|

시장보고서

상품코드

1950787

선박용 윤활유 시장 : 선박 유형별, 제품 유형별, 베이스오일별, 지역별 - 예측(-2030년)Marine Lubricants Market by Base Oil (Mineral Oil, Synthetic Oil, and Bio-based Oil), Product Type (Engine Oil, Hydraulic Fluid, Compressor Oil), Ship Type (Bulk Carriers, Container Ships, Tankers), and Region - Global Forecast to 2030 |

||||||

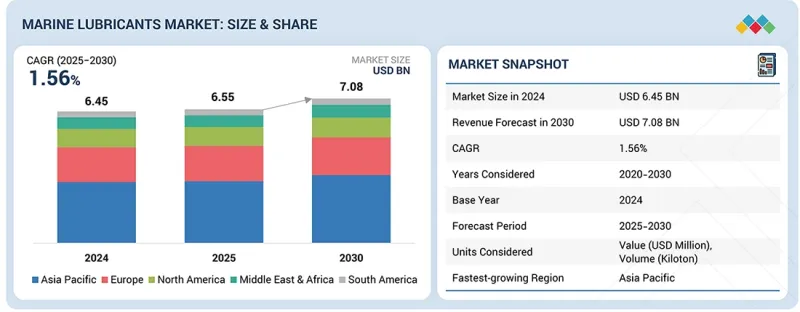

선박용 윤활유 시장 규모는 2025년에 65억 5,000만 달러로 평가되었고 2025년부터 2030년까지 연평균 복합 성장률(CAGR)1.56%로 성장을 지속하여, 2030년까지 70억 8,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 선박 유형별, 제품 유형별, 기유별, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

선박용 윤활유 시장은 세계 해상 무역 증가와 배출가스 및 선박 효율에 대한 엄격한 환경 규제로 인해 성장하고 있습니다. 선박 운영자는 규제 요건을 충족하기 위해 고성능 및 친환경 윤활유 사용을 늘리고 있습니다. 이러한 추세는 엔진의 신뢰성, 연료 효율성, 설비 수명에 대한 관심이 높아지면서 선박용 윤활유가 선박 운항에 필수적인 요소로 자리 잡았음을 반영합니다.

2024년 합성유 부문은 전체 선박용 윤활유 시장에서 가치 기준으로 두 번째 점유율을 차지했습니다. 이러한 우위는 우수한 성능 특성에 기인합니다. 합성유는 우수한 내열성, 긴 수명, 엔진 보호 성능을 제공하기 때문에 현대의 선박 엔진과 가혹한 운전 조건에서 널리 사용되고 있습니다.

압축기 오일 부문은 예측 기간 동안 가치 기준으로 가장 빠르게 성장하는 제품 유형이 될 것으로 예측됩니다. 이는 현대 선박의 압축공기 시스템 및 냉동 컴프레서 채택이 증가했기 때문입니다. 엔진의 고성능화에 대한 수요 증가, 유지보수 간격의 단축, 운영 신뢰성의 향상으로 고성능 압축기 오일의 사용이 촉진되고 있습니다.

북미는 2024년 세계 3위의 선박용 윤활유 시장 규모를 기록했습니다. 이 지역 시장은 활발한 해상 무역 활동과 대규모 상선 및 해양 선단의 존재에 의해 주도되고 있습니다. 또한, 해양 석유 및 가스 사업, 내륙 수로 운송, 정기적인 선박 유지보수 및 업그레이드 활동으로 수요가 뒷받침되고 있습니다. 이러한 요인에 더해 환경 보호 규제와 고성능 윤활유 채택은 선박용 윤활유 시장의 꾸준한 성장을 가속하고 있습니다.

시장 주요 기업은 BP p.l.c.(영국), Chevron Corporation(미국), Exxon Mobil Corporation(미국), Shell plc(영국), TotalEnergies SE(프랑스), Petronas(말레이시아), LUKOIL(러시아), Idemitsu Kosan(일본), ENEOS Holdings, Inc. 말레이시아), LUKOIL(러시아), Idemitsu Kosan(일본), China Petroleum & Chemical Corporation(중국), ENEOS Holdings, Inc. Emirates National Oil Company(UAE), ENI S.p.A(이탈리아), Indian Oil Corporation Limited(인도), PetroChina Company Limited(중국), Moeve(스페인), FUCHS(독일), Gazprom(러시아), ENEOS Holdings, Inc.(독일), Gazprom(러시아), Calumet, Inc.(미국)입니다.

조사 범위

이 보고서는 선박용 윤활유 시장을 기유별, 제품 유형별, 선박 유형별, 지역별로 세분화하여 각 지역별 시장 규모와 추정치(단위 - 백만 달러)를 제공합니다. 이 보고서는 주요 업계 진출 기업에 대한 상세한 분석을 통해 각 기업의 사업 개요, 서비스 및 선박용 윤활유 시장과 관련된 주요 전략에 대한 인사이트를 제공합니다.

본 보고서 구매 이유

본 조사 보고서는 산업 분석(업계 동향), 주요 기업의 시장 점유율 분석, 기업 프로파일 등 다양한 수준의 분석에 초점을 맞추었습니다. 이를 종합하여 선박용 윤활유 시장 경쟁 구도, 신흥 및 고성장 부문, 고성장 지역, 시장 성장 촉진요인, 억제요인, 성장 기회에 대한 전체 그림을 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 시장 침투 현황: 세계 시장의 주요 기업들이 제공하는 선박용 윤활유에 대한 종합적인 정보

- 주요 촉진요인(세계 해상 무역량 및 선박 가동률 증가, 노후화된 세계 선대별 유지보수 및 윤활유 교체 수요 증가, 고출력 고연비 선박용 엔진 채택, 해상 에너지 및 풍력 발전 설비 및 지원선박 확대, 운영 신뢰성 및 자산 수명 연장에 대한 관심 증가), 제약 요인 분석, 기회 요인(합성 윤활유의 높은 비용, 새로운 배합에 대한 복잡한 승인 및 OEM 승인 요구, 환경 친화적, 생분해성 윤활유에 대한 수요 증가), 제약 요인(합성 윤활유의 높은 비용, 새로운 배합에 대한 복잡한 승인 및 OEM 요구)(합성 및 친환경 선박용 윤활유의 높은 비용, 신규 배합에 대한 복잡한 승인 및 OEM 인증 요건), 기회(친환경 및 생분해성 윤활유 수요 증가, LNG, 메탄올, 암모니아 등 대체 연료용 특수 윤활유, 상태 모니터링형 유지보수 및 윤활유 모니터링 서비스 성장), 과제(다양화 다양해지는 환경 규제 대응, 원유 및 기유 가격 변동에 따른 배합 경제성 영향)이 선박용 윤활유 시장 성장에 미치는 영향

- 제품 개발/혁신 : 선박용 윤활유 시장의 향후 기술 동향, 연구개발 활동, 제품 및 서비스 출시에 대한 상세 분석

- 시장 개발: 수익성 높은 신흥 시장에 대한 종합적인 정보 - 이 보고서는 지역별 선박용 윤활유 시장을 분석합니다.

- 시장 다각화 : 신제품, 미개척 지역 및 세계 선박용 윤활유 시장의 최근 동향에 대한 종합적인 정보

- 경쟁 평가: 선박용 윤활유 시장 내 주요 기업의 시장 점유율, 전략, 제품, 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 선박용 윤활유 시장(선박 유형별)

제10장 선박용 윤활유 시장(제품 유형별)

제11장 선박용 윤활유 시장(베이스오일 별)

제12장 선박용 윤활유 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 인접 시장과 관련 시장

제17장 부록

LSH 26.03.13The marine lubricants market size was valued at USD 6.55 billion in 2025 and is projected to reach USD 7.08 billion by 2030, at a CAGR of 1.56% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Oil Type, Product Type, Ship Type, and Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and South America |

"Rising maritime trade and regulatory compliance requirements are driving the marine lubricants market growth."

The marine lubricants market is growing due to the increasing global seaborne trade and stringent environmental regulations related to emissions and vessel efficiency. Ship operators are increasingly using high-performance and environmentally friendly lubricants to meet regulatory demands. This trend reflects the growing emphasis on engine reliability, fuel economy, and equipment longevity, making marine lubricants essential for ship operation.

"The synthetic oil segment accounted for the second-largest market share of marine lubricants."

In 2024, the synthetic oil segment accounted for the second-largest value share in the overall marine lubricants market. This dominance is driven by its better performance properties. Synthetic oil provides better thermal properties, longer lifespan, and better protection for the engines; therefore, it is widely used in modern marine engines and demanding operating conditions.

"The compressor oil segment is projected to be the fastest-growing product type during the forecast period."

The compressor oil segment is estimated to be the fastest-growing product type, in terms of value, during the forecast period. This is due to the increased adoption of compressed air systems and the refrigeration compressors on modern vessels. Increasing demand for the high performance of the engines, the reduced maintenance intervals, and the enhanced reliability of the operations are leading to the use of high-performance compressor oils.

"North America accounted for the third-largest share in the global marine lubricants market, in terms of value, in 2024."

North America was the third-largest marine lubricants market in 2024. The market in the region is driven by strong maritime trade activity and the presence of a sizable commercial and offshore fleet. The demand is also backed by the offshore oil and gas operations, inland waterway transport, and regular vessel maintenance and upgrade activities. All these factors, along with the regulations for environmental protection and the adoption of high-performance lubricants, support steady market growth of marine lubricants.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, RoW- 5%

The key players profiled in the report include BP p.l.c. (UK), Chevron Corporation (US), Exxon Mobil Corporation (US), Shell plc (UK), TotalEnergies SE (France), Petronas (Malaysia), LUKOIL (Russia), Idemitsu Kosan Co., Ltd (Japan), China Petroleum & Chemical Corporation (China), ENEOS Holdings, Inc. (Japan), Gulf Oil International Ltd. (UK), Emirates National Oil Company (UAE), ENI S.p.A (Italy), Indian Oil Corporation Limited (India), PetroChina Company Limited (China), Moeve (Spain), FUCHS (Germany), Gazprom (Russia), and Calumet, Inc. (US).

Study Coverage

This report segments the market for marine lubricants based on base oil, product type, ship type, and region, and provides estimations of value (in USD Million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies associated with the marine lubricants market.

Reasons to Buy This Report

This research report is focused on various levels of analysis-industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the marine lubricants market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights into the following points:

- Market Penetration: Comprehensive information on marine lubricants offered by top players in the global market

- Analysis of key drivers (Growth in global seaborne trade and vessel utilization, aging global fleet increasing demand for maintenance and lubricant replacement, adoption of fuel-efficient and high-output marine engines, expansion of offshore energy, wind installation, and support vessels, and increasing focus on operational reliability and asset life extension), restraints (High cost of synthetic and environmentally acceptable marine lubricants and complex approval and OEM certification requirements for new formulations), opportunities (Rising demand for environmentally acceptable and biodegradable lubricants, lubricants tailored for alternative fuels such as LNG, methanol, and ammonia, and growth in condition-based maintenance and lubricant monitoring services), and challenges (Compliance with evolving and fragmented environmental regulations and volatility in crude oil and base oil prices affecting formulation economics) influencing the growth of the marine lubricants market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the marine lubricants market

- Market Development: Comprehensive information about lucrative emerging markets-the report analyzes the market for marine lubricants across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global marine lubricants market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the marine lubricants market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 MARKET DEFINITION AND INCLUSIONS, BY BASE OIL

- 1.3.4 MARKET DEFINITION AND INCLUSIONS, BY PRODUCT TYPE

- 1.3.5 MARKET DEFINITION AND INCLUSIONS, BY SHIP TYPE

- 1.3.6 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MARINE LUBRICANTS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MARINE LUBRICANTS MARKET

- 3.2 MARINE LUBRICANTS MARKET, BY BASE OIL AND REGION

- 3.3 MARINE LUBRICANTS MARKET, BY PRODUCT TYPE

- 3.4 MARINE LUBRICANTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in global seaborne trade and vessel utilization

- 4.2.1.2 Aging global fleet increasing demand for maintenance and lubricant replacement

- 4.2.1.3 Adoption of fuel-efficient and high-output marine engines

- 4.2.1.4 Expansion of offshore energy, wind installation, and support vessels

- 4.2.1.5 Increasing focus on operational reliability and asset life extension

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of synthetic and environmentally acceptable marine lubricants

- 4.2.2.2 Complex approval and OEM certification requirements for new formulations

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising demand for environmentally acceptable and biodegradable lubricants

- 4.2.3.2 Lubricants tailored for alternative fuels such as LNG, methanol, and ammonia

- 4.2.3.3 Growth in condition-based maintenance and lubricant monitoring services

- 4.2.4 CHALLENGES

- 4.2.4.1 Compliance with evolving and fragmented environmental regulations

- 4.2.4.2 Volatility in crude oil and base oil prices affecting formulation economics

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.4.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF SUBSTITUTES

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 MARINE LUBRICANT MANUFACTURERS

- 5.3.3 MARKETING & DISTRIBUTION

- 5.3.4 END-USE INDUSTRIES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF MARINE LUBRICANTS OFFERED BY KEY PLAYERS, BY TOP THREE BASE OILS, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF MARINE LUBRICANTS, BY REGION, 2023-2030

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE-2710)

- 5.6.2 IMPORT SCENARIO (HS CODE-2710)

- 5.7 KEY CONFERENCES & EVENTS IN 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 LUBRICANT SAVINGS AND CLEANER ENGINE WITH MOBILGARD 5100

- 5.10.2 SUSESEA BULK CARRIER FLEET CUTS CYLINDER OIL FEED BY 33% WITH CHEVRON'S TARO ULTRA ADVANCED 40

- 5.10.3 CHEVRON'S TARO ULTRA ADVANCED 40 ENHANCES ENGINE PERFORMANCE ON MV CARLOS FISCHER

- 5.11 IMPACT OF 2025 US TARIFF - MARINE LUBRICANTS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFFS

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BIO-BASED AND ENVIRONMENTALLY ACCEPTABLE MARINE LUBRICANTS (EALS)

- 6.1.2 SMART LUBRICANTS AND CONDITION-RESPONSIVE ADDITIVE SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DIGITAL OIL CONDITION MONITORING AND PREDICTIVE ANALYTICS

- 6.2.2 ADVANCED MARINE ENGINE AND FUEL SYSTEM TECHNOLOGIES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027)

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+)

- 6.4 PATENT ANALYSIS

- 6.4.1 APPROACH

- 6.4.2 DOCUMENT TYPE

- 6.4.3 TOP APPLICANTS

- 6.4.4 JURISDICTION ANALYSIS

- 6.5 IMPACT OF AI/GEN AI ON MARINE LUBRICANTS MARKET

- 6.5.1 ACCELERATED FORMULATION DEVELOPMENT AND REGULATORY COMPLIANCE

- 6.5.2 ENHANCED BLENDING EFFICIENCY AND QUALITY ASSURANCE

- 6.5.3 PREDICTIVE MAINTENANCE AND ASSET RELIABILITY OPTIMIZATION

- 6.5.4 OPTIMIZED DEMAND FORECASTING AND PORT-LEVEL INVENTORY MANAGEMENT

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 REGULATORY POLICY INITIATIVES

- 7.2.1 SAFETY PROTOCOLS

- 7.2.2 SUSTAINABLE DEVELOPMENT

- 7.2.3 STANDARDIZATION

- 7.2.4 CIRCULAR ECONOMY

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS APPLICATIONS

9 MARINE LUBRICANTS MARKET, BY SHIP TYPE

- 9.1 INTRODUCTION

- 9.2 BULK CARRIERS

- 9.2.1 HIGH FLEET DENSITY AND LONG-DURATION VOYAGES

- 9.3 TANKERS (OIL, GAS, CHEMICALS)

- 9.3.1 STRINGENT OPERATIONAL AND COMPLIANCE REQUIREMENTS

- 9.4 CONTAINER SHIPS

- 9.4.1 HIGH-SPEED OPERATIONS AND ENGINE STRESS

- 9.5 OTHER SHIP TYPES

10 MARINE LUBRICANTS MARKET, BY PRODUCT TYPE

- 10.1 INTRODUCTION

- 10.2 ENGINE OIL

- 10.2.1 ENGINE RELIABILITY REQUIREMENTS TO DRIVE MARKET FOR ENGINE OIL

- 10.3 HYDRAULIC FLUID

- 10.3.1 EXPANSION OF DECK AND CONTROL SYSTEMS TO DRIVE HYDRAULIC FLUID MARKET

- 10.4 COMPRESSOR OIL

- 10.4.1 INCREASED USE OF COMPRESSED AIR SYSTEMS TO DRIVE COMPRESSOR OIL MARKET

- 10.5 OTHER PRODUCT TYPES

11 MARINE LUBRICANTS MARKET, BY BASE OIL

- 11.1 INTRODUCTION

- 11.2 MINERAL OIL

- 11.2.1 COST-EFFECTIVE LUBRICATION SUPPORTING LARGE-SCALE MARINE OPERATIONS

- 11.3 SYNTHETIC OIL

- 11.3.1 PERFORMANCE RELIABILITY UNDER SEVERE AND HIGH-STRESS OPERATING CONDITIONS

- 11.4 BIO-BASED OIL

- 11.4.1 REGULATORY PRESSURE FOR ENVIRONMENTALLY ACCEPTABLE MARINE LUBRICANTS

12 MARINE LUBRICANTS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 High investment in domestic and international maritime trade activities

- 12.2.2 SINGAPORE

- 12.2.2.1 Well-established marine services infrastructure

- 12.2.3 HONG KONG

- 12.2.3.1 Rise in trading activities

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Advanced shipbuilding driving marine lubricants demand

- 12.2.5 MALAYSIA

- 12.2.5.1 Growth in shipbuilding industry

- 12.2.6 JAPAN

- 12.2.6.1 Government support and integrated maritime industry

- 12.2.7 TAIWAN

- 12.2.7.1 Growth in export and maritime trade

- 12.2.8 INDIA

- 12.2.8.1 Economic growth, favorable government policies & incentive framework, and long coastline

- 12.2.9 AUSTRALIA

- 12.2.9.1 Large exports of coal and metals

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Rise in domestic and international maritime trade

- 12.3.2 CANADA

- 12.3.2.1 Increase in demand for bulk carriers, oil tankers, and container ships

- 12.3.3 MEXICO

- 12.3.3.1 Rapid industrialization and rising population

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Growth of maritime industry

- 12.4.2 NETHERLANDS

- 12.4.2.1 Strong presence of world's leading manufacturers of high-end yachts and special vessels

- 12.4.3 BELGIUM

- 12.4.3.1 Geographical location makes Belgium an attractive market

- 12.4.4 SPAIN

- 12.4.4.1 Spanish shipbuilding industry plays major role in driving market

- 12.4.5 UK

- 12.4.5.1 Popular manufacturing hub for shipbuilding industry

- 12.4.6 ITALY

- 12.4.6.1 Leading manufacturer of fishing ships and cruise liners

- 12.4.7 FRANCE

- 12.4.7.1 Operational and regulatory drivers supporting marine lubricants demand

- 12.4.8 GREECE

- 12.4.8.1 Growing economy and investment in infrastructure to drive demand for marine lubricants

- 12.4.9 TURKEY

- 12.4.9.1 Rise in development of ships and other naval vessels

- 12.4.10 RUSSIA

- 12.4.10.1 Growing economy and investment in infrastructure

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 UAE

- 12.5.1.1 Increase in maritime activities owing to oil & gas exports

- 12.5.2 SAUDI ARABIA

- 12.5.2.1 Strong foothold of shipbuilding, shipbreaking, and refurbishment companies

- 12.5.3 SOUTH AFRICA

- 12.5.3.1 Increasing maritime traffic to support market growth

- 12.5.1 UAE

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Rapidly expanding economy to drive demand for marine lubricants

- 12.6.2 PANAMA

- 12.6.2.1 Increase in maritime traffic due to opening of Panama Canal to drive demand

- 12.6.3 ARGENTINA

- 12.6.3.1 Rapidly expanding economy to drive demand for marine lubricants

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 13.3 MARKET SHARE ANALYSIS, 2024

- 13.4 REVENUE ANALYSIS, 2020-2024

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Regional footprint

- 13.5.5.3 Ship type footprint

- 13.5.5.4 Product type footprint

- 13.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2024

- 13.6.5.1 List of start-ups/SMEs

- 13.6.5.2 Competitive benchmarking of start-ups/SMEs

- 13.7 PRODUCT COMPARISON

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 BP P.L.C. (UK)

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Expansions

- 14.1.1.4 MnM View

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 CHEVRON CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM View

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 EXXON MOBIL CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM View

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 SHELL PLC

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Expansions

- 14.1.4.3.3 Deals

- 14.1.4.4 MnM View

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 TOTALENERGIES SE

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Expansions

- 14.1.5.3.3 Deals

- 14.1.5.4 MnM View

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 PETRONAS

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.7 IDEMITSU KOSAN CO., LTD

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.8 CHINA PETROLEUM & CHEMICAL CORPORATION

- 14.1.8.1 Business Overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Expansions

- 14.1.9 PETROCHINA COMPANY LIMITED

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.10 FUCHS SE

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches

- 14.1.10.3.2 Deals

- 14.1.10.3.3 Expansions

- 14.1.11 LUKOIL

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Deals

- 14.1.12 ENEOS HOLDINGS, INC.

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.13 GULF OIL INTERNATIONAL LTD.

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Product launches

- 14.1.14 EMIRATES NATIONAL OIL COMPANY (ENOC)

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches

- 14.1.14.3.2 Deals

- 14.1.15 ENI S.P.A.

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Solutions/Services offered

- 14.1.16 INDIAN OIL CORPORATION LIMITED

- 14.1.16.1 Business overview

- 14.1.16.2 Products/Solutions/Services offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Deals

- 14.1.17 MOEVE

- 14.1.17.1 Business overview

- 14.1.17.2 Products/Solutions/Services offered

- 14.1.18 GAZPROM

- 14.1.18.1 Business overview

- 14.1.18.2 Products/Solutions/Services offered

- 14.1.19 CALUMET, INC.

- 14.1.19.1 Business overview

- 14.1.19.2 Products/Solutions/Services offered

- 14.1.1 BP P.L.C. (UK)

- 14.2 STARTUP/SME PLAYERS

- 14.2.1 ADDINOL LUBE OIL GMBH

- 14.2.2 SK ENMOVE CO., LTD.

- 14.2.3 GANDHAR OIL REFINERY (INDIA) LIMITED

- 14.2.4 PENRITE OIL COMPANY

- 14.2.5 SCHAEFFER MANUFACTURING CO.

- 14.2.6 DYADE LUBRICANTS

- 14.2.7 KLUBER LUBRICATION

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Primary participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 GROWTH FORECAST

- 15.3.1 SUPPLY SIDE

- 15.3.2 DEMAND SIDE

- 15.4 DATA TRIANGULATION

- 15.5 FACTOR ANALYSIS

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 RESEARCH LIMITATIONS

- 15.8 RISK ASSESSMENT

16 ADJACENT & RELATED MARKETS

- 16.1 INTRODUCTION

- 16.2 LIMITATIONS

- 16.3 BASE OIL MARKET

- 16.3.1 MARKET DEFINITION

- 16.3.2 MARKET OVERVIEW

- 16.4 BASE OIL MARKET, BY REGION

- 16.4.1 ASIA PACIFIC

- 16.4.2 EUROPE

- 16.4.3 NORTH AMERICA

- 16.4.4 MIDDLE EAST & AFRICA

- 16.4.5 SOUTH AMERICA

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS