|

시장보고서

상품코드

2004291

고성능 플라스틱 컴파운드 시장 - 플라스틱 유형별, 첨가제 유형별, 최종 이용 산업별, 지역별 - 세계 예측(-2030년)High-performance Plastic Compounds Market by Plastic Type, Additive Type, End-use Industry, and Region - Global Forecast to 2030 |

||||||

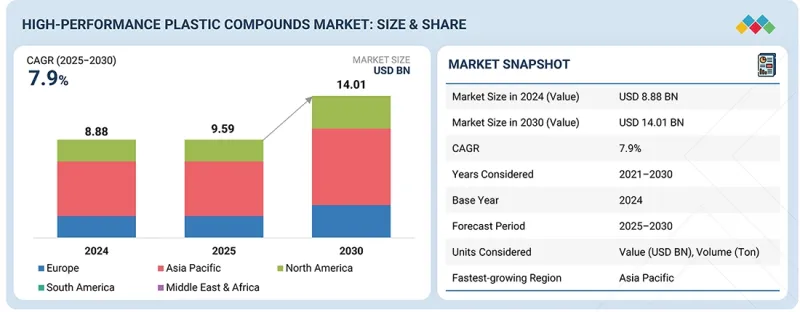

세계의 고성능 플라스틱 컴파운드 시장 규모는 2025년 95억 9,000만 달러에서 2030년까지 140억 1,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)에 CAGR로 7.9%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만/10억 달러, 톤 |

| 부문 | 플라스틱 유형, 최종 이용 산업, 첨가제 유형, 지역 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

고성능 플라스틱 컴파운드는 지난 몇 년 동안 꾸준한 성장세를 보이고 있으며, 고성능, 고강도 플라스틱 컴파운드에 대한 수요 증가로 인해 앞으로도 완만한 성장세를 이어갈 것으로 예상됩니다. 도시화, 인프라 개발, 경량화 및 전기자동차 등의 혁신으로 인한 자동차 산업의 성장은 구조 부품, 전기 시스템, 엔진룸 내 적용을 위한 고성능 플라스틱 컴파운드의 수요 증가를 촉진하는 주요 요인으로 작용하고 있습니다. 또한, 내열성과 내구성이 요구되는 전기 및 전자 부문과 산업용 부문에서 고성능 플라스틱 컴파운드에 대한 수요가 확대되고 있는 것도 수요를 촉진하고 있습니다. 또한, 아시아태평양은 활발한 제조 활동과 생산능력 확대로 인해 HPPC의 물량 기준 성장에 큰 촉진제 역할을 하고 있습니다. 마지막으로, 연비, 배출가스, 지속가능한 재료 사용에 대한 환경 규제가 고성능 플라스틱 컴파운드의 수요 증가를 촉진할 것으로 예상됩니다. 시장은 원자재 가격 변동과 환경 규제 등 여러 가지 도전에 직면해 있지만, 고급 응용 분야의 혁신과 고성능 플라스틱 화합물에 대한 수요 증가는 향후 수요를 촉진할 것으로 보입니다.

"플라스틱 유형별로는 PEEK가 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

플라스틱 유형별로는 PEEK가 고성능 플라스틱 컴파운드 시장을 주도할 것으로 예상됩니다. PEEK의 주요 용도는 높은 내열성, 기계적 강도, 신뢰성이 요구되는 장면입니다. PEEK의 특성으로 인해 고온 환경에서도 우수한 성능을 발휘합니다. PEEK의 내화학성과 내마모성이 매우 높아 이러한 특성이 요구되는 용도에 사용되고 있습니다. 이 외에도 PEEK는 의료, 산업, 석유 및 가스 분야에서도 사용되고 있으며, 이들 산업에서도 수요가 발생하고 있습니다. 다른 고성능 플라스틱 컴파운드에 비해 PEEK는 고온에서의 강도 유지성, 치수 안정성, 가혹한 화학제품에 대한 내성이 우수합니다. 이와 더불어, 경량화 및 고성능 소재에 대한 관심이 지속적으로 증가하고 있으며, 전기자동차 및 전자제품에 대한 채용이 진행되고 있어 PEEK의 인기는 더욱 높아질 것으로 예상됩니다. 아시아태평양의 생산능력 확대와 가공 및 배합 기술의 발전으로 PEEK의 우위는 더욱 강화될 것으로 예상됩니다.

"최종 용도별로는 항공우주 부문이 예측 기간 동안 가장 빠른 성장을 기록할 것으로 예상됩니다."

항공우주 산업은 경량화 및 성능 향상에 크게 기여하기 때문에 고성능 플라스틱 컴파운드의 주요 최종 사용 분야가 되었습니다. PEEK, PPS, 폴리이미드 등의 고성능 플라스틱 컴파운드는 내장부품, 구조부품, 전기부품, 엔진부품 등 항공기 부품에 사용되고 있습니다. 또한, 연비 효율이 높고 친환경적인 항공기에 대한 수요 증가와 배출가스 저감 노력으로 경량화 및 성능 향상을 위한 고성능 플라스틱 컴파운드의 사용은 꾸준히 증가하고 있습니다. 또한, 항공 운송 수요의 증가, 상업용 및 방산용 항공기의 기체 수 증가, 항공기 수리 및 정비 수요의 증가로 인해 고성능 플라스틱 컴파운드 산업은 빠르게 성장하고 있습니다. 이러한 플라스틱 컴파운드는 항공기의 경량화 및 성능 향상과 더불어 항공기 부품의 내구성과 내화학성에도 크게 기여하고 있습니다.

"아시아태평양이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

아시아태평양은 탄탄한 제조 기반, 강력한 산업 성장, 다양한 최종 사용 산업에서의 높은 수요로 인해 고성능 플라스틱 컴파운드의 가장 큰 시장으로 부상하고 있습니다. 이 지역의 주요 시장으로는 중국, 인도, 일본, 한국 등이 있습니다. 이들 시장에서는 자동차, 전기/전자, 항공우주 등의 산업에서 사용되는 고성능 플라스틱 컴파운드에 대한 수요가 강세를 보이고 있습니다. 이들 산업에서는 내열성과 강도가 높은 PEEK, PPS, 폴리아미드 등 고성능 플라스틱 컴파운드가 요구되고 있습니다. 아시아태평양은 전자, 자동차 등의 산업에서 중요한 시장이며, 이들 제품의 다양한 부품에 고성능 플라스틱 컴파운드가 사용되고 있습니다.

세계의 고성능 플라스틱 컴파운드 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 고성능 플라스틱 컴파운드 시장 : 플라스틱 유형별

제10장 고성능 플라스틱 컴파운드 시장 : 첨가제 유형별

제11장 고성능 플라스틱 컴파운드 시장 : 용도별

제12장 고성능 플라스틱 컴파운드 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

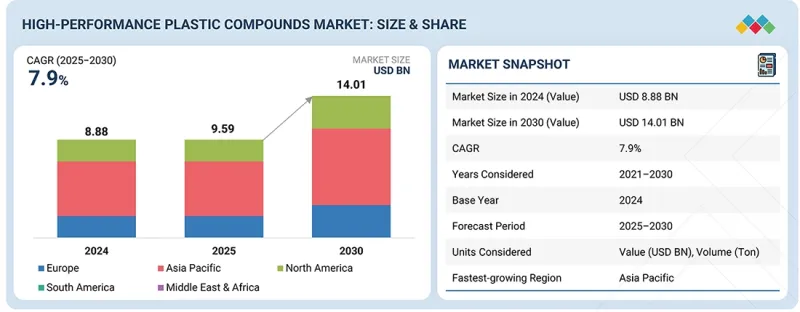

KSM 26.04.28The global high-performance plastic compounds market is projected to grow from USD 9.59 billion in 2025 to USD 14.01 billion by 2030, registering a CAGR of 7.9% during the forecast period (2025-2030).

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Ton) |

| Segments | Plastic Type, End-use Industry, Additive Type, and Region |

| Regions covered | Asia Pacific, North America, Europe, the Middle East & Africa, and South America |

High-Performance plastic compounds have registered steady growth over the past few years and are expected to continue at a moderate rate in the future, driven by increased demand for high-performance, high-strength plastic compounds. Urbanization, infrastructure development, and growth in the automobile industry, driven by innovations such as lightweight and electric cars, are major factors driving the increasing demand for high-performance plastic compounds for structural parts, electrical systems, and under-the-hood applications. In addition, the growing demand for high-performance plastic compounds in the electrical & electronics and industrial segments, where heat resistance and durability are required, is also driving demand. Moreover, the Asia Pacific region has been a major driver of overall HPPC volume growth, driven by strong manufacturing activity and capacity expansion. Finally, environmental regulations on fuel efficiency, emissions, and the use of sustainable materials will drive increasing demand for high-performance plastic compounds. The market faces several challenges to growth, including fluctuating raw-material prices and environmental regulations; however, innovations and increasing demand for high-performance plastic compounds in high-end applications will drive demand in the future.

"By plastic type, PEEK is anticipated to account for the largest market share during the forecast period."

Based on plastic type, PEEK is expected to dominate the high-performance plastic compounds market. The primary application of PEEK is in situations where high heat resistance, mechanical strength, and reliability are required. The properties of PEEK enable it to perform well at high temperatures. The chemical and wear properties of PEEK are very high, and it is used for applications that require these properties. Apart from these, PEEK is used for medical, industrial, and oil and gas applications, thereby generating demand from these industries as well. Compared with other high-performance plastic compounds, PEEK offers greater strength retention at high temperatures, dimensional stability, and resistance to harsh chemicals. Apart from these, as the focus on lightweight, high-performance materials continues to rise, coupled with their use in electric vehicles and electronic devices, it is expected that PEEK will gain greater popularity. The dominance of PEEK is further expected to grow due to rising production capacity in the Asia Pacific and advancements in processing and compounding technologies.

"By end-use industry, the aerospace segment is anticipated to register the fastest growth during the forecast period."

The aerospace industry is a key end-use sector for high-performance plastic compounds, as it contributes significantly to weight reduction and performance improvements. High-performance plastic compounds, such as PEEK, PPS, and polyimide, are used in aircraft parts, including interior, structural, electrical, and engine components. Additionally, owing to increased demand for fuel-efficient and environmentally friendly aircraft, as well as for reducing emissions, the use of high-performance plastic compounds for weight reduction and performance improvement has registered a steady increase. Moreover, owing to increased demand for air transportation and the expansion of fleets for commercial and defense aircraft, as well as for aircraft repairs and maintenance, high-performance plastic compounds have registered rapid growth in this industry. These plastic compounds contribute significantly to weight reduction and performance improvement in aircraft, as well as to the durability and chemical resistance of aircraft parts.

"Asia Pacific is expected to account for the largest market share during the forecast period."

Asia Pacific is the largest market for high-performance plastic compounds, driven by a well-established manufacturing base, strong industrial growth, and high demand across various end-use industries. Some of the important markets in this region include China, India, Japan, and South Korea. These markets have strong demand for high-performance plastic compounds used across industries such as automotive, electrical and electronics, and aerospace. These industries require high-performance plastic compounds such as PEEK, PPS, and polyamide due to their high heat resistance and high strength. Asia Pacific is an important market for industries such as electronics and automobiles, where high-performance plastic compounds are used for various parts of these products. Population growth, rising disposable incomes, and the expansion of the middle class across this region have driven strong demand for consumer electronics, automobiles, and industrial products. In addition, this region has large-scale production units, especially in countries such as China, which help achieve cost-effective production and supply of high-performance plastic compounds to the market. All these factors contribute to making the Asia Pacific the largest market for high-performance plastic compounds.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from key organizations operating in the high-performance plastic compounds market, and secondary research was used to determine and verify the market sizes of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers - 15%, Directors - 20%, and Others - 65%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, the Middle East & Africa - 10%, and South America - 5%

The high-performance plastic compounds market comprises of major companies like BASF (Germany), SABIC (Saudi Arabia), DAIKIN INDUSTRIES, Ltd. (Japan), Syensqo (Belgium), Celanese Corporation (US), RTP Company (US), MITSUBISHI CHEMICAL GROUP CORPORATION (Japan), Victrex plc (UK), Evonik Industries AG (Germany), and Ensinger (Germany). The study includes an in-depth competitive analysis of these key players in the high-performance plastic compounds market, with their company profiles, recent developments, and key market strategies.

Research Coverage

In this report, the high-performance plastic compounds market has been segmented on the basis of plastic type, end-use industry, additive type, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the high-performance plastic compounds market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the high-performance plastic compounds market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

- Analysis of drivers (increasing demand for lightweight and high-strength materials in automotive and transportation, growing use in medical & healthcare devices requiring sterilization-resistant and biocompatible materials, and expanding infrastructure and energy-efficient construction applications), restraints (high raw material and specialty resin costs and complex processing and capital-intensive manufacturing), opportunities (expansion in renewable energy, 5G infrastructure, and smart electronics and increasing industrialization and advanced manufacturing in emerging economies), and challenges (stringent environmental and chemical regulations, intense competition, and continuous innovation pressure) influencing the growth of high-performance plastic compounds market.

- Market Penetration: Comprehensive information on the high-performance plastic compounds offered by top players in the global high-performance plastic compounds market.

- Product Development/Innovation: Detailed insights on upcoming technologies, product launches, expansions, and acquisitions in the high-performance plastic compounds market.

- Market Development: Comprehensive information about lucrative emerging markets, the report analyzes the markets for high-performance plastic compounds market across regions.

- Market Capacity: Production capacity of the companies is provided wherever available, with upcoming capacities for the high-performance plastic compounds market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the high-performance plastic compounds market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 3.2 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY PLASTIC TYPE AND REGION

- 3.3 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY ADDITIVE TYPE

- 3.4 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY

- 3.5 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for lightweight and high-strength materials in automotive and transportation

- 4.2.1.2 Growing use in medical & healthcare devices requiring sterilization-resistant and biocompatible materials

- 4.2.1.3 Expanding infrastructure and energy-efficient construction applications

- 4.2.2 RESTRAINTS

- 4.2.2.1 High raw material and specialty resin costs

- 4.2.2.2 Complex processing and capital-intensive manufacturing

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion in renewable energy, 5G infrastructure, and smart electronics

- 4.2.3.2 Increasing industrialization and advanced manufacturing in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Stringent environmental and chemical regulations

- 4.2.4.2 Intense competition and continuous innovation pressure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN ELECTRICAL & ELECTRONICS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE, BY REGION (2021-2024)

- 5.4.2 AVERAGE SELLING PRICE, BY PLASTIC TYPE (2021-2024)

- 5.4.3 AVERAGE SELLING PRICE, BY ADDITIVE TYPE (2021-2024)

- 5.4.4 AVERAGE SELLING PRICE, BY END-USE INDUSTRY (2021-2024)

- 5.4.5 AVERAGE SELLING PRICE, BY PLASTIC TYPE (2024)

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 391190)

- 5.6.2 EXPORT SCENARIO (HS CODE 391190)

- 5.6.3 IMPORT SCENARIO (HS CODE 390469)

- 5.6.4 EXPORT SCENARIO (HS CODE 390469)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SOLVAY & VOLKSWAGEN GROUP COLLABORATED FOR LIGHTWEIGHT HIGH-PERFORMANCE POLYMER SOLUTIONS IN AUTOMOTIVE APPLICATIONS

- 5.10.2 SABIC & MEDTRONIC COLLABORATED FOR STERILIZATION-RESISTANT MEDICAL DEVICE COMPONENTS

- 5.10.3 VICTREX PLC & AIRBUS COLLABORATED FOR LIGHTWEIGHT AEROSPACE STRUCTURAL COMPONENTS

- 5.11 IMPACT OF 2025 US TARIFF ON HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 TWIN-SCREW EXTRUSION

- 6.1.2 REACTIVE EXTRUSION

- 6.1.3 HIGH-TEMPERATURE PROCESSING SYSTEMS

- 6.1.4 PELLETIZING TECHNOLOGIES (STRAND/UNDERWATER/HOT-FACE)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GRAVIMETRIC FEEDING & PRECISION DOSING

- 6.2.2 MATERIAL DRYING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INJECTION MOLDING (ADVANCED/PRECISION INJECTION MOLDING)

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 DOCUMENT TYPES

- 6.5.4 INSIGHTS

- 6.5.5 LEGAL STATUS

- 6.5.6 JURISDICTION ANALYSIS

- 6.5.7 TOP APPLICANTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AUTOMOTIVE & MOBILITY SYSTEMS

- 6.6.2 ELECTRICAL & ELECTRONICS

- 6.6.3 MEDICAL & HEALTHCARE DEVICES

- 6.6.4 BUILDING & CONSTRUCTION

- 6.7 IMPACT OF AI/GEN AI ON HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN HIGH-PERFORMANCE PLASTIC COMPOUNDS PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 SYENSQO: AI-ENABLED ADVANCED POLYMER FORMULATION & PROCESS OPTIMIZATION

- 6.8.2 SABIC: AI-DRIVEN COMPOUNDING EFFICIENCY AND QUALITY ENHANCEMENT

- 6.8.3 VICTREX PLC: AI-ACCELERATED HIGH-PERFORMANCE PEEK COMPOUND INNOVATION

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF HIGH-PERFORMANCE PLASTIC COMPOUNDS

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF HIGH-PERFORMANCE PLASTIC COMPOUNDS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, & ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY PLASTIC TYPE

- 9.1 INTRODUCTION

- 9.2 PEEK

- 9.2.1 STRONG AEROSPACE, EV MANUFACTURING, AND MEDICAL DEVICE INNOVATION TO DRIVE MARKET

- 9.3 PPS

- 9.3.1 EXPANDING USE IN AUTOMOTIVE ELECTRIFICATION AND ELECTRICAL INFRASTRUCTURE APPLICATIONS TO PROPEL MARKET

- 9.4 PEI

- 9.4.1 STRONG DEMAND FOR ELECTRICAL INSULATION, EV STRUCTURAL COMPONENTS, AND MEDICAL-GRADE APPLICATIONS TO DRIVE MARKET

- 9.5 PSU/PPSU/PESU

- 9.5.1 STRONG MEDICAL DEVICE PRODUCTION AND INFRASTRUCTURE MODERNIZATION TO DRIVE DEMAND

- 9.6 FLUOROPOLYMER COMPOUNDS

- 9.6.1 STRONG DEMAND FROM SEMICONDUCTOR EXPANSION AND CHEMICAL PROCESSING INDUSTRIES TO DRIVE MARKET

- 9.7 PAI

- 9.7.1 STRONG DEFENSE, SEMICONDUCTOR, AND HIGH-TEMPERATURE INDUSTRIAL APPLICATIONS TO DRIVE GROWTH

- 9.8 OTHER PLASTIC TYPES

10 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY ADDITIVE TYPE

- 10.1 INTRODUCTION

- 10.2 GLASS FIBER

- 10.2.1 INCREASING DEMAND FOR STRUCTURAL INTEGRITY, LIGHTWEIGHTING, AND COST-EFFICIENT METAL REPLACEMENT TO DRIVE ADOPTION

- 10.3 CARBON FIBER

- 10.3.1 RISING DEMAND FOR LIGHTWEIGHT, HIGH-STIFFNESS MATERIALS AND ADVANCED MANUFACTURING TO DRIVE MARKET

- 10.4 MINERAL FILLED

- 10.4.1 GROWING DEMAND FOR DIMENSIONAL STABILITY, COST OPTIMIZATION, AND THERMAL PERFORMANCE IN STRUCTURAL AND ELECTRICAL APPLICATIONS TO PROPEL MARKET

- 10.5 COLOR COMPOUNDED

- 10.5.1 RISING DEMAND FOR AESTHETIC DIFFERENTIATION, BRAND STANDARDIZATION, AND LONG-TERM COLOR STABILITY TO DRIVE MARKET

- 10.6 UV STABILIZED

- 10.6.1 INCREASING DEMAND FOR OUTDOOR DURABILITY IN AUTOMOTIVE AND APPLICATIONS TO SUPPORT MARKET GROWTH

- 10.7 FLAME RETARDANT

- 10.7.1 STRINGENT FIRE SAFETY REGULATIONS AND ELECTRIFICATION TRENDS TO DRIVE DEMAND

- 10.8 OTHER ADDITIVE TYPES

11 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 AUTOMOTIVE

- 11.2.1 RAPID ELECTRIFICATION, LIGHTWEIGHTING, AND REGULATORY COMPLIANCE TO DRIVE ADOPTION

- 11.3 ELECTRICAL & ELECTRONICS

- 11.3.1 GRID MODERNIZATION, DATA CENTER EXPANSION, AND HIGH-VOLTAGE ELECTRIFICATION TO DRIVE DEMAND

- 11.4 AEROSPACE

- 11.4.1 COMMERCIAL AVIATION RECOVERY, DEFENSE MODERNIZATION, AND SPACE PROGRAM EXPANSION TO DRIVE DEMAND

- 11.5 MEDICAL

- 11.5.1 ADVANCED HEALTHCARE INFRASTRUCTURE AND STRINGENT REGULATORY STANDARDS TO DRIVE DEMAND

- 11.6 INDUSTRIAL

- 11.6.1 ENERGY INFRASTRUCTURE EXPANSION AND AUTOMATION TO DRIVE DEMAND FOR DURABLE HIGH-PERFORMANCE MATERIALS

- 11.7 OTHER END-USE INDUSTRIES

12 HIGH-PERFORMANCE PLASTIC COMPOUNDS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Strong growth in automotive electrification to drive market

- 12.2.2 JAPAN

- 12.2.2.1 Strong automotive innovation and electronics manufacturing to propel market

- 12.2.3 INDIA

- 12.2.3.1 Rising automotive production and expanding electronics manufacturing to support market growth

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Strong automotive and semiconductor sectors to drive adoption

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Rising demand for lightweight and high-performance materials across automotive and aerospace industries to drive market

- 12.3.2 CANADA

- 12.3.2.1 Expansion of advanced aerospace and industrial manufacturing to drive market

- 12.3.3 MEXICO

- 12.3.3.1 Rapid expansion of automotive and electrical manufacturing sectors to propel growth

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Strong automotive manufacturing and advanced industrial base to drive market

- 12.4.2 ITALY

- 12.4.2.1 Automotive manufacturing and industrial machinery production to propel market

- 12.4.3 FRANCE

- 12.4.3.1 Strong demand from automotive and aerospace sectors to drive market

- 12.4.4 UK

- 12.4.4.1 Advanced automotive engineering sector to support market growth

- 12.4.5 SPAIN

- 12.4.5.1 Large automotive manufacturing industry to support market growth

- 12.4.6 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Petrochemical expansion and increase in oil & gas production to drive market

- 12.5.1.2 UAE

- 12.5.1.2.1 Energy infrastructure expansion and advanced manufacturing development to drive market

- 12.5.1.3 Rest of GCC Countries

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Rising demand from automotive, construction, and packaging sectors to propel market

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 ARGENTINA

- 12.6.1.1 Strong energy, automotive, and agro-industrial sectors to drive market

- 12.6.2 BRAZIL

- 12.6.2.1 Rising automotive output and offshore oil & gas development to support market growth

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 ARGENTINA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS, 2024

- 13.4 REVENUE ANALYSIS, 2020-2024

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Plastic type footprint

- 13.5.5.4 Additive type footprint

- 13.5.5.5 End-use industry footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 BRAND/PRODUCT COMPARISON

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 DAIKIN INDUSTRIES, LTD.

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Key strengths

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses and competitive threats

- 14.1.3 ENSINGER

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 VICTREX PLC

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 SYENSQO

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 CELANESE CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.4 MnM view

- 14.1.6.4.1 Key strengths

- 14.1.6.4.2 Strategic choices

- 14.1.6.4.3 Weaknesses and competitive threats

- 14.1.7 EVONIK INDUSTRIES AG

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 MnM view

- 14.1.7.3.1 Key strengths

- 14.1.7.3.2 Strategic choices

- 14.1.7.3.3 Weaknesses and competitive threats

- 14.1.8 MITSUBISHI CHEMICAL GROUP CORPORATION

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 MnM view

- 14.1.8.3.1 Key strengths

- 14.1.8.3.2 Strategic choices

- 14.1.8.3.3 Weaknesses and competitive threats

- 14.1.9 SABIC

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MnM view

- 14.1.9.3.1 Key strengths

- 14.1.9.3.2 Strategic choices

- 14.1.9.3.3 Weaknesses and competitive threats

- 14.1.10 RTP COMPANY

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MnM view

- 14.1.10.3.1 Key strengths

- 14.1.10.3.2 Strategic choices

- 14.1.10.3.3 Weaknesses and competitive threats

- 14.1.1 BASF

- 14.2 OTHER PLAYERS

- 14.2.1 SUN CHEMICAL

- 14.2.2 AMERICHEM

- 14.2.3 POLYMER INDUSTRIES

- 14.2.4 THE GUND COMPANY

- 14.2.5 SYMMTEK POLYMERS LLC

- 14.2.6 POLYPLASTICS CO., LTD.

- 14.2.7 TOSOH CORPORATION

- 14.2.8 KUREHA CORPORATION

- 14.2.9 TORAY INDUSTRIES, INC.

- 14.2.10 POLY FLUORO LTD.

- 14.2.11 ARKEMA

- 14.2.12 LON-SO PLASTICS

- 14.2.13 THE CHEMOURS COMPANY

- 14.2.14 PEFLON

- 14.2.15 POLYMER RESOURCES

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key primary interview participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH & TOP-DOWN APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 15.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS