|

시장보고서

상품코드

2008704

단일 소재 포장 필름 시장 : 유형별(PE, PP, PET, PVC), 포장 형태별(파우치, 백, 필름 및 랩, 롤스탁 및 시트), 최종 이용 산업별(식품 및 음료, 퍼스널케어 및 화장품, 의약품 및 의료), 지역별 - 세계 예측(-2030년)Monomaterial Packaging Films Market by Type (PE, PP, PET, PVC), Packaging Format (Pouch, Bag, Film & Wrap, Rollstock & Sheet), End-Use Industry (Food & Beverage, Personal Care & Cosmetic, Pharmaceutical & Medical), and Region - Global Forecast to 2030 |

||||||

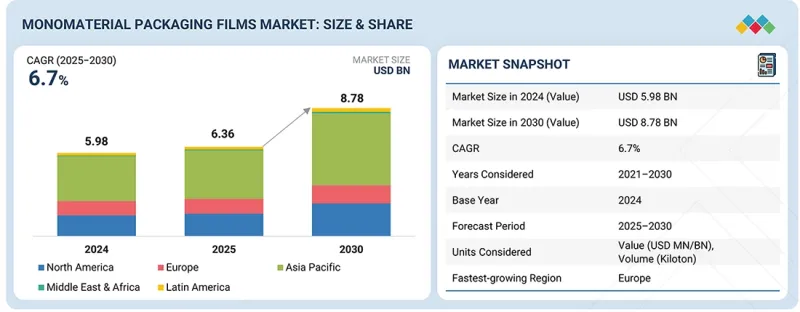

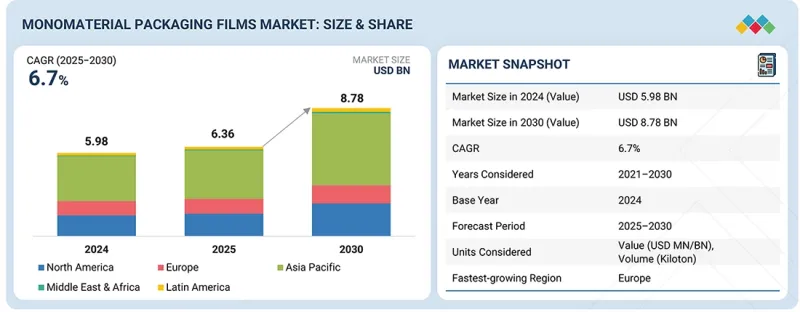

단일 소재 포장 필름 시장 규모는 예측 기간 동안 CAGR 6.7%로 확대되어 2025년 63억 6,000만 달러에서 2030년에는 87억 8,000만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러)·킬로톤 |

| 부문 | 유형, 포장 형태, 최종 이용 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

재활용 가능성과 순환형 소재에 대한 전 세계적인 노력의 증가로 인해 단일 소재 포장 필름의 수요는 앞으로도 계속 가속화될 것입니다.

"예측 기간 동안 PE가 가장 큰 부문이 될 것으로 예상됩니다."

PE 부문은 식품, 음료, 가정용품, 퍼스널케어 제품 포장에 널리 사용되는 다목적성, 비용 효율성, 식품, 음료, 가정용품, 퍼스널케어 제품 포장에 널리 사용되기 때문에 예측 기간 동안 시장에서 가장 큰 부문으로 남을 것으로 예상됩니다. 우수한 밀봉성, 유연성, 단일 소재의 재활용 가능한 구조와의 적합성으로 인해 순환형 사회 실현을 위한 포장 솔루션 채택을 추진하는 브랜드에서 선택되고 있습니다. 또한, 고차단성 모노 PE 필름의 지속적인 기술 혁신, 기계적 특성 향상 및 가공 성능 개선으로 인해 그 용도가 더욱 확대되어 주요 최종사용자 시장에서 이 부문의 우위에 큰 영향을 미치고 있습니다.

"예측 기간 동안 파우치가 가장 큰 부문이 될 것으로 예상됩니다."

파우치 부문은 다재다능하고, 가볍고, 모노머 포장 솔루션과 호환이 가능하기 때문에 예측 기간 동안 가장 큰 부문이 될 것으로 예상됩니다. 파우치는 높은 차단성, 적은 재료 소비, 휴대성이 뛰어나 식품, 음료, 퍼스널케어, 의약품에 적합합니다. 또한 고급 모노 PE 필름 및 모노 PP 필름과 호환이 가능하기 때문에 브랜드의 재활용 대응이 진전됨에 따라 그 채택이 더욱 증가하고 있습니다. 지속가능하면서도 작고 편리한 포장에 대한 수요 증가도 각 산업 분야에서 파우치 보급을 촉진하고 있습니다.

"예측 기간 동안 식음료 부문이 가장 큰 시장 규모가 될 것으로 예상됩니다."

식음료 부문은 가볍고 재활용이 가능하며 연포장재 사용량이 가장 많기 때문에 예측 기간 동안 가장 두드러진 성장을 보일 것으로 예상됩니다. 스낵, 유제품, 베이커리 제품, 냉동식품, 즉석식품, 휴대용 음료에 대한 지속적인 수요 확대가 단일 소재 필름, 파우치, 랩에 대한 수요를 견인하고 있습니다. 기업들이 규제 및 소비자 요구 사항을 충족시키기 위해 지속가능한 모노 PE 및 모노 PP 설계로 전환함에 따라 식품 및 음료는 단일 소재 포장의 가장 중요한 촉진제가 되고 있습니다.

"금액 기준으로는 아시아태평양이 예측 기간 동안 가장 큰 부문이 될 것으로 예상됩니다."

아시아태평양은 방대한 소비자 인구, 급속한 도시화, 가공식품, 퍼스널케어, 제약 산업의 성장으로 인해 예측 기간 동안 가장 큰 지역으로 남을 것으로 예상됩니다. 중국, 인도, 일본, 동남아시아의 주요 시장에서는 탄탄한 제조 기반, 소매 및 단일 소재 포장 필름 유통 채널의 확대, 지속가능한 포장 솔루션에 대한 선호도 증가로 인해 단일 소재 필름으로의 전환이 가속화되고 있습니다. 또한, 각국 정부의 다양한 지속가능성 이니셔티브는 아시아태평양을 가장 큰 성장 지역으로서의 역할을 강화하고 있습니다.

세계의 단일 소재 포장 필름 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

제6장 업계 동향

제7장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 디스럽션

제8장 지속가능성과 규제 상황

제9장 고객 상황과 구매 행동

제10장 단일 소재 포장 필름 시장 : 포장 형태별

제11장 단일 소재 포장 필름 시장 : 유형별

제12장 단일 소재 포장 필름 시장 : 최종 이용 산업별

제13장 단일 소재 포장 필름 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 부록

KSM 26.04.30The monomaterial packaging films market is projected to grow from USD 6.36 billion in 2025 to USD 8.78 billion by 2030, at a CAGR of 6.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) Volume (Kiloton) |

| Segments | Type, Packaging Format, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

Growing global commitments to recyclability and circular materials will continue to accelerate demand for monomaterial packaging films.

"PE projected to be the largest segment during the forecast period"

PE segment is expected to remain the largest segment of the monomaterial packaging films market during the forecast period because it is versatile, cost-effective, and is commonly used in food, beverages, household, and personal care packaging. Its good sealability, flexibility, and compatibility with monomaterial recyclable structures make it the choice of brands moving to use its packaging solutions to achieve circularity. Additionally, continuous innovation in high-barrier mono-PE films, enhancements in mechanical properties, and improved processing performance have further expanded its usage, which has a significant impact on its dominance in key end-use markets.

"Pouches projected to be the largest segment during the forecast period"

The pouches segment is expected to be the largest in the projected forecasting period because it has the capacity to be versatile, lightweight, and compatible with the monomaterial packaging solutions. Pouches possess high barrier properties, low material consumption, and portability, making them suitable for food, beverages, personal care, and pharmaceutical products. Their ability to be compatible with further advanced mono-PE and mono-PP films further increases their adoption as brands become recyclable. The popularity of pouches in various industries has been further enhanced by the growing demand for small and convenient packaging that is also sustainable.

"Food & beverages projected to be the largest segment during the forecast period"

The food & beverages segment will be the most prominent over the estimated period, as this sector has the greatest usage of light, recyclable, and flexible packaging materials. The continuous growth in demand for snacks, dairy products, bakery products, frozen foods, ready-to-eat services, and on-the-go beverages is driving the demand for monomaterial films, pouches, and wraps. Food and beverages are the most significant drivers of monomaterial use packaging, as brands are transitioning to sustainable mono-PE and mono-PP designs to meet regulatory and consumer demands.

"In terms of value, Asia Pacific projected to be the largest segment during the forecast period"

Asia Pacific is expected to remain the largest region during the forecast period owing to its sizeable consumer population, rapid urbanization, and growth of packaged food, personal care, and pharmaceutical industries. Strong manufacturing bases, expanding retail and monomaterial packaging film channels, and an increasing preference for sustainable packaging solutions are accelerating the shift toward monomaterial films in key markets across China, India, Japan, and Southeast Asia. In addition, several sustainability initiatives undertaken by governments are bolstering the APAC region's role as the largest growth region.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 billion; Tier 2: USD 500 million-1 billion; and Tier 3: <USD 500 million

Companies Covered: Amcor Plc (Switzerland), Mondi (UK), TOPPAN Holdings Inc. (Japan), SABIC (Saudi Arabia), Klockner Pentaplast (Germany), Huhtamaki (Finland), Constantia Flexibles (Austria), Sealed Air (US), Transcontinental Inc. (Canada), and UFlex Limited (India), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the monomaterial packaging films market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the monomaterial packaging films market based on type (PE, PP, PET, PVC, and other types), packaging format (pouches, bags, films & wraps, rollstock & sheets, and other packaging formats), end-use industry (food & beverages, personal care & cosmetics, pharmaceutical & medical, household products, and other end-use industries), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope encompasses detailed information regarding the drivers, restraints, challenges, and opportunities that influence the growth of the monomaterial packaging films market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, products offered, and key strategies, including partnerships, collaborations, product launches, expansions, and acquisitions, associated with the monomaterial packaging films market. This report covers a competitive analysis of upcoming startups in the monomaterial packaging films market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall monomaterial packaging films market and its subsegments. This report will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses more effectively, and develop suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Regulatory prioritization of single-polymer recyclability, escalating pressure to reduce multi-polymer waste in landfills and oceans, recycling gaps push global shift toward fully recyclable monomaterial films), restraints (Higher resin cost volatility for PE and PP grades, performance gaps in moisture, oxygen, and aroma barriers), opportunities (Post-consumer recycled (PCR) polyethylene supply chain integration, strategic partnerships with global mechanical & chemical recyclers), and challenges (Replicating multi-layer functional performance, inconsistent film recycling infrastructure and contamination sensitivity).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the monomaterial packaging films market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the monomaterial packaging films market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the monomaterial packaging films market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Amcor Plc (Switzerland), Mondi (UK), TOPPAN Holdings Inc. (Japan), SABIC (Saudi Arabia), Klockner Pentaplast (Germany), Huhtamaki (Finland), Constantia Flexibles (Austria), Sealed Air (US), Transcontinental Inc. (Canada), and UFlex Limited (India).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.2 SECONDARY DATA

- 2.2.1 KEY DATA FROM SECONDARY SOURCES

- 2.3 PRIMARY DATA

- 2.3.1 KEY DATA FROM PRIMARY SOURCES

- 2.4 MARKET SIZE ESTIMATION

- 2.5 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- 2.8 GROWTH RATE ASSUMPTIONS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIONS SHAPING MONOMATERIAL PACKAGING FILMS MARKET

- 3.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MONOMATERIAL PACKAGING FILMS MARKET

- 4.2 MONOMATERIAL PACKAGING FILMS MARKET, BY TYPE AND REGION

- 4.3 MONOMATERIAL PACKAGING FILMS MARKET, BY PACKAGING FORMAT

- 4.4 MONOMATERIAL PACKAGING FILMS MARKET, BY END-USE INDUSTRY

- 4.5 MONOMATERIAL PACKAGING FILMS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Regulatory prioritization of single-polymer recyclability

- 5.2.1.2 Escalating pressure to reduce multi-polymer waste in landfills and oceans

- 5.2.1.3 Recycling gaps push global shift toward fully recyclable monomaterial films

- 5.2.1.4 E-commerce growth demand for lightweight, protective, single-material pouches

- 5.2.2 RESTRAINTS

- 5.2.2.1 Higher resin cost volatility for PE and PP grades

- 5.2.2.2 Performance gaps in moisture, oxygen, and aroma barriers

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Post-consumer Recycled (PCR) polyethylene supply chain integration

- 5.2.3.2 Strategic partnerships with global mechanical & chemical recyclers

- 5.2.4 CHALLENGES

- 5.2.4.1 Replicating multi-layer functional performance

- 5.2.4.2 Inconsistent film recycling infrastructure and contamination sensitivity

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 COST REDUCTION IN ADVANCED MONOMATERIAL FILMS USING BIO-BASED OR RECYCLED FEEDSTOCK WHILE RETAINING FILM PERFORMANCE

- 5.3.2 HIGH-STIFFNESS MONO-FILMS THAT CAN TRULY REPLACE PET IN POUCHES

- 5.3.3 TAILORED BARRIER SOLUTIONS IN MONO FILMS FOR SENSITIVE HIGH-VALUE PRODUCTS (PHARMACEUTICALS, COSMETICS) REQUIRING ULTRA-LOW GAS TRANSMISSION

- 5.3.4 REGION-SPECIFIC SOLUTIONS ADDRESSING REGULATORY, INFRASTRUCTURE, AND MARKET MATURITY VARIATIONS IN MONOMATERIAL PACKAGING UPTAKE

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 5.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING INNOVATION AND SCALE IN MONOMATERIAL FILMS

- 5.5.1.1 Amcor

- 5.5.1.2 Mondi

- 5.5.2 TIER 2 PLAYERS: KEY INNOVATORS EXPANDING CIRCULARITY AND MARKET REACH

- 5.5.2.1 Innovia Films

- 5.5.2.2 UFlex Limited

- 5.5.3 TIER 3 PLAYERS: EMERGING SPECIALISTS ADVANCING NICHE MONOMATERIAL SOLUTIONS

- 5.5.3.1 ITP Spa

- 5.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING INNOVATION AND SCALE IN MONOMATERIAL FILMS

6 INDUSTRY TRENDS

- 6.1 PORTER'S FIVE FORCES ANALYSIS

- 6.1.1 THREAT OF NEW ENTRANTS

- 6.1.2 THREAT OF SUBSTITUTES

- 6.1.3 BARGAINING POWER OF SUPPLIERS

- 6.1.4 BARGAINING POWER OF BUYERS

- 6.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.2 MACROECONOMIC ANALYSIS

- 6.2.1 INTRODUCTION

- 6.2.2 GDP TRENDS AND FORECASTS

- 6.2.3 TRADE AND GLOBAL SUPPLY CHAIN DYNAMICS

- 6.3 VALUE CHAIN ANALYSIS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE TREND AMONG KEY PLAYERS, BY TYPE

- 6.5.2 AVERAGE SELLING PRICE TREND AMONG KEY PLAYERS, BY REGION

- 6.6 TRADE ANALYSIS

- 6.6.1 IMPORT DATA RELATED TO HS CODE 392010, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 6.6.2 EXPORT DATA RELATED TO HS CODE 392010, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 6.6.3 IMPORT DATA RELATED TO HS CODE 390210, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 6.6.4 EXPORT DATA RELATED TO HS CODE 390210, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 6.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.9 INVESTMENT AND FUNDING SCENARIO

- 6.9.1 INVESTMENT AND FUNDING SCENARIO

- 6.10 CASE STUDY ANALYSIS

- 6.10.1 ALL-PP RECYCLABLE LAMINATE WITH SOLVENT-FREE ADHESIVE

- 6.10.2 ALL-PE RECYCLABLE MOZZARELLA PACKAGING BY AMCOR & PFM

- 6.10.3 MONO-PP RECYCLABLE CHEESE FILM BY MONDI & SKANEMEJERIER

- 6.11 IMPACT OF 2025 US TARIFF ON MONOMATERIAL PACKAGING FILMS MARKET

- 6.11.1 INTRODUCTION

- 6.11.2 KEY TARIFF RATES

- 6.11.3 PRICE IMPACT ANALYSIS

- 6.11.4 KEY IMPACT ON VARIOUS REGIONS

- 6.11.4.1 US

- 6.11.4.2 Europe

- 6.11.4.3 Asia Pacific

- 6.11.5 END-USE INDUSTRY IMPACT

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 7.1 KEY TECHNOLOGIES

- 7.1.1 MACHINE-DIRECTION AND DOUBLE-ORIENTATION (MDO/DO) FILM STRETCHING

- 7.1.2 METALLOCENE & CONTROLLED-ARCHITECTURE POLYOLEFIN RESINS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 SOLVENTLESS POLYOLEFIN LAMINATION SYSTEMS

- 7.2.2 RECYCLABLE BARRIER TECHNOLOGIES (SIOX, ALOX, AND HIGH-BARRIER EVOH-IN-PE/PP DESIGN)

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 POLYOLEFIN CHEMICAL RECYCLING & SOLVENT PURIFICATION SYSTEMS

- 7.3.2 SMART MATERIAL TRACEABILITY & DIGITAL COMPLIANCE PLATFORMS

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.4.1 SHORT-TERM (2025-2027): PERFORMANCE STABILIZATION & MANUFACTURING INTEGRATION PHASE

- 7.4.2 MID-TERM (2027-2030): ADVANCED MATERIAL ENGINEERING & SYSTEM-LEVEL INTEGRATION PHASE

- 7.4.3 LONG-TERM (2030-2035+): FULL CIRCULARIZATION & MATERIAL CONVERGENCE PHASE

- 7.5 PATENT ANALYSIS

- 7.5.1 INTRODUCTION

- 7.5.2 APPROACH

- 7.5.3 TOP APPLICANTS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 MONOMATERIAL SMART-SENSOR FILMS FOR CONDITION MONITORING

- 7.6.2 MONOMATERIAL FILMS FOR SPACE-GRADE FOOD & EQUIPMENT PACKAGING

- 7.6.3 MONOMATERIAL SHAPE-MORPHING FILMS

- 7.7 IMPACT OF AI/GEN AI ON MONOMATERIAL PACKAGING FILMS MARKET

- 7.7.1 TOP USE CASES AND MARKET POTENTIAL

- 7.7.2 BEST PRACTICES IN MONOMATERIAL PACKAGING FILMS

- 7.7.3 CASE STUDIES OF AI IMPLEMENTATION IN MONOMATERIAL PACKAGING FILMS MARKET

- 7.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MONOMATERIAL PACKAGING FILMS MARKET

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF MONOMATERIAL PACKAGING FILMS

- 8.2.1.1 Carbon impact reduction

- 8.2.1.2 Eco-Applications

- 8.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF MONOMATERIAL PACKAGING FILMS

- 8.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

9 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 9.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 9.5 MARKET PROFITABILITY

- 9.5.1 REVENUE POTENTIAL

- 9.5.2 COST DYNAMICS

- 9.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

10 MONOMATERIAL PACKAGING FILMS MARKET, BY PACKAGING FORMAT

- 10.1 INTRODUCTION

- 10.2 POUCHES

- 10.2.1 OPTIMIZING MONOMATERIAL POUCHES FOR HIGH-PERFORMANCE, RECYCLABLE CONSUMER PACKAGING APPLICATIONS

- 10.3 BAGS

- 10.3.1 ENHANCING FUNCTIONAL INTEGRITY OF MONOMATERIAL BAGS TO DRIVE CONSUMER DEMAND

- 10.4 FILMS & WRAPS

- 10.4.1 MAXIMIZING PERFORMANCE AND RECYCLABILITY TO DRIVE MARKET

- 10.5 ROLLSTOCK & SHEETS

- 10.5.1 OPTIMIZING MONOMATERIAL ROLLSTOCK AND SHEETS TO ACCELERATE FLEXIBLE PACKAGING INNOVATION

- 10.6 OTHER PACKAGING FORMATS

11 MONOMATERIAL PACKAGING FILMS MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.2 PE

- 11.2.1 ACCELERATING FUNCTIONAL INNOVATION IN PE-BASED MONOMATERIAL PACKAGING FILMS FOR HIGH-DEMAND APPLICATIONS

- 11.3 PP

- 11.3.1 DRIVING PERFORMANCE TRANSFORMATION IN MONOMATERIAL PP FILMS FOR HIGH-BARRIER, HIGH-CLARITY APPLICATIONS

- 11.4 PET

- 11.4.1 ELEVATING PERFORMANCE CAPABILITIES IN MONOMATERIAL PET FILMS FOR DEMANDING PACKAGING APPLICATIONS

- 11.5 PVC

- 11.5.1 STRENGTHENING FUNCTIONAL ADOPTION OF MONOMATERIAL PVC FILMS IN HIGH-PRECISION PACKAGING SEGMENTS

- 11.6 OTHER TYPES

12 MONOMATERIAL PACKAGING FILMS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 FOOD & BEVERAGES

- 12.2.1 OPTIMIZING MONOMATERIAL PACKAGING FILMS TO TRANSFORM FOOD & BEVERAGE SUPPLY CHAINS AND SHELF PERFORMANCE

- 12.3 PERSONAL CARE & COSMETICS

- 12.3.1 INTEGRATING FUNCTIONAL COATINGS AND SURFACE ENGINEERING IN COSMETIC PACKAGING TO PROPEL MARKET DEMAND

- 12.4 PHARMACEUTICAL & MEDICAL

- 12.4.1 INTEGRATING HIGH-SPEED PROCESSING AND REGULATORY COMPLIANCE IN MEDICAL FILMS TO DRIVE DEMAND

- 12.5 HOUSEHOLD PRODUCTS

- 12.5.1 ENHANCING CHEMICAL RESISTANCE AND MECHANICAL STRENGTH IN HOUSEHOLD FILMS TO DRIVE DEMAND

- 12.6 OTHER END-USE INDUSTRIES

13 MONOMATERIAL PACKAGING FILMS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Growing snacking, premium beverages, healthcare spending, and beauty trade activity to drive demand

- 13.2.2 CANADA

- 13.2.2.1 Expansion in food processing, pharmaceuticals, medical devices, and beauty industries to propel demand

- 13.2.3 MEXICO

- 13.2.3.1 Growth in agri-food, packaged foods, pharmaceuticals, and beauty industries to drive demand

- 13.2.1 US

- 13.3 ASIA PACIFIC

- 13.3.1 CHINA

- 13.3.1.1 Expanding industrial output and consumer markets to intensify shift toward monomaterial packaging films

- 13.3.2 INDIA

- 13.3.2.1 Expanding consumer ecosystem to drive demand

- 13.3.3 JAPAN

- 13.3.3.1 Expanding food, healthcare, and beauty ecosystem to drive demand

- 13.3.4 SOUTH KOREA

- 13.3.4.1 Surging agri-food, pharma, and beauty exports to drive demand

- 13.3.5 INDONESIA

- 13.3.5.1 Expanding consumer industries intensifying shift toward monomaterial films to drive demand

- 13.3.6 REST OF ASIA PACIFIC

- 13.3.1 CHINA

- 13.4 SOUTH AMERICA

- 13.4.1 BRAZIL

- 13.4.1.1 Extensive food, beverage, healthcare, and beauty sectors to drive demand

- 13.4.2 ARGENTINA

- 13.4.2.1 Robust food, beverage, healthcare, and beauty sectors to drive demand

- 13.4.3 REST OF SOUTH AMERICA

- 13.4.1 BRAZIL

- 13.5 EUROPE

- 13.5.1 GERMANY

- 13.5.1.1 Powerful consumer industries accelerate shift toward monomaterial packaging films

- 13.5.2 UK

- 13.5.2.1 Expanding consumer industries to drive demand for monomaterial packaging films

- 13.5.3 FRANCE

- 13.5.3.1 Increased use in food, healthcare, and cosmetic sectors to drive demand

- 13.5.4 RUSSIA

- 13.5.4.1 Expanding food, cosmetic, and pharmaceutical sectors to drive demand

- 13.5.5 SPAIN

- 13.5.5.1 Thriving food, wine, beauty, and healthcare sectors to drive demand

- 13.5.6 ITALY

- 13.5.6.1 Robust food, pharmaceutical, and beauty industries to drive demand

- 13.5.7 REST OF EUROPE

- 13.5.1 GERMANY

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.2 SAUDI ARABIA

- 13.6.2.1 Diversified economy and growing sectors to drive demand

- 13.6.3 UAE

- 13.6.3.1 Thriving F&B, healthcare, and beauty sectors to drive demand

- 13.6.4 REST OF GCC COUNTRIES

- 13.6.5 SOUTH AFRICA

- 13.6.5.1 Strong economy and expanding F&B, healthcare, and beauty markets to drive demand

- 13.6.6 TURKEY

- 13.6.6.1 Expanding consumer and industrial base continues to drive demand

- 13.6.7 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Type footprint

- 14.6.5.4 Packaging format footprint

- 14.6.5.5 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8.1 COMPANY VALUATION

- 14.9 FINANCIAL METRICS

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES

- 14.10.2 DEALS

- 14.10.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AMCOR PLC

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 MONDI

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 TOPPAN HOLDINGS INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 SABIC

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 KLOCKNER PENTAPLAST

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 HUHTAMAKI

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.6.4 MnM view

- 15.1.6.4.1 Right to win

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses and competitive threats

- 15.1.7 CONSTANTIA FLEXIBLES

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.3.3 Expansions

- 15.1.7.4 MnM view

- 15.1.7.4.1 Right to win

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 SEALED AIR

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Expansions

- 15.1.8.4 MnM view

- 15.1.8.4.1 Right to win

- 15.1.8.4.2 Strategic choices

- 15.1.8.4.3 Weaknesses and competitive threats

- 15.1.9 TRANSCONTINENTAL INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.9.4 MnM view

- 15.1.10 UFLEX LIMITED

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.4 MnM view

- 15.1.11 BISCHOF+KLEIN SE & CO. KG

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Expansions

- 15.1.11.4 MnM view

- 15.1.12 PROAMPAC

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.12.4 MnM view

- 15.1.1 AMCOR PLC

- 15.2 OTHER PLAYERS

- 15.2.1 TORAY INDUSTRIES, INC.

- 15.2.2 COSMO FILMS

- 15.2.3 NOVOLEX

- 15.2.4 COVERIS

- 15.2.5 WINPAK LTD.

- 15.2.6 JINDAL FILMS

- 15.2.7 SUMITOMO BAKELITE CO., LTD.

- 15.2.8 GLENROY, INC.

- 15.2.9 EPAC HOLDINGS, LLC.

- 15.2.10 POLYPLEX CORPORATION LTD.

- 15.2.11 POLIFILM GMBH

- 15.2.12 PRINTPACK

- 15.2.13 C-P FLEXIBLE PACKAGING

- 15.2.14 INTEPLAST GROUP

- 15.2.15 ZOTEFOAMS PLC

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS