|

시장보고서

상품코드

2003243

산업용 차량 시장 예측(-2035년) : 유형별, 모터 유형별, 차종 및 용량별, 용도별, 자율 레벨별, 추진 방식별, 지역별Industrial Vehicles Market by Vehicle Type (Forklift, Aisle Truck, Tow Tractor, Container Handler), Propulsion (ICE, Battery-operated, Gas-powered), Application, Capacity, Level of Autonomy, Motor Type, and Region - Global Forecast to 2035 |

||||||

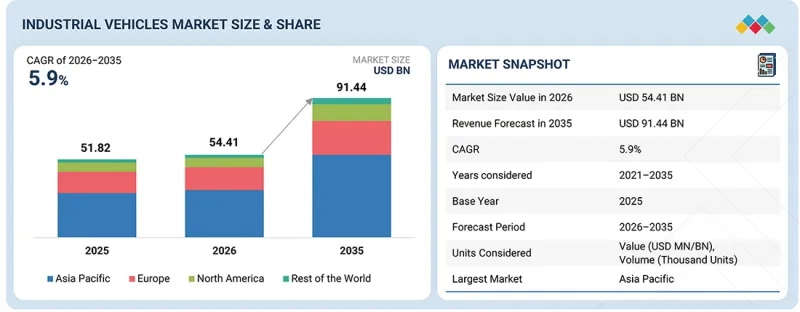

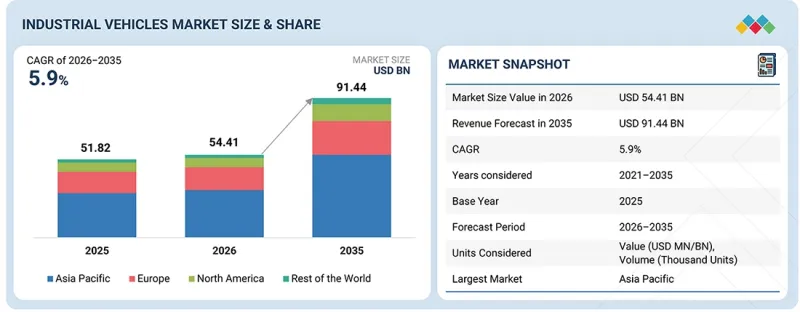

산업용 차량 시장 규모는 2026년 544억 1,000만 달러에서 2035년까지 914억 4,000만 달러로, CAGR 5.9%로 확대할 것으로 예측됩니다.

공급망 업무의 복잡화와 자동화 기술 도입으로 전 세계에서 시장이 확대되고 있습니다. 이러한 변화에 따라 효율성을 높이기 위해 AGV(무인운반차), 자율주행 지게차 등 첨단 산업용 차량이 요구되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2035년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 수량(1,000대) 및 금액(100만/10억 달러) |

| 부문 | 차종·적재량, 구동 방식, 용도, 자율주행 레벨, 고소작업차 시장(유형별) |

| 대상 지역 | 아시아태평양, 유럽, 북미 및 세계의 기타 지역 |

또한 IoT 및 AI를 활용한 분석과 같은 혁신적인 창고 관리 기술을 통합하여 실시간 재고 추적 및 최적화된 경로 계획이 가능해짐에 따라 시장의 성장이 더욱 가속화되고 있습니다. 동시에 많은 지역의 인력 부족과 인건비 상승으로 인해 수작업에 대한 의존도를 줄이기 위해 자동화 및 반자동화 설비로의 전환이 가속화되고 있습니다. 또한 배터리 기술(특히 리튬이온), 센서 시스템, 커넥티비티, 차량 관리 소프트웨어의 개선과 같은 기술적 진보로 인해 보다 안전하고 신뢰할 수 있으며 에너지 효율이 높은 산업용 차량을 구현할 수 있게 되었습니다.

ICE(내연기관) 방식의 산업용 차량은 그 효율성으로 인해 널리 사용되고 있으며, 다양한 산업 분야에서 선호되는 선택이 되고 있습니다. 자주 충전해야 하는 전기자동차와 달리, ICE 차량은 더 오랜 시간 동안 운행할 수 있습니다. 또한 ICE 산업용 차량은 중량물 운반이 가능하여 창고, 공장, 물류센터에서의 적재 효율을 향상시킬 수 있습니다. 높은 출력, 빠른 가속도 및 속도는 운송 및 자재 운반 작업의 효율성을 더욱 높여줍니다. 낮은 초기 비용, 높은 운영 효율성, 쉬운 급유, 그리고 무거운 작업에 대한 대응 능력 등이 내연기관(ICE) 탑재 산업용 차량에 대한 수요를 견인할 것으로 예상됩니다. 또한 아시아태평양, 특히 인도(예: 델리-뭄바이 산업 회랑), 중국(내륙 물류 구역), 동남아시아 지역(베트남, 태국) 및 걸프협력회의(GCC) 국가들에서 대규모 물류 허브 및 산업 회랑의 확장이 진행되고 있으며, 이는 내연기관(ICE) 산업용 차량의 성장을 가속화할 것입니다. 성장을 가속화할 것입니다.

대형 지게차(10-15톤 이상), 컨테이너 핸들러, 터미널 트랙터에서는 장시간의 가혹한 작업 교대시 지속적인 토크를 공급하기 위해 디젤 엔진이나 LPG 엔진이 여전히 선호되고 있습니다. 이 기계들은 가동률, 신속한 급유, 현장 서비스 지원이 전동화보다 더 중요한 항만, 제철소, 열악한 물류 현장에서 가동되고 있습니다. 특히 신흥 시장에서 내연기관(ICE)의 채택을 더욱 촉진하는 것은 이미 구축된 서비스 네트워크와 예측 가능한 재판매 가치입니다. 실내와 야외를 함께 운영하는 경우, 배터리 무게, 충전 물류, 인프라 업그레이드는 여전히 비용과 복잡성을 증가시키고 있습니다.

중국은 정부의 산업 인프라 개발에 대한 인센티브로 인해 예측 기간 중 아시아태평양의 산업용 차량 시장에서 가장 큰 시장이 될 것으로 예상됩니다. 또한 주요 제조업체들은 중국의 성장하고 있는 산업 부문을 활용하기 위해 중국내 제품 포트폴리오를 확장하고 있습니다. 산업단지, 항만, 철도 회랑, 물류 구역에 대한 지속적인 투자가 산업용 장비의 수요를 견인하고 있습니다. 항차그룹(Hangcha Group) 등의 기업은 수소연료전지 지게차(3.5톤급)와 자동운반 시스템용 경량 EzGo AGV를 출시했습니다. 안후이 헬리(HELI)는 창고 및 물류용으로 최대 적재량 3.0톤의 신형 리튬이온 배터리 전동 지게차 모델(H 시리즈 CPD 시리즈)을 출시했습니다. 주요 제조업체의 다양한 전동 지게차 모델과 AGV 공급, 국내 산업용 차량 제조업체의 다양한 제품 라인업, 그리고 산업화의 진전은 중국 전역의 산업용 차량 시장의 성장을 촉진할 것으로 예상됩니다.

산업용 차량 시장에는 Toyota Industries Corporation(일본), KION Group AG(독일), Mitsubishi Logisnext(일본), Jungheinrich AG(독일), Crown Equipment Corporation(미국), Hyster-Yale Materials Handling, Inc. 미국), Hyster-Yale Materials Handling, Inc.(미국) 등의 주요 제조업체가 포함됩니다.

조사 범위:

본 조사는 산업용 차량 시장의 다양한 부문를 대상으로 합니다. 차종 및 적재량, 추진 방식, 용도, 자율성 수준, 고소작업차 유형, 지역 등의 부문별로 시장 규모와 미래 성장 잠재력을 추정하는 것을 목표로 하고 있습니다. 또한 주요 시장 진입 기업에 대한 상세한 경쟁 분석, 기업 개요, 제품 및 사업 제공에 대한 주요 관찰 사항, 최근 동향, 인수 사례 등을 포함하고 있습니다.

이 보고서 구매의 주요 이점:

이 보고서는 산업용 차량 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 또한 산업용 차량 판매 동향의 변동에 대해서도 논의하여 부품 공급업체가 전략을 수립하는 데 도움이 될 수 있도록 했습니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 더 심층 인사이트를 얻고, 자신의 비즈니스를 더 나은 위치에 놓고, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 촉진요인, 제약, 과제 및 기회에 대한 인사이트를 제공하는 데 도움이 될 것입니다. 또한 산업용 차량 공급업체의 시장 점유율과 OEM 분석에 대한 이해에도 도움이 됩니다.

또한 이 보고서는 다음과 같은 인사이트를 제공합니다. :

- 시장 역학: 산업용 차량 시장 성장에 영향을 미치는 주요 촉진요인(창고 자동화 및 고밀도 보관 모델의 영향), 제약 요인(높은 설비 투자 및 총소유비용에 대한 민감성), 기회(서비스형 에너지 및 배터리 생태계 통합), 도전 과제(기술 전환 위험( ICE → 전기 및 디지털 플랫폼))) 분석

- 제품 개발/혁신: 산업용 차량 시장의 미래 기술 동향 및 신규 제품 및 서비스 출시에 대한 심층적인 인사이트 제공

- 시장 동향: 종합적인 시장 정보(이 보고서는 다양한 지역의 산업용 차량 시장을 분석합니다)

- 시장 다각화: 산업용 차량 시장의 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보

- 경쟁 분석: 산업용 차량 시장의 주요 기업 - Toyota Industries Corporation(일본), KION Group AG(독일), Mitsubishi Logisnext(일본), Jungheinrich AG(독일), Crown Equipment Corporation(미국), Hyster-Yale Materials Handling, Inc.(미국) 등의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고소작업대 시장(유형별)

제7장 산업용 차량용 모터 시장(모터 유형별)

제8장 산업용 차량 시장(차종별·적재량별)

제9장 산업용 차량 시장(용도별)

제10장 산업용 차량 시장(자율 레벨별)

제11장 산업용 차량 시장(추진 방식별)

제12장 산업용 차량 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.04.24The industrial vehicles market size is projected to grow from USD 54.41 billion in 2026 to USD 91.44 billion by 2035 at a CAGR of 5.9%. The market is expanding globally due to the growing complexity of supply chain operations and the adoption of automation technologies. This shift necessitates advanced industrial vehicles such as AGVs and autonomous forklifts to enhance efficiency.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Volume (Thousand Units) and Value (USD Million/Billion) |

| Segments | Vehicle Type & Capacity, Drive Type, Application, Level of Autonomy, Aerial Work Platforms Market (By Type) |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

Additionally, integrating innovative warehousing technologies, such as IoT and AI-driven analytics, further accelerates market growth by enabling real-time inventory tracking and optimized route planning. At the same time, labor shortages and rising wage costs in many regions are accelerating the shift toward automation and semi-automated equipment to reduce reliance on manual operations. Also, technological advancements, such as improvements in battery technology (particularly lithium-ion), sensor systems, connectivity, and fleet management software, are enabling safer, more reliable, and more energy-efficient industrial vehicles.

"The internal combustion engine (ICE) industrial vehicles segment is expected to grow substantially during the forecast period."

ICE-operated industrial vehicles are widely used due to their efficiency, making them a preferred choice across different industries. Unlike electric counterparts, which require frequent recharging, ICE vehicles can operate for longer periods. Additionally, ICE industrial vehicles can handle heavy loads and improve loading and unloading efficiency in warehouses, factories, and distribution centers. Their high-power output, swift acceleration, and speed further enhance their effectiveness in transporting and material-handling operations. Factors such as lower initial costs, high operational efficiency, ease of refueling, and ability to handle heavy-duty tasks are likely to drive the demand for ICE industrial vehicles. Further, the expansion of large logistics hubs and industrial corridors is growing in the Asia Pacific, especially in countries such as India (e.g., Delhi-Mumbai Industrial Corridor), China (inland logistics zones), Southeast Asia region (Vietnam, Thailand), and Gulf Cooperation Council countries, which will accelerate growth for ICE industrial vehicles.

In heavy-duty forklifts (10-15+ tons), container handlers, and terminal tractors, diesel and LPG engines remain preferred for delivering sustained torque during long, demanding shifts. These machines work in ports, steel yards, and rugged logistics sites where uptime, quick refueling, and field service support matter more than electrification. Established service networks and predictable resale values further support ICE adoption, especially in emerging markets. In mixed indoor-outdoor operations, battery weight, charging logistics, and infrastructure upgrades still add cost and complexity.

"China is expected to register considerable growth in the Asia Pacific industrial vehicles market."

China is expected to be the largest market in the Asia Pacific industrial vehicles market during the forecast period due to government incentives for industrial infrastructure development. Additionally, major manufacturers are expanding their product portfolios in China to capitalize on the country's growing industrial sector. Ongoing investments in industrial parks, ports, rail corridors, and logistics zones are driving demand for industrial equipment. Companies such as Hangcha Group Co., Ltd. released hydrogen fuel-cell forklifts (3.5-ton class) and lightweight EzGo AGVs for automated material handling. Anhui Heli (HELI) has launched new lithium-battery electric forklift models (H-Series CPD range) with a capacity of up to 3.0 tons, introduced for warehouse and logistics use. The availability of a diverse range of electric forklift models & AGVs from leading manufacturers, wide product offerings from domestic industrial vehicle manufacturers, and rising industrialization are expected to fuel the growth of the industrial vehicles market across China.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in the industrial vehicles market. The breakup of the primary interviews is as follows:

- By Company Type: OEMs - 80%, Tier 1 -10% and Others - 10%,

- By Designation: CXOs - 65%, Managers - 25%, and Executives - 10%

- By Region: North America - 36%, Europe - 32%, Asia Pacific - 28%, and Rest of the World - 4%

The industrial vehicles market comprises major manufacturers such as Toyota Industries Corporation (Japan), KION Group AG (Germany), Mitsubishi Logisnext Co., Ltd. (Japan), Jungheinrich AG (Germany), Crown Equipment Corporation (US), and Hyster-Yale Materials Handling, Inc. (US).

Research Coverage:

The study covers the industrial vehicles market across various segments. It aims to estimate the market size and future growth potential across segments such as vehicle type & capacity, propulsion, application, level of autonomy, aerial work platform type, and region. The study also includes an in-depth competitive analysis of key market players, their company profiles, key observations related to product and business offerings, recent developments, and acquisitions.

Key Benefits of Buying the Report:

The report will help market leaders/new entrants with information on the closest approximations of revenue for the industrial vehicles market and its sub-segments. The report also discusses the ups and downs in industrial vehicle sales, helping component suppliers plan their strategies. This report will help stakeholders understand the competitive landscape and gain deeper insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides insights into key drivers, restraints, challenges, and opportunities. The report also helps in understanding the industrial vehicle supplier market share and OEM analysis.

The report further provides insights into the following points:

- Market Dynamics: Analysis of key drivers (impact of warehouse automation and high-density storage models), restraints (high capex & total cost of ownership sensitivity), opportunities (energy as-a-service & battery ecosystem integration), and challenges (technology transition risk (ICE-> electric & digital platforms)) influencing the growth of the industrial vehicles market

- Product Development/Innovation: Detailed insights into upcoming technologies and product & service launches in the industrial vehicles market

- Market Development: Comprehensive market information (the report analyzes the industrial vehicles market across varied regions)

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the industrial vehicles market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Toyota Industries Corporation (Japan), KION Group AG (Germany), Mitsubishi Logisnext Co., Ltd. (Japan), Jungheinrich AG (Germany), Crown Equipment Corporation (US), and Hyster-Yale Materials Handling, Inc. (US), in the industrial vehicle market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS FOR INDUSTRIAL VEHICLES MARKET

- 2.4 HIGH-GROWTH SEGMENTS IN INDUSTRIAL VEHICLES MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL VEHICLES MARKET

- 3.2 INDUSTRIAL VEHICLES MARKET, BY REGION

- 3.3 INDUSTRIAL VEHICLES MARKET, BY VEHICLE TYPE

- 3.4 INDUSTRIAL VEHICLES MARKET, BY MOTOR TYPE

- 3.5 INDUSTRIAL VEHICLES MARKET, BY APPLICATION

- 3.6 INDUSTRIAL VEHICLES MARKET, BY PROPULSION

- 3.7 AERIAL WORK PLATFORM MARKET, BY TYPE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Need for warehouse automation and high-density storage models

- 4.2.1.2 Focus on electrification and indoor emission compliance

- 4.2.1.3 Port and intermodal terminal modernization

- 4.2.2 RESTRAINTS

- 4.2.2.1 High Capex and Total Cost of Ownership (TCO) sensitivity

- 4.2.2.2 Infrastructure and facility constraints

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of energy-as-a-service model and battery ecosystem

- 4.2.3.2 Fleet digitalization and shift toward 'productivity-as-a-service'

- 4.2.4 CHALLENGES

- 4.2.4.1 Technology transition risk from ICE to electric and digital platforms

- 4.2.4.2 Margin compression from commoditization and rental shift

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL INDUSTRIAL VEHICLE INDUSTRY

- 5.1.3.1 Powertrain transition and market dynamics

- 5.1.3.2 Growth in off-highway and industrial equipment

- 5.1.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.1.4.1 Regional GDP dynamics

- 5.1.4.1.1 Developed markets (Asia Pacific, Europe, North America, and RoW)

- 5.1.4.1.2 Emerging markets

- 5.1.4.2 Investment environment

- 5.1.4.1 Regional GDP dynamics

- 5.2 ECOSYSTEM ANALYSIS

- 5.3 PRICING ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE

- 5.3.2 AVERAGE SELLING PRICE, BY REGION

- 5.4 TOTAL COST OF OWNERSHIP (TCO)

- 5.4.1 COMPARISON BETWEEN TCO OF ELECTRIC AND ICE FORKLIFTS

- 5.5 BILL OF MATERIALS (BOM) ANALYSIS

- 5.6 OEM ANALYSIS: FORKLIFTS

- 5.6.1 FORKLIFT BATTERY CAPACITY AND LIFTING CAPACITY

- 5.6.2 LIFTING CAPACITY AND BATTERY VOLTAGE

- 5.6.3 BATTERY VOLTAGE AND MARKET SIZE OF FORKLIFTS

- 5.7 VALUE CHAIN ANALYSIS

- 5.8 CASE STUDIES

- 5.8.1 MITSUBISHI FORKLIFT ENHANCED SAFETY AT KELLOGG'S MANCHESTER SITE

- 5.8.2 DEMATIC'S AUTONOMOUS FORKLIFT REDUCED DELIVERY TIME AT L'OREAL

- 5.8.3 THYSSENKRUPP EMPLOYED JUNGHEINRICH AG FOR FLEXIBLE AUTOMATION

- 5.8.4 JUNGHEINRICH AG AUTOMATED COKO-WERK GMBH & CO. KG WAREHOUSES

- 5.8.5 TOYOTA DELIVERED SUSTAINABLE AGV SOLUTIONS TO PANASONIC ENERGY

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 PATENT ANALYSIS

- 5.11 TECHNOLOGY ANALYSIS

- 5.11.1 KEY TECHNOLOGIES

- 5.11.1.1 IoT for automated material handling

- 5.11.1.2 Smart braking technology for forklifts

- 5.11.2 COMPLEMENTARY TECHNOLOGIES

- 5.11.2.1 Collaborative robots

- 5.11.2.2 Sustainable forklift technologies

- 5.11.3 ADJACENT TECHNOLOGIES

- 5.11.3.1 5G connectivity for automated warehouses

- 5.11.3.2 Implementation of AI in industrial vehicles

- 5.11.1 KEY TECHNOLOGIES

- 5.12 TRADE ANALYSIS

- 5.12.1 IMPORT SCENARIO (HS CODE 842710)

- 5.12.2 EXPORT SCENARIO (HS CODE 842710)

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 SAFETY STANDARDS FOR AGVS

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 KEY CONFERENCES & EVENTS, 2025-2026

- 5.15 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.1.1 Key stakeholders in buying process

- 5.15.1.2 Buying criteria

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.16 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.17 IMPACT OF AI/GEN AI ON INDUSTRIAL VEHICLES MARKET

- 5.17.1 TOP USE CASES AND MARKET POTENTIAL

- 5.17.2 BEST PRACTICES IN ELECTRIC INDUSTRIAL VEHICLE DEVELOPMENT

- 5.17.3 CASE STUDIES: IMPLEMENTATION OF AI IN INDUSTRIAL VEHICLES MARKET

- 5.17.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.17.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN INDUSTRIAL VEHICLES

- 5.17.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 5.17.6.1 Toyota Industries Corporation: AI-enabled autonomous lift trucks for flexible loading

- 5.17.6.2 Jungheinrich AG: Autonomous intralogistics vehicles for smart manufacturing

- 5.17.6.3 Linde Material Handling: Autonomous mobile robots for warehouse automation

- 5.17.6.4 KION Group: AI-powered digital twin for warehouse optimization

- 5.17.6.5 Crown Equipment Corporation: Autonomous forklift deployment in logistics operations

- 5.17.6.6 Jungheinrich AG: Lithium-ion battery technology for smart electric fleets

6 AERIAL WORK PLATFORM MARKET, BY TYPE

- 6.1 INTRODUCTION

- 6.2 BY TYPE

- 6.3 BY PROPULSION

- 6.3.1 AERIAL LIFT PLATFORM MODELS, BY OEMS

- 6.4 BOOM LIFTS

- 6.4.1 INCREASED FOREIGN INVESTMENTS AND GOVERNMENT SUPPORT TO DRIVE MARKET

- 6.4.2 BY REGION

- 6.4.3 BY PROPULSION

- 6.5 SCISSOR LIFTS

- 6.5.1 NEED FOR EXPANSION OF INFRASTRUCTURE AND COMMERCIAL CONSTRUCTION ACTIVITY TO DRIVE MARKET

- 6.5.2 BY REGION

- 6.5.3 BY PROPULSION

- 6.6 KEY PRIMARY INSIGHTS

7 INDUSTRIAL VEHICLE MOTORS MARKET, BY MOTOR TYPE

- 7.1 INTRODUCTION

- 7.2 TRACTION MOTORS

- 7.2.1 FLEET ELECTRIFICATION AND RISING DEMAND FROM WAREHOUSE AUTOMATION AND E-COMMERCE LOGISTICS TO DRIVE MARKET

- 7.2.2 INDUSTRIAL VEHICLE MODELS EQUIPPED WITH TRACTION MOTORS, BY OEM

- 7.2.3 BY REGION

- 7.2.4 TRACTION MOTORS MARKET, BY POWER OUTPUT

- 7.2.4.1 <= 5 kW

- 7.2.4.2 > 5 kW

- 7.2.5 TRACTION MOTORS MARKET, BY POWER SOURCE

- 7.2.5.1 AC

- 7.2.5.2 DC

- 7.3 HYDRAULIC MOTORS

- 7.3.1 IMPLEMENTATION OF ENHANCED PRECISION CONTROL AND SMOOTHER LOAD HANDLING TO DRIVE MARKET

- 7.3.2 HYDRAULIC MOTORS MARKET, BY POWER OUTPUT

- 7.3.2.1 <= 5 kW

- 7.3.2.2 > 5 kW

- 7.3.3 HYDRAULIC MOTORS MARKET, BY POWER SOURCE

- 7.3.3.1 AC

- 7.3.3.2 DC

- 7.4 POWER STEERING MOTORS

- 7.4.1 RAPID ELECTRIFICATION OF INDUSTRIAL AND COMMERCIAL VEHICLE FLEETS TO DRIVE MARKET

- 7.4.2 POWER STEERING MOTORS MARKET, BY POWER OUTPUT

- 7.4.2.1 <= 5 kW

- 7.4.2.2 > 5 kW

- 7.4.3 POWER STEERING MOTORS MARKET, BY POWER SOURCE

- 7.4.3.1 AC

- 7.4.3.2 DC

- 7.5 KEY PRIMARY INSIGHTS

8 INDUSTRIAL VEHICLES MARKET, BY VEHICLE TYPE & CAPACITY

- 8.1 INTRODUCTION

- 8.1.1 INDUSTRIAL VEHICLE MODELS OFFERED BY OEMS

- 8.2 FORKLIFTS

- 8.2.1 NEED FOR TECHNOLOGICAL ADVANCEMENTS IN ELECTRIC FORKLIFTS TO DRIVE MARKET

- 8.2.2 FORKLIFTS MARKET, BY CAPACITY

- 8.2.2.1 < 5 tons

- 8.2.2.2 5-10 tons

- 8.2.2.3 11-36 tons

- 8.2.2.4 > 36 tons

- 8.3 AISLE TRUCKS

- 8.3.1 INCREASING DEMAND FOR SPACE OPTIMIZATION IN WAREHOUSES TO DRIVE MARKET

- 8.3.2 AISLE TRUCKS MARKET, BY CAPACITY

- 8.3.2.1 < 1 ton

- 8.3.2.2 1-2 tons

- 8.3.2.3 > 2 tons

- 8.4 TOW TRACTORS

- 8.4.1 INCREASING DEMAND FOR EFFICIENT MATERIAL HANDLING TO DRIVE MARKET

- 8.4.2 TOW TRACTORS MARKET, BY CAPACITY

- 8.4.2.1 < 5 tons

- 8.4.2.2 5-10 tons

- 8.4.2.3 11-30 tons

- 8.4.2.4 > 30 tons

- 8.5 CONTAINER HANDLERS

- 8.5.1 FOCUS ON STRENGTHENING INFRASTRUCTURE IN MARITIME TRANSPORT TO DRIVE MARKET

- 8.5.2 CONTAINER HANDLERS MARKET, BY CAPACITY

- 8.5.2.1 < 30 tons

- 8.5.2.2 30-40 tons

- 8.5.2.3 > 40 tons

- 8.6 AUTOMATED GUIDED VEHICLES

- 8.6.1 RAPID INDUSTRIAL AUTOMATION IN MATERIAL-HANDLING PROCESSES TO DRIVE MARKET

- 8.6.2 CHALLENGES OF AGVS

- 8.6.2.1 Availability of cost-effective labor restricting adoption of AGVs in emerging economies

- 8.6.2.2 Technical challenges related to sensing elements

- 8.6.2.3 High installation, maintenance, and switching costs associated with AGVs

- 8.7 PERSONNEL CARRIERS

- 8.7.1 RAPID INDUSTRIAL GROWTH, EXPANDING MANUFACTURING HUBS, AND GROWING WORKFORCE MOBILITY TO DRIVE MARKET

- 8.8 KEY PRIMARY INSIGHTS

9 INDUSTRIAL VEHICLES MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.1.1 INDUSTRIAL VEHICLES AND THEIR APPLICATIONS

- 9.2 MANUFACTURING

- 9.2.1 INCREASING ADOPTION OF INDUSTRIAL VEHICLES IN END-USE INDUSTRIES TO DRIVE MARKET

- 9.2.2 AUTOMOTIVE

- 9.2.3 METALS & HEAVY MACHINERY

- 9.2.4 CHEMICAL

- 9.2.5 HEALTHCARE

- 9.2.6 FOOD & BEVERAGES

- 9.2.7 OTHERS

- 9.3 WAREHOUSING

- 9.3.1 EXPANSION OF E-COMMERCE SECTOR TO FUEL GROWTH

- 9.4 FREIGHT & LOGISTICS

- 9.4.1 CONSUMER SHIFT TOWARD ONLINE SHOPPING TO DRIVE GROWTH

- 9.5 OTHERS

- 9.6 KEY PRIMARY INSIGHTS

10 INDUSTRIAL VEHICLES MARKET, BY LEVEL OF AUTONOMY

- 10.1 INTRODUCTION

- 10.2 SEMI-AUTONOMOUS

- 10.2.1 SEMI-AUTONOMOUS TECHNOLOGY ALLOWS LIFT TRUCKS TO MOVE AUTOMATICALLY ALONG PREDEFINED ROUTES USING NAVIGATION SYSTEMS

- 10.3 AUTONOMOUS

- 10.3.1 AUTONOMOUS INDUSTRIAL VEHICLES ENSURE CORRECT QUANTITY OF MATERIALS IS DELIVERED SAFELY TO RIGHT LOCATION AT RIGHT TIME

- 10.4 KEY PRIMARY INSIGHTS

11 INDUSTRIAL VEHICLES MARKET, BY PROPULSION

- 11.1 INTRODUCTION

- 11.2 INDUSTRIAL VEHICLES OFFERED BY COMPANIES, BY PROPULSION

- 11.3 ICE

- 11.3.1 INCREASING UTILIZATION OF ICE VEHICLES FOR DISTRIBUTION AND FREIGHT HANDLING TO DRIVE MARKET

- 11.4 BATTERY-OPERATED

- 11.4.1 GROWING ENVIRONMENTAL AWARENESS TO DRIVE ADOPTION OF BATTERY-OPERATED INDUSTRIAL VEHICLES

- 11.4.2 INTERNAL COMBUSTION ENGINES VS. ELECTRIC ENGINES

- 11.5 GAS-POWERED

- 11.5.1 NEED FOR COST-EFFECTIVE AND ENVIRONMENT-FRIENDLY MATERIAL-HANDLING SOLUTIONS TO DRIVE MARKET

- 11.6 KEY PRIMARY INSIGHTS

12 INDUSTRIAL VEHICLES MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Need for high-density logistics to drive market

- 12.2.2 INDIA

- 12.2.2.1 Focus on infrastructural expansion and e-commerce warehousing to boost growth

- 12.2.3 JAPAN

- 12.2.3.1 Demand for automation-driven replacement to strengthen market

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Need for technology-intensive manufacturing to drive demand

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Need for industrial automation to anchor market growth

- 12.3.2 UK

- 12.3.2.1 Post-Brexit supply chain restructuring to support demand for replacement

- 12.3.3 FRANCE

- 12.3.3.1 Modernization of logistics and sustainability commitments to drive demand

- 12.3.4 ITALY

- 12.3.4.1 Presence of small and medium manufacturing enterprises to drive momentum

- 12.3.5 SPAIN

- 12.3.5.1 Rising activities in logistics and warehousing sectors to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 NORTH AMERICA

- 12.4.1 US

- 12.4.1.1 Presence of mega fulfillment centers and lithium-ion fleets to reshape market

- 12.4.2 MEXICO

- 12.4.2.1 Nearshoring momentum and export manufacturing to boost forklift demand

- 12.4.3 CANADA

- 12.4.3.1 Emphasis on cold-chain logistics and electrified warehousing to drive market

- 12.4.1 US

- 12.5 REST OF THE WORLD

- 12.5.1 BRAZIL

- 12.5.1.1 Need for industrial recovery and agribusiness logistics to support demand

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Mining supply chains and port logistics to drive equipment utilization

- 12.5.3 OTHERS

- 12.5.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.3.1 TOYOTA INDUSTRIES CORPORATION

- 13.3.2 KION GROUP AG

- 13.3.3 MITSUBISHI LOGISNEXT CO., LTD.

- 13.3.4 JUNGHEINRICH AG

- 13.3.5 CROWN EQUIPMENT CORPORATION

- 13.4 REVENUE ANALYSIS, 2020-2024

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING

- 13.9 COMPANY EVALUATION MATRIX (AERIAL WORK PLATFORM MARKET): KEY PLAYERS, 2025

- 13.9.1 STARS

- 13.9.2 EMERGING LEADERS

- 13.9.3 PERVASIVE PLAYERS

- 13.9.4 PARTICIPANTS

- 13.9.5 COMPANY FOOTPRINT

- 13.10 COMPETITIVE SCENARIO

- 13.10.1 PRODUCT LAUNCHES

- 13.10.2 DEALS

- 13.10.3 EXPANSION

- 13.10.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS (INDUSTRIAL VEHICLES)

- 14.1.1 TOYOTA INDUSTRIES CORPORATION

- 14.1.1.1 Business overview

- 14.1.1.2 Recent developments

- 14.1.1.3 MnM view

- 14.1.1.3.1 Key strengths

- 14.1.1.3.2 Strategic choices

- 14.1.1.3.3 Weaknesses & competitive threats

- 14.1.2 KION GROUP AG

- 14.1.2.1 Business overview

- 14.1.2.2 Recent developments

- 14.1.2.3 MnM view

- 14.1.2.3.1 Key strengths

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses & competitive threats

- 14.1.3 MITSUBISHI LOGISNEXT CO., LTD.

- 14.1.3.1 Business overview

- 14.1.3.2 Recent developments

- 14.1.3.3 MnM view

- 14.1.3.3.1 Key strengths

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses & competitive threats

- 14.1.4 JUNGHEINRICH AG

- 14.1.4.1 Business overview

- 14.1.4.2 Recent developments

- 14.1.4.3 MnM view

- 14.1.4.3.1 Key strengths

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 CROWN EQUIPMENT CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Recent developments

- 14.1.5.3 MnM view

- 14.1.5.3.1 Key strengths

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 HYSTER-YALE MATERIALS HANDLING, INC.

- 14.1.6.1 Business overview

- 14.1.6.2 Recent developments

- 14.1.7 HANGCHA FORKLIFT

- 14.1.7.1 Business overview

- 14.1.7.2 Recent developments

- 14.1.8 CLARK

- 14.1.8.1 Business overview

- 14.1.8.2 Recent developments

- 14.1.9 ANHUI HELI CO. LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Recent developments

- 14.1.10 KONECRANES

- 14.1.10.1 Business overview

- 14.1.10.2 Recent developments

- 14.1.11 EP EQUIPMENT

- 14.1.11.1 Business overview

- 14.1.11.2 Recent developments

- 14.1.1 TOYOTA INDUSTRIES CORPORATION

- 14.2 OTHER PLAYERS

- 14.2.1 KOMATSU LTD.

- 14.2.2 DOOSAN BOBCAT

- 14.2.3 MANITOU GROUP

- 14.2.4 CARGOTEC

- 14.2.5 ACTION CONSTRUCTION EQUIPMENT LTD.

- 14.2.6 HYUNDAI CONSTRUCTION EQUIPMENT INDIA PVT. LTD.

- 14.2.7 V. MARIOTTI S.R.L.

- 14.2.8 COMBILIFT

- 14.2.9 DAIFUKU

- 14.2.10 JBT

- 14.2.11 LONKING MACHINERY CO., LTD.

- 14.2.12 HUBTEX MASCHINENBAU GMBH & CO. KG

- 14.2.13 GODREJ & BOYCE MANUFACTURING COMPANY LIMITED

- 14.2.14 SVETUCK AB

- 14.2.15 STOCKLIN LOGISTIK AG

- 14.2.16 O.M.G. SRL

- 14.2.17 PALETRANS FORKLIFTS

- 14.2.18 GENKINGER GMBH

- 14.2.19 FLEXI TRUCKS

- 14.2.20 AGILOX SERVICES GMBH

- 14.3 KEY PLAYERS (LIFTING PLATFORMS)

- 14.3.1 JLG INDUSTRIES, INC.

- 14.3.1.1 Business overview

- 14.3.1.2 Recent developments

- 14.3.2 TADANO LTD.

- 14.3.2.1 Business overview

- 14.3.2.2 Recent developments

- 14.3.3 TEREX CORPORATION

- 14.3.3.1 Business overview

- 14.3.3.2 Recent developments

- 14.3.4 LINAMAR

- 14.3.4.1 Business overview

- 14.3.4.2 Recent developments

- 14.3.5 MAGNI TELESCOPIC HANDLERS SRL

- 14.3.5.1 Business overview

- 14.3.5.2 Recent developments

- 14.3.1 JLG INDUSTRIES, INC.

- 14.4 OTHER KEY PLAYERS (LIFTING PLATFORMS)

- 14.4.1 HAULOTTE GROUP

- 14.4.2 AICHI CORPORATION

- 14.4.3 PALFINGER AG

- 14.4.4 IMER GROUP

- 14.4.5 SINOBOOM INTELLIGENT EQUIPMENT CO, LTD.

- 14.4.6 ALTEC INDUSTRIES

- 14.4.7 J C BAMFORD EXCAVATORS LTD.

- 14.4.8 NOBLELIFT INTELLIGENT EQUIPMENT CO., LTD.

- 14.4.9 BRONTO SKYLIFT

- 14.4.10 DINOLIFT OY

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Primary interviewees from demand and supply sides

- 15.1.2.2 Key primary insights

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 List of primary participants

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 DATA TRIANGULATION

- 15.4 FACTOR ANALYSIS

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

16 APPENDIX

- 16.1 KEY INSIGHTS FROM INDUSTRY EXPERTS

- 16.2 DISCUSSION GUIDE

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.4.1 BY CAPACITY, AT REGIONAL LEVEL, BY VEHICLE TYPE

- 16.4.2 BY DRIVE TYPE, AT REGIONAL LEVEL, BY VEHICLE TYPE

- 16.4.3 BY APPLICATION, AT GLOBAL LEVEL, BY VEHICLE TYPE

- 16.4.4 COMPANY INFORMATION

- 16.4.4.1 Profiling of additional market players (Up to 5)

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS