|

시장보고서

상품코드

1963143

극저온 장비 시장 : 장비별, 극저온 매체별, 최종 이용 산업별, 시스템 유형별, 용도별, 지역별 - 세계 예측(-2030년)Cryogenic Equipment Market by Equipment (Tanks, Valves, Vaporizers, Pumps), Cryogen (Nitrogen, Argon, Oxygen, LNG, Hydrogen), End-user Industry (Energy & Power, Chemical, Metallurgy, Transportation), System Type, Application, & Region - Forecast to 2030 |

||||||

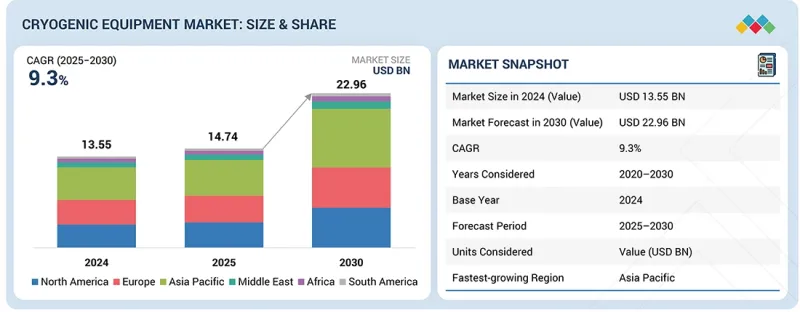

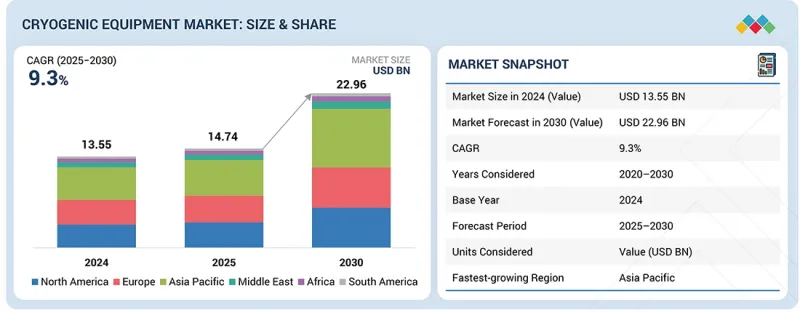

세계의 극저온 장비 시장 규모는 2024년 135억 5,000만 달러에서 2030년까지 229억 6,000만 달러에 달할 것으로 예측되며, CAGR로 9.3%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 장비, 극저온 매체, 최종 이용 산업, 시스템 유형, 용도, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

이러한 성장은 야금, 석유 및 가스, 에너지 및 전력 산업에서 산업용 가스의 사용 증가 등의 요인에 기인합니다. 깨끗하고 효율적인 에너지원인 액화천연가스의 보급이 극저온 장비 시장의 성장을 촉진하고 있습니다.

"최종 사용 산업별로는 전자 부문이 예측 기간 동안 극저온 장비 시장에서 가장 빠르게 성장할 것으로 예상됩니다."

전자 부문은 예측 기간 동안 극저온 장비 시장에서 가장 빠르게 성장하는 부문이 될 것으로 예상됩니다. 전자 산업에서는 질소, 산소, 아르곤 등 고순도 산업용 가스의 저장 및 취급에 극저온 장비가 널리 사용되고 있습니다. 이들 가스는 반도체 제조, 집적 회로, 평판 디스플레이, 인쇄회로기판에 필수적인 가스입니다. 그 중요성은 적용되는 중요한 제조 공정에 기인합니다. 특히 웨이퍼 냉각, 불활성화, 산화, 성막, 가공 등의 공정에서 오염 없는 환경에서 정밀한 온도 관리가 필수적이기 때문입니다. 전자장비, 전기자동차, 데이터센터, 첨단 컴퓨팅 시설에 대한 광범위한 소비자 니즈에 따른 수요가 반도체 생산능력 확대에 대한 수요를 촉진하고 있습니다. 또한, 이는 신뢰할 수 있는 극저온 가스 공급 시스템에 대한 수요를 뒷받침하고 있습니다. 칩의 미세화, 고밀도 실장, 차세대 전자재료의 지속적인 발전도 수요 증가를 보완적으로 촉진하고 있습니다. 전자장비 생산 활동이 복잡해지고 품질에 대한 요구가 높아짐에 따라, 이 분야에서는 이러한 장비의 채택이 점차 증가할 것으로 보입니다.

"시스템 유형별로는 스토리지 시스템 부문이 예측 기간 동안 가장 큰 부문이 될 것으로 예상됩니다."

저장 시스템 부문은 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이 부문의 큰 시장 점유율과 높은 성장률은 확대되는 항공우주 산업과 극저온 에너지 저장(CES) 시스템의 기술 발전이 가져다주는 수익성 높은 성장 기회에 기인하는 것으로 보입니다.

지역별로는 유럽이 예측 기간 동안 극저온 장비 시장에서 두 번째로 큰 규모를 차지할 것으로 예상됩니다.

유럽은 예측 기간 동안 극저온 장비 시장에서 두 번째로 큰 시장 규모가 될 것으로 예상됩니다. 유럽 시장은 주로 독일의 의료 산업 현대화와 프랑스의 순배출량 제로 목표 달성을 위한 노력에 영향을 받고 있습니다. LNG 수출에 대한 투자가 증가함에 따라 운송 산업, 특히 해운 부문의 극저온 장비에 대한 수요가 증가하여 이 지역의 극저온 장비 공급업체에게 유리한 성장 기회를 제공할 수 있습니다.

세계의 극저온 장비 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황과 지속가능성에 관한 대처

제8장 고객 상황과 구매 행동

제9장 극저온 장비 시장 : 장비별

제10장 극저온 장비 시장 : 극저온 매체별

제11장 극저온 장비 시장 : 시스템 유형별

제12장 극저온 장비 시장 : 용도별

제13장 극저온 장비 시장 : 최종 이용 산업별

제14장 극저온 장비 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.03.20The cryogenic equipment market is projected to reach USD 22.96 billion by 2030 from USD 13.55 billion in 2024, at a CAGR of 9.3%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | by Equipment, Cryogen, End-user Industry, System Type, Application & Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East, Africa, South America |

The growth is attributed to the factors such as Increasing utilization of industrial gases in metallurgy, oil & gas, and energy & power industries. Growing popularity of liquefied natural gas as source of clean and efficient energy has driven the growth of cryogenic equipment market.

"By end-user industry, Electronics segment is projected to be the fastest growing segment of the cryogenic equipment market during the forecast period."

The electronics segment is expected to be the fastest-growing end-user segment in the cryogenic equipment market during the forecast period. In the electronics industry, cryogenic equipment is used widely in the storage and handling of high-purity industrial gases such as nitrogen, oxygen, and argon. These gases are essential in semiconductor fabrication, integrated circuits, flat-panel displays, and printed circuit boards. Their critical importance arises from the important manufacturing processes for which they are to be applied: wafer cooling, inerting, oxidation, deposition, and processing, where precise temperatures must be maintained in an environment free of contamination. The demand owing to extensive consumer need for electronics, electric vehicles, data centers, and advanced computing facilities raises the demand for an infusion of production capacity for semiconductors. It also substantiates a demand for reliable supply systems for cryogenic gases. Continuous advancements in chip miniaturization, high-density packaging, and.next-generation electronic materials are complementary contributors to increased demand. As the activities in electronics production increase in complexity and continue to be quality-driven, more of such equipment will surely be adopted gradually in this segment.

"Storage system segment is expected to be the largest segment during the forecast period based on system type."

By system type, the cryogenic equipment market has been segmented into storage system, handling system, supply system, and others. The storage system segment is expected to hold the largest market share during the forecast period. The large market share and the high growth rate of this segment can be attributed to the lucrative growth opportunities provided by the expanding aerospace industry and technological advancements in cryogenic energy storage (CES) systems.

.

"By region, Europe is expected to be the second-largest region in the cryogenic equipment market during the forecast period."

Europe is expected to be the second-largest region in the cryogenic equipment market during the forecast period. The region has been segmented, by country, into Russia, the UK, Germany, France, and Rest of Europe. The market in Rest of Europe is primarily studied for the Netherlands, Italy, Norway, Sweden, Denmark, and Finland. The European market is mainly influenced by the modernization of Germany's healthcare industry and France's commitment to achieving net-zero emissions. the increasing investments in LNG exports are likely to create requirement for cryogenic equipment in the transportation industry, especially the shipping sector, thereby providing a lucrative growth opportunity for cryogenic equipment providers in the region.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3- 11%

By Designation: C-Level Executives - 30%, Managers- 25%, and Others- 45%

By Region North America- 27%, Europe- 20%, Asia Pacific- 33%, South America- 12%, The Middle East- 4% and Africa- 4%

Note: Others include product engineers, product specialists, and engineering leads.

Note: The tiers of the companies are defined based on their total revenues as of 2024. Tier 1: > USD 1 billion, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: < USD 500 million

The cryogenic equipment market is dominated by a few major players that have a wide regional presence. The leading players in the cryogenic equipment market are Linde plc (Ireland); Air Liquide (France); Air Products and Chemicals, Inc. (US); Chart Industries (US); and PARKER HANNIFIN CORP (US), among others.

Study Coverage:

The report defines, describes, and forecasts the global cryogenic equipment market by Equipment, Cryogen, End-user Industry, System Type, and Region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the cryogenic equipment market.

Key Benefits of Buying the Report

- The cryogenic equipment market is driven by a global trend toward cleaner, more efficient energy and industrial systems where ultra-low-temperature handling is key. Increased liquefied gas demand in relation to LNG, hydrogen, industrial gases, and energy security and emission reductions spurred the rapid adoption of cryogenic tanks, valves, pumps, and vaporizers. Many features of cryogenic equipment include safe liquefaction, storage, and transportation of gases-lending itself to LNG infrastructure development, hydrogen deployment, industrial processing, and medical applications. Another crucial and worth-noting feature of cryogenic equipment is that their inherent compatibility with existing gas value chains allows flexibility across energy, industrial, and transport sectors. The tighter safety and environmental regulations are complemented with the government push for clean fuels, thus propelling investment into cryogenic infrastructure. Meanwhile, advancement in insulation, materials, automation, and digital monitoring for better efficiency, reliability, and scalability would make cryogenic equipment a significant enabling infrastructure for low-carbon energy transition.

- Product Development/Innovation: The cryogenic equipment market is witnessing significant product development and innovation, driven by the growing demand for cryogenic equipment systems in the metallurgy industries. Companies are investing in developing advanced cryogenic equipments.

- Market Development: INOX India Limited built an LNG facility in Tamil Nadu, which comprises 2 x 113 KL LNG tanks, regas system with a capacity of 5,000 SCMH @ 22 Bar pressure and associated equipment was supplied by INOXCVA on a turnkey basis in a record time.

- Market Diversification: Chart Industries collaborated with 8 Rivers Capital, a North Carolina-based clean energy and climate technology company, to grab commercial opportunities for hydrogen technology and solutions. This collaboration includes developing equipment for 8 Rivers technologies backed up by Chart's decades of experience in designing and manufacturing cryogenic, compression, and process technologies, and help 8 Rivers in delivering reliable and cost-effective solutions to its customers. The companies will work together to identify and develop commercial opportunities to integrate Chart offerings into 8 Rivers's projects.

- Competitive Assessment: Assessment of rankings of some of the key players, including of Linde plc (Ireland); Air Liquide (France); Air Products and Chemicals, Inc. (US); Chart Industries (US); and PARKER HANNIFIN CORP (US), among others in the cryogenic equipment market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CRYOGENIC EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CRYOGENIC EQUIPMENT MARKET

- 3.2 CRYOGENIC EQUIPMENT MARKET, BY REGION

- 3.3 CRYOGENIC EQUIPMENT MARKET, BY SYSTEM TYPE

- 3.4 CRYOGENIC EQUIPMENT MARKET, BY CRYOGEN

- 3.5 CRYOGENIC EQUIPMENT MARKET, BY EQUIPMENT

- 3.6 CRYOGENIC EQUIPMENT MARKET, BY END-USE INDUSTRY

- 3.7 CRYOGENIC EQUIPMENT MARKET, BY APPLICATION

- 3.8 CRYOGENIC EQUIPMENT MARKET IN ASIA PACIFIC, BY SYSTEM TYPE AND COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising industrial gas consumption and data center expansion

- 4.2.1.2 Increasing investment in LNG projects to support clean energy transition

- 4.2.2 RESTRAINTS

- 4.2.2.1 High CAPEX and OPEX associated with cryogenic plants

- 4.2.2.2 Volatile raw material and metal prices

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising adoption of cryogenic fuels in space and advanced electronics applications

- 4.2.3.2 Increasing global hydrogen demand

- 4.2.4 CHALLENGES

- 4.2.4.1 Health hazards and environmental implications

- 4.2.4.2 Supply chain disruptions due to geopolitical tensions

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF SUBSTITUTES

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.1.1 Global energy investment trends

- 5.2.1.2 Hydrogen economy investment and capacity additions

- 5.2.1.3 Healthcare and life sciences expenditure

- 5.2.1.4 Tariffs, interest rates, and financing conditions

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL SPACE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL OIL & GAS INDUSTRY

- 5.2.1 INTRODUCTION

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 EXPORT SCENARIO (HS CODE 280410)

- 5.5.2 IMPORT SCENARIO (HS CODE 280410)

- 5.5.3 EXPORT SCENARIO (HS CODE 280430)

- 5.5.4 IMPORT SCENARIO (HS CODE 280430)

- 5.5.5 EXPORT SCENARIO (HS CODE 280421)

- 5.5.6 IMPORT SCENARIO (HS CODE 280421)

- 5.5.7 EXPORT SCENARIO (HS CODE 280440)

- 5.5.8 IMPORT SCENARIO (HS CODE 280440)

- 5.5.9 EXPORT SCENARIO (HS CODE 271111)

- 5.5.10 IMPORT SCENARIO (HS CODE 271111)

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 CRYOSTAR ADOPTS HEXAGON PPM SOLUTIONS TO IMPROVE CRYOGENIC PROJECT EFFICIENCY AND REDUCE REWORK

- 5.6.2 CES USES SOLIDWORKS PROFESSIONAL 3D DESIGN SOFTWARE TO ENHANCE CRYOGENIC EQUIPMENT DESIGN AND ACCURACY

- 5.6.3 SEMICONDUCTOR PLANT IN SINGAPORE INSTALLS ALCATRAZ INTERLOCKS' MECHANICAL INTERLOCK SYSTEM TO ELIMINATE HUMAN ERROR IN CRYOGENIC VALVE OPERATIONS

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND OF CRYOGENIC EQUIPMENT, BY EQUIPMENT, 2020-2024

- 5.8.2 AVERAGE SELLING PRICE TREND OF CRYOGENIC EQUIPMENT, BY REGION, 2020-2024

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFF - CRYOGENIC EQUIPMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 VACUUM-INSULATED/MULTI-LAYER CONTAINMENT AND THERMAL INSULATION SYSTEMS

- 6.1.2 CRYOGENIC VALVES AND LOW-TEMPERATURE ACTUATORS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BOIL-OFF GAS (BOG) MANAGEMENT AND RELIQUEFACTION SYSTEMS

- 6.2.2 VACUUM PUMPS, INSULATION TESTING SYSTEMS, AND MAINTENANCE TOOLS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 LNG INFRASTRUCTURE (LIQUEFACTION, SHIPPING, AND REGASIFICATION)

- 6.3.2 HYDROGEN LIQUEFACTION AND LIQUID HYDROGEN STORAGE SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON CRYOGENIC EQUIPMENT MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN CRYOGENIC EQUIPMENT MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN CRYOGENIC EQUIPMENT MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI/GEN AI IN CRYOGENIC EQUIPMENT MARKET

- 6.7.6 AI-ENABLED AUTONOMOUS OPTIMIZATION AND ADVANCED CONTROL OF LARGE-SCALE CRYOGENIC PLANTS

- 6.7.7 ENTERPRISE-WIDE PREDICTIVE MAINTENANCE AND AI-DRIVEN RELIABILITY FOR CRYOGENIC PRODUCTION ASSETS

- 6.7.8 DIGITAL TWIN AND PRESCRIPTIVE ANALYTICS FOR PERFORMANCE ENHANCEMENT OF CRYOGENIC ROTATING EQUIPMENT

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 BOIL-OFF GAS (BOG) CAPTURE AND RELIQUEFACTION

- 7.2.2 ENERGY-EFFICIENT LIQUEFACTION

- 7.2.3 LOW GLOBAL WARMING POTENTIAL (GWP) REFRIGERANT AND LEAK REDUCTION

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE AND BUYING BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 CRYOGENIC EQUIPMENT MARKET, BY EQUIPMENT

- 9.1 INTRODUCTION

- 9.2 TANKS

- 9.2.1 EXPANDING LNG PRODUCTION, TRANSPORTATION, AND STORAGE INFRASTRUCTURE TO FUEL SEGMENTAL GROWTH

- 9.3 VALVES

- 9.3.1 RISING DEVELOPMENT OF HYDROGEN INFRASTRUCTURE AND INDUSTRIAL GAS PROCESSING FACILITIES TO SPUR DEMAND

- 9.4 VAPORIZERS

- 9.4.1 INCREASING INDUSTRIAL GAS CONSUMPTION AND TECHNOLOGICAL ADVANCES TO FOSTER SEGMENTAL GROWTH

- 9.5 PUMPS

- 9.5.1 RAPID EXPANSION OF LNG IMPORT AND EXPORT TERMINALS TO ACCELERATE SEGMENTAL GROWTH

- 9.6 OTHER EQUIPMENT

10 CRYOGENIC EQUIPMENT MARKET, BY CRYOGEN

- 10.1 INTRODUCTION

- 10.2 NITROGEN

- 10.2.1 INCREASING ELECTRONICS AND SEMICONDUCTOR MANUFACTURING TO FACILITATE SEGMENTAL GROWTH

- 10.3 ARGON

- 10.3.1 RAPID EXPANSION OF FABRICATION FACILITIES AND ADVANCED MANUFACTURING HUBS TO AUGMENT SEGMENTAL GROWTH

- 10.4 OXYGEN

- 10.4.1 INCREASING INVESTMENT IN LOW-CARBON INDUSTRIAL GAS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 10.5 LNG

- 10.5.1 ENERGY SECURITY CONCERNS AND FUEL DIVERSIFICATION STRATEGIES TO FOSTER SEGMENTAL GROWTH

- 10.6 HYDROGEN

- 10.6.1 GROWING EMPHASIS ON NET-ZERO CARBON COMMITMENTS TO BOLSTER SEGMENTAL GROWTH

- 10.7 OTHER CRYOGENS

11 CRYOGENIC EQUIPMENT MARKET, BY SYSTEM TYPE

- 11.1 INTRODUCTION

- 11.2 STORAGE SYSTEMS

- 11.2.1 HIGH EMPHASIS ON EXPANDING LNG STORAGE CAPACITY TO ACCELERATE SEGMENTAL GROWTH

- 11.3 HANDLING SYSTEMS

- 11.3.1 RISING LNG TRADE VOLUMES AND TERMINAL UTILIZATION RATES TO FUEL SEGMENTAL GROWTH

- 11.4 SUPPLY SYSTEMS

- 11.4.1 MOUNTING ADOPTION OF ON-SITE AIR SEPARATION UNITS TO EXPEDITE SEGMENTAL GROWTH

- 11.5 OTHER SYSTEMS

12 CRYOGENIC EQUIPMENT MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 CASU

- 12.2.1 NEED FOR CONTINUOUS GENERATION OF INDUSTRIAL GASES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.3 NON-CASU

- 12.3.1 RAIL & ROAD TRANSPORT INDUSTRY

- 12.3.1.1 Increasing merchant industrial gas distribution and healthcare oxygen logistics to drive market

- 12.3.2 LNG BULK CARRIER SHIPS

- 12.3.2.1 Rising global LNG trade and fleet expansion to bolster segmental growth

- 12.3.3 LNG REGASIFICATION & LIQUEFACTION TERMINALS

- 12.3.3.1 Rapid expansion of floating storage and regasification units to expedite segmental growth

- 12.3.4 OTHER MINOR END USES

- 12.3.1 RAIL & ROAD TRANSPORT INDUSTRY

13 CRYOGENIC EQUIPMENT MARKET, BY END-USE INDUSTRY

- 13.1 INTRODUCTION

- 13.2 METALLURGY

- 13.2.1 REQUIREMENT FOR PRECISE REGULATION OF GAS FLOW AND TEMPERATURE TO AUGMENT SEGMENTAL GROWTH

- 13.3 ENERGY & POWER

- 13.3.1 STRONG FOCUS ON MAINTAINING ZERO-RESISTANCE CONDITIONS TO FOSTER SEGMENTAL GROWTH

- 13.4 CHEMICALS

- 13.4.1 HEAVY RELIANCE ON HIGH-PURITY INDUSTRIAL GASES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 13.5 ELECTRONICS

- 13.5.1 NEED FOR CONTAMINATION-FREE ENVIRONMENTS FOR SEMICONDUCTOR MATERIAL FABRICATION TO DRIVE MARKET

- 13.6 TRANSPORTATION

- 13.6.1 SHIPPING

- 13.6.1.1 Expanding LNG bunkering networks and strict emission rules to augment segmental growth

- 13.6.2 RAIL & ROAD TRANSPORT

- 13.6.2.1 Long-haul decarbonization targets and fleet conversions to LNG and hydrogen to drive market

- 13.6.1 SHIPPING

- 13.7 OTHER END-USE INDUSTRIES

14 CRYOGENIC EQUIPMENT MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 ASIA PACIFIC

- 14.2.1 CHINA

- 14.2.1.1 Increasing LNG imports and large-scale industrial manufacturing to boost market growth

- 14.2.2 INDIA

- 14.2.2.1 Rapid industrialization and expanding healthcare infrastructure to drive market

- 14.2.3 AUSTRALIA

- 14.2.3.1 Rising LNG production and mining-linked industrial activity to augment market growth

- 14.2.4 JAPAN

- 14.2.4.1 Increasing investment in LNG infrastructure and hydrogen supply-chain demonstration projects to fuel market growth

- 14.2.5 MALAYSIA

- 14.2.5.1 Growing focus on upgrading gas storage and processing infrastructure to accelerate market growth

- 14.2.6 REST OF ASIA PACIFIC

- 14.2.1 CHINA

- 14.3 EUROPE

- 14.3.1 RUSSIA

- 14.3.1.1 Increasing upgrade and replacement of legacy gas processing equipment to contribute to market growth

- 14.3.2 UK

- 14.3.2.1 Rising energy system innovation to accelerate market growth

- 14.3.3 GERMANY

- 14.3.3.1 Rapid modernization of healthcare infrastructure to bolster market growth

- 14.3.4 FRANCE

- 14.3.4.1 Heightened focus on energy transition and industrial gas adoption to augment market growth

- 14.3.5 REST OF EUROPE

- 14.3.1 RUSSIA

- 14.4 NORTH AMERICA

- 14.4.1 US

- 14.4.1.1 Increasing LNG export and extensive natural gas processing network to foster market growth

- 14.4.2 CANADA

- 14.4.2.1 Growing emphasis on advanced pilot projects related to liquid hydrogen production and storage to drive market

- 14.4.3 MEXICO

- 14.4.3.1 Rising industrial gas consumption and energy infrastructure development to fuel market growth

- 14.4.1 US

- 14.5 MIDDLE EAST

- 14.5.1 GCC

- 14.5.1.1 Saudi Arabia

- 14.5.1.1.1 Expanding gas processing infrastructure and oil export to accelerate market growth

- 14.5.1.2 UAE

- 14.5.1.2.1 Strong focus on low-carbon initiatives and LNG capacity expansion projects to expedite market growth

- 14.5.1.3 Qatar

- 14.5.1.3.1 Growing emphasis on industrial diversification and low-carbon energy to boost market growth

- 14.5.1.4 Rest of GCC

- 14.5.1.1 Saudi Arabia

- 14.5.2 REST OF MIDDLE EAST

- 14.5.1 GCC

- 14.6 AFRICA

- 14.6.1 SOUTH AFRICA

- 14.6.1.1 Increasing reliance on imported LNG and industrial gases to facilitate market growth

- 14.6.2 NIGERIA

- 14.6.2.1 Mounting production of natural gas to contribute to market growth

- 14.6.3 ALGERIA

- 14.6.3.1 Rising gas processing modernization and industrial gas consumption to foster market growth

- 14.6.4 REST OF AFRICA

- 14.6.1 SOUTH AFRICA

- 14.7 SOUTH AMERICA

- 14.7.1 BRAZIL

- 14.7.1.1 Mounting demand for natural gas and industrialization to accelerate market growth

- 14.7.2 ARGENTINA

- 14.7.2.1 Increasing investment in shale gas development to boost market growth

- 14.7.3 VENEZUELA

- 14.7.3.1 Thriving oil & gas industry and recovery in hydrocarbon production to augment market growth

- 14.7.4 REST OF SOUTH AMERICA

- 14.7.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 15.3 MARKET SHARE ANALYSIS, 2024

- 15.4 REVENUE ANALYSIS, 2020-2024

- 15.5 BRAND COMPARISON

- 15.6 COMPANY VALUATION AND FINANCIAL MATRIX

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Equipment footprint

- 15.7.5.4 Cryogen footprint

- 15.7.5.5 System type footprint

- 15.7.5.6 End-use industry footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2024

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

- 15.9.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY COMPANIES

- 16.1.1 AIR LIQUIDE

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 CHART INDUSTRIES

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.3.2 Expansions

- 16.1.2.3.3 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 NIKKISO CO., LTD.

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.3.2 Expansions

- 16.1.3.3.3 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 AIR PRODUCTS AND CHEMICALS, INC.

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Expansions

- 16.1.4.3.3 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 LINDE PLC

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 PARKER HANNIFIN CORP

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product Launches

- 16.1.6.4 MnM view

- 16.1.6.4.1 Key strengths/Right to win

- 16.1.6.4.2 Strategic choices

- 16.1.6.4.3 Weaknesses/Competitive threats

- 16.1.7 FLOWSERVE CORPORATION

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.7.3.2 Other developments

- 16.1.7.4 MnM view

- 16.1.7.4.1 Key strengths/Right to win

- 16.1.7.4.2 Strategic choices

- 16.1.7.4.3 Weaknesses/Competitive threats

- 16.1.8 INOX INDIA LIMITED

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.3.2 Other developments

- 16.1.8.4 MnM view

- 16.1.8.4.1 Key strengths/Right to win

- 16.1.8.4.2 Strategic choices

- 16.1.8.4.3 Weaknesses/Competitive threats

- 16.1.9 EMERSON ELECTRIC CO.

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Expansions

- 16.1.10 ALFA LAVAL

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.11 TAYLOR-WHARTON

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Deals

- 16.1.12 SULZER LTD

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.12.3.2 Expansions

- 16.1.12.3.3 Other developments

- 16.1.13 OPW

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.14 BAKER HUGHES COMPANY

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Expansions

- 16.1.14.3.2 Other developments

- 16.1.15 SLB

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.1 AIR LIQUIDE

- 16.2 OTHER PLAYERS

- 16.2.1 SHI CRYOGENICS GROUP

- 16.2.2 TRILLIUM FLOW TECHNOLOGIES

- 16.2.3 PHPK TECHNOLOGIES

- 16.2.4 SHELL-N-TUBE

- 16.2.5 HEROSE

- 16.2.6 CRYOFAB, INC.

- 16.2.7 CRYOSPAIN

- 16.2.8 WESSINGTON CRYOGENICS

- 16.2.9 CYY ENERGY

- 16.2.10 CRYOGAS EQUIPMENT PRIVATE LIMITED

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY AND PRIMARY RESEARCH

- 17.1.2 SECONDARY DATA

- 17.1.2.1 List of key secondary sources

- 17.1.2.2 Key data from secondary sources

- 17.1.3 PRIMARY DATA

- 17.1.3.1 List of primary interview participants

- 17.1.3.2 Key industry insights

- 17.1.3.3 Breakdown of primaries

- 17.1.3.4 Key data from primary sources

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 17.2.3.1 Demand-side analysis

- 17.2.3.1.1 Demand-side assumptions

- 17.2.3.1.2 Demand-side calculations

- 17.2.3.2 Supply-side analysis

- 17.2.3.2.1 Supply-side assumptions

- 17.2.3.2.2 Supply-side calculations

- 17.2.3.1 Demand-side analysis

- 17.3 FORECAST

- 17.4 DATA TRIANGULATION

- 17.5 FACTOR ANALYSIS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ANALYSIS

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS