|

시장보고서

상품코드

1942451

단열 금속 패널 시장 예측(-2030년) : 금속 유형별, 단열재별, 용도별, 최종 용도별, 지역별Insulated Metal Panels Market by Metal Type (Steel, Aluminum, Others), Insulation Material (PIR/PUR, Polystyrene, Mineral Wool), By Application (Exterior Wall, Others), By End-use (Residential, Non-residential), and Region - Global Forecast to 2030 |

||||||

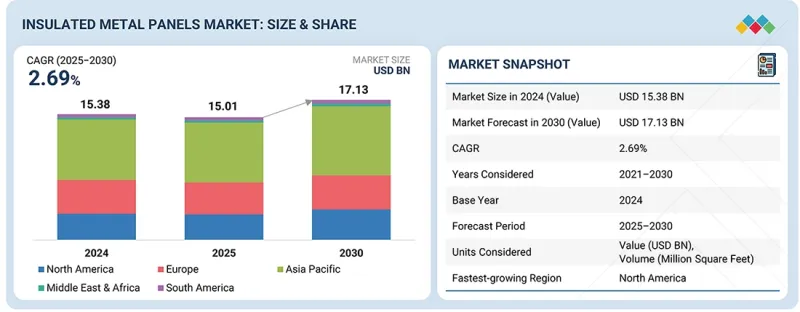

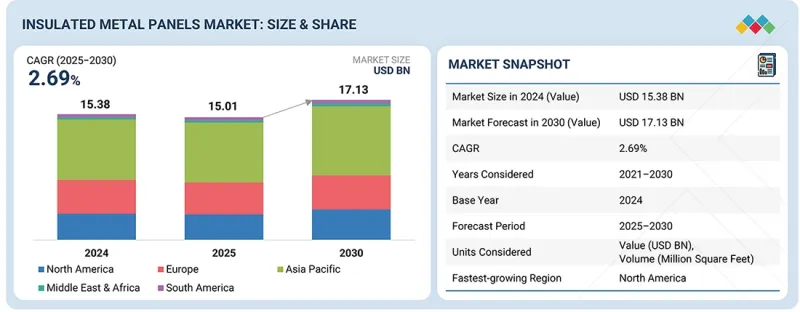

세계의 단열 금속 패널 시장 규모는 2025년에 150억 1,000만 달러, 2030년까지 171억 3,000만 달러에 달할 것으로 예측되며, 2025-2030년에 CAGR로 2.69%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러, 100만 평방피트 |

| 부문 | 금속 유형, 단열재, 용도, 최종 용도, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

도시화 수준이 높아지고, 특히 상산업 시설에서 신속하고 효율적이며 수명이 긴 건설 기술에 대한 수요가 증가함에 따라 시장이 확대될 것으로 예측됩니다. 정부는 이산화탄소 배출을 억제하기 위해 에너지 절약과 단열에 대한 요구사항을 더욱 엄격하게 시행하고 있습니다.

"철강 부문이 2030년에 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

2030년, 철강 부문은 높은 강도, 내구성, 구조적 신뢰성으로 인해 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 스틸 패널은 내화성과 수명이 길어 산업 및 비주거용 건축에 사용하기에 적합합니다. 비용 효율성이 뛰어나며, 잘 구축된 공급망을 통해 폭넓게 이용할 수 있습니다.

"미네랄울 부문이 2025-2030년 가장 높은 CAGR을 보일 것으로 예측됩니다. "

미네랄울 부문은 우수한 내화 및 방음 특성으로 인해 2025-2030년 가장 높은 CAGR을 보일 것으로 예측됩니다. 특히 대규모 수용시설과 산업시설의 화재 예방에 대한 관심이 높아지면서 그 개발이 가속화되고 있습니다. 또한 미네랄울은 안전성을 해치지 않으면서도 우수한 단열 성능을 제공합니다.

"외벽 부문이 2030년에 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

외벽 부문은 단열성과 건축 외피 성능에 있으며, 매우 중요하므로 2030년까지 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이러한 우위는 상업용 및 산업용 건축물의 에너지 절약형 파사드에 대한 수요 증가에 의해 지원되고 있습니다. 또한 미적 유연성이 뛰어나며, 이는 채택을 더욱 촉진하고 있습니다.

"비주거 부문이 2025-2030년 동안 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

비주거 부문은 창고, 냉장시설, 공장, 데이터센터 건설 증가로 인해 2025-2030년 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 이러한 건물은 높은 열효율, 내구성, 빠른 설치가 요구되며, 단열 금속 패널이 선호되고 있습니다.

"북미의 단열 금속 패널 시장은 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예측됩니다. "

북미의 단열 금속 패널 시장은 에너지 절약 건축 기준과 화재 예방 조치의 강력한 시행으로 인해 예측 기간 중 가장 높은 CAGR을 보일 것으로 예측됩니다. 냉장창고, 데이터센터, 상업용 건설에 대한 투자 확대로 수요가 증가하고 있습니다. 또한 넷 제로 빌딩과 그린 빌딩에 대한 정부의 우대 정책도 이러한 패널의 채택을 촉진하고 있습니다.

세계의 단열 금속 패널 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI의 채택에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 단열 패널 시장 : 금속 유형별

제10장 단열 금속 패널 시장 : 단열재별

제11장 단열 금속 패널 시장 : 용도별

제12장 단열 금속 패널 시장 : 최종 용도별

제13장 단열 금속 패널 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.03.09The insulated metal panels market is projected to reach USD 15.01 billion in 2025 and USD 17.13 billion by 2030, at a CAGR of 2.69% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) Volume (Million Square Feet) |

| Segments | Metal Type, Insulation Material, Application, End-use, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The market will expand as high levels of urbanization increase demand for quick, efficient, and long-lasting construction technologies, particularly in commercial and industrial structures. Governments are becoming more rigorous in implementing energy-saving and thermal insulation requirements to curb carbon emissions.

"The steel segment is projected to capture the largest market share in 2030."

In 2030, the steel segment is expected to have the highest market share because of its high strength, durability, and structural reliability in building practice. It is also good in terms of fire resistance and long service life; hence it can be used in industrial and non-residential works. Steel panels are cost-effective and universally available, with well-established supply chains.

"The mineral wool segment is projected to exhibit the highest CAGR from 2025 to 2030."

The mineral wool segment is forecast to have the highest CAGR between 2025 and 2030, owing to its superior fire resistance and acoustic insulation. The growing emphasis on fire safety measures, particularly in buildings with large occupancies and on industrial premises, favors its development. It also offers strong thermal performance without compromising safety.

"The exterior walls segment is projected to capture the largest market share in 2030."

The exterior walls segment is expected to get the highest market share in 2030 because they are critical in thermal insulation and building envelope performance. Dominance is supported by increasing demand for the energy-efficient facade of commercial and industrial buildings. They are also aesthetically flexible, which further increases adoption.

"The non-residential segment is projected to have the highest CAGR from 2025 to 2030."

The non-residential segment will record the highest CAGR between 2025 and 2030, driven by increased construction of warehouses, cold storage facilities, factories, and data centers. These buildings require high thermal efficiency, durability, and rapid installation, with insulated metal panels preferred.

"The North America insulated metal panels market is projected to grow at the highest CAGR during the forecast period."

The North America insulated metal panel market is expected to have the highest CAGR over the forecast period, driven by the strong implementation of energy-efficient building codes and fire safety measures. Demand is increasing due to greater investment in cold storage, data centers, and commercial construction. The adoption of these panels is also being prompted by government incentives for net-zero and green buildings.

By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

By Designation: C-level Executives - 33, Directors - 33%, and Others - 34%

By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, South America - 10%, and Middle East & Africa - 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Kingspan Group (Ireland), Nucor Corporation (US), ArcelorMittal (Luxembourg), Recticel NV/SA (Belgium), and Tata Steel (India), among other companies, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the insulated metal panels market, covering their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the insulated metal panels market by metal type (steel, aluminum, and other metals), insulation material (PIR/PUR, polystyrene, mineral wool, and other materials), application (interior walls, exterior walls, roofs, ceilings, and other applications), end use (residential and non-residential), and region (Asia Pacific, North America, Europe, South America, and the Middle East & Africa). The report's scope includes detailed information on the drivers, restraints, challenges, and opportunities influencing the growth of the insulated metal panels market. A detailed analysis of key industry players provides insights into their business overviews, products offered, and key strategies, such as expansions, acquisitions, product launches, partnerships, agreements, and contracts, associated with the insulated metal panels market. This report also includes a competitive analysis of upcoming startups in the insulated metal panels market.

Reasons to Buy the Report

The report will provide market leaders and new entrants with the closest available estimates of revenue for the overall insulated metal panels market and its subsegments. It will help stakeholders understand the competitive landscape, gain insights into positioning their businesses more effectively, and plan suitable go-to-market strategies. The report will also provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (global construction scale, urbanization, and sustainability mandates), restraints (high upfront costs that limit adoption of insulated metal panels despite long-term benefits), opportunities (expanding renovation and retrofit activities), and challenges (intense competition from alternative wall systems)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the insulated metal panels market

- Market Development: Comprehensive information about profitable markets-the report analyzes the insulated metal panels market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the insulated metal panels market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Kingspan Group (Ireland), Nucor Corporation (US), ArcelorMittal (Luxembourg), Recticel NV/SA (Belgium), Tata Steel (India), and others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING INSULATED METAL PANELS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: ASIA PACIFIC MARKET SIZE AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INSULATED METAL PANELS MARKET

- 3.2 INSULATED METAL PANELS MARKET, BY METAL TYPE AND REGION

- 3.3 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL

- 3.4 INSULATED METAL PANELS MARKET, BY APPLICATION

- 3.5 INSULATED METAL PANELS MARKET, BY END USE

- 3.6 INSULATED METAL PANELS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Global construction scale, urbanization, and sustainability mandates

- 4.2.1.2 GHGs reduction & sustainability initiatives

- 4.2.1.3 Rising demand for refrigerated and processed foods

- 4.2.2 RESTRAINTS

- 4.2.2.1 High upfront costs limit adoption despite long-term benefits

- 4.2.2.2 Awareness gaps and misconceptions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding renovation and retrofit activities

- 4.2.4 CHALLENGES

- 4.2.4.1 Intense competition from alternative wall systems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN INSULATED METAL PANELS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 Construction ↔ energy efficiency

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PRICING ANALYSIS

- 5.4.1.1 Pricing analysis based on region

- 5.4.1 PRICING ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 730890)

- 5.5.2 EXPORT SCENARIO (HS CODE 730890)

- 5.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 IMPACT OF 2025 US TARIFF: INSULATED METAL PANELS MARKET

- 5.9.1 INTRODUCTION

- 5.9.2 KEY TARIFF RATES

- 5.9.3 PRICE IMPACT ANALYSIS

- 5.9.4 IMPACT ON COUNTRY/REGION

- 5.9.4.1 US

- 5.9.4.2 Asia Pacific

- 5.9.4.3 Europe

- 5.9.5 END-USE SECTOR IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 PHASE CHANGE MATERIALS

- 6.1.2 AEROGEL INSULATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 PHOTOVOLTAIC (PV) SOLAR INTEGRATION

- 6.2.2 SMART BUILDING SENSORS AND IOT INTEGRATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 MODULAR AND PREFABRICATED CONSTRUCTION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | MATURITY & AUTONOMOUS SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 INSULATED METAL PANELS MARKET, PATENT ANALYSIS, 2014-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 INTEGRATION OF INSULATED METAL PANELS IN SMART & ENERGY-EFFICIENT BUILDINGS

- 6.7 IMPACT OF AI/GEN AI ON INSULATED METAL PANELS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN INSULATED METAL PANELS PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN INSULATED METAL PANELS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN INSULATED METAL PANELS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF INSULATED METAL PANELS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF INSULATED METAL PANELS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USE SEGMENTS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 INSULATED METAL PANELS MARKET, BY METAL TYPE

- 9.1 INTRODUCTION

- 9.2 STEEL

- 9.2.1 STEEL-BASED INSULATED METAL PANELS SUPPORT HIGH-LOAD, FIRE-SAFE, AND SUSTAINABLE CONSTRUCTION

- 9.3 ALUMINUM

- 9.3.1 ALUMINUM-BASED INSULATED METAL PANELS OFFER LIGHTWEIGHT DESIGN, SUPERIOR CORROSION RESISTANCE, AND SUSTAINABILITY

- 9.4 OTHER METAL TYPES

10 INSULATED METAL PANELS MARKET, BY INSULATION MATERIAL

- 10.1 INTRODUCTION

- 10.2 POLYURETHANE (PUR)/POLYISOCYANURATE (PIR)

- 10.2.1 SUPERIOR THERMAL AND FIRE PERFORMANCE OF PIR/PUR CORES

- 10.3 MINERAL WOOL

- 10.3.1 GROWING ADOPTION OF FIRE-RATED, HIGH-STABILITY BUILDING ENVELOPES

- 10.4 POLYSTYRENE

- 10.4.1 RISING PREFERENCE FOR LIGHTWEIGHT AND ECONOMICAL INSULATION SOLUTIONS

- 10.5 OTHER INSULATION MATERIALS

11 INSULATED METAL PANELS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 INTERIOR WALLS

- 11.2.1 ADOPTION OF MODULAR AND FAST-TRACK CONSTRUCTION SOLUTIONS

- 11.3 EXTERIOR WALLS

- 11.3.1 RISING DEMAND FOR SUSTAINABLE AND HIGH-PERFORMANCE BUILDING ENVELOPES

- 11.4 ROOFS

- 11.4.1 ADOPTION OF GREEN BUILDING AND COOL ROOF STANDARDS

- 11.5 CEILINGS

- 11.5.1 GROWTH OF COLD CHAIN, FOOD PROCESSING, AND CLEAN ROOM FACILITIES

- 11.6 OTHER APPLICATIONS

12 INSULATED METAL PANELS MARKET, BY END USE

- 12.1 INTRODUCTION

- 12.2 RESIDENTIAL

- 12.2.1 GROWTH IN URBAN HOUSING AND MULTI-FAMILY RESIDENTIAL DEVELOPMENTS

- 12.3 NON-RESIDENTIAL

- 12.3.1 EXPANSION OF COLD STORAGE, INDUSTRIAL, AND DATA-INTENSIVE FACILITIES

13 INSULATED METAL PANELS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Expansion of cold chain infrastructure and sustainable logistics

- 13.2.2 JAPAN

- 13.2.2.1 Stricter energy efficiency regulations and mandatory building standards

- 13.2.3 INDIA

- 13.2.3.1 Expansion of food processing, cold chain, and Agro-logistics infrastructure

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Renovation of aging building stock across residential, commercial, and industrial sectors

- 13.2.5 AUSTRALIA

- 13.2.5.1 Expansion of cold storage and temperature-controlled logistics infrastructure

- 13.2.6 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Rapid expansion of warehousing, logistics, and cold-chain infrastructure

- 13.3.2 GERMANY

- 13.3.2.1 Expansion of logistics and advanced manufacturing infrastructure

- 13.3.3 FRANCE

- 13.3.3.1 RE2020 energy and carbon regulations

- 13.3.4 ITALY

- 13.3.4.1 Expansion of agri-food, cold storage, and logistics infrastructure

- 13.3.5 SPAIN

- 13.3.5.1 Energy transition targets and large-scale renovation funding

- 13.3.6 REST OF EUROPE

- 13.3.1 UK

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 Expanding processed food infrastructure and energy-efficient construction

- 13.4.2 CANADA

- 13.4.2.1 Government initiatives aimed at reducing greenhouse gas emissions and improving building performance

- 13.4.3 MEXICO

- 13.4.3.1 Industrial expansion, green construction, and cold-chain growth

- 13.4.1 US

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Expanding processed food infrastructure and energy-efficient construction

- 13.5.2 ARGENTINA

- 13.5.2.1 Government push for energy-efficient and low-carbon buildings

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Saudi Arabia

- 13.6.1.1.1 Expanding construction industry to drive demand

- 13.6.1.2 UAE

- 13.6.1.2.1 Expansion of real estate sector to drive demand

- 13.6.1.3 Rest of GCC Countries

- 13.6.1.1 Saudi Arabia

- 13.6.2 SOUTH AFRICA

- 13.6.2.1 Public sector commitments to accelerate infrastructure rollout

- 13.6.3 REST OF MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.6 FINANCIAL METRICS

- 14.7 BRAND/PRODUCT COMPARISON

- 14.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 PERVASIVE PLAYERS

- 14.8.4 PARTICIPANTS

- 14.8.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.8.5.1 Company footprint

- 14.8.5.2 Region footprint

- 14.8.5.3 Insulation type footprint

- 14.8.5.4 Metal type footprint

- 14.8.5.5 Application footprint

- 14.8.5.6 End-use footprint

- 14.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.9.1 PROGRESSIVE COMPANIES

- 14.9.2 RESPONSIVE COMPANIES

- 14.9.3 DYNAMIC COMPANIES

- 14.9.4 STARTING BLOCKS

- 14.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.9.5.1 Detailed list of key startups/SMEs

- 14.9.5.2 Competitive benchmarking of key startups/SMEs

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES

- 14.10.2 DEALS

- 14.10.3 EXPANSIONS

- 14.10.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 KINGSPAN GROUP

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 NUCOR CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 ARCELORMITTAL

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 RECTICEL NV/SA

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 TATA STEEL

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 ISOPAN S.P.A.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.7 KPS GLOBAL LLC

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.7.4 MnM view

- 15.1.7.4.1 Key strengths

- 15.1.8 WGI WESTMAN GROUP INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.9 BRUCHA GMBH

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.10 ASSAN PANEL A.S.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 MnM view

- 15.1.1 KINGSPAN GROUP

- 15.2 OTHER PLAYERS

- 15.2.1 NORBEC INC.

- 15.2.2 ZAMIL STEEL HOLDING COMPANY LIMITED

- 15.2.3 LONDON ECO-METAL MANUFACTURING

- 15.2.4 BRDECO GROUP

- 15.2.5 STRUCTURAL PANELS, INC.

- 15.2.6 ADVANCED PANEL PRODUCTS LTD.

- 15.2.7 ATAS INTERNATIONAL, INC.

- 15.2.8 GREEN SPAN PROFILES

- 15.2.9 FALK BOUWSYSTEMEN B.V.

- 15.2.10 PERMATHERM

- 15.2.11 RAUTARUUKKI CORPORATION

- 15.2.12 AMERICAN INSULATED PANEL

- 15.2.13 LATTONEDIL

- 15.2.14 STRUCTALL BUILDING SYSTEMS, INC.

- 15.2.15 VULCAN STEEL STRUCTURES, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RISK ASSESSMENT

- 16.6 GROWTH RATE ASSUMPTIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 CUSTOMIZATION OPTIONS

- 17.3 RELATED REPORTS

- 17.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.5 AUTHOR DETAILS