|

시장보고서

상품코드

1984860

가스 혼합물 시장(-2030년) : 유형(O2, N2, CO2, AR, H2, 특수 가스), 최종사용자 산업(금속조 및 가공, 의료, 식품 및 음료, 일렉트로닉스), 저장 및 운송, 제조 공정, 지역별Gas Mixtures Market by Type (O2, N2, CO2, AR, H2, and Specialty Gas), End-Use Industry (Metal Manufacturing & Fabrication, Healthcare, Food & Beverages, Electronics), Storage & Distribution, Manufacturing Process, and Region - Global Forecast to 2030 |

||||||

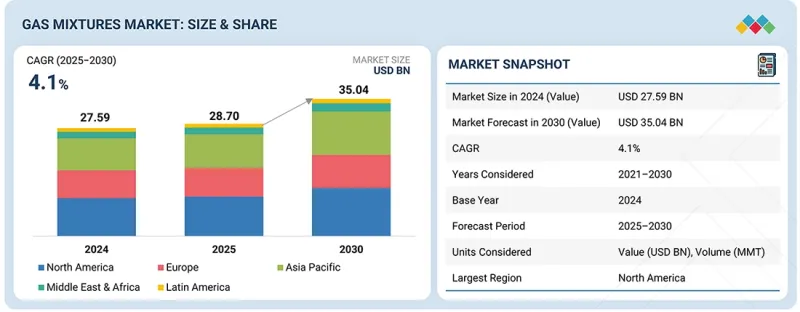

가스 혼합물 시장 규모는 2025년 287억 달러에서 2030년에는 350억 4,000만 달러로 성장하고,ㅡ 예측 기간 중 연평균 복합 성장률(CAGR)은 4.1%를 나타낼 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러), 톤 |

| 부문 | 유형, 최종사용자 산업, 저장, 유통, 운송, 제조 공정, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

반도체 생산 확대, 배출가스 모니터링 기준 강화, 고정밀 산업 공정에 대한 수요 증가로 인해 제어 분위기 형성 및 분석 정확도 확보를 위한 신뢰할 수 있는 응용 분야 특화 솔루션으로서 가스 혼합물의 필요성이 가속화되고 있습니다.

"유형별로는 아르곤 가스 혼합물 부문이 예측 기간 동안 두 번째로 큰 규모를 차지할 것으로 예측됩니다."

아르곤 가스 혼합물 부문은 금속 가공 및 고온 산업 공정에서 널리 사용되기 때문에 예측 기간 동안 두 번째로 큰 시장 규모에 이를 것으로 예측됩니다. 아르곤은 불활성 기체이며 용접 및 절단 응용 분야에서 이상적인 차폐 가스입니다. 산화를 방지하고 용접 작업자에게 안정적인 아크를 제공합니다. 아르곤-이산화탄소, 아르곤-산소 등의 가스 혼합물은 용접 품질 향상과 견고한 구조물 형성에 기여하기 때문에 자동차 제조, 건설, 조선, 중장비 제조 등 다양한 산업 분야에서 일반적으로 사용되고 있습니다. 아르곤 기반 가스 혼합물은 제조 공정에 사용되는 것 외에도 전자 제품 생산 및 제어된 비반응성 환경을 필요로 하는 특수 용도에도 사용됩니다. 그 결과, 다른 가스와 혼합하여 용융, 스패터 제어, 표면 마감 측면에서 맞춤형 가스 혼합물을 제공하여 최적의 솔루션이 될 수 있습니다. 인프라 개발 및 산업 확장의 지속적인 성장으로 아르곤 혼합물은 전체 가스 혼합물 시장에서 두 번째로 큰 부문으로 자리 잡았습니다.

"최종 사용자 산업별로는 식음료 부문이 예측 기간 동안 두 번째로 큰 시장 규모에 이를 것으로 예측됩니다."

식음료 부문은 예측 기간 동안 큰 폭의 성장이 예상됩니다. 이는 생산된 식품의 품질을 보존하고 유지하기 위해 제어된 분위기 기술을 사용하는 식음료 부문에서 가스 혼합물의 사용이 증가하고 있기 때문입니다. 동 업계에서는 식품 포장용 조정 분위기로 질소/이산화탄소 가스 혼합물을 사용하여 저장 기간 연장, 미생물 증식 억제, 제품 신선도 유지를 위해 노력하고 있습니다. 또한, 이 가스는 포장된 육류, 유제품, 구운 식품, 과자, 스낵, 인스턴트 식품의 보관 및 운송 중 산화 및 부패를 방지하는 데에도 일반적으로 사용됩니다. 탄산음료 생산 시 음료 제조업체는 음료의 맛을 일정하게 유지하고 생산 공정 중 안정성을 보장하기 위해 가스를 정확하게 측정하고 혼합해야 합니다. 전 세계적으로 포장 식품 및 편의 식품의 소비가 계속 증가함에 따라 식품 등급 인증 가스 혼합물에 대한 수요는 계속 견고할 것으로 예측됩니다. 또한, 식품 안전 및 품질 보증 기준이 업데이트되고 더욱 엄격해짐에 따라 제조업체는 원래 구성으로 거슬러 올라갈 수 있는 인증된 가스 혼합물을 사용하도록 권장될 것입니다.

"저장, 유통, 운송 측면에서 톤수 부문이 예측 기간 동안 두 번째로 큰 규모를 차지할 것으로 예측됩니다."

톤수 부문은 두 번째 점유율을 차지하고 있으며, 주로 단일 공급원으로부터 대량의 가스를 지속적으로 공급해야 하는 대규모 산업 고객을 대상으로 합니다. 톤수 공급은 일반적으로 현장에서 제조되며 전용 배관 시스템을 통해 공급됩니다. 이러한 시스템은 일반적으로 제철소, 정유공장, 석유화학 플랜트, 대규모 제조업체와 같은 최종 사용자에게 여러 가스 혼합물을 공급합니다. 톤수 공급 모델은 운송 위험을 최소화하면서 신뢰할 수 있는 가스 공급원을 제공하도록 설계되었습니다. 또한, 이러한 공정에서는 공급 중단이 허용되지 않기 때문에 공정 효율을 극대화하기 위한 목적도 있습니다. 또한, 톤수 공급은 장시간 연속 생산에 필수적인 것으로 간주되며, 일정한 유량과 안정된 가스 혼합물이 요구됩니다. 또한, 액체 가스 및 벌크 배송 서비스를 활용하면 여러 고객에게 유연한 서비스를 제공할 수 있는 기회가 생깁니다. 톤수 공급은 일반적으로 장기 계약에 따라 대규모 최종 사용자에게 장기간에 걸쳐 고정된 물량을 공급합니다. 톤수 공급 시스템을 위한 인프라 구축에 투입되는 자본 투자 규모는 공급자와 고객과의 관계 구축 및 유지에 기여하며, 그 결과 톤수 공급 계약에 따른 가스 공급으로 지속적인 수익을 창출합니다.

"제조 공정별로 보면, 수소 제조 기술 부문이 예측 기간 동안 두 번째로 큰 규모를 차지할 것으로 예측됩니다."

수소 제조 기술 부문은 다양한 제조 공정에서 수소가 주요 혼합 요소로 널리 사용됨에 따라 가스 혼합물 시장에서 두 번째로 큰 규모를 차지하고 있습니다. 수소는 열처리, 어닐링, 소결, 반도체 제조 등의 용도에 사용되는 가스 혼합물에서 질소나 아르곤과 자주 혼합됩니다. 수소는 환원 작용을 하기 때문에 산화를 방지하고, 이러한 공정으로 제조된 부품의 표면 품질을 향상시키는 데 도움이 됩니다. 수증기 메탄 개질, 전기분해 및 기타 수소 생성 방법은 가스 혼합물의 정확한 배합에 필요한 고순도 수준의 수소를 혼합하는 데 필요한 수소를 제공합니다. 수소 함유 가스 혼합물의 산업적 용도는 특히 금속 가공, 전자제품 제조 공정 및 청정 에너지 관련 노력에서 지속적으로 확대되고 있습니다. 예를 들어, 반도체 제조에서는 성막 및 에칭 공정에 초순수 수소가스가 필요합니다. 에너지 운반체로서 수소를 활용하려는 전반적인 움직임은 새로운 수소 생산 인프라에 대한 투자를 촉진하고 있으며, 그 결과 가스 혼합물 제조업체를 위한 전체 원료 공급이 증가하고 있습니다.

"예측 기간 동안 아시아태평양이 금액 기준으로 두 번째로 큰 시장 규모에 이를 것으로 예측됩니다."

가스 혼합물 분야에서 금액 기준으로 두 번째로 큰 시장인 아시아태평양은 탄탄한 산업 기반과 첨단 기술 제조 능력의 성장에 힘입어 지속적으로 성장하고 있습니다. 금속 가공, 화학, 식품 가공, 의료, 전자제품 조립 분야의 성장이 이 지역의 가스 혼합물 수요를 주도하고 있습니다. 이러한 가스는 공정 제어 및 품질 보증에 도움이 되기 때문입니다.

중국, 일본, 한국, 인도, 대만, 중국, 일본, 한국, 인도, 대만 등의 국가에서 가스 혼합물 수요가 크게 확대되고 있습니다. 이 지역에는 반도체 제조의 주요 제조업체와 대규모 수출 지향적 제조 클러스터가 다수 존재하기 때문에 특수 가스 및 전자 등급 가스 혼합물에 대한 안정적인 수요가 창출되고 있습니다. 또한, 식품 안전 기준의 강화와 환경 모니터링 규정의 강화로 인해 인증된 교정용 및 보존용 가스 블렌드에 대한 수요가 증가하고 있습니다. 북미는 탄탄한 인프라와 최고 수준의 가격 체계로 인해 전체 가스 혼합물 시장 규모가 가장 크지만, 아시아태평양은 강력한 수요량과 산업 역량이 빠르게 성장하고 있어 북미를 위협하는 경쟁자가 되고 있습니다. 따라서 아시아태평양은 가스 혼합물 시장 규모에서 두 번째로 큰 지역 시장으로 간주됩니다.

세계의 가스 혼합물(Gas Mixture) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 가스 혼합물 시장 : 유형별

제10장 가스 혼합물 시장 : 최종사용자 산업별

제11장 가스 혼합물 시장 : 저장, 유통, 운송별

제12장 가스 혼합물 시장 : 제조 공정별

제13장 가스 혼합물 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

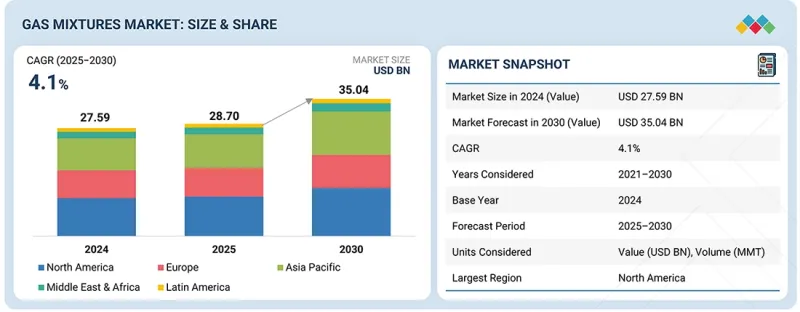

LSH 26.04.13The gas mixtures market is projected to grow from USD 28.70 billion in 2025 to USD 35.04 billion by 2030, at a CAGR of 4.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) Volume (MMT) |

| Segments | Type, End-Use Industry, Storage, Distribution and Transportation, Manufacturing Process, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Expanding semiconductor production, stricter emission monitoring standards, and growing demand for high-precision industrial processes are accelerating the need for gas mixtures as reliable, application-specific solutions for controlled atmospheres and analytical accuracy.

"By type, the argon mixtures segment is expected to be the second-largest segment during the forecast period."

The argon mixtures segment is expected to be the second-largest market during the forecast period, as they are used extensively in metalworking and high-temperature industrial operations. Argon is an inert gas that makes for the ideal shielding gas for welding and cutting applications. It prevents oxidation and provides a stable arc to the welder. Mixtures such as argon-carbon dioxide and argon-oxygen are also commonly used within various industrial sectors, such as automotive manufacturing, construction, shipbuilding, and heavy equipment manufacturing, as they contribute to improved weld quality and assist in creating stronger structures. In addition to being used in fabrication, argon-based mixtures are also used in the production of electronics and in specialized applications that require a controlled, non-reactive environment. As a result, they can provide an optimum solution when mixed with other gases to provide a customized gas mixture with respect to penetration, spatter control, and surface finish. The continued growth of infrastructure development and industrial expansion supports argon-based mixtures' position as the second-largest segment of the total gas mixtures market.

"By end-use industry, the food & beverages segment is expected to be the second-largest market during the forecast period."

The food & beverages segment is expected to grow significantly during the forecast period. This is due to increased use of gas mixtures in the food & beverage sector, which utilizes controlled atmosphere technologies to preserve and maintain the quality of food produced. The industry uses nitrogen/carbon dioxide mixtures as a modified atmosphere for food packaging to extend shelf life, inhibit microbial growth, and maintain the freshness of products. These gases are also commonly used to prevent oxidation and spoilage of packaged meats, dairy products, baked goods, snack foods, and ready-to-eat meals during storage and shipping. When manufacturing carbonated beverages, beverage manufacturers need to accurately measure and blend gases in order to ensure that beverages have consistent flavors and remain stable during production. As globally packaged and convenience food consumption continues to increase, the demand for food-grade certifiable gas mixtures will remain strong. Further, as food safety and quality assurance standards continue to be updated and made more stringent, manufacturers will be encouraged to use certifiable gas blends that can be traced back to their original composition.

"By storage, distribution, and transportation, the tonnage segment is expected to be the second-largest segment during the forecast period."

The tonnage segment represents the second-largest share in the gas mixtures market, catering primarily to very large industrial customers who have a need for large quantities and single sources of continual gas delivery. Tonnage supplies are generally manufactured on-site and delivered by dedicated piping systems; these systems typically supply multiple blended gases to end-users, such as steel mills, refineries, petrochemical plants, and large manufacturers. The tonnage supply model is designed to provide reliable sources of gaseous supplies with minimal risk of transportation, while maximizing process efficiency since these processes cannot tolerate interruptions. In addition, tonnage supplies are seen as essential in those applications that operate under long production runs, whereby there is a requirement for constant flow rates and stable mixtures. With merchant liquid and bulk distribution services, there are opportunities for flexibility in serving multiple customers. Tonnage supply typically provides a fixed supply over longer periods of time to larger end-users under long-term contracts. The level of capital investment in creating the infrastructure for tonnage systems also helps create and maintain supplier/customer relationships, thereby generating recurring revenue for gases supplied under a tonnage supply agreement.

"By manufacturing process, the hydrogen production technologies segment is expected to be the second-largest segment during the forecast period."

The hydrogen production technologies segment represents the second-largest segment in the gas mixtures market, following hydrogen's common use as a key blending element in many different types of manufacturing processes. Hydrogen is frequently blended with nitrogen and argon in gas mixtures used for applications like heat treatment, annealing, sintering, and semiconductor manufacturing. Because hydrogen has reducing properties, it helps to prevent oxidation and improve the quality of surfaces for parts being manufactured by these processes. Steam methane reforming, electrolysis, and other methods to generate hydrogen provide the high purity level needed to mix hydrogen into precise formulations of gas mixtures. The industrial use of hydrogen-containing gas mixtures continues to expand, particularly in metal processing, electronics manufacturing processes, and clean energy initiatives. Semiconductor manufacturing, for example, demands ultra-high purity levels of hydrogen gas for deposition and etching processes. The overall movement toward using hydrogen as an energy carrier is driving investment in new hydrogen production infrastructure, thereby increasing overall feedstock supply for gas mixture manufacturers.

"Asia Pacific is expected to be the second-largest segment in terms of value during the forecast period."

As the second-largest market, by value, in the gas mixtures realm, Asia Pacific continues to be supported by a strong industrial base and growth in high-tech manufacturing capabilities. The growth of the metal fabrication, chemicals, food processing, healthcare, and electronics assembly sectors is driving the demand for gas mixtures in the region, as these gases help with process control and quality assurance.

The demand for gas mixtures in the region is growing significantly in countries such as China, Japan, South Korea, India, and Taiwan. Many primary manufacturers of semiconductor fabrication, and large volume export-oriented manufacturing clusters in the region, create a steady stream of demand for specialty and electronic-grade gas mixtures. Additionally, the increasing food safety requirements and environmental monitoring regulations are driving a heightened demand for certified calibration and preserved gas blends. While North America has the largest overall market value for gas mixtures because of established infrastructure and top-tier pricing structures, Asia Pacific is a close competitor with strong volume demand and has experienced rapid growth in industrial capabilities; therefore, Asia Pacific is considered the second-largest regional market for gas mixtures by value.

By Company Type: Tier 1 - 25%, Tier 2 - 42%, and Tier 3 - 33%

By Designation: C-level Executives - 20%, Directors - 30%, and Others - 50%

By Region: North America - 20%, Europe - 10%, Asia Pacific - 40%, South America - 10%, and Middle East & Africa - 20%

The gas mixtures market include key players such as Linde PLC (Ireland), Air Liquide (France), Air Products and Chemicals, Inc. (US), Messer SE & Co. KGaA (Germany), Iwatani Corporation (Japan), TAIYO NIPPON SANSO CORPORATION (Japan), Westfalen AG (Germany), Gulf Cryo (UAE), The SIAD Group (Italy), and Holston Gases (US)among others are covered in the report.

The study includes an in-depth competitive analysis of these key players in the gas mixture market. It also studies their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the gas mixture market based on type (oxygen mixtures, carbon dioxide mixtures, argon mixtures, hydrogen mixtures, speciality gas mixtures, other mixtures), end-use industry (metal manufacturing & fabrication, food & beverages, healthcare, chemicals, electronics, other end-use industries), storage, distribution, and transportation (merchant liquid/bulk, cylinders & packaged gas, tonnage), manufacturing process (air separation technologies, hydrogen production technologies, other manufacturing process), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa).

The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the gas mixtures market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the gas mixtures market. This report covers a competitive analysis of upcoming startups in the gas mixtures market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall gas mixtures market and the subsegments. It will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (increased demand from semiconductor & electronics manufacturing, retail shift toward extended food & beverage shelf-life product, increased demand from stainless and duplex steel manufacturing using nitrogen-bearing n2/ar blends), restraints (raw gas feedstock volatility in rare and specialty component, high cost of gravimetric precision blending infrastructure), opportunities (on-site micro-blending units for high consumption industrial cluster, high-margin low-volume specialty blend portfolio, specialty gas recovery and re-blending programs), and challenges (maintaining composition stability at ppb and ppm levels, scaling customization without sacrificing throughput)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the gas mixtures market

- Market Development: Comprehensive information about profitable markets across varied regions

Market Diversification: Exhaustive information about products & services, untapped geographies, recent developments, and investments in the gas mixtures market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Linde PLC (Ireland), Air Liquide (France), Air Products and Chemicals, Inc. (US), Messer SE & Co. KGaA (Germany), Iwatani Corporation (Japan), TAIYO NIPPON SANSO CORPORATION (Japan), Westfalen AG (Germany), Gulf Cryo (UAE), The SIAD Group (Italy), Holston Gases (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.4.1 CURRENCY CONSIDERED

- 1.4.2 UNIT CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS & STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GAS MIXTURES MARKET

- 3.2 GAS MIXTURES MARKET, BY TYPE AND REGION

- 3.3 GAS MIXTURES MARKET, BY END-USE INDUSTRY

- 3.4 GAS MIXTURES MARKET, BY STORAGE, DISTRIBUTION, AND TRANSPORTATION

- 3.5 GAS MIXTURES MARKET, BY MANUFACTURING PROCESS

- 3.6 GAS MIXTURES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 High demand from manufacturers of semiconductors and electronics

- 4.2.1.2 Retail shift toward extended shelf-life of food and beverage products

- 4.2.1.3 Growing demand from manufacturers of stainless and duplex steel

- 4.2.2 RESTRAINTS

- 4.2.2.1 Volatile availability of raw gas feedstock for rare and specialty components

- 4.2.2.2 High cost of gravimetric precision blending infrastructure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 On-site micro-blending units for high-consumption industrial clusters

- 4.2.3.2 High-margin, low-volume specialty blend portfolios

- 4.2.3.3 Specialty gas recovery and re-blending programs

- 4.2.4 CHALLENGES

- 4.2.4.1 Maintaining composition stability at ppb and ppm levels

- 4.2.4.2 Scaling customization without compromising throughput

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 LONG-TERM STABILITY OF REACTIVE AND TRACE-LEVEL MULTI-COMPONENT MIXTURES

- 4.3.2 SCALABLE SUB-PPB BLENDING WITH TRACEABLE UNCERTAINTY CONTROL

- 4.3.3 ADVANCED CYLINDER MATERIAL AND SURFACE ENGINEERING FOR ULTRA-SENSITIVE BLENDS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: STRATEGIC INITIATIVES IN GAS MIXTURES MARKET

- 4.5.1.1 Linde plc (Ireland)

- 4.5.1.2 Air Liquide (France)

- 4.5.1.3 Air Products and Chemicals, Inc. (US)

- 4.5.2 TIER 2 PLAYERS: KEY STRATEGIC MOVES AND INNOVATIONS

- 4.5.2.1 Messer SE & Co. KGaA (Germany)

- 4.5.2.2 Taiyo Nippon Sanso Corporation (Japan)

- 4.5.3 TIER 3 PLAYERS: EMERGING STRATEGIES AND REGIONAL POSITIONING

- 4.5.3.1 Yingde Gases Group (China) & Guangdong Huate Gas Co., Ltd. (China)

- 4.5.3.2 Coregas Pty Ltd & Gulf Cryo (Australia & Middle East)

- 4.5.1 TIER 1 PLAYERS: STRATEGIC INITIATIVES IN GAS MIXTURES MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES' ANALYSIS

- 5.1.1 THREAT FROM NEW ENTRANTS

- 5.1.2 THREAT FROM SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 INDUSTRIAL MANUFACTURING OUTPUT CYCLES

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF GAS MIXTURE TYPES, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 280440, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.2 EXPORT DATA RELATED TO HS CODE 280440, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.3 IMPORT DATA RELATED TO HS CODE 280430, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.4 EXPORT DATA RELATED TO HS CODE 280430, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.5 IMPORT DATA RELATED TO HS CODE 281121, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.6 EXPORT DATA RELATED TO HS CODE 281121, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.7 IMPORT DATA RELATED TO HS CODE 280421, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.8 EXPORT DATA RELATED TO HS CODE 280421, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.9 IMPORT DATA RELATED TO HS CODE 280410, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.10 EXPORT DATA RELATED TO HS CODE 280410, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.7 KEY CONFERENCES & EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 LINDE PLC: CARBOFLEX(R) ATMOSPHERE CONTROL

- 5.10.2 AIR LIQUIDE: CALIBRATION GAS MIXTURES (EMISSION MONITORING & QUALITY ASSURANCE)

- 5.10.3 AIR PRODUCTS AND CHEMICALS, INC.: NITROGEN-HYDROGEN GAS MIXTURE MONITORING IN SINTERING APPLICATIONS

- 5.11 IMPACT OF 2025 US TARIFFS ON GAS MIXTURES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT OF COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 GRAVIMETRIC HIGH-PRECISION BLENDING SYSTEMS

- 6.1.2 REAL-TIME GAS CHROMATOGRAPHY (GC) & ANALYTICAL VERIFICATION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SMART GAS DENSITY & THERMAL CONDUCTIVITY SENSORS

- 6.2.2 CRYOGENIC STORAGE & MICROBULK DELIVERY SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ON-SITE MODULAR GAS GENERATION SYSTEMS

- 6.3.2 HYDROGEN & DECARBONIZATION-DRIVEN GAS BLENDING TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027): PERFORMANCE STABILIZATION AND DIGITAL QUALITY CONTROL PHASE

- 6.4.2 MID-TERM (2027-2030): SCALABLE LOCALIZED PRODUCTION AND HYBRID BLENDING INFRASTRUCTURE

- 6.4.3 LONG-TERM (2030-2035+): AUTONOMOUS PRECISION BLENDING AND LOW-CARBON GAS ECOSYSTEM INTEGRATION

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 APPROACH

- 6.5.3 TOP APPLICANTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 GREEN HYDROGEN BLENDING FOR INDUSTRIAL PROCESSES

- 6.6.2 SYNTHETIC MICROBIAL GROWTH ATMOSPHERES

- 6.6.3 BIOENGINEERED ORGAN PRESERVATION GASES

- 6.6.4 SMART INDOOR AIR QUALITY MIXTURES

- 6.7 IMPACT OF AI/GENERATIVE AI ON GAS MIXTURES MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN GAS MIXTURES

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN GAS MIXTURES MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN GAS MIXTURES MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GAS MIXTURES

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GAS MIXTURES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 GAS MIXTURES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 OXYGEN MIXTURES

- 9.2.1 OXYGEN MIXTURES ENABLE CONTROLLED OXIDATION PERFORMANCE UNDER STRICT SAFETY PARAMETERS

- 9.3 NITROGEN MIXTURES

- 9.3.1 NITROGEN MIXTURES PROVIDE INERT STABILITY AND ULTRA-HIGH PURITY MATRIX CONTROL

- 9.4 CARBON DIOXIDE MIXTURES

- 9.4.1 CARBON DIOXIDE MIXTURES OFFER DENSITY-DRIVEN PHASE BEHAVIOR AND SOLUBILITY CONTROL

- 9.5 ARGON MIXTURES

- 9.5.1 ARGON MIXTURES PROVIDE INERT ATOMIC STABILITY WITH PRECISE THERMAL MANAGEMENT

- 9.6 HYDROGEN MIXTURES

- 9.6.1 HYDROGEN MIXTURES ENABLE HIGH DIFFUSIVITY REDUCTION ENVIRONMENTS UNDER CONTROLLED COMPOSITION

- 9.7 SPECIALTY GAS MIXTURES

- 9.7.1 SPECIALTY GAS MIXTURES DELIVER MOLECULAR-LEVEL PRECISION WITH VALIDATED COMPOSITIONAL INTEGRITY

- 9.8 OTHER MIXTURES

10 GAS MIXTURES MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 METAL MANUFACTURING & FABRICATION

- 10.2.1 STEEL OUTPUT EXPANSION AND FABRICATION DEMAND TO DRIVE GAS MIXTURE OPTIMIZATION NEEDS

- 10.3 FOOD & BEVERAGES

- 10.3.1 FOCUS ON STABILIZING BEVERAGE OUTPUT AND POST-HARVEST GAS ADOPTION TO DRIVE DEMAND FOR FOOD GRADE GAS MIXTURES

- 10.4 MEDICAL & HEALTHCARE

- 10.4.1 RISING RESPIRATORY CARE AND SURGICAL VOLUMES TO DRIVE DEMAND FOR MEDICAL GAS MIXTURES

- 10.5 CHEMICALS

- 10.5.1 EXPANDING CLEAN CHEMICAL INVESTMENTS AND SPECIALTY OUTPUT TO DRIVE MARKET

- 10.6 ELECTRONICS

- 10.6.1 RISING SEMICONDUCTOR COMPLEXITY AND WAFER VOLUMES TO DRIVE DEMAND FOR SPECIALTY GAS MIXTURES

- 10.7 OTHER END-USE INDUSTRIES

11 GAS MIXTURES MARKET, BY STORAGE, DISTRIBUTION, AND TRANSPORTATION

- 11.1 INTRODUCTION

- 11.2 CYLINDERS & PACKAGED GAS

- 11.2.1 RISING DEMAND FOR PRECISION AND DECENTRALIZED SUPPLY TO STRENGTHEN CYLINDER-BASED GAS MIXTURE DISTRIBUTION

- 11.3 MERCHANT LIQUID/BULK

- 11.3.1 EXPANDING INDUSTRIAL SCALE OPERATIONS TO INCREASE RELIANCE ON MERCHANT LIQUID AND BULK GAS SUPPLY SYSTEMS

- 11.4 TONNAGE

- 11.4.1 LARGE-SCALE DEMAND FOR INDUSTRIAL GAS MIXTURES TO DRIVE ADOPTION OF ON-SITE TONNAGE GAS PRODUCTION SYSTEMS

12 GAS MIXTURES MARKET, BY MANUFACTURING PROCESS

- 12.1 INTRODUCTION

- 12.2 AIR SEPARATION TECHNOLOGIES

- 12.2.1 AIR SEPARATION TECHNOLOGIES ENABLE SCALABLE PRODUCTION OF HIGH PURITY INDUSTRIAL GAS MIXTURES

- 12.2.2 CRYOGENIC AIR SEPARATION

- 12.2.3 NON-CRYOGENIC AIR SEPARATION

- 12.3 HYDROGEN PRODUCTION TECHNOLOGIES

- 12.3.1 HYDROGEN PRODUCTION TECHNOLOGIES ENABLE CONTROLLED SYNTHESIS OF HIGH PURITY HYDROGEN STREAMS

- 12.3.2 STEAM REFORMING

- 12.3.3 PARTIAL OXIDATION

- 12.3.4 PLASMA REFORMING

- 12.4 OTHER MANUFACTURING PROCESSES

- 12.4.1 PRESSURE SWING ADSORPTION

13 GAS MIXTURES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Industrial expansion and healthcare trends to drive demand for gas mixtures

- 13.2.2 CANADA

- 13.2.2.1 Canada's expanding industries to drive demand for gas mixtures

- 13.2.3 MEXICO

- 13.2.3.1 Focus on expanding manufacturing to drive demand for gas mixtures

- 13.2.1 US

- 13.3 ASIA PACIFIC

- 13.3.1 CHINA

- 13.3.1.1 Industrial and high-tech expansion to drive demand

- 13.3.2 INDIA

- 13.3.2.1 Industrial expansion to drive demand for gas mixtures

- 13.3.3 JAPAN

- 13.3.3.1 Focus on growth of industrial recovery and technology to drive demand for gas mixtures

- 13.3.4 SOUTH KOREA

- 13.3.4.1 Emphasis on high-tech expansion to accelerate demand for gas mixtures

- 13.3.5 REST OF ASIA PACIFIC

- 13.3.1 CHINA

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Germany's industrial rebound to accelerate gas mixture demand

- 13.4.2 FRANCE

- 13.4.2.1 Green transition in country to boost demand for gas mixtures

- 13.4.3 UK

- 13.4.3.1 Rapid growth of manufacturing sector to strengthen demand for gas mixtures

- 13.4.4 BELGIUM

- 13.4.4.1 Belgium's industrial revival to boost demand for specialty gas

- 13.4.5 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Focus on industrial expansion to accelerate demand for gas mixtures

- 13.5.1.2 UAE

- 13.5.1.2.1 Need for gas mixtures for industrial surge to drive market

- 13.5.1.3 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 South Africa's industrial recovery to lift demand for gas mixtures

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Emphasis on industrial and healthcare expansion to drive demand for gas mixtures

- 13.6.2 ARGENTINA

- 13.6.2.1 Focus on industrial recovery to drive demand for gas mixtures

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 End-use industry footprint

- 14.6.5.5 Storage, distribution, and transportation footprint

- 14.6.5.6 Manufacturing process footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 List of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8.1 COMPANY VALUATION

- 14.8.2 FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 LINDE PLC

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 AIR LIQUIDE

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 AIR PRODUCTS AND CHEMICALS, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 MESSER SE & CO. KGAA

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.3.2 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 IWATANI CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 TAIYO NIPPON SANSO CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.4 MnM view

- 15.1.7 WESTFALEN AG

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.4 MnM view

- 15.1.8 GULF CRYO

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Expansions

- 15.1.8.4 MnM view

- 15.1.9 THE SIAD GROUP

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Expansions

- 15.1.9.4 MnM view

- 15.1.10 HOLSTON GASES

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 MnM view

- 15.1.1 LINDE PLC

- 15.2 OTHER PLAYERS

- 15.2.1 AXCEL GASES

- 15.2.2 BHORUKA SPECIALTY GASES PVT LTD.

- 15.2.3 ELLENBARRIE INDUSTRIAL GASES LTD

- 15.2.4 GOYAL MG GASES PVT. LTD.

- 15.2.5 STEELMAN GASES PVT. LTD.

- 15.2.6 CHEMIX SPECIALTY GASES AND EQUIPMENT

- 15.2.7 SPECGAS, INC.

- 15.2.8 INGAS

- 15.2.9 WESCO GAS & WELDING SUPPLY, INC. (WESCO)

- 15.2.10 MULTIGAS

- 15.2.11 PT SAMATOR INDO GAS TBK

- 15.2.12 BRISTOL GASES

- 15.2.13 BUZWAIR SPECIALTY GASES (BSG)

- 15.2.14 YIGAS INTERNATIONAL LIMITED

- 15.2.15 MESA SPECIALTY GASES & EQUIPMENT

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.2.2 BOTTOM-UP APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 SUPPLY-SIDE APPROACH

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 RESEARCH ASSUMPTIONS

- 16.7 RISK ASSESSMENT

- 16.8 GROWTH RATE ASSUMPTIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS