|

시장보고서

상품코드

1963141

핵의학 시장 : 유형별, 용도별, 시술별, 최종사용자별, 지역별 - 예측(-2030년)Nuclear Medicine Market by Type, Application (Oncology, Cardiology, Neurology), Procedure, End User (Imaging Center, Hospital), and Region - Global Forecast to 2030 |

||||||

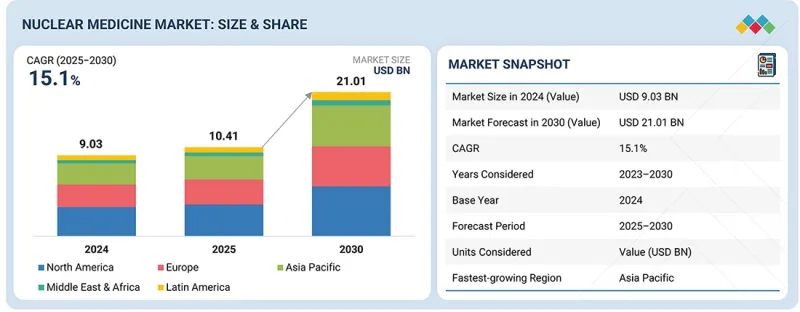

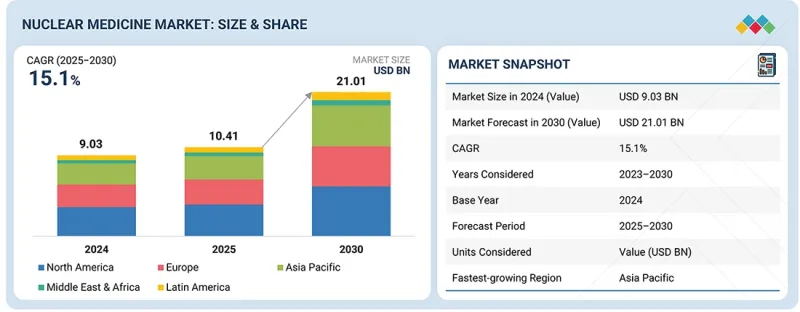

세계의 핵의학 시장 규모는 2025년 104억 1,000만 달러에서 2030년까지 210억 1,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 15.1%의 성장이 전망됩니다.

이는 종양학, 심장학, 신경학 분야의 진단/치료용 방사성의약품 및 의료용 방사성동위원소에 대한 수요 증가에 따른 것으로 분석됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 유형, 용도, 건수 평가, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중남미, 중동 및 아프리카 |

또한, 표적 방사성 핵종 치료의 사용 증가, 사이클로트론 및 원자로 기반 방사성 동위원소 생산의 성장, 핵약학 네트워크를 통한 이들 제품의 가용성 증가는 시장 성장을 가속하고 있습니다. 또한, 새로운 방사성의약품이 지속적으로 개발되고 규제 당국의 승인을 받음에 따라 전 세계적으로 방사성의약품의 사용이 크게 증가하고 있습니다. 이러한 방사성의약품의 사용 증가는 시장 성장을 더욱 촉진하고 있습니다.

"병원 부문이 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예측됩니다. "

최종 사용자별로는 병원 부문이 예측 기간 동안 핵의학 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이 예측은 병원의 복잡한 과정을 통해 방사성의약품을 준비하고 투여할 수 있는 능력, 방사성 동위원소를 취급할 수 있는 허가된 시설이 갖추어져 있고, 핵의학 전문가가 존재한다는 점을 근거로 하고 있습니다. 또한, 병원의 많은 환자 수, 진단 및 치료 서비스, 확립된 상환 시스템이 향후 몇 년 동안 이 부문의 성장을 더욱 촉진할 것으로 예측됩니다.

"예측 기간 동안 치료용 제품 부문이 진단용 제품 부문보다 더 높은 성장률을 나타낼 것으로 예측됩니다. "

치료용 부문은 예측 기간 동안 진단용 부문보다 더 높은 성장률을 보일 것으로 예측됩니다. 이러한 예측은 특히 세라믹 분야에서 암 치료에 표적 방사성의약품 치료와 방사성동위원소 활용이 확대되고 있기 때문입니다. 방사성 핵종 치료의 임상적 효능이 향상되고 치료용 방사성 동위원소 생산에 대한 규제 승인과 투자가 증가함에 따라 각 의료기관에서 방사성 핵종 치료의 수용성이 높아지고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 성장률을 나타낼 것으로 예측됩니다. "

아시아태평양은 예측 기간 동안 핵의학 시장에서 가장 높은 성장률을 나타낼 것으로 예측됩니다. 이는 암 발병률 증가, 병원 시설 확충, 핵의학 서비스 접근성 확대 등의 요인으로 인해 방사성의약품 및 방사성 동위원소 수요가 증가했기 때문입니다. 또한, 정부의 방사성 동위원소 생산, 규제 인프라 및 공급망 강화도 이 지역 시장 성장을 가속화하고 있습니다. 또한, 의료비 증가와 조기 진단 및 특이적 치료에 대한 인식이 높아지면서 핵의학 시술 건수 증가에 기여하고 있습니다.

세계의 핵의학(Nuclear Medicine) 시장에 대해 조사 분석했으며, 주요 촉진요인 및 억제요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 지견

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI 채택에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 핵의학 시장 : 유형별

제10장 핵의학 시장 : 용도별

제11장 핵의학 시장 : 시술 건수 평가

제12장 핵의학 시장 : 최종사용자별

제13장 핵의학 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.03.19The global nuclear medicine market is projected to reach USD 21.01 billion by 2030, growing from USD 10.41 billion in 2025 at a CAGR of 15.1% during the forecast period. This projection is driven by the growing demand for diagnostic and therapeutic radiopharmaceuticals and medical radioisotopes in the oncology, cardiology, and neurology fields.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Type, Application, Volume Assessment, End User, and Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

Additionally, the increased utilization of targeted radionuclide therapies, growth in cyclotron and reactor-based production of radioisotopes, and enhanced availability of these products through nuclear pharmacy networks are enhancing the growth of the market. Moreover, there is a significant increase in the use of radiopharmaceuticals across the globe as new ones are constantly developed and approved by regulatory bodies. This increased use of radiopharmaceuticals is further driving the growth of the market.

"The hospitals segment is projected to account for the largest share during the forecast period."

By end user, the hospitals segment is projected to account for the largest share of the nuclear medicine market during the forecast period. This projection is based on the capability of hospitals in preparing and administering radiopharmaceuticals through complex processes, available licensed facilities to deal with radioisotopes, and the presence of specialized nuclear medicine experts. Additionally, the presence of large volumes of patients, combined with diagnostic and therapeutic services, and well-established reimbursement systems in hospitals, is further expected to drive the growth of the segment in the coming years.

"The therapeutic applications segment is projected to register a higher growth than the diagnostic applications segment during the forecast period."

The therapeutic applications segment is projected to register a higher growth than the diagnostics applications segment during the forecast period. This projection is driven by the rising application of targeted radiopharmaceutical therapies and radioisotopes in treating cancer, especially in theranostics. Increasing clinical efficacy of radionuclide therapies and growing regulatory approval and investment in the production of therapeutic radioisotopes are boosting the acceptance across healthcare providers.

"Asia Pacific is projected to witness the highest growth rate during the forecast period."

Asia Pacific is projected to register the highest growth in the nuclear medicine market over the forecast period. This is due to the rising demand for radiopharmaceuticals and radioisotopes because of factors like increasing cancer prevalence, hospital facilities expansion, and growing access to nuclear medicine services. Additionally, the production of radioisotopes and the enhancement of regulatory infrastructure and supply chains by the governments are also increasing the growth of the markets in the region faster. Moreover, the growing healthcare spending and the rising awareness of early diagnosis and specific treatments are contributing to the rise in the number of nuclear medicine procedures.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the authentication and brand protection marketplace.

The breakdown of primary participants is mentioned below:

- By Company Type - Tier 1 - 64%; Tier 2 - 23%; and Tier 3 - 13%

- By Designation - C Level - 35%; Director Level - 25%; and Others - 40%

- By Region - North America - 44%; Europe - 23%; Asia Pacific - 28%; Latin America - 3%; Middle East & Africa - 2%

Key Players in the Nuclear Medicine Market

The key players operating in the nuclear medicine market include GE HealthCare (US), Cardinal Health (US), Curium (France), Bayer AG (Germany), Lantheus Holdings, Inc. (US), Novartis AG (Switzerland), Jubilant Pharmova Limited (India), Bracco Imaging S.P.A (Italy), Pharmalogic Holdings Corp. (US), NTP Radioisotopes SOC Ltd. (South Africa), Nordion Inc. (Canada), Siemens Healthineers AG (Germany), NorthStar Medical Radiosiotopes, LLC (US), Eckert & Ziegler (Germany), Isotope JSC (Russia), Global Medical Solutions (US), Telix Pharmaceuticals Limited (Australia), PDRadiopharma Inc. (Japan), ITM Isotope Technologies Munich SE (Germany), BWX Technologies Inc. (US), SHINE Technologies, LLC (US), Isotopia (Israel), Institutes of Isotopes (Hungary), China Isotope & Radiation Corporation (China), and IRE Elit (Turkey).

Research Coverage

The report analyzes the nuclear medicine market and aims to estimate the market size and future growth potential of various market segments by type, application, volume assessment, end user, and region. The report provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers (Increasing incidence and prevalence of target conditions, development of alpha-radioimmunotherapy-based targeted cancer treatments, initiatives to reduce demand and supply gap of Mo-99), restraints (Short half-life of radiopharmaceuticals), opportunities (Use of radiopharmaceuticals in neurological applications, growth opportunities in emerging economies), challenges (Hospital budget cuts and high equipment costs) influencing the growth of the nuclear medicine market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the nuclear medicine market

- Market Development: Comprehensive information on the lucrative emerging markets (based on type, application, volume assessment, and end user) across regions

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the nuclear medicine market

- Competitive Assessment: In-depth assessment of market share, growth strategies, product offerings, and capabilities of the leading players [GE HealthCare (US), Cardinal Health (US), Curium (France), Bayer AG (Germany), and Lantheus Holdings, Inc. (US)] operating in the nuclear medicine market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 REGIONAL SCOPE

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN NUCLEAR MEDICINE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 NUCLEAR MEDICINE MARKET OVERVIEW

- 3.2 NORTH AMERICA: NUCLEAR MEDICINE MARKET, BY TYPE & COUNTRY

- 3.3 NUCLEAR MEDICINE MARKET: GEOGRAPHIC SNAPSHOT

- 3.4 NUCLEAR MEDICINE MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing incidence and prevalence of target conditions

- 4.2.1.2 Rapid expansion of radioligand & targeted radionuclide therapy

- 4.2.1.3 Strategic entry of large pharma & capital inflows

- 4.2.1.4 Initiatives to reduce demand and supply gap of Mo-99

- 4.2.2 RESTRAINTS

- 4.2.2.1 Short half-life of radiopharmaceuticals

- 4.2.2.2 Structural isotope supply fragility

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of alpha-radioimmunotherapy-based targeted cancer treatments

- 4.2.3.2 Use of radiopharmaceuticals in neurological applications

- 4.2.3.3 Growth opportunities in emerging economies and expanding PET Infrastructure

- 4.2.4 CHALLENGES

- 4.2.4.1 High capital intensity of nuclear medicine infrastructure and hospital budget cuts

- 4.2.4.2 Workforce shortage in nuclear medicine

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL PHARMACEUTICAL INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE OF NUCLEAR MEDICINE PRODUCTS, BY TYPE, 2024

- 5.5.2 INDICATIVE PRICE OF NUCLEAR MEDICINE PRODUCTS, BY REGION, 2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 2844

- 5.6.2 EXPORT SCENARIO FOR HS CODE 2844

- 5.6.3 IMPORT SCENARIO FOR HS CODE 3002

- 5.6.4 EXPORT SCENARIO FOR HS CODE 3002

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.11 IMPACT OF 2025 US TARIFFS ON NUCLEAR MEDICINE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Hospitals

- 5.11.5.2 Diagnostic & imaging centers

- 5.11.5.3 Research & academic institutes

6 STRATEGIC DISRUPTIONS THROUGH TECHNOLOGY, PATENTS, AND DIGITAL & AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 NEXT-GENERATION RADIOLIGAND THERAPY & THERANOSTICS

- 6.1.2 RADIOISOTOPE PRODUCTION TECHNOLOGIES

- 6.1.3 HIGH-SPECIFIC-ACTIVITY RADIOLABELING AND CHELATION CHEMISTRY

- 6.1.4 GMP HOT-CELL MANUFACTURING & RADIOPHARMACEUTICAL QUALITY CONTROL

- 6.1.5 COLD KIT & GENERATOR TECHNOLOGIES

- 6.1.6 DECENTRALIZED ISOTOPE PRODUCTION & ADVANCED RADIOPHARMACY SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED RADIOTRACER SYNTHESIS & DISPENSING SYSTEMS

- 6.2.2 DOSIMETRY & TREATMENT PLANNING TECHNOLOGIES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 TARGET DISCOVERY & RADIOLIGAND DESIGN PLATFORMS

- 6.3.2 INTEGRATED THERANOSTIC WORKFLOWS & DATA PLATFORMS

- 6.3.3 AI-ENABLED QUANTITATIVE IMAGING & WORKFLOW AUTOMATION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR NUCLEAR MEDICINE MARKET

- 6.5.2 INSIGHTS: JURISDICTION & TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 PRECISION ONCOLOGY & THERANOSTICS EXPANSION

- 6.6.2 PERSONALIZED RADIONUCLIDE THERAPY USING DOSIMETRY-GUIDED DOSING

- 6.6.3 EARLY DISEASE DETECTION & RISK STRATIFICATION

- 6.6.4 NEURODEGENERATIVE & NEUROINFLAMMATORY DISORDERS

- 6.6.5 INFLAMMATION, INFECTION, AND IMMUNE SYSTEM IMAGING

- 6.7 IMPACT OF AI/GEN AI ON NUCLEAR MEDICINE MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN NUCLEAR MEDICINE MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 Clinical validation of AI-enabled standardization and workflow efficiency in PSMA PET imaging for prostate cancer

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED & ADJACENT ECOSYSTEMS

- 6.7.4.1 Radiopharmacy, manufacturing, and quality operations

- 6.7.4.2 Clinical imaging, dosimetry, and treatment planning infrastructure

- 6.7.4.3 Hospital systems, regulatory compliance, and theranostic data platforms

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Hospitals

- 6.7.5.1.2 User B: Diagnostic & imaging centers

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Hospitals

- 6.7.5.2.1.1 Implementation

- 6.7.5.2.1.2 Impact

- 6.7.5.2.2 User B: Diagnostic & imaging centers

- 6.7.5.2.2.1 Implementation

- 6.7.5.2.2.2 Impact

- 6.7.5.2.1 User A: Hospitals

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END-USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 NUCLEAR MEDICINE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 DIAGNOSTIC NUCLEAR MEDICINE

- 9.2.1 SPECT RADIOPHARMACEUTICALS

- 9.2.1.1 Tc-99m

- 9.2.1.1.1 Dominant role of Tc-99m in SPECT to boost market growth

- 9.2.1.2 I-123

- 9.2.1.2.1 Reduced exposure to radiation and lower risk of patients developing radiation-induced cancer to drive demand

- 9.2.1.3 Tl-201

- 9.2.1.3.1 Most commonly used substitute for Tc-99m in cardiac stress tests to support market growth

- 9.2.1.4 Ga-67

- 9.2.1.4.1 Long half-life of Ga-67 to facilitate easy sales and distribution

- 9.2.1.5 Other SPECT radiopharmaceuticals

- 9.2.1.1 Tc-99m

- 9.2.2 PET RADIOPHARMACEUTICALS

- 9.2.2.1 F-18

- 9.2.2.1.1 Advantages such as highly accurate, metabolism-based cancer imaging to boost demand

- 9.2.2.2 Rb-82

- 9.2.2.2.1 High accuracy offered by Rb-82 isotopes to support market growth

- 9.2.2.3 Other PET radiopharmaceuticals

- 9.2.2.1 F-18

- 9.2.1 SPECT RADIOPHARMACEUTICALS

- 9.3 THERAPEUTIC NUCLEAR MEDICINE

- 9.3.1 ALPHA EMITTERS

- 9.3.1.1 Ra-223

- 9.3.1.1.1 Rising metastatic prostate cancer burden and demand for bone-targeted, outpatient alpha therapy to drive adoption

- 9.3.1.1 Ra-223

- 9.3.2 BETA EMITTERS

- 9.3.2.1 I-131

- 9.3.2.1.1 I-131 to account for largest share of beta emitters market during forecast period

- 9.3.2.2 Y-90

- 9.3.2.2.1 Rising incidence of liver cancers and hepatocellular carcinoma to propel growth

- 9.3.2.3 Sm-153

- 9.3.2.3.1 Increasing incidence of bone metastasis to drive market

- 9.3.2.4 Lu-177

- 9.3.2.4.1 Rising cancer burden and expanding PRRT adoption to fuel growth

- 9.3.2.5 Other beta emitters

- 9.3.2.1 I-131

- 9.3.3 BRACHYTHERAPY ISOTOPES

- 9.3.3.1 I-125

- 9.3.3.1.1 I-125 to account for largest share of brachytherapy isotopes market

- 9.3.3.2 Ir-192

- 9.3.3.2.1 Precise, high-dose brachytherapy across multiple cancers to propel market

- 9.3.3.3 Pd-103

- 9.3.3.3.1 Ability to make brachytherapy permanent implant seeds for early-stage prostate cancer to drive adoption

- 9.3.3.4 Cs-131

- 9.3.3.4.1 Growing use of Cs-131 in gynecological applications to aid growth

- 9.3.3.5 Other brachytherapy isotopes

- 9.3.3.1 I-125

- 9.3.1 ALPHA EMITTERS

10 NUCLEAR MEDICINE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 DIAGNOSTIC APPLICATIONS

- 10.2.1 SPECT APPLICATIONS

- 10.2.1.1 Cardiology

- 10.2.1.1.1 Rising global cardiovascular disease burden and expanding, evidence-backed cardiology applications to drive growth

- 10.2.1.2 Bone scans

- 10.2.1.2.1 High precision of SPECT to boost adoption of bone scans

- 10.2.1.3 Thyroid

- 10.2.1.3.1 Rising demand for combination SPECT/CT therapy to drive market growth

- 10.2.1.4 Pulmonary scans

- 10.2.1.4.1 High accuracy and sensitivity of SPECT/CT pulmonary imaging to boost market

- 10.2.1.5 Other SPECT applications

- 10.2.1.1 Cardiology

- 10.2.2 PET APPLICATIONS

- 10.2.2.1 Oncology

- 10.2.2.1.1 Increasing incidence of cancer to fuel market growth

- 10.2.2.2 Cardiology

- 10.2.2.2.1 Growing preference for FDG in cardiac imaging to propel market

- 10.2.2.3 Neurology

- 10.2.2.3.1 Increasing incidence of AD, epilepsy, and Parkinson's disease to increase adoption of PET imaging

- 10.2.2.4 Other PET applications

- 10.2.2.1 Oncology

- 10.2.1 SPECT APPLICATIONS

- 10.3 THERAPEUTIC APPLICATIONS

- 10.3.1 THYROID INDICATIONS

- 10.3.1.1 Increasing prevalence of thyroid disorders to boost market

- 10.3.2 BONE METASTASIS

- 10.3.2.1 Introduction of novel therapies for bone metastasis to positively impact market growth

- 10.3.3 ENDOCRINE TUMORS

- 10.3.3.1 US to dominate therapeutic nuclear medicine market for endocrine tumor applications

- 10.3.4 LYMPHOMA

- 10.3.4.1 Development of new isotopes for treatment of lymphoma to present huge growth opportunities

- 10.3.5 OTHER THERAPEUTIC APPLICATIONS

- 10.3.1 THYROID INDICATIONS

11 NUCLEAR MEDICINE MARKET: PROCEDURAL VOLUME ASSESSMENT

- 11.1 INTRODUCTION

- 11.2 DIAGNOSTIC PROCEDURES

- 11.2.1 HIGH PREVALENCE OF CANCER AND CARDIAC DISEASES TO DRIVE MARKET GROWTH

- 11.3 THERAPEUTIC PROCEDURES

- 11.3.1 GROWING DEMAND FOR NON-INVASIVE METHODS TO SUPPORT MARKET GROWTH

12 NUCLEAR MEDICINE MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS

- 12.2.1 GROWING VOLUME OF DIAGNOSTIC PROCEDURES TO DRIVE MARKET GROWTH

- 12.3 DIAGNOSTIC & IMAGING CENTERS

- 12.3.1 GROWING NUMBER OF PRIVATE IMAGING CENTERS TO SUPPORT MARKET GROWTH

- 12.4 ACADEMIC & RESEARCH INSTITUTES

- 12.4.1 INCREASING COLLABORATIONS BETWEEN NUCLEAR IMAGING COMPANIES AND ACADEMIA TO PROPEL MARKET GROWTH

- 12.5 OTHER END USERS

13 NUCLEAR MEDICINE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 US to dominate North American nuclear medicine market during forecast period

- 13.2.3 CANADA

- 13.2.3.1 Increasing initiatives for medical isotope development to support market growth

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Well-established healthcare system to drive market growth

- 13.3.3 FRANCE

- 13.3.3.1 Rising incidence of diseases such as cancer, Alzheimer's, and Parkinson's disease to favor market growth

- 13.3.4 UK

- 13.3.4.1 Growing demand for diagnostic imaging and growing awareness to drive market growth

- 13.3.5 ITALY

- 13.3.5.1 Aging demographics, high procedure volumes, increasing cancer incidence, and domestic isotope self-sufficiency to fuel growth

- 13.3.6 SPAIN

- 13.3.6.1 Rising disease prevalence, regulatory modernization, and targeted radioligand expansion to create supportive environment

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 JAPAN

- 13.4.2.1 Japan to dominate APAC nuclear medicine market

- 13.4.3 CHINA

- 13.4.3.1 Increasing nuclear medicine infrastructure and growing prevalence of chronic diseases to augment market

- 13.4.4 INDIA

- 13.4.4.1 Rising cancer and cardiovascular disease burden and rapid expansion of nuclear medicine infrastructure to boost market

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Accelerating PET utilization and maturing domestic RPT innovation ecosystem to augment market

- 13.4.6 AUSTRALIA

- 13.4.6.1 Rising cancer prevalence, high PET penetration, and growing domestic isotope production to support growth

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Rising cancer incidence and expanding imaging infrastructure to drive market

- 13.5.3 MEXICO

- 13.5.3.1 Rising cancer and cardiovascular disease burden and expanding private-sector PET access to drive market

- 13.5.4 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Growing healthcare needs and favorable government support to boost market

- 13.6.3 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN NUCLEAR MEDICINE MARKET

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION & FINANCIAL METRICS

- 14.6.1 FINANCIAL METRICS

- 14.6.2 COMPANY VALUATION

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT APPROVALS

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 NOVARTIS AG

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product approvals

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 LANTHEUS HOLDINGS, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 GE HEALTHCARE

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product approvals

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.3.4 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 CURIUM

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product approvals & enhancements

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.3.4 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 TELIX PHARMACEUTICALS LIMITED

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product approvals

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 SIEMENS HEALTHINEERS

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Other developments

- 15.1.7 CHINA ISOTOPE & RADIATION CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Other developments

- 15.1.8 BAYER AG

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 BRACCO IMAGING S.P.A.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product approvals

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Other developments

- 15.1.10 CARDINAL HEALTH

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.11 JUBILANT PHARMOVA LIMITED

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product approvals

- 15.1.11.3.2 Deals

- 15.1.11.3.3 Other developments

- 15.1.12 ELI LILLY AND COMPANY

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.12.3.2 Other developments

- 15.1.13 BWXT MEDICAL LTD.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product approvals

- 15.1.14 NTP RADIOISOTOPES SOC LTD. (A SUBSIDIARY OF SOUTH AFRICAN NUCLEAR ENERGY CORPORATION)

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 ECKERT & ZIEGLER

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product approvals

- 15.1.15.3.2 Deals

- 15.1.15.3.3 Expansions

- 15.1.16 ISOTOPE JSC

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Deals

- 15.1.16.3.2 Other developments

- 15.1.17 PDRADIOPHARMA INC.

- 15.1.17.1 Business overview

- 15.1.17.2 Products offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Product launches & approvals

- 15.1.17.3.2 Deals

- 15.1.17.3.3 Expansions

- 15.1.18 ITM ISOTOPE TECHNOLOGIES MUNICH SE

- 15.1.18.1 Business overview

- 15.1.18.2 Products offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Product approvals

- 15.1.18.3.2 Deals

- 15.1.18.3.3 Expansions

- 15.1.18.3.4 Other developments

- 15.1.19 NARODOWE CENTRUM BADAN JĄDROWYCH OSRODEK RADIOIZOTOPOW - POLATOM

- 15.1.19.1 Business overview

- 15.1.19.2 Products offered

- 15.1.19.3 Recent developments

- 15.1.19.3.1 Deals

- 15.1.20 ANSTO

- 15.1.20.1 Business overview

- 15.1.20.2 Products offered

- 15.1.20.3 Recent developments

- 15.1.20.3.1 Deals

- 15.1.20.3.2 Other developments

- 15.1.1 NOVARTIS AG

- 15.2 OTHER PLAYERS

- 15.2.1 SHINE TECHNOLOGIES, LLC

- 15.2.2 ISOTOPIA MOLECULAR IMAGING LTD.

- 15.2.3 INSTITUTE OF ISOTOPES

- 15.2.4 GLOBAL MEDICAL SOLUTIONS

- 15.2.5 ISOTEX DIAGNOSTICS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 RESEARCH APPROACH

- 16.2.1 SECONDARY RESEARCH

- 16.2.1.1 Key data from secondary sources

- 16.2.2 PRIMARY RESEARCH

- 16.2.2.1 Primary sources

- 16.2.2.2 Key data from primary sources

- 16.2.2.3 Breakdown of primaries

- 16.2.2.4 Insights from primary experts

- 16.2.1 SECONDARY RESEARCH

- 16.3 RESEARCH METHODOLOGY DESIGN

- 16.4 MARKET SIZE ESTIMATION

- 16.4.1 APPROACH 1: REVENUE SHARE ANALYSIS (BOTTOM-UP APPROACH - SUPPLY-SIDE ANALYSIS)

- 16.4.2 APPROACH 2: SECONDARY DATA & PRIMARY INTERVIEWS

- 16.4.3 APPROACH 3: SEGMENTAL MARKET SIZE ASSESSMENT

- 16.4.4 APPROACH 4: TOP-DOWN APPROACH

- 16.4.5 GROWTH FORECAST

- 16.4.6 GEOGRAPHIC MARKET ASSESSMENT (BY REGION AND COUNTRY)

- 16.5 MARKET BREAKDOWN & DATA TRIANGULATION

- 16.6 STUDY ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS

- 16.7.1 METHODOLOGY-RELATED LIMITATIONS

- 16.7.2 SCOPE-RELATED LIMITATIONS

- 16.8 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS