|

시장보고서

상품코드

1963142

대량 알림 시스템 시장 : 소프트웨어별, 하드웨어별, 용도별 - 예측(-2030년)Mass Notification System Market by Software (Public Warning & Emergency Alerting, Operational & IT Alerting), Hardware (Fire Alarm System, Public Address Systems), Application (Critical Event Management, Reporting & Analytics) - Global Forecast to 2030 |

||||||

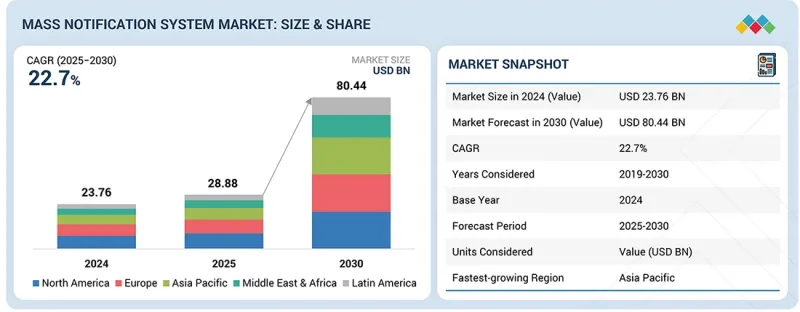

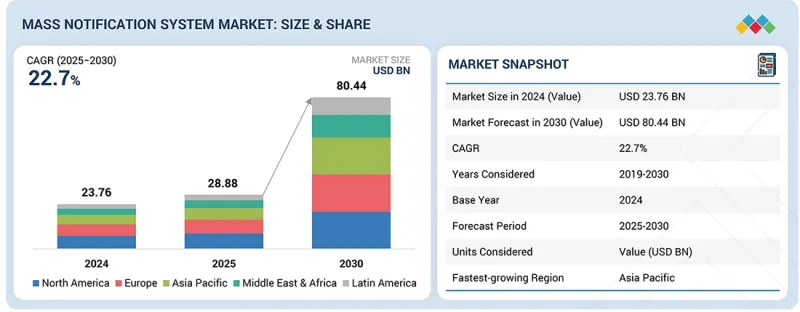

세계의 대량 알림 시스템 시장 규모는 2025년 288억 8,000만 달러에서 2030년까지 804억 4,000만 달러에 이를 것으로 예측되어 CAGR로 22.7%확대가 전망되고 있습니다.

규제 및 업계 요구사항으로 인해 조직이 보다 엄격한 컴플라이언스 의무와 보안 통신에 대한 높은 책임감에 직면함에 따라 고급 대규모 알림 솔루션의 채택이 가속화되고 있습니다. 연방, 주정부 및 특정 산업 표준은 다중 채널 경보, 검증 가능한 통신 로그, 중대 상황 발생 시 신속한 협업을 요구하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2019-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 제공, 통신 채널, 시설 유형, 용도, 업계 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 라틴아메리카 |

의료, 교육, 운송 등의 산업에서는 생명 안전 시스템 및 빌딩 자동화 네트워크와 연계된 규제 준수 알림 워크플로우의 도입이 요구되고 있습니다. 이러한 규제로 인해 기업들은 자동 에스컬레이션과 연속성을 중시하는 통신 프로토콜을 지원하는 확장성과 상호운용성이 뛰어난 MNS 아키텍처로 기존 시스템을 대체해야 하는 상황에 직면해 있습니다. 규제 감독이 강화됨에 따라 조직은 운영 준비성을 확보하고 위험을 줄이기 위해 현대적이고 규제에 부합하는 기술에 대한 투자를 늘리고 있습니다.

대규모 알림 시스템 시장 벤더들은 실시간 위협 인텔리전스와 멀티 채널 배포 기능을 통합한 통합 커뮤니케이션 플랫폼을 제공함으로써 대응하고 있습니다. 최신 솔루션은 인시던트 분석과 지리적 타겟팅 전송을 결합하여 분산된 환경에서의 긴급 커뮤니케이션을 효율화하는 중앙 집중식 지휘 계층을 조직에 제공합니다. 이 플랫폼은 중대한 사건을 신속하게 식별하고, 모바일, 데스크톱, 시설 기반 시스템 간에 경보를 동기화하여 대응 속도와 운영 일관성을 향상시킵니다. 하이브리드 워크플레이스와 중요 인프라 네트워크가 확대됨에 따라, 고 영향도 사고 발생 시 상황 인식을 강화하기 위해 중앙 집중식 알림 프레임워크가 필수적으로 요구되고 있습니다. 각 벤더들은 리스크 관리 요건을 충족하기 위해 보안 통제 및 컴플라이언스 보고를 강화하기 위해 노력하고 있습니다.

"확장 가능하고 탄력적인 통신 기능을 통해 클라우드 구축이 가속화되고 있습니다."

클라우드 구축은 산업을 막론하고 모든 조직이 확장 가능하고 탄력적이며 비용 효율적인 통신 인프라를 우선시하는 가운데 가장 빠르게 성장하는 분야로 부상하고 있습니다. 기업 및 정부 기관은 신속한 도입과 원활한 멀티채널 경보 전달을 위해 On-Premise 시스템에서 클라우드 네이티브 플랫폼으로 전환하고 있습니다. 클라우드 환경은 장치 간 실시간 동기화와 위치 정보, 위협 유형, 운영 상황에 따라 경보를 조정하는 동적 라우팅 인텔리전스를 실현합니다. 이를 통해 비즈니스 연속성 계획을 강화하고, 네트워크 장애나 물리적 시스템 중단 시에도 중단 없이 통신을 유지할 수 있습니다. 각 벤더들은 의료, 교육, 교통, 중요 인프라 부문의 규제 요건을 충족하기 위해 첨단 암호화 기술과 컴플라이언스 대응 보고 기능을 갖춘 클라우드 서비스를 강화하고 있습니다. 디지털 전환이 가속화되는 가운데, 클라우드 구축은 고가용성, 빠른 확장성, 미션 크리티컬한 대규모 통신 생태계를 구현하기 위한 최적의 아키텍처가 되고 있습니다.

"통신 채널별로는 음성통신이 즉각성, 명료성, 높은 신뢰성에 따른 경보 전달 능력으로 선두를 달리고 있습니다. "

음성 통신은 다양한 시설 유형과 고밀도 환경에서 명확하고 즉각적이며 권위 있는 경보를 전달할 수 있는 능력으로 인해 가장 큰 시장 점유율을 차지하고 있습니다. 조직은 음성 기반 시스템에 의존하여 긴급 상황에서 중요한 지시를 내릴 때, 메시지가 쉽게 이해되고 신속하게 실행될 수 있도록 보장합니다. 이 채널은 교육, 의료, 산업, 정부 시설에서 실시간 고신뢰성 통신이 필요한 사고 시나리오에서 여전히 필수적인 채널입니다. IP 기반 스피커, 분산형 오디오 아키텍처, 네트워크화된 공공 방송 시스템의 발전으로 시스템의 신뢰성, 음향 선명도, 특정 지역에 대한 메시지 전달 기능이 강화되었습니다. 음성 통신은 화재 경보 시스템, 빌딩 관리 플랫폼, 사고 지휘 센터와도 원활하게 통합되어 통합된 경보와 조정된 비상 대응을 가능하게 합니다. 이 부문은 신규 구축과 레거시 인프라 현대화 모두에서 높은 채택률을 보이고 있으며, MNS 생태계에서 선도적인 입지를 강화하고 있습니다.

세계의 대규모 알림 시스템 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 지견

제4장 시장 개요

제5장 업계 동향

제6장 전략적 파괴 : 특허, 디지털, AI 채택

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 대량 알림 시스템 시장 : 제품별

제10장 대량 알림 시스템 시장 : 통신 방식별

제11장 대량 알림 시스템 시장 : 용도별

제12장 대량 알림 시스템 시장 : 최종사용자별

제13장 대량 알림 시스템 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.03.19The global mass notification system market size is projected to grow from USD 28.88 billion in 2025 to USD 80.44 billion by 2030, at a CAGR of 22.7%. Regulatory and industry-mandated requirements are accelerating adoption of advanced mass notification solutions as organizations face stricter compliance obligations and higher accountability for safety communication. Federal, state, and sector-specific standards require multi-channel alert, verifiable communication logs, and rapid coordination during critical events.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | Offering, Communication Channel, Facility Type, Application, and Vertical |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and Latin America |

Industries such as healthcare, education and transportation must implement compliant notification workflows that integrate with life safety systems and building automation networks. These mandates push enterprises to replace legacy systems with scalable, interoperable MNS architectures that support automated escalation and continuity-driven communication protocols. As regulatory oversight intensifies, organizations increasingly invest in modern, compliance-aligned technologies to ensure operational readiness and risk mitigation.

Vendors in the Mass Notification System market are responding by integrating real-time threat intelligence and multi-channel delivery capabilities into unified communication platforms. Modern solutions combine incident analytics and geo-targeted distribution to provide organizations with a centralized command layer that streamlines emergency communication across distributed environments. These platforms enable the rapid identification of critical events and synchronize alerts across mobile, desktop, and facility-based systems, thereby improving response speed and operational consistency. As hybrid workplaces and critical infrastructure networks expand, centralized notification frameworks are becoming essential for enhancing situational awareness during high-impact incidents. Vendors are also strengthening security controls and compliance reporting to meet risk management requirements.

"Cloud deployment is accelerating due to its scalable, resilient communication capabilities"

Cloud deployment is emerging as the fastest growing segment as organizations across industries prioritize scalable, resilient, and cost-efficient communication infrastructure. Enterprises and government agencies are shifting from on-premises systems to cloud-native platforms to support rapid implementation and seamless multi-channel alert distribution. Cloud environments enable real-time synchronization across devices and dynamic routing intelligence that adjust alerts based on location, threat type, and operational context. This enhances continuity planning, allowing organizations to maintain uninterrupted communication even during network disruptions or physical system outages. Vendors are strengthening cloud offerings with advanced encryption and compliance-ready reporting to meet regulatory requirements in healthcare, education, transportation, and critical infrastructure sectors. As digital transformation accelerates, cloud deployment is becoming the preferred architecture for high-availability, rapidly scalable, and mission-critical mass communication ecosystems.

"By communication channel, voice communication leads due to its immediate, clear, high-assurance alert delivery."

Voice communication holds the largest market share due to its ability to deliver clear, immediate, and authoritative alerts across diverse facility types and high-occupancy environments. Organizations rely on voice-based systems to issue critical instructions during emergencies, ensuring messages are easily understood and quickly acted upon. This channel remains essential for incident scenarios that require real-time, high-assurance communication in education, healthcare, industrial sites and government facilities. Advancements in IP-based speakers, distributed audio architectures, and networked public address systems have strengthened system reliability, acoustic clarity, and zone-specific messaging capabilities. Voice communication also integrates seamlessly with fire alarm systems, building management platforms, and incident command centers, enabling unified alerting and coordinated emergency response. This segment benefits from strong adoption in both new installations and modernization of legacy infrastructure, reinforcing its dominant position in the MNS ecosystem.

"North America will have the largest market share in 2025, and Asia Pacific is slated to grow at the highest rate during the forecast period"

North America holds the largest share of the Mass Notification System market due to mature safety infrastructures and early adoption of advanced communication technologies across enterprise, education, government, and critical infrastructure sectors. Organizations in the US and Canada prioritize real-time alerting and unified incident communication with emergency management networks, which attracts investment in multi-channel notification platforms. Growth is further supported by increasing climate-related disruptions and modernization of public warning systems aligned with federal guidelines. The region is also rising demand for cloud-enabled orchestration, geo-intelligent routing, and automated escalation workflows that improve operational continuity during high-impact events. Continuous upgrades to IP-based communication endpoints and command-and-control platforms reinforce North America's leadership position. Vendors benefit from a well-established ecosystem that supports rapid deployment, advanced integration frameworks, and compliance-driven mass communication strategies.

Asia Pacific is the fastest growing region in the Mass Notification System market, driven by rapid urbanization and heightened focus on disaster preparedness across natural disaster-prone countries. Governments and enterprises are modernizing emergency communication frameworks to improve population-scale alerting and facility-level response coordination. Rising investments in smart city programs, transportation hubs, and industrial facilities are boosting adoption of scalable notification platforms with multilingual support and adaptive alert routing. Increasing regulatory emphasis on workplace safety, campus protection, and business continuity planning further accelerates adoption. Asia Pacific organizations are prioritizing resilient, interoperable, and high-speed communication systems to manage diverse emergency scenarios effectively.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the Mass notification system market.

- By Company: Tier I - 31%, Tier II - 42%, and Tier III - 27%

- By Designation: Directors - 29%, Managers - 44%, and others - 27%

- By Region: North America - 40%, Europe - 22%, Asia Pacific - 26%, Middle East & Africa - 5%, and Latin America - 7%

The report includes the study and in-depth company profiles of key players offering Mass notification system solutions and services. The major players in the Mass notification system market Siemens AG (Germany), Everbridge (US), Honeywell (US), Eaton (Ireland), Motorola Solutions (US), BlackBerry (Canada), Johnson Controls (Ireland), Singlewire Software (US), OnSolve (US), AlertMedia (US), Alertus Technologies (US), F24 AG (Germany), HipLink (US), American Signal Corporation (US), ATI Systems (US), Mircom (Canada), Finalsite (US), Omnilert (US), Regroup Mass Notification (US), Konexus (US), Netpresenter (Netherlands), Iluminr (US), CrisisGo (US), Omnigo (US), Ruvna (US), Kalxon Technologies (India), Crises Control (UK), ICESOFT Technologies (Canada), Squadcast (US), Pocketstop (US), Preparis (US), HQE Systems (US), Veoci (US), Text-Em-All (US), DialMyCalls (US).

Research Coverage

This research report categorizes the mass notification system market and has been segmented based on offering, communication channel, facility type, and vertical. The offering segment is split into hardware, software and services. The hardware segment is further split into Fire Alarm Systems, Public Address Systems, Duress Buttons, Electronic Messaging Displays, Visual Alerts Devices, Sirens. The software segment is bifurcated into type, integration and deployment mode. The software type includes Crisis & Event Notification Platform, Campus & Facility Notification Software, Public Warning & Emergency Alerting Platform, Operational & IT Alerting Software, and Others. The software integration includes Integrated and Standalone. The deployment mode is categorized into Cloud and On-premises. The services segment includes professional & managed services. The professional services are further categorized in Consulting & Planning Services and Training & Support Services. The communication channel segment spans Voice Communication, Digital Communication and Text-based Communication. The facility type is categorized in Indoor Facilities and Outdoor Facilities. The application segment covers Critical Event management, Public Safety & Warning, Business Continuity & Disaster management, Reporting & Analytics and Other Applications. The verticals include BFSI, Retail & eCommerce, Transportation & Logistics, Government & Defense, Healthcare & Life Sciences, Telecom, Energy & Utilities, Manufacturing, IT/ITeS, Media & Entertainment, Education, and Other Verticals. The regional analysis of the market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the Mass notification system market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments associated with the Mass notification system market. This report provides a competitive analysis of emerging startups in the Mass notification system market ecosystem.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall Mass notification system market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Growing need for real-time, multi-channel emergency communication across organizations, Regulatory and industry-mandated requirements for emergency preparedness), restraints (Legacy infrastructure and inconsistent endpoint environments limit smooth adoption, Data privacy concerns and strict regulatory controls around emergency communication), opportunities (Advanced content lifecycle automation, intelligent sync, and metadata-driven governance, Expansion into AI-driven alert automation, multilingual messaging, and behavioral response analytics), and challenges (Balancing ease of access with strong security posture across devices and external users, Managing cross-channel consistency, false alarms, and governance across large distributed organizations)

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the Mass Notification System market

Market Development: Comprehensive information about lucrative markets - analysis of the Mass Notification System market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Mass Notification System market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of Siemens AG (Germany), Everbridge (US), Honeywell (US), Eaton (Ireland), Motorola Solutions (US), BlackBerry (Canada), Johnson Controls (Ireland), Singlewire Software (US), OnSolve (US), AlertMedia (US), Alertus Technologies (US), F24 AG (Germany), HipLink (US), American Signal Corporation (US), ATI Systems (US), Mircom (Canada), Finalsite (US), Omnilert (US), Regroup Mass Notification (US), Konexus (US), Netpresenter (Netherlands), Iluminr (US), CrisisGo (US), Omnigo (US), Ruvna (US), Kalxon Technologies (India), Crises Control (UK), ICESOFT Technologies (Canada), Squadcast (US), Pocketstop (US), Preparis (US), HQE Systems (US), Veoci (US), Text-Em-All (US), DialMyCalls (US) among others, in the Mass Notification System market. The report also helps stakeholders understand the pulse of the Mass Notification System market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MASS NOTIFICATION SYSTEM MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES IN MASS NOTIFICATION SYSTEM MARKET

- 3.2 MASS NOTIFICATION SYSTEM MARKET, BY REGION

- 3.3 MASS NOTIFICATION SYSTEM MARKET: TOP THREE APPLICATIONS

- 3.4 NORTH AMERICA: MASS NOTIFICATION SYSTEM MARKET, BY OFFERING AND COMMUNICATION MODE

- 3.5 MASS NOTIFICATION SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 IPAWS/WEA-equivalent compliance as a structural market requirement

- 4.2.1.2 Embedding of MNS into regulated operational environments

- 4.2.1.3 Expectation of immediate, area-wide alerting for life safety

- 4.2.2 RESTRAINTS

- 4.2.2.1 Persistence of legacy, non-standard alerting assets

- 4.2.2.2 Adverse consequence of erroneous alerting

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Managed alerting and compliance services

- 4.2.3.2 Resilient, edge-enabled notification capability

- 4.2.3.3 Use of MNS for cyber and infrastructure incident communications

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited end-to-end delivery confirmation in broadcast alerting

- 4.2.4.2 Securing alert origination under heightened cyber and insider risk

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MASS NOTIFICATION SYSTEM MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 EVOLUTION OF MASS NOTIFICATION SYSTEMS

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN INCIDENT AND EMERGENCY MANAGEMENT MARKET INDUSTRY

- 5.3.4 TRENDS IN A2P MESSAGING MARKET INDUSTRY

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 NOTIFICATION DEVICE PROVIDERS

- 5.5.2 SOFTWARE PROVIDERS

- 5.5.2.1 Mass notification platforms

- 5.5.2.2 Incident & event management software

- 5.5.2.3 Operational & IT alerting software

- 5.5.2.4 Safety, risk, and threat intelligence software

- 5.5.2.5 Analytics, reporting, and intelligence software

- 5.5.2.6 Platform enablement & integration software

- 5.5.3 SERVICE PROVIDERS

- 5.5.3.1 Professional service providers

- 5.5.3.2 Managed service providers

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF OFFERINGS (HARDWARE), BY KEY PLAYER, 2025

- 5.6.2 AVERAGE SELLING PRICE OF APPLICATIONS, 2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8531)

- 5.7.2 EXPORT SCENARIO (HS CODE 8531)

- 5.8 KEY CONFERENCES AND EVENTS, 2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 HOLLAND HOSPITAL STRENGTHENS STAFF SAFETY WITH SINGLEWIRE INFORMACAST

- 5.11.2 BERENICE INTERNATIONAL AIRPORT ENABLES CENTRALIZED FIRE MONITORING WITH MIRCOM

- 5.11.3 MINNESOTA TWINS ENHANCE EVENT SECURITY AND THREAT AWARENESS WITH ALERTMEDIA

- 5.11.4 INDUSTRIAL MANUFACTURER IMPROVES EMPLOYEE COMMUNICATIONS WITH OMNILERT

- 5.11.5 BURNS & MCDONNELL STRENGTHENS GLOBAL SAFETY AND RESILIENCE WITH EVERBRIDGE

6 STRATEGIC DISRUPTION: PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY TECHNOLOGIES

- 6.1.1 CLOUD COMPUTING

- 6.1.2 BIG DATA

- 6.1.3 INTERNET OF THINGS (IOT)

- 6.1.4 PREDICTIVE ANALYTICS

- 6.1.5 A2P MESSAGING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GEOGRAPHIC INFORMATION SYSTEMS

- 6.2.2 GEOFENCING

- 6.2.3 LOCATION ANALYTICS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BLOCKCHAIN

- 6.4 TECHNOLOGY ROADMAP

- 6.4.1 SHORT TERM (2025-2027): FOUNDATION AND STANDARDIZATION PHASE

- 6.4.2 MID TERM (2028-2030): CONVERGENCE AND AUTOMATION PHASE

- 6.4.3 LONG TERM (2031-2035): AUTONOMOUS AND COGNITIVE INTEROPERABILITY PHASE

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2026

- 6.5.3 INNOVATION AND PATENT APPLICATIONS

- 6.6 IMPACT OF AI ON THE MASS NOTIFICATION SYSTEM MARKET

- 6.6.1 BEST PRACTICES IN MASS NOTIFICATION SYSTEM MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 KEY REGULATIONS

- 7.1.2.1 North America

- 7.1.2.1.1 Wireless Emergency Alerts (WEA) Regulations (US)

- 7.1.2.1.2 California Consumer Privacy Act/CPRA (US)

- 7.1.2.1.3 National Public Alerting System (Alert Ready) (Canada)

- 7.1.2.2 Europe

- 7.1.2.2.1 General Data Protection Regulation (GDPR) (European Union)

- 7.1.2.2.2 European Electronic Communications Code (EECC) - Article 110

- 7.1.2.2.3 FR-Alert Framework (France)

- 7.1.2.2.4 MoWaS (Germany)

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 Disaster Management Act, 2005 (India)

- 7.1.2.3.2 J-Alert System Framework (Japan)

- 7.1.2.3.3 Emergency Alert Service Regulations (South Korea)

- 7.1.2.4 Middle East & Africa

- 7.1.2.4.1 Telecommunications and Emergency Communication Regulations (UAE)

- 7.1.2.4.2 National Cybersecurity Authority Frameworks (Saudi Arabia)

- 7.1.2.4.3 Disaster Management Act (South Africa)

- 7.1.2.5 Latin America

- 7.1.2.5.1 General Data Protection Law (LGPD) (Brazil)

- 7.1.2.5.2 National Civil Protection Law (Mexico)

- 7.1.2.1 North America

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS INDUSTRY END USERS

- 8.5 IMPACT OF 2025 US TARIFF - MASS NOTIFICATION SYSTEM MARKET

- 8.5.1 INTRODUCTION

- 8.5.1.1 Tariff/Trade Policy Updates (August-December 2025)

- 8.5.2 KEY TARIFF RATES

- 8.5.3 PRICE IMPACT ANALYSIS

- 8.5.3.1 Strategic shifts and emerging trends

- 8.5.4 IMPACT ON COUNTRY/REGION

- 8.5.4.1 US

- 8.5.4.2 China

- 8.5.4.3 Europe

- 8.5.4.4 Asia Pacific (excluding China)

- 8.5.5 IMPACT ON END-USE INDUSTRIES

- 8.5.5.1 Government & Public Sector

- 8.5.5.2 Transportation & Transit Operators

- 8.5.5.3 Energy & Utilities

- 8.5.5.4 Manufacturing & Industrial Campuses

- 8.5.5.5 Healthcare & Educational Institutions

- 8.5.1 INTRODUCTION

9 MASS NOTIFICATION SYSTEM MARKET, BY OFFERINGS

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 9.2 SOFTWARE

- 9.2.1 BY TYPE

- 9.2.1.1 Mass notification platforms

- 9.2.1.1.1 Centralized mass notification orchestration across multi-channel communication environments to drive segment

- 9.2.1.2 Incident & event management software

- 9.2.1.2.1 Stronger incident lifecycle coordination to drive segment

- 9.2.1.3 Operational & IT alerting software

- 9.2.1.3.1 Automated alert distribution through real-time monitoring integration to drive segment

- 9.2.1.4 Safety, risk & threat intelligence software

- 9.2.1.4.1 Enhanced threat detection and workforce protection to boost market

- 9.2.1.5 Analytics, reporting & intelligence software

- 9.2.1.5.1 Support for compliance visibility and response performance measurement to drive market

- 9.2.1.6 Platform enablement & integration software

- 9.2.1.6.1 Accelerated system interoperability within mass notification ecosystems to boost segment

- 9.2.1.1 Mass notification platforms

- 9.2.2 BY DEPLOYMENT MODE

- 9.2.2.1 Cloud

- 9.2.2.1.1 Scalable and remotely accessible mass notification capabilities to boost segment

- 9.2.2.2 On-premises

- 9.2.2.2.1 Maintaining infrastructure control and regulatory alignment - key segment driver

- 9.2.2.1 Cloud

- 9.2.1 BY TYPE

- 9.3 NOTIFICATION DEVICES

- 9.3.1 FIRE ALARM SYSTEMS

- 9.3.1.1 Automated life-safety detection and evacuation signaling to boost segment

- 9.3.2 PUBLIC ADDRESS SYSTEMS

- 9.3.2.1 Facility-wide voice communication during emergencies and operational events

- 9.3.3 DURESS BUTTONS

- 9.3.3.1 Immediate distress signaling for rapid security response activation to boost segment

- 9.3.4 ELECTRONIC MESSAGING DISPLAYS

- 9.3.4.1 Real-time visual instructions across public and enterprise environments

- 9.3.5 VISUAL ALERT DEVICES

- 9.3.5.1 Support for inclusive emergency signaling through strobes and indicator systems to drive segment

- 9.3.6 SIRENS

- 9.3.6.1 Efficiency in large-area emergency notification to propel growth

- 9.3.1 FIRE ALARM SYSTEMS

- 9.4 SERVICES

- 9.4.1 PROFESSIONAL SERVICES

- 9.4.1.1 Assured operationally effective and compliant deployment to boost growth

- 9.4.1.2 Advisory & planning services

- 9.4.1.3 System design & engineering services

- 9.4.1.4 Integration & deployment services

- 9.4.1.5 Training & enablement services

- 9.4.2 MANAGED SERVICES

- 9.4.2.1 Continuous monitoring, optimization, and resilience assurance for mass notification environments to drive market

- 9.4.2.2 Migration & transition services

- 9.4.2.3 Testing & validation services

- 9.4.2.4 Drill & simulation services

- 9.4.1 PROFESSIONAL SERVICES

10 MASS NOTIFICATION SYSTEM MARKET, BY COMMUNICATION MODE

- 10.1 INTRODUCTION

- 10.1.1 DRIVERS: MASS NOTIFICATION SYSTEM MARKET, BY COMMUNICATION MODE

- 10.2 AUDITORY COMMUNICATION

- 10.2.1 COMPLIANCE-LED MODERNIZATION OF IN-BUILDING EMERGENCY VOICE INFRASTRUCTURE TO BOOST SEGMENT

- 10.3 TEXT-BASED COMMUNICATION

- 10.3.1 HIGH-REACH, VERIFIABLE ALERT DISTRIBUTION ACROSS DECENTRALIZED OPERATING ENVIRONMENTS - KEY DRIVER

- 10.4 MULTIMODAL COMMUNICATION

- 10.4.1 SEGMENT DRIEN BY REDUNDANCY-CENTRIC COMMUNICATION ARCHITECTURE FOR HIGH-IMPACT INCIDENT ENVIRONMENTS

11 MASS NOTIFICATION SYSTEM MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.1.1 APPLICATION: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 11.2 EMERGENCY & CRISIS NOTIFICATION

- 11.2.1 IMMEDIATE ACTIVATION OF LIFE-SAFETY ALERTS AND GUIDED EMERGENCY RESPONSE COMMUNICATION - KEY SEGMENT DRIVER

- 11.3 CRITICAL EVENT & INCIDENT MANAGEMENT

- 11.3.1 NEED FOR COORDINATION OF CROSS-FUNCTIONAL RESPONSE AND ESCALATION WORKFLOWS DURING DISRUPTIVE EVENTS TO BOOST SEGMENT

- 11.4 PUBLIC SAFETY & GOVERNMENT ALERTING

- 11.4.1 DELIVERY OF GEO-TARGETED PUBLIC WARNING MESSAGES THROUGH NATIONAL ALERT FRAMEWORKS TO DRIVE GROWTH

- 11.5 BUSINESS CONTINUITY & ORGANIZATIONAL RESILIENCE

- 11.5.1 MAINTAINING OPERATIONAL STABILITY THROUGH STRUCTURED CONTINUITY COMMUNICATIONS - KEY ROLE OF SEGMENT

- 11.6 OPERATIONAL & IT ALERTING

- 11.6.1 NOTIFYING TECHNICAL TEAMS OF SYSTEM FAILURES AND INFRASTRUCTURE DISRUPTIONS

- 11.7 PREPAREDNESS, TRAINING, AND DRILLS

- 11.7.1 CONDUCTING SCHEDULED TEST ALERTS AND EMERGENCY SIMULATION EXERCISES

- 11.8 AWARENESS, INFORMATION, AND ADMINISTRATIVE COMMUNICATION

- 11.8.1 DISTRIBUTION OF NON-EMERGENCY UPDATES AND ORGANIZATIONAL ANNOUNCEMENTS AT SCALE TO BOOST GROWTH

- 11.9 OTHER APPLICATIONS

- 11.9.1 NEED FOR COORDINATION IN LARGE-SCALE PUBLIC EVENTS AND COMMUNITY ENGAGEMENT CAMPAIGNS TO DRIVE SEGMENT

12 MASS NOTIFICATION SYSTEM MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.1.1 END USER: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 12.2 GOVERNMENT & PUBLIC SECTOR

- 12.2.1 FEDERAL, STATE, AND LOCAL GOVERNMENT AGENCIES

- 12.2.1.1 Modernization of public alert infrastructure strengthens citizen reach and continuity of government operations

- 12.2.2 EMERGENCY MANAGEMENT & CIVIL DEFENSE AUTHORITIES

- 12.2.2.1 Rising climate and disaster risks accelerate deployment of integrated early warning and mass alert systems

- 12.2.3 MILITARY & DEFENSE

- 12.2.3.1 Escalating security threats to drive investment in secure installation-wide notification and personnel accountability systems

- 12.2.4 PUBLIC SAFETY & LAW ENFORCEMENT AGENCIES

- 12.2.4.1 Growing urban incident complexity increases demand for real-time multi-channel emergency communication platforms

- 12.2.5 COURTS, CIVIC, AND PUBLIC INFRASTRUCTURE

- 12.2.5.1 Heightened public safety and infrastructure risk exposure to boost adoption

- 12.2.1 FEDERAL, STATE, AND LOCAL GOVERNMENT AGENCIES

- 12.3 COMMERCIAL END USERS

- 12.3.1 CORPORATE OFFICES & ENTERPRISE CAMPUSES

- 12.3.1.1 Need for workforce safety and ensuring business continuity across enterprise locations to propel segment

- 12.3.2 BFSI

- 12.3.2.1 Managing operational risk and regulatory compliance in financial services to drive growth

- 12.3.3 HEALTHCARE PROVIDERS

- 12.3.3.1 Coordinating patient safety and clinical operations in healthcare facilities

- 12.3.4 EDUCATIONAL INSTITUTIONS

- 12.3.4.1 Need to strengthen campus safety and academic continuity to boost segment

- 12.3.5 TRANSPORTATION & TRANSIT OPERATORS

- 12.3.5.1 Segment driven by need to manage passenger safety and service disruptions across transit networks

- 12.3.6 DATA CENTERS & MISSION-CRITICAL FACILITIES

- 12.3.6.1 Safeguarding infrastructure resilience and operational uptime

- 12.3.7 HOSPITALITY & CONSUMER-FACING VENUES

- 12.3.7.1 Enhancing guest safety and operational coordination in public venues

- 12.3.8 RETAIL & E-COMMERCE OPERATORS

- 12.3.8.1 Managing store operations, workforce safety, and customer communication across retail networks

- 12.3.1 CORPORATE OFFICES & ENTERPRISE CAMPUSES

- 12.4 INDUSTRIAL END USERS

- 12.4.1 MANUFACTURING PLANTS & INDUSTRIAL CAMPUSES

- 12.4.1.1 Rising automation and workplace risk complexity drive deployment of real-time plant-wide mass notification systems

- 12.4.2 ENERGY & UTILITIES

- 12.4.2.1 Grid modernization and infrastructure vulnerability increase investment in critical event notification and incident response systems

- 12.4.3 OIL, GAS, AND CHEMICAL/PROCESS INDUSTRIES

- 12.4.3.1 High-consequence operational environments accelerate adoption of integrated hazard and emergency communication platforms

- 12.4.4 LOGISTICS, WAREHOUSING, AND DISTRIBUTION CENTERS

- 12.4.4.1 Expanding distribution networks elevate demand for workforce coordination and facility-wide alert systems

- 12.4.5 MINING & HEAVY INDUSTRY SITES

- 12.4.5.1 Remote and high-risk operations fuel need for reliable, multi-channel emergency communication infrastructure

- 12.4.6 CONSTRUCTION & LARGE-SCALE INFRASTRUCTURE PROJECTS

- 12.4.6.1 Large, multi-contractor project environments increase dependence on centralized safety and incident notification systems

- 12.4.1 MANUFACTURING PLANTS & INDUSTRIAL CAMPUSES

13 MASS NOTIFICATION SYSTEM MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 13.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 13.2.3 US

- 13.2.3.1 Mature, multi-layered MNS ecosystem driven by stringent regulations, enterprise risk management, and high-frequency threat scenarios

- 13.2.4 CANADA

- 13.2.4.1 Centrally coordinated, mobile-first notification system supported by national public warning frameworks and steady enterprise adoption

- 13.3 EUROPE

- 13.3.1 EUROPE: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 13.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 13.3.3 UK

- 13.3.3.1 Government-led strategy and defense partnerships to accelerate advanced alert notification system adoption

- 13.3.4 GERMANY

- 13.3.4.1 Federal scale modernization with strong public sector dominance to drive market

- 13.3.5 FRANCE

- 13.3.5.1 Centralized public warning systems key to enterprise expansion

- 13.3.6 ITALY

- 13.3.6.1 Disaster resilience to lead growth with phased enterprise uptake

- 13.3.7 REST OF EUROPE

- 13.3.7.1 Climate risk and mobile alert modernization to accelerate public and enterprise MNS adoption

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 13.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 13.4.3 CHINA

- 13.4.3.1 National early warning powerhouse with multi-channel dominance to drive market

- 13.4.4 INDIA

- 13.4.4.1 Nationwide, multilingual public warning at population scale to boost market

- 13.4.5 JAPAN

- 13.4.5.1 Highly automated national instant warning system with multi-channel reach - key driver

- 13.4.6 ASEAN

- 13.4.6.1 Precision-driven, smart nation-aligned emergency communication to drive market

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 13.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 13.5.3 SAUDI ARABIA

- 13.5.3.1 National emergency testing and expanding alert readiness - key drivers

- 13.5.4 UAE

- 13.5.4.1 Market driven by smart city emergency communication at population scale

- 13.5.5 TURKEY

- 13.5.5.1 Disaster management modernization with multi-stage public warning evolution to drive market

- 13.5.6 SOUTH AFRICA

- 13.5.6.1 Urban risk and infrastructure resilience to drive growth

- 13.5.7 REST OF MIDDLE EAST & AFRICA

- 13.6 LATIN AMERICA

- 13.6.1 LATIN AMERICA: MASS NOTIFICATION SYSTEM MARKET DRIVERS

- 13.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 13.6.3 BRAZIL

- 13.6.3.1 Rapid commercial and municipal MNS uptake driven by public-warning upgrades and private-sector investment

- 13.6.4 MEXICO

- 13.6.4.1 Government push for cell broadcast and city-level drills accelerates mobile-first alerts

- 13.6.5 REST OF LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES, 2021-2025

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 MARKET RANKING ANALYSIS, 2025

- 14.5 BRAND COMPARATIVE ANALYSIS

- 14.5.1 BRAND COMPARATIVE ANALYSIS: NOTIFICATION DEVICES

- 14.5.2 BRAND COMPARATIVE ANALYSIS: SOFTWARE

- 14.6 COMPANY EVALUATION MATRIX: TIER 1 SOFTWARE VENDORS

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 COMPANY FOOTPRINT: TIER 1 SOFTWARE VENDORS, 2025

- 14.6.3.1 Company footprint

- 14.6.3.2 Regional footprint

- 14.6.3.3 Offering footprint

- 14.6.3.4 Communication mode footprint

- 14.6.3.5 Application footprint

- 14.6.3.6 End user footprint

- 14.7 COMPANY EVALUATION MATRIX: TIER 2 SOFTWARE VENDORS

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: TIER 2 SOFTWARE VENDORS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Regional footprint

- 14.7.5.3 Offering footprint

- 14.7.5.4 Communication mode footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: NOTIFICATION DEVICE VENDORS

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 COMPANY FOOTPRINT: NOTIFICATION DEVICE VENDORS, 2025

- 14.8.3.1 Company footprint

- 14.8.3.2 Regional footprint

- 14.8.3.3 Offering footprint

- 14.8.3.4 Communication mode footprint

- 14.8.3.5 Application footprint

- 14.8.3.6 End user footprint

- 14.9 COMPANY VALUATION AND FINANCIAL METRICS

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 14.10.2 DEALS

15 COMPANY PROFILES

- 15.1 INTRODUCTION

- 15.2 KEY NOTIFICATION DEVICE PROVIDERS

- 15.2.1 MOTOROLA SOLUTIONS

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Product launches and enhancements

- 15.2.1.3.2 Deals

- 15.2.1.4 MnM view

- 15.2.1.4.1 Key strengths

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses and competitive threats

- 15.2.2 SIEMENS AG

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches and enhancements

- 15.2.2.4 MnM view

- 15.2.2.4.1 Key strengths

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses and competitive threats

- 15.2.3 HONEYWELL

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches and enhancements

- 15.2.3.3.2 Deals

- 15.2.3.4 MnM view

- 15.2.3.4.1 Key strengths

- 15.2.3.4.2 Strategic choices

- 15.2.3.4.3 Weaknesses and competitive threats

- 15.2.4 EATON

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches and enhancements

- 15.2.4.4 MnM view

- 15.2.4.4.1 Key strengths

- 15.2.4.4.2 Strategic choices

- 15.2.4.4.3 Weaknesses and competitive threats

- 15.2.5 JOHNSON CONTROLS

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches and enhancements

- 15.2.5.3.2 Deals

- 15.2.5.4 MnM view

- 15.2.5.4.1 Key strengths

- 15.2.5.4.2 Strategic choices

- 15.2.5.4.3 Weaknesses and competitive threats

- 15.2.6 MICROM

- 15.2.6.1 Business overview

- 15.2.6.2 Products/Solutions/Services offered

- 15.2.6.3 Recent developments

- 15.2.6.3.1 Product launches and enhancements

- 15.2.6.3.2 Deals

- 15.2.7 AMERICAN SIGNAL CORPORATION

- 15.2.7.1 Business overview

- 15.2.7.2 Products/Solutions/Services offered

- 15.2.7.3 Recent developments

- 15.2.7.3.1 Product launches and enhancements

- 15.2.7.3.1.1 Deals

- 15.2.7.3.1 Product launches and enhancements

- 15.2.1 MOTOROLA SOLUTIONS

- 15.3 OTHER NOTIFICATION DEVICE PROVIDERS

- 15.3.1 KLAXON SIGNALS

- 15.3.2 ALERTUS TECHNOLOGIES

- 15.3.3 ATI SYSTEMS

- 15.4 KEY SOFTWARE PROVIDERS

- 15.4.1 EVERBRIDGE

- 15.4.1.1 Business overview

- 15.4.1.2 Products/Solutions/Services offered

- 15.4.1.3 Recent developments

- 15.4.1.3.1 Product launches and enhancements

- 15.4.1.3.2 Deals

- 15.4.2 SINGLEWIRE SOFTWARE

- 15.4.2.1 Business overview

- 15.4.2.2 Products/Solutions/Services offered

- 15.4.2.3 Recent developments

- 15.4.2.3.1 Product launches and enhancements

- 15.4.2.3.2 Deals

- 15.4.3 CRISIS24

- 15.4.3.1 Business overview

- 15.4.3.2 Products/Solutions/Services offered

- 15.4.3.3 Recent developments

- 15.4.3.3.1 Product launches and enhancements

- 15.4.3.3.2 Deals

- 15.4.1 EVERBRIDGE

- 15.5 OTHER SOFTWARE PROVIDERS

- 15.5.1 ALERTMEDIA

- 15.5.2 BLACKBERRY

- 15.5.3 F24 AG

- 15.5.4 HIPLINK

- 15.5.5 FINALSITE

- 15.5.6 OMNILERT

- 15.5.7 REGROUP MASS NOTIFICATION

- 15.5.8 KONEXUS

- 15.5.9 NETPRESENTER

- 15.5.10 ILUMINR

- 15.5.11 CRISISGO

- 15.5.12 OMNIGO

- 15.5.13 CRISES CONTROL

- 15.5.14 ICESOFT TECHNOLOGIES

- 15.5.15 SQUADCAST

- 15.5.16 REDFLAG ALERTS

- 15.5.17 PREPARIS (MITRATECH)

- 15.5.18 HQE SYSTEMS

- 15.5.19 VEOCI

- 15.5.20 TEXT-EM-ALL

- 15.5.21 DIALMYCALLS

- 15.5.22 RUVNA

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Breakup of primary profiles

- 16.1.2.2 Key industry insights

- 16.2 MARKET BREAKUP AND DATA TRIANGULATION

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 TOP-DOWN APPROACH

- 16.3.2 BOTTOM-UP APPROACH

- 16.4 MARKET FORECAST

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 STUDY LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS