|

시장보고서

상품코드

1950781

미분화 PTFE 시장 : 유형별, 용도별, 최종 이용 산업별, 지역별 예측(-2030년)Micronized PTFE Market by Type, Application, End-use Industry, and Region - Global Forecast to 2030 |

||||||

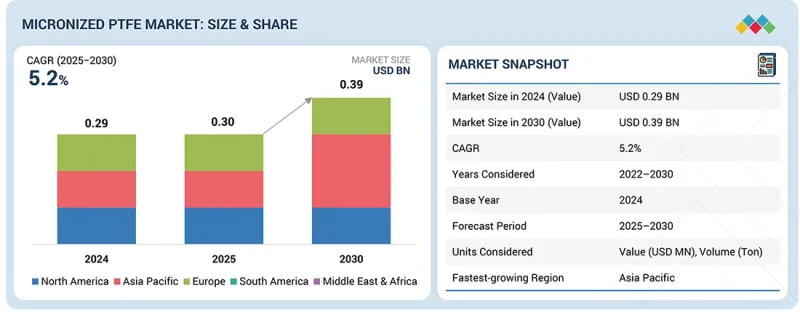

세계의 미분화 PTFE 시장 규모는 2025년 3억 달러로 평가되었고, 2030년까지 3억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 CAGR은 5.2%로 성장이 예상되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만 달러, 톤 |

| 부문 | 유형, 용도, 최종 이용 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

미분화 PTFE는 주로 우수한 표면 특성, 제품 수명 연장 및 가공성 향상에 대한 수요가 증가함에 따라 코팅, 플라스틱, 잉크, 윤활제 및 기타 전문 산업에서 새로운 성분으로 점차 보급되고 있습니다. 뛰어난 내마모성, 마찰 저감, 내약품성, 열안정성에 대한 수요 증가가 미분화 PTFE 수요를 창출하고 있습니다. 미분화 PTFE는 입자 크기의 제어와 다양한 폴리머 내에서의 균일한 분산을 가능하게 하는 첨단 가공 기술에 의해 제조됩니다. 게다가 기술 혁신에 의해 수성 및 저 VOC 제품이 이용되게 되어, 지속가능성 및 규제 준수를 향한 한 걸음이 되고 있습니다. 성능 최적화 및 재료 효율화의 요구가 증가함에 따라 미분화 PTFE는 고급 재료 용도 분야에서 기능성 첨가제로서 중요성을 증가시키고 있습니다.

'재생 PTFE가 예측 기간에 미분화 PTFE 시장에서 가장 빠르게 성장하는 유형이 될 것으로 예측됩니다.'

예측 기간 미분화 PTFE 시장에서 재생 PTFE가 가장 빠르게 성장하는 유형이 될 것으로 전망되고 있습니다. 이는 지속가능성에 대한 요구 증가 및 순환형 경제 동향의 채택 때문입니다. 재생 미분화 PTFE는 산업 폐기물 및 소비자 폐기물의 PTFE에서 생산됩니다. 처녀 PTFE와 유사한 특성을 가지므로 코팅, 잉크, 폴리머, 윤활제 등의 용도에 적합합니다. 재생 미분화 PTFE를 사용하는 주요 이점은 내마모성 향상, 저마찰성, 표면 특성 개선 등을 포함합니다. 시장 성장은 원재료 비용 절감과 환경 부하 경감에 따른 환경적, 경제적 우위성에 의해 더욱 촉진되고 있습니다. 또한 엄격한 환경 기준 도입, 탄소 풋 프린트 감소, 버진 불소 수지 감소도 시장 확대를 뒷받침하고 있습니다.

'열가소성 수지 및 엘라스토머가 예측 기간에 미분화 PTFE 시장에서 두 번째로 높은 성장률을 나타내는 용도가 될 전망입니다.'

열가소성 수지 및 엘라스토머는 자동차, 공업, 전기 및 전자, 소비재 업계에 있어서의 고성능 폴리머 수요의 확대에 의해 예측 기간 미분화 PTFE 시장에서 제2위의 성장률을 나타낼 전망입니다. 미분화 PTFE는 내마모성의 부여, 마찰 저감, 표면 평활성의 향상, 스틱 슬립 현상의 억제를 목적으로, 열가소성 수지 및 엘라스토머의 기능성 첨가제로서 널리 사용되고 있습니다. 미분화 PTFE는 기계적 특성을 손상시키지 않고 이형성, 내마모성, 장기 내구성을 향상시키는 특성을 가지므로 엔지니어링 플라스틱이나 고무 컴파운드에 적합합니다. 게다가 경량 재료에 대한 관심 증가, 제품 수명 연장, 에너지 절약 가공에 대한 주목도 폴리머 가공업자에 의한 미분화 PTFE의 사용을 촉진하고 있습니다. 컴파운딩 기술의 지속적인 발전 및 낮은 유지보수성 폴리머 부품에 대한 수요 증가는 미분화 PTFE 시장의 급속한 성장을 뒷받침하고 있습니다.

'자동차 및 운송 부문이 예측 기간에 미분화 PTFE 시장에서 가장 빠르게 성장하는 최종 이용 산업이 될 것으로 전망되고 있습니다.'

자동차 및 운송 부문은 컴포넌트의 효율성 및 내구성을 높이는 고성능 재료에 대한 수요 증가로 예측 기간 미분화 PTFE 시장에서 가장 급속히 성장하는 최종 이용 산업으로 전망되고 있습니다. 미분화 PTFE는 플라스틱, 엘라스토머 및 윤활제 코팅으로 자동차 부문에서 널리 사용되며 마찰 저항성, 내마모성, 내마모성 및 표면 특성을 향상시킵니다. 자동차 부문에서의 경량화, 연비 효율 향상, 전기자동차 개발 등의 동향 증가도 중량을 크게 증가시키지 않고 재료 특성을 향상시키는 미분화 PTFE 수요를 뒷받침하고 있습니다. 또한 보다 엄격한 배출 가스 규제 및 품질 기준을 충족할 필요성이 높아짐에도 신뢰성을 높이고 유지보수를 최소화하는 첨단 첨가제의 채용을 촉진하고 있어 자동차 및 운송 업계에서 미분화 PTFE 시장의 성장이 가속화되고 있습니다.

이 보고서는 세계의 미분화 PTFE 시장에 대한 조사 분석을 통해 주요 촉진요인 및 억제요인, 제품 개발 및 혁신 및 경쟁 구도에 대한 지식을 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요한 지견

- 미분화 PTFE 시장에서 기업에게 매력적인 기회

- 미분화 PTFE 시장 : 유형별

- 미분화 PTFE 시장 : 용도별

- 미분화 PTFE 시장 : 최종 이용 산업별

- 미분화 PTFE 시장 : 국가별

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 요구 및 화이트 스페이스

- 미분화 PTFE 시장에서 미충족 요구

- 화이트 스페이스의 기회

- 상호접속된 시장 및 부문 간 기회

- 상호연결된 시장

- 부문 간 기회

- Tier 1/2/3 기업의 전략적 움직임

- Tier 1 기업 : 공급망 및 시장 진입을 강화하는 세계 리더

- Tier 2 기업 : 용도 범위를 확대하는 혁신 주도의 스페셜리스트

- Tier 3 기업 : 생산 능력 및 운용 효율을 확대하는 현지 제조업체

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- GDP 동향 및 예측

- 자동차 및 운송 업계 동향

- 화학제품 및 공업 가공 업계 동향

- 밸류체인 분석

- 생태계 분석

- 가격 설정 분석

- 미분화 PTFE의 평균 판매 가격 : 주요 기업별(2024년)

- 미분화 PTFE의 가격 설정 동향 : 최종 이용 산업별(2022-2024년)

- 미분화 PTFE의 평균 판매 가격 동향 : 지역별(2022-2024년)

- 무역 분석

- 수출 시나리오(HS 코드 390461)

- 수입 시나리오(HS 코드 390461)

- 주요 컨퍼런스 및 이벤트(2026-2027년)

- 고객 사업에 영향을 주는 동향 및 혼란

- 투자 및 자금 조달 시나리오

- 사례 연구 분석

- 미분화 PTFE 시장에 대한 2025년 미국 관세의 영향

- 주요 관세율

- 가격의 영향 분석

- 국가 및 지역에 미치는 영향

- 최종 이용 산업에 대한 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래 용도

- 주요 기술

- 미분화 PTFE

- 기계적 미분화

- 방사선 조사에 의한 미립자화

- 표면 개질 및 PTFE 미세 분말 캡슐화

- 보완 기술

- 분산 및 배합

- 마스터 배치 및 컴파운드의 통합

- 조립, 저분진 제법, 응집 제어

- 기술 및 제품 로드맵

- 단기 : 프로세스 최적화 및 배합 안정성(2025-2027년)

- 중기 : 기능 통합 및 특정 용도 등급(2027-2030년)

- 장기 : 지속가능성 및 규제 준수(2030-2035년 이후)

- 특허 분석

- 조사 방법

- 미분화 PTFE 시장, 특허 분석(2016-2025년)

- 미래의 용도

- 고성능 코팅 및 표면 개질 용도

- 트라이볼로지 컴포넌트 및 산업 기계 용도

- 고성능 전자 및 전기 용도

- 미분화 PTFE 시장에 대한 AI 및 생성형 AI의 영향

- 주요 이용 사례 및 시장 장래성

- 미분화 PTFE 시장에서 제조업체 및 OEM 모범 사례

- 미분화 PTFE 시장에서 AI 및 생성형 AI 도입에 관한 사례 연구

- 상호연결, 인접하는 생태계와 시장 기업에 미치는 영향

- 미분화 PTFE 시장에서 AL 및 생성형 AI 채용에 대한 고객의 준비 상황

- 성공 사례 및 실세계에 대한 용도

제7장 규제 정세 및 지속가능성에 관한 대처

- 지역 규제 및 규정 준수

- 규제기관, 정부기관, 기타 조직

- 업계 표준

- 지속가능성에 대한 노력

- 그린 재료의 효율 및 수명 주기 최적화

- 미분화 PTFE 생산에 있어서 지속 가능한 생산 방식 및 배출 제어

- 최종 용도에 있어서 자원 효율 및 라이프사이클 퍼포먼스 혜택

- 공동연구 및 규제에 준거한 지속가능성 개발

- 환경 성능 및 효율성을 중시한 이용

- 지속가능성에 대한 규제 정책의 영향

제8장 고객 정세 및 구매 행동

- 의사 결정 프로세스

- 구매 프로세스에 참여하는 주요 이해관계자 및 그 평가 기준

- 구매 프로세스의 주요 이해 관계자

- 구입 기준

- 채용 장벽 및 내부 과제

- 다양한 최종 이용 산업으로부터 미충족 요구

- 시장의 수익성

- 잠재적인 수익

- 비용 역학

- 마진 기회 : 용도별

제9장 미분화 PTFE 시장 : 유형별

- 재생 PTFE 재료

- 버진 PTFE 재료

제10장 미분화 PTFE 시장 : 용도별

- 잉크 및 코팅

- 열가소성 수지 및 엘라스토머

- 페인트

- 윤활제 및 그리스

- 기타 용도

제11장 미분화 PTFE 시장 : 최종 이용 산업별

- 자동차 및 운송

- 화학제품 및 공업 가공

- 전기 및 전자 공학

- 건축 및 건설

- 의료 및 의약품

- 기타 최종 이용 산업

제12장 미분화 PTFE 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

제13장 경쟁 구도

- 개요

- 주요 기업의 경쟁 전략 및 강점(2020-2025년)

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 제품 비교

- THE CHEMOURS COMPANY(ZONYL MICROPOWDERS)(US)

- DAIKIN INDUSTRIES, LTD, LTD.(PTFE MICROPOWDER HL SERIES)(JAPAN)

- 3M(DYNEON)(US)

- SYENSQO(ALGOFLON L PTFE MICRONIZED POWDERS)(BELGIUM)

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

- 기업 평가 및 재무 지표

- 경쟁 시나리오

제14장 기업 프로파일

- 주요 기업

- THE CHEMOURS COMPANY

- DAIKIN INDUSTRIES, LTD.

- 3M

- SYENSQO

- AGC INC.

- DONGYUE GROUP

- SHAMROCK TECHNOLOGIES

- GUJARAT FLUOROCHEMICALS LIMITED

- HALOPOLYMER

- NANJING TIANSHI NEW MATERIAL TECHNOLOGIES CO., LTD.

- 기타 기업

- MAFLON SPA

- FUZHOU TOPDA NEW MATERIAL CO., LTD.

- PEFLON

- SUZHOU NORSHINE PERFORMANCE MATERIAL CO. LTD.

- REPROLON

- ZHEJIANG QUZHOU WANNENGDA TECHNOLOGY CO., LTD.

- ZHONGHAO CHENGUANG RESEARCH INSTITUTE OF CHEMICAL INDUSTRY CO., LTD.

- KITAMURA LIMITED

- POLYMER ADD(THAILAND) CO., LTD.

- HANGZHOU JUFU NEW MATERIAL TECHNOLOGY CO., LTD.

- SHANGHAI TONGS SCIENCE & TECHNOLOGY CO., LTD.

- HANGZHOU FINE FLUOROTECH CO., LTD.

- ITAFLON

- XEON PTFE

- SHANGHAI KAYSON CHEMICAL

제15장 조사 방법

제16장 부록

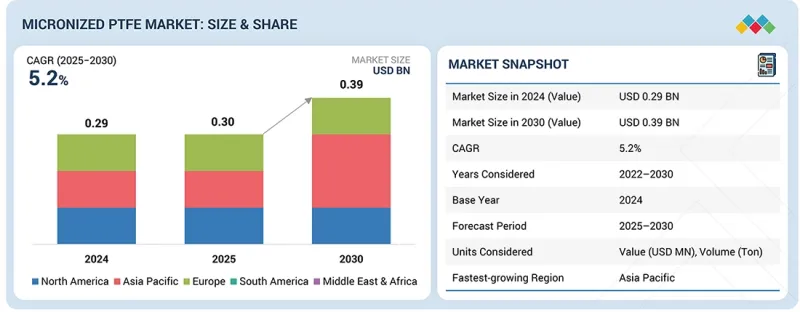

AJY 26.03.05The micronized PTFE market is expected to reach USD 0.39 billion by 2030 from USD 0.30 billion in 2025, at a CAGR of 5.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Ton) |

| Segments | Type, Application, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Micronized PTFE is gradually becoming the new ingredient in coatings, plastics, inks, lubricants, and other specialized industries, primarily because of the ever-increasing demand for better surface properties, longer product life, and easier processing. The increasing demand for better wear & abrasion resistance, friction reduction, chemical resistance, & thermal stability is thus creating a demand for micronized PTFE. Micronized PTFE is manufactured via advanced processing techniques that enable regulated particle size and consistent dispersion in various polymers. Moreover, innovation has led to the use of water-based, low-VOC products, a step toward sustainability and regulatory compliance. With the growing need for performance optimization and material efficiency, micronized PTFE is gaining importance as a functional additive in advanced materials applications.

"Recycled PTFE is projected to be the fastest-growing type in the micronized PTFE market during the forecast period."

Recycled PTFE is projected to be the fastest-growing type in the micronized PTFE market during the forecast period. This is due to rising sustainability demands and the adoption of circular-economy trends. Recycled micronized PTFE is produced from post-industrial and post-consumer waste PTFE. It possesses qualities similar to virgin PTFE, making it suitable for applications such as coatings, inks, polymers, and lubricants. The key advantages of using recycled micronized PTFE include improved wear resistance, low friction, and improved surface properties. Market growth is further driven by the environmental and economic advantages associated with lower raw material costs and reduced environmental impact. Moreover, the implementation of rigorous environmental standards and the decrease in carbon footprints and virgin fluoropolymers are also facilitating market expansion.

"Thermoplastics & elastomers are projected to be the second-fastest-growing application in the micronized PTFE market during the forecast period."

Thermoplastics & elastomers are anticipated to witness the second-fastest growth rate as applications in the micronized PTFE market during the forecast period, driven by the growing need for high-performance polymers across the automotive, industrial, electrical & electronics, and consumer goods industries. Micronized PTFE is widely used as a functional additive in thermoplastics and elastomers to impart wear resistance, reduce friction, improve surface smoothness, and reduce stick-slip effects. The micronized PTFE's ability to improve mold release, abrasion resistance, and long-term durability without affecting mechanical properties makes it suitable for engineering plastics and rubber compounds. Moreover, the increasing focus on lightweight materials, longer product life, and energy-efficient processing is also encouraging polymer processors to use micronized PTFE. Ongoing developments in compounding technology and the increasing demand for low-maintenance polymer parts are also fueling the rapid growth of the micronized PTFE market.

"Automotive & transportation is projected to be the fastest-growing end-use industry in the micronized PTFE market during the forecast period."

The automotive & transportation sector is anticipated to be the fastest-growing end-use industry for the micronized PTFE market during the forecast period, driven by rising demand for high-performance materials to enhance the efficiency and durability of components. Micronized PTFE has wide applications in the automotive sector as a coating agent for plastics, elastomers, and lubricants, enhancing friction, wear, and abrasion resistance, as well as surface properties. The rising trend of lightweighting, fuel efficiency, and the development of electric vehicles in the automotive sector is also boosting demand for micronized PTFE, as it enhances material properties without significantly increasing weight. Moreover, the rising need to meet tougher emission and quality standards is also driving the adoption of advanced additives that enhance reliability and minimize maintenance, thereby fueling the growth of the micronized PTFE market in the automotive and transportation industries.

"Asia Pacific is projected to be the fastest-growing region in the micronized PTFE market during the forecast period."

The Asia Pacific market is expected to be the fastest-growing in the micronized PTFE market during the forecast period, driven by rapid industrialization and increased manufacturing capacity in the region, as well as the growing demand for high-performance materials across key end-use industries. The strong growth of coatings, plastics, the automotive industry, electronics, and manufacturing in the region, including countries such as China, India, Japan, and South Korea, is driving the use of micronized PTFE as a functional additive. The Asia Pacific market has a large polymer-processing base, and the region also offers cost-effective manufacturing and increasing investments in specialty chemicals and high-performance materials. Moreover, the trend toward water-based and low-VOC products, along with increasingly stringent environmental regulations, is driving demand for performance-enhancing additives such as micronized PTFE.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: <USD 500 million.

Companies Covered: The Chemours Company (US), DAIKIN INDUSTRIES, Ltd. (Japan), 3M (US), Syensqo (Belgium), AGC Inc. (Japan), DONGYUE GROUP (China), Shamrock Technologies Inc. (US), Gujarat Fluorochemicals Limited (India), HaloPolymer (Russia), and Nanjing Tianshi New Material Technologies Co., Ltd. (China) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the micronized PTFE market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the micronized market based on type (recycled PTFE, virgin PTFE material), application (inks & coatings, thermoplastics & elastomers, paints, lubricants & greases, other applications), and end-use industry (automotive & transportation, electrical & electronics, chemical & industrial processing, medical & pharmaceutical, building & construction, other end-use industries). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the micronized PTFE market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the micronized PTFE market. This report covers a competitive analysis of upcoming startups in the micronized PTFE market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall micronized PTFE market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points: Analysis of key drivers (strong demand in coatings, lubricants, and high-performance additives, superior functional properties, and advancements in processing technology), restraints (high production and processing costs and substitution risk from alternative materials), opportunities (expansion into emerging industries and advanced applications, recycled and sustainable PTFE grades, and regional expansion and industrial growth in Asia Pacific are driving micronized PTFE demand), and challenges (maintaining consistent ultra-fine particle control & supply chain volatility and raw material price fluctuations).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the micronized PTFE market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the micronized PTFE market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the micronized PTFE market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as The Chemours Company (US), DAIKIN INDUSTRIES, Ltd. (Japan), 3M (US), Syensqo (Belgium), AGC Inc. (Japan), DONGYUE GROUP (China), Shamrock Technologies Inc. (US), Gujarat Fluorochemicals Limited (India), HaloPolymer (Russia), and Nanjing Tianshi New Material Technologies Co., Ltd. (China).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MICRONIZED PTFE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MICRONIZED PTFE MARKET

- 3.2 MICRONIZED PTFE MARKET, BY TYPE

- 3.3 MICRONIZED PTFE MARKET, BY APPLICATION

- 3.4 MICRONIZED PTFE MARKET, BY END-USE INDUSTRY

- 3.5 MICRONIZED PTFE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Surging demand for electric vehicles

- 4.2.1.2 Pressing need for high-performance additives in coatings, inks, and surface formulations

- 4.2.1.3 Rising use of micronized PTFE in thermoplastics, elastomers, and engineered polymers

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production and processing costs

- 4.2.2.2 Regulatory scrutiny on fluoropolymers and PFAS

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing emphasis on circular economy and sustainability

- 4.2.3.2 Emerging applications of micronized PTFE

- 4.2.4 CHALLENGES

- 4.2.4.1 Maintaining uniform ultra-fine particle size and reliable dispersion

- 4.2.4.2 Shift toward PFAS-free alternatives

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MICRONIZED PTFE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.2.1 CHEMICAL PROCESSING & OIL/GAS -> RENEWABLE ENERGY

- 4.4.2.2 AUTOMOTIVE & TRANSPORTATION -> ELECTRICAL & ELECTRONICS

- 4.4.2.3 SEMICONDUCTOR MANUFACTURING -> MEDICAL & LIFE SCIENCE DEVICES

- 4.4.2.4 INDUSTRIAL COATINGS & INKS -> PACKAGING & CONSUMER GOODS

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS STRENGTHENING SUPPLY CHAINS AND MARKET ACCESS

- 4.5.1.1 THE CHEMOURS COMPANY - STRATEGIC MANUFACTURING AGREEMENT WITH SRF LIMITED (INDIA)

- 4.5.1.2 AGC INC.- DEVELOPMENT OF SURFACTANT-FREE FLUOROPOLYMER MANUFACTURING TECHNOLOGY

- 4.5.2 TIER 2 PLAYERS: INNOVATION-DRIVEN SPECIALISTS EXPANDING APPLICATION REACH

- 4.5.2.1 SHAMROCK TECHNOLOGIES - ADVANCED MICRONIZED & NANO-SCALE PTFE PORTFOLIO SHOWCASED AT CHINAPLAS 2025

- 4.5.3 TIER 3 PLAYERS: REGIONAL MANUFACTURERS SCALING CAPACITY AND OPERATIONAL EFFICIENCY

- 4.5.3.1 ITAFLON - EXPANSION AND RELOCATION TO NEW ADVANCED PRODUCTION FACILITY

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS STRENGTHENING SUPPLY CHAINS AND MARKET ACCESS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2.4 TRENDS IN CHEMICALS & INDUSTRIAL PROCESSING INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF MICRONIZED PTFE TYPES, BY KEY PLAYER, 2024

- 5.5.2 PRICING TREND OF MICRONIZED PTFE, BY END-USE INDUSTRY, 2022-2024

- 5.5.3 AVERAGE SELLING PRICE TREND OF MICRONIZED PTFE, BY REGION, 2022-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 390461)

- 5.6.2 IMPORT SCENARIO (HS CODE 390461)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 IMPROVING FRICTION AND WEAR-RESISTANCE WITH ENGINEERED PTFE@SIO2 STRUCTURES

- 5.10.2 STRENGTHENING INDUSTRIAL COMPONENT RELIABILITY WITH PTFE-BASED EPOXY ENHANCEMENTS

- 5.10.3 OPTIMIZING POLYMER DURABILITY AND LUBRICATION WITH PTFE ADDITIVE TECHNOLOGIES

- 5.11 IMPACT OF 2025 US TARIFFS ON MICRONIZED PTFE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 China

- 5.11.4.3 Europe

- 5.11.4.4 Mexico

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 MICRONIZED PTFE

- 6.1.2 MECHANICAL MICRONIZATION

- 6.1.3 IRRADIATION-ASSISTED MICRONIZATION

- 6.1.4 SURFACE MODIFICATION AND PTFE MICROPOWDER ENCAPSULATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DISPERSION AND FORMULATION

- 6.2.2 MASTERBATCH AND COMPOUND INTEGRATION

- 6.2.3 GRANULATION, LOW-DUST FORMULATION, AND AGGLOMERATION CONTROL

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | PROCESS OPTIMIZATION AND FORMULATION STABILITY

- 6.3.2 MID-TERM (2027-2030) | FUNCTIONAL INTEGRATION AND APPLICATION-SPECIFIC GRADES

- 6.3.3 LONG-TERM (2030-2035+) | SUSTAINABILITY AND REGULATORY COMPLIANCE

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 MICRONIZED PTFE MARKET, PATENT ANALYSIS, 2016-2025

- 6.5 FUTURE APPLICATIONS

- 6.5.1 HIGH-PERFORMANCE COATINGS AND SURFACE MODIFICATION APPLICATIONS

- 6.5.2 TRIBOLOGICAL COMPONENTS AND INDUSTRIAL MACHINERY APPLICATIONS

- 6.5.3 HIGH-PERFORMANCE ELECTRONICS AND ELECTRICAL APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON MICRONIZED PTFE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN MICRONIZED PTFE MARKET

- 6.6.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN MICRONIZED PTFE MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AL/GEN AI IN MICRONIZED PTFE MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 ZONYL PTFE MICROPOWDERS BY CHEMOURS ENHANCE WEAR AND SURFACE PERFORMANCE IN COATINGS, INKS, AND POLYMER SYSTEMS

- 6.7.2 DAIKIN POLYFLON MICRONIZED PTFE ENABLES LOW-FRICTION PERFORMANCE IN INDUSTRIAL COATINGS AND PRINTING INKS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 GREEN MATERIAL EFFICIENCY AND LIFECYCLE OPTIMIZATION

- 7.2.2 SUSTAINABLE MANUFACTURING PRACTICES AND EMISSION CONTROL IN MICRONIZED PTFE PRODUCTION

- 7.2.3 RESOURCE EFFICIENCY AND LIFECYCLE PERFORMANCE BENEFITS IN END-USE APPLICATIONS

- 7.2.4 COLLABORATIVE RESEARCH AND REGULATORY-ALIGNED SUSTAINABILITY DEVELOPMENT

- 7.2.5 ENVIRONMENTAL PERFORMANCE AND EFFICIENCY-DRIVEN APPLICATIONS

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 MICRONIZED PTFE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 RECYCLED PTFE MATERIAL

- 9.2.1 RISING FOCUS ON ENVIRONMENTAL COMPLIANCE AND RESOURCE EFFICIENCY TO STIMULATE SEGMENTAL GROWTH

- 9.3 VIRGIN PTFE MATERIAL

- 9.3.1 REQUIREMENT FOR PREMIUM ADDITIVE PERFORMANCE TO BOOST DEMAND

10 MICRONIZED PTFE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 INKS & COATINGS

- 10.2.1 CHEMICAL INERTNESS, THERMAL STABILITY, AND NON-STICK PROPERTIES OF MICRONIZED PTFE TO BOOST DEMAND

- 10.3 THERMOPLASTICS & ELASTOMERS

- 10.3.1 STRINGENT MECHANICAL, THERMAL, AND CHEMICAL PERFORMANCE REQUIREMENTS ACROSS INDUSTRIAL SECTORS TO SPIKE ADOPTION

- 10.4 PAINTS

- 10.4.1 STRICT DURABILITY AND AESTHETIC STANDARDS ACROSS DECORATIVE, INDUSTRIAL, AND AUTOMOTIVE SECTORS TO STIMULATE DEMAND

- 10.5 LUBRICANTS & GREASES

- 10.5.1 ABILITY TO EXTEND SERVICE LIFE OF BEARINGS, GEARS, CHAINS, AND SLIDING COMPONENTS TO INCREASE ADOPTION

- 10.6 OTHER APPLICATIONS

11 MICRONIZED PTFE MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 AUTOMOTIVE & TRANSPORTATION

- 11.2.1 SIGNIFICANT FOCUS ON REDUCING EMISSIONS AND IMPROVING FUEL EFFICIENCY TO ACCELERATE DEMAND

- 11.3 CHEMICALS & INDUSTRIAL PROCESSING

- 11.3.1 POTENTIAL TO PROTECT VESSELS, PIPING, AND HEAT EXCHANGERS FROM AGGRESSIVE CHEMICAL ATTACK TO SUPPORT MARKET GROWTH

- 11.4 ELECTRICAL & ELECTRONICS

- 11.4.1 ABILITY TO PRESERVE SIGNAL INTEGRITY IN HIGH-SPEED DATA TRANSMISSION AND RF/MICROWAVE SYSTEMS TO SPIKE DEMAND

- 11.5 BUILDING & CONSTRUCTION

- 11.5.1 INCLINATION TOWARD SPECIALTY CONSTRUCTION MATERIALS FOR LONG-TERM ASSET DURABILITY TO SPUR ADOPTION

- 11.6 MEDICAL & PHARMACEUTICALS

- 11.6.1 INCREASING DEMAND FOR MINIMALLY INVASIVE PROCEDURES TO FOSTER MARKET GROWTH

- 11.7 OTHER END-USE INDUSTRIES

12 MICRONIZED PTFE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Robust industrial base and regulatory frameworks for environmental safety to accelerate demand

- 12.2.2 CANADA

- 12.2.2.1 Strong base of advanced manufacturing and environmental stewardship to spike demand

- 12.2.3 MEXICO

- 12.2.3.1 High foreign direct investment in specialty chemicals, polymers, and downstream industrial applications to facilitate market growth

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Strong automotive and industrial machinery sectors to contribute to market growth

- 12.3.2 FRANCE

- 12.3.2.1 Constant activities in construction, infrastructure development and maintenance, and public facilities to propel market

- 12.3.3 UK

- 12.3.3.1 Stringent chemical regulation and strong downstream coatings and engineering sectors to support market growth

- 12.3.4 ITALY

- 12.3.4.1 Urban regeneration initiatives and strong coatings and surface treatment ecosystem to drive market

- 12.3.5 SPAIN

- 12.3.5.1 Rapid urbanization and infrastructure development to boost adoption

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 SOUTH AMERICA

- 12.4.1 BRAZIL

- 12.4.1.1 Booming automotive, chemical processing, electrical equipment, and industrial machinery sectors to support market growth

- 12.4.2 ARGENTINA

- 12.4.2.1 Industrial and public infrastructure projects in chemicals, utilities, and energy sectors to create growth opportunities

- 12.4.3 REST OF SOUTH AMERICA

- 12.4.1 BRAZIL

- 12.5 ASIA PACIFIC

- 12.5.1 CHINA

- 12.5.1.1 Sustainable industrial practices under Beautiful China initiative to expedite market growth

- 12.5.2 JAPAN

- 12.5.2.1 Demographic-driven industrial density and sustainability-focused regulations to reinforce market expansion

- 12.5.3 INDIA

- 12.5.3.1 Urban industrial hubs and expanding manufacturing capacity to foster market growth

- 12.5.4 SOUTH KOREA

- 12.5.4.1 Aging industrial infrastructure and regulatory focus on chemical safety and sustainability to create market opportunities

- 12.5.5 REST OF ASIA PACIFIC

- 12.5.1 CHINA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC

- 12.6.1.1 Saudi Arabia

- 12.6.1.1.1 Expanding oil & gas, petrochemicals, chemicals, energy, and water treatment sectors to support market growth

- 12.6.1.2 UAE

- 12.6.1.2.1 Expo-related developments and ongoing urban master plans to increase micronized PTFE penetration

- 12.6.1.3 Rest of GCC

- 12.6.1.1 Saudi Arabia

- 12.6.2 SOUTH AFRICA

- 12.6.2.1 Surging adoption of high-performance materials in energy, water, chemicals, and manufacturing sectors to stimulate demand

- 12.6.3 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.5 PRODUCT COMPARISON

- 13.5.1 THE CHEMOURS COMPANY (ZONYL MICROPOWDERS) (US)

- 13.5.2 DAIKIN INDUSTRIES, LTD, LTD. (PTFE MICROPOWDER HL SERIES) (JAPAN)

- 13.5.3 3M (DYNEON) (US)

- 13.5.4 SYENSQO (ALGOFLON L PTFE MICRONIZED POWDERS) (BELGIUM)

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Type footprint

- 13.6.5.4 Application footprint

- 13.6.5.5 End-use industry footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 THE CHEMOURS COMPANY

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 DAIKIN INDUSTRIES, LTD.

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 3M

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Products offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses & competitive threats

- 14.1.4 SYENSQO

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic Choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 AGC INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 DONGYUE GROUP

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 MnM view

- 14.1.7 SHAMROCK TECHNOLOGIES

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Developments

- 14.1.7.4 MnM view

- 14.1.8 GUJARAT FLUOROCHEMICALS LIMITED

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.4 MnM view

- 14.1.9 HALOPOLYMER

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MnM view

- 14.1.10 NANJING TIANSHI NEW MATERIAL TECHNOLOGIES CO., LTD.

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MnM view

- 14.1.1 THE CHEMOURS COMPANY

- 14.2 OTHER PLAYERS

- 14.2.1 MAFLON S.P.A.

- 14.2.2 FUZHOU TOPDA NEW MATERIAL CO., LTD.

- 14.2.3 PEFLON

- 14.2.4 SUZHOU NORSHINE PERFORMANCE MATERIAL CO. LTD.

- 14.2.5 REPROLON

- 14.2.6 ZHEJIANG QUZHOU WANNENGDA TECHNOLOGY CO., LTD.

- 14.2.7 ZHONGHAO CHENGUANG RESEARCH INSTITUTE OF CHEMICAL INDUSTRY CO., LTD.

- 14.2.8 KITAMURA LIMITED

- 14.2.9 POLYMER ADD (THAILAND) CO., LTD.

- 14.2.10 HANGZHOU JUFU NEW MATERIAL TECHNOLOGY CO., LTD.

- 14.2.11 SHANGHAI TONGS SCIENCE & TECHNOLOGY CO., LTD.

- 14.2.12 HANGZHOU FINE FLUOROTECH CO., LTD.

- 14.2.13 ITAFLON

- 14.2.14 XEON PTFE

- 14.2.15 SHANGHAI KAYSON CHEMICAL

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.1.2 List of key secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 List of primary interview participants

- 15.1.2.3 Key industry insights

- 15.1.2.4 Breakdown of primary interviews

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 DATA TRIANGULATION

- 15.4 RESEARCH ASSUMPTIONS

- 15.5 RESEARCH LIMITATIONS

- 15.6 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS