|

시장보고서

상품코드

1972227

드론 통신 시장(-2030년) : 기술, 기능, 커넥티비티, 용도, 컴포넌트, 지역별Drone Communication Market by Technology, Function, Connectivity, Application, Component, and Region - Global Forecast to 2030 |

||||||

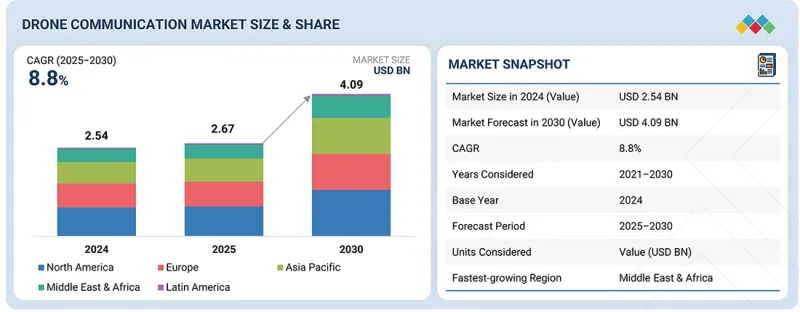

드론 통신 시장 규모는 예측 기간 중에 CAGR 8.8%로 성장하여 2025년 26억 7,000만 달러에서 2030년에는 40억 9,000만 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 커넥티비티별, 컴포넌트별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

시장 성장은 주로 안정적이고 안전한 연결성이 매우 중요한 국방, 국토 안보 및 상업적 작업에서 드론의 활용에 의해 주도되고 있습니다. 또한, BVLOS 비행에 대한 규제 당국의 지원과 항공 공간 통합의 진전 또한 검사, 농업, 물류 등의 분야로 시장 확대를 촉진하고 있습니다.

"커넥티비티별로 보면, 예측 기간 동안 비지상 네트워크 부문의 성장률이 지상 네트워크보다 더 높을 것으로 예측됩니다."

예측 기간 동안 비지상 네트워크 부문은 지상 네트워크가 닿지 않는 지역에서도 통신이 가능하기 때문에 가장 빠르게 성장할 것으로 예측됩니다. 위성 링크와 고고도 플랫폼 시스템을 통해 드론은 일반 지상 네트워크가 약하거나 이용할 수 없는 원격지, 해상, 사막, 국경 지역에서도 운영할 수 있습니다. 이는 장시간 임무, 국방 감시 활동, 해양 산업 운영에서 매우 중요합니다. BVLOS(비가시권) 비행 증가와 장거리에서 지속적인 통신의 필요성도 비지상 솔루션에 대한 수요를 촉진하고 있습니다. 또한, 새로운 저궤도 위성 별자리로 인해 통신 속도가 빨라지고 지연이 줄어들어 이전보다 실용성이 높아졌습니다. 드론 운영이 보다 복잡하고 분산된 장소로 이동함에 따라, 비지상 네트워크는 커넥티비티 부문에서 가장 높은 성장률을 보일 가능성이 높습니다.

"기능별로 보면, 예측 기간 동안 지휘 및 제어(C2) 부문이 가장 큰 시장 점유율을 차지할 것으로 예측됩니다."

지휘통제(C2) 부문은 드론과 지상 관제 시스템 간의 주요 연결 수단이기 때문에 예측 기간 동안 시장을 주도할 것으로 예측됩니다. 국방용이든 상업용이든 모든 드론 임무는 비행 운영, 항법, 임무 수행을 위해 안정적이고 안전한 지휘 통제에 의존하고 있습니다. 이 연결이 없으면 드론이 정상적으로 작동할 수 없습니다. 또한, C2 시스템은 전체 통신 인프라에서 미션 크리티컬한 요소로 간주되며, 특히 군사, 국토 안보, BVLOS(비가시권) 비행에서 강력한 암호화를 갖춘 매우 안정적이고 빠른 시스템입니다. 드론의 규모가 확대되고 임무가 복잡해짐에 따라 신뢰할 수 있는 때로는 백업 기능을 갖춘 지휘통제 네트워크의 필요성도 증가하고 있습니다. 이러한 모든 요인들이 지휘통제(C2) 부문의 성장을 견인하고 있습니다.

"중동 및 아프리카이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다."

중동 및 아프리카은 많은 국가들이 국방 시스템을 현대화하고 감시 및 국경 보안에 대한 지출을 늘리면서 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. 각국 정부는 중요 인프라 보호와 국토 안보 강화에 주력하고 있으며, 이는 안전하고 신뢰할 수 있는 드론 통신 네트워크에 대한 수요를 견인하고 있습니다. 또한, 진화하는 위협에 대응하기 위한 무인 시스템 조달 증가도 이러한 성장을 뒷받침하고 있습니다. 상업 분야에서는 주로 걸프 지역을 중심으로 석유 및 가스, 광업, 건설, 혁신적 도시 프로젝트에서 드론의 활용이 확대되고 있습니다. 이러한 활동이 제대로 작동하려면 안정적인 통신 시스템이 필요합니다. 동시에 5G의 보급과 위성 통신의 개선으로 커버리지가 향상되고 있습니다. 따라서 이 지역은 드론 통신 솔루션의 고성장 시장으로 떠오르고 있습니다.

세계의 드론 통신(Drone Communication) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 현황과 구매 행동

제7장 지속가능성과 규제 상황

제8장 기술 진보, AI의 영향, 특허, 혁신, 향후 용도

제9장 드론 통신 시장 : 용도별

제10장 드론 통신 시장 : 컴포넌트별

제11장 드론 통신 시장 : 커넥티비티별

제12장 드론 통신 시장 : 기능별

제13장 드론 통신 시장 : 기술별

제14장 드론 통신 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

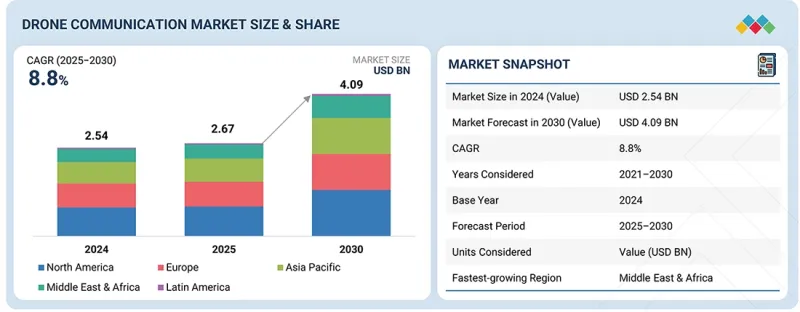

LSH 26.03.31The drone communication market is projected to grow from USD 2.67 billion in 2025 to USD 4.09 billion by 2030, at a CAGR of 8.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Component , Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

Market growth is primarily driven by the use of drones in defense, homeland security, and commercial work, where stable and secure connectivity really matters. Additionally, support from regulators for BVLOS flights and better airspace integration is also helping the market expand into areas like inspection, farming, and logistics.

"By connectivity, the non-terrestrial network segment is expected to grow at a higher rate than the terrestrial network segment during the forecast period."

The non-terrestrial network segment is expected to be the fastest-growing segment in the drone communication market during the forecast period because it can provide coverage where ground networks do not reach. Satellite links and high altitude platform systems allow drones to operate in remote areas, over the sea, in deserts, and across borders where normal terrestrial networks are weak or not available. This becomes very important for long endurance missions, defense surveillance work, and offshore industrial operations. The increase in BVLOS flights and the need for continuous communication over long distances are also pushing demand for non-terrestrial solutions. Moreover, new low-earth orbit satellite constellations are improving speed and reducing delay, which makes these systems more practical than before. As drone operations move into more complex and spread-out locations, non-terrestrial networks are likely to grow at the highest rate within the connectivity segment.

"By function, the command & control (C2) segment is expected to account for the largest market share during the forecast period."

The command & control (C2) segment is expected to lead the market during the forecast period because it is the main link between the drone and the ground control system. Every drone mission, whether in defense or commercial use, depends on stable and secure command and control for flight operations, navigation, and mission tasks. Without this link, drones can't operate properly. Additionally, C2 systems are seen as mission-critical parts of the overall communication setup, and are very reliable and fast, with strong encryption, especially for military, homeland security, and BVLOS flights. As drone fleets become larger and missions get more complex, the need for dependable and sometimes backup command and control networks is also increasing. All these factors are driving the growth of the command & control (C2) segment in the drone communication market.

"Middle East & Africa is projected to grow at the highest rate during the forecast period."

Middle East & Africa is likely to grow at the highest rate during the forecast period as many countries are upgrading defense systems and spending more on surveillance and border security. Governments are focusing on protecting critical infrastructure and improving homeland security, which is driving the demand for secure and dependable drone communication networks. Higher procurement of unmanned systems to handle evolving threats is also supporting this growth. On the commercial side, drones are being used more in oil and gas, mining, construction, and innovative city projects, mainly in the Gulf region. These activities need stable communication systems to run correctly. At the same time, better 5G rollout and satellite connectivity are improving coverage. Thus, the region is becoming a high-growth market for drone communication solutions.

Research Coverage:

This study covers the drone communication market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Extensive primary interviews were conducted with key industry experts in the drone communication market to determine and verify the market size for various segments and subsegments gathered through secondary research.

The breakdown of primary participants for the report is shown below:

- By Company Type: Tier 1 - 35%; Tier 2 - 45%; Tier 3 - 20%

- By Designation: C Level - 35%; Director Level - 25%; Others - 40 %

- By Region: North America - 30%; Europe - 20%; Asia Pacific - 35%; Middle East & Africa - 10%; Latin America- 5%

The drone communication market is dominated by a few globally established players, such as DJI (US), RTX (US), Northrop Grumman (US), Israel Aerospace Industries (Israel), L3Harris Technologies, Inc. (US), BAE Systems (UK), AeroVironment, Inc. (US), Honeywell International Inc. (US), Viasat, Inc. (US), Elbit Systems Ltd. (Israel), Thales (France), ASELSAN A.S. (Turkey), EchoStar Corporation (US), General Dynamics Corporation (US) and Iridium Communications Inc (US).

The study includes an in-depth competitive analysis of these key players in the drone communication market. It also includes their company profiles, recent developments, and key market strategies.

Key Benefits of Buying this Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall drone communication market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Regulatory push for beyond visual line of sight (BVLOS) and airspace integration, rising deployment of drones in mission-critical defense and homeland security operations; expansion of commercial drone fleets for inspection, mapping, agriculture, and logistics), Restraints (Spectrum congestion and interference in unlicensed frequency bands; high cost of aviation-grade, secure, and redundant communication systems), Opportunities (Deployment of next-generation, AI-enabled, and multi-layer drone communication architectures; growing demand for satellite communication for remote and maritime drone missions), Challenges (Ensuring cyber security and protection against jamming and spoofing; achieving seamless network handover across radio frequency, cellular, and satellite links; standardization gaps across communication protocols and interoperability layers)

- Market Penetration: Comprehensive information on drone communication systems and components offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DRONE COMMUNICATION MARKET

- 3.2 DRONE COMMUNICATION MARKET, BY APPLICATION

- 3.3 DRONE COMMUNICATION MARKET, BY FUNCTION

- 3.4 DRONE COMMUNICATION MARKET, BY COMPONENT

- 3.5 DRONE COMMUNICATION MARKET, BY TECHNOLOGY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Regulatory push for beyond visual line of sight (BVLOS) and airspace integration

- 4.2.1.2 Rising deployment of drones in mission-critical defense and homeland security operations

- 4.2.1.3 Expansion of commercial drone fleets for inspection, mapping, agriculture, and logistics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Spectrum congestion and interference in unlicensed frequency bands

- 4.2.2.2 High cost of aviation-grade, secure, and redundant communication systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Deployment of next-generation, AI-enabled, and multi-layer drone communication architectures

- 4.2.3.2 Growing demand for satellite communication for remote and maritime drone missions

- 4.2.4 CHALLENGES

- 4.2.4.1 Ensuring cyber security and protection against jamming and spoofing

- 4.2.4.2 Achieving seamless network handover across radio frequency, cellular, and satellite links

- 4.2.4.3 Standardization gaps across communication protocols and interoperability layers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 LIMITED AVAILABILITY OF LIGHTWEIGHT, LOW-POWER SATELLITE AND HYBRID COMMUNICATION MODULES

- 4.3.2 ABSENCE OF INTELLIGENT COMMUNICATION MANAGEMENT INTEGRATED WITH EDGE ANALYTICS

- 4.3.3 ABSENCE OF SEAMLESS ROAMING AND SERVICE CONTINUITY ACROSS GEOGRAPHIES AND NETWORK PROVIDERS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CONVERGENCE WITH TELECOM INFRASTRUCTURE AND PRIVATE CELLULAR NETWORK ECOSYSTEMS

- 4.4.2 INTEGRATION WITH SATELLITE COMMUNICATION AND SPACE-BASED CONNECTIVITY PROVIDERS

- 4.4.3 ALIGNMENT WITH CLOUD, EDGE COMPUTING, AND UNMANNED TRAFFIC MANAGEMENT (UTM) PLATFORMS

- 4.4.4 SYNERGIES WITH DEFENSE COMMUNICATION NETWORKS AND ELECTRONIC WARFARE ECOSYSTEMS

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL DEFENSE INDUSTRY

- 5.1.4 TRENDS IN GLOBAL DRONE COMMUNICATION INDUSTRY

- 5.2 VALUE CHAIN ANALYSIS

- 5.2.1 R&D ENGINEERS (~30%)

- 5.2.2 RAW MATERIAL SUPPLIERS (10~%)

- 5.2.3 COMPONENT AND PRODUCT MANUFACTURERS (~10%)

- 5.2.4 ASSEMBLERS AND INTEGRATORS (~30%)

- 5.2.5 END USERS (~20%)

- 5.3 ECOSYSTEM ANALYSIS

- 5.3.1 MANUFACTURERS

- 5.3.2 SOLUTION AND SERVICE PROVIDERS

- 5.3.3 END USERS

- 5.4 INVESTMENT AND FUNDING SCENARIO

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS, BY APPLICATION

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY COMPONENT

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8517)

- 5.6.2 EXPORT SCENARIO (HS CODE 8517)

- 5.7 KEY CONFERENCES & EVENTS

- 5.8 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 AEROVIRONMENT - SECURE TACTICAL UAV COMMUNICATION ARCHITECTURE

- 5.9.2 IRIDIUM COMMUNICATIONS - SATELLITE-ENABLED BVLOS DRONE CONNECTIVITY

- 5.9.3 L3HARRIS TECHNOLOGIES - TACTICAL DATA LINKS FOR NETWORKED DRONE OPERATIONS

- 5.10 IMPACT OF 2025 US TARIFFS

- 5.10.1 KEY TARIFF RATES

- 5.10.2 PRICE IMPACT ANALYSIS

- 5.10.3 IMPACT ON COUNTRY/REGION

- 5.10.3.1 US

- 5.10.3.2 Europe

- 5.10.3.3 Asia Pacific

- 5.10.4 IMPACT ON DIFFERENT APPLICATIONS

- 5.10.4.1 Government/Military/Law enforcement

- 5.10.4.2 Commercial

- 5.10.4.3 Consumer

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING EVALUATION CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 KEY EMERGING TECHNOLOGIES

- 8.1.1 COGNITIVE RADIO SYSTEMS

- 8.1.2 MULTIPLE-INPUT MULTIPLE-OUTPUT (MIMO) TECHNOLOGY

- 8.1.3 SOFTWARE-DEFINED NETWORKING

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 ANTENNA BEAMFORMING TECHNOLOGY

- 8.2.2 ADVANCED ENERGY AND BATTERY STORAGE SYSTEMS

- 8.3 TECHNOLOGY ROADMAP

- 8.4 DRONE COMMUNICATION MARKET: OPERATIONAL DATA

- 8.5 TECHNOLOGY TRENDS

- 8.5.1 BEYOND VISUAL LINE OF SIGHT (BVLOS) COMMUNICATION

- 8.5.2 MESH NETWORKING

- 8.5.3 DRONE COMMUNICATION ENCRYPTION

- 8.5.4 INTERNET OF DRONES (IOD) AND VEHICLE-TO-EVERYTHING (V2X) COMMUNICATION

- 8.5.5 HYBRID COMMUNICATION SYSTEMS

- 8.5.6 SATCOM INTEGRATION

- 8.6 IMPACT OF MEGATRENDS

- 8.6.1 AI

- 8.6.2 5G

- 8.6.3 SMART MANUFACTURING

- 8.7 IMPACT OF GEN AI/AI

- 8.7.1 INTRODUCTION

- 8.7.2 ADOPTION OF AI IN COMMERCIAL AVIATION, BY KEY COUNTRY

- 8.8 PATENT ANALYSIS

9 DRONE COMMUNICATION MARKET, BY APPLICATION (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 9.1 INTRODUCTION

- 9.2 CLASSIFICATION OF DRONE COMMUNICATION FREQUENCIES BASED ON DRONE PLATFORMS

- 9.2.1 ULTRA HIGH FREQUENCY (301 MHZ-4 GHZ)

- 9.2.2 SUPER HIGH FREQUENCY (4-40 GHZ)

- 9.2.3 EXTREMELY HIGH FREQUENCY (40-300 GHZ)

- 9.3 MILITARY

- 9.3.1 COMBAT

- 9.3.1.1 High security, anti-jamming, and low probability of intercept links to strengthen combat drone communication

- 9.3.1.2 Use case: LAC-12 Terminal, from General Atomics, provides secure, high-speed, anti-jamming laser communication

- 9.3.1.3 Lethal drones

- 9.3.1.4 Stealth drones

- 9.3.1.5 Loitering munitions

- 9.3.1.6 Target drones

- 9.3.2 ISR

- 9.3.2.1 Real-time intelligence transmission and secure multi-band connectivity to drive ISR communication growth

- 9.3.2.2 Use case: MxC-Mini data links, from Tomahawk, provide secure and AI-enhanced communication for ISR operations

- 9.3.3 DELIVERY

- 9.3.3.1 Autonomous military logistics and battlefield resupply to accelerate secure UAV connectivity

- 9.3.3.2 Use case: Verizon's Airborne LTE operations establish communication infrastructure for drone delivery

- 9.3.1 COMBAT

- 9.4 COMMERCIAL

- 9.4.1 SMALL

- 9.4.1.1 Secure command and control systems to support expanding small UAV applications

- 9.4.1.2 Use case: CNPC-1000 UAS Command and Control Data Link, from Collins Aerospace, provides secure and efficient communication solution

- 9.4.2 MEDIUM

- 9.4.2.1 Need for high-capacity communication systems for large-scale operations to drive segment

- 9.4.2.2 Use case: IMS, from SKYTRAC, delivers advanced, lightweight satellite communication for medium UAVs

- 9.4.3 LARGE

- 9.4.3.1 Broadband satellite and multi-network integration to enable long-endurance commercial UAV communication

- 9.4.3.2 Use case: Velaris, from Viasat, provides satellite communication for large uncrewed aerial vehicles (UAVs) and advanced air mobility (AAM) aircraft

- 9.4.1 SMALL

- 9.5 GOVERNMENT & LAW ENFORCEMENT

- 9.5.1 NEED FOR REAL-TIME CONNECTIVITY TO ENABLE GOVERNMENT AND LAW ENFORCEMENT UAV OPERATIONS

- 9.5.2 USE CASE: HONEYWELL'S VERSAWAVE PROVIDES LIGHTWEIGHT, COMPACT SATELLITE COMMUNICATION SYSTEM

- 9.6 CONSUMER

- 9.6.1 DEMAND FOR SMART DRONES FOR PERSONALIZED AND RECREATIONAL APPLICATIONS TO DRIVE MARKET

- 9.6.2 USE CASE: DJI O4 DIGITAL TRANSMISSION ENHANCING SMART CONSUMER DRONE CONNECTIVITY

10 DRONE COMMUNICATION MARKET, BY COMPONENT (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 10.1 INTRODUCTION

- 10.2 TRANSCEIVERS

- 10.2.1 GROWING DEMAND FOR MULTI-BAND, SOFTWARE-DEFINED, AND ANTI-JAMMING COMMUNICATION LINKS TO FUEL MARKET

- 10.3 ANTENNAS

- 10.3.1 EXPANSION OF SATCOM AND 5G-ENABLED UAV OPERATIONS TO ACCELERATE ADVANCED ANTENNA INTEGRATION

- 10.4 MODEMS

- 10.4.1 ADOPTION OF 5G, SDR, AND EDGE PROCESSING TECHNOLOGIES TO STRENGTHEN INTELLIGENT SIGNAL MANAGEMENT

- 10.5 OTHER COMPONENTS

11 DRONE COMMUNICATION MARKET, BY CONNECTIVITY (MARKET SIZE & FORECAST TO 2030 - USD MILLION)

- 11.1 INTRODUCTION

- 11.2 TERRESTRIAL NETWORK (TN)

- 11.2.1 EXPANSION OF 4G AND 5G INFRASTRUCTURE TO ENABLE SCALABLE AND LOW-LATENCY BVLOS DRONE OPERATIONS

- 11.2.2 USE CASE: VERIZON 5G DRONE MONITORING FOR INDUSTRIAL OPERATIONS

- 11.3 NON-TERRESTRIAL NETWORK (NTN)

- 11.3.1 GROWING DEMAND FOR LONG-RANGE AND REMOTE AREA OPERATIONS TO FUEL SATELLITE-BASED DRONE CONNECTIVITY

- 11.3.2 USE CASE: STARLINK-ENABLED UAV CONNECTIVITY FOR REMOTE OPERATIONS

12 DRONE COMMUNICATION MARKET, BY FUNCTION (MARKET SIZE & FORECAST TO 2030 - IN VALUE, USD MILLION)

- 12.1 INTRODUCTION

- 12.2 COMMAND & CONTROL (C2)

- 12.2.1 GROWING DEMAND FOR SECURE AND LOW-LATENCY LINKS TO STRENGTHEN C2 COMMUNICATION INVESTMENTS

- 12.3 MISSION & PAYLOAD DATA TRANSMISSION

- 12.3.1 RISING DEMAND FOR HIGH-RESOLUTION IMAGERY AND REAL-TIME ANALYTICS TO DRIVE BANDWIDTH EXPANSION

- 12.4 NAVIGATION, POSITIONING & TIMING COMMUNICATIONS (PNT)

- 12.4.1 GROWING FOCUS ON GNSS RESILIENCE AND ANTI-SPOOFING TECHNOLOGIES TO STRENGTHEN PNT COMMUNICATION SYSTEMS

- 12.5 SWARM OPERATIONS

- 12.5.1 AUTONOMOUS FLEET COORDINATION AND DISTRIBUTED INTELLIGENCE TO ACCELERATE INTER-UAV COMMUNICATION GROWTH

- 12.6 BACKUP & RECOVERY

- 12.6.1 RISING REGULATORY MANDATES AND SAFETY REQUIREMENTS TO DRIVE REDUNDANT COMMUNICATION ARCHITECTURES

13 DRONE COMMUNICATION MARKET, BY TECHNOLOGY (MARKET SIZE & FORECAST TO 2030 - IN VALUE, USD MILLION)

- 13.1 INTRODUCTION

- 13.2 DRONE COMMUNICATION TECHNOLOGIES: LINK TYPE-BASED CLASSIFICATION

- 13.2.1 DRONE-TO-DRONE

- 13.2.1.1 Autonomous swarming and distributed intelligence to fuel inter-UAV mesh networks

- 13.2.2 DRONE-TO-INFRASTRUCTURE

- 13.2.2.1 Convergence of cellular, satellite, and airspace integration systems to drive connected UAV ecosystems

- 13.2.2.2 Drone-to-satellite

- 13.2.2.3 Drone-to-network

- 13.2.3 DRONE-TO-GROUND STATION

- 13.2.3.1 Continued demand for secure, independent, and high-reliability tactical links to sustain market for dedicated RF systems

- 13.2.1 DRONE-TO-DRONE

- 13.3 HARDWARE-BASED RADIO (HBR)

- 13.3.1 EMPHASIS ON HIGH POWER TRANSMISSION AND HARDENED SECURITY TO SUPPORT FIXED ARCHITECTURE RADIOS

- 13.4 SOFTWARE-DEFINED RADIO (SDR)

- 13.4.1 RISING NEED FOR SPECTRUM FLEXIBILITY AND INTEROPERABILITY TO DRIVE ADOPTION OF RECONFIGURABLE RADIO ARCHITECTURES

14 DRONE COMMUNICATION MARKET, BY REGION (MARKET SIZE & FORECAST TO 2030 - IN VALUE, USD MILLION)

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Rising defense modernization and 5G integration to strengthen secure UAV communication systems

- 14.2.2 CANADA

- 14.2.2.1 Growing need for remote connectivity to support industrial and arctic UAV operations

- 14.2.1 US

- 14.3 ASIA PACIFIC

- 14.3.1 CHINA

- 14.3.1.1 Growing 5G leadership and domestic UAV manufacturing to strengthen drone communication integration

- 14.3.2 INDIA

- 14.3.2.1 Rising indigenous UAV ecosystem and satellite integration to drive secure drone communication growth

- 14.3.3 JAPAN

- 14.3.3.1 Growing 5G-enabled BVLOS infrastructure to accelerate advanced drone communication systems

- 14.3.4 AUSTRALIA

- 14.3.4.1 Growing need for long-range satellite connectivity to support remote UAV communication expansion

- 14.3.5 SOUTH KOREA

- 14.3.5.1 Rising smart city and defense modernization programs to drive high-speed UAV communication deployment

- 14.3.6 REST OF ASIA PACIFIC

- 14.3.1 CHINA

- 14.4 EUROPE

- 14.4.1 UK

- 14.4.1.1 Need to strengthen 5G-enabled drone communication through strategic partnerships to drive growth

- 14.4.2 GERMANY

- 14.4.2.1 Focus on enhancing interoperable military drone communication through software integration to boost market

- 14.4.3 FRANCE

- 14.4.3.1 Expanding swarm and secure UAV communication capabilities through strategic acquisition to boost market

- 14.4.4 RUSSIA

- 14.4.4.1 Emphasis on advancing UAV software and communication training integration to drive market

- 14.4.5 ITALY

- 14.4.5.1 Need for strengthening UAV communication infrastructure through aerospace collaboration to boost growth

- 14.4.6 REST OF EUROPE

- 14.4.1 UK

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.5.1.1 UAE

- 14.5.1.1.1 Growing smart city and defense investments to drive advanced drone communication infrastructure

- 14.5.1.2 Saudi Arabia

- 14.5.1.2.1 Rising investments in 'Vision 2030' to strengthen secure and satellite-integrated UAV communication

- 14.5.1.1 UAE

- 14.5.2 ISRAEL

- 14.5.2.1 Rising defense innovation and secure data link exports to strengthen advanced drone communication leadership

- 14.5.3 TURKEY

- 14.5.3.1 Rising export-oriented UAV manufacturing to drive demand for advanced tactical communication systems

- 14.5.4 SOUTH AFRICA

- 14.5.4.1 Growing security and infrastructure monitoring needs to drive UAV communication adoption

- 14.5.5 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.6 LATIN AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Need for advanced drone communication for environmental monitoring to drive market

- 14.6.2 MEXICO

- 14.6.2.1 Increasing demand for drones with secure communication systems to drive market

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 15.3 REVENUE ANALYSIS, 2021-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Technology footprint

- 15.5.5.4 Application footprint

- 15.5.5.5 Function footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING

- 15.6.5.1 List of startups/SMEs

- 15.6.5.2 Competitive benchmarking of startups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 DEALS

- 15.9.2 OTHER DEVELOPMENTS

- 15.9.3 PRODUCT LAUNCHES

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 DJI

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 MnM view

- 16.1.1.3.1 Right to win

- 16.1.1.3.2 Strategic choices

- 16.1.1.3.3 Weaknesses and competitive threats

- 16.1.2 RTX

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 MnM view

- 16.1.2.3.1 Right to win

- 16.1.2.3.2 Strategic choices

- 16.1.2.3.3 Weaknesses and competitive threats

- 16.1.3 NORTHROP GRUMMAN

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ISRAEL AEROSPACE INDUSTRIES

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 L3HARRIS TECHNOLOGIES, INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 ELBIT SYSTEMS LTD.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Other developments

- 16.1.7 BAE SYSTEMS

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.7.3.2 Deals

- 16.1.7.3.3 Other developments

- 16.1.8 AEROVIRONMENT, INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.3.2 Other developments

- 16.1.9 HONEYWELL INTERNATIONAL INC.

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.3.2 Deals

- 16.1.9.3.3 Other developments

- 16.1.10 VIASAT, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.11 IRIDIUM COMMUNICATIONS INC.

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.12 THALES

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.13 GENERAL DYNAMICS CORPORATION

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Other developments

- 16.1.14 ASELSAN A.S.

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.15 ECHOSTAR

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.1 DJI

- 16.2 OTHER PLAYERS

- 16.2.1 ELSIGHT

- 16.2.2 DOODLE LABS LLC

- 16.2.3 SKYTRAC SYSTEMS LTD.

- 16.2.4 TRIAD RF SYSTEMS

- 16.2.5 TUALCOM

- 16.2.6 UAVIONIX

- 16.2.7 ULTRA I&C

- 16.2.8 SILVUS TECHNOLOGIES

- 16.2.9 PERSISTENT SYSTEMS

- 16.2.10 METEKSAN DEFENSE INDUSTRY

- 16.2.11 DTC CODAN

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary insights

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.1 SECONDARY DATA

- 17.2 FACTOR ANALYSIS

- 17.2.1 INTRODUCTION

- 17.2.2 DEMAND-SIDE INDICATORS

- 17.2.3 SUPPLY-SIDE INDICATORS

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.2 TOP-DOWN APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 ANNEXURE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS