|

시장보고서

상품코드

1996976

의료용 가구 시장 예측(-2031년) : 제품·서비스별, 용도별, 최종사용자별, 지역별Medical Furniture Market By Product [Medical Beds (Electric, Manual), Chairs (Gynecology, Bariatric), Tables, Cabinets, Trolleys], By Application [Long-term, Patient Care & Accommodation], End User [Hospitals, ASCs], By Region - Global Forecast to 2031 |

||||||

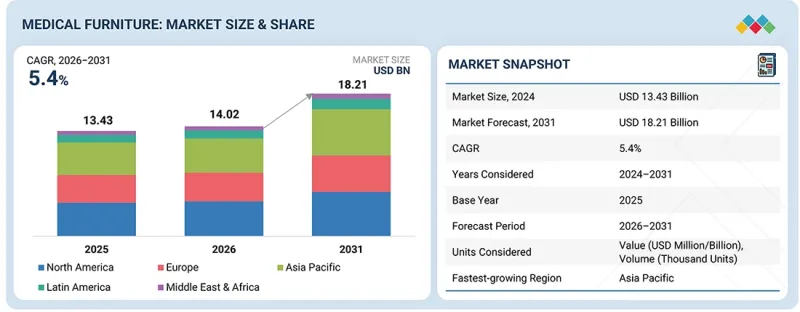

세계의 의료용 가구 시장 규모는 2026년 140억 2,000만 달러에서 2031년까지 182억 1,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 5.4%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품·서비스별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

의료용 가구 시장은 의료 인프라의 확대, 입원율 증가, 만성질환 증가, 병원, 외래수술센터(ASC), 장기 요양 시설의 첨단 인체공학적 환자 중심 치료 환경에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 현대화를 위한 정부의 투자와 스마트하고 디지털로 통합된 가구로의 전환은 그 보급을 더욱 가속화하고 있습니다. 그러나 높은 자본 비용, 공공 병원 및 신흥 시장 병원의 예산 제약, 긴 갱신 주기, 오래된 시설의 인프라 비호환성, 저비용의 현지 대체품의 가용성 등으로 인해 시장 확대가 제한되고 있으며, 이로 인해 조달 및 업그레이드 결정이 늦어지고 있습니다.

제품 및 서비스 부문별로 시장은 의료용 침대, 의자 및 좌석, 테이블, 스트레처, 스트레처, 트롤리 및 카트, 캐비닛, 보관함, 사물함, 서비스, 기타로 분류됩니다. 이 중 의자 및 좌석 부문은 수술 건수 증가, 진단 절차 확대, 수술실 현대화에 대한 투자 확대로 인해 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예측됩니다. 수술대 부문은 다시 일반 수술대, 정형외과수술대, 산부인과 수술대, 영상 진단용 수술대, 검사대, 기타 수술대로 세분화됩니다. 이러한 하위 부문의 성장은 만성질환의 유병률 증가, 최소침습 수술에 대한 수요 증가, 전문 의료 서비스 확대에 힘입어 성장세를 보이고 있습니다. 전동식 포지셔닝, 방사선 투과성 표면, 영상 진단 장비와의 호환성, 모듈식 설계 등의 기술 발전은 제품의 부가가치를 높이고 교체 수요를 견인하고 있습니다. 또한 외래수술센터(ASC) 및 진단 시설 증가로 첨단 수술대 도입이 가속화되고 있습니다. 병원이 수술의 효율성과 환자 안전을 향상시키기 위해 인프라를 업그레이드함에 따라 전문적이고 다기능적인 수술대에 대한 수요는 크게 확대될 것으로 예측됩니다.

최종사용자별로 의료용 가구 시장은 병원, 진료소, 외래수술센터(ASC), 장기 요양 및 요양 시설, 기타 최종사용자로 분류됩니다. 이 중 외래수술센터(ASC) 부문은 2025년 시장에서 두 번째로 큰 점유율을 차지할 것으로 예측됩니다. 이는 시술 비용의 감소, 입원 기간 단축 및 상환 인센티브의 개선에 의해 주도되고 있습니다. ASC는 선진국과 신흥 시장에서 빠르게 성장하고 있으며, 수술대, 시술용 의자, 스트레처, 캐비닛, 회복용 침대 등 전문 의료용 가구에 대한 많은 투자가 필요합니다. 최소침습 수술과 선택적 수술 증가는 고성능, 소형, 워크플로우에 최적화된 가구에 대한 수요를 더욱 촉진하고 있습니다. 또한 ASC 네트워크에 대한 사모펀드 투자와 탈중앙화 의료에 대한 지향이 지속적인 수용력 확대를 지원하고 있으며, ASC는 가장 빠르게 성장하는 최종사용자 부문으로 자리매김하고 있습니다.

의료용 가구 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 등 5개 주요 지역으로 분류됩니다.

아시아태평양은 주요 경제권의 의료 서비스 확대, 급속한 인구 고령화, 의료비 증가로 인해 가장 높은 CAGR로 성장할 것으로 추정됩니다. 인도의 의료 부문은 병원, 진단 및 전문 의료에 대한 투자 증가에 힘입어 놀라운 속도로 성장하고 있으며, 2025년까지 6,380억 달러에 달할 것으로 예상되고 있습니다. 이로 인해 의료용 침대, 스트레처, 테이블 및 환자 치료용 가구에 대한 수요가 가속화되고 있습니다. 세계 최고의 고령화 사회인 일본은 1인당 5,251달러, GDP의 11.5%를 의료비로 지출하고 있으며, 급성기 의료, 노인 의료, 장기요양시설의 지속적인 개보수를 추진하고 있습니다. 중국에는 65세 이상 노인이 2억 1,676만 명에 달하고, 재활센터, 요양시설 및 병원의 수용능력 확대에 대한 요구가 증가하고 있습니다. 또한 아시아태평양 국가들은 의료 인프라의 현대화가 빠르게 진행되고 있으며, 보험 가입률의 상승과 의료관광 증가를 볼 수 있습니다. 이러한 추세와 함께 아시아태평양은 예측 기간 중 의료용 가구 시장에서 가장 빠르게 성장하는 지역이 될 것입니다.

의료용 가구 시장의 주요 기업 : Arjo(스웨덴), Getinge AB(스웨덴), Baxter(미국), Stryker(미국), PARAMOUNT BED(일본), GPC Medical Ltd(인도), MillerKnoll, Inc.(미국), KOVONAX spol. s r.o.(체코), Drive DeVilbiss Healthcare(미국), LINET Group SE(Netherlands), Joerns Healthcare(미국), Stiegelmeyer GmbH & Co. KG(독일), Steris Corporation(미국), Savaria(캐나다), PROMOTAL(France), Skytron, LLC(미국), GF Health Products, Inc.(미국), Midmark Corporation(미국), Opera Beds(영국), medifa(독일), Malvestio Spa(이탈리아), Merivaara Corp(핀란드), Amico Group of Companies(캐나다), Narang Medical Limited(인도), Umano Medical Inc.(캐나다).

조사 범위

이 보고서는 제품 및 서비스, 용도, 최종사용자, 지역 등 다양한 부문을 기반으로 의료용 가구 시장을 분석하고 시장 규모와 미래 성장 잠재력을 추정하는 것을 목표로 합니다. 또한 주요 기업의 기업 개요, 제공 서비스, 최근 동향 및 주요 시장 전략과 함께 주요 시장 진출기업의 경쟁 분석도 포함하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 전체 의료용 가구 시장의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공하여 시장 리더와 신규 시장 진출기업에게 도움을 줄 것입니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진출 전략을 수립할 수 있는 인사이트을 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트을 제공

- 주요 시장 성장 촉진요인(만성질환 부담 증가 및 입원율 증가, 고령화로 인한 장기요양 및 노인요양 수요 증가, 의료 현대화를 위한 정부의 구상), 제약요인(고급 의료용 가구의 높은 비용 및 제품수명주기별 낮은 갱신율), 기회요인(비만 환자를 위한 의료용 가구 수요 증가), 도전요인(맞춤형 맞춤화 제한으로 프리미엄 제품 채택 저조) 과제(커스터마이징의 한계와 낮은 프리미엄 제품 채택률이 의료용 가구 시장의 성장을 저해하고 있음) 분석

- 시장 침투: 이 보고서에는 세계 의료용 가구 시장의 주요 기업이 제공하는 제품에 대한 광범위한 정보가 포함되어 있습니다. 이 보고서는 제품 및 서비스, 용도, 최종사용자, 지역 등 다양한 부문으로 구성되어 있습니다.

- 제품 강화 및 혁신 : 세계 의료용 가구 시장의 신제품 출시 및 예상 동향에 대한 종합적인 세부 사항

- 시장 개발: 제품/서비스, 용도, 최종사용자, 지역별, 수익성 높은 성장 시장에 대한 심층적인 인사이트와 분석

- 시장 다각화 : 세계 의료용 가구 시장의 신제품 출시, 시장 확대, 현재 진행 상황 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : 세계 의료용 가구 시장에서 주요 경쟁사 시장 점유율, 성장 계획, 제품 라인업 및 생산 능력에 대한 철저한 평가

자주 묻는 질문

목차

제1장 서론

제2장 벤처 캐피털리스트용 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 의료용 가구 시장(제품별·서비스별)

제10장 의료용 가구 시장(용도별)

제11장 의료용 가구 시장(최종사용자별)

제12장 의료용 가구 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

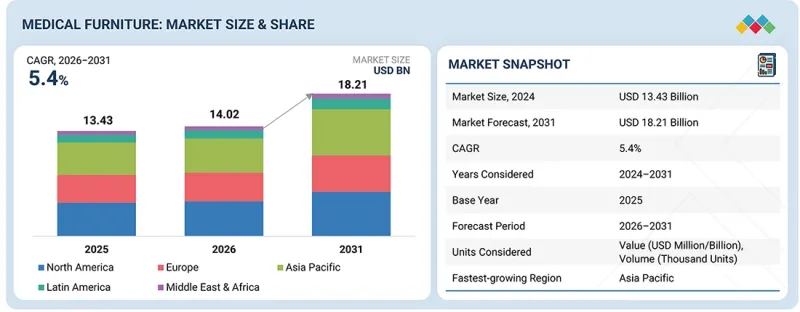

KSA 26.04.21The global medical furniture market is projected to reach USD 18.21 billion by 2031 from USD 14.02 billion in 2026, at a CAGR of 5.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Products & Services, Application, End User, and Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The medical furniture market is driven by expanding healthcare infrastructure, rising hospitalization rates, increasing chronic disease burden, and growing demand for advanced, ergonomic, and patient-centric care environments across hospitals, ASCs, and long-term care facilities. Government investments in modernization and the shift toward smart, digitally integrated furniture further accelerate adoption. However, market expansion is restrained by high capital costs, budget constraints in public and emerging-market hospitals, long replacement cycles, infrastructural incompatibilities in older facilities, and the availability of low-cost local alternatives, which collectively slow procurement and upgrade decisions.

"By products & services segment, the chairs & seating segment is projected to grow at the fastest CAGR in the medical furniture market during the forecast period."

By products & services segment, the market is divided into medical beds, chairs & seatings, tables, stretchers, trolleys & carts, cabinets, storage units, lockers, services, and others. Among these, the chairs & segment sub-segment is projected to grow at the fastest CAGR during the forecast period, owing to rising surgical volumes, expanding diagnostic procedures, and increasing investments in operating room modernization. The tables segment is further bifurcated into general surgery operating tables, orthopedic tables, gynecology/obstetric tables, imaging tables, examination tables, and other tables. Growth across these sub-segments is supported by the increasing prevalence of chronic diseases, higher demand for minimally invasive surgeries, and expansion of specialty care services. Technological advancements such as motorized positioning, radiolucent surfaces, imaging compatibility, and modular designs are enhancing product value and driving replacement demand. Additionally, growing ambulatory surgery centers and diagnostic facilities are accelerating procurement of advanced tables. As hospitals upgrade infrastructure to improve procedural efficiency and patient safety, demand for specialized and multi-functional tables is expected to expand significantly.

"By end user, the ambulatory surgery centers segment accounted for the second largest share in the medical furniture market in 2025."

By end users, the medical furniture market is divided into hospitals, clinics, ambulatory surgery centers, long-term & nursing facilities, and other end users. Among these, in 2025, the ambulatory surgery centers (ASCs) segment held the second largest share in the market. This is driven by lower procedure costs, reduced hospital stays, and improved reimbursement incentives. ASCs are rapidly expanding across developed and emerging markets, requiring substantial investments in specialized medical furniture, including operating tables, procedure chairs, stretchers, cabinets, and recovery beds. Increasing adoption of minimally invasive and elective procedures further boosts demand for high-performance, compact, and workflow-optimized furniture. Additionally, private equity investment in ASC networks and the preference for decentralized care support continuous capacity expansion, positioning ASCs as the fastest-growing end-user segment.

"The Asia Pacific region segment is projected to grow at the fastest CAGR in the medical furniture market during the forecast period."

The medical furniture market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The Asia Pacific region is estimated to grow at the fastest CAGR due to substantial healthcare expansion, rapid demographic aging, and rising healthcare spending across major economies. India's healthcare sector is growing at an exceptional pace, projected to reach USD 638 billion by 2025, supported by increasing investments in hospitals, diagnostics, and specialty care, which accelerates demand for medical beds, stretchers, tables, and patient-care furniture. Japan, one of the world's oldest nations, spends USD 5,251 per capita on health, 11.5% of its GDP, driving continuous upgrades in acute, geriatric, and long-term care facilities. China's aging population of 216.76 million people aged 65+ is intensifying the need for rehabilitation centers, nursing care, and hospital capacity expansion. Additionally, Asia Pacific countries are rapidly modernizing their healthcare infrastructure and witnessing rising insurance penetration and medical tourism. Together, these developments make Asia Pacific the fastest-growing region for medical furniture during the forecast period.

A breakdown of the primary participants (supply-side) for the medical furniture market referred to in this report is provided below:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: C-level - 50%, Director Level - 30%, and Others - 20%

- By Region: North America - 30%, Europe - 25%, Asia Pacific - 20%, Latin America - 15%, Middle East & Africa - 10%

Prominent players in the medical furniture market: Arjo (Sweden), Getinge AB (Sweden), Baxter (US), Stryker (US), PARAMOUNT BED CO., LTD. (Japan), GPC Medical Ltd (India), MillerKnoll, Inc. (US), KOVONAX spol. s r.o. (Czech Republic), Drive DeVilbiss Healthcare (US), LINET Group SE (Netherlands), Joerns Healthcare (US), Stiegelmeyer GmbH & Co. KG (Germany), Steris Corporation (US), Savaria (Canada), PROMOTAL (France), Skytron, LLC (US), GF Health Products, Inc. (US), Midmark Corporation (US), Opera Beds (UK), medifa (Germany), Malvestio Spa (Italy), Merivaara Corp (Finland), Amico Group of Companies (Canada), Narang Medical Limited (India), and Umano Medical Inc. (Canada).

Research Coverage

The report analyzes the medical furniture market and aims to estimate the market size and future growth potential of this market based on various segments such as products & services, application, end user, and region. The report also includes a competitive analysis of the key players in this market along with their company profiles, service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall medical furniture market. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (rising burden of chronic diseases & increasing hospitalization rates, aging population driving long-term and geriatric care needs, and government initiatives for healthcare modernization), restraints (high cost of advanced medical furniture & long product life cycle leading to slow replacement rate), opportunities (rising need for bariatric care furniture), and challenges (limited customization and low premium product adoption is challenging the medical furniture market growth)

- Market Penetration: It includes extensive information on products offered by the major players in the global medical furniture market. The report consists of various segments in products & services, applications, end users, and regions.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global medical furniture market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by products & services, application, end user, and region

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global medical furniture market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products, and capacities of the major competitors in the global medical furniture market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 VENTURE CAPITALISTS EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 MEDICAL FURNITURE MARKET OVERVIEW

- 3.2 NORTH AMERICA: MEDICAL FURNITURE MARKET, BY END USER

- 3.3 GEOGRAPHIC SNAPSHOT OF MEDICAL FURNITURE MARKET (2025)

- 3.4 GEOGRAPHIC MIX: MEDICAL FURNITURE MARKET, 2026-2031 (USD MILLION)

- 3.5 MEDICAL FURNITURE MARKET: DEVELOPING VS. DEVELOPED MARKETS, 2026 VS. 2031 (USD MILLION)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising chronic disease burden and hospital admissions

- 4.2.1.2 Aging population drives demand for long-term care medical furniture

- 4.2.1.3 Rising government healthcare investments

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital costs and long replacement cycles

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising obesity prevalence to drive demand for specialized bariatric medical furniture

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited customization and low-premium product adoption

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MEDICAL FURNITURE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL DURABLE MEDICAL EQUIPMENT INDUSTRY

- 5.2.4 TRENDS IN MEDICAL FACILITY PRODUCTS INDUSTRY

- 5.3 REIMBURSEMENT ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 PRICING ANALYSIS (2023-2025)

- 5.7.1 AVERAGE SELLING PRICE TREND, BY PRODUCT (2023-2025)

- 5.7.2 AVERAGE SELLING PRICE TREND, BY REGION (2023-2025)

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 9402)

- 5.8.2 EXPORT DATA (HS CODE 9402)

- 5.9 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11 INVESTMENT AND FUNDING SCENARIO

- 5.12 IMPACT OF 2025 US TARIFF - MEDICAL FURNITURE MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ELECTROMECHANICAL ACTUATION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 IOT AND REMOTE MONITORING INTEGRATION

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2031) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AI-ENABLED SMART ICU BEDS

- 6.5.2 CONNECTED & INTEROPERABLE HOSPITAL FURNITURE

- 6.6 IMPACT OF AI/GEN AI ON MEDICAL FURNITURE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST OPERATIONAL PRACTICES IN MEDICAL FURNITURE MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN MEDICAL FURNITURE MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN POWERED MEDICAL FURNITURE MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.3 US MEDICAL FURNITURE HCPCS CODING LANDSCAPE

- 7.3.1 HCPCS CODE ARCHITECTURE AND SEGMENT CONCENTRATION

- 7.3.2 CLAIMS-BASED DEMAND ANALYSIS AND VOLUME STABILITY

- 7.3.3 COMPETITIVE BIDDING AND PRICING PRESSURE ANALYSIS

- 7.3.4 STRATEGIC INSIGHTS AND CONCLUSION

- 7.4 PURCHASING MODEL

- 7.4.1 PROVIDERS PURCHASING MEDICAL FURNITURE

- 7.4.2 PURCHASING BEHAVIOR

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 MEDICAL FURNITURE MARKET, BY PRODUCT & SERVICE

- 9.1 INTRODUCTION

- 9.2 MEDICAL BEDS

- 9.2.1 BY PRODUCT

- 9.2.1.1 Electric beds

- 9.2.1.1.1 Electric beds to dominate medical beds segment

- 9.2.1.2 Semi-electric beds

- 9.2.1.2.1 Cost-performance advantage accelerates adoption

- 9.2.1.3 Manual beds

- 9.2.1.3.1 Cost-effective infrastructure expansion to drive demand

- 9.2.1.1 Electric beds

- 9.2.2 BY TYPE

- 9.2.2.1 Critical care beds

- 9.2.2.1.1 Increasing prevalence of chronic diseases to drive segmental growth

- 9.2.2.2 Long-term & home care beds

- 9.2.2.2.1 Rising long-term diseases to drive growth

- 9.2.2.3 Maternity & pediatric beds

- 9.2.2.3.1 Expanding maternal and neonatal care infrastructure to drive segment

- 9.2.2.4 General ward beds

- 9.2.2.4.1 High inpatient volumes driving sustained demand for general ward beds

- 9.2.2.5 Other beds

- 9.2.2.1 Critical care beds

- 9.2.1 BY PRODUCT

- 9.3 CHAIRS & SEATING

- 9.3.1 GYNECOLOGY/OB-GYN CHAIRS

- 9.3.1.1 Rising women's preventive healthcare drives demand

- 9.3.2 DIALYSIS CHAIRS

- 9.3.2.1 Rising incidence of chronic kidney disease drives demand

- 9.3.3 BARIATRIC CHAIRS

- 9.3.3.1 Rising global obesity rates drive demand

- 9.3.4 OTHER CHAIRS

- 9.3.1 GYNECOLOGY/OB-GYN CHAIRS

- 9.4 TABLES

- 9.4.1 GENERAL SURGERY OPERATING TABLES

- 9.4.1.1 High surgical volumes drive demand

- 9.4.2 GYNECOLOGY/OBSTETRIC TABLES

- 9.4.2.1 Continuous childbirth volumes and reproductive care to drive demand

- 9.4.3 ORTHOPEDIC TABLES

- 9.4.3.1 Rising musculoskeletal disorders and joint replacements to drive demand

- 9.4.4 EXAMINATION TABLES

- 9.4.4.1 High outpatient volumes sustain demand

- 9.4.5 IMAGING TABLES

- 9.4.5.1 Rising diagnostic imaging volumes to drive demand

- 9.4.6 OTHER TABLES

- 9.4.1 GENERAL SURGERY OPERATING TABLES

- 9.5 STRETCHERS

- 9.5.1 EMERGENCY STRETCHERS

- 9.5.1.1 Rising emergency admissions and trauma cases to drive demand

- 9.5.2 SPECIALTY STRETCHERS

- 9.5.2.1 Procedure-specific clinical needs to drive demand

- 9.5.3 TRANSFER & PROCEDURE TROLLEYS

- 9.5.3.1 Expanding ambulatory surgeries to accelerate demand

- 9.5.1 EMERGENCY STRETCHERS

- 9.6 CABINETS, LOCKERS, AND STORAGE UNITS

- 9.6.1 BEDSIDE & WARD STORAGE

- 9.6.1.1 Universal inpatient deployment to drive segment

- 9.6.2 CLINICAL STORAGE

- 9.6.2.1 Regulatory compliance and infection control to drive demand

- 9.6.3 PERSONAL & STAFF STORAGE

- 9.6.3.1 Expanding healthcare workforce and hygiene protocols to drive segment

- 9.6.4 OTHER CABINETS, LOCKERS, AND STORAGE UNITS

- 9.6.1 BEDSIDE & WARD STORAGE

- 9.7 TROLLEYS & CARTS

- 9.7.1 INSTRUMENT TROLLEYS

- 9.7.1.1 Essential surgical workflow requirements to drive segmental growth

- 9.7.2 LOGISTIC & UTILITY CARTS

- 9.7.2.1 Increasing hospital throughput to drive demand

- 9.7.3 ANESTHESIA CARTS

- 9.7.3.1 Rising surgical procedures and medication safety to drive segment growth

- 9.7.4 OTHER TROLLEYS & CARTS

- 9.7.1 INSTRUMENT TROLLEYS

- 9.8 SERVICES

- 9.8.1 MAINTENANCE & ANNUAL MAINTENANCE CONTRACTS

- 9.8.1.1 Growing installed base of powered furniture drives segment dominance

- 9.8.2 INSTALLATION & COMMISSIONING

- 9.8.2.1 Expanding healthcare infrastructure to drive demand

- 9.8.3 OTHER SERVICES

- 9.8.1 MAINTENANCE & ANNUAL MAINTENANCE CONTRACTS

- 9.9 OTHER PRODUCTS

10 MEDICAL FURNITURE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 PATIENT CARE & ACCOMMODATION

- 10.2.1 LARGE BASE OF INSTALLED BEDS TO DRIVE SEGMENT

- 10.3 CRITICAL CARE FACILITIES

- 10.3.1 RISING CHRONIC DISEASE PREVALENCE TO DRIVE SEGMENT GROWTH

- 10.4 LONG-TERM & BARIATRIC CARE

- 10.4.1 RISING LONG-TERM DISEASES TO DRIVE DEMAND

- 10.5 MATERNITY & PEDIATRICS

- 10.5.1 SUSTAINED CHILDBIRTH RATES DRIVE DEMAND

- 10.6 OTHER APPLICATIONS

11 MEDICAL FURNITURE MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HOSPITALS

- 11.2.1 PRIVATE HOSPITALS

- 11.2.1.1 Higher capital spending drives private hospital segment

- 11.2.2 PUBLIC HOSPITALS

- 11.2.2.1 Extensive patient coverage sustains demand in public hospitals

- 11.2.1 PRIVATE HOSPITALS

- 11.3 AMBULATORY SURGERY CENTERS

- 11.3.1 SHIFT TOWARD OUTPATIENT SURGERIES DRIVES SEGMENT GROWTH

- 11.4 LONG-TERM & NURSING FACILITIES

- 11.4.1 RISING PREVALENCE OF LONG-TERM DISEASES & AGING POPULATION BURDEN TO DRIVE SEGMENTAL GROWTH

- 11.5 CLINICS

- 11.5.1 EXPANDING OUTPATIENT SERVICES TO DRIVE GROWTH

- 11.6 OTHER END USERS

12 MEDICAL FURNITURE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 US to dominate North American market during forecast period

- 12.2.3 CANADA

- 12.2.3.1 Growth in disabled population to fuel medical furniture market

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Dominant European medical furniture market

- 12.3.3 UK

- 12.3.3.1 Rising government investment in hospital infrastructure to drive market

- 12.3.4 FRANCE

- 12.3.4.1 High healthcare expenditure and government investment foster rapid market growth

- 12.3.5 ITALY

- 12.3.5.1 Rapidly aging population and rising injury rates to drive market

- 12.3.6 SPAIN

- 12.3.6.1 Growing disability prevalence and mobility challenges increases demand for patient handling equipment

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 China to dominate regional market during forecast period

- 12.4.3 JAPAN

- 12.4.3.1 Rapidly aging population and expanding healthcare infrastructure drives market expansion

- 12.4.4 INDIA

- 12.4.4.1 Sustained, broad-based growth driven by growing hospital infrastructure and demand for long-term care

- 12.4.5 AUSTRALIA

- 12.4.5.1 Intensive hospital utilization set to drive demand across care settings

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Increasing investment in hospital equipment to drive market growth

- 12.4.7 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Expanding hospital network, dual public-private coverage, and rising chronic disease burden to drive market

- 12.5.3 MEXICO

- 12.5.3.1 Rising obesity rates and associated hospitalization needs to propel market growth

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 12.6.2 GCC COUNTRIES

- 12.6.2.1 Expanding hospital capacity and smart hospital investments to accelerate medical furniture demand

- 12.6.3 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MEDICAL FURNITURE MARKET

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Product & service footprint

- 13.5.5.4 Application footprint

- 13.5.5.5 End user footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 ARJO

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 GETINGE AB

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches & approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 BAXTER

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches & approvals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 STRYKER CORPORATION

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & approvals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses & competitive threats

- 14.1.5 PARAMOUNT BED HOLDINGS CO., LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches & approvals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 STERIS

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.7 MILLERKNOLL, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches & approvals

- 14.1.8 SAVARIA

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.9 LINET

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches & approvals

- 14.1.9.3.2 Deals

- 14.1.9.3.3 Expansions

- 14.1.10 DRIVE DEVILBISS HEALTHCARE

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Other developments

- 14.1.11 JOERNS HEALTHCARE

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & approvals

- 14.1.12 STIEGELMEYER GMBH & CO. KG

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 MALVESTIO SPA

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.1 ARJO

- 14.2 OTHER PLAYERS

- 14.2.1 NARANG MEDICAL LIMITED

- 14.2.2 GF HEALTH PRODUCTS, INC.

- 14.2.3 PROMOTAL

- 14.2.4 GPC MEDICAL LTD

- 14.2.5 KOVONAX SPOL. S R.O.

- 14.2.6 SKYTRON LLC

- 14.2.7 MIDMARK CORPORATION

- 14.2.8 MEDIFA

- 14.2.9 MERIVAARA CORP.

- 14.2.10 AMICO GROUP OF COMPANIES.

- 14.2.11 UMANO MEDICAL INC

- 14.2.12 OPERA BEDS

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 15.4 MARKET RANKING ANALYSIS

- 15.5 STUDY ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.6.1 METHODOLOGY-RELATED LIMITATIONS

- 15.6.2 SCOPE-RELATED LIMITATIONS

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS