|

시장보고서

상품코드

2004293

위성용 추진제 탱크 시장 : 아키텍처별, 용량별, 위성 질량별, 재료별, 추진제 유형별, 위성 궤도별, 지역별 - 예측(-2032년)Satellite Propellant Tanks Market by Capacity (<5, 5-50, 51-100, 101-250, 251-500, 501-1000, >1000 L), Propellant (Chemical, Electric, Cold-Gas), Architecture (Positive-Expulsion, PMD, HPV), Material, Mass, Orbit, and Region - Global Forecast to 2032 |

||||||

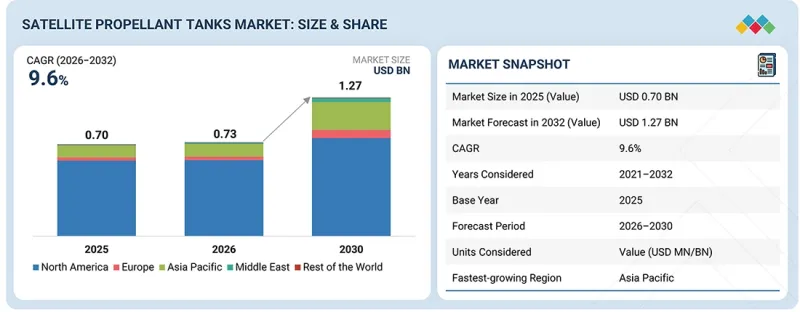

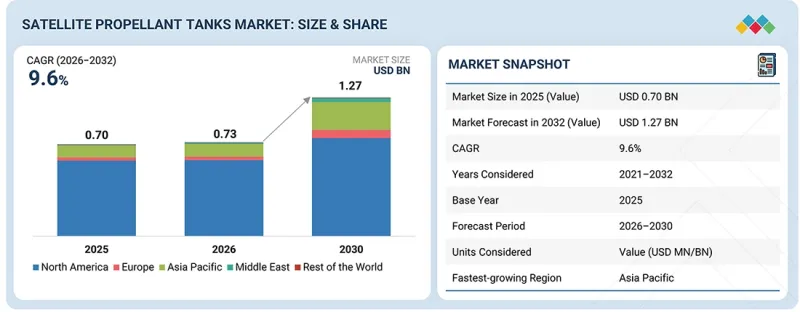

위성용 추진제 탱크 시장 규모는 2026년 7억 3,000만 달러에서 2032년까지 12억 7,000만 달러로 성장하여 CAGR은 9.6%가 될 것으로 예상되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 아키텍처별, 용량별, 위성 질량별, 재료별, 추진제 유형별, 위성 궤도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

수요는 전기 추진 시스템 및 소형 위성 플랫폼의 이용 확대에 따라 경량화, 공간 효율성, 고성능 추진제 탱크 시스템에 대한 요구가 증가하고 있습니다.

티타늄 합금 부문은 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 티타늄이 강도와 무게의 균형이 우수하기 때문입니다. 또한, 내식성이 뛰어나 위성에서 일반적으로 사용되는 많은 추진제에 대해 우수한 성능을 발휘합니다. 티타늄 탱크는 고압을 쉽게 견딜 수 있으며, 우주의 가혹한 환경에서도 안정성을 유지할 수 있습니다. 그 결과, 위성 추진 시스템에 널리 사용되고 있습니다. 특히 신뢰성과 장기적인 임무 수명이 필수적인 임무에서 상업용 및 정부 위성 모두 이 탱크가 선호되고 있습니다.

전기 추진제 부문은 예측 기간 동안 가장 높은 성장률을 나타낼 것으로 예측됩니다. 현재 더 많은 위성이 위치 유지, 궤도 상승 및 장기 궤도 운영을 위해 전기 추진을 사용하고 있습니다. 이러한 시스템은 화학 추진에 비해 추진제 소비량이 현저히 적습니다. 그 결과, 위성 운영 사업자는 미션의 수명을 연장하고 발사 질량을 줄일 수 있습니다. 통신 위성 별자리와 새로운 우주선 플랫폼 증가도 전기 추진 기술의 채택을 촉진하고 있습니다.

북미는 2032년까지 위성용 추진제 탱크 시장을 주도할 것으로 예측됩니다. 이는 주로 이 지역에 위성 제조업체, 추진시스템 개발업체, 발사 사업자가 다수 존재하기 때문입니다. 국가 안보 우주 프로그램에 대한 정부의 막대한 투자도 시장을 지탱하고 있습니다. 한편, 상업용 위성 콘스텔레이션은 지속적으로 확대되고 있으며, 추진 시스템 부품에 대한 안정적인 수요를 창출하고 있습니다. 또한, 이 지역은 높은 수준의 제조 능력과 발전된 우주 기술 분야의 생태계의 혜택을 누리고 있습니다.

조사 범위

이 시장 조사는 위성용 추진제 탱크 시장을 다양한 부문 및 하위 부문에 걸쳐 분석합니다. 그 목적은 각 지역 시장 규모와 성장 가능성을 추정하는 것입니다. 또한, 주요 기업에 대한 상세한 경쟁 분석도 제공하고 있으며, 기업 프로파일, 제품 및 사업 내용, 최근 동향, 전략적 접근 방식 등을 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 위성용 추진제 탱크 시장 전체에 대한 예상 매출액을 제시함으로써 시장 리더와 신규 시장 진출기업을 지원합니다. 또한, 이해관계자들이 경쟁 구도를 이해하고, 자신의 비즈니스를 더 나은 위치에 올려놓으며, 효과적인 시장 진출 전략을 수립할 수 있는 귀중한 인사이트를 얻을 수 있도록 돕습니다. 또한, 이 보고서는 주요 시장 성장 촉진요인 및 과제를 포함한 시장 동향에 대한 인사이트를 제공합니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(위성 발사 횟수 증가, 궤도 기동 필요), 억제요인(긴 인증 주기, 부품 수준의 가격 책정 가시성 부족), 기회 요인(친환경 추진제 전환, 전기 추진의 급속한 보급), 과제(경량화와 구조적 무결성의 균형, 추진제 유형 간 재료 적합성 확보) 확보)

- 시장 침투도 : 시장을 선도하는 주요 기업이 제공하는 위성용 추진제 탱크에 대한 종합적인 정보

- 제품 개발 및 혁신 : 위성용 추진제 탱크 시장 전망 기술, 연구개발 활동 및 신제품 출시에 대한 심층 분석

- 시장 개발: 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화 : 위성용 추진제 탱크 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁 분석 : 위성용 추진제 탱크 시장의 주요 업체들 시장 점유율, 성장 전략, 제품 및 제조 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성 이니셔티브

제8장 고객 현황과 구매 행동

제9장 위성용 추진제 탱크 시장(아키텍처별)

제10장 위성용 추진제 탱크 시장(용량별)

제11장 위성용 추진제 탱크 시장(위성 질량별)

제12장 위성용 추진제 탱크 시장(재료별)

제13장 위성용 추진제 탱크 시장(추진제 유형별)

제14장 위성용 추진제 탱크 시장(위성 궤도별)

제15장 위성용 추진제 탱크 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH 26.05.06The satellite propellant tanks market is expected to grow from USD 0.73 billion in 2026 to USD 1.27 billion by 2032, with a CAGR of 9.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Capacity, Architecture and Region |

| Regions covered | North America, Europe, APAC, RoW |

The demand is driven by the increasing use of electric propulsion and compact satellite platforms, which are boosting the need for lightweight, space-efficient, and high-performance propellant tank systems.

"Titanium alloys are expected to surpass other materials during the forecast period."

The titanium alloys segment is expected to hold the largest share during the forecast period because titanium provides a strong balance between strength and weight. It also has good resistance to corrosion and performs well with many propellants commonly used in satellites. Titanium tanks can easily withstand high pressure and stay stable in the harsh conditions of space. As a result, they are widely used in satellite propulsion systems. Both commercial and government satellites prefer these tanks, especially for missions where reliability and long mission life are crucial.

"Electric propellants are the fastest-growing propellant type during the forecast period."

The electric propellants segment is expected to record the highest growth rate during the forecast period. More satellites are now utilizing electric propulsion for station-keeping, orbit raising, and long-duration maneuvers. These systems consume significantly less propellant compared to chemical propulsion. As a result, satellite operators can extend mission lifespans and reduce launch mass. The increasing number of communication satellite constellations and new spacecraft platforms is also driving the adoption of electric propulsion technologies.

"North America is expected to be the largest regional market during the forecast period."

North America is expected to dominate the satellite propellant tanks market through 2032. This is mainly because the region has a strong presence of satellite manufacturers, propulsion system developers, and launch providers. Large government investments in national security space programs also support the market. Meanwhile, commercial satellite constellations continue to grow, creating steady demand for propulsion components. The region also benefits from advanced manufacturing capabilities and a developed space technology sector ecosystem.

The breakdown of profiles for primary participants in the satellite propellant tanks market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 20%, Middle East - 10%, Rest of the World - 10%

Research Coverage

This market study examines the satellite propellant tanks market across various segments and subsegments. It aims to estimate the market size and growth potential in different regions. The study also provides a detailed competitive analysis of key players, including their company profiles, product and business offerings, recent developments, and strategic approaches.

Reasons to Buy this Report

The report will assist market leaders and new entrants by providing approximate revenue figures for the overall satellite propellant tanks market. It will also help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and develop effective go-to-market strategies. Additionally, the report will offer insights into the market pulse, including key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Key Drivers (increasing satellite launch volumes, need for in-orbit maneuvering), Restraints (long qualification cycles, limited visibility into component-level pricing), Opportunities (shift toward green propellants, rapid adoption of electric propulsion), and Challenges (balancing weight reduction with structural integrity, ensuring material compatibility across propellant types)

- Market Penetration: Comprehensive information on satellite propellant tanks offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and product launches in the satellite propellant tanks market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the satellite propellant tanks market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the satellite propellant tanks market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 DISRUPTIVE TRENDS IN SATELLITE PROPELLANT TANKS MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

- 2.6 TOTAL COST OF OWNERSHIP

- 2.7 BILL OF MATERIALS

- 2.8 BUSINESS MODELS

- 2.8.1 PROGRAM-BASED SUPPLY AGREEMENT

- 2.8.2 INTEGRATED PROPULSION SUBSYSTEM DELIVERY

- 2.8.3 TECHNOLOGY-LED DIFFERENTIATION

- 2.8.4 INDUSTRIAL RAMP-UP AND LONG-TERM PARTNERSHIP

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SATELLITE PROPELLANT TANKS MARKET

- 3.2 SATELLITE PROPELLANT TANKS MARKET, BY ARCHITECTURE

- 3.3 SATELLITE PROPELLANT TANKS MARKET, BY CHEMICAL PROPELLANT TYPE

- 3.4 SATELLITE PROPELLANT TANKS MARKET, BY ELECTRIC PROPELLANT TYPE

- 3.5 SATELLITE PROPELLANT TANKS MARKET, BY SATELLITE ORBIT

- 3.6 SATELLITE PROPELLANT TANKS MARKET, BY CAPACITY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.1.1 DRIVERS

- 4.1.1.1 Increasing satellite launch volumes

- 4.1.1.2 Need for in-orbit maneuvering

- 4.1.1.3 Expanding defense satellite programs

- 4.1.1.4 Standardization of propulsion across satellite platforms

- 4.1.2 RESTRAINTS

- 4.1.2.1 Long qualification cycles

- 4.1.2.2 Limited visibility into component-level pricing

- 4.1.2.3 Dependence on mission-specific customization

- 4.1.3 OPPORTUNITIES

- 4.1.3.1 Shift toward green propellants

- 4.1.3.2 Rapid adoption of electric propulsion

- 4.1.3.3 Surge in domestic satellite manufacturing

- 4.1.3.4 Development of standardized tank platforms

- 4.1.4 CHALLENGES

- 4.1.4.1 Balancing weight reduction with structural integrity

- 4.1.4.2 Ensuring material compatibility across propellant types

- 4.1.4.3 Maintaining consistent quality in high-precision manufacturing

- 4.1.1 DRIVERS

- 4.2 UNMET NEEDS AND WHITE SPACES

- 4.2.1 STRUCTURAL MARGIN CONSERVATISM

- 4.2.2 PROPELLANT UTILIZATION EFFICIENCY

- 4.2.3 QUALIFICATION DUPLICATION

- 4.2.4 SUPPLY CHAIN CONCENTRATION RISK

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INDUSTRIAL GAS AND HYDROGEN STORAGE

- 4.3.2 CRYOGENIC AND ENERGY STORAGE

- 4.3.3 ADVANCED COMPOSITE MANUFACTURING AND AUTOMATION

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL SATELLITES INDUSTRY

- 5.1.3 TRENDS IN GLOBAL SATELLITE PROPELLANT TANKS INDUSTRY

- 5.2 VALUE CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.3.1 PROMINENT COMPANIES

- 5.3.2 PRIVATE AND SMALL ENTERPRISES

- 5.3.3 END USERS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY SATELLITE MASS, 2021-2025

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2025

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 880790)

- 5.5.2 EXPORT SCENARIO (HS CODE 880790)

- 5.6 KEY CONFERENCES AND EVENTS, 2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 NORTHROP GRUMMAN INTEGRATES FLIGHT-QUALIFIED PROPELLANT TANKS INTO MISSION EXTENSION VEHICLES

- 5.8.2 AIRBUS IMPLEMENTS ADVANCED METALLIC AND COMPOSITE TANK CONFIGURATIONS INTO EUROSTAR

- 5.8.3 SPACEX ADOPTS VERTICALLY INTEGRATED MANUFACTURING AND MODULAR TANK ARCHITECTURES FOR STARLINK

- 5.8.4 NASA DEVELOPS NONDESTRUCTIVE EVALUATION TECHNIQUES AND FRACTURE MECHANICS MODELING FOR SPACE MISSION

- 5.8.5 MAXAR IMPLEMENTS OPTIMIZED METALLIC TANK GEOMETRIES IN GEO COMMUNICATION SATELLITES

- 5.9 IMPACT OF 2025 US TARIFF

- 5.9.1 KEY TARIFF RATES

- 5.9.2 PRICE IMPACT ANALYSIS

- 5.9.3 IMPACT ON COUNTRY/REGION

- 5.9.3.1 US

- 5.9.3.2 Europe

- 5.9.3.3 Asia Pacific

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 COMPOSITE OVERWRAPPED PRESSURE VESSELS

- 6.1.2 PROPELLANT MANAGEMENT DEVICES

- 6.1.3 LIGHTWEIGHT METALLIC AND TITANIUM ALLOY TANKS

- 6.1.4 ADDITIVE MANUFACTURING FOR STRUCTURAL AND INTERNAL COMPONENTS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ELECTRIC PROPULSION SYSTEMS

- 6.2.2 PRESSURIZATION AND FEED SYSTEMS

- 6.2.3 STRUCTURAL HEALTH MONITORING AND DIGITAL TWIN TECHNOLOGIES

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI/GEN AI

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES

- 6.5.3 CASE STUDIES OF AI IMPLEMENTATION

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT AI/GEN AI

- 6.6 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT REDUCTION

- 7.2.2 ECO-APPLICATIONS

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE INDUSTRIES

9 SATELLITE PROPELLANT TANKS MARKET, BY ARCHITECTURE

- 9.1 INTRODUCTION

- 9.2 POSITIVE-EXPULSION TANKS

- 9.2.1 RELIABLE PROPELLANT DELIVERY REQUIREMENTS TO DRIVE MARKET

- 9.2.2 USE CASE: POSITIVE-EXPULSION PROPELLANT TANK APPLICATION IN SENTINEL-2 FOR ORBIT MANEUVERING

- 9.3 PMD TANKS

- 9.3.1 DEMAND FOR HIGHER DELTA-V CAPABILITIES AND EXTENDED OPERATIONAL LIFETIMES TO DRIVE MARKET

- 9.3.2 USE CASE: PMD-BASED PROPELLANT TANK INTEGRATION IN INTELSAT 29E FOR GEO ORBIT RAISING AND STATION-KEEPING

- 9.4 HIGH-PRESSURE VESSELS

- 9.4.1 RAPID ADOPTION OF ELECTRIC PROPULSION SYSTEMS TO DRIVE MARKET

- 9.4.2 USE CASE: HIGH-PRESSURE XENON PROPELLANT TANK DEPLOYMENT IN EUTELSAT 172B FOR ELECTRIC ORBIT RAISING

10 SATELLITE PROPELLANT TANKS MARKET, BY CAPACITY

- 10.1 INTRODUCTION

- 10.2 <5 L

- 10.2.1 PROLIFERATION OF PROPULSION-ENABLED CUBESATS TO DRIVE MARKET

- 10.3 5-50 L

- 10.3.1 RISE OF SYNTHETIC APERTURE RADAR AND DEFENSE SURVEILLANCE SATELLITES TO DRIVE MARKET

- 10.4 51-100 L

- 10.4.1 HEIGHTENED PROPELLANT STORAGE REQUIREMENTS IN SMALL SATELLITE MISSIONS TO DRIVE MARKET

- 10.5 101-250 L

- 10.5.1 EXPANDING EARTH OBSERVATION, METEOROLOGY, AND NAVIGATION AUGMENTATION MISSIONS TO DRIVE MARKET

- 10.6 251-500 L

- 10.6.1 SURGE IN DEMAND FOR BROADBAND CONNECTIVITY TO DRIVE MARKET

- 10.7 501-1,000 L

- 10.7.1 HIGHER PROPELLANT MASS FRACTIONS PER SPACECRAFT TO DRIVE MARKET

- 10.8 >1,000 L

- 10.8.1 PREDOMINANCE IN HEAVY GEOSTATIONARY SATELLITES AND FLAGSHIP COMMUNICATIONS PLATFORMS TO DRIVE MARKET

11 SATELLITE PROPELLANT TANKS MARKET, BY SATELLITE MASS

- 11.1 INTRODUCTION

- 11.2 CLASSIFICATION OF SATELLITE PROPELLANT TANKS BY END USER

- 11.2.1 COMMERCIAL

- 11.2.2 GOVERNMENT & CIVIL

- 11.2.3 DEFENSE

- 11.3 SMALL (1-1,200 KG)

- 11.3.1 LOWER LAUNCH COSTS AND FLEXIBLE DEPLOYMENT STRATEGIES TO DRIVE MARKET

- 11.3.2 USE CASE: PRESSURIZED HYDRAZINE PROPELLANT TANK UTILIZATION IN SENTINEL-2 FOR SUSTAINED ORBIT MAINTENANCE

- 11.4 MEDIUM (1,201-2,000 KG)

- 11.4.1 NEED FOR FREQUENT MANEUVER CYCLES AND STABLE PROPELLANT DELIVERY TO DRIVE MARKET

- 11.4.2 USE CASE: HYDRAZINE PROPELLANT TANK IN TERRASAR-X FOR PRECISION ORBIT CONTROL AND LONG-TERM MISSION RELIABILITY

- 11.5 LARGE (>2,000 KG)

- 11.5.1 GROWING DEMAND FOR STRATEGIC NATIONAL SPACE INFRASTRUCTURE TO DRIVE MARKET

- 11.5.2 USE CASE: HIGH-CAPACITY PRESSURIZED PROPELLANT TANK IN VIASAT-2 FOR GEO ORBIT RAISING

12 SATELLITE PROPELLANT TANKS MARKET, BY MATERIAL

- 12.1 INTRODUCTION

- 12.2 ALUMINUM ALLOYS

- 12.2.1 LIGHTWEIGHT STRUCTURAL PROPERTIES TO DRIVE MARKET

- 12.2.2 USE CASE: ALUMINUM PROPELLANT TANK INTEGRATION IN SKYSAT FOR EFFICIENT CONSTELLATION MANEUVERING

- 12.3 TITANIUM ALLOYS

- 12.3.1 SUPERIOR STRENGTH-TO-WEIGHT RATIO AND CHEMICAL COMPATIBILITY TO DRIVE MARKET

- 12.3.2 USE CASE: TITANIUM ALLOY PROPELLANT TANK IN SENTINEL SATELLITES FOR RELIABLE EARTH OBSERVATION MANEUVERING

- 12.4 STAINLESS STEEL & NICKEL ALLOYS

- 12.4.1 HIGH-PRESSURE TOLERANCE AND CHEMICAL STABILITY TO DRIVE MARKET

- 12.4.2 USE CASE: HIGH-STRENGTH METALLIC PROPELLANT TANK IN INTELSAT 29E FOR GEO ORBIT RAISING

- 12.5 COMPOSITE MATERIALS

- 12.5.1 EMPHASIS ON MASS EFFICIENCY AND PROPULSION PERFORMANCE TO DRIVE MARKET

- 12.5.2 USE CASE: COMPOSITE OVERWRAPPED HIGH-PRESSURE XENON TANK IN EUTELSAT 172B FOR ELECTRIC PROPULSION OPERATIONS

- 12.6 OTHER MATERIALS

13 SATELLITE PROPELLANT TANKS MARKET, BY PROPELLANT TYPE

- 13.1 INTRODUCTION

- 13.2 CHEMICAL PROPELLANTS

- 13.2.1 HIGH THRUST REQUIREMENTS AND PROVEN FLIGHT HERITAGE TO DRIVE MARKET

- 13.2.2 HYDRAZINE

- 13.2.3 HTP

- 13.2.4 GREEN MONOPROPELLANTS

- 13.2.5 OTHERS

- 13.3 ELECTRIC PROPELLANTS

- 13.3.1 EXTENSIVE USE OF ELECTRIC PROPULSION IN MODERN SATELLITE MISSIONS TO DRIVE MARKET

- 13.3.2 XENON

- 13.3.3 KRYPTON

- 13.3.4 ARGON

- 13.3.5 OTHERS

- 13.4 COLD-GAS PROPELLANTS

- 13.4.1 RELIABILITY AND LOW COMPLEXITY IN SMALL SATELLITE MISSIONS TO DRIVE MARKET

- 13.5 OTHER PROPELLANTS

14 SATELLITE PROPELLANT TANKS MARKET, BY SATELLITE ORBIT

- 14.1 INTRODUCTION

- 14.2 LEO

- 14.2.1 RISING SATELLITE DEPLOYMENT TO DRIVE MARKET

- 14.3 MEO & GEO

- 14.3.1 INTEGRATION OF LARGER PROPELLANT TANKS TO DRIVE MARKET

15 SATELLITE PROPELLANT TANKS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Contracts reinforcing propulsion system demand and commercial constellation expansion to drive market

- 15.2.2 CANADA

- 15.2.2.1 National space programs and active participation in international missions to drive market

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 UK

- 15.3.1.1 Domestic focus on in-orbit servicing and refueling technologies to drive market

- 15.3.2 GERMANY

- 15.3.2.1 Strong industrial base and advanced propulsion research capabilities to drive market

- 15.3.3 ITALY

- 15.3.3.1 Institutional alignment with European propulsion programs to drive market

- 15.3.4 RUSSIA

- 15.3.4.1 Long-standing national space programs and vertically integrated aerospace enterprises to drive market

- 15.3.5 FRANCE

- 15.3.5.1 Robust national space policy framework and deep industrial expertise to drive market

- 15.3.1 UK

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Expansion of LEO constellations and continuous deployment of geostationary satellites to drive market

- 15.4.2 INDIA

- 15.4.2.1 Growing national satellite programs and private sector participation to drive market

- 15.4.3 JAPAN

- 15.4.3.1 Modernization of satellite fleets and investments in next-generation propulsion systems to drive market

- 15.4.4 SOUTH KOREA

- 15.4.4.1 Transition toward propulsion-enabled satellite autonomy to drive market

- 15.4.5 AUSTRALIA

- 15.4.5.1 Development of domestic satellite manufacturing capabilities to drive market

- 15.4.1 CHINA

- 15.5 MIDDLE EAST

- 15.5.1 GCC

- 15.5.1.1 UAE

- 15.5.1.1.1 Transition toward advanced propulsion architectures to drive market

- 15.5.1.2 Saudi Arabia

- 15.5.1.2.1 National satellite expansion initiatives to drive market

- 15.5.1.1 UAE

- 15.5.2 ISRAEL

- 15.5.2.1 Increasing deployment of compact, defense-focused satellites to drive market

- 15.5.3 TURKEY

- 15.5.3.1 Substantial investments in indigenous satellite programs and local manufacturing to drive market

- 15.5.1 GCC

- 15.6 REST OF THE WORLD

- 15.6.1 LATIN AMERICA

- 15.6.1.1 Rapid integration of propulsion-enabled small satellites to drive market

- 15.6.2 AFRICA

- 15.6.2.1 Expanding connectivity missions to drive market

- 15.6.1 LATIN AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 16.3 REVENUE ANALYSIS, 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 BRAND/PRODUCT COMPARISON

- 16.6 COMPANY VALUATION AND FINANCIAL METRICS

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Architecture footprint

- 16.7.5.4 Material footprint

- 16.7.5.5 Propellant type footprint

- 16.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING

- 16.8.5.1 List of start-ups/SMEs

- 16.8.5.2 Competitive benchmarking of start-ups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 16.9.2 DEALS

- 16.9.3 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 MT AEROSPACE AG

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.3.2 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 AIRBUS

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 MnM view

- 17.1.2.3.1 Right to win

- 17.1.2.3.2 Strategic choices

- 17.1.2.3.3 Weaknesses and competitive threats

- 17.1.3 NORTHROP GRUMMAN

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Other developments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 ARIANEGROUP

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 L3HARRIS TECHNOLOGIES, INC.

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches/developments

- 17.1.7 INFINITE COMPOSITES TECHNOLOGIES

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches/developments

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Other developments

- 17.1.8 MOOG INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Other developments

- 17.1.9 NAMMO AS

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches/developments

- 17.1.10 SCORPIUS SPACE LAUNCH COMPANY

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches/developments

- 17.1.10.3.2 Deals

- 17.1.11 ANTRIX CORPORATION LIMITED

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.12 IHI AEROSPACE CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Other developments

- 17.1.13 APPLIED AEROSPACE & DEFENSE

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.14 VIVACE INTERNATIONAL CORPORATION

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.15 EATON

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Other developments

- 17.1.1 MT AEROSPACE AG

- 17.2 OTHER PLAYERS

- 17.2.1 LMO

- 17.2.2 STANDEX INTERNATIONAL CORPORATION

- 17.2.3 HINDUSTAN AERONAUTICS LIMITED

- 17.2.4 DAWN AEROSPACE

- 17.2.5 STEELHEAD COMPOSITES, INC.

- 17.2.6 SIERRA SPACE CORPORATION

- 17.2.7 BENCHMARK SPACE SYSTEMS

- 17.2.8 MJOLNIR SPACEWORKS CO., LTD.

- 17.2.9 STEAMJET

- 17.2.10 RESHETNEV

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary sources

- 18.1.2.2 Key data from primary sources

- 18.1.2.3 Breakdown of primary interviews

- 18.1.1 SECONDARY DATA

- 18.2 FACTOR ANALYSIS

- 18.2.1 DEMAND-SIDE INDICATORS

- 18.2.2 SUPPLY-SIDE INDICATORS

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 BOTTOM-UP APPROACH

- 18.3.1.1 Market size estimation methodology (demand side)

- 18.3.2 TOP-DOWN APPROACH

- 18.3.1 BOTTOM-UP APPROACH

- 18.4 DATA TRIANGULATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS