|

시장보고서

상품코드

2000340

바이오소재 시장 예측(-2030년) : 유형(금속(금, 마그네슘), 세라믹(산화알루미늄, 탄소), 폴리머(폴리에틸렌, 폴리에스테르), 천연 소재(히알루론산, 콜라겐, 젤라틴)), 용도별(정형외과, 치과, 순환기 및 혈관 외과, 안과)Biomaterials Market by Type [Metallic (Gold, Magnesium), Ceramic (Aluminum Oxide, Carbon), Polymer (Polyethylene, Polyester), Natural (Hyaluronic acid, Collagen, Gelatin)], Application (Orthopedic, Dental, CVD, Ophthalmology) - Global Forecast to 2030 |

||||||

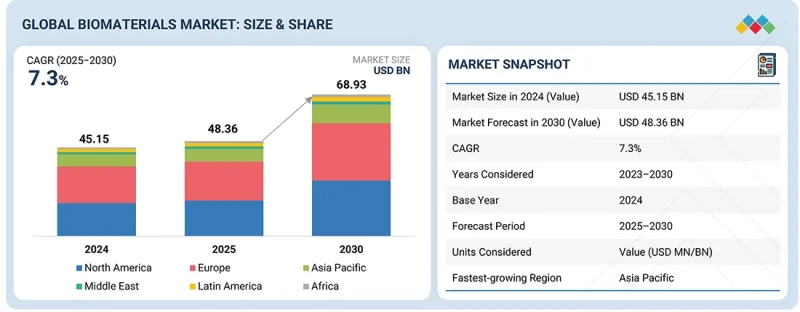

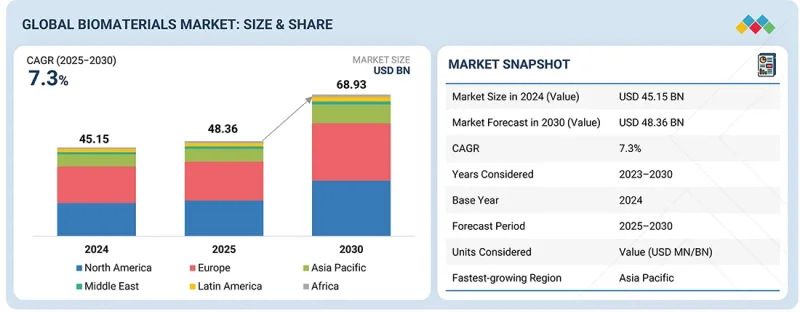

세계의 바이오소재 시장 규모는 2025년 483억 6,000만 달러에서 2030년까지 689억 3,000만 달러에 달할 것으로 예측되고 있으며, 2025-2030년 CAGR은 7.3%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 유형별, 용도별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

세계 바이오소재 시장의 확대는 의료시설 및 시스템의 발전, 스마트하고 생체 적합성 있는 3D 프린팅 바이오소재의 기술 발전으로 인해 주도되고 있습니다.

2024년 유형별로는 금속 바이오소재가 시장에서 가장 큰 점유율을 차지했습니다.

시장에서는 금속 바이오소재, 고분자 바이오소재, 세라믹 바이오소재, 천연 바이오소재로 분류됩니다. 정형외과, 치과, 심혈관 분야에서의 폭넓은 적용으로 유형별로는 금속 바이오소재가 가장 큰 점유율을 차지했습니다. 기계적 특성으로 인해 관절 치환술, 골절 고정 장치, 치과용 임플란트, 스텐트 등의 임플란트에 적용하기에 적합합니다. 일반적으로 사용되는 바이오소재에는 티타늄 및 그 합금, 스테인리스강, 코발트 크롬 몰리브덴 합금, 최근에는 마그네슘 금속과 같은 생분해성 금속 합금 등이 있습니다. 이들은 피로 파괴 및 부식에 대한 우수한 내성과 뛰어난 생체적합성을 나타냅니다. 또한 생리적 환경에서 장기간 사용해도 안전한 것으로 확인되었습니다. 한편, 코팅 및 표면 처리를 통한 표면 개질 기술의 끊임없는 발전으로 골유착, 마찰 특성, 감염 저항성이 크게 향상되었습니다. 또한 수술 건수 증가, 고령화, 근골격계 및 심장 질환 증가로 인해 전 세계에서 금속 바이오소재에 대한 수요가 증가하여 세계 바이오소재 시장에서의 확고한 입지를 더욱 공고히할 것으로 예측됩니다.

용도별로는 관절 치환술 부문이 2024년 정형외과 용도 부문 중 가장 큰 점유율을 차지할 것으로 보고되고 있습니다.

용도별로 시장은 순환기, 정형외과, 안과, 치과, 성형외과, 조직공학, 신경학, 상처 치유, 비뇨기과, 기타로 분류됩니다. 2024년 시장에서는 관절 치환술이 정형외과 응용 분야 중 주요 부문으로 부상할 것으로 예측됩니다. 이는 골관절염, 류마티스 관절염 등 퇴행성 관절 질환을 앓고 있는 사람들이 증가하고 있기 때문입니다. 또한 고령화, 비만율 증가 등의 요인도 무릎, 어깨, 고관절 치환술을 받는 사람들 증가로 이어지고 있습니다. 관절 치환술에 사용되는 재료는 강도, 내구성, 생체 적합성이 향상되어 고부하가 걸리는 용도에 매우 적합합니다. 임플란트 디자인, 표면 기술, 이식 방법의 발전은 임플란트 환자의 생존율을 지속적으로 향상시키고 있습니다. 또한 저침습적 수술의 확대, 개발도상국에서의 정형외과 의료의 보급, 끊임없이 발전하는 임플란트 기술도 이 시장을 주도하고 있습니다.

2025-2030년 아시아태평양이 가장 높은 시장 점유율 성장률을 보였습니다.

아시아태평양은 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예측됩니다. 이러한 급격한 성장은 중국, 인도, 일본의 의료 인프라의 급속한 확대와 더불어 의료관광의 급증, 정형외과, 심장질환 등 만성질환의 부담 증가에 따른 의료관광의 급격한 증가에 의해 주도되고 있습니다. 고령화, 정부의 R&D 투자, 3D 프린팅 임플란트 및 생체흡수성 폴리머의 채택은 관절 치환술, 스텐트 및 조직 공학 분야에서 첨단 금속, 폴리머 및 세라믹 솔루션에 대한 수요를 촉진하고 있습니다. 현지 제조 거점 및 규제 간소화가 시장 침투를 더욱 가속화하여 아시아태평양을 주요 혁신 거점으로 자리매김하고 있습니다.

세계의 바이오소재(Biomaterials) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 바이오소재 시장 : 유형별

제10장 바이오소재 시장 : 용도별

제11장 바이오소재 시장 : 최종사용자별

제12장 바이오소재 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.04.23The global Biomaterials market is projected to reach USD 68.93 billion by 2030 from USD 48.36 billion in 2025, at CAGR of 7.3% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | By Type, By Application |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East and Africa |

The expansion of the Global Biomaterials market has been fueled by the advancements in healthcare facilities and systems, and the rising advancements in smart, biocompatible, and 3D-printed biomaterials.

In 2024, The metallic biomaterials held the highest share in the Global Biomaterials market by type.

The market is segmented into Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, Natural Biomaterials. The highest share by type was of metallic biomaterials due to their wide application in orthopedic, dental, and cardiovascular fields. The mechanical properties make them the suitable for application in implants such as joint replacements, fracture fixation devices, dental implants, and stints. The commonly used biomaterials are titanium and its alloys, stainless steel, cobalt chromoly alloys, and more recently, biodegradable metal alloys like magnesium-based metal. These exhibit remarkable resistance to fatigue failure, corrosion, and remarkable compatibility. They were also found to be safe for long-term use in a physiological environment. However, constant progress in surface modification technologies such as surface modification through coating and surface treatment has greatly improved their osseointegration, friction, and resistance to infections. Moreover, rising surgical procedures, an ageing population, and an increase in musculoskeletal and cardiac disorders are expected to propel the demand for metallic biomaterials across the globe, consolidating their strong position in the global biomaterials.

"Joint replacement segment reported for the highest share of the orthopedic application segment in 2024."

Within the application segment, the Global Biomaterials market is divided into Cardiovascular, Orthopedic, Ophthalmology, Dental, Plastic Surgery, Tissue engineering, neurological application Wound Healing, Urinary application, and Other Applications. In 2024, Joint replacement represents the leading segment in orthopedic applications in the global biomaterials. Due to an increasing number of people suffering from degenerative joint diseases like osteoarthritis and rheumatoid arthritis. factors like an aging population, and an increasing rate of obesity have also led to an increasing number of people undergoing knee, shoulder, or hip replacements. However, materials used in joint replacements, have improved strength, durability, or biocompatibility that makes these materials highly suitable for applications involving heavy loading. Advances in implant design, surface technology, or method of implantation also continue to increase patient survival with these implants. Furthermore, increasing utilization of minimal invasiveness in surgeries, increasing availability of orthopedic care in developing nations, or ever-improving implant technologies continue to drive this market.

APAC accounted for the fastest growing market share in the global Biomaterials market from 2025 to 2030.

The biomaterials market is segmented into North America, Europe, Asia Pacific, Latin America, Middle East and Africa. APAC region is projected to grow at the highest CAGR during the forecast period . This surge is driven by rapid healthcare infrastructure expansion in China, India, and Japan, alongside booming medical tourism and rising chronic disease burdens like orthopedics and cardiology. An aging population, government R&D investments, and adoption of 3D-printed implants and bioresorbable polymers fuel demand for advanced metallic, polymeric, and ceramic solutions in joint replacements, stents, and tissue engineering. Local manufacturing hubs and regulatory streamlining further accelerate market penetration, positioning APAC as a key innovation powerhouse.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side-70% and Demand Side-30%

- By Designation: Managers-45%, CXO and Directors-30%, and Executives-25%

- By Region: North America-40%, Europe-25%, the Asia Pacific-25%, Latin America-5%, and the Middle East & Africa-5%

List of Key Companies Profiled in the Report:

Key players in the Global Biomaterials market include BASF SE (Germany), Covestro AG (Germany), Celanese Corporation (US), Carpenter Technology Corporation (US), DSM (Netherlands), Corbion NV (Netherlands), Evonik Industries AG (Germany), Victrex Plc (UK), CeramTec GmbH (Germany), Mitsubishi Chemical Group Corporation (Japan), CoorsTek Inc. (US), Berkeley Advanced Biomaterials (US), CAM Bioceramics B.V. (Netherlands), Zeus Company Inc. (US), AMETEK Inc. (US), and GELITA AG (Germany).

Research Coverage:

This research report categorizes the Global Biomaterials market, By Type: Metallic Biomaterials, Polymeric Biomaterials, Ceramic Biomaterials, Natural Biomaterials, By Application: Cardiovascular Orthopaedic, Dental, Plastic Surgery, Urinary, Wound Healing, Tissue Engineering, Ophthalmology, Neurological/Central Nervous System, Other Applications. and by region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the Biomaterials market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, solutions, key strategies, collaborations, partnerships, and agreements. New approvals/launches, collaborations, acquisitions, and recent developments associated with the Global Biomaterials market.

Key Benefits of Buying the Report:

The report will help market leaders and new entrants by providing them with the closest approximations of the revenue numbers for the overall Biomaterials market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their businesses and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising advancements in smart, biocompatible, and 3D-printed biomaterials, Advancements in healthcare facilities and systems), restraints (High development and production costs associated with advanced biomaterials.), opportunities (Expanding applications in tissue engineering and regenerative medicine.) and Challenges (Concerns related to biocompatibility, safety, and adverse immune responses).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the Global Biomaterials market

- Market Development: Comprehensive information about lucrative markets - the report analyses the market across varied regions.

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the Global Biomaterials market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players. A detailed analysis of the key industry players has been done to provide insights into their key strategies, product launches/ approvals, pipeline analysis, acquisitions, partnerships, agreements, collaborations, other recent developments, investment and funding activities, brand/product comparative analysis, and vendor valuation and financial metrics of the Global Biomaterials market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS & STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING BIOMATERIALS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 BIOMATERIALS MARKET OVERVIEW

- 3.2 NORTH AMERICA: BIOMATERIALS MARKET, BY TYPE AND COUNTRY, 2025

- 3.3 BIOMATERIALS MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising advancements in smart, biocompatible, and 3D printed biomaterials

- 4.2.1.2 Advancements in healthcare systems, physical infrastructure, and reimbursement frameworks

- 4.2.1.3 Growing demand for biomaterials in wound healing and plastic surgery

- 4.2.1.4 Increasing use of biomaterials in multiple therapeutic areas

- 4.2.2 RESTRAINTS

- 4.2.2.1 High development and production cost of advanced biomaterials

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding applications in tissue engineering and regenerative medicine

- 4.2.3.2 Development of novel biomaterials

- 4.2.4 CHALLENGES

- 4.2.4.1 Concerns related to biocompatibility, safety, and adverse immune responses

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL BIOMATERIALS MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 ROLE IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE SELLING PRICE OF BIOMATERIALS, BY KEY PLAYER, 2025

- 5.5.2 INDICATIVE SELLING PRICE OF BIOMATERIALS, BY REGION, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA FOR HS CODE 7221 (STAINLESS STEEL), 2021-2025

- 5.6.2 EXPORT DATA FOR HS CODE 7221 (STAINLESS STEEL), 2021-2025

- 5.6.3 IMPORT VOLUME FOR HS 7221 (STAINLESS STEEL), 2021-2025

- 5.6.4 EXPORT VOLUME FOR HS CODE 7221 (STAINLESS STEEL), 2021-2025

- 5.6.5 IMPORT DATA FOR HS CODE 284329 (SILVER), 2021-2025

- 5.6.6 EXPORT DATA FOR HS CODE 284329 (SILVER), 2021-2025

- 5.6.7 IMPORT VOLUME FOR HS 284329 (SILVER), 2021-2025

- 5.6.8 EXPORT VOLUME FOR HS CODE 284329 (SILVER), 2021-2025

- 5.6.9 IMPORT DATA FOR HS CODE 281820 (ALUMINUM OXIDE), 2021-2025

- 5.6.10 EXPORT DATA FOR HS CODE 281820 (ALUMINUM OXIDE), 2021-2025

- 5.6.11 IMPORT VOLUME FOR HS CODE 281820 (ALUMINUM OXIDE), 2021-2025

- 5.6.12 EXPORT VOLUME FOR HS CODE 281820 (ALUMINUM OXIDE), 2021-2025

- 5.6.13 IMPORT DATA FOR HS CODE 3910 (SILICONE), 2021-2025

- 5.6.14 EXPORT DATA FOR HS CODE 3910 (SILICONE), 2021-2025

- 5.6.15 IMPORT VOLUME FOR HS 3910 (SILICONE), 2021-2025

- 5.6.16 EXPORT VOLUME FOR HS CODE 3910 (SILICONE), 2021-2025

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SCALING MEDICAL-GRADE POLYMER SUPPLY THROUGH INTEGRATED VERBUND MANUFACTURING

- 5.10.2 STRENGTHENING HIGH-PERFORMANCE POLYMER PLATFORMS FOR REGULATED BIOMATERIALS APPLICATIONS

- 5.10.3 ADVANCING BIORESORBABLE AND BIOCOMPATIBLE MATERIALS FOR CLINICAL AND COMMERCIAL SCALE-UP

- 5.11 IMPACT OF 2025 US TARIFF ON BIOMATERIALS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Medical device manufacturers

- 5.11.5.2 Pharmaceutical & biotechnology companies

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Precision technologies

- 6.1.1.2 Biomimetics

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 3D bioprinting

- 6.1.2.2 Electrospinning

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR BIOMATERIAL PATENTS, 2015-2025

- 6.3.2 LIST OF PATENTS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON BIOMATERIALS MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM KEY END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 BIOMATERIALS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 METALLIC BIOMATERIALS

- 9.2.1 STAINLESS STEEL

- 9.2.1.1 Favorable mechanical properties, corrosion resistance, and cost-effectiveness to drive usage

- 9.2.2 TITANIUM & TITANIUM ALLOYS

- 9.2.2.1 Rising number of joint replacement procedures to aid market growth

- 9.2.3 COBALT-CHROME ALLOYS

- 9.2.3.1 Low cost and excellent corrosion resistance to augment market growth

- 9.2.4 SILVER

- 9.2.4.1 Toxic properties and low aesthetic to limit use of silver in biomaterial-based products

- 9.2.5 GOLD

- 9.2.5.1 Expanding applications of gold nanoparticles to drive demand for gold biomaterials

- 9.2.6 MAGNESIUM

- 9.2.6.1 Biodegradable characteristics of magnesium to aid segment growth

- 9.2.7 OTHER METALLIC BIOMATERIALS

- 9.2.1 STAINLESS STEEL

- 9.3 POLYMERIC BIOMATERIALS

- 9.3.1 POLYMETHYLMETHACRYLATE (PMMA)

- 9.3.1.1 Long-standing clinical record demonstrating safety and biocompatibility to spur market growth

- 9.3.2 POLYETHYLENE

- 9.3.2.1 Wear and tear resistance of polyethylene to popularize usage in hip and knee joint replacements

- 9.3.3 POLYESTER

- 9.3.3.1 Biodegradable nature and biocompatibility to boost use in various medical applications

- 9.3.4 POLYVINYLCHLORIDE

- 9.3.4.1 Heavy chlorine content of polyvinylchloride to hamper market growth

- 9.3.5 SILICONE RUBBER

- 9.3.5.1 Non-reactive, stable, and resistant in extreme environments and temperatures to drive adoption of silicone rubber

- 9.3.6 NYLON

- 9.3.6.1 Low weight, corrosion resistance, and wide applications to propel market demand

- 9.3.7 POLYETHERETHERKETONE

- 9.3.7.1 Polyetheretherketone to gain popularity as viable alternative to metals

- 9.3.8 OTHER POLYMERIC BIOMATERIALS

- 9.3.1 POLYMETHYLMETHACRYLATE (PMMA)

- 9.4 CERAMIC BIOMATERIALS

- 9.4.1 CALCIUM PHOSPHATE

- 9.4.1.1 Close structural and chemical resemblance to natural bone and teeth to drive adoption in biomedical applications

- 9.4.2 ZIRCONIA

- 9.4.2.1 Bio-inertness and low wear rate of zirconia to boost market adoption

- 9.4.3 ALUMINUM OXIDE

- 9.4.3.1 Increasing use of aluminum oxide in hip replacements and dental implants to drive market

- 9.4.4 CALCIUM SULFATE

- 9.4.4.1 Better biocompatibility and bioresorbability to augment market adoption

- 9.4.5 CARBON

- 9.4.5.1 Increasing use of carbon nanofibers in regenerative medicine and cancer treatment to drive market growth

- 9.4.6 GLASS

- 9.4.6.1 Rising number of orthopedic and dental procedures to fuel demand for glass biomaterials

- 9.4.1 CALCIUM PHOSPHATE

- 9.5 NATURAL BIOMATERIALS

- 9.5.1 HYALURONIC ACID

- 9.5.1.1 Rising incidences of osteoarthritis to drive hyaluronic acid biomaterials market

- 9.5.2 COLLAGEN

- 9.5.2.1 High tensile strength to be useful in plastic and cosmetic surgeries, cardiology, ophthalmology, and drug delivery

- 9.5.3 FIBRIN

- 9.5.3.1 Fibrin biomaterials to be useful in clinical practice for controlling bleeding and accelerating wound repair

- 9.5.4 CELLULOSE

- 9.5.4.1 Cellulose to be useful in wound healing, skin regeneration, and ophthalmology

- 9.5.5 CHITIN

- 9.5.5.1 Chitin to accelerate skin regeneration and possess high biocompatibility

- 9.5.6 ALGINATES

- 9.5.6.1 Use in wound healing, tissue engineering & regenerative medicine, and drug delivery to drive adoption

- 9.5.7 GELATIN

- 9.5.7.1 Low cost and comparable biocompatibility of gelatin to fuel market adoption

- 9.5.8 CHITOSAN

- 9.5.8.1 Non-toxicity of Chitosan to increase adoption in biomedical research

- 9.5.9 SILK

- 9.5.9.1 Flexibility and adhesive abilities to drive usage in wound healing applications

- 9.5.10 OTHER NATURAL BIOMATERIALS

- 9.5.1 HYALURONIC ACID

10 BIOMATERIALS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 ORTHOPEDIC

- 10.2.1 JOINT REPLACEMENT

- 10.2.1.1 Knee replacement

- 10.2.1.1.1 Rising count of knee replacement procedures globally to drive market growth

- 10.2.1.2 Hip replacement

- 10.2.1.2.1 Hip & knee joint replacements to be most commonly performed procedures

- 10.2.1.3 Shoulder replacement

- 10.2.1.3.1 Increasing shoulder surgeries to drive production of implants

- 10.2.1.4 Other joint replacement applications

- 10.2.1.1 Knee replacement

- 10.2.2 BIORESORBABLE TISSUE FIXATION

- 10.2.2.1 Suture anchors

- 10.2.2.1.1 Growing awareness about suture anchor devices to propel market growth

- 10.2.2.2 Interference screws

- 10.2.2.2.1 Growing ACL reconstruction procedures to contribute to market growth

- 10.2.2.3 Meniscal repair tacks

- 10.2.2.3.1 Rising sports injuries to fuel growth in meniscal repair tacks market

- 10.2.2.4 Meshes

- 10.2.2.4.1 Wear resistance and proper shaping of bioresorbable implants to increase demand for bioresorbable meshes

- 10.2.2.1 Suture anchors

- 10.2.3 SPINE SURGERIES

- 10.2.3.1 Spinal fusion

- 10.2.3.1.1 Introduction of minimally invasive spinal fusion procedures and better clinical outcomes to drive market growth

- 10.2.3.2 Minimally invasive fusion

- 10.2.3.2.1 Lesser post-surgery pain and faster recovery to drive demand for minimally invasive fusion procedures

- 10.2.3.3 Motion preservation & dynamic stabilization

- 10.2.3.3.1 Pedicle-based rod systems

- 10.2.3.3.1.1 Rising geriatric population to result in market growth

- 10.2.3.3.2 Interspinous spacers

- 10.2.3.3.2.1 High prevalence of degenerative spinal conditions to contribute to market growth

- 10.2.3.3.3 Artificial discs

- 10.2.3.3.3.1 High biocompatibility to increase usage in artificial discs

- 10.2.3.3.1 Pedicle-based rod systems

- 10.2.3.1 Spinal fusion

- 10.2.4 FRACTURE FIXATION DEVICES

- 10.2.4.1 Bone plates

- 10.2.4.1.1 High biocompatibility of biomaterials to be an integral component of bone plates

- 10.2.4.2 Screws

- 10.2.4.2.1 Metallic biomaterial screws to be extensively used in orthopedic procedures

- 10.2.4.3 Pins

- 10.2.4.3.1 Nonreactive nature of metallic biomaterial pins to favor usage in fracture fixation

- 10.2.4.4 Rods

- 10.2.4.4.1 High rigidity, easy mobility, and cost efficiency to make rods preferred for fracture fixation procedures

- 10.2.4.5 Wires

- 10.2.4.5.1 Wires made up of metallic biomaterials to help treat fractures of small bones

- 10.2.4.1 Bone plates

- 10.2.5 ORTHOBIOLOGICS

- 10.2.5.1 Rising cases of osteoarthritis to drive growth in viscosupplementation market

- 10.2.1 JOINT REPLACEMENT

- 10.3 CARDIOVASCULAR

- 10.3.1 CATHETERS

- 10.3.1.1 Shift in patient preference from traditional open surgeries to minimally invasive surgeries to drive market

- 10.3.2 STENTS

- 10.3.2.1 Increasing number of coronary intervention procedures to boost demand for implantable stents

- 10.3.3 IMPLANTABLE CARDIAC DEFIBRILLATORS

- 10.3.3.1 Growing geriatric population and rising prevalence of chronic diseases to drive market

- 10.3.4 PACEMAKERS

- 10.3.4.1 High prevalence of bradycardia to aid demand for pacemakers

- 10.3.5 SENSORS

- 10.3.5.1 Increasing prevalence of cardiac disorders to boost demand for cardiovascular sensors

- 10.3.6 HEART VALVES

- 10.3.6.1 Growing geriatric population to increase demand for prosthetic valves

- 10.3.7 VASCULAR GRAFTS

- 10.3.7.1 Focus on research on use of biomaterials in vascular grafts to open opportunities for market growth

- 10.3.8 GUIDEWIRES

- 10.3.8.1 Guidewires to be used for guiding catheters and placing stents inside the heart

- 10.3.9 OTHER CARDIOVASCULAR APPLICATIONS

- 10.3.1 CATHETERS

- 10.4 OPHTHALMOLOGY

- 10.4.1 CONTACT LENSES

- 10.4.1.1 Growing cases of refractive errors and preference for contact lenses over spectacles to drive market growth

- 10.4.2 INTRAOCULAR LENSES

- 10.4.2.1 Increasing prevalence of cataracts to boost number of cataract surgeries performed

- 10.4.3 FUNCTIONAL REPLACEMENT OF OCULAR TISSUES

- 10.4.3.1 Increasing funding and research activities for developing bionic eyes to propel segment growth

- 10.4.4 SYNTHETIC CORNEAS

- 10.4.4.1 Increasing number of corneal blindness cases globally to boost demand for synthetic collagen biomaterials

- 10.4.5 OTHER OPHTHALMOLOGY APPLICATIONS

- 10.4.1 CONTACT LENSES

- 10.5 DENTAL

- 10.5.1 DENTAL IMPLANTS

- 10.5.1.1 Rising awareness about dental health and increasing dental procedures to augment market growth

- 10.5.2 DENTAL BONE GRAFTS & SUBSTITUTES

- 10.5.2.1 Growing demand for dental implants during cosmetic dentistry to drive market

- 10.5.3 DENTAL MEMBRANES

- 10.5.3.1 Dental membranes in oral and periodontal surgery to prevent unwanted infections in oral cavity

- 10.5.4 TISSUE REGENERATION MATERIALS

- 10.5.4.1 Increasing prevalence of periodontal disease to augment market growth

- 10.5.1 DENTAL IMPLANTS

- 10.6 PLASTIC SURGERY

- 10.6.1 SOFT TISSUE FILLERS

- 10.6.1.1 Long-lasting capacity and fewer allergic reactions to drive demand for soft-tissue fillers

- 10.6.2 CRANIOFACIAL SURGERY

- 10.6.2.1 Increasing incidence of trauma cases and head & neck cancer to augment market growth

- 10.6.3 FACIAL WRINKLE TREATMENT

- 10.6.3.1 Increase in demand for non-surgical cosmetic treatments to propel market growth

- 10.6.4 BIOENGINEERED SKINS

- 10.6.4.1 Increasing incidence of trauma cases and head & neck cancer to increase number of craniofacial surgeries

- 10.6.5 PERIPHERAL NERVE REPAIR

- 10.6.5.1 Increasing incidence of trauma cases to rise in peripheral nerve injuries

- 10.6.6 ACELLULAR DERMAL MATRICES

- 10.6.6.1 Ability to provide scaffold for tissue regeneration and reduce risk of immune rejection and adverse reactions to drive segment

- 10.6.1 SOFT TISSUE FILLERS

- 10.7 WOUND HEALING

- 10.7.1 WOUND CLOSURE DEVICES

- 10.7.1.1 Sutures

- 10.7.1.1.1 Sutures to be used as advanced biologically active components for better drug delivery

- 10.7.1.2 Staples

- 10.7.1.2.1 Ease of placement and ability to shorten closure to augment segment growth

- 10.7.1.1 Sutures

- 10.7.2 SURGICAL HEMOSTATS

- 10.7.2.1 Surgical hemostats to control bleeding and reduce frequent blood transfusions during surgical procedures

- 10.7.3 INTERNAL TISSUE SEALANTS

- 10.7.3.1 Increasing number of surgeries to drive use of internal tissue sealants

- 10.7.4 ADHESION BARRIERS

- 10.7.4.1 Focus on inflammatory healing process to drive adoption of adhesion barriers in surgical procedures

- 10.7.5 HERNIA MESHES

- 10.7.5.1 Polymeric biomaterial-based meshes to be used in hernia repair

- 10.7.6 SKIN SUBSTITUTES

- 10.7.6.1 Focus on prompting tissue regeneration and replacing damaged skin with functional tissue to aid market growth

- 10.7.1 WOUND CLOSURE DEVICES

- 10.8 TISSUE ENGINEERING

- 10.8.1 SCAFFOLDS FOR BIOMATERIALS

- 10.8.1.1 Rise in organ transplantation procedures to drive market

- 10.8.2 NANOMATERIALS FOR BIOSENSING

- 10.8.2.1 Rising research in nanotechnology to augment market growth

- 10.8.3 TAILORING OF INORGANIC NANOPARTICLES

- 10.8.3.1 Growing demand for nanotechnological medical products to drive market

- 10.8.1 SCAFFOLDS FOR BIOMATERIALS

- 10.9 NEUROLOGICAL/CENTRAL NERVOUS SYSTEM

- 10.9.1 SHUNTING SYSTEMS

- 10.9.1.1 Rising cases of hydrocephalus to boost market growth

- 10.9.2 CORTICAL NEURAL PROSTHETICS

- 10.9.2.1 Increased use of polymer-coated CNPs to treat paralyzed patients

- 10.9.3 HYDROGEL SCAFFOLDS FOR CNS REPAIR

- 10.9.3.1 Increasing incidence of spinal cord surgeries to drive demand for hydrogel scaffolds

- 10.9.4 NEURAL STEM CELL ENCAPSULATION

- 10.9.4.1 Lack of substitutes for neurotrauma treatment to boost market growth

- 10.9.1 SHUNTING SYSTEMS

- 10.10 URINARY

- 10.10.1 URINARY CATHETERS

- 10.10.1.1 Rise in implant-related cases of biofilm-associated infections to hinder market growth

- 10.10.2 URETHRAL STENTS

- 10.10.3 OTHER URINARY APPLICATIONS

- 10.10.1 URINARY CATHETERS

- 10.11 OTHER APPLICATIONS

- 10.11.1 DRUG DELIVERY SYSTEMS

- 10.11.2 GASTROINTESTINAL APPLICATIONS

- 10.11.3 BARIATRIC SURGERY

11 BIOMATERIALS MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 MEDICAL DEVICE MANUFACTURERS

- 11.2.1 DEMOGRAPHIC SHIFTS, TECHNOLOGICAL INNOVATION, AND EXPANDING CLINICAL APPLICATIONS TO DRIVE MARKET

- 11.3 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 11.3.1 INVESTMENT AND INNOVATION MOMENTUM IN PHARMA & BIOTECH TO ACCELERATE GLOBAL BIOMATERIAL ADOPTION

- 11.4 OTHER END USERS

12 BIOMATERIALS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Rising incidence of cancer and ongoing research in developing biocompatible materials to drive market

- 12.2.2 CANADA

- 12.2.2.1 Growing incidence of cardiovascular diseases to propel market growth

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Rising focus on clinical research and increasing number of patent approvals to aid market growth

- 12.3.2 UK

- 12.3.2.1 Increasing research activities and rising number of cardiovascular procedures to support market growth

- 12.3.3 FRANCE

- 12.3.3.1 Increased healthcare expenditure and structured regulatory framework to augment market growth

- 12.3.4 ITALY

- 12.3.4.1 Rising prevalence of neurological and cardiovascular disorders to boost market growth

- 12.3.5 SPAIN

- 12.3.5.1 Increased focus on research for biomaterial development to propel market growth

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Lucrative medical devices industry and large geriatric population to drive market

- 12.4.2 JAPAN

- 12.4.2.1 Growing medical devices industry and rising focus on medical research to support market growth

- 12.4.3 INDIA

- 12.4.3.1 Large population base and high focus on medical tourism to aid market growth

- 12.4.4 SOUTH KOREA

- 12.4.4.1 High demand for healthcare services and advanced treatments to spur market growth

- 12.4.5 AUSTRALIA

- 12.4.5.1 Strategic public and sector-wide investments with clinical trial system reform to underpin biomedical research growth

- 12.4.6 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 LATIN AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Gradual increase in pharmaceutical R&D to fuel market growth

- 12.5.2 MEXICO

- 12.5.2.1 Rising number of cosmetic procedures to boost adoption of biomaterials

- 12.5.3 ARGENTINA

- 12.5.3.1 Increased incidence of cardiovascular diseases and favorable government healthcare system to aid market growth

- 12.5.4 REST OF LATIN AMERICA

- 12.5.1 BRAZIL

- 12.6 MIDDLE EAST

- 12.6.1 GCC COUNTRIES

- 12.6.1.1 Kingdom of Saudi Arabia

- 12.6.1.1.1 Increasing prevalence of cardiovascular diseases to drive market

- 12.6.1.2 UAE

- 12.6.1.2.1 Strategic partnerships and regulatory alignment to drive global biomaterials market growth

- 12.6.1.3 Rest of GCC countries

- 12.6.1.1 Kingdom of Saudi Arabia

- 12.6.2 REST OF MIDDLE EAST

- 12.6.1 GCC COUNTRIES

- 12.7 AFRICA

- 12.7.1 EXPANSION IN HEALTHCARE INDUSTRY AND SUPPORTIVE REGULATORY POLICIES TO AID MARKET GROWTH

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

- 13.2.1 STRATEGIES ADOPTED BY KEY PLAYERS IN BIOMATERIALS MARKET

- 13.3 REVENUE ANALYSIS, 2023-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPETITIVE BENCHMARKING: KEY PLAYERS, 2025

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Type footprint

- 13.5.5.4 Application footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 13.6.5.1 List of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF SE

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Services/Solutions offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 COVESTRO AG

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Services/Solutions offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.3.4 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 CELANESE CORPORATION

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Services/Solutions offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 CARPENTER TECHNOLOGY CORPORATION

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Services/Solutions offered

- 14.1.4.2.1 Other developments

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 EVONIK INDUSTRIES AG

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Services/Solutions offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 DSM

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Services/Solutions offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.7 CORBION NV

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Services/Solutions offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Expansions

- 14.1.8 VICTREX PLC

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Services/Solutions offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Expansions

- 14.1.9 MITSUBISHI CHEMICAL CORPORATION

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Services/Solutions offered

- 14.1.10 COORSTEK INC.

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Services/Solutions offered

- 14.1.11 BERKELEY ADVANCED BIOMATERIALS

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Services/Solutions offered

- 14.1.12 CAM BIOCERAMICS B.V.

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Services/Solutions offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Deals

- 14.1.13 ZEUS COMPANY INC.

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Services/Solutions offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Product launches

- 14.1.13.3.2 Expansions

- 14.1.14 AMETEK INC.

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Services/Solutions offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Deals

- 14.1.14.3.2 Expansions

- 14.1.15 GELITA AG

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Services/Solutions offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Product launches

- 14.1.1 BASF SE

- 14.2 OTHER PLAYERS

- 14.2.1 COLLAGEN SOLUTIONS (US) LLC

- 14.2.2 BIOCOMPOSITES

- 14.2.3 NOBLE BIOMATERIALS, INC.

- 14.2.4 REGENITY

- 14.2.5 KURARAY CO., LTD.

- 14.2.6 SOLESIS

- 14.2.7 INSTITUT STRAUMANN AG

- 14.2.8 FOSTER CORPORATION

- 14.2.9 CDI PRODUCTS

- 14.2.10 REVBIO, INC.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key objectives of secondary research

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Breakdown of primaries

- 15.1.2.2 Key objectives of primary research

- 15.1.1 SECONDARY DATA

- 15.2 MARKET ESTIMATION METHODOLOGY

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 COMPANY REVENUE ANALYSIS (BOTTOM-UP APPROACH)

- 15.3.2 MNM REPOSITORY ANALYSIS

- 15.3.3 PRIMARY INTERVIEWS

- 15.3.4 INSIGHTS OF PRIMARY EXPERTS

- 15.3.5 TOP-DOWN APPROACH

- 15.4 MARKET GROWTH RATE PROJECTIONS

- 15.5 DATA TRIANGULATION

- 15.6 STUDY ASSUMPTIONS

- 15.7 RESEARCH LIMITATIONS

- 15.8 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS