|

시장보고서

상품코드

2003239

심장 모니터링 및 리듬 관리 디바이스 시장 예측(-2031년) : 유형(심장 모니터링, 심장 리듬 관리(페이스메이커)), 제세동기), 용도, 최종사용자별Cardiac Monitoring & Rhythm Management Devices Market by Type (Cardiac Monitoring, Cardiac Rhythm Management (Pacemaker ), Defibrillator ), Application, End User - Global Forecast to 2031 |

||||||

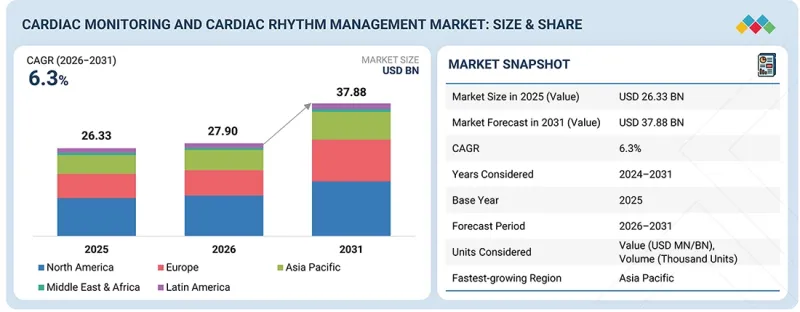

세계의 심장 모니터링 및 리듬 관리 디바이스 시장 규모는 2026년 279억 달러에서 2031년까지 378억 8,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 6.3%로 성장할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 금액(달러) |

| 부문 | 유형, 용도, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

시장 성장은 심혈관 질환의 조기 발견을 위한 인식 개선 캠페인과 검진 프로그램 확대 등의 요인에 의해 주도되고 있으며, 이는 특히 고위험군에서 심장 모니터링 기기에 대한 수요 확대에 기여하고 있습니다. 한편, 원격 모니터링 및 원격의료 기술의 도입과 함께 데이터 보안 및 환자 프라이버시에 대한 우려가 증가하고 있으며, 이는 환자의 수용과 도입을 방해할 수 있습니다.

"예측 기간 중 이식형 제세동기가 가장 큰 시장 점유율을 차지했습니다. "

유형별로는 이식형 제세동기가 2025년에 가장 큰 시장 점유율을 차지했습니다. 이는 심장 리듬을 지속적으로 모니터링하고 필요한 경우 적절한 치료를 시행하여 갑작스러운 심장마비로부터 환자를 보호하기 위함입니다. 이러한 지속적인 모니터링과 개입을 통해 생명을 위협하는 부정맥의 위험에 처한 환자들에게 24시간 보호가 제공됩니다. 한편, 체외형 제세동기는 일반적으로 응급상황에서 급성기 중재에 사용됩니다. 마찬가지로 이식형 제세동기는 심실성 부정맥이나 심근병증과 같은 기저질환으로 인해 돌연사 위험이 높은 환자에게 외과적 수술이나 최소침습적 시술로 이식합니다. 장기적인 사용을 목적으로 하며, 지속적인 리듬 관리가 필요한 환자에게 적합합니다. 자동 체외식 제세동기(AED)와 병원에서 사용되는 수동식 제세동기와 같은 체외형 제세동기는 주로 심정지시 응급 소생술에 사용됩니다.

"예측 기간 중 홈케어 분야가 가장 높은 CAGR을 기록할 것으로 예상됩니다. "

홈케어 부문은 원격 환자 모니터링과 재택 심장 관리로의 전환이 진행됨에 따라 가장 빠르게 성장하는 최종사용자층입니다. 웨어러블, 휴대용, 커넥티드 디바이스의 발전으로 기존 임상 현장 밖에서도 지속적인 모니터링과 리듬 관리가 가능해져 환자의 편의성과 치료 결과가 향상되고 있습니다. 또한 만성 심장 질환의 유병률 증가, 고령화, 입원 및 의료비 절감에 대한 노력은 재택 의료 환경에서의 이러한 장치의 도입을 더욱 가속화시키고 있습니다.

"북미 지역이 가장 큰 점유율을 차지했습니다. "

지역별 분석에 따르면 북미 지역은 2025년 이후에도 계속해서 큰 시장 점유율을 유지할 것으로 예상됩니다. 북미 시장은 심장병 환자 증가, 의료비 증가, 질병 조기 진단에 대한 인식이 높아지면서 시장을 주도하고 있습니다.

세계의 심장 모니터링 및 리듬 관리 디바이스 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다. 을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 도입에 의한 전략적 디스럽션

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 리듬 관리 디바이스 시장 : 유형별

제10장 심장 모니터링 기기 시장 : 유형별

제11장 심장 모니터링 및 리듬 관리 디바이스 시장 : 용도별

제12장 심장 모니터링 및 리듬 관리 디바이스 시장 : 최종사용자별

제13장 심장 모니터링 및 리듬 관리 디바이스 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

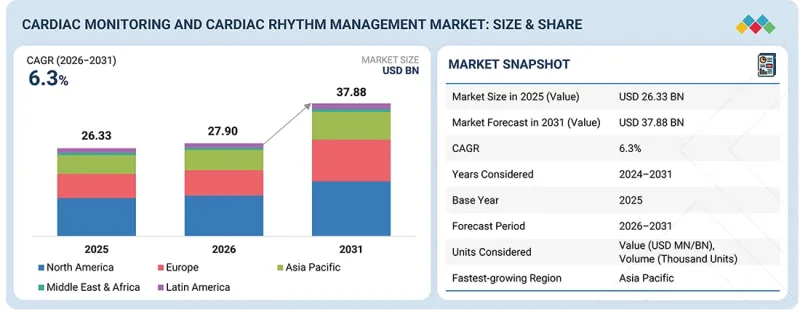

KSA 26.04.24The global cardiac monitoring and cardiac rhythm management devices market is projected to reach USD 37.88 billion by 2031, up from USD 27.90 billion in 2026, growing at a CAGR of 6.3% over the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Application, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Market growth is driven by factors such as rising public awareness campaigns and screening programs aimed at early detection of cardiovascular diseases, which contribute to growing demand for cardiac monitoring devices, especially in high-risk populations. On the other hand, the adoption of remote monitoring and telemedicine technologies raises concerns about data security and patient privacy, which may hinder patient acceptance and adoption of these devices.

"The implantable cardioverter defibrillators accounted for the largest market share in the cardiac rhythm management device market, during the forecast period."

By type, cardiac rhythm management devices in the market are classified into implantable cardioverter defibrillators and external defibrillators. In 2025, implantable cardioverter defibrillators accounted for a sizable market share because they provide continuous protection against sudden cardiac arrest by continuously monitor the heart's rhythm and deliver appropriate therapy when needed, protecting against sudden cardiac arrest. This constant monitoring and intervention offer round-the-clock protection for patients at risk of life-threatening arrhythmias, whereas external defibrillators are typically used for acute interventions in emergencies. Likewise, Implantable defibrillators are implanted surgically or via minimally invasive procedures in patients at high risk of sudden cardiac death due to underlying cardiac conditions such as ventricular arrhythmias or cardiomyopathy. They are intended for long-term use and are suitable for patients who require ongoing arrhythmia management. In contrast, external defibrillators, such as automated external defibrillators (AEDs) or manual defibrillators used in hospitals, are used mainly for emergency resuscitation in cases of cardiac arrest.

The home care settings are projected to register the highest CAGR during the forecast period."

In the cardiac monitoring and rhythm management devices market, the home care segment is the fastest-growing end user due to the growing shift toward remote patient monitoring and home-based cardiac care. Advances in wearable, portable, and connected devices enable continuous monitoring and rhythm management outside traditional clinical settings, improving patient convenience and outcomes. Additionally, rising prevalence of chronic cardiac conditions, an aging population, and efforts to reduce hospitalizations and healthcare costs are further accelerating the adoption of these devices in home care environments.

"The North American region accounted for the highest share."

The global cardiac monitoring and cardiac rhythm management devices market is divided into four regions: North America, Asia-Pacific, Europe, and the Rest of the World. According to the regional analysis, the North American region is likely to retain a significant market share in 2025 and beyond. The North American market is being propelled by rising cases of heart disease, increased healthcare expenditure, and greater awareness of early disease diagnosis.

The primary interviews conducted for this report can be categorized as follows:

- By Company Type: Tier 1 - 32%, Tier 2 - 44%, and Tier 3 - 24%

- By Designation: C-level - 30%, D-level - 34%, and Others - 36%

- By Region: North America - 40%, Europe - 28%, Asia Pacific - 20%, and the Rest of the World - 12%

The prominent players in the GE HealthCare (US), Koninklijke Philips N.V. (Netherlands), Boston Scientific Corporation (US), Baxter (US), Medtronic (Ireland), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), Abbott (US), Stryker (US), NIHON KOHDEN CORPORATION (Japan), MicroPort Scientific Corporation (China), FUKUDA DENSHI (Japan), OSI Systems, Inc. (US), iRhythm Inc. (US), Lepu Medical Technology (Beijing) Co., Ltd. (China), and AliveCor, Inc. (US) among others.

Research Coverage

This report studies the Cardiac monitoring and cardiac rhythm management devices market based on type, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets by their individual growth trends and forecasts market segment revenue for five central regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the market pulse, which, in turn, will help them garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

- Analysis of key drivers (rapidly expanding global geriatric population and subsequent surge in cardiac diseases, increasing incidence of lifestyle and cardiovascular diseases), restraints (rapidly expanding global geriatric population and subsequent surge in cardiac diseases, Increasing incidence of lifestyle and cardiovascular diseases), opportunities (untapped growth potential in emerging markets), and challenges (frequent product recalls) influencing the growth of the cardiac monitoring and cardiac rhythm management devices market

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the Cardiac monitoring and cardiac rhythm management devices market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product developments in the Cardiac monitoring and cardiac rhythm management devices market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the Cardiac monitoring and cardiac rhythm management devices market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 TUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 CARDIAC MONITORING AND RHYTHM MANAGEMENT MARKET DEVICES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET, BY APPLICATION AND COUNTRY

- 3.3 GEOGRAPHIC SNAPSHOT OF CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising geriatric population with chronic cardiovascular diseases

- 4.2.1.2 Increasing incidence of lifestyle and cardiovascular diseases

- 4.2.1.3 Development of wireless monitoring and wearable cardiac devices

- 4.2.1.4 Rapid adoption of leadless pacemakers

- 4.2.1.5 Increasing focus on providing public-access defibrillators

- 4.2.2 RESTRAINTS

- 4.2.2.1 Increasing regulatory scrutiny extending time-to-market for cardiac devices

- 4.2.2.2 High device costs and reimbursement gaps

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Untapped growth potential in emerging markets

- 4.2.3.2 Emergence of leadless CRT platforms

- 4.2.4 CHALLENGES

- 4.2.4.1 Frequent product recalls

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY STRATEGIC MOVES BY TIER-1/2/3 PLAYERS IN CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.3 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 ROLE IN ECOSYSTEM

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF CARDIAC MONITORING DEVICES, BY KEY PLAYER, 2024 AND 2025 (USD)

- 5.6.1.1 Average selling price of Holter monitors, by key player, 2025

- 5.6.1.2 Average selling price of external defibrillators, by key player, 2024

- 5.6.2 AVERAGE SELLING PRICE TREND OF CARDIAC RHYTHM MANAGEMENT DEVICES, BY REGION, 2023-2025

- 5.6.1 AVERAGE SELLING PRICE TREND OF CARDIAC MONITORING DEVICES, BY KEY PLAYER, 2024 AND 2025 (USD)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 901811, 2021-2024

- 5.7.2 EXPORT DATA FOR HS CODE 901811, 2021-2024

- 5.8 KEY CONFERENCES & EVENTS, 2025-2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 DUAL-CHAMBER LEADLESS PACEMAKER BY ABBOTT

- 5.11.2 CARDIOSOFT ECG-BICESTER HEALTH CENTRE IN NUMED HEALTHCARE

- 5.11.3 POST-STROKE ATRIAL FIBRILLATION DETECTION WITH PHILIPS BIOTEL HEART MCOT

- 5.12 IMPACT OF 2025 US TARIFF ON CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET

- 5.12.1 KEY TARIFF RATES

- 5.12.2 PRICE IMPACT ANALYSIS

- 5.12.3 IMPACT ON COUNTRY/REGION

- 5.12.4 IMPACT ON END-USE INDUSTRIES

6 DSTRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Artificial intelligence (AI) and predictive analytics

- 6.1.1.2 Miniaturization of cardiac devices

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Wearable biosensors

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Vital sign monitors

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR TERM (2025-2027)

- 6.2.2 MID TERM (2028-2030)

- 6.2.3 LONG TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 FULLY AUTONOMOUS CARDIAC DIAGNOSTICS & DECISION-SUPPORT ECOSYSTEMS

- 6.4.2 PRECISION RHYTHM MANAGEMENT THROUGH PREDICTIVE & PRE-EMPTIVE THERAPY DELIVERY

- 6.4.3 FULLY LEADLESS, MODULAR, AND WIRELESSLY NETWORKED CARDIAC SYSTEMS

- 6.4.4 REGENERATIVE-INTEGRATED RHYTHM MANAGEMENT SYSTEMS

- 6.5 IMPACT OF AI/GEN AI ON CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET

- 6.5.1 MARKET POTENTIAL OF AI

- 6.5.2 AI USE CASES

- 6.5.3 KEY COMPANIES IMPLEMENTING AI

- 6.5.4 BEST PRACTICES IN CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES

- 6.5.5 CASE STUDIES OF AI IMPLEMENTATION

- 6.5.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.4 Latin America

- 7.1.1.5 Middle East & Africa

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLABLE BIOMATERIALS FOR ECG PATCHES

- 7.2.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 RHYTHM MANAGEMENT DEVICES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 PACEMAKERS

- 9.2.1 SINGLE-CHAMBER PACEMAKERS

- 9.2.1.1 Increasing use of single-chamber pacemakers for managing bradyarrhythmias and conduction disorders to aid market growth

- 9.2.2 DUAL-CHAMBER PACEMAKERS

- 9.2.2.1 Dual-chamber pacemakers to witness high demand with widespread usage

- 9.2.3 LEADLESS CHAMBER PACEMAKERS

- 9.2.3.1 Focus on minimally invasive implantation and reduced complication rates to propel market growth

- 9.2.1 SINGLE-CHAMBER PACEMAKERS

- 9.3 DEFIBRILLATORS

- 9.3.1 IMPLANTABLE CARDIOVERTER DEFIBRILLATORS (ICDS)

- 9.3.1.1 Single-chamber implantable cardioverter-defibrillators (ICDs)

- 9.3.1.1.1 Utilization in arterial monitoring to support market growth

- 9.3.1.2 Dual-chamber implantable cardioverter-defibrillators (ICDs)

- 9.3.1.2.1 Ability to reduce incidence of inappropriate shocks to drive market

- 9.3.1.3 Subcutaneous implantable cardioverter-defibrillators (ICDs)

- 9.3.1.3.1 Benefits of eliminating cardiac leads to drive market

- 9.3.1.1 Single-chamber implantable cardioverter-defibrillators (ICDs)

- 9.3.2 EXTERNAL DEFIBRILLATORS

- 9.3.2.1 Automated external defibrillators (AEDs)

- 9.3.2.1.1 Smart automated external defibrillators advancing public cardiac emergency response to aid market growth

- 9.3.2.2 Manual external defibrillators

- 9.3.2.2.1 Innovation in manual external defibrillators to enhance emergency cardiac care

- 9.3.2.3 Wearable cardioverter defibrillators (WCDs)

- 9.3.2.3.1 Operational difficulties and false alarms to restrain market adoption

- 9.3.2.1 Automated external defibrillators (AEDs)

- 9.3.1 IMPLANTABLE CARDIOVERTER DEFIBRILLATORS (ICDS)

- 9.4 CARDIAC RESYNCHRONIZATION THERAPY (CRT)

- 9.4.1 CARDIAC RESYNCHRONIZATION THERAPY-PACEMAKERS (CRT-P)

- 9.4.2 CARDIAC RESYNCHRONIZATION THERAPY-DEFIBRILLATORS (CRT-D)

10 CARDIAC MONITORING DEVICES MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 NON-INVASIVE CARDIAC MONITORING DEVICES

- 10.2.1 ELECTROCARDIOGRAM (ECG/EKG) MONITORS

- 10.2.1.1 Standard 12-lead ECG machines (resting ECG monitors)

- 10.2.1.1.1 Wide availability of resting ECG devices to support market growth

- 10.2.1.2 Stress ECG systems

- 10.2.1.2.1 High cost of stress ECG devices to limit adoption

- 10.2.1.3 Handheld/Smart ECG monitors

- 10.2.1.3.1 Rising adoption of AI technology and growing need to minimize treatment costs to support market growth

- 10.2.1.1 Standard 12-lead ECG machines (resting ECG monitors)

- 10.2.2 AMBULATORY CARDIAC MONITORS

- 10.2.2.1 Holter monitors

- 10.2.2.1.1 Growing demand for continuous monitoring to fuel segment growth

- 10.2.2.2 Event monitors

- 10.2.2.2.1 Increasing outsourcing of monitoring devices to propel market growth

- 10.2.2.3 Mobile cardiac telemetry (MCT) devices

- 10.2.2.3.1 Increasing demand for cardiac monitoring solutions in home care settings to aid segment growth

- 10.2.2.4 Long-term continuous ECG monitors

- 10.2.2.4.1 Increasing adoption of patch-based ECG monitors for extended ambulatory cardiac monitoring to aid market growth

- 10.2.2.1 Holter monitors

- 10.2.1 ELECTROCARDIOGRAM (ECG/EKG) MONITORS

- 10.3 INVASIVE CARDIAC MONITORING DEVICES

- 10.3.1 INTRODUCTION OF TECHNOLOGICALLY ADVANCED IMPLANTABLE LOOP RECORDERS TO SUPPORT MARKET GROWTH

11 CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 ARRHYTHMIAS

- 11.2.1 GROWING NUMBER OF ATRIAL FIBRILLATION CASES TO DRIVE MARKET

- 11.3 HEART FAILURE

- 11.3.1 GROWING PREVALENCE OF CHRONIC LIFESTYLE DISEASES TO DRIVE PREVALENCE OF HEART FAILURE

- 11.4 MYOCARDIAL INFARCTION (MI)

- 11.4.1 RISING GERIATRIC POPULATION TO SPUR MARKET GROWTH

- 11.5 OTHER APPLICATIONS

12 CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS

- 12.2.1 INCREASING UTILIZATION OF CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES IN HOSPITALS TO AID MARKET GROWTH

- 12.3 PRIMARY CARE CENTERS

- 12.3.1 WIDENING ACCESS TO ECG MONITORING IN PRIMARY CARE CENTERS TO BOOST MARKET PENETRATION

- 12.4 CARDIAC CENTERS

- 12.4.1 INCREASED INCIDENCE OF CARDIOVASCULAR DISEASE AND HIGH DEMAND FOR SPECIALIZED CARE TO BOOST MARKET GROWTH

- 12.5 AMBULATORY SURGICAL CENTERS

- 12.5.1 GROWING NEED FOR PRE-OPERATIVE CARDIAC SCREENING IN AMBULATORY SURGICAL CENTERS TO INFLUENCE MARKET DEMAND

- 12.6 HOME CARE SETTINGS

- 12.6.1 RISING PREFERENCE FOR REMOTE CARDIAC MONITORING TO FUEL MARKET GROWTH

- 12.7 OTHER END USERS

13 CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 US to dominate North American cardiac monitoring and rhythm management devices market during forecast period

- 13.2.3 CANADA

- 13.2.3.1 High burden of cardiovascular diseases to support market growth

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 High healthcare spending to propel market growth

- 13.3.3 FRANCE

- 13.3.3.1 Favorable government initiatives to support market growth

- 13.3.4 UK

- 13.3.4.1 Rising demand for home-based smart ECG devices to support market growth

- 13.3.5 ITALY

- 13.3.5.1 Growing focus on improvements in patient care to drive market

- 13.3.6 SPAIN

- 13.3.6.1 Rising geriatric population to support market growth in Spain

- 13.3.7 AUSTRIA

- 13.3.7.1 Favourable insurance coverage for cardiac diagnostic procedures to support market growth

- 13.3.8 NETHERLANDS

- 13.3.8.1 Strong primary care referral pathway to aid adoption of cardiac monitoring and rhythm devices

- 13.3.9 SWEDEN

- 13.3.9.1 Expansion of long-term ambulatory ECG monitoring to augment market growth

- 13.3.10 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 JAPAN

- 13.4.2.1 High healthcare expenditure and favorable reimbursement and insurance coverage to support market growth

- 13.4.3 CHINA

- 13.4.3.1 Government support for infrastructural improvement to drive market

- 13.4.4 INDIA

- 13.4.4.1 Increasing cardiac disease burden intensifies demand for cardiac monitoring and rhythm management devices

- 13.4.5 AUSTRALIA

- 13.4.5.1 Australia to strengthen community access to rhythm management devices through policy and targeted funding

- 13.4.6 SOUTH KOREA

- 13.4.6.1 Rising geriatric population to propel market growth

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Improving access to diagnostic services to drive market growth

- 13.5.3 MEXICO

- 13.5.3.1 Rising incidences of heart disease to propel market growth

- 13.5.4 COLOMBIA

- 13.5.4.1 High arrhythmia burden to drive demand for cardiac rhythm monitoring in Colombia

- 13.5.5 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Kingdom of Saudi Arabia

- 13.6.2.1.1 High prevalence of cardiovascular diseases and increased demand for cardiac diagnostic solutions to drive market

- 13.6.2.2 UAE

- 13.6.2.2.1 Focus on national CVD screening programs and digital health strategies to augment market growth

- 13.6.2.3 Rest of GCC Countries

- 13.6.2.1 Kingdom of Saudi Arabia

- 13.6.3 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY PRODUCT FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Type footprint

- 14.6.5.5 Application footprint

- 14.7 COMPANY EVALUATION MATRIX FOR STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION & FINANCIAL METRICS

- 14.8.1 FINANCIAL METRICS

- 14.8.2 COMPANY VALUATION

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES & APPROVALS

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 GE HEALTHCARE

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 KONINKLIJKE PHILIPS N.V.

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.3.4 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 BOSTON SCIENTIFIC CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 BAXTER (HILL-ROM HOLDINGS, INC.)

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.5 MEDTRONIC

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product approvals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches & approvals

- 15.1.6.3.2 Other developments

- 15.1.7 ABBOTT

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches & approvals

- 15.1.8 STRYKER

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Other developments

- 15.1.9 NIHON KOHDEN CORPORATION

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 MICROPORT SCIENTIFIC CORPORATION

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches and approvals

- 15.1.11 FUKUDA DENSHI

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 OSI SYSTEMS, INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Expansions

- 15.1.13 IRHYTHM INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches and approvals

- 15.1.13.3.2 Deals

- 15.1.14 LEPU MEDICAL TECHNOLOGY (BEIJING) CO., LTD.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches

- 15.1.15 ALIVECOR, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches and approvals

- 15.1.15.3.2 Deals

- 15.1.1 GE HEALTHCARE

- 15.2 OTHER PLAYERS

- 15.2.1 SCHILLER

- 15.2.2 CARDIAC INSIGHT, INC.

- 15.2.3 BIOTRONIK

- 15.2.4 BITTIUM

- 15.2.5 BPL MEDICAL TECHNOLOGIES

- 15.2.6 LIFESIGNALS

- 15.2.7 CUMEDICAL

- 15.2.8 BIOTRICITY

- 15.2.9 EDAN INSTRUMENTS, INC.

- 15.2.10 VITALCONNECT

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Primary sources

- 16.1.2.2 Key objectives of primary research

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primaries

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION OF CARDIAC MONITORING AND RHYTHM MANAGEMENT DEVICES

- 16.2.1 REVENUE SHARE ANALYSIS (BOTTOM-UP APPROACH)

- 16.2.2 MNM REPOSITORY ANALYSIS

- 16.2.3 COMPANY INVESTORS PRESENTATIONS AND PRIMARY INTERVIEWS

- 16.2.4 TOP-DOWN APPROACH

- 16.2.5 BOTTOM-UP APPROACH

- 16.2.6 PRIMARY INTERVIEWS

- 16.2.7 DEMAND-SIDE APPROACH

- 16.3 MARKET GROWTH RATE PROJECTION

- 16.4 DATA TRIANGULATION

- 16.4.1 STUDY ASSUMPTIONS

- 16.4.2 RESEARCH LIMITATIONS

- 16.5 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.3.1 COMPANY INFORMATION

- 17.3.2 GEOGRAPHIC ANALYSIS

- 17.3.3 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 17.3.4 COUNTRY-LEVEL VOLUME ANALYSIS

- 17.3.5 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS