|

시장보고서

상품코드

1950785

치과 기공소 시장(-2030년) : 진료 분야(교정 치과), 제품(재료(금속 세라믹 및 유리 세라믹), 기기(CAD/CAM 시스템), 소프트웨어(실험실 관리)), 기술(디지털), 소비자(치과 병원, DSO)Dental Laboratories Market By Practice (Orthodontics), Product [Material (Metal Ceramic, Glass Ceramic), Equipment (CAD/CAM System), Software (Lab management)], Technology (Digital), and Consumer (Dental Hospitals, DSOs) - Global Forecast to 2030 |

||||||

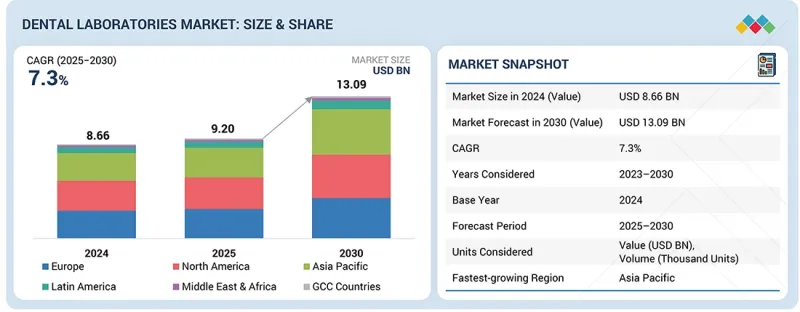

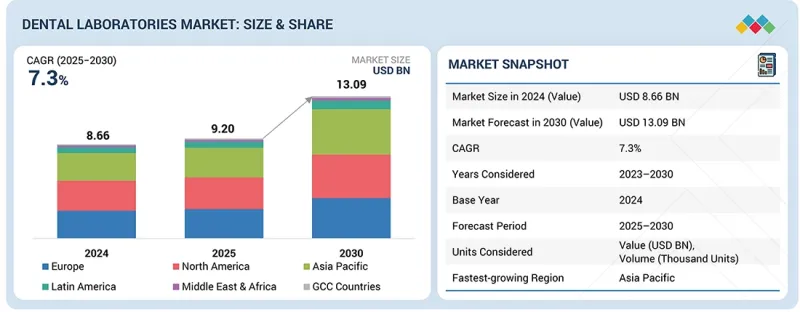

세계의 치과 기공소 시장 규모는 예측 기간 중에 CAGR 7.3%로 성장하여 2025년 92억 달러에서 2030년에는 130억 9,000만 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 업무 분야, 기술, 소비자 유형, 지역 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

치과기공소 시장은 인구통계학적, 임상적, 기술적 요인이 맞물려 큰 폭의 성장이 예상됩니다. 치과 질환 증가, 급속한 고령화, 미용 및 수복 치과에 대한 인식 증가로 인해 치과 기공소에서 제조되는 치과 솔루션에 대한 수요가 증가하고 있습니다. 디지털 치과 워크플로우, CAD/CAM 시스템, 3D 프린팅, AI 탑재 설계 소프트웨어 등의 기술 혁신으로 제조 정확도, 납기, 맞춤화 능력이 크게 향상되어 치과 기공소에서의 도입이 가속화되고 있습니다. 또한, 구강 위생 개선을 위한 정부 지원책, 치과 의료 인프라 정비, 민간 및 DSO 주도의 치과 의료 접근성 향상도 시장 확대에 기여하고 있습니다. 이러한 추세는 향후 몇 년 동안 선진국과 신흥국 모두에서 강력한 성장세를 유지할 것으로 예측됩니다.

제품별로는 2024년 소재 부문이 가장 큰 점유율을 차지했습니다.

제품별로는 재료 부문이 가장 큰 비중을 차지하고 있는데, 이는 일상적인 기공소 업무에서 수복 재료와 보철 재료가 빈번하고 지속적으로 사용되기 때문입니다. 다양한 치과 시술에서 세라믹, 금속, 폴리머, 수지 기반 재료에 대한 수요가 지속적으로 존재합니다. 이 수요는 케이스 수 증가와 미용 치과에 대한 관심 증가에 의해 주도되고 있습니다. 또한, 정기적인 보충의 필요성, 제품 수명주기 단축, 기존 및 디지털 워크플로우의 적용 범위 확대가 재료 부문의 우위를 점하는 데 기여하고 있습니다.

재료별로는 CAD/CAM 재료 부문이 2024년 시장에서 가장 큰 점유율을 차지했습니다.

이는 주로 디지털 워크플로우의 보급과 정밀한 밀링 가공이 가능한 수리 솔루션에 대한 수요 증가에 기인합니다. CAD/CAM 재료는 기존 제법의 수복물에 비해 안정된 품질, 빠른 납기, 우수한 적합성을 제공합니다. 크라운, 브릿지, 임플란트 수복물에 지르코니아, 유리세라믹, 리튬 디실리케이트의 사용 증가도 이 부문의 성장에 기여하고 있습니다. 또한, 체어사이드 및 랩사이드 CAD/CAM 시스템의 확대로 디지털 호환 재료로의 전환이 가속화되면서 CAD/CAM 재료가 치과 기공소 시장의 주요 카테고리로 자리매김하고 있습니다.

2024년에는 북미가 가장 큰 점유율을 기록했습니다.

북미는 전 세계 치과기공소 시장에서 가장 큰 점유율을 차지하고 있습니다. 이는 선진화된 치과 의료 인프라, 구강 위생과 심미성에 대한 높은 의식, 디지털 치과 기술 도입이 활발하게 이루어지고 있는 것이 배경입니다. 이 지역에서는 CAD/CAM 시스템, 구강 내 스캐너, 3D 프린팅 솔루션의 보급이 진행되고 있으며, 이는 모두 유리한 상환 정책과 확립된 민간 치과 의료 시스템에 의해 뒷받침되고 있습니다. 또한, 주요 치과 기술 및 재료 기업의 강력한 존재감, 지속적인 제품 혁신, 치과 서비스 제공업체와 제조업체 간의 전략적 제휴를 통해 북미의 우위는 더욱 강화되고 있습니다. 치과 의료비 증가, 수복 및 보철 솔루션을 필요로 하는 고령화 인구, AI 지원 및 커넥티드 디지털 워크플로우의 급속한 통합 등의 요인이 이 지역 전체에서 지속적인 시장 성장을 뒷받침하고 있습니다.

세계의 치과기공소 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 치과 기공소 시장 : 진료 분야별

제10장 치과 기공소 시장 : 제품별

제11장 치과 기공소 시장 : 기술별

제12장 치과 기공소 시장 : 소비자 유형별

제13장 치과 기공소 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.03.13The global dental laboratories market is projected to reach USD 13.09 billion by 2030 from USD 9.20 billion in 2025, at a CAGR of 7.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Practice, Technology, Consumer Type, and Region |

| Regions covered | Asia Pacific, North America, Europe, Latin America, the Middle East & Africa, and GCC Countries |

The dental laboratories market is poised for significant growth, driven by a combination of demographic, clinical, and technological factors. The increasing prevalence of dental disorders, the rapidly aging global population, and growing awareness of aesthetic and restorative dentistry are fueling the demand for laboratory-fabricated dental solutions. Technological advancements, such as digital dentistry workflows, CAD/CAM systems, 3D printing, and AI-enabled design software, have greatly improved production accuracy, turnaround times, and customization capabilities, leading to faster adoption by dental laboratories. Additionally, supportive government initiatives aimed at improving oral health, better dental infrastructure, and enhanced access to private and DSO-led care are all contributing to market expansion. These trends are expected to sustain strong growth momentum in both developed and emerging economies in the coming years.

Based on product, the materials segment accounted for the largest share of the dental laboratories market in 2024.

Based on product, the global dental laboratories market is divided into materials, equipment, and software. Among these segments, the materials segment holds the largest share due to the frequent and ongoing use of restorative and prosthetic materials in daily laboratory operations. There is a continuous demand for ceramics, metals, polymers, and resin-based materials across various dental procedures. This demand is driven by increasing case volumes and a growing focus on aesthetic dentistry. Furthermore, the need for regular restocking, shorter product life cycles, and the expansion of applications in both traditional and digital workflows contribute to the dominance of the materials segment.

Based on materials, the CAD/CAM materials segment accounted for the largest share of the dental laboratories market in 2024.

Based on materials, the global dental laboratories market is divided into metal-ceramics, traditional all-ceramics, CAD/CAM materials, plastics, metals, and processing materials. Among these, the CAD/CAM materials segment holds the largest market share. This is primarily due to the widespread adoption of digital workflows and the growing demand for precise, millable restorative solutions. CAD/CAM materials offer consistent quality, faster turnaround times, and a superior fit compared to traditionally fabricated restorations. The increased use of zirconia, glass ceramics, and lithium disilicate in crowns, bridges, and implant restorations further contributes to the growth of this segment. Additionally, the expansion of chairside and lab-side CAD/CAM systems has accelerated the transition toward digitally compatible materials, reinforcing the position of CAD/CAM materials as the leading category in the dental laboratories market.

North America registered the largest share of the dental laboratories market in 2024.

The global market for dental laboratories is divided into six main regions: North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and the GCC Countries.

North America holds the largest share of the global dental laboratories market. This is driven by its advanced dental healthcare infrastructure, high awareness of oral health and aesthetics, and strong adoption of digital dentistry technologies. The region benefits from the widespread adoption of CAD/CAM systems, intraoral scanners, and 3D printing solutions, all of which are supported by favorable reimbursement policies and a well-established private dental care system. Additionally, North America's dominant position is further reinforced by the strong presence of leading dental technology and materials companies, continuous product innovation, and strategic collaborations between dental service providers and manufacturers. Factors such as rising dental expenditures, an aging population in need of restorative and prosthetic solutions, and the rapid integration of AI-enabled and connected digital workflows continue to support sustained market growth throughout the region.

A breakdown of the primary participants (supply side) for the dental laboratories market referred to in this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (35%), and Tier 3 (35%)

- By Designation: C-level Executives (20%), Director-level Executives (35%), and Others (45%)

- By Region: North America (30%), Europe (25%), Asia Pacific (20%), Latin America (20%), the Middle East & Africa (2%), and the GCC Countries (3%)

Prominent players in the dental laboratories market are Dentsply Sirona (US), Envista (US), Solventum (US), Ivoclar Vivadent AG (Liechtenstein), Planmeca Oy (Finland), GC Corporation (Japan), Mitsui Chemicals, Inc. (Japan), Kuraray Noritake Dental, Inc. (Japan), VOCO GmbH (Germany), Amann Girrbach AG (Austria), BEGO GmbH & Co. KG (Germany), Schutz Dental GmbH (Germany), Institut Straumann AG (Switzerland), VITA Zahnfabrik H. Rauter GmbH & Co. KG (US), Coltene Group (Switzerland), Shofu Inc. (Japan), 3D Systems, Inc. (US), Stratasys (US & Israel), Nakanishi Inc. (Japan), A-dec Inc. (US), Zirkonzahn (Italy), Smart Dent (Brazil), 3Shape A/S (Denmark), SHINING 3D (China), and Exocad (Germany).

Research Coverage

The report provides an analysis of the dental laboratories market, focusing on estimating the market size and potential for future growth across various segments, including products, practices, technologies, regions, and consumer types. Additionally, the report features a competitive analysis of the key players in the market, detailing their company profiles, product & service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report provides valuable insights for market leaders and new entrants in the dental laboratories industry, offering approximate revenue figures for the overall market and its subsegments. It helps stakeholders understand the competitive landscape, enabling them to better position their businesses and develop effective go-to-market strategies. Additionally, the report highlights key market drivers, restraints, challenges, and opportunities, enabling stakeholders to assess the current state of the market.

This report provides insights into the following pointers:

- Analysis of key drivers (rising cases of dental caries and subsequent increase in tooth repair procedures, increasing outsourcing of manufacturing functions to dental laboratories, increasing outsourcing of manufacturing functions to dental laboratories, increasing number of dental laboratories investing in CAD/CAM, and development of technologically advanced solutions), restraints (high cost of dental equipment and materials and increasing surgical costs and lack of access to reimbursement), opportunities (rapid growth of dental service organizations and growing focus on emerging economies and rising disposable income levels), and challenges (pricing pressure faced by prominent market players and dearth of skilled lab professionals).

- Market Penetration: It provides detailed information on the product portfolios offered by major players in the global dental laboratories market. The report covers various segments, including product, practice, technology, region, and consumer type.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global dental laboratories market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product, practice, technology, region, and consumer type.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global dental laboratories market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global dental laboratories market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DENTAL LABORATORIES MARKET OVERVIEW

- 3.2 DENTAL LABORATORIES MARKET, BY REGION, 2025 VS. 2030 (USD MILLION)

- 3.3 DENTAL LABORATORIES MARKET, BY PRODUCT AND COUNTRY, 2024 (USD MILLION)

- 3.4 GEOGRAPHIC SNAPSHOT OF DENTAL LABORATORIES MARKET

- 3.5 DENTAL LABORATORIES MARKET: DEVELOPED VS. EMERGING MARKETS

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising cases of dental caries and increase in tooth repair procedures

- 4.2.1.2 Increasing outsourcing of manufacturing functions to dental laboratories

- 4.2.1.3 Increasing number of dental laboratories investing in CAD/CAM

- 4.2.1.4 Development of technologically advanced solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of dental equipment and materials

- 4.2.2.2 Increasing surgical costs and lack of access to reimbursement

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid growth of dental service organizations

- 4.2.3.2 Growing focus on emerging economies and rising disposable income levels

- 4.2.4 CHALLENGES

- 4.2.4.1 Pricing pressure faced by prominent market players

- 4.2.4.2 Dearth of skilled lab professionals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN DENTAL CONSUMABLES INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DENTAL IMPLANTS & PROSTHETICS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 ROLE IN ECOSYSTEM

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF DENTAL LABORATORY EQUIPMENT, BY KEY PLAYER, 2024

- 5.6.2 AVERAGE SELLING PRICE TREND OF DENTAL LABORATORY EQUIPMENT, BY REGION, 2022-2024

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE: 9021, 2020-2024

- 5.7.2 EXPORT DATA FOR HS CODE: 9021, 2020-2024

- 5.8 KEY CONFERENCES & EVENTS, 2025-2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 STRATASYS TRUEDENT WITH ROBERT DENTAL LABORATORY TO SCALE DIGITAL DENTURE PRODUCTION WITH FASTER TURNAROUND AND SUPERIOR PRECISION

- 5.11.2 DANTECH DENTAL LAB TO ADOPT INTEGRATED CIMSYSTEM MILLBOX WORKFLOW TO BOOST PRECISION, EFFICIENCY, AND DIGITAL MANUFACTURING CAPABILITIES

- 5.11.3 ADT TO BOOST DENTAL PRODUCTION CAPACITY SEVENFOLD AND REDUCE LABOR WITH STRATASYS J3 DENTAJET 3D PRINTING

- 5.12 IMPACT OF 2025 US TARIFF ON DENTAL LABORATORIES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON REGION

- 5.12.4.1 North America

- 5.12.4.1.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.4.1 North America

- 5.12.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CONE BEAM COMPUTED TOMOGRAPHY (CBCT)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 PATENT PUBLICATION TRENDS FOR DENTAL LABORATORIES MARKET

- 6.4.2 TOP APPLICANTS (COMPANIES) OF DENTAL LABORATORY PATENTS

- 6.4.3 JURISDICTION ANALYSIS: TOP APPLICANTS (COUNTRIES) FOR PATENTS IN DENTAL LABORATORIES MARKET

- 6.4.4 LIST OF MAJOR PATENTS

- 6.5 IMPACT OF AI/GEN AI ON DENTAL LABORATORIES MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 TOP CASE STUDIES OF GEN AI IMPLEMENTATION

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI

- 6.6 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 6.6.1 DENTSPLY SIRONA: PRIMESCAN CONNECT TO STREAMLINE DIGITAL IMPRESSION WORKFLOWS

- 6.6.2 STRAUMANN: DIGITAL DENTAL SOLUTIONS TO FOCUS ON AI-ENABLED WORKFLOW AUTOMATION

- 6.6.3 ALIGN TECHNOLOGY: ITERO & EXOCAD TO HAVE SEAMLESS CLINIC-LAB CONNECTIVITY

- 6.6.4 IVOCLAR: PROGAIA PLATFORM TO BUILD SUSTAINABLE AND AUTOMATED PRODUCTION MODEL

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.1.2 Canada

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 China

- 7.1.2.3.2 Japan

- 7.1.2.4 Latin America

- 7.1.2.4.1 Brazil

- 7.1.2.4.2 Mexico

- 7.1.2.5 Middle East

- 7.1.2.6 Africa

- 7.1.2.1 North America

- 7.2 CERTIFICATIONS, LABELLING, AND ECO-STANDARDS

- 7.2.1 CERTIFICATIONS, LABELLING, AND ECO-STANDARDS IN DENTAL LABORATORIES MARKET

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DENTAL LABORATORIES MARKET, BY PRACTICE

- 9.1 INTRODUCTION

- 9.2 RESTORATIVE

- 9.2.1 SHIFT TOWARDS DIGITALLY MANUFACTURED OPTIONS TO SUPPORT MARKET GROWTH

- 9.3 ORTHODONTICS

- 9.3.1 EXPANSION OF DIGITAL ORTHODONTIC WORKFLOWS TO DRIVE MARKET GROWTH

- 9.4 IMPLANTS

- 9.4.1 EXPANSION OF DIGITAL IMPLANTOLOGY TO PROPEL MARKET GROWTH

- 9.5 PROSTHODONTICS

- 9.5.1 INCREASING ADOPTION OF DIGITAL DENTURE WORKFLOWS TO FUEL ADOPTION OF DENTAL LABORATORY MATERIALS

10 DENTAL LABORATORIES MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 MATERIALS

- 10.2.1 METAL CERAMICS

- 10.2.1.1 Established clinical success for restoring damaged or missing teeth to drive growth

- 10.2.2 TRADITIONAL ALL-CERAMICS

- 10.2.2.1 Excellent aesthetic properties to propel segment growth

- 10.2.3 CAD/CAM MATERIALS

- 10.2.4 ZIRCONIA

- 10.2.4.1 Zirconia to hold largest share of CAD/CAM materials segment

- 10.2.5 GLASS CERAMICS

- 10.2.5.1 Focus on production of stronger and tougher materials to aid market growth

- 10.2.6 LITHIUM DISILICATE

- 10.2.6.1 Popularity for usage in dental restorations in anterior and premolar regions to drive growth

- 10.2.7 OTHER CAD/CAM MATERIALS

- 10.2.8 PLASTICS

- 10.2.8.1 High resistance and flexibility of thermoplastics to support market growth

- 10.2.9 METALS

- 10.2.9.1 Anti-leakage properties to augment use of metals in dentistry

- 10.2.10 PROCESSING MATERIALS

- 10.2.10.1 Focus on dental laboratory fabrication workflows to drive usage

- 10.2.1 METAL CERAMICS

- 10.3 EQUIPMENT

- 10.3.1 3D PRINTING SYSTEMS

- 10.3.1.1 Need for rapid and cost-efficient fabrication of dental consumables to drive popularity

- 10.3.2 INTEGRATED CAD/CAM SYSTEMS

- 10.3.2.1 Increasing adoption of CAD/CAM systems in dental laboratories to spur market growth

- 10.3.3 CASTING MACHINES

- 10.3.3.1 Continued use of metal-based restorations in cost-sensitive markets to sustain market demand

- 10.3.4 MILLING EQUIPMENT

- 10.3.4.1 Rapid adoption of CAD/CAM workflows results to provide sustained growth

- 10.3.5 FURNACES

- 10.3.5.1 Technological innovations in dental furnaces to ensure sustained end-use demand

- 10.3.6 ARTICULATORS

- 10.3.6.1 Lower cost of articulators to fuel market demand

- 10.3.7 SCANNERS

- 10.3.7.1 Rising demand for digital dental products and increasing need for faster treatment options to propel market growth

- 10.3.8 OTHER EQUIPMENT

- 10.3.1 3D PRINTING SYSTEMS

- 10.4 SOFTWARE

- 10.4.1 LIMS

- 10.4.1.1 Need for end-to-end visibility into laboratory operations to drive popularity

- 10.4.2 CASE MANAGEMENT SYSTEMS

- 10.4.2.1 Increasing demand for seamless clinic-laboratory coordination to aid market growth

- 10.4.3 OTHER SOFTWARE

- 10.4.1 LIMS

11 DENTAL LABORATORIES MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 CONVENTIONAL TECHNOLOGIES

- 11.2.1 LOWER COST AND WIDESPREAD FAMILIARITY AMONG TECHNICIANS TO SUPPORT MARKET GROWTH

- 11.3 DIGITAL TECHNOLOGIES

- 11.3.1 GROWING DEMAND FOR FASTER, HIGHLY PRECISE, AND STANDARDIZED RESTORATIONS TO DRIVE GROWTH

12 DENTAL LABORATORIES MARKET, BY CONSUMER TYPE

- 12.1 INTRODUCTION

- 12.2 DENTAL HOSPITALS & CLINICS

- 12.2.1 RISING NUMBER OF DENTAL HOSPITALS & CLINICS IN EMERGING ECONOMIES TO SUPPORT MARKET GROWTH

- 12.3 DENTAL SERVICE ORGANIZATIONS

- 12.3.1 NEED FOR LARGE-SCALE, BULK PURCHASING OF MATERIALS AND EQUIPMENT TO DRIVE SEGMENT

- 12.4 OTHER CONSUMER TYPES

13 DENTAL LABORATORIES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 EUROPE

- 13.2.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.2.2 GERMANY

- 13.2.2.1 Favorable government reimbursement policies to drive demand for dental prosthetics

- 13.2.3 ITALY

- 13.2.3.1 Rising penetration of dental products and growing focus on privatized dental care system to aid market growth

- 13.2.4 SPAIN

- 13.2.4.1 Presence of well-established dental healthcare infrastructure to propel market growth

- 13.2.5 FRANCE

- 13.2.5.1 Favorable distribution network and greater awareness about dental health to fuel market demand

- 13.2.6 UK

- 13.2.6.1 Increasing demand for dental implant procedures to drive market

- 13.2.7 REST OF EUROPE

- 13.3 NORTH AMERICA

- 13.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.3.2 US

- 13.3.2.1 High per capita income and high treatment quality to support market growth

- 13.3.3 CANADA

- 13.3.3.1 Rising healthcare expenditure and increasing public awareness of oral healthcare to fuel market growth

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 SOUTH KOREA

- 13.4.2.1 High geriatric population to support market demand for dental treatments

- 13.4.3 JAPAN

- 13.4.3.1 Rising geriatric population and favorable reimbursement scenario to spur market growth

- 13.4.4 CHINA

- 13.4.4.1 Growing prevalence of dental diseases and increasing geriatric population to drive market

- 13.4.5 INDIA

- 13.4.5.1 Growing dental tourism and expanding access to dental care to support market growth

- 13.4.6 AUSTRALIA

- 13.4.6.1 Increasing registered dental practitioners to spur market growth

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Improving access to advanced dental care and rising prevalence of partial edentulism to drive market

- 13.5.3 MEXICO

- 13.5.3.1 Focus on improving healthcare infrastructure and availability of skilled dentists to drive market

- 13.5.4 COLOMBIA

- 13.5.4.1 Lower dental care costs to support market growth

- 13.5.5 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.7 GCC COUNTRIES

- 13.7.1 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN DENTAL LABORATORIES MARKET

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Product footprint

- 14.5.5.4 Technology footprint

- 14.5.5.5 Consumer type footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/PRODUCT COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES & UPGRADES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 DENTSPLY SIRONA

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches & upgrades

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 PLANMECA OY

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 ENVISTA

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 SOLVENTUM

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 IVOCLAR VIVADENT

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 GC CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Expansions

- 15.1.7 MITSUI CHEMICALS, INC.

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Expansions

- 15.1.8 KURARAY NORITAKE DENTAL, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Expansions

- 15.1.9 VOCO GMBH

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 AMANN GIRRBACH AG

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Expansions

- 15.1.11 BEGO GMBH & CO. KG

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 SCHUTZ DENTAL GMBH

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.13 INSTITUT STRAUMANN AG

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.13.3.2 Expansions

- 15.1.14 VITA ZAHNFABRIK H. RAUTER GMBH & CO. KG

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.15 COLTENE GROUP

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.1 DENTSPLY SIRONA

- 15.2 OTHER PLAYERS

- 15.2.1 SHOFU INC.

- 15.2.2 3D SYSTEMS, INC.

- 15.2.3 STRATASYS

- 15.2.4 NAKANISHI INC.

- 15.2.5 A-DEC INC.

- 15.2.6 ZIRKONZAHN

- 15.2.7 SMART DENT

- 15.2.8 3SHAPE A/S

- 15.2.9 SHINING 3D

- 15.2.10 EXOCAD

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key objectives of primary research

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.2.3 BASE NUMBER ESTIMATION

- 16.2.3.1 Supply-side analysis (revenue share analysis)

- 16.2.3.2 Company presentations and primary interviews

- 16.3 MARKET FORECAST APPROACH

- 16.4 DATA TRIANGULATION

- 16.5 STUDY ASSUMPTIONS

- 16.5.1 MARKET SHARE ASSUMPTIONS

- 16.6 FACTOR ANALYSIS

- 16.7 RISK ASSESSMENT

- 16.8 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS