|

시장보고서

상품코드

1996977

동물용 의약품 시장 예측(-2031년) : 제품(의약품, 모노클로널 항체, 면역 조절제, 약용 사료첨가제), 투여 경로, 제형, 적응증, 동물 유형(반려동물, 가축), 유통 채널, 최종사용자별Veterinary Pharmaceuticals Market by Product (Drugs, mAbs, Immunomodulators, Medicated Feed Additives), Route of Administration, Formulation Type, Indication, Animal Type (Companion, Livestock), Distribution Channel, End User-Global Forecast to 2031 |

||||||

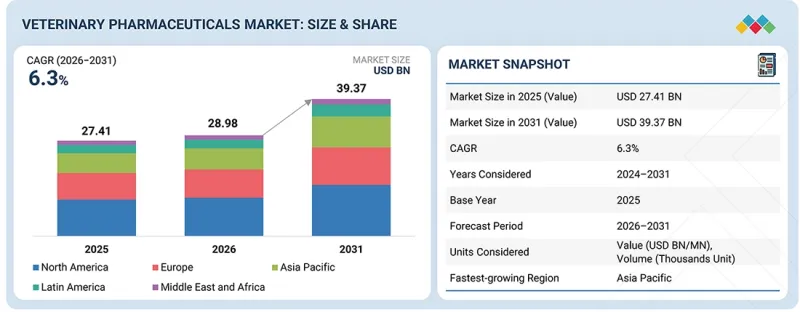

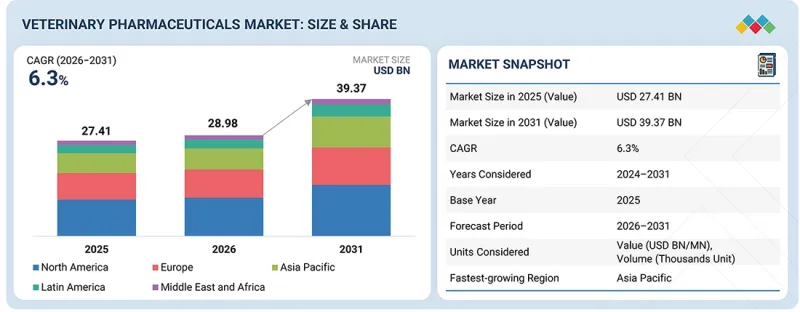

세계의 동물용 의약품 시장 규모는 2026-2031년에 CAGR 6.3%로 성장할 것으로 예측됩니다.

이는 반려동물용과 가축용 두 부문 모두에서 꾸준한 성장세를 보이고 있음을 반영합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) , 수량(유닛) |

| 부문 | 제품 유형별, 투여 경로별, 제형별, 적응증별, 동물 유형별, 유통 채널별, 최종사용자별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

이 시장의 성장은 반려동물의 '인간화', 만성질환 및 감염성 질환의 유병률 증가, 첨단 치료법에 대한 지출 확대에 힘입어 성장세를 보이고 있습니다. 축산 분야에서는 생산성에 대한 압박과 엄격한 식품 안전 기준이 의약품 수요를 지속적으로 견인하고 있으며, 시장은 지속적으로 5%대 초반의 성장률을 유지하고 있습니다.

"제품 유형별로는 모노클로널 항체 부문이 예측 기간 중 가장 높은 성장률을 보일 것으로 예측됩니다. "

특히 반려동물의 경우, 표적화된 지속형 치료법에 대한 선호도가 높아지면서 모노클로널 항체 부문이 가장 빠르게 성장할 것으로 예측됩니다. 아토피피부염, 골관절염, 면역매개질환 등 만성질환의 부담이 증가하고 있는 것도 수요를 증가시키고 있습니다. 이러한 치료법은 작용이 정확하고, 부작용이 적으며, 투여 간격이 길다는 장점이 있으며, 순응도 향상에 기여하고 있습니다. 바이오의약품 개발에 대한 지속적인 투자와 프리미엄 애완동물 케어 시장 확대도 이 부문의 성장을 촉진하고 있습니다.

"적응증별로는 피부질환 부문이 2025년 가장 큰 점유율을 차지할 것으로 예측됩니다. "

이는 주로 반려동물과 가축 모두에서 피부 관련 질병이 광범위하게 발생하고 있기 때문입니다. 아토피 피부염, 기생충 감염, 진균증, 세균성 피부 감염 등 일반적인 질환은 지속적인 관리와 투약이 필요합니다. 반려동물 사육두수 증가, 동물 위생에 대한 관심 증가, 구충제, 항진균제, 항염증약에 대한 강한 수요는 이 부문의 우위를 더욱 강화시키고 있습니다.

"북미가 2025년 시장을 주도한다."

북미는 성숙한 동물의료 생태계와 강력한 구매력을 바탕으로 2025년 시장을 주도할 것으로 예측됩니다. 이 지역에서는 반려동물의 치료비가 비싸고, 대규모 상업용 가축의 기반이 유지되고 있습니다. 활발한 R&D 투자, 혁신적인 의약품에 대한 신속한 승인 절차, 대형 제조업체의 강력한 존재감은 그 입지를 더욱 공고히 하고 있습니다. 또한 잘 정비된 유통망과 예방적 동물 관리에 대한 인식이 높아진 것도 이 지역 시장에서의 선도적 지위에 기여하고 있습니다.

세계의 동물용 의약품 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 동물용 의약품 시장 : 제품 유형별

제10장 동물용 의약품 시장 : 투여 경로별

제11장 동물용 의약품 시장 : 제제 유형별

제12장 동물용 의약품 시장 : 적응증별

제13장 동물용 의약품 시장 : 동물 유형별

제14장 동물용 의약품 시장 : 유통 채널별

제15장 동물용 의약품 시장 : 최종사용자별

제16장 동물용 의약품 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSA 26.04.21The global veterinary pharmaceuticals market is projected to grow at a CAGR of 6.3% from 2026 to 2031, reflecting steady expansion across both companion and livestock segments.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD million/billion), Volume (thousand units) |

| Segments | By Product Type, Route Of Administration, Formulation Type, Indications, Animal Types, Distribution Channels, End User |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

Growth is supported by rising pet humanization, increasing prevalence of chronic and infectious diseases, and higher spending on advanced therapeutics. In livestock, productivity pressures and stricter food safety standards continue to drive pharmaceutical demand, sustaining consistent mid-single-digit market growth.

"By product type, the monoclonal antibodies segment is expected to witness the fastest growth rate during the forecast period."

The monoclonal antibodies segment is expected to grow fastest in the global veterinary pharmaceuticals market, supported by a growing preference for targeted and durable treatment options, especially in companion animals. The rising burden of chronic disorders, including atopic dermatitis, osteoarthritis, and immune-mediated conditions, is boosting demand. These therapies offer precise action, fewer adverse effects, and longer dosing intervals, improving compliance. Continued investment in biologics development and the expanding premium pet care market are further driving segment expansion.

"By indication, the dermatological diseases segment has accounted for the largest share in the Veterinary pharmaceuticals market in 2025."

The dermatological conditions segment is projected to hold the largest share of the global veterinary pharmaceuticals market in 2025, primarily due to the widespread occurrence of skin-related disorders in both companion and livestock animals. Common conditions such as atopic dermatitis, parasitic infections, fungal diseases, and bacterial skin infections require ongoing management and medication. Growing pet adoption, heightened focus on animal hygiene, and strong demand for anti-parasitic, antifungal, and anti-inflammatory treatments continue to reinforce the segment's dominant position.

"North America dominated the global veterinary pharmaceuticals market in 2025."

North America leads the veterinary pharmaceuticals market in 2025, supported by a mature animal healthcare ecosystem and strong purchasing power. The region records high spending on companion animal treatments and maintains a large commercial livestock base. Robust R&D investments, rapid approval pathways for innovative drugs, and the strong presence of established manufacturers further strengthen its position. Well-developed distribution networks and growing awareness of preventive animal care also contribute to its leading market position.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 - 45%, Tier 2 - 20%, and Tier 3 - 35%

- By Designation: C-level - 35%, Director-level - 25%, and Others - 40%

- By Region: North America - 40%, Europe - 25%, APAC - 20%, Latin America - 10%, Middle East & Africa - 5%

Research Coverage

This report examines the veterinary pharmaceuticals market by product type, route of administration, formulation type, indications, animal type, distribution channel, end user, and region. It also examines factors (such as drivers, restraints, opportunities, and challenges) that affect market growth. It analyzes market opportunities and challenges and provides details on the competitive landscape for market leaders. Furthermore, the report analyzes micro-markets by their individual growth trends and forecasts market segment revenue across five main regions and their respective countries.

Reasons to Buy the Report

The report can help established firms as well as new entrants/smaller firms gauge the market pulse, which, in turn, would help them gain a greater share. Firms purchasing the report could use one or a combination of the following five strategies.

This report provides insights into the following pointers:

- Analysis of key drivers, restraints, opportunities, and challenges influencing the growth of the veterinary pharmaceuticals market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the veterinary pharmaceuticals market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of catheterization procedures across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary pharmaceuticals market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary pharmaceuticals market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN VETERINARY PHARMACEUTICALS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN VETERINARY PHARMACEUTICALS MARKET

- 3.2 ASIA PACIFIC: VETERINARY PHARMACEUTICALS MARKET, BY PRODUCT TYPE AND COUNTRY

- 3.3 VETERINARY PHARMACEUTICALS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 VETERINARY PHARMACEUTICALS MARKET: DEVELOPING VS. DEVELOPED ECONOMIES, 2026-2031

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising companion animal ownership and pet humanization

- 4.2.1.2 Growing prevalence of infectious and dermatological diseases in animals

- 4.2.1.3 Increasing demand for animal-derived food products

- 4.2.2 RESTRAINTS

- 4.2.2.1 Growing concerns over antimicrobial resistance (AMR)

- 4.2.2.2 Stringent regulatory approval processes for veterinary drugs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising demand for parasiticides and dermatology products

- 4.2.3.2 Growth potential in rural and low-income regions

- 4.2.4 CHALLENGES

- 4.2.4.1 Monitoring drug residues in food-producing animals

- 4.2.4.2 Balancing animal welfare, productivity, and compliance requirements

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKET AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ANIMAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL VETERINARY PHARMACEUTICALS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY KEY PLAYERS, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF FORMULATION TYPES, BY KEY PLAYERS, 2023-2025

- 5.6.3 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 30, 2021-2024

- 5.7.1.1 Import scenario (HS code 30)

- 5.7.2 EXPORT DATA FOR HS CODE 30, 2021-2024

- 5.7.3 EXPORT SCENARIO (HS CODE 30)

- 5.7.1 IMPORT DATA FOR HS CODE 30, 2021-2024

- 5.8 KEY CONFERENCES AND EVENTS IN 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ZOETIS INC.

- 5.11.2 BOEHRINGER INGELHEIM ANIMAL HEALTH

- 5.11.3 MERCK ANIMAL HEALTH

- 5.11.4 ELANCO ANIMAL HEALTH

- 5.11.5 CEVA SANTE ANIMALE

- 5.12 IMPACT OF 2025 US TARIFF - VETERINARY PHARMACEUTICALS MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Veterinary hospitals & clinics

- 5.12.5.2 Home care settings

- 5.12.5.3 Livestock farms

- 5.12.5.4 Rescue centers & NGOs

- 5.12.5.5 Other end users

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Controlled release formulation

- 6.1.1.2 Biologics and monoclonal antibodies

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Digital health and telemedicine platforms

- 6.1.2.2 Veterinary biomarker analysis

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Wearable animal health monitoring devices

- 6.1.3.2 Stem cell therapy and regenerative medicine

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 PUBLICATION TRENDS FOR VETERINARY PHARMACEUTICALS

- 6.3.2 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS AND JURISDICTION FOR VETERINARY PHARMACEUTICALS MARKET, JANUARY 2015-DECEMBER 2025

- 6.3.3 LIST OF MAJOR PATENTS, 2023-2025

- 6.4 FUTURE APPLICATIONS

- 6.4.1 PRECISION LIVESTOCK HEALTH MANAGEMENT

- 6.4.2 ONCOLOGY AND CHRONIC DISEASE MANAGEMENT

- 6.4.3 REPRODUCTIVE AND FERTILITY ENHANCEMENT IN LIVESTOCK

- 6.4.4 INTEGRATED DISEASE SURVEILLANCE AND OUTBREAK CONTROL

- 6.5 IMPACT OF GEN AI ON VETERINARY PHARMACEUTICALS MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.3.1 VICH Guidelines (International Co-operation on Harmonisation of Technical Requirements for Registration of Veterinary Medicinal Products)

- 7.1.3.2 Good Manufacturing Practice (GMP) Standards - PIC/S Guide (PE 009 series)

- 7.1.3.3 Codex Alimentarius Standards for Veterinary Drug Residues (CXM 2 - Maximum Residue Limits)

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ECO-FRIENDLY AND RECYCLABLE MATERIALS IN VETERINARY PHARMACEUTICALS MARKET

- 7.2.1.1 Virbac - Eco-pack to reduce single-use plastic in veterinary products

- 7.2.1.2 Boehringer Ingelheim Animal Health - Renewable energy-powered manufacturing

- 7.2.1.3 Boehringer Ingelheim - Recyclable veterinary delivery device (Aservo, EquiHaler)

- 7.2.1 ECO-FRIENDLY AND RECYCLABLE MATERIALS IN VETERINARY PHARMACEUTICALS MARKET

- 7.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE SETTINGS

- 8.5 MARKET PROFITABILITY

- 8.5.1 PRODUCT INNOVATION AND DIFFERENTIATION

- 8.5.2 EXPANSION OF COMPANION ANIMAL HEALTHCARE SPENDING

- 8.5.3 OPERATIONAL SCALE AND DISTRIBUTION EFFICIENCY

9 VETERINARY PHARMACEUTICALS MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.1.1 VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 9.2 DRUGS

- 9.2.1 ANTI-BACTERIAL DRUGS

- 9.2.1.1 Routine use in livestock and companion animals underpins strong market share and steady growth

- 9.2.2 ANTI-FUNGAL DRUGS

- 9.2.2.1 Limited approvals and off-label systemic use result in smaller but clinically essential segment

- 9.2.3 ANTI-VIRAL DRUGS

- 9.2.3.1 Low current penetration but rising research interest driven by outbreak response and targeted therapies

- 9.2.4 ANTI-INFLAMMATORY DRUGS

- 9.2.4.1 Rising surgical volumes and chronic pain management drive stable double-digit market share

- 9.2.5 ANTI-PARASITIC DRUGS

- 9.2.5.1 High parasitic burden and preventive care practices sustain market share and strong growth trajectory

- 9.2.6 ANTI-CANCER DRUGS

- 9.2.6.1 Increasing pet oncology awareness and advanced therapeutics to fuel growth from small base

- 9.2.7 CARDIOVASCULAR AND RENAL DRUGS

- 9.2.7.1 Rising diagnosis of chronic heart and kidney disorders supports steady mid-single-digit market share

- 9.2.8 GASTROINTESTINAL DRUGS

- 9.2.8.1 High incidence of digestive disorders and dietary transitions drive sustained demand

- 9.2.9 OTHER DRUGS

- 9.2.1 ANTI-BACTERIAL DRUGS

- 9.3 MONOCLONAL ANTIBODIES

- 9.3.1 TARGETED BIOLOGICS AND RISING COMPANION ANIMAL THERAPEUTICS TO DRIVE DEMAND

- 9.4 IMMUNOMODULATORS

- 9.4.1 INCREASING FOCUS ON IMMUNE-MEDIATED DISEASES AND PREVENTIVE HEALTH TO SUPPORT GRADUAL EXPANSION FROM SMALLER BASE

- 9.5 MEDICATED FEED ADDITIVES

- 9.5.1 AMINO ACIDS

- 9.5.1.1 Protein optimization and feed cost efficiency to drive demand

- 9.5.2 ENZYMES

- 9.5.2.1 Improved nutrient digestibility and cost optimization to support steady adoption

- 9.5.3 VITAMINS AND MINERALS

- 9.5.3.1 Essential micronutrient supplementation ensures largest market share

- 9.5.4 OTHER MEDICATED FEED ADDITIVES

- 9.5.1 AMINO ACIDS

10 VETERINARY PHARMACEUTICALS MARKET, BY ROUTE OF ADMINISTRATION

- 10.1 INTRODUCTION

- 10.2 ORAL

- 10.2.1 EASE OF DOSING AND HIGH COMPLIANCE IN COMPANION AND LIVESTOCK ANIMALS

- 10.3 PARENTERAL

- 10.3.1 RAPID THERAPEUTIC ACTION AND HIGHER BIOAVAILABILITY IN CRITICAL CARE AND PRODUCTION SETTINGS

- 10.4 TOPICAL

- 10.4.1 RISING DERMATOLOGY CASES AND DEMAND FOR LOCALIZED, NON-INVASIVE TREATMENTS

- 10.5 OTHER ROUTES OF ADMINISTRATION

11 VETERINARY PHARMACEUTICALS MARKET, BY FORMULATION TYPE

- 11.1 INTRODUCTION

- 11.2 SOLID

- 11.2.1 DOSING STABILITY, COST EFFICIENCY, AND EASE OF LARGE-SCALE ADMINISTRATION IN LIVESTOCK AND COMPANION ANIMALS

- 11.3 LIQUID

- 11.3.1 RAPID ABSORPTION, FLEXIBLE DOSING, AND SUITABILITY FOR INJECTABLES AND ORAL SUSPENSIONS

- 11.4 SEMI-SOLID

- 11.4.1 RISING DERMATOLOGY CASES AND INCREASING COMPANION ANIMAL CARE EXPENDITURE

- 11.5 AEROSOL/SPRAY

- 11.5.1 CONVENIENCE, TARGETED DELIVERY, AND REDUCED CROSS-CONTAMINATION RISK

- 11.6 PREMIX FORMULATIONS

- 11.6.1 DEMAND FOR MEDICATED FEED AND PREVENTIVE HERD-LEVEL DISEASE MANAGEMENT TO DRIVE MARKET

12 VETERINARY PHARMACEUTICALS MARKET, BY INDICATION

- 12.1 INTRODUCTION

- 12.2 INFECTIOUS DISEASES

- 12.2.1 ZOONOTIC RISK AND LIVESTOCK DISEASE CONTROL PROGRAMS TO DRIVE MARKET

- 12.3 DERMATOLOGICAL DISEASES

- 12.3.1 RISING CHRONIC SKIN CONDITIONS AND PREMIUM COMPANION ANIMAL SPENDING TO DRIVE MARKET

- 12.4 PAIN MANAGEMENT

- 12.4.1 RISING SURGICAL PROCEDURES AND AGING PET POPULATION TO DRIVE MARKET

- 12.5 CARDIOVASCULAR AND RENAL DISEASES

- 12.5.1 INCREASED DIAGNOSIS IN AGING COMPANION ANIMALS TO DRIVE MARKET

- 12.6 GASTROINTESTINAL DISEASES

- 12.6.1 HIGH PREVALENCE OF ENTERIC INFECTIONS AND DIETARY DISORDERS TO DRIVE MARKET

- 12.7 OTHER INDICATIONS

13 VETERINARY PHARMACEUTICALS MARKET, BY ANIMAL TYPE

- 13.1 INTRODUCTION

- 13.2 COMPANION ANIMALS

- 13.2.1 DOGS

- 13.2.1.1 Increasing population and adoption of dogs to drive market

- 13.2.2 CATS

- 13.2.2.1 Emerging trends in feline pharmaceuticals to boost market

- 13.2.3 HORSES

- 13.2.3.1 Higher risk of traumatic injuries in horses to drive demand for veterinary pharmaceutical products

- 13.2.4 OTHER COMPANION ANIMALS

- 13.2.1 DOGS

- 13.3 LIVESTOCK ANIMALS

- 13.3.1 CATTLE

- 13.3.1.1 Economic importance of dairy and beef cattle to drive growth

- 13.3.2 SWINE

- 13.3.2.1 Growing surgical volume for acute conditions in swine to drive market

- 13.3.3 POULTRY

- 13.3.3.1 Growing focus on infection prevention and flock health management to drive market

- 13.3.4 OTHER LIVESTOCK ANIMALS

- 13.3.1 CATTLE

14 VETERINARY PHARMACEUTICALS MARKET, BY DISTRIBUTION CHANNEL

- 14.1 INTRODUCTION

- 14.2 VETERINARY HOSPITAL PHARMACIES

- 14.2.1 HIGH IMPORTANCE AND BETTER OPPORTUNITIES IN ON-FARM VETERINARY PHARMACEUTICALS TO DRIVE MARKET

- 14.3 RETAIL PHARMACIES

- 14.3.1 RETAIL PHARMACIES TO AID ACCESSIBILITY AND MARKET REACH IN VETERINARY PHARMACEUTICALS

- 14.4 ONLINE PHARMACIES

- 14.4.1 CONVENIENCE AND ACCESSIBILITY TO AUGMENT MARKET GROWTH

- 14.5 DIRECT SALES

- 14.5.1 DIRECT SALES TO STRENGTHEN MANUFACTURER-TO-CUSTOMER CONNECTIONS

15 VETERINARY PHARMACEUTICALS MARKET, BY END USER

- 15.1 INTRODUCTION

- 15.2 VETERINARY HOSPITALS & CLINICS

- 15.2.1 FIRST POINT OF CONTACT FOR ANIMAL OWNERS AND LIVESTOCK CAREGIVERS

- 15.3 LIVESTOCK FARMS

- 15.3.1 GROWING IMPORTANCE AND OPPORTUNITIES IN ON-FARM ANIMAL CARE

- 15.4 HOME CARE SETTINGS

- 15.4.1 RISING PET EXPENDITURE TO PROPEL SEGMENT GROWTH

- 15.5 OTHER END USERS

16 VETERINARY PHARMACEUTICALS MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 16.2.2 NORTH AMERICA: VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 16.2.3 US

- 16.2.3.1 Surge in animal healthcare expenditure to boost market

- 16.2.4 CANADA

- 16.2.4.1 Growing pet population and advanced veterinary services to drive market

- 16.3 EUROPE

- 16.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 16.3.2 EUROPE: VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 16.3.3 GERMANY

- 16.3.3.1 Increased focus on animal welfare to drive demand for veterinary pharmaceutical products

- 16.3.4 UK

- 16.3.4.1 Increasing pet ownership to propel market

- 16.3.5 FRANCE

- 16.3.5.1 High standards of veterinary care to provide attractive growth opportunities for market players

- 16.3.6 ITALY

- 16.3.6.1 Growing pet owner awareness and increasing livestock population to drive market

- 16.3.7 SPAIN

- 16.3.7.1 Increasing awareness of animal health to drive market

- 16.3.8 REST OF EUROPE

- 16.4 ASIA PACIFIC

- 16.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 16.4.2 ASIA PACIFIC: VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 16.4.3 JAPAN

- 16.4.3.1 Surge in pet care expenditure and growing adoption of companion animals to drive market

- 16.4.4 CHINA

- 16.4.4.1 Increasing animal healthcare expenditure and advancements in veterinary medicines to drive market

- 16.4.5 INDIA

- 16.4.5.1 Increasing livestock population to propel market growth

- 16.4.6 AUSTRALIA

- 16.4.6.1 Growing companion animal ownership and rise in animal health awareness to support market growth

- 16.4.7 SOUTH KOREA

- 16.4.7.1 Growing pet ownership and advancements in veterinary medicine to favor market growth

- 16.4.8 PHILIPPINES

- 16.4.8.1 Tourism-linked pet culture and veterinary advancements to fuel market

- 16.4.9 REST OF ASIA PACIFIC

- 16.5 LATIN AMERICA

- 16.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 16.5.2 LATIN AMERICA: VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 16.5.3 BRAZIL

- 16.5.3.1 Growing pet population and rising disposable incomes to drive market

- 16.5.4 MEXICO

- 16.5.4.1 Robust livestock base and growing companion animal care to drive market

- 16.5.5 REST OF LATIN AMERICA

- 16.6 MIDDLE EAST & AFRICA

- 16.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 16.6.2 MIDDLE EAST & AFRICA: VETERINARY PHARMACEUTICALS MARKET VOLUME ANALYSIS BY PRODUCT TYPE, 2024-2031 (THOUSAND UNITS)

- 16.7 GCC COUNTRIES

- 16.7.1 KINGDOM OF SAUDI ARABIA (KSA)

- 16.7.1.1 Vision 2030 investments to drive market

- 16.7.2 UNITED ARAB EMIRATES (UAE)

- 16.7.2.1 Increasing adoption of advanced diagnostic technologies to contribute to market growth

- 16.7.3 REST OF GCC COUNTRIES

- 16.7.4 REST OF MIDDLE EAST & AFRICA

- 16.7.1 KINGDOM OF SAUDI ARABIA (KSA)

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.1.1 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2023-2026

- 17.2 REVENUE ANALYSIS, 2023-2025

- 17.3 MARKET SHARE ANALYSIS, 2025

- 17.3.1 US: VETERINARY PHARMACEUTICALS MARKET SHARE ANALYSIS, 2025

- 17.3.2 EUROPE: VETERINARY PHARMACEUTICALS MARKET SHARE ANALYSIS, 2025

- 17.4 PRODUCT/BRAND COMPARISON

- 17.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.5.1 STARS

- 17.5.2 EMERGING LEADERS

- 17.5.3 PERVASIVE PLAYERS

- 17.5.4 PARTICIPANTS

- 17.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 17.5.5.1 Company footprint

- 17.5.5.2 Region footprint

- 17.5.5.3 Product type footprint

- 17.5.5.4 Route of administration footprint

- 17.5.5.5 Indication footprint

- 17.5.5.6 End user footprint

- 17.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.6.1 PROGRESSIVE COMPANIES

- 17.6.2 RESPONSIVE COMPANIES

- 17.6.3 DYNAMIC COMPANIES

- 17.6.4 STARTING BLOCKS

- 17.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 17.6.5.1 Detailed list of key startups/SMEs

- 17.6.5.2 Competitive benchmarking of key startups/SMEs

- 17.7 COMPANY VALUATION AND FINANCIAL METRICS

- 17.8 COMPETITIVE SCENARIO

- 17.8.1 PRODUCT LAUNCHES & APPROVALS

- 17.8.2 DEALS

- 17.8.3 EXPANSIONS

- 17.8.4 OTHER DEVELOPMENTS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 ZOETIS INC.

- 18.1.1.1 Business overview

- 18.1.1.2 Products offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches & approvals

- 18.1.1.3.2 Expansions

- 18.1.1.3.3 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Right to win

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 MERCK & CO., INC

- 18.1.2.1 Business overview

- 18.1.2.2 Products offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches & approvals

- 18.1.2.3.2 Deals

- 18.1.2.3.3 Expansions

- 18.1.2.4 MnM view

- 18.1.2.4.1 Right to win

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 BOEHRINGER INGELHEIM INTERNATIONAL GMBH

- 18.1.3.1 Business overview

- 18.1.3.2 Products offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product launches & approvals

- 18.1.3.3.2 Deals

- 18.1.3.3.3 Expansions

- 18.1.3.4 MnM view

- 18.1.3.4.1 Right to win

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 ELANCO ANIMAL HEALTH INCORPORATED

- 18.1.4.1 Business overview

- 18.1.4.2 Products offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches & approvals

- 18.1.4.3.2 Expansions

- 18.1.4.3.3 Other developments

- 18.1.4.4 MnM view

- 18.1.4.4.1 Right to win

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 VIRBAC

- 18.1.5.1 Business overview

- 18.1.5.2 Products offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches & approvals

- 18.1.5.3.2 Deal

- 18.1.5.3.3 Expansions

- 18.1.5.4 MnM view

- 18.1.5.4.1 Right to win

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 CEVA

- 18.1.6.1 Business overview

- 18.1.6.2 Products offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Deals

- 18.1.6.3.2 Expansions

- 18.1.7 VETOQUINOL

- 18.1.7.1 Business overview

- 18.1.7.2 Products offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches & approvals

- 18.1.7.3.2 Deals

- 18.1.8 DECHRA PHARMACEUTICALS PLC

- 18.1.8.1 Business overview

- 18.1.8.2 Products offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches & approvals

- 18.1.8.3.2 Deals

- 18.1.8.3.3 Other developments

- 18.1.9 NORBROOK

- 18.1.9.1 Business overview

- 18.1.9.2 Products offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches & approvals

- 18.1.9.3.2 Deals

- 18.1.9.3.3 Expansions

- 18.1.9.3.4 Other developments

- 18.1.10 BIMEDA CORPORATE

- 18.1.10.1 Business overview

- 18.1.10.2 Products offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches & approvals

- 18.1.10.3.2 Deals

- 18.1.10.3.3 Expansions

- 18.1.11 HESTER BIOSCIENCES LIMITED

- 18.1.11.1 Business overview

- 18.1.11.2 Products offered

- 18.1.12 INDIAN IMMUNOLOGICALS LTD.

- 18.1.12.1 Business overview

- 18.1.12.2 Products offered

- 18.1.13 ANIMALCARE GROUP PLC

- 18.1.13.1 Business overview

- 18.1.13.2 Products offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.13.3.2 Product launches & approvals

- 18.1.14 KYORITSU SEIYAKU CORPORATION

- 18.1.14.1 Business overview

- 18.1.14.2 Products offered

- 18.1.14.3 Recent developments

- 18.1.14.3.1 Product launches & approvals

- 18.1.14.3.2 Deals

- 18.1.15 CALIER

- 18.1.15.1 Business overview

- 18.1.15.2 Products offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 Product launches & approvals

- 18.1.1 ZOETIS INC.

- 18.2 OTHER PLAYERS

- 18.2.1 DOPHARMA

- 18.2.2 PHARMGATE ANIMAL HEALTH

- 18.2.3 BIOVETA, A.S.

- 18.2.4 NEXTMUNE

- 18.2.5 TRIVIUMVET

- 18.2.6 DOMES PHARMA

- 18.2.7 UNIVET LIMITED

- 18.2.8 CENAVISA, S.L.

- 18.2.9 FATRO S.P.A.

- 18.2.10 CHANELLE PHARMA

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Key data from primary sources

- 19.1.2.2 Key industry insights

- 19.1.2.3 Key industry insights

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.3 GROWTH FORECAST

- 19.3.1 KEY INDUSTRY INSIGHTS

- 19.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ASSESSMENT

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.3.1 PRODUCT ANALYSIS

- 20.3.2 US END USER ANALYSIS

- 20.3.3 GEOGRAPHIC ANALYSIS

- 20.3.4 COMPANY INFORMATION

- 20.3.5 REGIONAL/COUNTRY LEVEL MARKET SHARE ANALYSIS

- 20.3.6 COUNTRY LEVEL VOLUME ANALYSIS BY PRODUCT TYPE

- 20.3.7 BY PRODUCT TYPE MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 20.3.8 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS