|

시장보고서

상품코드

2008701

데이터센터용 배관 시장 예측(-2032년) : 배관 유형별, 배관 재질별, 용도별, 데이터센터 유형별, 지역별Data Center Pipes Market by Pipe Type (Pre-Insulated Pipes, Flexible Pipes), Pipe Material (Plastic & Composite Pipes, Stainless Steel Pipes, Carbon Steel Pipes, Copper Pipes), Data Center Type, Applications, and Region - Global Forecast to 2032 |

||||||

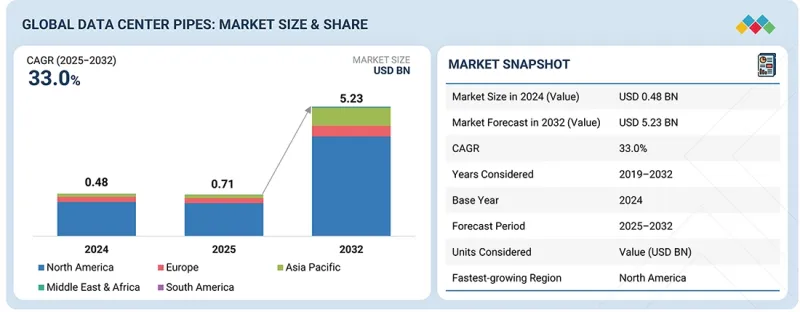

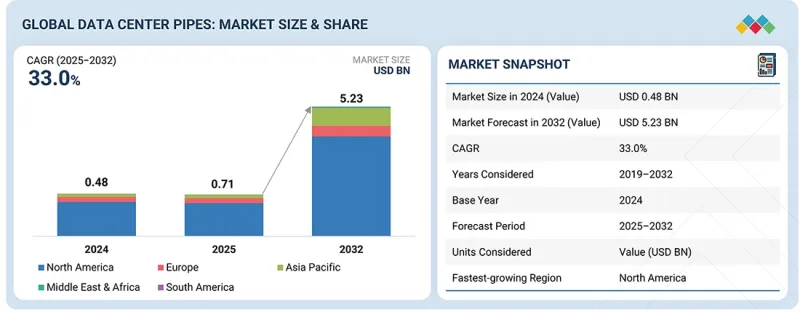

데이터센터용 배관 시장 규모는 예측 기간 중 CAGR 33.0%로 확대하며, 2025년 7억 1,000만 달러에서 2032년에는 52억 3,000만 달러에 달할 것으로 전망되고 있습니다.

미션 크리티컬한 시설에서 인프라의 신뢰성과 위험 감소에 대한 관심이 높아짐에 따라 글로벌 데이터센터 배관 시장이 확대되고 있습니다. 이러한 시설에서는 지속적인 운영에 필수적인 냉각과 유체 순환이 중단 없이 이루어져야 합니다. 서버 밀도의 증가와 열 부하 증가에 직면한 시설 운영자들은 운영 비용과 시스템 장애를 최소화하기 위해 누수 방지와 구조적 강도, 그리고 긴 수명을 겸비한 배관 시스템 선택에 집중하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 대상 단위 | 금액(100만/10억 달러)/킬로톤 |

| 부문 | 배관 유형별, 배관 재질별, 용도별, 데이터센터 유형별, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

조립식 및 모듈식 인프라 시스템의 보급과 함께 신속한 설치가 가능하고, 건설 및 개보수 공사 전 과정에서 품질을 유지할 수 있는 배관 솔루션에 대한 수요가 증가하고 있습니다. 냉각 시스템에서 첨단 모니터링 및 제어 기술의 채택이 확대됨에 따라 이러한 시스템과 호환되는 배관 재료에 대한 수요가 증가하고 있습니다. 현재 수립되고 있는 운영 요구사항으로 인해 현대 데이터센터 시설에서 첨단 배관 시스템에 대한 요구가 증가하고 있습니다.

데이터센터에서는 냉각 시스템 및 유체 수송에서 우수한 성능, 긴 수명, 효율적인 운영을 위해 플라스틱 및 복합재 파이프의 사용이 확대되고 있습니다. 이들 재료는 부식, 스케일 및 화학적 열화에 대한 높은 내성을 통해 원래의 특성을 유지하며 냉각 유체 배관 시스템에서 신뢰할 수 있는 구성 요소로 작용합니다. 제품의 경량 설계로 작업자가 쉽게 취급 및 설치가 가능하여 시공상의 어려움을 줄이고, 대규모 데이터센터 및 모듈형 데이터센터 시스템의 신속한 설치가 가능합니다. 플라스틱 및 복합재 파이프는 내부 표면이 매끄러운 유로를 형성하여 압력 손실을 줄이고 냉각 시스템의 성능을 향상시킵니다. 이 시스템은 다양한 온도 및 습도 변화를 견딜 수 있으며, 현대의 액체 냉각 시스템 및 기존 데이터센터 인프라 프로젝트에서 작동할 수 있습니다.

하이퍼스케일 데이터센터 부문은 데이터센터용 배관 시장에서 가장 큰 점유율을 차지하는 것으로 추정됩니다. 이는 이러한 시설들이 광범위한 인프라를 필요로 하고 대량의 물을 처리해야 하기 때문입니다. 하이퍼스케일 시설은 방대한 클라우드 컴퓨팅 워크로드뿐만 아니라 지속적이고 효율적인 냉각 시스템을 필요로 하는 인공지능 작업 및 디지털 서비스 플랫폼에 대응할 수 있도록 설계되었습니다. 이러한 시설에는 DTC(Direct-to-Chip) 및 액침냉각 기술을 포함한 첨단 액체 냉각 시스템이 적용되며, 냉각수 수송, 열 전달 및 운영상의 신뢰성을 보장하기 위해 대규모 배관 시스템이 필요합니다. 하이퍼스케일 사업자들은 에너지를 절약하면서 시스템을 장시간 가동하는 것을 목표로 하고 있습니다. 따라서 부식에 강하고, 고온에 견디며, 누출을 방지하는 특수 배관 소재를 선호하고 있습니다. 주요 기술 기업 및 클라우드 서비스 프로바이더들은 하이퍼스케일 인프라를 지속적으로 확장하고 있으며, 이는 배관 시스템에 대한 수요를 더욱 증가시키고 있습니다.

열 관리 시스템 운영에는 광범위한 배관이 필요하므로 냉각 시스템 부문은 데이터센터 배관 시장에서 가장 큰 용도를 차지할 것으로 예상됩니다. 냉각 시스템에서는 상호 연결된 배관 네트워크를 이용하여 열교환기, 냉각기, 냉각 분배 장치, 서버 냉각 시스템 등을 통해 냉각제를 순환시킵니다. 인공지능, 클라우드 컴퓨팅, 고성능 워크로드의 확산으로 컴퓨팅 밀도가 높아짐에 따라 데이터센터에는 더 높은 냉각수 유량 용량과 대규모 배관 시스템을 갖춘 첨단 냉각 시스템이 필요합니다. 열 관리를 위해 전용 배관을 필요로 하는 액체 냉각 시스템의 채택이 증가함에 따라 냉각 시스템 도입시 배관 사용량이 증가하고 있습니다. 운영 성능과 에너지 효율을 유지하는 냉각 시스템의 필수적인 기능은 배관 시스템에 대한 지속적인 수요를 창출하여 이 부문이 시장을 독점하는 요인이 되고 있습니다.

GF Piping Systems(스위스), Aquatherm(미국), IPEX USA LLC(미국), BRUGG GROUP COMPANY(스위스), ISCO INDUSTRIES(미국)는 데이터센터용 배관 시장의 주요 기업입니다. 이들 기업은 시장 점유율과 사업 매출을 확대하기 위해 제휴, 합작투자, 사업 확장 등 다양한 전략을 채택하고 있습니다.

조사 범위:

이 보고서는 배관 유형, 배관 재료, 데이터센터 유형, 용도, 지역별로 데이터센터용 파이프 시장 규모를 정의, 세분화, 예측하고 있습니다. 주요 기업의 전략적 프로파일을 작성하고 시장 점유율과 핵심 경쟁력을 종합적으로 분석합니다. 또한 시장내 각 기업의 사업 확장, 계약, 인수 등 경쟁 동향을 추적 및 분석하고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 데이터센터 배관 시장과 각 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것으로 기대됩니다. 또한 이 보고서는 이해관계자들이 시장의 경쟁 상황을 보다 깊이 이해하고, 사업적 입지를 강화하기 위한 귀중한 인사이트를 얻고, 효과적인 시장 진입 전략을 수립하는 데 도움이 될 것으로 기대됩니다. 또한 이해관계자들이 시장 동향을 파악할 수 있도록 주요 시장 촉진요인, 제약 조건, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(액체 냉각 기술 채택 확대, 하이퍼스케일 및 코로케이션 데이터센터 확장, 에너지 효율 및 운영 안정성에 대한 관심), 억제요인(높은 초기 인프라 및 설치 비용, 기존 인프라와의 복잡한 통합, 재료 성능 및 내구성 문제), 기회(모듈형 및 조립식 데이터센터 인프라 확장, 엣지 데이터센터 인프라 확장, 지속가능하고 진보된 배관 재료 개발), 도전 과제(누수 방지, 시스템 무결성 유지, 누수 방지, 시스템 무결성 유지)를 분석했습니다. 모듈형 및 조립식 데이터센터 채택 확대, 엣지 데이터센터 인프라 확장, 지속가능한 첨단 배관 재료 개발), 도전과제(누수 방지 및 시스템 무결성 유지, 다양한 냉각 시스템 요구사항 관리)에 대한 인사이트를 제공하며, 데이터센터 배관 시장의 성장에 영향을 미칠 것으로 예상됩니다. 데이터센터 배관 시장의 성장에 영향을 미치고 있습니다.

- 제품 개발/혁신: 데이터센터 배관 시장의 미래 기술 동향과 R&D 활동에 대한 심층적인 인사이트

- 시장 동향: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 다양한 지역의 데이터센터 배관 시장을 분석합니다.

- 시장 다각화: 데이터센터 배관 시장의 신제품, 다양한 유형, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보를 제공합니다.

- 경쟁사 분석: GF Piping Systems(스위스), Aquatherm(미국), IPEX USA LLC(미국), BRUGG GROUP COMPANY(스위스), ISCO INDUSTRIES(미국) 등 데이터센터용 배관 시장의 주요 기업별 시장점유율, 성장전략, 제품 라인업에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 데이터센터용 배관 시장(배관 유형별)

제10장 데이터센터용 배관 시장(배관 재질별)

제11장 데이터센터용 배관 시장(용도별)

제12장 데이터센터용 배관 시장(데이터센터 유형별)

제13장 데이터센터용 배관 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.04.29The data center pipes market is projected to grow from USD 0.71 billion in 2025 to USD 5.23 billion by 2032, at a CAGR of 33.0% during the forecast period. The global data center pipes market is expanding as the focus on infrastructure reliability and risk mitigation in mission-critical facilities intensifies, where uninterrupted cooling and fluid circulation are essential for continuous operations. Operators in facilities with rising server densities and increasing thermal loads focus on selecting piping systems that combine leak resistance and structural strength with long service life to minimize operational expenses and system breakdowns.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) / Volume (Kiloton) |

| Segments | Pipe Type, Pipe Material, Data Center Type, Application, and Region |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

The demand for piping solutions that provide fast installation and maintain quality throughout construction and retrofit operations has increased as prefabricated and modular infrastructure systems become more prevalent. The growing adoption of advanced monitoring and control technologies in cooling systems is driving demand for piping materials compatible with these systems. The operational requirements currently being developed create an increasing need for advanced piping systems in contemporary data center facilities.

"By pipe material, the plastic & composite pipes segment is estimated to hold the largest share, in terms of volume, during the forecast period."

Data centers are increasingly using plastic and composite pipes as these materials offer excellent performance, long-lasting durability, and efficient operation for cooling systems and fluid transportation. The materials retain their original state due to their high resistance to corrosion, scaling, and chemical deterioration, enabling them to serve as dependable components in cooling fluid distribution systems. The product's lightweight design allows workers to handle and install it easily, reducing construction difficulties and enabling quick installation of both large data centers and modular data center systems. Plastic and composite pipes deliver internal surfaces that create smooth flow paths, reducing pressure losses and enhancing the performance of cooling systems. The system can withstand various temperature and moisture changes, enabling it to function in contemporary liquid-cooling systems and existing data center infrastructure projects.

"By data center type, the hyperscale data centers segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The hyperscale data center segment is estimated to account for the largest share in the data center pipes market, as these facilities require extensive infrastructure and handle large volumes of water. Hyperscale facilities are built to handle massive cloud computing workloads, as well as artificial intelligence tasks and digital service platforms that require constant, efficient cooling systems. These facilities use advanced liquid-cooling systems that include direct-to-chip and immersion cooling technologies, which require extensive pipe systems for coolant transport, heat transfer, and operational dependability. Hyperscale operators want to keep their systems operational for extended periods while saving energy. They prefer specialized piping materials that resist corrosion, withstand high temperatures, and prevent leaks. Major technology companies and cloud service providers continue to expand their hyperscale infrastructure, creating additional demand for piping systems.

"By application, the cooling systems segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The cooling systems segment is estimated to be the largest application in the data center pipes market, as thermal management systems require extensive piping for their operations. Cooling systems use interconnected piping networks to move coolants through their systems, which include heat exchangers, chillers, cooling distribution units, and server cooling systems. Data centers need advanced cooling systems that provide higher coolant flow capacity and larger piping systems, as artificial intelligence, cloud computing, and high-performance workloads increase computing density. The increasing use of liquid-based cooling systems, which require specialized piping to manage heat, results in greater pipe usage in cooling system implementations. The essential function of cooling systems in maintaining operational performance and energy efficiency creates ongoing demand for piping systems, enabling this segment to dominate the market.

Break-up of primary participants for the report:

- By Company Type: Tier 1 - 65%, Tier 2 - 20%, and Tier 3 - 15%

- By Designation: C-Level Executives- 25%, Directors- 30%, and Others - 45%

- By Region: North America - 30%, Asia Pacific - 40%, Europe - 20%, Middle East & Africa - 7%, and South America - 3%

GF Piping Systems (Switzerland), Aquatherm (US), IPEX USA LLC (US), BRUGG GROUP COMPANY (Switzerland), and ISCO INDUSTRIES (US) are the key players in the data center pipes market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines, segments, and projects the size of the data center pipes market by pipe type, pipe material, data center type, application, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the data center pipes market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Rising adoption of liquid cooling technologies, Expansion of hyperscale and colocation data centers, Focus on energy efficiency and operational reliability), restraints (High initial infrastructure and installation costs, Complex integration with existing infrastructure, Material performance and durability concerns), opportunities (Growing adoption of modular and prefabricated data centers, Expansion of edge data center infrastructure, Development of sustainable and advanced pipe materials), and challenges (Maintaining leak prevention and system integrity, Managing diverse cooling system requirements) influencing the growth of the data center pipes market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the data center pipes market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the data center pipes market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the data center pipes market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as GF Piping Systems (Switzerland), Aquatherm (US), IPEX USA LLC (US), BRUGG GROUP COMPANY (Switzerland), ISCO INDUSTRIES (US), and others are the key players in the data center pipes market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER PIPES MARKET

- 3.2 DATA CENTER PIPES MARKET, BY PIPE TYPE

- 3.3 DATA CENTER PIPES MARKET, BY PIPE MATERIAL

- 3.4 DATA CENTER PIPES MARKET, BY REGION

- 3.5 DATA CENTER PIPES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expansion of high-density computing like AI and hyperscale data centers

- 4.2.1.2 Rising shift toward data center liquid cooling architectures

- 4.2.1.3 Energy efficiency & sustainability regulations

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial capital investment

- 4.2.2.2 Leakage & reliability concerns

- 4.2.2.3 Retrofitting & maintenance challenges

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration with smart & digital technologies

- 4.2.3.2 Development of advanced materials & smart piping systems

- 4.2.3.3 Modular & prefabricated data center designs

- 4.2.4 CHALLENGES

- 4.2.4.1 Thermal management complexity at high densities

- 4.2.4.2 Lack of standardization

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER PIPES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS

- 5.2.3 TRENDS IN DATA CENTER INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DATA CENTER COOLING INDUSTRY

- 5.2.5 MANUFACTURING INDUSTRY

- 5.2.6 TRENDS IN GLOBAL HYPERSCALE AND AI DATA CENTER INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 IMPORT SCENARIO (HS CODE 3917)

- 5.5.2 EXPORT SCENARIO (HS CODE 3917)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DATA CENTER PIPING SYSTEM FOR CHILLED WATER COOLING

- 5.9.2 HIGH-RELIABILITY PIPING SYSTEM FOR NOVVA DATA CENTER

- 5.9.3 OFF-SITE PREFABRICATION FOR HYPERSCALE DATA CENTER - DUBLIN

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED PIPE MATERIALS ENGINEERING

- 6.1.2 LIQUID COOLING PIPE SYSTEMS

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 PREFABRICATION & MODULAR PIPE MANUFACTURING

- 6.2.2 HEAT PIPE TECHNOLOGY

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 SMART/SENSOR-INTEGRATED PIPES

- 6.3.2 INSULATED & PRE-INSULATED PIPE SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2026-2028) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2028-2032) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2032-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AI & HIGH-DENSITY COMPUTING COOLING SYSTEMS: NEXT-GENERATION COOLING INFRASTRUCTURE

- 6.5.2 TWO-PHASE & IMMERSION COOLING INFRASTRUCTURE: CLOSED-LOOP THERMAL CYCLES

- 6.5.3 SMART & AUTONOMOUS DATA CENTER OPERATIONS: INTEGRATION OF IOT-ENABLED SMART PIPES

- 6.5.4 SUSTAINABLE & WATER-EFFICIENT COOLING SYSTEMS: CARBON-NEUTRAL DATA CENTER INITIATIVES

- 6.5.5 MODULAR & PREFABRICATED DATA CENTER DESIGNS: REDUCING CONSTRUCTION TIME

- 6.6 IMPACT OF AI/GEN AI ON DATA CENTER PIPES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN ADOPTION OF DATA CENTER PIPES

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN DATA CENTER PIPES MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DATA CENTER PIPES MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 SCHNEIDER ELECTRIC: THE LIQUID COOLING REVOLUTION

- 6.7.2 T5 DATA CENTERS: DELIVERING A LIQUID COOLING SOLUTION

- 6.7.3 UV NETWARE: AI-DRIVEN DEMAND & SUSTAINABLE COOLING

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF DATA CENTER PIPES

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF DATA CENTER PIPES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITIBILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 DATA CENTER PIPES MARKET, BY PIPE TYPE

- 9.1 INTRODUCTION

- 9.2 PRE-INSULATED PIPES

- 9.2.1 RISING NEED FOR EFFICIENT THERMAL INSULATION AND ENERGY-EFFICIENT COOLING DISTRIBUTION TO INCREASE DEMAND

- 9.3 FLEXIBLE PIPES

- 9.3.1 RAPID ADOPTION OF LIQUID COOLING IN HIGH-PERFORMANCE COMPUTING AND AI-DRIVEN DATA CENTERS TO DRIVE DEMAND

- 9.4 DOUBLE-CONTAINMENT SYSTEMS

- 9.4.1 NEED TO PREVENT COOLANT LEAKAGE IN HIGH-DENSITY LIQUID-COOLED FACILITIES TO INCREASE ADOPTION

- 9.5 RIGID PIPES

- 9.5.1 EXPANSION OF HYPERSCALE FACILITIES AND NEW DATA CENTER CAMPUSES TO PROPEL MARKET

10 DATA CENTER PIPES MARKET, BY PIPE MATERIAL

- 10.1 INTRODUCTION

- 10.2 CARBON STEEL PIPES

- 10.2.1 EXPANSION OF HYPERSCALE DATA CENTERS AND LARGE-SCALE AI COMPUTING FACILITIES TO DRIVE MARKET

- 10.3 STAINLESS STEEL PIPES

- 10.3.1 ADOPTION OF LIQUID COOLING TECHNOLOGIES DRIVEN BY AI, MACHINE LEARNING WORKLOADS, AND HIGH-DENSITY COMPUTING CLUSTERS TO DRIVE MARKET

- 10.4 COPPER PIPES

- 10.4.1 RISING DEPLOYMENT OF PRECISION COOLING SYSTEMS AND EXPANSION OF EDGE DATA CENTERS TO INCREASE DEMAND

- 10.5 PLASTIC & COMPOSITE PIPES

- 10.5.1 GROWTH OF MODULAR DATA CENTER CONSTRUCTION AND NEED FOR CORROSION-RESISTANT INFRASTRUCTURE TO DRIVE MARKET

- 10.6 OTHER MATERIALS

- 10.6.1 ADOPTION OF FLEXIBLE AND LIGHTWEIGHT PIPING SOLUTIONS IN ADVANCED DATA CENTER COOLING SYSTEMS TO BOOST DEMAND

11 DATA CENTER PIPES MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 COOLING SYSTEMS

- 11.2.1 RISING ADOPTION OF LIQUID COOLING AND HIGH-DENSITY COMPUTING INFRASTRUCTURE TO BOOST MARKET

- 11.3 FIRE SUPPRESSION

- 11.3.1 CONSTRUCTION OF LARGE-SCALE DATA CENTERS AND STRINGENT SAFETY REGULATIONS TO INCREASE DEMAND

- 11.4 FUEL SUPPLY

- 11.4.1 NEED FOR RELIABLE BACKUP POWER INFRASTRUCTURE IN DATA CENTERS TO DRIVE MARKET

- 11.5 DRAINAGE & WASTE

- 11.5.1 EXPANSION OF WATER-BASED COOLING SYSTEMS AND FACILITY MANAGEMENT REQUIREMENTS TO BOOST MARKET GROWTH

- 11.6 OTHER APPLICATIONS

- 11.6.1 INCREASING FOCUS ON ENVIRONMENTAL CONTROL AND WATER EFFICIENCY IN DATA CENTERS TO INCREASE DEMAND

12 DATA CENTER PIPES MARKET, BY DATA CENTER TYPE

- 12.1 INTRODUCTION

- 12.2 HYPERSCALE DATA CENTERS

- 12.2.1 EXPANSION OF LARGE-SCALE CLOUD AND AI INFRASTRUCTURE REQUIRING EXTENSIVE COOLING NETWORKS TO BOOST MARKET

- 12.3 COLOCATION DATA CENTERS

- 12.3.1 RISING DEMAND FOR SCALABLE MULTI-TENANT DATA CENTER FACILITIES TO INCREASE DEMAND

- 12.4 ENTERPRISE DATA CENTERS

- 12.4.1 MODERNIZATION OF IN-HOUSE IT INFRASTRUCTURE AND COOLING SYSTEM UPGRADES TO DRIVE MARKET

13 DATA CENTER PIPES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 AI-driven hyperscale data center expansion and increasing adoption of liquid cooling technologies to drive market

- 13.2.2 CANADA

- 13.2.2.1 Renewable-powered hyperscale projects and energy-efficient cooling infrastructure to increase demand

- 13.2.3 MEXICO

- 13.2.3.1 Rapid cloud expansion, hyperscale investments, and nearshoring-driven data center development to propel market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Large technology investments and expansion of high-density data centers to boost market growth

- 13.3.2 UK

- 13.3.2.1 Government initiatives on large-scale AI infrastructure deployment and hyperscale cloud capacity to support market

- 13.3.3 FRANCE

- 13.3.3.1 Expansion of AI-ready hyperscale data centers to fuel market growth

- 13.3.4 ITALY

- 13.3.4.1 Rapid growth of AI and hyperscale data centers supported by government initiatives to drive demand

- 13.3.5 RUSSIA

- 13.3.5.1 Increase in demand for advanced cooling systems to fuel market

- 13.3.6 NETHERLANDS

- 13.3.6.1 Expansion of high-capacity and AI-ready data center campuses increasing deployment of advanced cooling infrastructure

- 13.3.7 SPAIN

- 13.3.7.1 Hyperscale cloud and AI infrastructure investments to drive demand for advanced cooling and piping systems

- 13.3.8 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Large-scale AI and hyperscale cloud data center expansion to drive market

- 13.4.2 JAPAN

- 13.4.2.1 Rapid growth of AI computing campuses, high-density GPU clusters, and liquid cooling adoption to boost market growth

- 13.4.3 INDIA

- 13.4.3.1 High hyperscale AI and cloud investments supported by government initiatives to fuel market

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Expansion of AI-ready hyperscale facilities and government policies promoting energy-efficient cooling systems to boost market

- 13.4.5 THAILAND

- 13.4.5.1 Large-scale hyperscale data center investments supported by government policies to drive market

- 13.4.6 INDONESIA

- 13.4.6.1 Digital surge and supportive policies accelerating data center pipe demand

- 13.4.7 AUSTRALIA

- 13.4.7.1 Large hyperscale AI campuses and government-backed digital infrastructure projects to boost market growth

- 13.4.8 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Technology collaborations and investments, along with hyperscale AI data centers, to drive demand

- 13.5.1.2 UAE

- 13.5.1.2.1 Expansion of hyperscale facilities and cloud partnerships to increase demand for high-performance pipe networks

- 13.5.1.3 Rest of GCC Countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Rapid expansion of hyperscale and AI-ready facilities in major cities to create high demand for piping systems

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Rise in adoption of cloud computing, artificial intelligence workloads, and high-performance computing to increase demand

- 13.6.2 ARGENTINA

- 13.6.2.1 Investments in digital infrastructure, hyperscale facilities, and colocation data centers to increase demand

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.3.1 TOP 4 PLAYERS' REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 BRAND/PRODUCT COMPARISON

- 14.5.1 COOL-FIT 2.0

- 14.5.2 AQUATHERM BLUE

- 14.5.3 GUARDIAN

- 14.5.4 DATA MASTER MEGAFLEX

- 14.5.5 MICROFLEX

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Pipe material footprint

- 14.6.5.4 Data center type footprint

- 14.6.5.5 Application footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT LAUNCHES

- 14.8.2 DEALS

- 14.8.3 EXPANSIONS

- 14.9 COMPANY VALUATION AND FINANCIAL METRICS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 GF PIPING SYSTEMS

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 PARKER-HANNIFIN CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 MnM view

- 15.1.2.3.1 Right to win

- 15.1.2.3.2 Strategic choices

- 15.1.2.3.3 Weaknesses and competitive threats

- 15.1.3 GATES INDUSTRIAL CORPORATION PLC

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 WATTS

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 MnM view

- 15.1.4.3.1 Right to win

- 15.1.4.3.2 Strategic choices

- 15.1.4.3.3 Weaknesses and competitive threats

- 15.1.5 IPEX USA LLC

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 AQUATHERM GMBH

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 FUTURE PIPE INDUSTRIES

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.8 STEEL & O'BRIEN

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 BRUGG GROUP COMPANY

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 POLYMELT PIPE SYSTEMS GMBH

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.11 AGRU KUNSTSTOFFTECHNIK GMBH

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.12 ALFA GOMMA SPA

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.13 ZEKELMAN INDUSTRIES

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.14 PENFLEX

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.15 ISCO INDUSTRIES

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.16 LUOHE LETONE HYDRAULIC TECHNOLOGY CO., LTD.

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.17 KPS

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.18 AEROFLEX INDUSTRIES LIMITED

- 15.1.18.1 Business overview

- 15.1.18.2 Products/Solutions/Services offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Expansions

- 15.1.19 CONTINENTAL AG

- 15.1.19.1 Business overview

- 15.1.19.2 Products/Solutions/Services offered

- 15.1.1 GF PIPING SYSTEMS

- 15.2 OTHER PLAYERS

- 15.2.1 HEAT PIPE TECHNOLOGY INC.

- 15.2.2 ZHONGTONG PIPE CO. LTD

- 15.2.3 TUDERTECHNICA

- 15.2.4 CENFLEX, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 List of primary participants

- 16.1.2.4 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 DEMAND-SIDE ANALYSIS

- 16.4 SUPPLY-SIDE ANALYSIS

- 16.4.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 16.5 GROWTH FORECAST

- 16.6 DATA TRIANGULATION

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS

- 16.9 RISK ASSESSMENT

- 16.10 FACTOR ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS