|

시장보고서

상품코드

1964924

RFID 안테나 시장 예측(-2032년) : 유형별, 방사 패턴별, 폼팩터별, 용도별RFID Antenna Market by Type (Far-field Antenna, Near-field Antenna), Radiation Pattern (Directional, Omnidirectional), Form Factor (Patch/Panel, Gate, Embedded), and Application (Ticketing, Airport & Baggage Handling) - Global Forecast to 2032 |

||||||

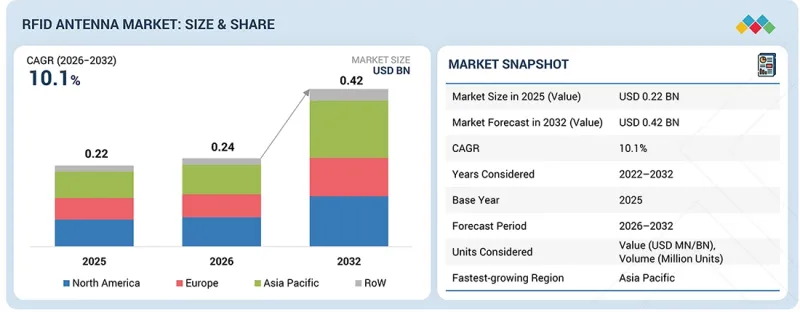

세계의 RFID 안테나 시장 규모는 2026년에 2억 4,000만 달러로, 2032년까지 4억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 10.1%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 10억 달러 |

| 부문 | 유형, 폼팩터, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

"용도별로는 공항 및 수하물 처리 부문이 예측 기간 중 가장 높은 CAGR을 나타낼 것으로 예측됩니다. "

공항 및 수하물 처리 부문은 스마트 공항 인프라에 대한 투자 증가와 정확한 실시간 수하물 추적에 대한 요구로 인해 RFID 안테나 시장에서 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 공항에서는 오처리 감소, 승객 만족도 향상, 운영 효율성 강화를 목적으로 RFID 대응 수하물 처리 시스템 도입이 추진되고 있습니다. 전 세계 항공 여객 수가 증가함에 따라 신뢰할 수 있는 장거리 고속 태그 감지를 실현하는 고성능 RFID 안테나를 이용한 자동 분류, 추적, 보안 검사 시스템에 대한 수요가 증가하고 있습니다. 또한 수하물 추적을 장려하는 규제 요건과 업계 표준, 그리고 공항의 IT 시스템 현대화는 전 세계에서 RFID 안테나 솔루션의 도입을 가속화하고 있습니다.

"배치 유형별로는 고정식 배치가 가장 큰 시장 규모를 차지할 것으로 예측됩니다. "

고정형 전개는 창고, 유통센터, 소매점, 제조공장, 공항 등 영구적이고 수량이 많은 추적 환경에서 광범위하게 사용되어 RFID 안테나 시장에서 가장 큰 시장 규모를 차지하고 있습니다. 고정식 RFID 안테나는 출입문, 컨베이어 벨트, 도크 도어, 생산 라인에 설치되어 수동 개입 없이 연속적이고 자동화된 스캐닝을 실현합니다. 안정적인 판독 성능, 광범위한 범위, ERP 및 WMS와의 통합성을 갖추고 있으며, 대규모 운영에 적합합니다. 또한 공급망 자동화 및 산업용 IoT 인프라에 대한 투자 확대는 고정형 RFID 안테나의 보급을 더욱 촉진하는 요인으로 작용하고 있습니다.

"아시아태평양이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

아시아태평양은 예측 기간 중 RFID 안테나 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 중국, 인도, 일본, 동남아시아의 급속한 산업화, 제조 및 물류 부문의 확대, 자동화 공급망 및 창고 관리 솔루션의 채택 증가가 주요 원인으로 꼽힙니다. 이 지역은 전자, 소매, E-Commerce의 주요 거점으로서 자산 추적, 재고 관리, 수하물 처리를 위한 고성능 RFID 안테나에 대한 수요를 촉진하고 있습니다. 스마트 제조, 디지털화, 인더스트리 4.0 채택을 촉진하는 정부 지원책과 함께 소매업 현대화 및 교통 인프라에 대한 투자 증가는 RFID 안테나 솔루션의 도입을 더욱 가속화하여 아시아태평양을 지배적인 지역 시장으로 만들고 있습니다.

세계의 RFID 안테나 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 상호 연결된 시장과 부문 횡단 기회

- 상호 접속된 시장

- 크로스 부문 기회

- Tier 1/2/3 기업의 전략적 활동

제5장 업계 동향

- Porter의 Five Forces 분석

- 거시경제 전망

- GDP 동향과 예측

- 세계 물류 공급망 업계 동향

- 세계 소매업계 동향

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- RFID 안테나의 평균 판매 가격 동향 : 주요 기업별(2022-2025년)

- RFID 안테나의 평균 판매 가격 동향 : 지역별(2022-2025년)

- 무역 분석

- 수입 시나리오(HS 코드 8523)

- 수출 시나리오(HS 코드 8523)

- 2025년-2026년 주요 컨퍼런스 및 이벤트

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 2025년 미국 관세 영향 - RFID 안테나 시장

- 주요 관세율

- 가격 영향 분석

- 국가/지역에 미치는 영향

- 최종 용도 산업에 미치는 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

- 주요 신기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- RFID 안테나 시장에서 AI의 영향

제7장 규제 상황

- 지역 규정 및 규정 준수

- 규제기관, 정부기관 및 기타 조직

- 산업 표준

제8장 고객 상황과 구매 행동

- 의사결정 프로세스

- 구입자 이해관계자와 구입 평가 기준

- 채택 장벽과 내부 과제

- 다양한 최종 이용 산업으로부터 미충족 요구

제9장 RFID 안테나 시장 : 유형별

- 원거리 안테나

- 근거리 안테나

제10장 RFID 안테나 시장 : 기술별

- 수동 안테나

- 저주파

- 고주파

- 초고주파

- 스마트 안테나

제11장 RFID 안테나 시장 : 방사 패턴별

- 방향성

- 전방향

제12장 RFID 안테나 시장 : 폼팩터별

- 패치/패널

- 다이폴

- 문

- 천장 설치

- 내장형

- 맞춤형/특수

제13장 RFID 안테나 시장 : 배포 유형별

- 고정식

- 이동식

제14장 RFID 안테나 시장 : 용도별

- 재고 및 자산 관리

- 보안 액세스 제어

- 발권 업무

- 공항·수하물 처리

- 기타 용도

제15장 RFID 안테나 시장 : 업계별

- 자동차

- 산업 및 제조

- 의료, 보건 및 제약

- 농업

- 식품 가공

- 소매

- 동물 추적

- 항공우주 및 방위

- 스포츠

- 운송, 물류 및 공급망

- 데이터센터

제16장 RFID 안테나 시장 : 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 폴란드

- 기타

- 남미

- 브라질

- 기타

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주 및 뉴질랜드

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 터키

- 남미

- 기타

제17장 경쟁 구도

- 주요 시장 진출기업의 전략/강점(2022-2026년)

- 매출 분석(2022-2026년)

- 시장 점유율 분석(2025년)

- 제품 비교(2025년)

- 기업 평가 매트릭스 : 주요 시장 진출기업(2025년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2025년)

- 기업 평가와 재무 지표

- 경쟁 시나리오

제18장 기업 개요

- 주요 시장 진출기업

- ZEBRA TECHNOLOGIES CORP.

- TE CONNECTIVITY

- SHANGHAI INLAY LINK INC.(INLAYLINK)

- NEDAP NV

- TIMES-7

- KATHREIN SOLUTIONS GMBH

- PEPPERL+FUCHS SE

- IMPINJ, INC.

- INVENGO INFORMATION TECHNOLOGY CO., LTD.

- CAEN RFID SRL

- MTI WIRELESS EDGE LTD.

- 기타 기업

- GAO RFID INC.

- UNITECH ELECTRONICS CO., LTD.

- CYKEO INFORMATION TECHNOLOGY CO.

- WINNIX TECHNOLOGIES CO., LIMITED PRODUCTS, CORP.

- FLEXIRAY

- IDENTIUM TECH SOLUTIONS

- SYNERGY TELECOM PVT. LTD.

- GREENFUTURZ

- C&T RF ANTENNAS INC.

- E-CARTES TECHNOLOGY PVT. LTD.

- ID TECH

- MANTRA SOFTECH (INDIA) PVT. LTD.

- GLEAM LIGHT INDIA

- KEONN TECHNOLOGIES, SL

- FEIG ELECTRONIC GMBH

제19장 조사 방법

제20장 부록

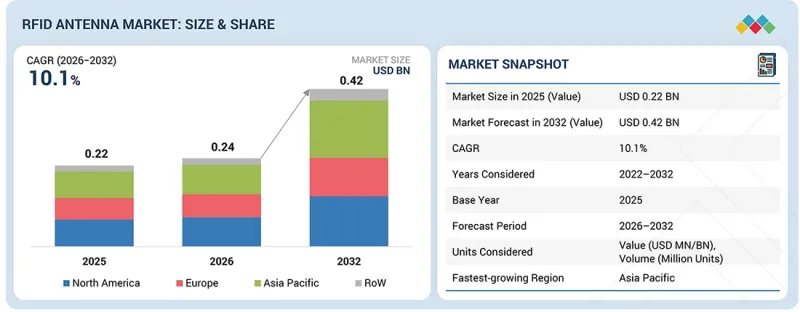

KSA 26.03.24The global RFID antenna market was valued at USD 0.24 billion in 2026 and is projected to reach USD 0.42 billion by 2032, growing at a CAGR of 10.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Form Factor, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Based on Application, Airport & Baggage Handling is expected to witness the highest CAGR during the forecast period."

The airport & baggage handling segment is expected to witness the highest CAGR in the RFID antenna market due to increasing investments in smart airport infrastructure and the need for accurate, real-time baggage tracking. Airports are adopting RFID-enabled baggage handling systems to reduce mishandling, improve passenger satisfaction, and enhance operational efficiency. Growing air passenger traffic worldwide is driving demand for automated sorting, tracking, and security screening systems that rely on high-performance RFID antennas for reliable, long-range, and high-speed tag detection. Additionally, regulatory mandates and industry standards encouraging baggage traceability, along with the modernization of airport IT systems, are accelerating the deployment of RFID antenna solutions globally.

"Based on Deployment Type, Fixed Deployment is expected to hold the largest market size."

The fixed deployment type holds the largest market size in the RFID antenna market due to its widespread use in permanent, high-volume tracking environments such as warehouses, distribution centers, retail stores, manufacturing plants, and airports. Fixed RFID antennas are installed at entry and exit gates, conveyor belts, dock doors, and production lines to enable continuous, automated scanning without manual intervention. Their ability to provide consistent read performance, broader coverage, and integration with enterprise resource planning (ERP) and warehouse management systems (WMS) makes them ideal for large-scale operations. Additionally, growing investments in supply chain automation and industrial IoT infrastructure further drive the adoption of fixed RFID antenna deployments.

"The Asia Pacific is projected to account for the largest market share during the forecast period."

The Asia Pacific region is expected to hold the largest market share in the RFID antenna market during the forecast period, driven by rapid industrialization, expanding manufacturing and logistics sectors, and the increasing adoption of automated supply chain and warehouse management solutions across China, India, Japan, and Southeast Asia. The region is home to major electronics, retail, and e-commerce hubs, driving demand for high-performance RFID antennas for asset tracking, inventory management, and baggage handling. Supportive government initiatives promoting smart manufacturing, digitalization, and Industry 4.0 adoption, along with rising investments in retail modernization and transportation infrastructure, are further accelerating the deployment of RFID antenna solutions, positioning the Asia Pacific as the dominant regional market.

Extensive primary interviews were conducted with key industry experts in the RFID antenna market to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type-Tier 1 - 25%, Tier 2 - 35%, and Tier 3 - 40%

- By Designation-C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region-North America - 35%, Europe - 25%, Asia Pacific - 25%, and RoW - 15%

The RFID antenna market is dominated by a few globally established players, such as Zebra Technologies Corp. (US), TE Connectivity (Ireland), SHANGHAI INLAY LINK INC. (INLAYLINK) (China), Nedap N.V. (Netherlands), Times-7 (New Zealand), Kathrein Solutions GmbH (Germany), Pepperl+Fuchs SE (Germany), GAO RFID Inc. (Canada), Impinj, Inc. (US), Invengo Information Technology Co., Ltd. (China), among others.

The study includes an in-depth competitive analysis of these key players in the RFID antenna market, with their company profiles, recent developments, and key market strategies.

Study Coverage:

The report segments the RFID antenna market and forecasts its size by type (far-field antenna, near-field antenna), by technology (passive antenna, smart antenna), by radiation pattern (directional, omnidirectional), by deployment type (fixed, portable), by form factor (patch/panel, dipole, gate, ceiling-mounted, embedded, custom/specialty), by application (inventory & asset management, security & access control, ticketing, airport & baggage handling, other applications), by vertical (automotive, industrial & manufacturing, medical, healthcare & pharmaceutical, agriculture, retail, animal tracking, food processing, aerospace & defense, sports, transportation, logistics & supply chain, data center). The report also analyzes key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across North America, Europe, Asia Pacific, and the Rest of the World, along with country-level insights for major markets. In addition, the study includes value chain analysis and a competitive landscape assessment of leading players in the global RFID antenna ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (regulatory traceability mandates accelerate item-level RFID antenna deployments across enterprise supply chains, large-scale retail and apparel RFID rollouts drive sustained demand for high-performance antenna infrastructure, automated material handling expansion accelerates demand for fixed and portable RFID antennas, brand protection and anti-counterfeiting programs drive deployment of RFID antennas across global supply chains, cold chain digitization drives adoption of RFID antennas in temperature-sensitive logistics networks), restraints (high total cost of ownership constrains enterprise-scale RFID antenna deployments, legacy infrastructure and space constraints limit RFID antenna deployment flexibility, complex RF site design and tuning requirements slow enterprise RFID antenna deployments), opportunities (smart packaging and embedded product identification create new growth avenues for RFID antenna deployments, growing demand for custom and application-specific RFID antenna designs across niche verticals), and challenges (RF interference and harsh operating conditions challenge consistent RFID antenna performance).

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the RFID antenna market.

- Market Development: Comprehensive information about lucrative markets-the report analyses the RFID antenna market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the RFID antenna market

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, such as Zebra Technologies Corp. (US), TE Connectivity (Ireland), SHANGHAI INLAY LINK INC. (INLAYLINK) (China), Nedap N.V. (Netherlands), Times-7 (New Zealand), Kathrein Solutions GmbH (Germany), Pepperl+Fuchs SE (Germany), GAO RFID Inc. (Canada), Impinj, Inc. (US), Invengo Information Technology Co., Ltd. (China), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN RFID ANTENNA MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN RFID ANTENNA MARKET

- 3.2 RFID ANTENNA MARKET, BY TYPE

- 3.3 RFID ANTENNA MARKET, BY TECHNOLOGY

- 3.4 RFID ANTENNA MARKET, BY RADIATION PATTERN

- 3.5 RFID ANTENNA MARKET, BY DEPLOYMENT TYPE

- 3.6 RFID ANTENNA MARKET, BY FORM FACTOR

- 3.7 RFID ANTENNA MARKET, BY APPLICATION

- 3.8 RFID ANTENNA MARKET, BY VERTICAL

- 3.9 RFID ANTENNA MARKET, BY REGION

- 3.10 RFID ANTENNA MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Regulatory traceability mandates accelerate item-level RFID antenna deployments across enterprise supply chains

- 4.2.1.2 Large-scale retail and apparel RFID rollouts drive sustained demand for high-performance antenna infrastructure

- 4.2.1.3 Automated material handling expansion accelerates demand for fixed and portable RFID antennas

- 4.2.1.4 Brand protection and anti-counterfeiting programs drive deployment of RFID antennas across global supply chains

- 4.2.1.5 Cold chain digitization drives adoption of RFID antennas in temperature-sensitive logistics networks

- 4.2.2 RESTRAINTS

- 4.2.2.1 High total cost of ownership constrains enterprise-scale RFID antenna deployments

- 4.2.2.2 Legacy infrastructure and space constraints limit RFID antenna deployment flexibility

- 4.2.2.3 Complex RF site design and tuning requirements slow enterprise RFID antenna deployments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Smart packaging and embedded product identification create new growth avenues for RFID antenna deployments

- 4.2.3.2 Growing demand for custom and application-specific RFID antenna designs across niche verticals

- 4.2.4 CHALLENGES

- 4.2.4.1 RF interference and harsh operating conditions challenge consistent RFID antenna performance

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.4.1 MARKET DYNAMICS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL LOGISTICS & SUPPLY CHAIN INDUSTRY

- 5.3.4 TRENDS IN GLOBAL RETAIL INDUSTRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 REGION-WISE LIST OF MAJOR SYSTEM INTEGRATORS OF RFID ANTENNAS

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia Pacific

- 5.5.1.4 Rest of the World

- 5.5.1 REGION-WISE LIST OF MAJOR SYSTEM INTEGRATORS OF RFID ANTENNAS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF RFID ANTENNAS, BY KEY PLAYER (2022-2025)

- 5.6.2 AVERAGE SELLING PRICE TREND OF RFID ANTENNAS, BY REGION (2022-2025)

- 5.6.2.1 Average selling price trend of far-field RFID antennas, by region (2022-2025)

- 5.6.2.2 Average selling price trend of near-field RFID antennas, by region (2022-2025)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8523)

- 5.7.2 EXPORT SCENARIO (HS CODE 8523)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2021-2025

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 CASE STUDY 1: RETAIL INVENTORY VISIBILITY USING FIXED UHF RFID ANTENNAS

- 5.11.2 CASE STUDY 2: WAREHOUSE AUTOMATION USING PORTAL RFID ANTENNAS

- 5.11.3 CASE STUDY 3: HEALTHCARE ASSET TRACKING USING COMPACT RFID ANTENNAS

- 5.12 IMPACT OF 2025 US TARIFFS-RFID ANTENNA MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE VERTICALS

- 5.12.5.1 Retail

- 5.12.5.2 Transportation, logistics, and supply chain

- 5.12.5.3 Industrial & manufacturing

- 5.12.5.4 Medical, healthcare, and pharmaceutical

- 5.12.5.5 Data centers

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 UHF RFID ANTENNA TECHNOLOGY

- 6.1.2 MULTI-FREQUENCY AND WIDEBAND RFID ANTENNA TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 RFID READERS AND INTERROGATOR TECHNOLOGY

- 6.2.2 RFID MIDDLEWARE AND DATA MANAGEMENT PLATFORMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 NEAR-FIELD COMMUNICATION (NFC) ANTENNA TECHNOLOGY

- 6.3.2 IOT AND WIRELESS SENSOR NETWORK ANTENNA TECHNOLOGY

- 6.4 TECHNOLOGY ROADMAP

- 6.4.1 SHORT-TERM (2025-2027): PERFORMANCE OPTIMIZATION & DEPLOYMENT EXPANSION

- 6.4.2 MID-TERM (2027-2030): SMART ANTENNAS & SYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+): AUTONOMOUS & APPLICATION-SPECIFIC ANTENNA ECOSYSTEMS

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON RFID ANTENNA MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN RFID ANTENNA MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN RFID ANTENNA MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI IN RFID ANTENNA MARKET

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 INDUSTRY STANDARDS

- 7.2.2.1 RFID Antenna Air-Interface and RF Performance Standards (ISO/IEC 18000 Series)

- 7.2.2.2 Regional RF and EMC Standards for RFID Antennas (ETSI, FCC, and Equivalent Frameworks)

- 7.2.2.3 EPCglobal and GS1 Framework (Deployment Interoperability)

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS END-USE VERTICALS

9 RFID ANTENNA MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 FAR-FIELD ANTENNA

- 9.2.1 LINEAR POLARIZED ANTENNA

- 9.2.1.1 Controlled read zones and higher-gain requirements drive linear polarized far-field RFID antenna selection

- 9.2.2 CIRCULAR POLARIZED ANTENNA

- 9.2.2.1 Orientation-independent read performance shapes adoption

- 9.2.1 LINEAR POLARIZED ANTENNA

- 9.3 NEAR-FIELD ANTENNA

- 9.3.1 LOCALIZED WORKFLOW ZONES AND PROXIMITY VALIDATION DRIVE MARKET ADOPTION

10 RFID ANTENNA MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 PASSIVE ANTENNA

- 10.2.1 LOW FREQUENCY

- 10.2.1.1 Access control and asset identification applications drive growth

- 10.2.2 HIGH FREQUENCY

- 10.2.2.1 Smart card ecosystems and NFC-based infrastructure expand deployment

- 10.2.3 ULTRA-HIGH FREQUENCY

- 10.2.3.1 High-throughput supply chains and item-level retail programs accelerate adoption

- 10.2.1 LOW FREQUENCY

- 10.3 SMART ANTENNA

- 10.3.1 EDGE-BASED RFID PROCESSING AND AUTOMATED FULFILMENT ARCHITECTURES PROPEL MARKET GROWTH

11 RFID ANTENNA MARKET, BY RADIATION PATTERN

- 11.1 INTRODUCTION

- 11.2 DIRECTIONAL

- 11.2.1 CONTROLLED READ ZONES AND PORTAL-BASED MATERIAL FLOW DRIVE DIRECTIONAL RFID ANTENNA MARKET GROWTH

- 11.3 OMNIDIRECTIONAL

- 11.3.1 EXPANSION OF WAREHOUSE AUTOMATION AND FLEXIBLE READ-ZONE REQUIREMENTS ACCELERATE OMNIDIRECTIONAL RFID ANTENNA ADOPTION

12 RFID ANTENNA MARKET, BY FORM FACTOR

- 12.1 INTRODUCTION

- 12.2 PATCH/PANEL

- 12.2.1 WAREHOUSE AUTOMATION AND STRUCTURED PORTAL DEPLOYMENTS DRIVE GROWTH OF PATCH/PANEL RFID ANTENNA MARKET

- 12.3 DIPOLE

- 12.3.1 MOBILE RFID DEPLOYMENTS AND EMBEDDED READER DESIGNS DRIVE ADOPTION

- 12.4 GATE

- 12.4.1 AUTOMATED DOCK OPERATIONS AND LANE-LEVEL VALIDATION PROPEL MARKET GROWTH

- 12.5 CEILING-MOUNTED

- 12.5.1 OPEN-FLOOR INVENTORY WORKFLOWS AND SPACE-CONSTRAINED FACILITIES ACCELERATE DEPLOYMENT

- 12.6 EMBEDDED

- 12.6.1 BLIND-ZONE ELIMINATION AND SHELF-LEVEL VISIBILITY DRIVE EMBEDDED RFID ANTENNA INTEGRATION

- 12.7 CUSTOM/SPECIALTY

- 12.7.1 APPLICATION-SPECIFIC RF DESIGNS AND NON-STANDARD GEOMETRIES TO PROPEL ADOPTION

13 RFID ANTENNA MARKET, BY DEPLOYMENT TYPE

- 13.1 INTRODUCTION

- 13.2 FIXED

- 13.2.1 WAREHOUSE AUTOMATION AND PORTAL-BASED TRACKING PROPEL FIXED RFID ANTENNA GROWTH

- 13.3 PORTABLE 142 13.3.1 FIELD MOBILITY AND ON-DEMAND SCANNING TO DRIVE PORTABLE RFID ANTENNA ADOPTION

14 RFID ANTENNA MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 INVENTORY & ASSET MANAGEMENT

- 14.2.1 RECEIVING DOCK AUTOMATION AND REAL-TIME STOCK VISIBILITY DRIVE ADOPTION

- 14.3 SECURITY & ACCESS CONTROL

- 14.3.1 SECURE FACILITY MODERNIZATION AND CONTACTLESS AUTHENTICATION BOOSTS DEMAND

- 14.4 TICKETING

- 14.4.1 CONTACTLESS ENTRY SYSTEMS AND PASSENGER THROUGHPUT OPTIMIZATION SUPPORT MARKET GROWTH

- 14.5 AIRPORT & BAGGAGE HANDLING

- 14.5.1 AUTOMATED BAGGAGE HANDLING AND PASSENGER FLOW OPTIMIZATION EXPAND RFID ANTENNA USAGE

- 14.6 OTHER APPLICATIONS

15 RFID ANTENNA MARKET, BY VERTICAL

- 15.1 INTRODUCTION

- 15.2 AUTOMOTIVE

- 15.3 INDUSTRIAL & MANUFACTURING

- 15.3.1 PRODUCTION LINE TRACEABILITY AND YARD AUTOMATION DRIVE DEMAND

- 15.3.2 PAPER & PULP

- 15.3.3 METAL & MINING

- 15.3.4 CEMENT

- 15.3.5 OTHERS

- 15.4 MEDICAL, HEALTHCARE & PHARMACEUTICAL

- 15.4.1 ASSET VISIBILITY AND MEDICATION MANAGEMENT EXPAND USAGE

- 15.5 AGRICULTURE

- 15.5.1 FIELD-LEVEL CROP MONITORING AND SUPPLY CHAIN TRACEABILITY TO PROPEL MARKET GROWTH

- 15.6 FOOD PROCESSING

- 15.6.1 BATCH TRACEABILITY AND COLD-CHAIN VISIBILITY BOOSTS DEMAND

- 15.7 RETAIL

- 15.7.1 OMNICHANNEL INVENTORY ACCURACY AND SHRINK REDUCTION ACCELERATE DEMAND

- 15.8 ANIMAL TRACKING

- 15.8.1 MANDATORY IDENTIFICATION PROGRAMS AND MOVEMENT TRACEABILITY ACCELERATE DEPLOYMENT

- 15.9 AEROSPACE & DEFENSE

- 15.9.1 MRO WORKFLOW DIGITIZATION AND SECURE ASSET TRACEABILITY DRIVE ADOPTION

- 15.10 SPORTS

- 15.10.1 HIGH-DENSITY VENUE OPERATIONS AND CONTACTLESS ACCESS PROPELS INTEGRATION

- 15.11 TRANSPORTATION, LOGISTICS & SUPPLY CHAIN

- 15.11.1 HUB AUTOMATION AND REAL-TIME FREIGHT VISIBILITY TO DRIVE MARKET GROWTH

- 15.12 DATA CENTER

- 15.12.1 INFRASTRUCTURE AUTOMATION AND REAL-TIME EQUIPMENT CONTROL SUPPORT GROWTH

16 RFID ANTENNA MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 US fixed and smart RFID antenna deployments accelerated by warehouse automation and item-level retail tracking

- 16.2.2 CANADA

- 16.2.2.1 Canada RFID antenna demand supported by distribution center modernization and cross-border logistics

- 16.2.3 MEXICO

- 16.2.3.1 Mexico RFID antenna uptake strengthened by manufacturing expansion and export-oriented logistics

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 RFID antenna deployments accelerated by apparel retail automation and fulfillment center digitization

- 16.3.2 GERMANY

- 16.3.2.1 Industry 4.0 traceability and factory automation initiatives to propel market growth

- 16.3.3 FRANCE

- 16.3.3.1 RFID antenna market shaped by store-level automation and parcel flow optimization

- 16.3.4 ITALY

- 16.3.4.1 Emphasis on quick traceability and brand-centric logistics support RFID antenna adoption

- 16.3.5 RUSSIA

- 16.3.5.1 Centralized procurement and compliance-led deployments to propel adoption in Russia

- 16.3.6 POLAND

- 16.3.6.1 Demand reinforced by e-commerce fulfillment growth and logistics corridor expansion

- 16.3.7 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Factory automation and mega-scale logistics infrastructure to be key contributors to market growth

- 16.4.2 JAPAN

- 16.4.2.1 Growing precision manufacturing and smart transit infrastructure to augment market growth

- 16.4.3 SOUTH KOREA

- 16.4.3.1 Rising adoption of manufacturing programs and logistics digitization to drive market

- 16.4.4 INDIA

- 16.4.4.1 Rising warehouse modernization and infrastructure-led digitization supporting market growth

- 16.4.5 AUSTRALIA & NEW ZEALAND

- 16.4.5.1 Retail distribution modernization and cold-chain logistics control driving RFID antenna deployment

- 16.4.6 ASEAN

- 16.4.6.1 Growth in export manufacturing corridors and fulfillment warehouse expansion supporting market growth

- 16.4.7 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 REST OF THE WORLD

- 16.5.1 MIDDLE EAST & AFRICA

- 16.5.1.1 GCC Countries

- 16.5.1.1.1 Port modernization and industrial zone automation to drive the market

- 16.5.1.2 South Africa

- 16.5.1.2.1 Retail distribution networks and automotive logistics underpinning RFID antenna adoption in South Africa

- 16.5.1.3 Turkey

- 16.5.1.3.1 Export manufacturing and regional transit logistics advancing RFID antenna deployments in Turkey

- 16.5.1.4 Rest of Middle East & Africa

- 16.5.1.1 GCC Countries

- 16.5.2 SOUTH AMERICA

- 16.5.2.1 Brazil

- 16.5.2.1.1 Domestic integrators and warehouse-led deployment economics accelerating demand

- 16.5.2.2 Rest of South America

- 16.5.2.1 Brazil

- 16.5.1 MIDDLE EAST & AFRICA

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 17.3 REVENUE ANALYSIS, 2021-2025

- 17.4 MARKET SHARE ANALYSIS, 2025

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 Type footprint

- 17.6.5.4 Technology footprint

- 17.6.5.5 Radiation pattern footprint

- 17.6.5.6 Deployment type footprint

- 17.6.5.7 Form factor footprint

- 17.6.5.8 Application footprint

- 17.6.5.9 Vertical footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 17.7.5.1 Detailed list of startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 BRAND COMPARISON

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 INTRODUCTION

- 18.2 KEY PLAYERS

- 18.2.1 ZEBRA TECHNOLOGIES CORP.

- 18.2.1.1 Business overview

- 18.2.1.2 Products offered

- 18.2.1.3 Recent developments

- 18.2.1.3.1 Product launches & upgrades

- 18.2.1.3.2 Deals

- 18.2.1.3.3 Expansions

- 18.2.1.4 MnM view

- 18.2.1.4.1 Key strengths/Right to win

- 18.2.1.4.2 Strategic choices

- 18.2.1.4.3 Weaknesses/Competitive threats

- 18.2.2 TE CONNECTIVITY

- 18.2.2.1 Business overview

- 18.2.2.2 Products offered

- 18.2.2.3 MnM view

- 18.2.2.3.1 Key strengths/Right to win

- 18.2.2.3.2 Strategic choices

- 18.2.2.3.3 Weaknesses/Competitive threats

- 18.2.3 SHANGHAI INLAY LINK INC. (INLAYLINK)

- 18.2.3.1 Business overview

- 18.2.3.2 Products offered

- 18.2.3.3 MnM view

- 18.2.3.3.1 Key strengths/Right to win

- 18.2.3.3.2 Strategic choices

- 18.2.3.3.3 Weaknesses/Competitive threats

- 18.2.4 NEDAP N.V.

- 18.2.4.1 Business overview

- 18.2.4.2 Products offered

- 18.2.4.3 Recent developments

- 18.2.4.3.1 Deals

- 18.2.4.3.2 Expansions

- 18.2.4.4 MnM view

- 18.2.4.4.1 Key strengths/Right to win

- 18.2.4.4.2 Strategic choices

- 18.2.4.4.3 Weaknesses/Competitive threats

- 18.2.5 TIMES-7

- 18.2.5.1 Business overview

- 18.2.5.2 Products offered

- 18.2.5.3 MnM view

- 18.2.5.3.1 Key strengths/Right to win

- 18.2.5.3.2 Strategic choices

- 18.2.5.3.3 Weaknesses/Competitive threats

- 18.2.6 KATHREIN SOLUTIONS GMBH

- 18.2.6.1 Business overview

- 18.2.6.2 Products offered

- 18.2.6.3 Recent developments

- 18.2.6.3.1 Product launches/upgrades

- 18.2.6.3.2 Deals

- 18.2.6.4 MnM view

- 18.2.6.4.1 Key strengths/Right to win

- 18.2.6.4.2 Strategic choices

- 18.2.6.4.3 Weaknesses/Competitive threats

- 18.2.7 PEPPERL+FUCHS SE

- 18.2.7.1 Business overview

- 18.2.7.2 Products offered

- 18.2.7.3 Recent developments

- 18.2.7.3.1 Product launches

- 18.2.8 IMPINJ, INC.

- 18.2.8.1 Business overview

- 18.2.8.2 Products offered

- 18.2.9 INVENGO INFORMATION TECHNOLOGY CO., LTD.

- 18.2.9.1 Business overview

- 18.2.9.2 Products offered

- 18.2.10 ALIEN TECHNOLOGY, LLC

- 18.2.10.1 Business overview

- 18.2.10.2 Products offered

- 18.2.11 CAEN RFID S.R.L.

- 18.2.11.1 Business overview

- 18.2.11.2 Products offered

- 18.2.12 MTI WIRELESS EDGE LTD.

- 18.2.12.1 Business overview

- 18.2.12.2 Products offered

- 18.2.1 ZEBRA TECHNOLOGIES CORP.

- 18.3 OTHER PLAYERS

- 18.3.1 GAO RFID INC.

- 18.3.2 UNITECH ELECTRONICS CO., LTD.

- 18.3.3 CYKEO INFORMATION TECHNOLOGY CO.

- 18.3.4 WINNIX TECHNOLOGIES CO., LIMITED PRODUCTS, CORP.

- 18.3.5 FLEXIRAY

- 18.3.6 IDENTIUM TECH SOLUTIONS

- 18.3.7 SYNERGY TELECOM PVT. LTD.

- 18.3.8 GREENFUTURZ

- 18.3.9 C&T RF ANTENNAS INC.

- 18.3.10 E-CARTES TECHNOLOGY PVT. LTD.

- 18.3.11 ID TECH

- 18.3.12 MANTRA SOFTECH (INDIA) PVT. LTD.

- 18.3.13 GLEAM LIGHT INDIA

- 18.3.14 KEONN TECHNOLOGIES, S.L.

- 18.3.15 FEIG ELECTRONIC GMBH

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY AND PRIMARY RESEARCH

- 19.1.2 SECONDARY DATA

- 19.1.2.1 List of key secondary sources

- 19.1.2.2 Key data from secondary sources

- 19.1.3 PRIMARY DATA

- 19.1.3.1 List of primary interview participants

- 19.1.3.2 Breakdown of primaries

- 19.1.3.3 Key data from primary sources

- 19.1.3.4 Key industry insights

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 BOTTOM-UP APPROACH

- 19.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 19.2.2 TOP-DOWN APPROACH

- 19.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 19.2.1 BOTTOM-UP APPROACH

- 19.3 DATA TRIANGULATION

- 19.4 RESEARCH ASSUMPTIONS

- 19.5 RESEARCH LIMITATIONS

- 19.6 RISK ASSESSMENT

20 APPENDIX

- 20.1 INSIGHTS FROM INDUSTRY EXPERTS

- 20.2 DISCUSSION GUIDE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS