|

시장보고서

상품코드

2007700

지향성 에너지 무기 시장 : 기술별, 투자별, 고객별, 용도별, 임무별, 아키텍처별, 솔루션별, 전개별, 지역별 - 세계 예측(-2035년)Directed Energy Weapons Market by Technology, Investment, Customer, Application, Mission, Architecture, Deployment, and Region - Global Forecast to 2035 |

||||||

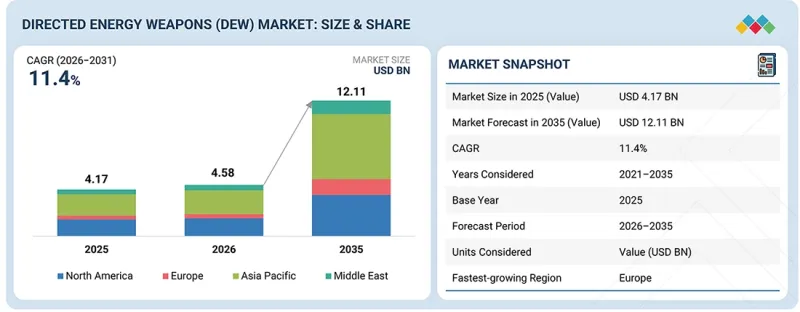

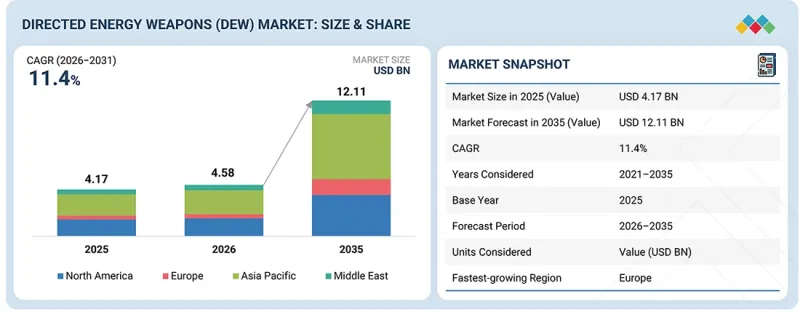

지향성 에너지 무기(DEW) 시장 규모는 2025년에 41억 7,000만 달러로 평가되었습니다.

이 시장은 2026년 45억 8,000만 달러에서 2035년까지 121억 1,000만 달러로 성장할 것으로 예상되며, 예측 기간 동안 11.4%의 CAGR을 기록할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2035년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 기술별, 투자별, 고객별, 용도별, 임무별, 아키텍처별, 솔루션별, 전개별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

드론, 로켓, 포탄, 순항 미사일에 대한 비용 효율적인 방공 및 미사일 방어에 대한 수요가 증가함에 따라 시장이 확대되고 있습니다. 군은 동적 요격 시스템에 비해 신속한 교전 능력, 풍부한 탄약 탑재량, 그리고 물류 부담 감소를 실현하는 레이저 및 마이크로파 시스템에 대한 투자를 진행하고 있습니다. 또한 발전, 에너지 저장 및 열 관리 기술의 발전으로 육상, 해상 및 항공 플랫폼에 DEW 시스템을 배치할 수 있게 되었습니다.

많은 새로운 방위 플랫폼이 처음부터 이러한 시스템을 탑재하도록 설계되었기 때문에 OEM-Fit 부문은 지향성 에너지 무기 시장을 주도할 것으로 예상됩니다. 제조 단계에서 지향성 에너지 시스템을 통합하면 전원, 냉각, 시스템 레이아웃을 보다 적절하게 계획할 수 있습니다. 이를 통해 사후 개조와 비교하여 통합 문제를 줄일 수 있습니다. 각국은 새로운 차량, 함정, 항공기를 개발할 때 초기 설계에 지향성 에너지 무기를 통합하고 있으며, 이는 OEM-Fit 프로그램에서의 도입 확대를 뒷받침하고 있습니다.

예측 기간 동안 지향성 에너지 무기(DEW) 시장에서 '기타' 부문이 가장 높은 성장률을 기록할 것으로 예상됩니다. 이 부문에는 센서, 지휘통제시스템, 플랫폼 통합 시스템 등이 포함됩니다. 이러한 시스템은 표적 탐지, 추적 및 전체 시스템 운영에 필수적입니다. 지향성 에너지 무기가 육상, 해상, 항공 및 기타 플랫폼에 배치됨에 따라 이러한 지원 시스템에 대한 수요가 증가하고 있습니다. 또한 대 드론 및 미사일 방어와 같은 임무의 확대도 이러한 구성요소에 대한 수요를 촉진하고 있습니다.

아시아태평양은 국방비 증가와 지역 안보 우려 증가로 인해 예측 기간 동안 지향성 에너지 무기(DEW) 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 중국, 인도, 일본, 한국 등의 국가들은 대 드론 및 미사일 방어를 위한 레이저 및 마이크로파 시스템에 투자하고 있습니다. 각국 정부는 국내 개발 프로그램을 지원하고 육상 및 해상 플랫폼에서 이러한 시스템을 테스트하고 있습니다. 또한, 국경, 중요 인프라, 군사 자산을 보호해야 할 필요성도 지향성 에너지 시스템의 보급을 촉진하고 있습니다.

조사 범위:

이 시장 조사는 다양한 부문 및 하위 부문에 걸쳐 지향성 에너지 무기(DEW) 시장을 포괄합니다. 이 조사는 지역 및 분야별 시장 규모와 성장 잠재력을 추정하는 것을 목표로 하고 있습니다. 또한, 시장 내 주요 기업들의 상세한 경쟁 분석, 기업 개요, 제품 및 사업 제공에 대한 주요 관찰 사항, 최근 동향, 각 기업이 채택한 주요 시장 전략에 대한 내용도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 시장 리더와 신규 진입자에게 전체 지향성 에너지 무기(DEW) 시장 매출에 대한 가장 정확한 추정치를 제공합니다. 또한, 이해관계자들이 경쟁 상황을 이해하고, 자신의 비즈니스를 더 나은 위치에 놓고, 적절한 시장 진입 전략을 수립하기 위한 인사이트를 얻을 수 있도록 돕습니다. 또한, 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 억제요인, 도전 과제 및 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 시장 촉진요인(여러 군사 플랫폼에서 대드론, 로켓, 포병, 미사일 방어에 대한 수요 증가, 레이저, 마이크로파 및 관련 지향성 에너지 기술에 대한 정부의 연구개발, 시험, 평가(RDT&E) 및 조달 투자 확대), 제약요인(실전 배치에 따른 고출력 발전, 에너지 저장 및 열 관리 요구사항, 악천후 및 열악한 환경 조건에서 지향성 에너지 시스템의 성능 제약), 기회(다층 방공 및 미사일 방어 아키텍처에 지향성 에너지 무기를 통합, 육상, 해군, 항공, 무인, 우주 플랫폼에 대한 배치 확대), 도전과제(유사한 방위 임무에 대한 운동에너지 기술), 그리고 도전과제(유사한 방어 임무에서 운동에너지 요격기 및 전자전 시스템에 대한 지속적인 의존, 국제 협력 및 판매에 영향을 미치는 수출 규제 및 기술 보안 제약)

- 시장 침투 : 시장을 선도하는 주요 기업이 제공하는 지향성 에너지 무기에 대한 종합적인 정보를 제공합니다.

- 제품 개발 및 혁신 : 시장에서의 미래 기술, R&D 활동 및 제품 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화 : 지향성 에너지 무기(DEW) 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁 분석 : 지향성 에너지 무기(DEW) 시장 내 주요 기업의 시장 점유율, 성장 전략, 제품, 제조 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 지향성 에너지 무기(DEW) 시장(기술별)

제10장 지향성 에너지 무기(DEW) 시장(투자별)

제11장 지향성 에너지 무기(DEW) 시장(고객별)

제12장 지향성 에너지 무기(DEW) 시장(용도별)

제13장 지향성 에너지 무기(DEW) 시장(임무별)

제14장 지향성 에너지 무기(DEW) 시장(아키텍처별)

제15장 지향성 에너지 무기(DEW) 시장(솔루션별)

제16장 지향성 에너지 무기(DEW) 시장(전개별)

제17장 지향성 에너지 무기(DEW) 시장(지역별)

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSM 26.04.28The directed energy weapons (DEW) market was valued at USD 4.17 billion in 2025. It is projected to grow from USD 4.58 billion in 2026 to USD 12.11 billion by 2035, at a CAGR of 11.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Deployment and Region |

| Regions covered | North America, Europe, APAC, RoW |

The market is growing due to the increasing demand for cost-effective air and missile defense against drones, rockets, artillery, and cruise missiles. Armed forces are investing in laser and microwave systems that provide rapid engagement, deep magazines, and reduced logistics compared with kinetic interceptors. Additionally, progress in power generation, energy storage, and thermal management is also enabling the deployment of DEW systems on land, naval, and airborne platforms.

"By deployment, the OEM-Fit segment is projected to lead the market during the forecast period."

The OEM-Fit segment is projected to lead the directed energy weapons market as many new defense platforms are being designed with these systems from the start. Integrating directed energy systems during manufacturing allows better planning for power supply, cooling, and system layout. This reduces integration issues compared to upgrades. As countries develop new vehicles, ships, and aircraft, they are including directed energy weapons in initial designs, which supports higher adoption under OEM-fit programs.

"By solution, the others segment is projected to achieve the highest CAGR during the forecast period."

The others segment is projected to achieve the highest growth in the directed energy weapons market (DEW) during the forecast period. This segment covers sensors, command and control systems, and platform integration systems. These systems are needed for target detection, tracking, and overall system operation. As directed energy weapons are deployed across land, naval, airborne, and other platforms, the need for these supporting systems is increasing. Growth in missions such as counter-drone and missile defense is also adding to demand for these components.

"Asia Pacific is projected to account for the largest share during the forecast period."

Asia Pacific is projected to account for the largest share in the directed energy weapons (DEW) market during the forecast period due to the increasing defense spending and rising regional security concerns. Countries such as China, India, Japan, and South Korea are investing in laser and microwave systems for counter-drone and missile defense. Governments are supporting domestic development programs and testing these systems on land and naval platforms. Additionally, the need to protect borders, critical infrastructure, and military assets is also supporting the wider adoption of directed energy systems.

Breakdown of Primary Participants:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: Asia Pacific - 40%, Europe - 20%, North America - 20%, Middle East - 10%, and Rest of the World - 10%

Research Coverage:

This market study covers the directed energy weapons (DEW) market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to Buy this Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall directed energy weapons (DEW) Market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. Additionally, the report will help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Increasing demand for counter-drone, rocket, artillery, and missile defense across multiple military platforms; growing government RDT&E and procurement investments in laser, microwave, and related directed energy technologies), Restraints (High power generation, energy storage, and thermal management requirements for operational deployment; performance limitations of directed energy systems under adverse atmospheric and environmental conditions), Opportunities (Integration of directed energy weapons with layered air and missile defense architectures; expansion of deployment across land, naval, airborne, unmanned, and space platforms), Challenges (Continued reliance on kinetic interceptors and electronic warfare systems for similar defense missions, export controls and technology security restrictions affecting international collaboration and sales)

- Market Penetration: Comprehensive information on directed energy weapons offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the directed energy weapons (DEW) market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the directed energy weapons (DEW) market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DIRECTED ENERGY WEAPONS (DEW) MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIRECTED ENERGY WEAPONS (DEW) MARKET

- 3.2 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY TECHNOLOGY

- 3.3 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY CUSTOMER

- 3.4 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY INVESTMENT

- 3.5 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY GUIDANCE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for counter-drone, rocket, artillery, and missile defense across multiple military platforms

- 4.2.1.2 Growing government RDT&E and procurement investments in laser, microwave, and directed energy technologies

- 4.2.1.3 Advancements in power scaling, beam control, and thermal management enabling transition from prototype systems to operational deployment

- 4.2.2 RESTRAINTS

- 4.2.2.1 High power generation, energy storage, and thermal management requirements for operational deployment

- 4.2.2.2 Performance limitations of directed energy systems under adverse atmospheric and environmental conditions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of directed energy weapons with layered air and missile defense architecture

- 4.2.3.2 Expansion of deployment across land, naval, airborne, unmanned, and space platforms

- 4.2.4 CHALLENGES

- 4.2.4.1 Continued reliance on kinetic interceptors and electronic warfare systems for similar defense missions

- 4.2.4.2 Export controls and technology security restrictions affecting international collaboration and sales

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES IN DIRECTED ENERGY WEAPONS (DEW) MARKET

- 4.4 INTER-CONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER 1, 2, AND 3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL DIRECTED ENERGY WEAPON (DEW) INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DEFENSE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 9301)

- 5.5.2 EXPORT SCENARIO (HS CODE 9301)

- 5.6 KEY CONFERENCES & EVENTS, 2025-2026

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT & FUNDING SCENARIO

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE TREND FOR DIRECTED ENERGY WEAPONS, KEY PLAYER

- 5.9.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.10 OPERATIONAL DATA

- 5.11 TOTAL COST OF OWNERSHIP

- 5.11.1 TOTAL COST OF OWNERSHIP (TCO) FOR DIRECTED ENERGY WEAPONS

- 5.11.1.1 Integration and fielding

- 5.11.1.2 Training and spares costs

- 5.11.1.3 Annual O&M costs

- 5.11.1.4 Mid-life overhaul costs

- 5.11.1.5 Other costs

- 5.11.1 TOTAL COST OF OWNERSHIP (TCO) FOR DIRECTED ENERGY WEAPONS

- 5.12 CASE STUDIES

- 5.12.1 CASE STUDY 1: DEPLOYMENT OF SHIPBORNE HIGH-ENERGY LASER SYSTEMS FOR AIR AND DRONE DEFENSE

- 5.12.2 CASE STUDY 2: HIGH-POWER MICROWAVE (HPWM) SYSTEM FOR SWARM DEFEAT BY EPIRUS

- 5.12.3 CASE STUDY 3: DEPLOYMENT OF HIGH-ENERGY LASERS (HEL) FOR COUNTER-UAS (LAND PLATFORM) BY AEROVIRONMENT

- 5.13 IMPACT OF 2025 US TARIFFS

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRY/REGION

- 5.13.4.1 US

- 5.13.4.2 Europe

- 5.13.4.3 Asia Pacific

- 5.13.5 IMPACT ON END-USER INDUSTRIES

- 5.14 BILL OF MATERIALS (BOM) ANALYSIS

- 5.14.1 BILL OF MATERIALS (BOM) ANALYSIS FOR DIRECTED ENERGY WEAPONS

- 5.15 VOLUME DATA

- 5.16 BUSINESS MODELS

- 5.16.1 DIRECT PROCUREMENT MODEL

- 5.16.2 RESEARCH, DEVELOPMENT, TEST, AND EVALUATION MODEL

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ULTRA-SHORT PULSE LASERS

- 6.1.2 PLASMA WEAPONRY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ADAPTIVE OPTICS (AO)

- 6.2.2 PRECISION SENSORS AND IMU/GNSS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 RAILGUNS

- 6.3.2 COILGUNS (GAUSS GUNS)

- 6.3.3 HYPERVELOCITY PROJECTILE ARTILLERY

- 6.3.4 DIRECTED ENERGY DEPOSITION (DED)

- 6.3.5 COUNTER-DIRECTED ENERGY (CDEW)

- 6.4 TECHNOLOGY ROADMAP

- 6.5 EMERGING TECHNOLOGY TRENDS

- 6.6 PATENT ANALYSIS

- 6.7 FUTURE APPLICATIONS

- 6.8 IMPACT OF AI/GENERATIVE AI ON DIRECTED ENERGY WEAPONS (DEW) MARKET

- 6.8.1 TOP USE CASES AND MARKET POTENTIAL

- 6.8.2 BEST PRACTICES IN DIRECTED ENERGY WEAPONS (DEW) MARKET

- 6.8.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.8.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DIRECTED ENERGY WEAPONS (DEW) MARKET

- 6.9 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.9.1 LOCKHEED MARTIN - NAVAL LASER SYSTEM INTEGRATION FOR AIR DEFENSE

- 6.9.2 RTX - MICROWAVE-BASED COUNTER-DRONE SYSTEM DEPLOYMENT

- 6.9.3 RHEINMETALL AG - MOBILE LASER AIR DEFENSE SYSTEM INTEGRATION SYSTEM PROVIDER

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 TARIFF DATA

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 REGULATORY FRAMEWORK

- 7.2.1 NORTH AMERICA

- 7.2.2 EUROPE

- 7.2.3 ASIA PACIFIC

- 7.2.4 MIDDLE EAST

- 7.2.5 INDUSTRY STANDARDS

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 ENERGY-EFFICIENT POWER AND COOLING SYSTEMS

- 7.3.2 SYSTEM DESIGN AND LIFECYCLE UPGRADES

- 7.4 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 HIGH-ENERGY LASERS (HEL)

- 9.2.1 < 20 KW

- 9.2.1.1 Lasers with power under 20 kW are mainly used for counter-drone missions and technology testing

- 9.2.2 20-100 KW

- 9.2.2.1 Mid-power lasers support short-range air defense against drones and small aerial threats

- 9.2.3 101-300 KW

- 9.2.3.1 High-power lasers are designed to counter rockets, artillery, mortars, and larger drones

- 9.2.4 > 300 KW

- 9.2.4.1 Very high-power lasers are used for advanced air and missile defense missions

- 9.2.1 < 20 KW

- 9.3 HIGH-POWER MICROWAVES (HPWM)

- 9.3.1 10-500 MW

- 9.3.1.1 HPWM systems in 10-500 MW power range are used for tactical electronic disruption and counter-drone missions

- 9.3.2 501 MW-1 GW

- 9.3.2.1 Microwave systems provide stronger electronic disruption against larger drones and guided munitions

- 9.3.3 1-100 GW

- 9.3.3.1 HPWM systems in 1-100 GW power range support advanced electronic attack missions against radar and communication systems

- 9.3.4 101-300 GW

- 9.3.4.1 High-intensity microwave systems are designed for wide-area electronic disruption and counter-swarm operations

- 9.3.5 > 300 GW

- 9.3.5.1 HPWM systems with power above 300 GW are researched for large-scale electronic disruption in high-intensity conflict environments

- 9.3.1 10-500 MW

- 9.4 MILLIMETER WAVE DEVICES

- 9.4.1 10-50 KW

- 9.4.1.1 Millimeter wave systems with 10-50 kW power range are used for short-range non-lethal security and testing applications

- 9.4.2 51-100 KW

- 9.4.2.1 Millimeter wave systems operating between 50 and 100 kW improve range and effectiveness for vehicle-mounted non-lethal security operations

- 9.4.3 > 100 KW

- 9.4.3.1 Millimeter wave systems above 100 kW power range provide wider coverage and stronger deterrence for large security zones

- 9.4.1 10-50 KW

- 9.5 RADIOFREQUENCY DEVICES & ELECTRONIC WARFARE (EW) JAMMERS

- 9.5.1 < 100 W

- 9.5.1.1 RF jammers with power below 100 W provide portable short-range disruption for counter-drone and local security missions

- 9.5.2 100 W-1 KW

- 9.5.2.1 Radiofrequency jammers in this power range support vehicle-mounted counter-UAS and tactical communication disruption operations

- 9.5.3 2-10 KW

- 9.5.3.1 RF and EW jammers in this range enable tactical electronic warfare against drones, radar, and battlefield communications

- 9.5.4 > 10 KW

- 9.5.4.1 RF jammers with power above 10 kW deliver high-power electronic warfare capabilities against radar and communication networks

- 9.5.1 < 100 W

- 9.6 PARTICLE BEAM

- 9.6.1 50-200 MEV/M

- 9.6.1.1 Particle beam systems operating in 50-200 MeV/m energy range represent early-stage accelerator-based directed energy systems

- 9.6.2 201-400 MEV/M

- 9.6.2.1 Particle beam systems within 200-400 MeV/m range represent more advanced accelerator technologies capable of generating significantly higher energy particle streams

- 9.6.1 50-200 MEV/M

10 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY INVESTMENT

- 10.1 INTRODUCTION

- 10.2 PROCUREMENT

- 10.2.1 PROCUREMENT PROGRAMS ARE INCREASING AS DIRECTED ENERGY SYSTEMS MOVE FROM TESTING TO OPERATIONAL DEPLOYMENT

- 10.3 RDT&E

- 10.3.1 RDT&E INVESTMENT SUPPORTS RESEARCH, TESTING, AND TECHNOLOGY DEVELOPMENT FOR FUTURE DIRECTED ENERGY CAPABILITIES

11 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY CUSTOMER

- 11.1 INTRODUCTION

- 11.2 MILITARY

- 11.2.1 NEED FOR MILITARY FORCES TO ADOPT DIRECTED ENERGY SYSTEMS TO DRIVE MARKET

- 11.3 HOMELAND SECURITY

- 11.3.1 HOMELAND SECURITY AGENCIES ARE EXPLORING DIRECTED ENERGY TECHNOLOGIES TO PROTECT INFRASTRUCTURE AND COUNTER UNAUTHORIZED DRONES

12 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 AIRBORNE

- 12.2.1 FIGHTER JETS

- 12.2.1.1 Fighter aircraft are being studied as platforms for directed energy systems to improve self-protection against missiles and aerial threats

- 12.2.2 ATTACK HELICOPTERS

- 12.2.2.1 Helicopters use compact directed energy systems to counter low-altitude drones and support short-range defensive missions

- 12.2.3 SPECIAL MISSION AIRCRAFT

- 12.2.3.1 Special mission aircraft support directed energy operations such as electronic disruption, surveillance protection, and counter-drone missions

- 12.2.4 UNMANNED AERIAL VEHICLES (UAVS)

- 12.2.4.1 UAVs are used as platforms for smaller directed energy systems that can remotely engage drones and electronic targets

- 12.2.1 FIGHTER JETS

- 12.3 MUNITIONS

- 12.3.1 CRUISE MISSILES

- 12.3.1.1 Cruise missiles are long-range precision strike weapons used to attack strategic targets during modern military operations

- 12.3.2 LOITERING MUNITIONS

- 12.3.2.1 Loitering munitions combine surveillance and strike functions by searching for targets before carrying out direct attacks

- 12.3.3 ROCKET ARTILLERY

- 12.3.3.1 Rocket artillery systems deliver rapid, long-range firepower to support ground operations and suppress enemy positions

- 12.3.1 CRUISE MISSILES

- 12.4 LAND

- 12.4.1 FIXED

- 12.4.1.1 Palletized/containerized systems

- 12.4.1.1.1 Containerized directed energy systems allow rapid transport and deployment of counter-drone capabilities

- 12.4.1.2 Heavy-trailer-mounted systems

- 12.4.1.2.1 Trailer-mounted platforms provide semi-mobile deployment of higher-power directed energy systems

- 12.4.1.1 Palletized/containerized systems

- 12.4.2 MOBILE

- 12.4.2.1 Infantry fighting vehicles

- 12.4.2.1.1 Infantry fighting vehicles integrate compact directed energy systems to protect frontline troops from aerial threats

- 12.4.2.2 Armored personnel carriers

- 12.4.2.2.1 Armored personnel carriers support mobile defense roles by carrying directed energy systems for protection against aerial attacks

- 12.4.2.3 Tactical trucks

- 12.4.2.3.1 Tactical trucks provide space and power capacity to transport and operate directed energy systems for base defense and convoy protection

- 12.4.2.4 Unmanned ground vehicles

- 12.4.2.4.1 Unmanned ground vehicles enable remote operation of directed energy systems in high-risk environments without exposing soldiers to danger

- 12.4.2.1 Infantry fighting vehicles

- 12.4.1 FIXED

- 12.5 NAVAL

- 12.5.1 DESTROYERS

- 12.5.1.1 Destroyers have power capacity and space required to support higher-power directed energy systems for ship defense

- 12.5.2 AMPHIBIOUS ASSAULT/LANDING SHIPS

- 12.5.2.1 Amphibious ships use directed energy systems to protect troops, landing operations, and nearby vessels from aerial threats

- 12.5.3 FRIGATES & LITTORAL COMBAT SHIPS (LCS)

- 12.5.3.1 Frigates and littoral combat ships strengthen short-range maritime defense

- 12.5.4 PATROL BOATS

- 12.5.4.1 Patrol boats can deploy smaller directed energy systems for coastal security and counter-drone missions

- 12.5.5 UNMANNED SURFACE VEHICLES

- 12.5.5.1 Unmanned surface vehicles may operate directed energy payloads to support remote maritime surveillance and defense tasks

- 12.5.1 DESTROYERS

- 12.6 SPACE

- 12.6.1 LOW EARTH ORBIT (LEO) SATELLITES

- 12.6.1.1 LEO satellites are studied for receiving and converting transmitted laser energy for power and other space operations

- 12.6.2 SPACEPLANES

- 12.6.2.1 Spaceplanes are examined for potential use of laser energy in propulsion concepts and future space mission support

- 12.6.1 LOW EARTH ORBIT (LEO) SATELLITES

13 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY MISSION

- 13.1 INTRODUCTION

- 13.2 COUNTER-UNMANNED AERIAL SYSTEMS (C-SUAS/C-UAS)

- 13.2.1 RISING DRONE THREATS TO DRIVE ADOPTION OF DIRECTED ENERGY WEAPONS FOR COUNTER-UAS MISSIONS

- 13.3 COUNTER-ROCKET, ARTILLERY, AND MORTAR (C-RAM)

- 13.3.1 FOCUS ON PROTECTING FORWARD FORCES FROM INDIRECT FIRE THREATS TO DRIVE C-RAM MISSIONS TO BOOST GROWTH

- 13.4 CRUISE MISSILE DEFENSE (CMD)

- 13.4.1 GROWING CRUISE MISSILE THREATS TO STRENGTHEN ROLE OF DIRECTED ENERGY WEAPONS IN AIR DEFENSE

- 13.5 BALLISTIC & HYPERSONIC MISSILE DEFENSE

- 13.5.1 FOCUS ON EMERGING HIGH-SPEED MISSILE THREATS TO DRIVE RESEARCH IN DIRECTED ENERGY DEFENSE

- 13.6 COUNTER-ELECTRONICS & CISR DEFEAT AND SENSOR BUILDING

- 13.6.1 ELECTRONIC WARFARE REQUIREMENTS TO EXPAND USE OF DIRECTED ENERGY WEAPONS FOR SENSOR DISRUPTION

- 13.7 COUNTER-ELECTRONICS & CISR DEFEAT AND SENSOR BUILDING

- 13.7.1 NAVAL SECURITY CHALLENGES TO DRIVE DEMAND FOR DIRECTED ENERGY AGAINST SMALL ATTACK BOATS

- 13.8 COUNTER-ELECTRONICS & CISR DEFEAT AND SENSOR BUILDING

- 13.8.1 GROWING DEMAND FOR SCALABLE AND NON-LETHAL SECURITY SOLUTIONS TO DRIVE ADOPTION OF DIRECTED ENERGY WEAPONS

14 DIRECTED ENERGY WEAPONS (DEW), BY ARCHITECTURE

- 14.1 INTRODUCTION

- 14.2 STANDALONE DEW SYSTEMS (FIXED/TOWED & MOBILE)

- 14.2.1 EMPHASIS ON DEPLOYING INDEPENDENT DIRECTED ENERGY SYSTEMS ON FIXED SITES AND MOBILE MILITARY PLATFORMS TO DRIVE GROWTH

- 14.3 HYBRID EFFECTOR TURRETS

- 14.3.1 DEW WITH ANTI-AIRCRAFT ARTILLERY (AAA)

- 14.3.1.1 Need for combining directed energy systems with anti-aircraft guns for short-range air defense to drive market

- 14.3.2 DEW WITH SURFACE-TO-AIR MISSILE (SAM)

- 14.3.2.1 Focus on combining directed energy weapons and missile systems to support layered air defense to drive market

- 14.3.3 DEW WITH AAA & SHORAD MISSILE

- 14.3.3.1 Need for using directed energy, artillery, and short-range missiles together for multi-layer defense to boost growth

- 14.3.1 DEW WITH ANTI-AIRCRAFT ARTILLERY (AAA)

- 14.4 DIRECTED ENERGY CLOSE-IN WEAPON SYSTEMS (DE-CIWS)

- 14.4.1 NAVAL DE-CIWS

- 14.4.1.1 Need for deploying directed energy close-in defense systems on naval ships to counter missiles and drones to drive market

- 14.4.2 LAND-BASED DE-CIWS

- 14.4.2.1 Focus on using directed energy close-in weapon systems to protect military bases and ground installations to boost market

- 14.4.1 NAVAL DE-CIWS

- 14.5 EXPENDABLE PAYLOADS/WARHEADS

- 14.5.1 SINGLE-USE EMP PAYLOAD

- 14.5.1.1 Electromagnetic pulse payloads disrupt electronic circuits and communication systems

- 14.5.2 MICROWAVE WARHEADS

- 14.5.2.1 High-power microwave energy interferes with electronic systems on military targets

- 14.5.1 SINGLE-USE EMP PAYLOAD

15 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY SOLUTION

- 15.1 INTRODUCTION

- 15.2 POWER GENERATION & ENERGY STORAGE SYSTEM

- 15.2.1 PRIME POWER GENERATION SYSTEM

- 15.2.1.1 Reliable onboard electricity generation is essential to support continuous operation of directed energy weapons

- 15.2.2 POWER DISTRIBUTION SYSTEM

- 15.2.2.1 Need for efficient power distribution to ensure high electrical loads from directed energy weapons to drive market

- 15.2.3 PULSED POWER SYSTEM

- 15.2.3.1 Pulsed power systems enable directed energy weapons to release large amounts of energy in very short bursts

- 15.2.4 ENERGY STORAGE SYSTEM

- 15.2.4.1 Energy storage systems provide reserve power that allows directed energy weapons to operate during high-energy engagements

- 15.2.1 PRIME POWER GENERATION SYSTEM

- 15.3 THERMAL MANAGEMENT SYSTEM (TMS)

- 15.3.1 LIQUID COOLING SYSTEM

- 15.3.1.1 Liquid cooling systems remove heat quickly from laser components to prevent overheating and maintain continuous weapon operation

- 15.3.2 HEAT ABSORPTION SYSTEM

- 15.3.2.1 Heat absorption systems use advanced materials to store and dissipate excess heat produced during laser operation

- 15.3.1 LIQUID COOLING SYSTEM

- 15.4 BEAM GENERATION & CONTROL SYSTEM

- 15.4.1 BEAM DIRECTOR ASSEMBLY SYSTEM

- 15.4.1.1 Beam director assemblies guide and focus energy beam toward target with high accuracy

- 15.4.2 BEAM GENERATION SYSTEM

- 15.4.2.1 Beam generation systems convert electrical power into focused laser or microwave energy used to engage targets

- 15.4.3 TURRET & STABILIZATION SYSTEM

- 15.4.3.1 Turret and stabilization systems maintain beam accuracy by compensating for platform movement and vibration

- 15.4.1 BEAM DIRECTOR ASSEMBLY SYSTEM

- 15.5 OTHERS

- 15.5.1 SENSOR & TARGET ACQUISITION SYSTEM

- 15.5.1.1 Sensor and target acquisition systems detect and track threats so that directed energy weapons can engage them

- 15.5.2 COMMAND & CONTROL SYSTEM

- 15.5.2.1 Command and control systems coordinate target engagement and manage operation of directed energy weapons

- 15.5.3 PLATFORM INTEGRATION SYSTEMS

- 15.5.3.1 Platform integration systems ensure that directed energy weapons operate effectively within host vehicle or platform

- 15.5.1 SENSOR & TARGET ACQUISITION SYSTEM

16 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY DEPLOYMENT

- 16.1 INTRODUCTION

- 16.2 OEM-FIT

- 16.2.1 INTEGRATION OF DIRECTED ENERGY WEAPONS DURING PLATFORM MANUFACTURING TO SUPPORT STABLE DEPLOYMENT AND SYSTEM COMPATIBILITY

- 16.3 MODERNIZATION & UPGRADATION

- 16.3.1 NEED FOR UPGRADING EXISTING MILITARY PLATFORMS WITH DIRECTED ENERGY WEAPONS TO DRIVE MARKET

17 DIRECTED ENERGY WEAPONS (DEW) MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Ongoing US military programs and prototype development to support transition of directed energy weapons from research to field deployment

- 17.2.1 US

- 17.3 ASIA PACIFIC

- 17.3.1 CHINA

- 17.3.1.1 China expands directed energy weapon development to strengthen counter-drone and advanced air defense capabilities

- 17.3.2 JAPAN

- 17.3.2.1 Japan deploys high-power microwave and laser systems to build cost-effective counter-drone defense capabilities

- 17.3.3 INDIA

- 17.3.3.1 Need to develop domestically built laser-based directed energy weapons to counter drones and improve air defense response

- 17.3.4 SOUTH KOREA

- 17.3.4.1 Focus on strengthening counter-drone defense through acquisition and local production of high-energy laser weapon systems

- 17.3.5 AUSTRALIA

- 17.3.5.1 Need for deploying integrated counter-UAS technologies to address drone threats to drive market

- 17.3.1 CHINA

- 17.4 EUROPE

- 17.4.1 GERMANY

- 17.4.1.1 Technological advancements in naval laser weapon development to drive market

- 17.4.2 FRANCE

- 17.4.2.1 France expands directed energy capabilities to develop integrated counter-drone and force protection laser solutions

- 17.4.3 UK

- 17.4.3.1 Need to accelerate deployment of DragonFire laser weapon program to strengthen naval air defense

- 17.4.1 GERMANY

- 17.5 MIDDLE EAST

- 17.5.1 GCC

- 17.5.1.1 UAE

- 17.5.1.1.1 Focus on strengthening air defense through laser-based aircraft protection and counter-drone programs to spur demand

- 17.5.1.2 Saudi Arabia

- 17.5.1.2.1 Emphasis on expanding counter-drone and air defense capabilities to boost growth

- 17.5.1.1 UAE

- 17.5.2 ISRAEL

- 17.5.2.1 Need for strengthening multi-layered air defense systems to propel demand

- 17.5.3 TURKEY

- 17.5.3.1 Focus on developing and testing mobile laser weapon systems to drive market

- 17.5.1 GCC

18 COMPETITIVE LANDSCAPE

- 18.1 INTRODUCTION

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 18.3 REVENUE ANALYSIS, 2021-2025

- 18.4 MARKET SHARE ANALYSIS, 2025

- 18.4.1 LOCKHEED MARTIN CORPORATION (US)

- 18.4.2 RTX (US)

- 18.4.3 NORTHROP GRUMMAN (US)

- 18.4.4 BOEING (US)

- 18.4.5 L3HARRIS TECHNOLOGIES, INC. (US)

- 18.5 BRAND/PRODUCT COMPARISON

- 18.6 COMPANY VALUATION AND FINANCIAL METRICS

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Technology footprint

- 18.7.5.4 Investment footprint

- 18.8 COMPETITIVE SCENARIO

- 18.8.1 PRODUCT LAUNCHES

- 18.8.2 DEALS

- 18.8.3 OTHER DEVELOPMENTS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 LOCKHEED MARTIN CORPORATION

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Other developments

- 19.1.1.4 MnM view

- 19.1.1.4.1 Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 RTX

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Deals

- 19.1.2.3.2 Other developments

- 19.1.2.4 MnM view

- 19.1.2.4.1 Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 NORTHROP GRUMMAN

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Other developments

- 19.1.3.4 MnM view

- 19.1.3.4.1 Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weakness and competitive threats

- 19.1.4 BOEING

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Other developments

- 19.1.4.4 MnM view

- 19.1.4.4.1 Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weakness and competitive threats

- 19.1.5 L3HARRIS TECHNOLOGIES, INC.

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 MnM view

- 19.1.5.3.1 Right to win

- 19.1.5.3.2 Strategic choices

- 19.1.5.3.3 Weakness and competitive threats

- 19.1.6 BAE SYSTEMS

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Deals

- 19.1.7 GENERAL DYNAMICS CORPORATION

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Deals

- 19.1.8 THALES

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Other developments

- 19.1.9 ELBIT SYSTEMS LTD.

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Other developments

- 19.1.10 GENERAL ATOMICS

- 19.1.10.1 Business overview

- 19.1.10.2 Products offered

- 19.1.11 LEIDOS

- 19.1.11.1 Business overview

- 19.1.11.2 Products offered

- 19.1.11.3 MnM view

- 19.1.11.3.1 Right to win

- 19.1.11.3.2 Strategic choices

- 19.1.11.3.3 Weaknesses and competitive threats

- 19.1.12 RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- 19.1.12.1 Business overview

- 19.1.12.2 Products offered

- 19.1.12.3 Recent developments

- 19.1.12.3.1 Product launches

- 19.1.12.3.2 Deals

- 19.1.12.3.3 Other developments

- 19.1.12.4 MnM view

- 19.1.12.4.1 Right to win

- 19.1.12.4.2 Strategic choices

- 19.1.12.4.3 Weaknesses and competitive threats

- 19.1.13 EPIRUS INC.

- 19.1.13.1 Business overview

- 19.1.13.2 Products offered

- 19.1.13.3 Recent developments

- 19.1.13.3.1 Deals

- 19.1.13.3.2 Other developments

- 19.1.14 ISRAEL AEROSPACE INDUSTRIES

- 19.1.14.1 Business overview

- 19.1.14.2 Products offered

- 19.1.15 MBDA

- 19.1.15.1 Business overview

- 19.1.15.2 Products offered

- 19.1.15.3 Recent developments

- 19.1.15.3.1 Deals

- 19.1.15.3.2 Other developments

- 19.1.15.4 MnM view

- 19.1.15.4.1 Right to win

- 19.1.15.4.2 Strategic choices

- 19.1.15.4.3 Weaknesses and competitive threats

- 19.1.1 LOCKHEED MARTIN CORPORATION

- 19.2 OTHER PLAYERS

- 19.2.1 AEROVIRONMENT, INC.

- 19.2.2 RHEINMETALL AG

- 19.2.3 MBDA

- 19.2.4 LEONARDO DRS

- 19.2.5 QINETIQ

- 19.2.6 CILAS

- 19.2.7 APPLIED RESEARCH ASSOCIATES, INC.

- 19.2.8 EAGLEPICHER TECHNOLOGIES

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 Primary interview participants

- 20.1.2.2 Key data from primary sources

- 20.1.2.3 Breakdown of primary interviews

- 20.1.2.4 Insights from industry experts

- 20.1.1 SECONDARY DATA

- 20.2 FACTOR ANALYSIS

- 20.2.1 MACRO-ECONOMIC AND POLICY FACTORS

- 20.2.2 INDUSTRY AND OPERATIONAL FACTORS

- 20.2.3 DEMAND-SIDE AND END-USER FACTORS

- 20.2.4 QUANTITATIVE WEIGHTING AND SENSITIVITY

- 20.2.5 DEMAND-SIDE INDICATORS

- 20.2.6 SUPPLY-SIDE INDICATORS

- 20.3 MARKET SIZE ESTIMATION

- 20.3.1 BOTTOM-UP APPROACH

- 20.3.1.1 Market size estimation methodology

- 20.3.2 TOP-DOWN APPROACH

- 20.3.1 BOTTOM-UP APPROACH

- 20.4 DATA TRIANGULATION

- 20.5 RESEARCH ASSUMPTIONS

- 20.6 RESEARCH LIMITATIONS

- 20.7 RISK ASSESSMENT

21 APPENDIX

- 21.1 DISCUSSION GUIDE

- 21.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.3 CUSTOMIZATION OPTIONS

- 21.4 RELATED REPORTS

- 21.5 AUTHOR DETAILS