|

시장보고서

상품코드

2003240

환자 참여 솔루션 시장 : 치료법, 기능성, 최종사용자, 미충족 수요, 투자, 시장 점유율, 동향 - 세계 예측(-2030년)Patient Engagement Solutions Market by Therapy, Functionality, End User, Unmet Need, Investment, Market Share, and Trends - Global Forecast to 2030 |

||||||

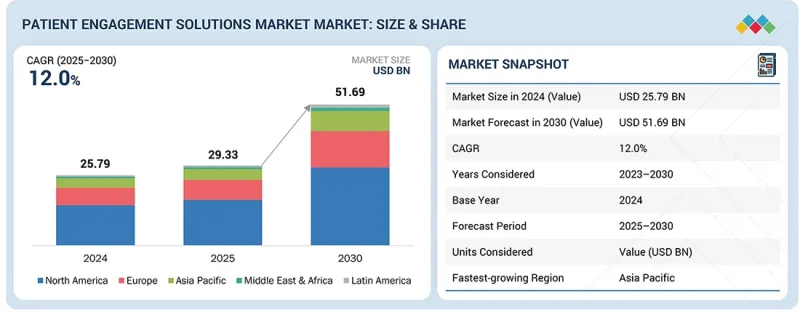

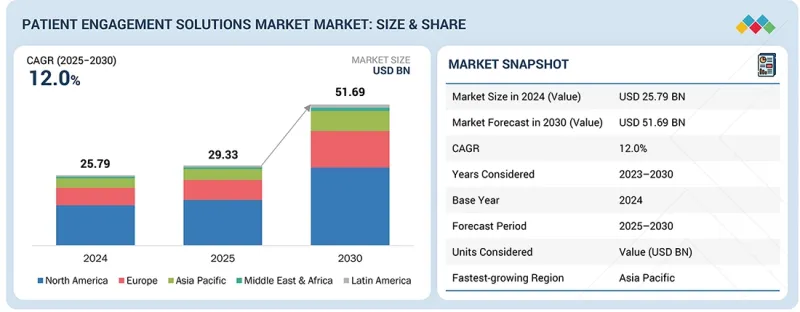

세계의 환자 참여 솔루션 시장 규모는 2025년 293억 3,000만 달러에서 2030년까지 516억 9,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 12.0%의 성장이 전망됩니다.

이는 실시간 커뮤니케이션, 개인화된 대화, 손쉬운 연락을 가능하게 하는 디지털 솔루션의 사용 확대와 같은 요인들을 들 수 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 구성요소, 투여 경로, 치료 분야, 용도, 기능성, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

그 외에도 클라우드 솔루션, 모바일 솔루션, 애널리틱스 등의 발전이 포함될 수 있습니다. 의료 인프라에 대한 대규모 투자 요구와 의료 부문의 숙련된 IT 전문가 부족이 이 시장의 성장을 저해할 것으로 예상됩니다.

"서비스 부문이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

구성요소별로 환자 참여 솔루션 시장은 소프트웨어, 하드웨어, 서비스로 구분됩니다. 의료 기관이 도입, 맞춤화, EHR 통합, 변경 관리, 교육, 참여 기술의 지속적인 최적화에 대한 지원을 점점 더 많이 요구함에 따라 서비스 부문이 가장 높은 성장률을 보일 것으로 예상됩니다. 이러한 전문 서비스 및 매니지드 서비스는 의료 서비스 제공자와 보험사가 참여 플랫폼의 가치를 극대화하고, 진화하는 임상 워크플로우에 적응하며, 복잡한 의료 환경 전반에 걸쳐 원활한 배포를 보장할 수 있도록 돕습니다.

"온프레미스 부문이 2024년 환자 참여 솔루션 시장을 장악할 것으로 예상됩니다."

제공 방식에 따라 환자 참여 솔루션 시장은 온프레미스와 클라우드/웹 기반으로 구분됩니다. 2024년에는 많은 의료기관, 특히 대형 병원과 의료 시스템이 민감한 환자 데이터와 핵심 임상 시스템을 직접 관리하는 것을 선호하기 때문에 온프레미스 부문이 시장을 장악할 것으로 예상됩니다. 또한, 온프레미스 구축은 이미 구축된 IT 인프라, 기존 EHR 환경, 엄격한 보안 컴플라이언스 요건과 일치하기 때문에 데이터 거버넌스 및 내부 통합을 우선시하는 조직에 적합한 선택이 되고 있습니다.

"용도별로는 헬스케어 부문이 전 세계 환자 참여 솔루션 시장에서 가장 큰 점유율을 차지했습니다."

용도별로 환자 참여 솔루션 시장은 건강 관리, 재택 건강 관리, 사회 및 행동 관리, 재무 건전성 관리로 분류됩니다. 2024년, 헬스케어 애플리케이션 부문이 세계 환자 참여 솔루션 시장에서 가장 큰 점유율을 차지했습니다. 이 부문에는 종합적인 치료 조정, 만성질환 관리, 지속적인 환자 소통을 위해 참여 도구에 크게 의존하는 지역 주민의 건강 증진을 위한 노력이 포함됩니다. 이러한 솔루션은 의료 제공자와 보험사가 환자의 치료 결과를 모니터링하고, 치료의 격차를 해소하고, 예방 의료를 지원하는 데 도움을 주며, 헬스케어 분야가 참여형 플랫폼의 채택을 촉진하는 주요 용도입니다.

"의료 제공자 부문이 2024년 최종사용자별 세계 환자 참여 솔루션 시장에서 가장 큰 점유율을 차지했습니다."

최종사용자별로 환자 참여 솔루션 시장은 의료 제공자, 보험사, 환자, 기타 최종사용자로 분류됩니다. 의료 제공자는 다시 병원 및 의료 시스템, 외래진료센터, 재택의료, 기타 의료 제공자로 구분됩니다. 또한, 보험자는 민간과 공공으로 나뉩니다. 최종사용자별로는 의료 제공자 부문이 2024년 세계 환자 참여 솔루션 시장에서 가장 큰 점유율을 차지했습니다. 이 부문의 점유율이 높은 이유는 치솟는 의료비를 억제하고, 가치 기반 의료를 제공하며, 재무적 성과를 확대하기 위한 환자 참여 솔루션의 도입이 증가하고 있기 때문입니다. 이러한 것들이 이 부문의 성장 촉진요인으로 작용하고 있습니다.

세계의 환자 참여 솔루션 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 채용에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 환자 참여 솔루션 시장 : 구성요소별

제10장 환자 참여 솔루션 시장 : 딜리버리 방식별

제11장 환자 참여 솔루션 시장 : 용도별

제12장 환자 참여 솔루션 시장 : 치료 분야별

제13장 환자 참여 솔루션 시장 : 기능성별

제14장 환자 참여 솔루션 시장 : 최종사용자별

제15장 환자 참여 솔루션 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.04.27The patient engagement solutions market is projected to reach USD 51.69 billion by 2030 from USD 29.33 billion in 2025, at a CAGR of 12.0% during the forecast period. Factors such as the rising use of digital solutions that allow real-time communication, personalized interaction, and easy interfacing.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Component, Delivery Mode, Therapeutic Area, Application, Functionality, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East & Africa |

Others may include advancements such as cloud solutions, mobile solutions, and analytics. High investment requirements for healthcare infrastructure and a lack of skilled IT professionals in the healthcare sector are anticipated to impede the growth of this market .

"Services segment is expected to grow at the highest rate during the forecast period."

By components, the patient engagement solutions market is divided into software, hardware, and services. The services segment is expected to grow at the fastest rate as healthcare organizations increasingly seek support for implementation, customization, integration with EHRs, change management, training, and ongoing optimization of engagement technologies. These professional and managed services help providers and payers maximize the value of engagement platforms, adapt to evolving clinical workflows, and ensure seamless deployment across complex healthcare environments .

"The on-premise segment is anticipated to dominate the Patient Engagement Solutions market in 2024"

By delivery modes, the patient engagement solutions market is categorized into on-premise and cloud-based/web-based modes. In 2024, the on-premise segment is expected to dominate because many healthcare organizations, especially large hospitals and health systems, prefer to maintain direct control over sensitive patient data and core clinical systems. On-premise deployments also align with established IT infrastructures, existing EHR environments, and stringent security and compliance requirements, making them a dominant choice for organizations prioritizing data governance and internal integration .

"Health management segment accounted for the largest share of the global patient engagement solutions market, by applications"

By application, the patient engagement solutions market is divided into health management, home health management, social and behavioral management, and financial health management. In 2024, the health management applications segment accounts held the largest share of the global patient engagement solutions market. It encompasses comprehensive care coordination, chronic disease management, and population health initiatives that rely heavily on engagement tools to maintain continuous patient communication. These solutions help providers and payers monitor patient outcomes, close care gaps, and support preventive care, making health management the dominant application driving adoption of engagement platforms .

"Providers' segment accounted for the largest share of the global patient engagement solutions market, by end user in 2024."

By end users, the patient engagement solutions market is divided into providers, payers, patients, and other end users. The providers are further bifurcated into hospitals and healthcare system, ambulatory care centers, home healthcare, and other providers. Moreover the payers is further divided into private and public. By end users, the providers' segment accounted for the largest share of the global patient engagement solutions market in 2024. The large share of this segment is due to increasing implementation of patient engagement solutions to curtail mounting healthcare costs, offer value-based care, and expand financial outcomes are factors that are driving the growth of this segment.

"North America to dominate the patient engagement solutions market

In 2024, North America dominated the global patient engagement solutions market by region. Factors such as favorable government initiatives and regulations, the imperative to reduce healthcare costs, the increasing prevalence of chronic diseases, and the presence of key market players contribute significantly to the growth of the patient engagement solutions market in North America. Strong regulatory frameworks promoting patient access, data interoperability, and value-based care, along with the presence of leading healthcare IT vendors and high healthcare spending, continue to drive market leadership in the region .

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (45%), Tier 2 (30%), and Tier 3 (25%)

- By Designation: C-level (44%), Director-level (35%), and Others (21%)

- By Region: North America (46%), Europe (26%), Asia Pacific (18%), Latin America (7%), and Middle East & Africa (10%)

McKesson Corporation (US), Veradigm LLC (US), Oracle (US), athenahealth (US), Health Catalyst (US), GetWellNetwork, Inc. (US), Lincata, Inc. (US), Cognizant (US), TruBridge (US), Oneview Healthcare (Ireland), AdvancedMD, Inc. (US), Epic Systems Corporation (US), Harris Healthcare (US), Medical Information Technology, Inc. (US), Tebra Technologies, Inc. (US), Televox (US), Medhost (US), Nuance Communications, Inc. (US) (Microsoft), Solutionreach, Inc. (US), Experian Information Solutions, Inc. (US). These players are increasingly focusing on new product launches and partnerships to expand their product offerings in the patient engagement solutions market.

Research Coverage

- The report studies the Patient Engagement Solutions market based on component, delivery mode, therapeutic area, application, functionality, end user, and region.

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micro-markets with respect to their growth trends, prospects, and contributions to the total patient engagement solutions market.

- The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

- This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their positions in the market.

- Analysis of key drivers (implementation of government regulations and initiatives to promote patient centric care, increasing adoption of patient engagement solutions, rising number of collaborations and partnerships between stakeholders, increasing utilisation of mobile health apps, rising geriatric population and subsequent increase in prevalence of chronic diseases), restraints (large investment requirement for healthcare infrastructure, protection of patient information, inadequate interoperability across healthcare providers and shortage of skilled IT professionals in the healthcare industry ), opportunities (growth opportunities in emerging markets, wearable health technology, cloud computing solutions), and challenges (high deployment cost of healthcare IT systems, low levels of healthcare literacy) impacting the growth of the patient engagement solutions market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the patient engagement solutions market.

- Market Development: Comprehensive information on the lucrative emerging markets, component, delivery mode, therapeutic area, application, functionality, end user, and region

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the patient engagement solutions market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, company evaluation quadrant, and capabilities of leading players in the global patient engagement market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PATIENT ENGAGEMENT SOLUTIONS MARKET OVERVIEW

- 3.2 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE AND REGION

- 3.3 PATIENT ENGAGEMENT SOLUTIONS MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of telehealth and remote care

- 4.2.1.2 Increasing smartphone use and digital comfort

- 4.2.1.3 Implementation of government regulations and initiatives to promote patient-centric care

- 4.2.1.4 Growing prevalence of chronic diseases and rising demand for long-term patient involvement

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data privacy and cybersecurity concerns

- 4.2.2.2 Inadequate interoperability across healthcare providers

- 4.2.2.3 Shortage of skilled IT professionals in healthcare industry

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of remote and home-based care models

- 4.2.3.2 AI-driven personalization in patient engagement solutions

- 4.2.3.3 Integration with wearables and personalized health tech

- 4.2.4 CHALLENGES

- 4.2.4.1 Low patient adoption and engagement over time

- 4.2.4.2 Fragmented data and siloed digital tools

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 ROLE IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY COMPONENT, 2025

- 5.5.2 INDICATIVE PRICE FOR PATIENT ENGAGEMENT SOLUTIONS, BY REGION, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO FOR HS CODE 8528, 2021-2024

- 5.6.2 IMPORT SCENARIO FOR HS CODE 8471, 2021-2024

- 5.6.3 EXPORT SCENARIO FOR HS CODE 8528, 2021-2024

- 5.6.4 EXPORT SCENARIO FOR HS CODE 8471, 2021-2024

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ACHIEVING USD 15 MILLION IN SAVINGS BY REDUCING READMISSIONS WITH POST-DISCHARGE FOLLOW-UP

- 5.10.2 BUILD TRUST THROUGH PATIENT ENGAGEMENT TECHNOLOGY: CHILDREN'S HOSPITAL CASE STUDY

- 5.10.3 IMPROVING PATIENT ENGAGEMENT AT SPARTA COMMUNITY HOSPITAL WITH TRUBRIDGE PATIENT CONNECT

- 5.11 IMPACT OF 2025 US TARIFF ON PATIENT ENGAGEMENT SOLUTIONS MARKET

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRY/REGION

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE INDUSTRIES

- 5.11.4.1 Hospitals and healthcare systems

- 5.11.4.2 ASCs, ACCs, and other outpatient settings

- 5.11.4.3 Home healthcare providers

- 5.11.4.4 Private payers

- 5.11.4.5 Public payers

- 5.11.4.6 Other end users

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 CLOUD COMPUTING

- 6.1.2 API & EHR INTEGRATION TECHNOLOGIES

- 6.1.3 DATA ANALYTICS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE (AI) AND MACHINE LEARNING (ML)

- 6.2.2 CONVERSATIONAL AI/CHATBOTS

- 6.2.3 BEHAVIORAL ANALYTICS AND PERSONALIZATION ENGINES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CYBERSECURITY AND DATA ENCRYPTION

- 6.3.2 BLOCKCHAIN

- 6.3.3 BIG DATA AND ADVANCED ANALYTICS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR PATIENT ENGAGEMENT SOLUTION

- 6.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5.3 LIST OF PATENTS/PATENT APPLICATIONS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE ENGAGEMENT

- 6.6.2 CONTINUOUS REMOTE CARE AND HOSPITAL-AT-HOME ENABLEMENT

- 6.6.3 PERSONALIZED DIGITAL THERAPEUTICS AND BEHAVIORAL COACHING

- 6.6.4 CLOSED-LOOP CARE COORDINATION AND VALUE-BASED PERFORMANCE OPTIMIZATION

- 6.6.5 DECENTRALIZED CLINICAL TRIALS AND REAL-WORLD EVIDENCE GENERATION

- 6.7 IMPACT OF AI/GEN AI ON PATIENT ENGAGEMENT SOLUTIONS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 AI-driven conversational AI for pre/post-op engagement

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Patient communication & virtual care platforms

- 6.7.4.2 Remote patient monitoring & digital therapeutics

- 6.7.4.3 Population health & health equity programs

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Hospitals & clinics

- 6.7.5.1.2 User B: Healthcare providers, employers, and forensic agencies

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Clinical, reference, and toxicology laboratories

- 6.7.5.2.2 User B: Healthcare providers, employers, and forensic agencies

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS/END-USER EXPECTATIONS

- 8.5.1 UNMET NEEDS

- 8.5.2 END-USER EXPECTATIONS

- 8.6 MARKET PROFITIBILITY

9 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 IN-ROOM TELEVISIONS

- 9.2.1.1 Rising patient demand for real-time health transparency and smart room modernization initiatives to drive market

- 9.2.2 INTEGRATED BEDSIDE TERMINALS/ASSISTED DEVICES

- 9.2.2.1 Hospitals to increasingly adopt bedside terminals to address workforce shortages and reduce nursing workload

- 9.2.3 TABLETS

- 9.2.3.1 Strong ROI profile, lower upfront investment, and rapid rollout capability to propel market growth

- 9.2.1 IN-ROOM TELEVISIONS

- 9.3 SOFTWARE

- 9.3.1 PRE-CARE ENGAGEMENT

- 9.3.1.1 Increasing adoption of consumer-centric access models to aid segment growth

- 9.3.2 POINT-OF-CARE ENGAGEMENT

- 9.3.2.1 Exponential growth in healthcare data and rising information complexity to augment segment growth

- 9.3.3 POST-CARE ENGAGEMENT

- 9.3.3.1 Shift toward value-based care and reimbursement models for readmission rates to drive segment growth

- 9.3.1 PRE-CARE ENGAGEMENT

- 9.4 SERVICES

- 9.4.1 IMPLEMENTATION & INTEGRATION SERVICES

- 9.4.1.1 Need for expertise to operationalize sophisticated patient engagement ecosystems to fuel market growth

- 9.4.2 TRAINING & EDUCATION SERVICES

- 9.4.2.1 Need to eradicate measurable staff usability challenges and patient digital access gaps to drive segment

- 9.4.3 SUPPORT & MAINTENANCE SERVICES

- 9.4.3.1 Dependency on patient portals, telehealth systems, and integrated EHR infrastructures to aid market growth

- 9.4.4 CONSULTING SERVICES

- 9.4.4.1 Shift from volume-based to value-based care models to drive consulting services market

- 9.4.1 IMPLEMENTATION & INTEGRATION SERVICES

10 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY DELIVERY MODE

- 10.1 INTRODUCTION

- 10.2 ON-PREMISES

- 10.2.1 ON-PREMISES ADOPTION TO ACCELERATE AMID SECURITY, REGULATORY, AND INTEGRATION PRIORITIES

- 10.3 CLOUD-BASED

- 10.3.1 CLOUD-BASED PATIENT ENGAGEMENT TO PROPEL SCALABLE, SECURE, AND INTEROPERABLE CARE

11 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CLINICAL CARE

- 11.2.1 VALUE-BASED CARE MODELS AND TELEHEALTH EXPANSION TO PROPEL CLINICAL CARE SEGMENT

- 11.3 CARE COORDINATION & COMMUNICATION

- 11.3.1 FRAGMENTED CARE PATHWAYS AND INTEROPERABILITY MANDATES TO ACCELERATE MARKET GROWTH

- 11.4 HOME & REMOTE CARE

- 11.4.1 HOSPITAL-AT-HOME EXPANSION, READMISSION PENALTIES, AND RPM REIMBURSEMENT TO FUEL SEGMENT GROWTH

- 11.5 POPULATION HEALTH & BEHAVIORAL ENGAGEMENT

- 11.5.1 VALUE-BASED CARE MANDATES, RISK STRATIFICATION, AND BEHAVIORAL HEALTH INTEGRATION TO PROPEL SEGMENT GROWTH

- 11.6 FINANCIAL ENGAGEMENT

- 11.6.1 RISING OUT-OF-POCKET COSTS, CONSUMERISM, AND REVENUE PRESSURE TO DRIVE FINANCIAL ENGAGEMENT ADOPTION

- 11.7 OTHER APPLICATIONS

12 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY THERAPEUTIC AREA

- 12.1 INTRODUCTION

- 12.2 CHRONIC DISEASES

- 12.2.1 CARDIOVASCULAR DISEASES

- 12.2.1.1 Need for continuous monitoring and preventive engagement through digital health platforms to drive market

- 12.2.2 DIABETES

- 12.2.2.1 Continuous glucose monitoring, behavioral adherence, and data-driven self-management through digital engagement to drive market

- 12.2.3 OBESITY

- 12.2.3.1 Preventive engagement, behavioral modification, and long-term risk reduction through digital health platforms to drive market

- 12.2.4 RESPIRATORY DISORDERS

- 12.2.4.1 Advancing continuous symptom monitoring and preventive care through digital engagement platforms to fuel market growth

- 12.2.5 ONCOLOGY

- 12.2.5.1 Longitudinal care coordination, symptom monitoring, and survivorship engagement to boost market

- 12.2.6 OTHER CHRONIC DISEASES

- 12.2.1 CARDIOVASCULAR DISEASES

- 12.3 WOMEN'S HEALTH

- 12.3.1 PREVENTIVE SCREENING, REPRODUCTIVE CARE COORDINATION, AND LIFECYCLE ENGAGEMENT TO AID MARKET GROWTH

- 12.4 BEHAVIORAL & MENTAL HEALTH

- 12.4.1 INCREASING GLOBAL PREVALENCE OF DEPRESSION, ANXIETY, SUBSTANCE USE DISORDERS TO AID MARKET GROWTH

- 12.5 OTHER THERAPEUTIC AREAS

13 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY FUNCTIONALITY

- 13.1 INTRODUCTION

- 13.2 PATIENT/CLIENT SCHEDULING

- 13.2.1 DIGITAL-FIRST, MOBILE-DRIVEN SCHEDULING TO REDUCE NO-SHOWS AND STRENGTHEN ACCESS PERFORMANCE

- 13.3 TELEHEALTH

- 13.3.1 TELEHEALTH TO DRIVE QUALITY IMPROVEMENT AND HYBRID CARE DELIVERY GROWTH

- 13.4 E-PRESCRIBING

- 13.4.1 E-PRESCRIBING TO STRENGTHEN MEDICATION SAFETY REGULATORY COMPLIANCE

- 13.5 DOCUMENT MANAGEMENT

- 13.5.1 DIGITAL RECORD ACCESS TO DRIVE DOCUMENT MANAGEMENT IN CORE PATIENT ENGAGEMENT INFRASTRUCTURE

- 13.6 BILLING & PAYMENTS

- 13.6.1 RISING PATIENT FINANCIAL RESPONSIBILITY AND GROWING DEMAND FOR DIGITAL TRANSPARENCY TO DRIVE MARKET

- 13.7 PATIENT EDUCATION

- 13.7.1 SELF-DIRECTED HEALTH RESEARCH AND DIGITAL LITERACY GAPS TO RISE DEMAND FOR INTEGRATED PATIENT EDUCATION TOOLS

- 13.8 OTHER FUNCTIONALITIES

14 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 PROVIDERS

- 14.2.1 HOSPITALS & HEALTHCARE SYSTEMS

- 14.2.1.1 Healthcare systems to drive patient experience and operational efficiency through integrated patient engagement solutions

- 14.2.2 ASCS, ACCS, AND OTHER OUTPATIENT SETTINGS

- 14.2.2.1 Need for optimizing patient access and engagement in outpatient care settings to propel segment growth

- 14.2.3 HOME HEALTHCARE PROVIDERS

- 14.2.3.1 Home healthcare provides to enhance patient engagement and remote care delivery in home settings

- 14.2.4 OTHER PROVIDERS

- 14.2.1 HOSPITALS & HEALTHCARE SYSTEMS

- 14.3 PAYERS

- 14.3.1 PRIVATE PAYERS

- 14.3.1.1 Private payers to enhance member experience and cost efficiency through digital-first engagement strategies

- 14.3.2 PUBLIC PAYERS

- 14.3.2.1 Public payers to strengthen population health management through inclusive and scalable digital engagement

- 14.3.1 PRIVATE PAYERS

- 14.4 OTHER END USERS

15 PATIENT ENGAGEMENT SOLUTIONS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Value-based care reforms and long-term care management need to accelerate market growth

- 15.2.3 CANADA

- 15.2.3.1 Government policies to strengthen digital health infrastructure and interoperability

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 GERMANY

- 15.3.2.1 Nationwide ePA rollout and digital therapeutics leadership to propel market growth

- 15.3.3 FRANCE

- 15.3.3.1 Near-universal digital health record adoption and strategic investment to aid market growth

- 15.3.4 UK

- 15.3.4.1 NHS app scale-up and virtual care expansion to boost market growth

- 15.3.5 ITALY

- 15.3.5.1 Rising digital health investment and growing focus on national telemedicine infrastructure to fuel market growth

- 15.3.6 SPAIN

- 15.3.6.1 Rising telemedicine expansion and growing mHealth adoption to strengthen market

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 CHINA

- 15.4.2.1 High digital health adoption and internet hospital expansion to accelerate market growth

- 15.4.3 JAPAN

- 15.4.3.1 Healthcare digitalization to accelerate patient engagement in Japan

- 15.4.4 INDIA

- 15.4.4.1 Digital public health infrastructure and mobile penetration to augment market growth

- 15.4.5 SOUTH KOREA

- 15.4.5.1 National digital integration and rapid population aging to aid market growth

- 15.4.6 AUSTRALIA

- 15.4.6.1 Near-universal digital records and embedded telehealth adoption to fuel market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 15.5.2 BRAZIL

- 15.5.2.1 Government-led telehealth scale and institutionalized patient participation to propel digital engagement

- 15.5.3 MEXICO

- 15.5.3.1 Structural health system gaps to spur digital patient engagement adoption

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 High NCD burden and government-owned digital platforms to augment patient engagement

- 15.6.2.2 Kingdom of Saudi Arabia

- 15.6.2.2.1 Government-led digital health innovations to accelerate patient engagement

- 15.6.2.3 UAE

- 15.6.2.3.1 Progressive digital health innovations to strengthen UAE patient engagement solutions market

- 15.6.2.4 Rest of GCC countries

- 15.6.3 SOUTH AFRICA

- 15.6.3.1 Massive telemedicine adoption and innovative digital platforms to aid market growth

- 15.6.4 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.2.1 OVERVIEW OF KEY STRATEGIES ADOPTED BY KEY PLAYERS IN PATIENT ENGAGEMENT SOLUTIONS MARKET

- 16.3 REVENUE ANALYSIS, 2020-2024

- 16.4 MARKET SHARE ANALYSIS, 2024

- 16.5 BRAND COMPARISON

- 16.6 COMPANY VALUATION & FINANCIAL METRICS

- 16.6.1 FINANCIAL METRICS

- 16.6.2 COMPANY VALUATION

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Component footprint

- 16.7.5.4 Application footprint

- 16.7.5.5 End-user footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 MCKESSON CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 ORACLE

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 MICROSOFT (NUANCE COMMUNICATIONS, INC.)

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 TRUBRIDGE

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 HEALTH CATALYST

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses & competitive threats

- 17.1.6 VERADIGM LLC

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 ATHENAHEALTH

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches and enhancements

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Other developments

- 17.1.8 GETWELLNETWORK, INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product enhancements

- 17.1.8.3.2 Deals

- 17.1.9 LINCATA, INC.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 COGNIZANT

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.11 ONEVIEW HEALTHCARE

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches and enhancements

- 17.1.11.3.2 Deals

- 17.1.11.3.3 Other developments

- 17.1.12 ADVANCEDMD, INC.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product enhancements

- 17.1.12.3.2 Deals

- 17.1.13 EPIC SYSTEMS CORPORATION

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product enhancement

- 17.1.13.3.2 Deals

- 17.1.14 HARRIS HEALTHCARE

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.15 MEDICAL INFORMATION TECHNOLOGY, INC.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Deals

- 17.1.15.3.2 Other developments

- 17.1.16 TEBRA TECHNOLOGIES, INC.

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product enhancements

- 17.1.16.3.2 Deals

- 17.1.17 TELEVOX

- 17.1.17.1 Business overview

- 17.1.17.2 Products offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Product launches

- 17.1.17.3.2 Deals

- 17.1.18 SOLUTIONREACH, INC.

- 17.1.18.1 Business overview

- 17.1.18.2 Products offered

- 17.1.18.3 Recent developments

- 17.1.18.3.1 Product launches and enhancements

- 17.1.19 EXPERIAN INFORMATION SOLUTIONS, INC.

- 17.1.19.1 Business overview

- 17.1.19.2 Products offered

- 17.1.20 ECLINICALWORKS

- 17.1.20.1 Business overview

- 17.1.20.2 Products offered

- 17.1.1 MCKESSON CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 WELLSTACK

- 17.2.2 RELATIENT

- 17.2.3 LUMA HEALTH INC.

- 17.2.4 CIPHERHEALTH INC.

- 17.2.5 YOSI HEALTH

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH APPROACH

- 18.1.1 SECONDARY RESEARCH

- 18.1.1.1 Key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY RESEARCH

- 18.1.2.1 Primary sources

- 18.1.2.2 Key objectives of primary research

- 18.1.2.3 Key data from primary sources

- 18.1.2.4 Breakdown of primaries

- 18.1.2.5 Insights from primary experts

- 18.1.1 SECONDARY RESEARCH

- 18.2 RESEARCH METHODOLOGY DESIGN

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 BOTTOM-UP APPROACH (REVENUE SHARE ANALYSIS)

- 18.3.2 TOP-DOWN OF PARENT MARKET ASSESSMENT

- 18.3.3 PRIMARY INTERVIEWS

- 18.3.4 TOP-DOWN APPROACH

- 18.4 DATA TRIANGULATION

- 18.5 MARKET SHARE ESTIMATION

- 18.6 STUDY ASSUMPTIONS

- 18.7 RESEARCH LIMITATIONS

- 18.8 RISK ANALYSIS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS