|

시장보고서

상품코드

1961003

CAR-T 세포치료 시장 예측(-2031년) : 제품별, 표적별, 적응증별, 인구통계별, 최종사용자별, 지역별CAR T-Cell Therapy Market by Product (Abecma, Breyanzi, Carvykti, Yescarta, Tecartus), Target (CD19, BCMA), Indication (Multiple Myeloma, Leukemia, Lymphoma), Demographic (Adult, Pediatric), Region, Competitive Landscape - Global Forecast to 2031 |

||||||

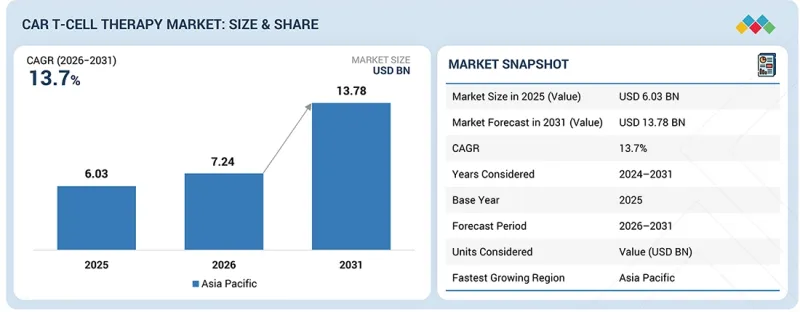

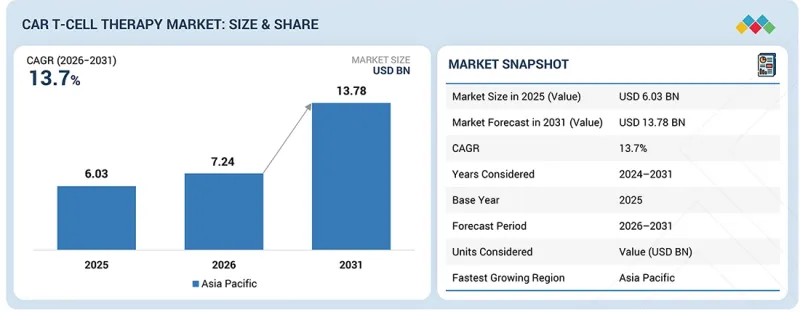

세계의 CAR T 세포치료 시장 규모는 2026년 72억 4,000만 달러에서 2031년에는 137억 8,000만 달러에 달할 것으로 예측되고 있으며, CAGR은 13.7%로 전망되고 있습니다.

시장 성장의 주요 요인은 전 세계 암 발병률 증가입니다. CAR T 세포 치료제의 기술 발전과 치료제 개발에 대한 투자 및 자금 조달 증가가 시장 성장을 가속할 가능성이 높을 것으로 보입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 표적별, 적응증별, 인구통계별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

그러나 CAR T 세포 치료의 부작용과 높은 치료비는 예측 기간 중 시장 성장을 저해하는 주요 요인 중 하나가 될 것으로 예측됩니다.

제품별로는 CAR T세포치료제 시장은 크게 아벡마(이데카부타진 비클레어셀), 브레이얀지(리소카부타진 말라웨어셀), 칼빅티(실타카부타진 오토로이셀), 예스카타(악티카부타진 실로이셀), 테카르타스(브렉사부타진 오토로이셀), 김리아(티사겐 레클레어셀), 기타 제품 등으로 나뉩니다. 테카르타스(브렉사부타진 오토로이셀), 킴리아(티사겐 레클레어셀), 기타 제품으로 크게 분류됩니다.

2025년에는 예스카르타 부문이 가장 큰 시장 점유율을 차지했습니다. 재발/불응성 암 치료에서 예스카르타의 높은 반응률과 지속적인 관해율로 인해 시장 성장이 견인되고 있으며, 이는 치료법 채택 증가로 이어지고 있습니다.

최종사용자별로 세계 CAR T 세포 치료 시장은 병원, 장기 요양 시설, 전문 치료 센터로 구분됩니다. 2025년에는 병원 부문이 세계 CAR T 세포 치료 시장의 주요 촉진요인으로 부상하여 예측 기간 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다.

병원에서는 CAR T 세포 치료를 표준 종양 치료 프로토콜에 통합하고 있습니다. 이러한 추세에 따라 더 많은 병원들이 CAR T 세포 치료를 채택함에 따라 그 수요가 증가하고 있습니다. 또한 병원은 CAR T 세포 치료의 임상시험을 촉진하는 데 중요한 역할을 하고 있습니다. 연구 구상에 적극적으로 참여하고 제약사 및 병원과의 협력을 통해 근거기반을 확대하고 규제당국의 승인을 가속화할 수 있습니다. 이는 시장 성장을 더욱 촉진하는 요인이 될 것입니다.

CAR T 세포 치료 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분됩니다. 예측 기간 중 아시아태평양이 가장 높은 CAGR로 성장할 것으로 예측됩니다. 지원적인 규제 프레임워크, 풍부한 CAR-T 세포치료제 파이프라인, 신속한 승인 절차가 혁신적인 치료제 시장 진입을 촉진하고 아시아태평양의 성장을 촉진할 것입니다. 또한 중국내 병원, 대학, 산업계 간의 협력 강화는 견고한 시장 성장을 가속할 것으로 예측됩니다. 중국에서 다양한 암종을 대상으로 CAR T세포 치료의 안전성과 유효성을 평가하는 임상시험이 빠르게 증가하고 있는 것도 주목할 만한 진전을 보이고 있습니다. 이 연구들은 백혈병, 림프종, 고형암 치료에서 유망한 결과를 보여주었으며, 특정 환자군에서 완전관해율과 지속적 반응률을 크게 증가시켰습니다. 이러한 추세는 아시아태평양이 CAR T 세포 치료제의 개발 및 검증에 있으며, 진전을 이루며 암 치료 성과 향상에 중요한 역할을 하는 지역으로 자리매김하고 있음을 보여줍니다.

이 보고서에서 다룬 기업 개요 리스트:

- Bristol-Myers Squibb Company(미국)

- Gilead Sciences Inc.(미국)

- Novartis AG(스위스)

- Johnson & Johnson(미국)

- CARsgen Therapeutics Holdings Limited(중국)

- IASO Biotherapeutics(중국)

- JW(Cayman) Therapeutics(중국)

- ImmunoAct(India)

- CRISPR Therapeutics(스위스)

- Autolus Therapeutics(영국)

- Allogene Therapeutics(미국)

- Cartesian Therapeutics Inc.(미국)

- Guangzhou Bio-gene Technology(중국)

- Wugen(미국)

이 보고서 구매의 주요 이점:

이 보고서는 전체 CAR-T 세포치료제 시장과 그 하위 부문의 매출에 대한 가장 정확한 예측치를 제공함으로써 시장 리더와 신규 시장 진출기업을 지원합니다. 또한 이해관계자들이 경쟁 구도를 더 깊이 이해하고, 비즈니스를 더 효과적으로 포지셔닝하고, 적절한 시장 진출 전략을 수립할 수 있는 인사이트을 얻을 수 있도록 돕습니다. 이 보고서를 통해 이해관계자들은 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 기회 및 과제에 대한 정보를 얻을 수 있습니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

주요 촉진요인(CAR-T 세포치료제의 기술 발전, 혈액암에서 강력한 효능 신호에 따른 적응증 확대, 치료법 개발에 대한 투자 증가), 제약 요인(높은 비용과 상환 문제), 기회(혈액암에서 고형암 및 새로운 질병 영역으로 확대, 동종 CAR-T 및 CAR-NK로의 초점 전환), 그리고 과제(장기 안전성 모니터링 및 진화하는 적응증 요건)가 CAR T 세포치료제 시장의 성장에 영향을 미치고 있습니다.

- 제품 개발 및 혁신 : CAR T세포치료제 시장의 신제품 출시에 대한 상세한 분석.

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 CAR T 세포 치료제 시장을 분석합니다.

- 시장 다각화 : CAR T 세포치료제 시장의 신제품, 미개발 지역, 최근 동향, 투자에 대한 종합적인 정보.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 CAR-T 세포치료 시장(제품별)

제10장 CAR-T 세포치료 시장(표적별)

제11장 CAR-T 세포치료 시장(적응증별)

제12장 CAR-T 세포치료 시장(인구통계별)

제13장 CAR-T 세포치료 시장(최종사용자별)

제14장 CAR-T 세포치료 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSA 26.03.20The global CAR T-cell therapy market is projected to reach USD 13.78 billion in 2031 from USD 7.24 billion in 2026, at a CAGR of 13.7%. Market growth is primarily driven by rising global cancer prevalence. Technological advancements in CAR T-cell therapies and rising investment and funding for therapy development are likely to propel market growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product | By Target | By Indication | By Demographic | By End user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

However, adverse effects associated with CAR T-cell therapy and high treatment costs are among the major factors expected to restrain market growth during the forecast period.

"The Yescarta product segment accounted for the largest share by product in the CAR T-cell therapy market in 2025."

Based on product, the CAR T-cell therapy market is broadly segmented into Abecma (idecabtagene vicleucel), Breyanzi (lisocabtagene maraleucel), Carvykti (ciltacabtagene autoleucel), Yescarta (axicabtagene ciloleucel), Tecartus (brexucabtagene autoleucel), Kymriah (tisagenlecleucel), and other products.

The Yescarta segment held the largest market share in 2025. Market growth is driven by high response rates and durable remissions with Yescarta in treating relapsed/refractory cancers, leading to increased therapy adoption.

"The hospitals segment accounted for the largest share by end user segment in the CAR T-cell therapy market in 2025."

Based on end users, the global CAR T-cell therapy market is segmented into hospitals, long-term care facilities, and specialty centers. In 2025, the hospitals segment emerged as the primary growth driver in the global CAR T-cell therapy market, with the highest CAGR during the forecast period.

Hospitals are incorporating CAR T-cell therapies into their standard oncology treatment protocols. This trend is boosting demand for CAR T-cell therapies as more hospitals embrace them. Furthermore, hospitals play a key role in facilitating clinical trials for CAR T-cell therapies. By actively participating in research initiatives and collaborating with pharmaceutical companies and hospitals, the evidence base expands, and regulatory approvals accelerate, which, in turn, stimulate market growth.

"Asia Pacific is projected to grow at the highest CAGR in the CAR T-cell therapy market from 2026 to 2031."

The CAR T-cell therapy market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. During the forecast period, Asia Pacific is estimated to grow at the highest CAGR. The supportive regulatory frameworks, rich CAR T-cell therapy product pipeline, and expedited approval processes facilitate quicker market entry for innovative therapies, driving growth in Asia Pacific. In addition, increased collaborations among hospitals, universities, and industries in China are expected to drive robust market growth. The rapid increase in clinical trials evaluating the safety and effectiveness of CAR T-cell therapy across diverse cancer types in China also signals significant advancements. These studies have demonstrated encouraging results in treating leukemia, lymphoma, and solid tumors, with specific patient cohorts showing substantial rates of complete remission and sustained responses. This trend highlights Asia Pacific's progress in developing and validating CAR T-cell therapies, positioning the region as a key player in advancing oncology therapeutic outcomes.

The primary interviews conducted for this report can be categorized as follows:

- By Company Type: Tier 1- 40%, Tier 2- 30%, and Tier 3- 30%

- By Designation: Directors- 20%, Managers- 10%, and Others - 70%,

- By Region: North America -35%, Europe -25%, Asia Pacific -25%, Latin America -10%, and Middle East -5%.

List of Companies Profiled in the Report:

- Bristol-Myers Squibb Company (US)

- Gilead Sciences Inc. (US)

- Novartis AG (Switzerland)

- Johnson & Johnson (US)

- CARsgen Therapeutics Holdings Limited (China)

- IASO Biotherapeutics (China)

- JW (Cayman) Therapeutics Co., Ltd (China)

- ImmunoAct (India)

- CRISPR Therapeutics (Switzerland)

- Autolus Therapeutics (UK)

- Allogene Therapeutics (US)

- Cartesian Therapeutics Inc. (US)

- Guangzhou Bio-gene Technology Co., Ltd (China)

- Wugen (US)

Research Coverage:

This research report categorizes the CAR T-cell therapy market by product (YESCARTA, KYMRIAH, CARVYKTI, ABECMA, TECARTUS, BREYANZI, Other products); by target: CD19, BCMA, other targets; by indication: Multiple myeloma, B-cell lymphoma, Acute lymphoblastic leukemia, Other indications; by demographics: adult, pediatric; by End User: Hospitals, Specialty centers, Long-term care facilities, and by region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa.

The scope of the report covers detailed information regarding the major factors, such as drivers, challenges, opportunities, and restraints, influencing the growth of the CAR T-cell therapy market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, product portfolios, key strategies, such as product launches, collaborations, partnerships, expansions, agreements, and recent developments in the CAR T-cell therapy market. This report provides a competitive analysis of top players and emerging startups in the CAR T-cell therapy market ecosystem.

Key Benefits of Buying the Report:

The report will help market leaders/new entrants by providing the closest approximations of revenue for the overall CAR T-cell therapy market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business more effectively and develop suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

Analysis of key drivers (Technological advancements in CAR T-cell therapies, Label expansions along with strong efficacy signals in hematologic cancers, Growing investments in the development of therapies), restraints (High cost and reimbursement challenges), opportunities (Expanding beyond hematologic malignancies into solid tumors and new disease areas, Focus shift on allogeneic CAR-T and CAR-NK), and challenges (Long-term safety surveillance and evolving labeling requirements) are influencing the growth of CAR T-cell therapy market.

- Product Development/Innovation: Detailed insights on newly launched products of the CAR T-cell therapy market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the CAR T-cell therapy market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the CAR T-cell therapy market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players include Bristol-Myers Squibb Company (US), Gilead Sciences, Inc. (US), Novartis AG (Switzerland), Johnson & Johnson (US), JW (Cayman) Therapeutics Co. Ltd (China), ImmunoAct (India), among others in the CAR T-cell therapy market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 CAR T-CELL THERAPY MARKET OVERVIEW

- 3.2 NORTH AMERICA: CAR T-CELL THERAPY MARKET, BY DEMOGRAPHIC AND COUNTRY, 2025

- 3.3 CAR T-CELL THERAPY MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Technological advancements in CAR T-cell therapies

- 4.2.1.2 Label expansions and strong efficacy signals in hematologic cancers

- 4.2.1.3 Growing investment in CAR T-cell therapy development

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost and reimbursement challenges for CAR T-cell therapy

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding beyond hematologic malignancies into solid tumors and new disease areas

- 4.2.3.2 Focus shift on allogeneic CAR-T and CAR-NK

- 4.2.3.3 Growing collaborations among biopharmaceutical companies, academic institutions, and research organizations

- 4.2.4 CHALLENGES

- 4.2.4.1 Long-term safety surveillance and evolving labeling requirements

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6 PIPELINE ANALYSIS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN GLOBAL CAR-T-CELL THERAPY MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 ROLE IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF CAR T-CELL THERAPY PRODUCTS, BY TYPE, 2025

- 5.5.2 AVERAGE SELLING PRICE OF CAR T-CELL THERAPY PRODUCTS, BY KEY PLAYER, 2025

- 5.5.3 AVERAGE SELLING PRICE OF CAR T-CELL THERAPY PRODUCTS, BY REGION, 2025

- 5.6 KEY CONFERENCES & EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.8 INVESTMENT/FUNDING SCENARIO

- 5.9 IMPACT OF 2025 US TARIFF ON CAR T-CELL THERAPY MARKET

- 5.9.1 KEY TARIFF RATES

- 5.9.2 PRICE IMPACT ANALYSIS

- 5.9.3 IMPACT ON COUNTRY/REGION

- 5.9.3.1 North America

- 5.9.3.1.1 US

- 5.9.3.2 Europe

- 5.9.3.3 Asia Pacific

- 5.9.3.1 North America

- 5.9.4 IMPACT ON END-USE INDUSTRIES

- 5.9.4.1 Hospitals

- 5.9.4.2 Specialty oncology centers

- 5.9.4.3 Long-term care facilities

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Car design and optimization

- 6.1.1.2 Viral vector technology

- 6.1.1.3 Cell culture and expansion techniques

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Gene editing technology (CRISPR-CAS9-based genome editing)

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Monitoring and imaging technologies

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 FUTURE APPLICATIONS

- 6.4 IMPACT OF AI/GEN AI ON CAR T-CELL THERAPY MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.4 REIMBURSEMENT SCENARIO

- 7.5 COMBINATION THERAPIES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 CAR T-CELL THERAPY MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 ABECMA

- 9.2.1 FOCUS ON INCREASED RESEARCH ACTIVITIES FOR INDICATION EXPANSIONS TO DRIVE MARKET

- 9.3 BREYANZI

- 9.3.1 NEED FOR TREATMENT OF MULTIPLE INDICATIONS TO PROPEL MARKET GROWTH

- 9.4 CARVYKTI

- 9.4.1 GLOBAL REACH AND SIGNIFICANT REVENUE GROWTH TO SUPPORT MARKET

- 9.5 YESCARTA

- 9.5.1 FOCUS ON REGULATORY APPROVALS ACROSS MAJOR REGIONS TO BOOST MARKET GROWTH

- 9.6 TECARTUS

- 9.6.1 EFFORTS TO SECURE REIMBURSEMENT AND IMPROVE MARKET ACCESS FACILITATE PATIENT TO AID MARKET ADOPTION

- 9.7 KYMRIAH

- 9.7.1 APPROVAL FOR PEDIATRIC USE TO AUGMENT MARKET GROWTH

- 9.8 OTHER PRODUCTS

10 CAR T-CELL THERAPY MARKET, BY TARGET

- 10.1 INTRODUCTION

- 10.2 CD19

- 10.2.1 RISING INDICATION EXPANSIONS AND NEW APPROVALS TO DRIVE MARKET

- 10.3 BCMA

- 10.3.1 GROWING PIPELINE PRODUCTS TO PROPEL MARKET GROWTH

- 10.4 CD19/20

- 10.4.1 DUAL TARGETING TO OFFER COMPETITIVE ADVANTAGE IN ANTIGEN ESCAPE AND TUMOR HETEROGENEITY ISSUES

- 10.5 CD7

- 10.5.1 ALLOGENEIC CELL SOURCE OF CD7 THERAPIES IN DEVELOPMENT TO SUPPORT GROWTH

- 10.6 OTHER TARGETS

11 CAR T-CELL THERAPY MARKET, BY INDICATION

- 11.1 INTRODUCTION

- 11.2 B-CELL LYMPHOMA (BCL)

- 11.2.1 RISING PREVALENCE OF B-CELL LYMPHOMAS TO PROPEL MARKET GROWTH

- 11.3 MULTIPLE MYELOMA

- 11.3.1 GROWING PRODUCT REVENUE AND RISING GLOBAL INCIDENCE OF MYELOMA TO DRIVE MARKET

- 11.4 ACUTE LYMPHOBLASTIC LEUKEMIA (ALL)

- 11.4.1 EXPANDING R&D PIPELINE TO AUGMENT MARKET GROWTH

- 11.5 OTHER INDICATIONS

12 CAR T-CELL THERAPY MARKET, BY DEMOGRAPHIC

- 12.1 INTRODUCTION

- 12.2 ADULTS

- 12.2.1 GROWING PREVALENCE OF HEMATOLOGIC CANCERS TO DRIVE MARKET

- 12.3 PEDIATRIC

- 12.3.1 HIGH UNMET NEEDS TO LIMIT SEGMENT GROWTH

13 CAR T-CELL THERAPY MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 HOSPITALS

- 13.2.1 GROWING NEED FOR STANDARD ONCOLOGY TREATMENT PROTOCOLS TO DRIVE MARKET

- 13.3 SPECIALTY CENTRES

- 13.3.1 NEED FOR OPTIMAL PATIENT CARE AND SPECIALIZED TREATMENT OPTIONS TO SPUR MARKET GROWTH

- 13.4 LONG-TERM CARE FACILITIES

- 13.4.1 INCREASING INCIDENCE OF CHRONIC DISORDERS AMONG GERIATRIC POPULATION TO PROPEL MARKET GROWTH

14 CAR T-CELL THERAPY MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 US to dominate CAR T-cell therapy market during study period

- 14.2.2 CANADA

- 14.2.2.1 Regulatory approvals and government initiatives for regenerative medicine research to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Key product approvals and focus on clinical research to aid market growth

- 14.3.2 UK

- 14.3.2.1 Technological advancements in automation and presence of robust research infrastructure to spur market growth

- 14.3.3 FRANCE

- 14.3.3.1 Growing focus on cell & gene therapy initiatives to boost market growth

- 14.3.4 ITALY

- 14.3.4.1 Growth in biotech sector to augment market growth

- 14.3.5 SPAIN

- 14.3.5.1 Rising focus on cell therapies and growing focus on stringent regulations to augment market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Rising number of CAR T-cell clinical trials to fuel market growth

- 14.4.2 JAPAN

- 14.4.2.1 Increasing number of product approvals and rising geriatric population to propel market growth

- 14.4.3 INDIA

- 14.4.3.1 Growing focus on product commercialization and rising cancer incidence to boost market demand

- 14.4.4 AUSTRALIA

- 14.4.4.1 Robust infrastructure for clinical trials and well-developed healthcare sector to aid market growth

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Growth in biopharmaceutical industry to facilitate market growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Product approvals and high healthcare expenditure to support market growth

- 14.5.2 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.6.2 KINGDOM OF SAUDI ARABIA

- 14.6.2.1 Increased number of product approvals and high healthcare expenditure to boost market growth

- 14.6.3 UAE

- 14.6.3.1 UAE market growth to be driven by localized manufacturing, expanded clinical applications, and strategic collaborations

- 14.6.4 REST OF MIDDLE EAST

- 14.7 AFRICA

- 14.7.1 SIGNIFICANT BURDEN OF HEMATOLOGIC MALIGNANCIES AND INFECTIOUS DISEASES TO PROPEL MARKET GROWTH

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 15.2.1 OVERVIEW OF MAJOR STRATEGIES ADOPTED BY PLAYERS IN CAR T-CELL THERAPY MARKET

- 15.3 REVENUE ANALYSIS, 2023-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Target footprint

- 15.5.5.5 Indication footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of startups/SMEs

- 15.7 COMPANY VALUATION & FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 JOHNSON & JOHNSON

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 GILEAD SCIENCES, INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product approvals

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses & competitive threats

- 16.1.3 BRISTOL-MYERS SQUIBB COMPANY

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product approvals

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 NOVARTIS AG

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product approvals

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses & competitive threats

- 16.1.5 AUTOLUS THERAPEUTICS

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product approvals

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses & competitive threats

- 16.1.6 JW (CAYMAN) THERAPEUTICS CO., LTD.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product approvals

- 16.1.6.3.2 Deals

- 16.1.7 IMMUNOADOPTIVE CELL THERAPY PRIVATE LIMITED (IMMUNOACT)

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Other developments

- 16.1.8 CARSGEN THERAPEUTICS HOLDINGS LIMITED

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product approvals

- 16.1.8.3.2 Deals

- 16.1.8.3.3 Expansions

- 16.1.9 IASO BIOTHERAPEUTICS

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product approvals

- 16.1.9.3.2 Deals

- 16.1.10 IMMUNEEL THERAPEUTICS

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches

- 16.1.1 JOHNSON & JOHNSON

- 16.2 OTHER PLAYERS

- 16.2.1 WUGEN

- 16.2.2 CARTESIAN THERAPEUTICS, INC.

- 16.2.3 ALLOGENE THERAPEUTICS

- 16.2.4 LYELL IMMUNOPHARMA, INC.

- 16.2.5 KYVERNA THERAPEUTICS, INC.

- 16.2.6 CELLICTIS SA

- 16.2.7 BRAINCHILD BIO

- 16.2.8 ATARA BIOTHERAPEUTICS, INC.

- 16.2.9 CARIBOU BIOSCIENCES

- 16.2.10 ARCELLX

- 16.2.11 CRISPR THERAPEUTICS

- 16.2.12 POSEIDA THERAPEUTICS

- 16.2.13 CABALETTA BIO

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Objectives of secondary research

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakdown of primaries

- 17.1.2.2 Objectives of primary research

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 INSIGHTS FROM PRIMARY EXPERTS

- 17.2.3 SEGMENTAL MARKET SIZE ESTIMATION

- 17.3 GROWTH RATE ASSUMPTIONS

- 17.3.1 CAGR PROJECTIONS

- 17.3.2 IMPACT OF SUPPLY- AND DEMAND-SIDE FACTORS

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH LIMITATIONS

- 17.6 STUDY ASSUMPTIONS

- 17.7 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS