DIVISION HOLDING

- 16.2.7 HYGIENA LLC

- 16.2.8 HIMEDIA LABORATORIES

- 16.2.9 CONDALAB

- 16.2.10 E&O LABORATORIES LTD

- 16.2.11 MAST GROUP LTD.

- 16.2.12 MEDICAL WIRE & EQUIPMENT

- 16.2.13 HACH

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.2 RESEARCH APPROACH

- 17.2.1 SECONDARY DATA

- 17.2.1.1 Key secondary sources

- 17.2.1.2 Key data from secondary sources

- 17.2.2 PRIMARY DATA

- 17.2.2.1 Primary sources

- 17.2.2.2 Key data from primary sources

- 17.2.2.3 Key industry insights

- 17.2.2.4 Breakdown of primary interviews

- 17.2.1 SECONDARY DATA

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.1.1 Approach 1: Company revenue estimation approach

- 17.3.1.2 Approach 2: Presentations of companies and primary interviews

- 17.3.1.3 Growth forecast

- 17.3.1.4 CAGR projections

- 17.3.2 TOP-DOWN APPROACH

- 17.3.1 BOTTOM-UP APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 MARKET SHARE ASSESSMENT

- 17.6 RESEARCH ASSUMPTIONS

- 17.6.1 PARAMETRIC ASSUMPTIONS

- 17.7 RESEARCH LIMITATIONS

- 17.8 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS