|

시장보고서

상품코드

2007116

디지털 자산 관리 시장 : 제공별, 용도별, 자산 유형별, 조직 규모별, 산업별, 지역별 - 세계 예측(-2031년)Digital Asset Management Market by Offering (Solutions and Services), Application (Brand & Marketing Asset Management, Media Production & Broadcast Asset Management), Asset Type, Organization Size, Vertical, and Region - Global Forecast to 2031 |

||||||

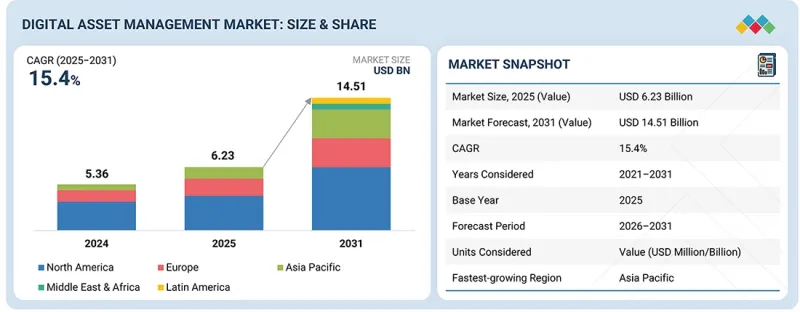

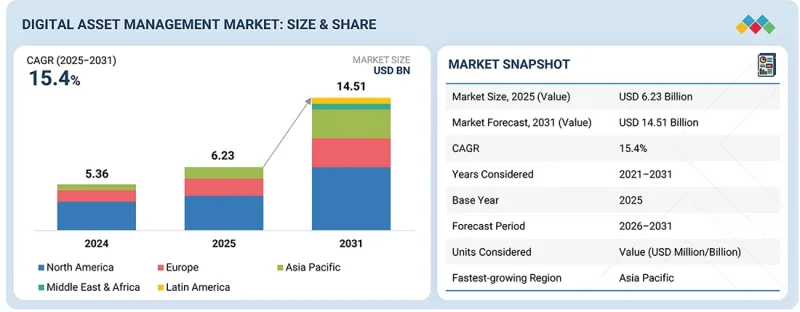

세계의 디지털 자산 관리 시장은 빠르게 확대하고 있으며, 시장 규모는 2025년 약 62억 3,000만 달러에서 2031년까지 145억 1,000만 달러로, CAGR 15.4%로 확대될 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제공, 자산 유형, 업무 기능, 용도, 도입 형태, 자산 유형, 조직 규모, 업종 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

세계 디지털 자산 관리(DAM) 시장은 기업 전반의 디지털 컨텐츠 양 증가, 중앙 집중식 저장 및 검색에 대한 수요 증가, 옴니채널 고객 접점 전반에 걸친 일관된 컨텐츠 배포의 필요성에 힘입어 꾸준히 성장하고 있습니다. 기업들은 이미지, 동영상, 문서, 디자인 파일, 기타 리치 미디어 자산을 관리하는 동시에 마케팅, 크리에이티브, 영업, E-Commerce 각 팀 간의 협업을 강화하기 위해 디지털 자산 관리 플랫폼을 도입하고 있습니다. 자동 태깅, 메타데이터 강화, 지능형 검색, 컨텐츠 분류, 자산 추천 등 AI를 활용한 기능 추가를 통해 플랫폼의 효율성이 더욱 향상되고 자산의 발견 가능성이 높아졌습니다. 각 벤더들은 또한 확장 가능한 컨텐츠 운영을 지원하기 위해 컨텐츠 관리, 제품 정보 관리, 고객 경험, 워크플로우 자동화 플랫폼과의 연계를 강화하고 있습니다. 그러나 레거시 시스템 간 통합의 복잡성, 메타데이터 표준화 문제, 디지털 권리 거버넌스에 대한 우려, 규제 환경에서의 데이터 보안 요구사항 등이 시장 성장을 제약하고 있습니다. 이러한 제약에도 불구하고, 컨텐츠 재사용, 시장 출시 시간 단축, 지능형 자산 라이프사이클 관리에 대한 지속적인 관심은 기업 전반에 걸쳐 디지털 자산 관리 플랫폼의 지속적인 도입을 뒷받침할 것으로 예상됩니다.

"도입 형태별로는 클라우드 부문이 예측 기간 동안 더 높은 CAGR로 성장할 것으로 예상됩니다."

클라우드 기반 DAM 솔루션은 조직이 인터넷을 통해 이미지, 동영상, 문서, 크리에이티브 파일 등의 디지털 자산을 안전하게 저장, 관리, 정리, 배포할 수 있는 중앙 집중식 플랫폼을 제공합니다. 이러한 솔루션은 클라우드 컴퓨팅 인프라를 활용하며, 사용자는 인터넷 연결만 있으면 언제, 어디서나, 어떤 기기에서든 자산에 접근할 수 있습니다. 클라우드 기반 DAM 시스템은 메타데이터 태깅, 버전 관리, 권한 관리, 고급 검색 기능 등의 기능을 갖추고 있어 효율적인 자산 검색과 팀 협업을 촉진합니다. 클라우드 기반 DAM 솔루션은 확장 가능한 스토리지 옵션과 자동 백업을 통해 비용이 많이 드는 온프레미스 인프라의 필요성을 없애고, 증가하는 디지털 자산 라이브러리에 유연하게 대응할 수 있습니다. 또한, 다른 클라우드 기반 도구 및 애플리케이션과 원활하게 통합되어 워크플로우의 효율성을 높이고 다양한 채널에서 원활한 컨텐츠 제작 및 배포를 가능하게 합니다.

"산업별로는 미디어 및 엔터테인먼트가 가장 큰 시장 점유율을 차지할 것으로 전망"

미디어 및 엔터테인먼트 산업은 스트리밍, 방송, 출판, 음악, 스포츠, 스튜디오 워크플로우 등에서 방대한 양의 고부가가치 디지털 자산을 생성, 관리, 현지화, 배포, 수익화하기 때문에 예측 기간 동안 가장 큰 점유율을 차지할 것으로 예상됩니다. DAM 플랫폼은 동영상, 이미지, 오디오, 그래픽, 자막, 자막, 예고편, 아카이브 자산을 중앙에서 관리하고, 여러 포맷, 지역, 공개 시기에 걸친 메타데이터 관리, 검색성, 버전 관리, 승인 워크플로우, 권한 관리를 향상시켜야 하는 요구가 점점 더 커지고 있습니다. 예를 들어, 2024년 4월 IAB는 미국의 디지털 동영상 광고 지출이 2023년 전년 대비 15% 증가한 540억 달러에 달할 것이며, 2024년에는 629억 달러에 달할 것으로 예상했습니다. 이는 동영상 중심의 미디어 운영 규모가 확대되고 커넥티드 TV, 소셜 동영상, 온라인 동영상 환경 전반에서 캠페인 자산을 효율적으로 관리해야 할 필요성이 높아진 것을 반영합니다. 또한, 2025년 3월 IFPI는 2024년 전 세계 음반 음악 수익이 296억 달러에 달할 것이며, 그 중 스트리밍이 총 수익의 69.0%를 차지할 것이라고 발표하며, 디지털 유통 컨텐츠 생태계로의 전환이 지속되고 있음을 강조했습니다. 이러한 디지털 컨텐츠 제작 및 유통의 확대는 컨텐츠의 재사용, 신속한 패키징, 다국어 배포, 아카이브의 수익화, 그리고 라이선스, 기한, 지역별 이용권의 엄격한 관리를 위해 미디어 기업의 DAM 도입을 가속화하고 있습니다.

"북미가 가장 큰 시장 점유율을 차지하고 있으며, 이는 미국과 캐나다 전역의 기업 컨텐츠의 광범위한 디지털화, 옴니채널 마케팅의 성숙도, AI를 활용한 컨텐츠 운영 플랫폼의 채택 확대에 기인합니다"

북미 디지털 자산 관리 시장은 이 지역의 성숙한 디지털 커머스, 마케팅, 미디어 및 엔터프라이즈 컨텐츠 생태계에 의해 주도되고 있습니다. 미국 및 캐나다 기업들은 웹사이트, 마켓플레이스, 앱, 사내 협업 환경에서 대량의 이미지, 동영상, 제품 컨텐츠, 캠페인 크리에이티브, 브랜드 자산을 관리하고 있으며, 중앙 집중식 자산 스토리지, 메타데이터 관리, 검색, 버전 관리, 권한 거버넌스에 대한 강력한 수요를 창출하고 있습니다. 권리 거버넌스에 대한 강력한 수요를 창출하고 있습니다. 또한, 조직이 컨텐츠 관리, E-Commerce, 제품 정보 관리, 워크플로우 시스템과 이러한 플랫폼을 통합하고, 컨텐츠 재사용을 개선하고, 옴니채널 배포를 가속화함에 따라 DAM 도입이 증가하고 있습니다. 예를 들어, 2026년 3월 미국 인구조사국은 2025년 미국 소매 E-Commerce 매출이 총 1조 2,337억 달러에 달해 전체 소매 매출의 16.4%를 차지했다고 발표했습니다. 또한 2025년 7월, 국제무역국은 2024년 12월 캐나다의 총 소매 매출에서 E-Commerce가 차지하는 비중이 6.1%로, 온라인 소매 매출은 약 31억 4,000만 달러에 달했다고 발표했습니다. 이러한 디지털 커머스의 규모 확대는 기업이 생성, 업데이트, 현지화, 각 채널에 배포해야 하는 제품 이미지, 동영상, 배너, 카탈로그, 홍보용 자산의 양을 직접적으로 증가시키고 있습니다. 그 결과, 기업들은 DAM 플랫폼에 대한 투자를 확대하고, 자산의 발견성을 높이고, 중복성을 줄이고, 브랜드 일관성을 유지하며, 소매, 미디어, 소비자 워크플로우 전반에 걸쳐 컨텐츠 공개를 가속화하고 있습니다. 이러한 추세에 따라 북미에서의 플랫폼 도입이 더욱 가속화되고 있으며, DAM은 보다 광범위한 컨텐츠 운영 및 디지털 경험 인프라의 핵심 계층으로 자리매김하고 있습니다.

세계의 디지털 자산 관리 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황

제8장 고객 상황·구매 행동

제9장 디지털 자산 관리 시장 : 제공별

제10장 디지털 자산 관리 시장 : 도입 형태별

제11장 디지털 자산 관리 시장 : 자산별

제12장 디지털 자산 관리 시장 : 사업 기능별

제13장 디지털 자산 관리 시장 : 용도별

제14장 디지털 자산 관리 시장 : 조직 규모별

제15장 디지털 자산 관리 시장 : 산업별

제16장 디지털 자산 관리 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSM 26.04.28The global digital asset management market is expanding rapidly, with a projected market size rising from about USD 6.23 billion in 2025 to USD 14.51 billion by 2031, at a CAGR of 15.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Offering, Asset Type, Business Function, Application, Deployment Type, Asset type, Organization Size, Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The global digital asset management market is growing steadily, driven by rising volumes of digital content across enterprises, increasing demand for centralized storage and retrieval, and the need for consistent content delivery across omnichannel customer touchpoints. Organizations are adopting digital asset management platforms to manage images, videos, documents, design files, and other rich media assets while improving collaboration across marketing, creative, sales, and e-commerce teams. The addition of AI-enabled capabilities such as auto-tagging, metadata enrichment, intelligent search, content classification, and asset recommendations is further enhancing platform efficiency and improving asset discoverability. Vendors are also strengthening integrations with content management, product information management, customer experience, and workflow automation platforms to support scalable content operations. However, market growth is constrained by integration complexity across legacy systems, challenges with metadata standardization, digital rights governance concerns, and data security requirements in regulated environments. Despite these restraints, the continued emphasis on content reuse, faster time-to-market, and intelligent asset lifecycle management is expected to support sustained adoption of digital asset management platforms across enterprises.

"By deployment type, the cloud segment is expected to grow at a higher CAGR during the forecast period. "

Cloud-based DAM solutions offer a centralized platform for organizations to securely store, manage, organize, and distribute digital assets such as images, videos, documents, and creative files over the internet. These solutions leverage cloud computing infrastructure, enabling users to access their assets anytime, anywhere, and from any device with an internet connection. Cloud-based DAM systems offer features such as metadata tagging, version control, permissions management, and advanced search capabilities, facilitating efficient asset retrieval and team collaboration. With scalable storage options and automatic backups, cloud-based DAM solutions eliminate the need for costly on-premises infrastructure and provide flexibility to accommodate growing digital asset libraries. Additionally, they often integrate seamlessly with other cloud-based tools and applications, enhancing workflow efficiency and enabling seamless content creation and distribution across various channels.

"By vertical, media & entertainment is expected to hold the largest market share."

Media & entertainment is expected to hold the largest share of the digital asset management market during the forecast period because the industry creates, manages, localizes, distributes, and monetizes very large volumes of high-value digital assets across streaming, broadcasting, publishing, music, sports, and studio workflows. DAM platforms are increasingly required to centralize video, image, audio, graphics, subtitle, trailer, and archive assets while improving metadata management, searchability, version control, approval workflows, and rights governance across multiple formats, regions, and release windows. For instance, in April 2024, IAB reported that US digital video ad spend increased 15% year over year to USD 54 billion in 2023 and was projected to reach USD 62.9 billion in 2024, reflecting the rising scale of video-led media operations and the growing need to manage campaign assets efficiently across connected TV, social video, and online video environments. For instance, in March 2025, IFPI reported that global recorded music revenues reached USD 29.6 billion in 2024, with streaming accounting for 69.0% of total revenues, highlighting the continued shift toward digitally distributed content ecosystems. This expansion in digital content production and distribution is accelerating DAM adoption across media enterprises to support content reuse, faster packaging, multilingual delivery, archive monetization, and tighter control over licensing, expiry, and regional usage rights.

"North America holds the largest share of the digital asset management market, driven by widespread enterprise content digitization, strong omnichannel marketing maturity, and rising adoption of AI-enabled content operations platforms across the US and Canada."

The digital asset management market in North America is driven by the region's mature digital commerce, marketing, media, and enterprise content ecosystems. Enterprises in the US and Canada manage large volumes of images, videos, product content, campaign creatives, and branded assets across websites, marketplaces, apps, and internal collaboration environments, creating strong demand for centralized asset storage, metadata control, search, versioning, and rights governance. DAM adoption is also increasing as organizations integrate these platforms with content management, e-commerce, product information management, and workflow systems to improve content reuse and accelerate omnichannel delivery. For instance, in March 2026, the US Census Bureau reported that US retail e-commerce sales totaled USD 1,233.7 billion in 2025, accounting for 16.4% of total retail sales. In addition, in July 2025, the International Trade Administration stated that e-commerce accounted for 6.1% of total Canadian retail sales in December 2024, with online retail sales totaling approximately USD 3.14 billion. This scale of digital commerce directly increases the volume of product images, videos, banners, catalogs, and promotional assets that enterprises must create, update, localize, and distribute across channels. As a result, organizations are investing more in DAM platforms to improve asset discoverability, reduce duplication, maintain brand consistency, and accelerate content publishing across retail, media, and consumer-facing workflows. These dynamics continue to strengthen platform adoption in North America, where DAM is increasingly positioned as a core layer within broader content operations and digital experience infrastructure.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the digital asset management market.

- By Company: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: Directors - 35%, Managers - 25%, and others - 40%

- By Region: North America - 35%, Europe - 15%, Asia Pacific - 40%, Middle East & Africa - 5%, and Latin America - 5%

The report includes a study of key players in the digital asset management market. It profiles major vendors in the digital asset management market. The major market players include Adobe (US), OpenText (Canada), Cognizant (US), Cloudinary (Israel), Aprimo (US), Bynder (Netherlands), Hyland (US), Veeva Systems (US), Acquia (US), Frontify (Switzerland), Sitecore (US), Pattern (US), Esko (Belgium), Papirfly (Norway), censhare (Germany), CELUM (Austria), Macrocentral (India), Extensis (US), PhotoShelter (US), Chetu (US), IntelligenceBank (Australia), Orange Logic (US), Wedia (France), Asset Bank (UK), Brandfolder (US), MediaValet (Canada), DemoUp Cliplister (Germany), Filecamp (Denmark), WoodWing (Netherlands), IgniteTech (US), and ImageKit.io (India).

Research Coverage

This research report categorizes the digital asset management market based on based on offering (solutions [traditional digital asset management, AI-powered digital asset management], services [professional services (implementation & integration, training & consulting), managed services (support & maintenance)]), deployment type (on-premises, cloud), asset type (video & audio assets, document assets, web & interactive assets, creative & design assets), application (brand & marketing asset management, product content management, digital rights governance & compliance, media production & broadcast asset management, enterprise content & knowledge management, others), business function (human resources, marketing & sales, IT & operations, finance & accounting), organization size (large enterprises, SMEs), vertical (BFSI, retail & consumer goods, healthcare & life sciences, IT & ITeS, telecommunications, media & entertainment, manufacturing, government & public sector, travel & hospitality, education, other verticals), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the DAM market. A detailed analysis of key industry players was conducted to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments in the DAM market. This report also covers the competitive analysis of upcoming startups in the DAM market ecosystem.

Reason to buy this report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall DAM market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Exploding volumes of rich media assets increasing need for centralized management, Generative AI accelerating enterprise demand for scalable digital content production, Growth of digital commerce ecosystems requiring structured product media management platforms, Increasing demand for faster campaign localization across geographically distributed marketing teams), restraints (Complex metadata structuring requirements slowing enterprise-wide digital asset standardization initiatives), opportunities (AI-driven asset intelligence enabling predictive content reuse and automated creative workflows, Expansion of DAM platforms into enterprise content supply chain orchestration solutions, Demand for composable architectures enabling headless DAM integration across digital experience stacks, Growing need for rights-managed content distribution across global partner and creator ecosystems), and challenges (Managing global content compliance across copyright, licensing, and regional regulations, Ensuring high-performance asset delivery across distributed multi-cloud digital infrastructure, Fragmented martech ecosystems limiting seamless interoperability between DAM and content platforms)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the DAM market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the DAM market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the DAM market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as Adobe (US), OpenText (Canada), Cognizant (US), Cloudinary (Israel), Aprimo (US), Bynder (Netherlands), Hyland (US), Veeva Systems (US), Acquia (US), Frontify (Switzerland), Sitecore (US), Pattern (US), Esko (Belgium), Papirfly (Norway), censhare (Germany), CELUM (Austria), Macrocentral (India), Extensis (US), PhotoShelter (US), Chetu (US), IntelligenceBank (Australia), Orange Logic (US), Wedia (France), Asset Bank (UK), Brandfolder (US), MediaValet (Canada), DemoUp Cliplister (Germany), Filecamp (Denmark), WoodWing (Netherlands), IgniteTech (US), and ImageKit.io (India). The report also helps stakeholders understand the DAM market's pulse and provides information on key market drivers, restraints, challenges, and opportunities

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DIGITAL ASSET MANAGEMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIGITAL ASSET MANAGEMENT MARKET

- 3.2 DIGITAL ASSET MANAGEMENT MARKET, BY OFFERING

- 3.3 DIGITAL ASSET MANAGEMENT MARKET, BY SOLUTION

- 3.4 DIGITAL ASSET MANAGEMENT MARKET, BY ASSET

- 3.5 DIGITAL ASSET MANAGEMENT MARKET, BY APPLICATION

- 3.6 DIGITAL ASSET MANAGEMENT MARKET, BY BUSINESS FUNCTION

- 3.7 DIGITAL ASSET MANAGEMENT MARKET, BY DEPLOYMENT TYPE

- 3.8 DIGITAL ASSET MANAGEMENT MARKET, BY ORGANIZATION SIZE

- 3.9 DIGITAL ASSET MANAGEMENT MARKET, BY VERTICAL

- 3.10 DIGITAL ASSET MANAGEMENT MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expanding volumes of rich media assets

- 4.2.1.2 Rising applications of generative AI

- 4.2.1.3 Growth of digital commerce ecosystems

- 4.2.1.4 Increasing demand for faster campaign localization

- 4.2.2 RESTRAINTS

- 4.2.2.1 Complex metadata structuring requirements

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of AI-driven asset intelligence

- 4.2.3.2 Expansion of DAM platforms into enterprise content supply chain orchestration

- 4.2.3.3 Demand for composable digital experience architectures

- 4.2.3.4 Growing need for rights-managed content distribution

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing content compliance across copyright, licensing, and regional regulations

- 4.2.4.2 Ensuring high-performance asset delivery across distributed multi-cloud digital infrastructure

- 4.2.4.3 Fragmented MarTech ecosystems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DIGITAL ASSET MANAGEMENT MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Digital asset management business models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN GLOBAL WEB CONTENT MANAGEMENT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ENTERPRISE CONTENT MANAGEMENT INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY SOFTWARE, 2026

- 5.5.2 INDICATIVE PRICING ANALYSIS OF PRODUCTS, BY VENDOR, 2026

- 5.6 KEY CONFERENCES AND EVENTS, 2026

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 HACHETTE BOOK GROUP MODERNIZES DIGITAL ASSET OPERATIONS WITH APRIMO DIGITAL ASSET MANAGEMENT PLATFORM

- 5.9.2 AMNESTY INTERNATIONAL STRENGTHENS SECURE DIGITAL MEDIA MANAGEMENT WITH ASSET BANK DIGITAL ASSET MANAGEMENT PLATFORM

- 5.9.3 HOOTSUITE IMPROVES GLOBAL CONTENT MANAGEMENT AND BRAND CONSISTENCY WITH ACQUIA DAM PLATFORM

- 5.9.4 LIONSGATE CENTRALIZES GLOBAL MARKETING ASSETS WITH ORANGE LOGIC DIGITAL ASSET MANAGEMENT PLATFORM

- 5.9.5 INSPIRE BRANDS ACCELERATES MULTI-BRAND DIGITAL CONTENT OPERATIONS USING BYNDER DIGITAL ASSET MANAGEMENT PLATFORM

- 5.10 IMPACT OF 2025 US TARIFF - DIGITAL ASSET MANAGEMENT MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON VERTICALS

- 5.10.5.1 Media & entertainment

- 5.10.5.2 Retail & consumer goods

- 5.10.5.3 BFSI

- 5.10.5.4 IT & ITeS

- 5.10.5.5 Manufacturing

- 5.10.5.6 Government & public sector

- 5.10.5.7 Healthcare & life sciences

- 5.10.5.8 Travel & hospitality

- 5.10.5.9 Education

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Cloud-native digital asset management architecture

- 6.1.1.2 API-first integration and composable content infrastructure

- 6.1.1.3 Automated metadata management and content indexing

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Content delivery network (CDN) integration

- 6.1.2.2 Digital rights management (DRM) and usage governance

- 6.1.2.3 Workflow automation and creative collaboration platforms

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Product information management (PIM) platforms

- 6.1.3.2 Customer data platforms (CDP)

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM (2026-2028) | CLOUD DAM MODERNIZATION & CONTENT GOVERNANCE

- 6.2.1.1 Focus Areas:

- 6.2.1.1.1 Material Development

- 6.2.1.1.2 Product Innovations

- 6.2.1.1.3 Market Adoption

- 6.2.1.1 Focus Areas:

- 6.2.2 MID-TERM (2028-2031) | COMPOSABLE CONTENT OPERATIONS & OMNICHANNEL DELIVERY ECOSYSTEM

- 6.2.2.1 Focus Areas:

- 6.2.2.1.1 Material Development

- 6.2.2.1.2 Product Innovations

- 6.2.2.1.3 Market Adoption

- 6.2.2.1 Focus Areas:

- 6.2.3 LONG-TERM (2031-2035+) | INTELLIGENT CONTENT ECOSYSTEMS & GLOBAL BRAND INFRASTRUCTURE

- 6.2.3.1 Focus Areas:

- 6.2.3.1.1 Material Development

- 6.2.3.1.2 Product Innovations

- 6.2.3.1.3 Market Adoption

- 6.2.3.1 Focus Areas:

- 6.2.1 SHORT-TERM (2026-2028) | CLOUD DAM MODERNIZATION & CONTENT GOVERNANCE

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-ORCHESTRATED CONTENT INTELLIGENCE PLATFORMS (GENERATIVE METADATA & AUTONOMOUS ASSET TAGGING)

- 6.4.2 OMNICHANNEL CONTENT ACTIVATION HUBS (HEADLESS DAM FOR MULTIPLATFORM EXPERIENCE DELIVERY)

- 6.4.3 DIGITAL RIGHTS GOVERNANCE AND AUTOMATED BRAND COMPLIANCE PLATFORMS

- 6.4.4 REAL-TIME MEDIA TRANSFORMATION AND DYNAMIC ASSET DELIVERY ENGINES

- 6.4.5 CONTENT SUPPLY CHAIN AUTOMATION AND MARKETING OPERATIONS INTEGRATION

- 6.5 IMPACT OF AI/GENERATIVE AI ON DIGITAL ASSET MANAGEMENT MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN DIGITAL ASSET MANAGEMENT

- 6.5.3 CASE STUDY OF AI IMPLEMENTATION IN DIGITAL ASSET MANAGEMENT MARKET

- 6.5.3.1 Siemens Healthineers saves USD 4.1 million+ with Bynder's AI-powered DAM solution

- 6.5.4 INTERCONNECTED ADJACENCY ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DIGITAL ASSET MANAGEMENT MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 ADOBE: ADOBE EXPERIENCE MANAGER ASSETS

- 6.6.2 APRIMO: APRIMO AI-ENABLED DIGITAL ASSET MANAGEMENT PLATFORM

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS, BY REGION

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Middle East & South Africa

- 7.1.2.5 Latin America

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DIGITAL ASSET MANAGEMENT MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 9.2 SOLUTIONS

- 9.2.1 TRADITIONAL DIGITAL ASSET MANAGEMENT

- 9.2.1.1 Enabling structured enterprise content governance, secure asset control, and scalable brand content distribution

- 9.2.2 AI-POWERED DIGITAL ASSET MANAGEMENT

- 9.2.2.1 Accelerating enterprise content operations and intelligent asset discovery

- 9.2.1 TRADITIONAL DIGITAL ASSET MANAGEMENT

- 9.3 SERVICES

- 9.3.1 PROFESSIONAL SERVICES

- 9.3.1.1 Strengthening platform adoption through implementation expertise, integration capabilities, and operational support

- 9.3.1.2 Implementation & Integration

- 9.3.1.3 Training & Consultation

- 9.3.1.4 Support & Maintenance

- 9.3.2 MANAGED SERVICES

- 9.3.2.1 Enabling continuous platform administration, asset governance, and performance optimization for enterprise-scale digital content operations

- 9.3.1 PROFESSIONAL SERVICES

10 DIGITAL ASSET MANAGEMENT MARKET, BY DEPLOYMENT TYPE

- 10.1 INTRODUCTION

- 10.1.1 DEPLOYMENT TYPE: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 10.2 ON-PREMISES

- 10.2.1 REQUIREMENT FOR INTERNAL DATA GOVERNANCE TO SUPPORT ON-PREMISES DAM IMPLEMENTATIONS

- 10.3 CLOUD

- 10.3.1 ENHANCING DIGITAL ASSET MANAGEMENT WITH SCALABLE CLOUD INFRASTRUCTURE

11 DIGITAL ASSET MANAGEMENT MARKET, BY ASSET

- 11.1 INTRODUCTION

- 11.1.1 ASSET: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 11.2 VIDEO & AUDIO ASSETS

- 11.2.1 DAM SOLUTIONS STREAMLINE MANAGEMENT OF HIGH-VOLUME VIDEO AND AUDIO ASSETS

- 11.3 DOCUMENT ASSETS

- 11.3.1 RISING DEMAND FOR ACCURATE AND CONSISTENT CONTENT DISTRIBUTION TO ACCELERATE DAM ADOPTION FOR DOCUMENT ASSETS

- 11.4 WEB & INTERACTIVE ASSETS

- 11.4.1 DAM SOLUTIONS STREAMLINE MANAGEMENT OF DYNAMIC WEB AND INTERACTIVE ASSETS

- 11.5 CREATIVE & DESIGN ASSETS

- 11.5.1 MANAGING DISTRIBUTED CREATIVE TEAMS DRIVES DEMAND FOR CENTRALIZED ASSET ACCESS

12 DIGITAL ASSET MANAGEMENT MARKET, BY BUSINESS FUNCTION

- 12.1 INTRODUCTION

- 12.1.1 BUSINESS FUNCTION: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 12.2 MARKETING & SALES

- 12.2.1 DAM ENABLES CAMPAIGN EXECUTION AND CONSISTENT BRAND DELIVERY ACROSS CHANNELS

- 12.3 IT & OPERATIONS

- 12.3.1 INTEGRATING DIGITAL ASSET MANAGEMENT WITH ENTERPRISE SYSTEMS IMPROVED CONTENT FLOW AND OPERATIONAL EFFICIENCY

- 12.4 FINANCE & ACCOUNTING

- 12.4.1 CENTRALIZING FINANCIAL CONTENT TO ENSURE REGULATORY COMPLIANCE AND IMPROVE AUDIT READINESS

- 12.5 HUMAN RESOURCES

- 12.5.1 STANDARDIZING HR DOCUMENTATION TO ENSURE CONSISTENCY ACROSS EMPLOYEE RECORDS AND SUBMISSIONS

13 DIGITAL ASSET MANAGEMENT MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.1.1 APPLICATION: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 13.2 BRAND & MARKETING ASSET MANAGEMENT

- 13.2.1 CENTRALIZING BRAND ASSETS TO ENSURE CONSISTENT MARKETING EXECUTION ACROSS GLOBAL CHANNELS AND CAMPAIGNS

- 13.3 PRODUCT CONTENT MANAGEMENT

- 13.3.1 IMPLEMENTING DIGITAL ASSET MANAGEMENT TO IMPROVE PRODUCT CONTENT DISCOVERABILITY AND REDUCE MANUAL SEARCH EFFORTS

- 13.4 MEDIA PRODUCTION & BROADCAST ASSET MANAGEMENT

- 13.4.1 CENTRALIZING MEDIA ASSETS TO STREAMLINE PRODUCTION WORKFLOWS AND ENABLE EFFICIENT CONTENT DISTRIBUTION ACROSS PLATFORMS

- 13.5 ENTERPRISE CONTENT & KNOWLEDGE MANAGEMENT

- 13.5.1 IMPLEMENTING DAM SOLUTIONS TO ENHANCE INTERNAL CONTENT MANAGEMENT AND REDUCE INFORMATION SILOS ACROSS TEAMS

- 13.6 OTHER APPLICATIONS

14 DIGITAL ASSET MANAGEMENT MARKET, BY ORGANIZATION SIZE

- 14.1 INTRODUCTION

- 14.1.1 ORGANIZATION SIZE: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 14.2 LARGE ENTERPRISES

- 14.2.1 MANAGING LARGE-SCALE DIGITAL CONTENT OPERATIONS ACROSS GLOBAL ENTERPRISE ENVIRONMENTS USING DAM PLATFORMS

- 14.3 SMALL & MEDIUM-SIZED ENTERPRISES (SMES)

- 14.3.1 SMES EMBRACING DAM FOR CENTRALIZED CONTENT, WORKFLOW STANDARDIZATION, AND EFFICIENCY

15 DIGITAL ASSET MANAGEMENT MARKET, BY VERTICAL

- 15.1 INTRODUCTION

- 15.1.1 VERTICAL: DIGITAL ASSET MANAGEMENT MARKET DRIVERS

- 15.2 BFSI

- 15.2.1 DIGITAL ASSET MANAGEMENT STRENGTHENS CONTENT GOVERNANCE AND OPERATIONAL EFFICIENCY IN BFSI

- 15.3 RETAIL & CONSUMER GOODS

- 15.3.1 RETAIL & CONSUMER GOODS SECTOR LEVERAGES DAM FOR EFFICIENT CONTENT MANAGEMENT AND OMNICHANNEL CONSISTENCY

- 15.4 HEALTHCARE & LIFE SCIENCES

- 15.4.1 HEALTHCARE ORGANIZATIONS LEVERAGE DAM TO STREAMLINE ACCESS TO COMPLEX MEDICAL CONTENT

- 15.5 TELECOMMUNICATIONS

- 15.5.1 DIGITAL ASSET MANAGEMENT IMPROVES CAMPAIGN SPEED AND COLLABORATION IN TELECOMMUNICATIONS

- 15.6 IT & ITES

- 15.6.1 IT & ITES FIRMS LEVERAGE DAM TO STREAMLINE CONTENT ACCESS AND REDUCE DUPLICATION

- 15.7 MEDIA & ENTERTAINMENT

- 15.7.1 DIGITAL ASSET MANAGEMENT IMPROVES CONTENT ACCESSIBILITY AND DELIVERY IN MEDIA WORKFLOWS

- 15.8 MANUFACTURING

- 15.8.1 DAM SOLUTIONS STREAMLINE PRODUCT CONTENT MANAGEMENT ACROSS MANUFACTURING OPERATIONS

- 15.9 GOVERNMENT & PUBLIC SECTOR

- 15.9.1 GOVERNMENT ORGANIZATIONS LEVERAGE DAM TO STREAMLINE CONTENT ACCESS AND COLLABORATION

- 15.10 EDUCATION

- 15.10.1 EDUCATION SECTOR USES DAM TO IMPROVE CONTENT ACCESSIBILITY AND LEARNING EXPERIENCES

- 15.11 TRAVEL & HOSPITALITY

- 15.11.1 TRAVEL & HOSPITALITY COMPANIES LEVERAGE DAM TO MANAGE DYNAMIC AND MULTILINGUAL CONTENT

- 15.12 OTHER VERTICALS

16 DIGITAL ASSET MANAGEMENT MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 AI-driven content operations and enterprise cloud adoption to accelerate digital asset management deployment

- 16.2.2 CANADA

- 16.2.2.1 AI-enabled asset intelligence and multilingual content management to drive digital asset management adoption

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 AI-driven creative production and media innovation to accelerate digital asset management adoption

- 16.3.2 GERMANY

- 16.3.2.1 Product content governance and industrial digitalization to drive digital asset management adoption

- 16.3.3 FRANCE

- 16.3.3.1 Creative industry expansion and digital rights governance to accelerate digital asset management adoption

- 16.3.4 ITALY

- 16.3.4.1 Digital media transformation and luxury brand marketing to drive digital asset management adoption

- 16.3.5 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Digital media production expansion and AI-driven content workflows to accelerate digital asset management adoption

- 16.4.2 INDIA

- 16.4.2.1 Streaming content expansion and national AI initiatives to increase digital asset management adoption

- 16.4.3 JAPAN

- 16.4.3.1 Digital transformation initiatives and AI-driven asset automation to drive digital asset management adoption

- 16.4.4 AUSTRALIA

- 16.4.4.1 Cloud-first enterprise strategies and digital governance to drive digital asset management adoption

- 16.4.5 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.5.1.1 Saudi Arabia

- 16.5.1.1.1 Giga-project infrastructure development and digital hub expansion to drive digital asset management adoption

- 16.5.1.2 UAE

- 16.5.1.2.1 National digital archives expansion and AI-enabled government platforms to drive digital asset management adoption

- 16.5.1.3 Other GCC countries

- 16.5.1.1 Saudi Arabia

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Financial technology innovation and cloud-based media operations to expand digital asset management use cases

- 16.5.3 REST OF MIDDLE EAST & AFRICA

- 16.5.1 GCC COUNTRIES

- 16.6 LATIN AMERICA

- 16.6.1 BRAZIL

- 16.6.1.1 Large-scale digital content operations to drive market

- 16.6.2 MEXICO

- 16.6.2.1 Strengthening digital content governance to drive market

- 16.6.3 REST OF LATIN AMERICA

- 16.6.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2024-2026

- 17.3 REVENUE ANALYSIS, 2021-2025

- 17.4 MARKET SHARE ANALYSIS, 2025

- 17.5 PRODUCT COMPARISON

- 17.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 17.6.1 STARS

- 17.6.2 EMERGING LEADERS

- 17.6.3 PERVASIVE PLAYERS

- 17.6.4 PARTICIPANTS

- 17.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 17.6.5.1 Company footprint

- 17.6.5.2 Region footprint

- 17.6.5.3 Asset footprint

- 17.6.5.4 Deployment type footprint

- 17.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2026

- 17.7.1 PROGRESSIVE COMPANIES

- 17.7.2 RESPONSIVE COMPANIES

- 17.7.3 DYNAMIC COMPANIES

- 17.7.4 STARTING BLOCKS

- 17.7.5 COMPETITIVE BENCHMARKING: STARTUP/SMES, 2026

- 17.7.5.1 Detailed list of key startups/SMEs

- 17.7.5.2 Competitive benchmarking of key startups/SMEs

- 17.8 COMPANY VALUATION AND FINANCIAL METRICS

- 17.8.1 COMPANY VALUATION OF KEY VENDORS

- 17.8.2 FINANCIAL METRICS OF KEY VENDORS

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 17.9.2 DEALS

18 COMPANY PROFILES

- 18.1 INTRODUCTION

- 18.2 MAJOR PLAYERS

- 18.2.1 ADOBE

- 18.2.1.1 Business overview

- 18.2.1.2 Products/Solutions/Services offered

- 18.2.1.3 Recent developments

- 18.2.1.3.1 Product launches/enhancements

- 18.2.1.3.2 Deals

- 18.2.1.4 MnM view

- 18.2.1.4.1 Right to win

- 18.2.1.4.2 Strategic choices

- 18.2.1.4.3 Weaknesses and competitive threats

- 18.2.2 OPENTEXT

- 18.2.2.1 Business overview

- 18.2.2.2 Products/Solutions/Services offered

- 18.2.2.3 Recent developments

- 18.2.2.3.1 Product launches/enhancements

- 18.2.2.3.2 Deals

- 18.2.2.4 MnM view

- 18.2.2.4.1 Right to win

- 18.2.2.4.2 Strategic choices

- 18.2.2.4.3 Weaknesses and competitive threats

- 18.2.3 COGNIZANT

- 18.2.3.1 Business overview

- 18.2.3.2 Products/Solutions/Services offered

- 18.2.3.3 Recent developments

- 18.2.3.3.1 Deals

- 18.2.3.4 MnM view

- 18.2.3.4.1 Right to win

- 18.2.3.4.2 Strategic choices

- 18.2.3.4.3 Weaknesses and competitive threats

- 18.2.4 CLOUDINARY

- 18.2.4.1 Business overview

- 18.2.4.2 Products/Solutions/Services offered

- 18.2.4.3 Recent developments

- 18.2.4.3.1 Product launches/enhancements

- 18.2.4.3.2 Deals

- 18.2.4.4 MnM view

- 18.2.4.4.1 Right to win

- 18.2.4.4.2 Strategic choices

- 18.2.4.4.3 Weaknesses and competitive threats

- 18.2.5 APRIMO

- 18.2.5.1 Business overview

- 18.2.5.2 Products/Solutions/Services offered

- 18.2.5.3 Recent developments

- 18.2.5.3.1 Product launches/enhancements

- 18.2.5.3.2 Deals

- 18.2.5.4 MnM view

- 18.2.5.4.1 Right to win

- 18.2.5.4.2 Strategic choices

- 18.2.5.4.3 Weaknesses and competitive threats

- 18.2.6 BYNDER

- 18.2.6.1 Business overview

- 18.2.6.2 Products/Solutions/Services offered

- 18.2.6.3 Recent developments

- 18.2.6.3.1 Product launches/enhancements

- 18.2.6.3.2 Deals

- 18.2.7 HYLAND

- 18.2.7.1 Business overview

- 18.2.7.2 Products/Solutions/Services offered

- 18.2.7.3 Recent developments

- 18.2.7.3.1 Product launches/enhancements

- 18.2.8 VEEVA SYSTEMS

- 18.2.8.1 Business overview

- 18.2.8.2 Products/Solutions/Services offered

- 18.2.9 ACQUIA

- 18.2.9.1 Business overview

- 18.2.9.2 Products/Solutions/Services offered

- 18.2.9.3 Recent developments

- 18.2.9.3.1 Product launches/enhancements

- 18.2.9.3.2 Deals

- 18.2.10 FRONTIFY

- 18.2.10.1 Business overview

- 18.2.10.2 Products/Solutions/Services offered

- 18.2.10.3 Recent developments

- 18.2.10.3.1 Deals

- 18.2.1 ADOBE

- 18.3 OTHER PLAYERS

- 18.3.1 SITECORE

- 18.3.2 PATTERN

- 18.3.3 ESKO

- 18.3.4 PAPIRFLY

- 18.3.5 CENSHARE

- 18.3.6 CELUM

- 18.3.7 MARCOMCENTRAL

- 18.3.8 TENOVOS

- 18.3.9 STOCKPRESS

- 18.3.10 PHOTOSHELTER

- 18.3.11 CHETU

- 18.3.12 INTELLIGENCEBANK

- 18.3.13 ORANGE LOGIC

- 18.3.14 WEDIA

- 18.3.15 ASSET BANK

- 18.3.16 BRANDFOLDER

- 18.3.17 MEDIAVALET

- 18.3.18 DEMOUP CLIPLISTER

- 18.3.19 FILECAMP

- 18.3.20 WOODWING

- 18.3.21 KONTAINER

- 18.3.22 IMAGEKIT

- 18.3.23 SCALEFLEX

- 18.3.24 CONTENTCLOUD

- 18.3.25 ATROCORE

- 18.3.26 APOLLON

- 18.3.27 CANTO

- 18.3.28 RESOURCESPACE

- 18.3.29 LINGO

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Data & list of key secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Breakdown of primary interviews

- 19.1.2.2 Key industry insights

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.3 DATA TRIANGULATION

- 19.4 FACTOR ANALYSIS

- 19.5 RESEARCH ASSUMPTIONS

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS