|

시장보고서

상품코드

1956047

분취 및 공정용 크로마토그래피 시장 : 제품 유형별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2031년)Preparative and Process Chromatography Market by Product (Preparative, Process ), Application, End User, Region - Global Forecast to 2031 |

||||||

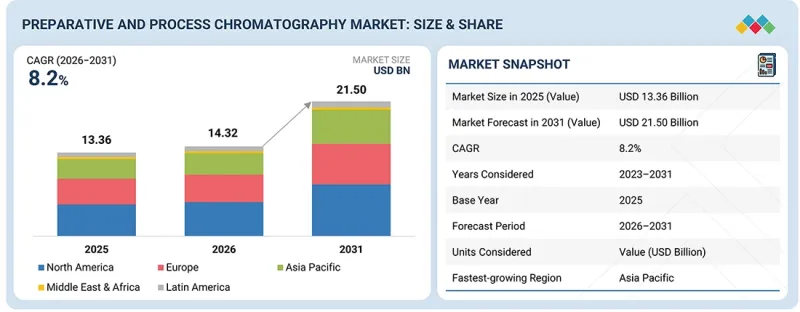

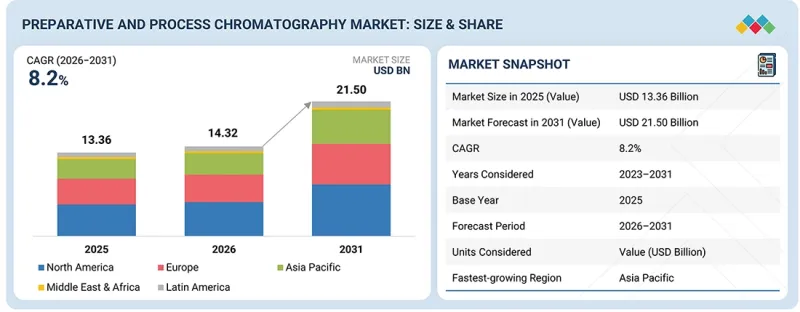

세계의 분취 및 공정용 크로마토그래피 시장 규모는 2026년 143억 2,000만 달러에서 2031년까지 215억 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 8.2%로 성장할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품 유형별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

CGT, 올리고, mRNA 등 새로운 기법을 이용한 백신 및 재조합 단백질은 일부 선진국에서 맞춤형 치료에 대한 수요가 증가함에 따라 그 수요가 증가할 것으로 예상됩니다. 수요량이 증가함에 따라 이러한 다양한 생물학적 제제의 정제가 필요합니다. 이러한 변화로 인해 크로마토그래피는 특히 포집 및 정제에 있어 중요한 단위 작업으로 자리 잡으면서 시장 성장의 여지가 생기고 있습니다. 세계 단클론항체(mAb) 파이프라인이 확대되고 있으며, FDA 승인 건수 증가와 신규 이중특이성항체-항체약물접합체(ADC) 출시가 두드러지게 나타나고 있습니다. 이에 따라 최종사용자의 정제 요구가 증가하고 있으며, 분취 및 공정용 크로마토그래피 제품의 시장 확대가 기대되고 있습니다.

제품별로 분취 및 공정용 크로마토그래피 시장은 분취용 크로마토그래피와 공정용 크로마토그래피로 구분됩니다. 공정용 크로마토그래피가 가장 큰 시장 점유율을 차지했습니다. 주요 제약 시설과 CDMO를 포함한 전 세계 제약 및 바이오의약품 최종사용자는 분획 단계보다 공정 크로마토그래피용으로 설계된 상업용 다운스트림 워크플로우에 초점을 맞추고 있습니다. 신규 플랜트 및 대규모 제조 시설은 공정용 수지, 컬럼 및 서비스에 대한 지속적인 다년간의 수요를 주도하고 있습니다. 이러한 요인으로 인해 공정 규모 크로마토그래피 제품이 세계 시장에서 가장 큰 점유율을 차지했습니다.

용도별로 분리 및 공정용 크로마토그래피 시장은 단클론항체 및 재조합 단백질, 백신, 펩타이드 및 올리고뉴클레오티드, 세포 및 유전자 치료, 기타 용도로 분류됩니다. 단클론항체 및 재조합 단백질 생산 분야가 2025년 가장 큰 시장 점유율을 차지했습니다. 단클론항체(mAb)는 종양학, 면역학, 감염학, 희귀질환의 적응증에서 널리 사용되는 생물학적 치료법이 되었습니다. 규제 경로가 확립되고, 제조 공정이 표준화되었으며, 바이오시밀러 경쟁이 시장 성장을 촉진하고 있습니다. 표준화된 다단계 정제 워크플로는 수지 및 소모품에 대한 안정적인 수요를 창출하고 있습니다. 업계에서는 mAb 정제에 있어 입증된 3단계 크로마토그래피 트레인이 주류로 자리 잡고 있습니다. 단백질 A 친화성 포획(세포배양액에서 표적 항체를 분리), 중간 정제(일반적으로 이온 교환을 통한 응집체 및 잔류 불순물 제거), 최종 정제(사양 등급 순도 달성 및 잔류 리간드 제거). 이러한 요인으로 인해 단클론항체 및 재조합 단백질 생산 응용 분야가 가장 큰 점유율을 차지할 수 있었습니다.

최종사용자별로 분취 및 공정용 크로마토그래피 시장은 제약 및 바이오 제약 기업, 식품 및 건강보조식품 기업, 연구 기관 및 학술 기관, 기타 최종사용자로 분류됩니다. 2024년에는 제약 및 바이오 기업이 가장 큰 점유율을 차지했습니다. 일관된 품질, 높은 수율, 규제 준수를 통해 대규모 상업용 바이오의약품을 생산해야 하는 통합 제약 및 바이오의약품 제조업체는 분취 및 공정용 크로마토그래피의 주요 고객 기반을 형성하고 있습니다. 이들 조직은 mAb, 재조합 단백질, 백신 정제에 최적화된 전용 다운스트림 공정 시설을 운영하고 있으며, 수지, 컬럼, 시스템, 기술 지원의 지속적인 공급을 필요로 합니다. 대형 제약사들은 자체적으로 공정 개발 및 제조 전문성을 보유하고 있으며, 첨단 크로마토그래피 플랫폼에 많은 투자를 하고 있습니다. 이러한 사업의 안정성과 규모, 엄격한 품질 및 규제 요건과 결합하여 이 회사는 주요 최종사용자 부문에서 큰 수요를 창출하고 있습니다. 이러한 요인들이 이 회사의 최대 점유율 확보에 기여했습니다.

분취 및 공정용 크로마토그래피 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카의 5개 주요 지역으로 구성되어 있습니다. 2025년 기준, 북미는 분취 및 공정용 크로마토그래피 제품 시장에서 가장 큰 점유율을 차지했습니다. 그 우위는 상업적 규모와 임상시험 공급 생산에 초점을 맞춘 제조 능력의 강화에 기인합니다. 투자 동향에 따르면, 미국 연방 및 주 정부의 지원은 전염병 대응 및 국제 공급망에 대한 의존도를 줄이기 위해 국내 바이오 제조를 촉진하고 있습니다. 중소규모의 바이오기업들이 CDMO와의 제휴를 확대하는 것도 2025년 북미가 가장 큰 시장 점유율을 확보한 요인으로 꼽힙니다.

분취 및 공정용 크로마토그래피 시장의 주요 기업 프로파일은 다음과 같습니다. Danaher Corporation(미국), Repligen Corporation(미국), Merck KGaA(독일), Thermo Fisher Scientific(미국), Agilent Technologies, Inc. Laboratories, Inc.(미국), Avantor, Inc.(미국), Sartorius AG(독일), Shimadzu Corporation(일본), Ecolab Inc.(미국), Tosoh Bioscience(일본), Mitsubishi Chemical Group Corporation(일본), Revvity(미국), PerkinElmer(미국), Cecil Instruments Limited(영국), W.R. Grace & Co.(미국), Ecom SPO(체코공화국), BUCHI Labortechnik AG(스위스), Good Science(천진) Instrument Technologies(중국), Bio Works Technologies(스웨덴), Sykam GmbH(독일), Sunresin New Materials(중국)(중국), YMC(일본), Geno Technology Inc.)

조사 범위

이 보고서는 분취 및 공정용 크로마토그래피 시장을 제품별, 용도별, 최종사용자별, 지역별로 분석하고 있습니다. 시장 성장을 이끄는 요인, 산업 전반의 과제와 기회, 시장 리더부터 중소기업까지 포함한 경쟁 구도를 살펴봅니다. 또한, 5개 지역의 각 시장 부문에 대한 수익 예측과 마이크로 시장 분석이 포함되어 있습니다.

본 보고서 구매의 의의

이 보고서는 전체 분별 및 공정 크로마토그래피 시장과 그 하위 부문의 정확한 시장 수익 추정치를 제공함으로써 시장 리더와 신규 진입자를 지원합니다. 이해관계자가 경쟁 상황을 이해하고, 비즈니스를 보다 효과적으로 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있도록 돕습니다. 또한, 주요 촉진요인, 억제요인, 도전 과제, 기회 등 시장 역학에 대한 인사이트를 제공합니다.

이 보고서는 다음 사항에 대한 통찰력 있는 데이터를 제공합니다.

- 시장 침투 현황 : 분취 및 공정용 크로마토그래피 시장에서 주요 기업이 제공하는 제품 포트폴리오에 대한 상세 분석

- 제품 개발/혁신 : 분별 및 공정 크로마토그래피 시장의 주요 기업이 제공하는 제품 포트폴리오에 대한 심층 분석

- 시장 개발 : 수익성 높은 성장 분야에 대한 인사이트가 담긴 데이터

- 시장 다각화 : 분취 및 공정용 크로마토그래피 시장의 최근 동향과 발전에 대한 자세한 내용

- 경쟁사 평가 : 주요 경쟁사 제품, 성장 전략, 수익 예측, 시장 범주에 대한 광범위한 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 및 AI 도입을 통한 전략적 혁신

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 분취 및 공정용 크로마토그래피 시장(제품 유형별)

제10장 분취 및 공정용 크로마토그래피 시장(용도별)

제11장 분취 및 공정용 크로마토그래피 시장(최종사용자별)

제12장 분취 및 공정용 크로마토그래피 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.03.19The global preparative and process chromatography market is projected to reach USD 21.50 billion by 2031 from USD 14.32 billion in 2026, growing at a CAGR of 8.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Vaccines and recombinant proteins using new modalities such as CGT, oligos, and mRNA are expected to grow in volume as demand for more personalized treatments rises in some developed economies. With increased volume, this diversity of biologics needs to be purified. These shifts make chromatography a critical unit operation, especially for capture and purification, creating space for market growth. The global monoclonal antibody (mAb) pipeline is expanding, marked by high FDA approvals and new bispecific and antibody-drug conjugate launches. This has helped boost purification requirements among end users, which is expected to increase the market for preparative and process chromatography products.

"Based on product type, process chromatography products held the largest share of the market in 2025."

Based on product, the preparative and process chromatography market is segmented into preparative chromatography and process chromatography. Process chromatography accounted for the largest share of the market. Global pharmaceutical and biopharmaceutical end users-which include major pharma facilities and CDMOs-are focused on commercial downstream workflows designed for process chromatography rather than preparative stages. New plants or large-scale manufacturing facilities drive recurring, multi-year demand for process resins, columns, and services. These factors helped process-scale chromatography products capture the largest share of the global market.

"Based on applications, the monoclonal antibodies and recombinant proteins segment held the largest share in 2025."

By application, the market for preparative and process chromatography is categorized into monoclonal antibodies & recombinant proteins, vaccines, peptides and oligonucleotides, cell and gene therapies, and other applications. The monoclonal antibodies & recombinant proteins production application acquired the largest market share in 2025. Monoclonal antibodies (mAbs) have become a widely adopted biotherapeutic modality across oncology, immunology, infectious disease, and rare disease indications. Regulatory pathways are well established, manufacturing processes are standardized, and biosimilar competition has driven market growth. Standardized, multi-step purification workflows drive consistent resin and consumables demand. The industry has converged on proven three-step chromatography trains for mAb purification: Protein A affinity capture (to isolate the target antibody from cell culture fluid), intermediate polishing (typically ion-exchange to remove aggregates and remaining impurities), and final polishing (to achieve specification-grade purity and remove residual ligands). These factors have helped the monoclonal antibodies & recombinant proteins production application segment acquire the largest share.

"Based on end user, the pharma and biopharma companies segment accounted for the largest share in 2025."

By end user, the preparative and process chromatography market is categorized into pharma & biopharma companies, food & nutraceutical companies, research & academia, and other end users. Pharma & biopharma companies held the largest share in 2024. Integrated pharmaceutical and biopharmaceutical manufacturers represent the anchor customer base for preparative and process chromatography, driven by their need to produce large-scale commercial biologics with consistent quality, high yield, and regulatory compliance. These organizations operate dedicated downstream facilities optimized for mAb, recombinant protein, and vaccine purification, requiring a continuous supply of resins, columns, systems, and technical support. Large pharma companies maintain in-house process development and manufacturing expertise and invest heavily in advanced chromatography platforms. The stability and scale of these operations, combined with their strict quality and regulatory requirements, make them a key end user segment with significant demand. These factors have helped them acquire the largest share.

"North America is expected to hold a significant share in the preparative and process chromatography market throughout the forecast period."

The preparative and process chromatography market comprises five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, North America held a significant share of the market for preparative and process chromatography products. Its dominant position stems from increased manufacturing capacity focused on both commercial-scale and clinical-trial supply production. Investment trends indicate that US federal and state support promotes domestic biomanufacturing for pandemic preparedness and to reduce reliance on international supply chains. Small- to mid-sized biotech firms are increasingly partnering with CDMOs. These factors helped North America secure the largest market share in 2025.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (45%), and Tier 3 (20%)

- By Designation: C-level Executives (35%), Directors (25%), and Others (40%)

- By Region: North America (40%), Europe (30%), Asia Pacific (20%), Latin America (5%), and the Middle East & Africa (5%)

The key players profiled in the preparative and process chromatography market are Danaher Corporation (US), Repligen Corporation (US), Merck KGaA (Germany), Thermo Fisher Scientific (US), Agilent Technologies, Inc. (US), Bio-Rad Laboratories, Inc. (US), Avantor, Inc. (US), Sartorius AG (Germany), Shimadzu Corporation (Japan), Ecolab Inc. (US), Tosoh Bioscience (Japan), Mitsubishi Chemical Group Corporation (Japan), Revvity (US), PerkinElmer (US), Cecil Instruments Limited (UK), W.R. Grace & Co. (US), Ecom SPO (Czech Republic), BUCHI Labortechnik AG (Switzerland), Good Science (Tianjin) Instrument Technologies Co., Ltd. (China), Bio Works Technologies (Sweden), Sykam GmbH (Germany), Sunresin New Materials Co., Ltd. (China), YMC Co., Ltd. (Japan), and Geno Technology Inc. (US)

Research Coverage

The research report analyzes the preparative and process chromatography market by product, application, end user, and region. It examines the factors driving market growth, the challenges and opportunities across industries, and the competitive landscape, including market leaders and small- to medium-sized enterprises. It also estimates revenue for different market segments across five regions and includes a micromarket analysis.

Reasons to Buy the Report

The report will help market leaders and new entrants by providing accurate revenue estimates for the entire preparative and process chromatography market and its subsegments. It will help stakeholders understand the competitive landscape, enabling them to position their businesses more effectively and develop suitable go-to-market strategies. Additionally, the report offers insights into market dynamics, including key drivers, restraints, challenges, and opportunities.

This report provides insightful data on the following.

- Market Penetration: In-depth coverage of product portfolios offered by the top players in the preparative and process chromatography market

- Product Development/Innovation: In-depth coverage of product portfolios offered by the top players in the preparative and process chromatography market

- Market Development: Insightful data on profitable developing areas

- Market Diversification: Details about recent developments and advancements in the preparative and process chromatography market

- Competitive Assessment: Extensive assessment of the products, growth tactics, revenue projections, and market categories of the top competitors

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET OVERVIEW

- 3.2 ASIA PACIFIC PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET, BY END USER AND COUNTRY

- 3.3 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased demand for complex biologics and advanced therapeutic modalities

- 4.2.1.2 Increased outsourcing to CDMOs

- 4.2.1.3 Technological advancements in chromatography media and systems

- 4.2.1.4 Need for cost optimization in downstream processing

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lowered replacement rate due to incomplete single-use adoption

- 4.2.2.2 Limited resin lifetime and performance degradation

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Ongoing investments in bioprocessing capacity and analytical capabilities

- 4.2.3.2 Expansion of integrated, intensified, and continuous chromatography columns

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of skilled chromatography professionals

- 4.2.4.2 High capital and operating costs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER1/2/3 PLAYERS

- 4.5.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF BUYERS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL BIOPROCESS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 PROMINENT COMPANIES

- 5.3.2 SMALL & MEDIUM-SIZED ENTERPRISES

- 5.3.3 END USERS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.4.2 RAW MATERIAL PROCUREMENT

- 5.4.3 MANUFACTURING

- 5.4.4 DISTRIBUTION, MARKETING & SALES, AND POST-SALES SERVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF PREPARATIVE AND PROCESS CHROMATOGRAPHY PRODUCTS, BY KEY PLAYER, 2025

- 5.6.2 AVERAGE SELLING PRICE OF PREPARATIVE AND PROCESS CHROMATOGRAPHY PRODUCTS, BY REGION, 2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 902720)

- 5.7.2 EXPORT DATA (HS CODE 902720)

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFFS ON PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRY/REGION

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 RECOMBINANT PROTEIN A LIGAND ENGINEERING

- 6.1.2 ALKALINE-STABLE LIGAND DEVELOPMENT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED COLUMN PACKING SYSTEMS

- 6.2.2 IN-LINE MONITORING AND PAT (PROCESS ANALYTICAL TECHNOLOGY)

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CONTINUOUS CHROMATOGRAPHY SYSTEMS

- 6.3.2 AFFINITY MEMBRANE TECHNOLOGY

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI ON PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

- 6.5.1 TOP USE CASES & MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

- 6.5.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PREPARATIVE AND PROCESS CHROMATOGRAPHY

- 6.6 SUCCESS STORIES & REAL-WORLD APPLICATIONS

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE & SUSTAINABILITY INITIATIVES

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY TRENDS

- 7.1.2.1 North America

- 7.1.2.1.1 US

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Rest of the World

- 7.1.2.1 North America

- 7.2 INDUSTRY STANDARDS

- 7.2.1 SUSTAINABILITY INITIATIVES

- 7.2.2 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING EVALUATION CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 PROCESS CHROMATOGRAPHY PRODUCTS

- 9.2.1 CHEMICALS & REAGENTS

- 9.2.1.1 Recurring consumption to drive demand for chemicals & reagents

- 9.2.2 RESINS

- 9.2.2.1 Increased purification volume to drive demand for resins

- 9.2.3 COLUMNS

- 9.2.3.1 Reproducible results and low cross-contamination risk to drive demand for columns in process chromatography operations

- 9.2.4 SYSTEMS

- 9.2.4.1 Less changeover time and maintenance needs to boost demand for single-use chromatography systems

- 9.2.5 AFTER-MARKET SERVICES

- 9.2.5.1 Capacity expansions and routine calibration needs to drive market growth

- 9.2.1 CHEMICALS & REAGENTS

- 9.3 PREPARATIVE CHROMATOGRAPHY PRODUCTS

- 9.3.1 CHEMICALS & REAGENTS

- 9.3.1.1 Method development focus and high-purity results to drive market for reagents in preparative operations

- 9.3.2 RESINS

- 9.3.2.1 Cost-effective supply chain metrics to drive demand for bulk resins

- 9.3.3 COLUMNS

- 9.3.3.1 Flexibility, low sample consumption, and high throughput to drive adoption

- 9.3.4 SYSTEMS

- 9.3.4.1 Biologics innovation and strong mAb pipeline to support demand for systems

- 9.3.5 AFTER-MARKET SERVICES

- 9.3.5.1 Consultative and technical services to drive demand for after-market services

- 9.3.1 CHEMICALS & REAGENTS

10 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 MONOCLONAL ANTIBODIES & RECOMBINANT PROTEINS

- 10.2.1 SHIFT TOWARDS MORE COST-EFFECTIVE OPTIONS TO OPEN NEW REVENUE CHANNELS

- 10.3 VACCINES

- 10.3.1 WIDE APPLICATION BASE OF STANDARDIZED CHROMATOGRAPHY TECHNIQUES IN VACCINE MANUFACTURING TO DRIVE MARKET GROWTH

- 10.4 PEPTIDES & OLIGONUCLEOTIDES

- 10.4.1 SHIFT TOWARDS HYBRID SYNTHESIS TO DRIVE MARKET GROWTH

- 10.5 CELL & GENE THERAPIES

- 10.5.1 LOWER TARGET PRODUCT YIELD TO HAMPER GROWTH OF CHROMATOGRAPHY AS PRIMARY TECHNIQUE

- 10.6 OTHER APPLICATIONS

11 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 11.2.1 EXTENSIVE USE IN BIOLOGICAL DRUG PRODUCTION TO ENSURE STRONG DEMAND

- 11.3 FOOD & NUTRACEUTICAL COMPANIES

- 11.3.1 EXPANDING USE CASES IN NUTRACEUTICAL INDUSTRY TO BOOST MARKET GROWTH

- 11.4 RESEARCH & ACADEMIC INSTITUTES

- 11.4.1 INCREASING R&D IN DRUG DISCOVERY TO DRIVE USE OF CHROMATOGRAPHY

- 11.5 OTHER END USERS

12 PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 Expansion in biomanufacturing and domestic capacity to drive market

- 12.2.3 CANADA

- 12.2.3.1 Policy-led capacity build and CDMO growth to drive market

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Capacity expansion in end-use facilities to generate new demand channels for target products

- 12.3.3 UK

- 12.3.3.1 Government policies and public-private partnerships to drive market

- 12.3.4 FRANCE

- 12.3.4.1 Demand-side developments to add new revenue channels for chromatography OEMs and suppliers

- 12.3.5 ITALY

- 12.3.5.1 Increased CAPEX from major end-user categories to fuel demand for target products

- 12.3.6 SPAIN

- 12.3.6.1 Increased number of CDMOs and CROs to propel demand for chromatography and related products

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 JAPAN

- 12.4.2.1 CDMO capacity expansions, policy backing, and CDMO investments to propel market

- 12.4.3 CHINA

- 12.4.3.1 Robust biopharmaceutical expansion to support demand

- 12.4.4 INDIA

- 12.4.4.1 Growth of pharma and biotech industries to drive demand for preparative and process chromatography

- 12.4.5 AUSTRALIA

- 12.4.5.1 Increasing demand for protein-based therapeutics to drive growth

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Developments in biopharmaceutical sector to drive market growth

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Biomanufacturing emphasis and public-private partnerships to catalyze demand

- 12.5.3 MEXICO

- 12.5.3.1 Supportive government initiatives to boost demand for preparative and process chromatography products

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Favorable government policies to propel market growth

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PREPARATIVE AND PROCESS CHROMATOGRAPHY MARKET

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 MARKET RANKING OF KEY PLAYERS, 2025

- 13.5 COMPANY VALUATION & FINANCIAL METRICS

- 13.5.1 FINANCIAL METRICS

- 13.5.2 COMPANY VALUATION

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Product type footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 End-user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 DANAHER

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 THERMO FISHER SCIENTIFIC INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 MERCK KGAA

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.3.2 Expansions

- 14.1.3.3.3 Other developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 SARTORIUS AG

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 WATERS CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 AGILENT TECHNOLOGIES, INC.

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.6.3.3 Expansions

- 14.1.7 AVANTOR, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.8 BIO-RAD LABORATORIES, INC.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.9 REPLIGEN CORPORATION

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches

- 14.1.9.3.2 Deals

- 14.1.10 SHIMADZU CORPORATION

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 ECOLAB INC.

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Expansions

- 14.1.12 TOSOH BIOSCIENCE

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Expansions

- 14.1.1 DANAHER

- 14.2 OTHER PLAYERS

- 14.2.1 MITSUBISHI CHEMICAL CORPORATION

- 14.2.2 REVVITY

- 14.2.3 PERKINELMER

- 14.2.4 CECIL INSTRUMENTS LIMITED

- 14.2.5 W. R. GRACE & CO.-CONN

- 14.2.6 ECOM SPOL. S R.O

- 14.2.7 BUCHI LABORTECHNIK AG

- 14.2.8 GOOD SCIENCE (TIANJIN) INSTRUMENT TECHNOLOGIES CO., LTD.

- 14.2.9 BIO WORKS TECHNOLOGIES

- 14.2.10 SYKAM GMBH

- 14.2.11 SUNRESIN NEW MATERIALS CO. LTD.

- 14.2.12 YMC CO., LTD.

- 14.2.13 GENO TECHNOLOGY INC.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY RESEARCH

- 15.1.1.1 Key secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.1.3 Objectives of secondary research

- 15.1.2 PRIMARY RESEARCH

- 15.1.2.1 Key primary sources

- 15.1.2.2 Key supply- and demand-side participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Objectives of primary research

- 15.1.2.5 Key primary insights

- 15.1.1 SECONDARY RESEARCH

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.1.1 Company revenue estimation

- 15.2.1.2 Customer-based market estimation

- 15.2.1.3 Primary interviews

- 15.2.2 TOP-DOWN APPROACH

- 15.2.1 BOTTOM-UP APPROACH

- 15.3 GROWTH RATE ASSUMPTIONS

- 15.4 DATA TRIANGULATION

- 15.5 STUDY ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS