|

시장보고서

상품코드

1956050

그래프트 폴리올레핀 시장 : 유형별, 가공 기술별, 용도별, 최종 이용 산업별, 지역별 - 세계 예측(-2030년)Grafted Polyolefins Market by Type (Maleic Anhydride Grafted PE, PP, EVA), Application (Adhesion Promotion, Compatibilization), End-use Industry (Automotive, Packaging, Construction), Processing Technology, Region - Global Forecast to 2030 |

||||||

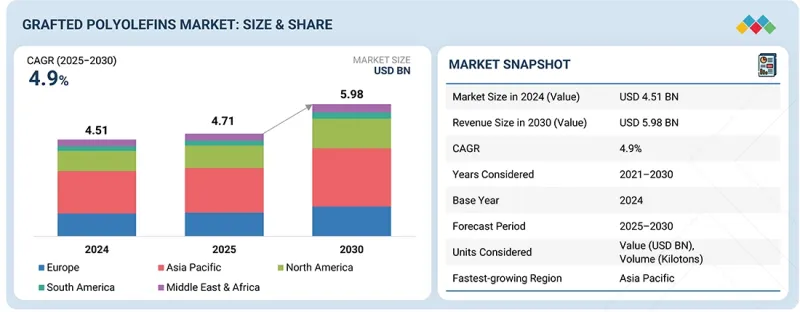

그래프트 폴리올레핀 시장 규모는 2025년 47억 1,000만 달러에서 2030년까지 59억 8,000만 달러로 성장하여 예측 기간 동안 CAGR 4.9%를 기록할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(100만/10억 달러), 킬로톤 |

| 부문 | 유형별, 가공 기술별, 용도별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

자동차, 포장, 건설 분야에서의 다재료 적합성 및 접착 성능에 대한 수요가 그래프트 폴리올레핀 시장의 성장을 주도하고 있습니다. 폴리머 블렌드, 복합재료, 재생 플라스틱을 채택하는 기업이 늘어나는 가운데, 효과적인 상용화제로서 그래프트 폴리올레핀이 주목받고 있습니다. 자동차 분야의 경량화 노력과 다층 포장 시스템의 개발은 이 시장의 성장을 지속적으로 뒷받침하고 있습니다. 새로운 제도가 지속가능성과 재활용성을 중시하는 가운데, 금속이나 용매 대체 방식을 사용하지 않고 성능을 향상시키기 위해 기능성 폴리올레핀의 채택이 증가하고 있습니다. 반응성 압출 및 컴파운딩 공정과 같은 새로운 기술은 비용 효율성과 용도의 다양성을 높이고 있습니다.

그래프트 폴리올레핀 시장에서 가장 큰 비중을 차지하는 유형은 무수말레인산 그래프트 폴리에틸렌입니다. 저비용, 높은 범용성, 가공의 용이성 등 다양한 특징으로 인해 가장 널리 사용되는 그래프트 폴리올레핀입니다. 무수말레산 그래프트 폴리에틸렌은 극성 기판에 대한 우수한 접착력과 상용성을 가지면서도 폴리에틸렌에 비해 넓은 유연성 범위와 내화학성을 유지합니다. 이 때문에 무수말레인산 그라프트 폴리에틸렌은 다층 포장 필름, 파이프, 케이블, 재생 폴리머 블렌드 등 대량 생산 응용 분야에서 타이제 또는 상용화제로 자주 사용됩니다. 그래프트 폴리에틸렌은 포장 및 건설 산업의 높은 수요, 폴리에틸렌 원료의 풍부함, 확장 가능한 압출 기반 그래프트화 기술을 통한 제조 가능성으로 인해 그래프트 폴리에틸렌은 여전히 그래프트 폴리올레핀의 주류 유형입니다.

그래프트 폴리올레핀 시장의 가장 큰 최종 사용 산업 중 하나는 자동차 산업입니다. 동 산업에서는 복합재료를 이용한 경량화 및 다양한 용도의 다양한 소재 사용이 강조되고 있기 때문입니다. 따라서 그래프트 폴리올레핀은 호환제(다양한 종류의 폴리머 재료와의 호환제)로서 폴리머 가공 및 기계 구조물 내의 혼합 재료 구성에서 접착력 강화 및 밀착력 향상에 폭넓게 활용되고 있습니다. 이질적인 재료의 혼합물에 대해 우수한 접착 특성 및 접착력을 제공하기 때문입니다. 이를 통해 자동차 내 금속 부품을 대체하는 복합재료 구성의 기계적 강도, 내충격성, 열 안정성이 획기적으로 향상됩니다. 자동차 내장, 외장, 엔진룸 내부 용도에 대량으로 사용되는 플라스틱 부품과 더불어 정부의 연비 기준 및 배기가스 규제, 차량/엔진 성능 전반에 대한 요구사항으로 인해 자동차 제조용 그래프트 폴리올레핀에 대한 수요가 증가하고 있습니다.

아시아태평양은 거대한 제조 능력, 발전하는 산업 구조, 자동차, 포장, 건설, 소비재 등 다양한 산업에서 플라스틱을 많이 사용함에 따라 그라프티드 폴리올레핀의 가장 크고 빠르게 성장하는 지역 시장입니다. 또한, 폴리올레핀의 대규모 생산과 더불어 비용 효율적인 압출 및 컴파운딩 설비와 원료의 가용성이 이 지역의 성장을 지속적으로 견인하고 있습니다. 자동차 생산 증가, 유연 포장에 대한 수요 증가, 폴리머 블렌드 및 재생 플라스틱의 사용 증가도 이 시장의 성장을 뒷받침하고 있습니다. 첨단 고분자 가공 기술에 대한 투자 증가, 개발도상국의 수출 확대, 수출 지향적 환경을 촉진하는 정부의 제조 지원 정책으로 인해 그래프트 폴리올레핀의 시장 성장이 크게 증가했습니다.

그래프트 폴리올레핀 시장에는 Mitsubishi Chemical Group Corporation(일본),Guangzhou Lushan New Materials(중국),LyondellBasell Industries Holdings B.V.(미국), Mitsui Chemicals Asia Pacific, Ltd. Mitsui Chemicals Asia Pacific, Ltd.(일본), Arkema(프랑스), Clariant(스위스), Borealis AG(오스트리아), SI Group, Inc. Limited(중국) 등 주요 기업들이 진출해 있습니다. 세계 그래프트 폴리올레핀 시장의 주요 기업들에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시하였습니다.

조사 범위

이 보고서는 유형, 가공 기술, 최종 사용 산업, 용도, 지역별로 그래프트 폴리올레핀 시장을 세분화하여 각 지역의 전체 시장 가치 예측을 제공합니다. 주요 업계 진출기업에 대한 상세한 분석을 실시하여 그래프트 폴리올레핀 시장과 관련된 사업 개요, 제품 및 서비스, 주요 전략, 사업 확장에 대한 인사이트를 제공합니다.

본 보고서 구매의 주요 이점

이 보고서는 산업 분석(업계 동향), 주요 기업의 시장 순위 분석, 기업 개요 등 다양한 수준의 분석에 초점을 맞추고 있으며, 이를 종합하여 경쟁 상황, 그래프트 폴리올레핀 시장의 신흥 및 고성장 부문, 고성장 지역, 시장 촉진요인, 억제요인, 기회, 과제에 대한 종합적인 시각을 제공합니다. 기회 및 과제에 대한 종합적인 견해를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 성장 촉진요인 분석 : (폴리머 블렌드 및 복합재료의 성능 향상, 포장 접착력 및 자동차 경량화 지원, 재활용 호환성 및 재활용 재료 성능 개선), 억제요인(재료 비용 프리미엄 및 배합 복잡성 관리), 기회(혼합 폐기물 재활용 호환제의 성장 포착), 도전 과제(그래프트 수준과 용융 가공의 균형) 성의 균형)이 그래프트 폴리올레핀 시장 성장에 미치는 영향.

- 시장 침투 현황 : 세계 그래프트 폴리올레핀 시장의 주요 기업이 제공하는 그래프트 폴리올레핀에 대한 종합적인 정보를 제공합니다.

- 제품 개발/혁신 : 그래프트 폴리올레핀 시장의 향후 기술 동향, 제품 출시, 사업 확장, 인수합병에 대한 상세한 분석.

- 시장 개발 : 수익성 높은 신흥 시장에 대한 종합적인 정보. 본 보고서에서는 지역별 그래프트 폴리올레핀 시장 동향을 분석하고 있습니다.

- 시장 용량 : 각 사의 생산능력을 가용한 범위 내에서 제시하고, 향후 그래프트 폴리올레핀 시장에서의 생산능력 확대 계획도 언급합니다.

- 경쟁 평가 : 그래프트 폴리올레핀 시장에서 주요 기업의 시장 점유율, 전략, 제품, 제조 능력에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 그래프트 폴리올레핀 시장(유형별)

제10장 그래프트 폴리올레핀 시장(가공 기술별)

제11장 그래프트 폴리올레핀 시장(용도별)

제12장 그래프트 폴리올레핀 시장(최종 이용 산업별)

제13장 그래프트 폴리올레핀 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

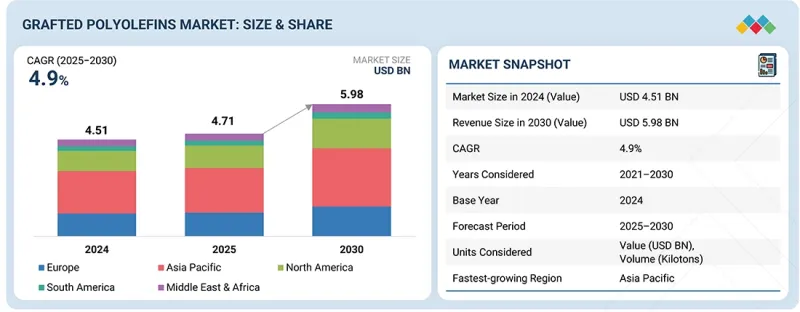

KSM 26.03.19The grafted polyolefins market size is projected to grow from USD 4.71 billion in 2025 to USD 5.98 billion by 2030, registering a CAGR of 4.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Segments | Type, Processing Technology, End-use Industry, Application, and Region |

| Regions covered | Asia Pacific, North America, Europe, the Middle East & Africa, and South America |

The demand for multimaterial compatibility and adhesion performance in the automotive, packaging, and construction sectors drives growth in the grafted polyolefin market. As more companies use polymer blends, composites, and recycled plastics, they are turning to grafted polyolefins as effective compatibilizers. Lightweighting initiatives in the automotive sector and the development of multilayer packaging systems continue to support growth in this market. As new regulations emphasize sustainability and recyclability, functionalized polyolefins are increasingly specified for improved performance without using metal or solvent substitute methods. Newer technologies, such as reactive extrusion and compounding processes, enhance the cost-effectiveness and versatility of applications.

"By type, the maleic anhydride grafted PE segment is anticipated to account for the largest market share during the forecast period (2025-2030)."

The segment of the grafted polyolefin market showing the largest type is maleic anhydride grafted polyethylene, which is the most widely used grafted polyolefin because of a variety of features, including its low cost, high versatility, and ease of working. Maleic anhydride grafted polyethylene has exceptional adhesion and compatibility properties with polar substrates while still maintaining a wide flexibility range as well as chemical resistance as compared to polyethylene. As a result, maleic anhydride grafted polyethylene is often utilized as a tie or compatibilizing agent for high-volume applications such as multilayer packaging films, pipes, cables, and blends of recycled polymers. Grafted polyethylene continues to be the dominant type of grafted polyolefin because of the high levels of demand from the packaging and construction industries, the abundance of polyethylene feedstock, and the ability to produce grafted polyethylene using scalable extrusion-based grafting technologies.

By end-use industry, the automotive segment is anticipated to account for the largest market share during the forecast period (2025-2030)

One of the largest end-use industries for the grafted polyolefin market is automotive, as the industry places a high degree of emphasis on lightweighting (by use of composites) and using many materials in different types of applications. Therefore, grafted polyolefins provide extensive use in the processing of polymers for use as compatibilizers (with many different types of polymer materials) and in bond enhancement or adhesion of mixed material configurations within mechanical structures, by providing the improved bonding characteristics/adhesion properties to the mix of dissimilar materials. This dramatically increases the mechanical strength, impact resistance, and thermal stability of multiple material configurations used to replace metal components within an automobile. Due to the high volume of plastic components used for interiors, exteriors, and for "under the hood" applications, along with the government's fuel economy standards/requirements regarding air emissions and general vehicle/engine performance, there is a high demand for grafted polyolefins for automotive manufacturing in large quantities and with increased frequency.

"Asia Pacific is anticipated to account for the largest market share during the forecast period (2025-2030).

Due to Asia Pacific's considerable manufacturing capacity, developing industrial structure, and heavy use of plastics in multiple industries such as automotive, packaging, construction, and consumer goods, Asia Pacific is the largest and fastest-growing regional market for grafted polyolefins. In addition, large-scale production of polyolefins coupled with cost-effective extrusion and compounding facilities and availability of raw materials continue to drive growth in this region. Increasing vehicle production, growing demand for flexible packaging, and increasing use of polymer blends and recycled plastics also support the growth of this market. As a result of the increased investment in advanced polymer processing technologies, as well as increased exports from developing countries and supporting governmental policies for manufacturing in favor of export-oriented environments, there has been a substantial increase in the market growth of grafted polyolefins.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the grafted polyolefins market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers - 15%, Directors - 20%, and Others - 65%

- By Region: North America - 30%, Europe - 25%, Asia Pacific - 35%, the Middle East & Africa - 5%, and South America - 5%

The grafted polyolefins market comprises of major companies like Mitsubishi Chemical Group Corporation (Japan), Guangzhou Lushan New Materials Co., Ltd. (China), LyondellBasell Industries Holdings B.V.(US), Mitsui Chemicals Asia Pacific, Ltd. (Japan), Arkema (France), Clariant (Switzerland), Borealis AG (Austria), SI Group, Inc. (US), Dow (US), and COACE Chemical Company Limited (China). The study includes in-depth competitive analysis of these key players in the grafted polyolefins market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for grafted polyolefins market on the basis of type, processing technology, end-use industry, application, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the grafted polyolefins market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the grafted polyolefins market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of drivers: (Enabling performance improvement in polymer blends and composites, supporting packaging adhesion and automotive lightweighting, improving recycling compatibility and circular material performance), restraints (Managing material cost premium and formulation complexity), opportunities (Capturing growth in mixed waste recycling compatibilizers), and challenges (Balancing graft level with melt processability) influencing the growth of grafted polyolefins market.

- Market Penetration: Comprehensive information on the grafted polyolefins offered by top players in the global grafted polyolefins market.

- Product Development/Innovation: Detailed insights on upcoming technologies, product launches, expansions, and acquisitions in the grafted polyolefins market.

- Market Development: Comprehensive information about lucrative emerging markets, the report analyzes the markets for grafted polyolefins market across regions.

- Market Capacity: Production capacity of the companies is provided wherever available, with upcoming capacities for the grafted polyolefins market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the grafted polyolefins market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GRAFTED POLYOLEFINS MARKET

- 3.2 GRAFTED POLYOLEFINS MARKET, BY TYPE AND REGION

- 3.3 GRAFTED POLYOLEFINS MARKET, BY PROCESSING TECHNOLOGY

- 3.4 GRAFTED POLYOLEFINS MARKET, BY APPLICATION

- 3.5 GRAFTED POLYOLEFINS MARKET, BY END-USE INDUSTRY

- 3.6 GRAFTED POLYOLEFINS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Need for performance improvement in polymer blends and composites

- 4.2.1.2 Supporting packaging adhesion and automotive lightweighting

- 4.2.1.3 Improving recycling compatibility and circular material performance

- 4.2.1.4 Growth in polymer processing industries

- 4.2.2 RESTRAINTS

- 4.2.2.1 Cost sensitivity and perceived formulation complexity

- 4.2.2.2 Raw material price volatility and competitive substitution pressure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid expansion of mixed plastic recycling

- 4.2.3.2 Demand for advanced automotive polymer systems in EVs

- 4.2.3.3 Development of bio-based monomers and sustainability branding

- 4.2.3.4 Expansion into niche, high-margin markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Optimizing functional performance without sacrificing melt processability

- 4.2.4.2 Ensuring consistent performance across variable recycled feedstock streams

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN GRAFTED POLYOLEFINS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.4.2 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.4.3 AVERAGE SELLING PRICE TREND, BY PROCESSING TECHNOLOGY

- 5.4.4 AVERAGE SELLING PRICE TREND, BY END-USE INDUSTRY

- 5.4.5 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 390230)

- 5.6.2 EXPORT SCENARIO (HS CODE 390230)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ADVANCING AUTOMOTIVE LIGHTWEIGHTING THROUGH GRAFTED POLYOLEFIN COMPATIBILIZATION

- 5.10.2 ENABLING HIGH-VALUE RECYCLING THROUGH MIXED PLASTIC WASTE COMPATIBILIZERS

- 5.10.3 EXPANDING HIGH-MARGIN PACKAGING AND ADHESIVES APPLICATIONS

- 5.11 IMPACT OF 2025 US TARIFF - GRAFTED POLYOLEFINS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 REACTIVE EXTRUSION (MELT GRAFTING TECHNOLOGY)

- 6.1.2 SOLUTION GRAFTING TECHNOLOGY

- 6.1.3 SOLID-STATE AND POST-REACTOR GRAFTING

- 6.1.4 ADVANCED COMPATIBILIZATION AND REACTIVE COMPOUNDING FOR RECYCLING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 REACTIVE COMPOUNDING AND MASTERBATCH TECHNOLOGY

- 6.2.2 ADHESIVE AND TIE-LAYER CO-EXTRUSION TECHNOLOGY

- 6.2.3 FIBER REINFORCEMENT AND COMPOSITE PROCESSING TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ADVANCED COMPATIBILIZER ELASTOMERS (FUNCTIONALIZED POE & SEBS SYSTEMS)

- 6.3.2 SURFACE TREATMENT AND PLASMA ACTIVATION TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM ROADMAP (2024-2026): PERFORMANCE OPTIMIZATION AND COST RATIONALIZATION

- 6.4.2 MID-TERM ROADMAP (2026-2029): CUSTOMIZATION, APPLICATION-SPECIFIC GRADES, AND SUSTAINABILITY INTEGRATION

- 6.4.3 LONG-TERM ROADMAP (2029-2035): ADVANCED FUNCTIONALIZATION AND CIRCULAR MATERIAL ENABLEMENT

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 GRANTED PATENTS, 2016-2025

- 6.5.3 PUBLICATION TRENDS FOR LAST TEN YEARS

- 6.5.4 INSIGHTS

- 6.5.5 LEGAL STATUS

- 6.5.6 JURISDICTION ANALYSIS

- 6.5.7 TOP APPLICANTS

- 6.5.8 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 ADVANCED MIXED-PLASTIC RECYCLING & CIRCULAR POLYMER BLENDS

- 6.6.2 ELECTRIC VEHICLE (EV) STRUCTURAL AND BATTERY-ADJACENT POLYMER SYSTEMS

- 6.6.3 HIGH-PERFORMANCE SUSTAINABLE PACKAGING & BARRIER STRUCTURES

- 6.6.4 SPECIALTY MEDICAL, HEALTHCARE, AND HIGH-BARRIER TECHNICAL APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON GRAFTED POLYOLEFINS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN GRAFTED POLYOLEFINS MANUFACTURING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN GRAFTED POLYOLEFINS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN GRAFTED POLYOLEFINS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 ARKEMA (FRANCE): SPECIALTY POLYOLEFINS & FUNCTIONAL POLYMERS

- 6.8.2 DUPONT (US): ENGINEERED POLYMER SOLUTIONS FOR DEMANDING APPLICATIONS

- 6.8.3 MITSUI CHEMICALS ASIA PACIFIC LTD. (JAPAN): HIGH-VALUE FUNCTIONAL POLYOLEFINS FOR MULTIPLE INDUSTRIES

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GRAFTED POLYOLEFINS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITIBILITY

- 8.5.1 VALUE ADDITION AND FUNCTIONAL PREMIUMS

- 8.5.2 FEEDSTOCK AND COST STRUCTURE SENSITIVITY

- 8.5.3 SCALE, CUSTOMIZATION, AND OPERATING LEVERAGE

- 8.5.4 CUSTOMER LOCK-IN AND SWITCHING COSTS

9 GRAFTED POLYOLEFINS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 MALEIC ANHYDRIDE GRAFTED PE

- 9.2.1 WIDESPREAD APPLICATION IN ADHESIVE AND SEALANT FORMULATIONS TO DRIVE MARKET

- 9.3 MALEIC ANHYDRIDE GRAFTED PP

- 9.3.1 ENHANCED THERMAL STABILITY AND TEMPERATURE RESISTANCE TO BOOST DEMAND

- 9.4 MALEIC ANHYDRIDE GRAFTED EVA

- 9.4.1 RISING USE IN COMPOSITE MATERIALS AND POLYMER BLENDS TO BOOST MARKET

- 9.5 OTHER TYPES

- 9.5.1 MALEIC ANHYDRIDE PET

- 9.5.2 MALEIC ANHYDRIDE PPT

- 9.5.3 MALEIC ANHYDRIDE PS

- 9.5.4 ACRYLIC ACID GRAFTED POLYOLEFINS

10 GRAFTED POLYOLEFINS MARKET, BY PROCESSING TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 EXTRUSION

- 10.2.1 INCREASING DEMAND FOR HIGH-PERFORMANCE PACKAGING SOLUTIONS TO DRIVE MARKET

- 10.3 MELT GRAFTING

- 10.3.1 ENHANCED SIGNAL INTEGRITY AND SYSTEM PERFORMANCE TO BOOST DEMAND

- 10.4 OTHER PROCESSING TECHNOLOGIES

- 10.4.1 EMULSION GRAFTING

- 10.4.2 RADIATION GRAFTING

- 10.4.3 BULK GRAFTING

- 10.4.4 REACTIVE EXTRUSION

11 GRAFTED POLYOLEFINS MARKET, BY APPLICATION

- 11.1 NTRODUCTION

- 11.2 ADHESION PROMOTION

- 11.2.1 PRESSING NEED IN LAMINATES AND BARRIER COATINGS TO DRIVE MARKET

- 11.3 IMPACT MODIFICATION

- 11.3.1 RISING DEMAND FOR TOUGHENING AGENTS TO FUEL MARKET

- 11.4 COMPATIBILIZATION

- 11.4.1 INCREASING USE OF POLYMER BLENDS TO BOOST MARKET GROWTH

- 11.5 BONDING

- 11.5.1 EXTENSIVE USE OF POLYOLEFINS IN PACKAGING INDUSTRY TO DRIVE MARKET

- 11.6 OTHER APPLICATIONS

- 11.6.1 STABILIZATION

- 11.6.2 FLAME RETARDANCY

- 11.6.3 ANTIMICROBIAL PROPERTIES

- 11.6.4 BARRIER PROPERTIES

- 11.6.5 ELECTRICAL CONDUCTIVITY

12 GRAFTED POLYOLEFINS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 AUTOMOTIVE

- 12.2.1 INCREASING DEMAND FOR POLYOLEFINS IN INSULATION AND SOUNDPROOFING TO DRIVE MARKET

- 12.3 PACKAGING

- 12.3.1 RISING DEMAND IN MEDICAL PACKAGING TO DRIVE MARKET

- 12.4 CONSTRUCTION

- 12.4.1 ENHANCED DURABILITY AND THERMAL RESISTANCE TO BOOST DEMAND

- 12.5 TEXTILE

- 12.5.1 HIGH TENSILE STRENGTH AND ABRASION RESISTANCE TO SUPPORT MARKET GROWTH

- 12.6 ADHESIVES & SEALANTS

- 12.6.1 ENHANCED BONDING STRENGTH AND SEALING PROPERTIES TO BOOST DEMAND

- 12.7 OTHER END-USE INDUSTRIES

- 12.7.1 ELECTRICAL & ELECTRONICS

- 12.7.2 MEDICAL & HEALTHCARE

- 12.7.3 RENEWABLE ENERGY

- 12.7.4 MARINE & OFFSHORE

- 12.7.5 AEROSPACE & DEFENSE

13 GRAFTED POLYOLEFINS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Downstream industry growth and materials integration to drive market

- 13.2.2 JAPAN

- 13.2.2.1 Demand from advanced manufacturing and healthcare expansion to support market growth

- 13.2.3 INDIA

- 13.2.3.1 Policy support and end-use industry expansion to drive demand

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Automotive & semiconductor exports growth driving grafted polyolefins demand

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 NORTH AMERICA

- 13.3.1 US

- 13.3.1.1 Strong automotive, packaging, and construction industries fueling market growth

- 13.3.2 CANADA

- 13.3.2.1 Adoption in automotive lightweighting and polymer composites to drive demand

- 13.3.3 MEXICO

- 13.3.3.1 Strong automotive sector and expansion of construction activities to drive demand

- 13.3.1 US

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Growth of automotive and packaging sectors to drive market

- 13.4.2 ITALY

- 13.4.2.1 Established manufacturing and textile sectors to boost market

- 13.4.3 FRANCE

- 13.4.3.1 Expansion of manufacturing sector to fuel demand

- 13.4.4 UK

- 13.4.4.1 Focus on innovation in automotive sector and commitment to circular economy to drive market

- 13.4.5 SPAIN

- 13.4.5.1 Resurgence of automotive industry to drive demand

- 13.4.6 RUSSIA

- 13.4.6.1 Growth of packaging and technical textile industries to drive demand

- 13.4.7 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Rising availability of cheaper raw materials to drive market

- 13.5.1.2 UAE

- 13.5.1.2.1 Rapid urbanization and industrial development to boost market

- 13.5.1.3 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Increasing demand for recycled plastic products to drive market

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 ARGENTINA

- 13.6.1.1 Surge in construction and automotive activities to drive market

- 13.6.2 BRAZIL

- 13.6.2.1 Diverse industrial landscape and sustainable industrial activities to drive market

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 ARGENTINA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS, 2024

- 14.4 REVENUE ANALYSIS

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Type footprint

- 14.5.5.4 Application footprint

- 14.5.5.5 End-use industry footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 BRAND/PRODUCT COMPARISON

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 DEALS

- 14.9.2 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 MITSUBISHI CHEMICAL GROUP CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 MnM view

- 15.1.1.3.1 Key strengths

- 15.1.1.3.2 Strategic choices

- 15.1.1.3.3 Weaknesses and competitive threats

- 15.1.2 GUANGZHOU LUSHAN NEW MATERIALS CO., LTD.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 MnM view

- 15.1.2.3.1 Key strengths

- 15.1.2.3.2 Strategic choices

- 15.1.2.3.3 Weaknesses and competitive threats

- 15.1.3 LYONDELLBASELL INDUSTRIES HOLDINGS B.V.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 MITSUI CHEMICALS ASIA PACIFIC, LTD.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 MnM view

- 15.1.4.3.1 Key strengths

- 15.1.4.3.2 Strategic choices

- 15.1.4.3.3 Weaknesses and competitive threats

- 15.1.5 ARKEMA

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 MnM view

- 15.1.5.3.1 Key strengths

- 15.1.5.3.2 Strategic choices

- 15.1.5.3.3 Weaknesses and competitive threats

- 15.1.6 CLARIANT

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 MnM view

- 15.1.6.3.1 Key Strengths

- 15.1.6.3.2 Strategic choices

- 15.1.6.3.3 Weaknesses and competitive threats

- 15.1.7 BOREALIS GMBH

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.4 MnM view

- 15.1.7.4.1 Key strengths

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 SI GROUP, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 MnM view

- 15.1.8.3.1 Key Strengths

- 15.1.8.3.2 Strategic choices

- 15.1.8.3.3 Weaknesses and competitive threats

- 15.1.9 DOW

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.9.3.1 Key strengths

- 15.1.9.3.2 Strategic choices

- 15.1.9.3.3 Weaknesses and competitive threats

- 15.1.10 COACE CHEMICAL COMPANY LIMITED

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 MnM view

- 15.1.10.3.1 Key strengths

- 15.1.10.3.2 Strategic choices

- 15.1.10.3.3 Weaknesses and competitive threats

- 15.1.1 MITSUBISHI CHEMICAL GROUP CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 SWASTIK INTERCHEM PRIVATE LIMITED

- 15.2.2 THE COMPOUND COMPANY

- 15.2.3 WILL & CO B.V.

- 15.2.4 FAER WAX

- 15.2.5 NAGASE AMERICA LLC

- 15.2.6 PAYESH C-ONE POLYMER

- 15.2.7 WESTLAKE CORPORATION

- 15.2.8 FINE-BLEND POLYMER (SHANGHAI) CO., LTD.

- 15.2.9 SYNTHOMER PLC

- 15.2.10 SACO AEI POLYMERS

- 15.2.11 SHENYANG KETONG PLASTIC CO., LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary interview participants

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 16.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS