|

시장보고서

상품코드

2008706

AI 활용 예지보전 시장 예측(-2032년) : 오퍼링별, 솔루션별, 도입 형태별, 조직 규모별, 기법별, 업계별, 지역별AI Driven Predictive Maintenance Market by Offering (Software, Services), Solution (Integrated, Standalone), Deployment Mode (Cloud-based, On-premises), Technique (Vibration Analysis, Oil Analysis), and Organization Size-Global Forecast to 2032 |

||||||

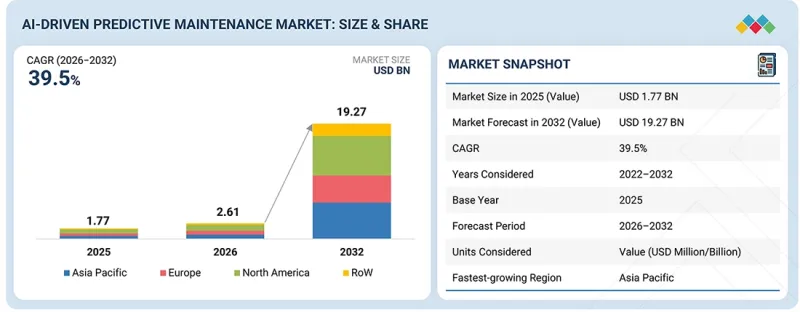

AI 활용 예지보전 시장 규모는 2026년 26억 1,000만 달러에서 2032년까지 192억 7,000만 달러로 성장하며, 2026-2032년까지 CAGR은 39.5%에 달할 것으로 예측됩니다.

산업을 막론하고 비용 최적화 및 자산 수명주기 연장에 대한 관심이 높아지면서 시장 성장을 촉진하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 오퍼링별, 솔루션별, 도입 형태별, 조직 규모별, 기법별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

기업은 핵심 설비의 효율성과 수명을 극대화하면서 유지보수 비용을 절감해야 한다는 압박을 받고 있으며, 이에 따라 사후 대응 및 정기적인 유지보수에서 데이터베이스 접근방식으로 전환하고 있습니다. AI 활용 예지보전 솔루션은 잠재적 고장을 사전에 파악하여 예비 부품 재고를 최적화하고 불필요한 유지보수 작업을 줄임으로써 운영 비용 절감과 자산 이익률 향상에 기여합니다. 이러한 비용 효율성으로 인해 제조업, 에너지, 운송 및 기타 자산 집약적인 분야에서 널리 도입되고 있습니다.

진동 분석은 현재 AI 활용 예지보전 시장에서 가장 큰 점유율을 차지하고 있으며, 예측 기간 중도 주요 부문 중 하나로 남을 것으로 예상됩니다. 그 장점은 조기 고장 감지 및 설비 모니터링을 위해 업계 전반에 걸쳐 널리 채택되고 있다는 점입니다. 이 방법은 모터, 펌프, 터빈 등 회전 기계에 널리 사용되며, 진동 패턴의 변화를 통해 불균형, 위치 오차, 부품 마모 등의 문제를 식별하는 데 도움이 됩니다.

열화상 진단이나 오일 분석과 같은 다른 기술도 주목을 받고 있지만, 진동 분석은 여전히 예지보전의 기초적인 접근 방식입니다. 각 산업계가 점점 더 예방적 유지보수 전략을 채택하고 운영 효율성에 집중함에 따라 진동 분석에 대한 수요는 계속 강세를 보일 것으로 예상되며, 이에 따라 큰 시장 점유율을 유지할 수 있을 것입니다.

의료 부문은 기기의 신뢰성과 환자 치료 향상을 위한 AI 도입 확대에 힘입어 AI 활용 예지보전 시장에서 가장 높은 CAGR로 성장할 것으로 예측됩니다. 의료 업계에서는 영상 진단 시스템, 진단 장비, 병원 인프라 등 중요한 의료기기를 모니터링하기 위해 AI를 활용하는 움직임이 가속화되고 있으며, 잠재적인 문제를 조기에 발견하고 예기치 못한 다운타임을 줄이는 데 도움을 주고 있습니다. 커넥티드 디바이스 및 디지털 시스템의 사용 확대로 인해 대량의 데이터가 생성되고 있으며, 실시간 인사이트를 통해 보다 정확하고 시기적절한 유지보수 계획이 가능해졌다. 또한 지속적인 운영을 보장하고, 유지보수 비용을 절감하며, 자산 활용도를 높이기 위해 의료시설 전반에 걸쳐 예지보전 솔루션의 도입이 진행되고 있습니다. IoT와 첨단 분석 기술의 통합은 이러한 예방적 유지보수 전략으로의 전환을 더욱 촉진하고 있습니다. 의료 서비스 제공자들이 업무 효율성, 서비스 품질, 환자 안전에 지속적으로 집중하면서 예측 기간 중 AI 활용 예지보전 솔루션에 대한 수요가 크게 증가할 것으로 예상됩니다.

아시아태평양은 급속한 디지털 혁신과 산업 전반의 AI 도입 확대에 힘입어 AI 기반 예지보전 시장에서 가장 높은 CAGR로 성장할 것으로 예상됩니다. 중국, 일본, 한국, 인도 등의 국가들은 스마트 제조, 산업 자동화, 디지털 인프라에 대한 투자를 진행하고 있으며, 이는 예지보전 솔루션에 대한 수요를 견인하고 있습니다. 이 지역의 각국 정부는 인더스트리 4.0, 스마트 팩토리, 디지털 경제 발전에 초점을 맞춘 구상을 통해 기술 도입을 지원하고 있습니다. 커넥티드 기기 및 IoT 기기의 사용 확대로 인해 방대한 양의 운영 데이터가 생성되고 있으며, 이를 통해 조직은 실시간 모니터링 및 조기 고장 감지를 위한 AI 기반 솔루션을 도입할 수 있습니다.

이 보고서에서는 AI 활용 예지보전 시장의 주요 기업 개요과 시장 순위를 포함하여 소개합니다. 이 보고서에서 다루는 주요 기업으로는 IBM(미국), Siemens(독일), SAP SE(독일), GE Vernova(미국), C3.ai(미국), ABB(스위스), Schneider Electric(프랑스), Hitachi, Ltd. Uptake Technologies Inc.(미국) 등이 있습니다.

KONE(핀란드),PTC(미국),Emerson Electric Co.(미국),Honeywell International Inc.(미국),Augury Ltd.(미국),Nanoprecise(캐나다),Oracle(미국),SKF AB(스웨덴) ), Falkonry(미국), Capgemini(프랑스), Hexagon AB(스웨덴), Dynamox(브라질), Bosch Global Software Technologies Private Limited(인도), eMaint(미국), Rockwell Automation(미국) 등이 있습니다. Rockwell Automation(미국) 등이 이 시장의 주요 업체로 꼽힙니다.

조사 범위:

본 조사 보고서에서는 AI 활용 예지보전 시장을 제공, 솔루션, 도입 형태, 조직 규모, 기술, 산업, 지역에 따라 분류하고 있습니다. 이 보고서는 시장의 주요 촉진요인, 저해요인, 도전과제, 기회요인을 설명하고 2032년까지 예측하고 있습니다. 또한 이 보고서에는 생태계내 모든 기업에 대한 리더십 매핑 및 분석이 포함되어 있습니다.

이 보고서 구매의 주요 이점

이 보고서는 전체 시장과 그 하위 부문에 대한 가장 정확한 수치 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움을 줄 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 도전 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인 분석(실시간 상태 모니터링 시스템에 대한 수요 증가, 예기치 못한 설비 다운타임 감소에 대한 수요 증가, 인더스트리 4.0 및 스마트 제조 도입 확대, IoT 지원 커넥티드 자산 및 센서의 확대)

- 제품 개발/혁신: 향후 기술 동향, R&D 활동 및 시장에서의 신제품 출시에 대한 심층적인 인사이트

- 시장 동향: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 다양한 지역의 시장을 분석합니다.

- 시장 다각화: 신제품, 미개발 지역, 최근 동향 및 시장 투자에 대한 포괄적인 정보

- 경쟁사 분석: IBM(미국), Siemens(독일), SAP SE(독일), GE Vernova(미국), C3.ai(미국) 등 주요 시장 진출 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 AI 활용 예지보전 시장(오퍼링별)

제10장 AI 활용 예지보전 시장(솔루션별)

제11장 AI 활용 예지보전 시장(도입 형태별)

제12장 AI 활용 예지보전 시장(조직 규모별)

제13장 AI 활용 예지보전 시장(기법별)

제14장 AI 활용 예지보전 시장(업계별)

제15장 AI 활용 예지보전 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

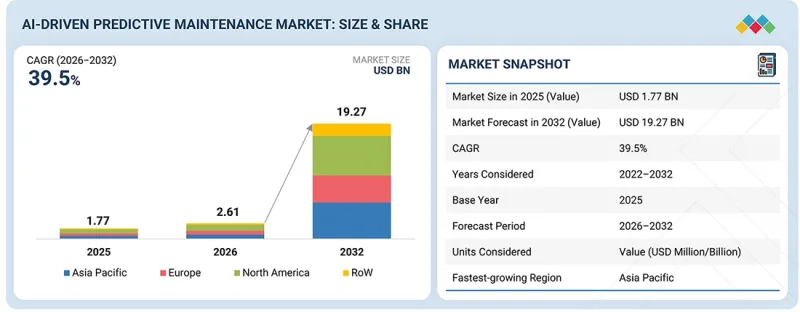

KSA 26.04.29The AI-driven predictive maintenance market is anticipated to grow from USD 2.61 billion in 2026 to USD 19.27 billion by 2032, at a CAGR of 39.5% between 2026 and 2032. The increasing focus on cost optimization and asset lifecycle extension across industries drives the market growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Solution, Technique and Region |

| Regions covered | North America, Europe, APAC, RoW |

Organizations are under growing pressure to reduce maintenance costs while maximizing the efficiency and lifespan of critical equipment, leading to a shift from reactive and scheduled maintenance to data-driven approaches. AI-enabled predictive maintenance solutions help identify potential failures in advance, optimize spare parts inventory, and reduce unnecessary maintenance activities, thereby lowering operational expenditure and improving return on assets. This cost-efficiency advantage is encouraging widespread adoption across manufacturing, energy, transportation, and other asset-intensive sectors.

"Vibration analysis is expected to hold the largest share, by technique, in 2032."

Vibration analysis currently holds the largest share of the AI-driven predictive maintenance market and is expected to remain one of the leading segments during the forecast period. Its dominance can be attributed to its widespread adoption across industries for early fault detection and equipment monitoring. This technique is extensively used in rotating machinery such as motors, pumps, and turbines, where changes in vibration patterns help identify issues such as imbalance, misalignment, and component wear.

While other techniques, such as thermal imaging and oil analysis, are gaining traction, vibration analysis remains a foundational approach in predictive maintenance. As industries increasingly adopt proactive maintenance strategies and focus on operational efficiency, the demand for vibration analysis is expected to remain strong, thereby supporting its significant market share.

"The healthcare industry is estimated to record the highest CAGR during the forecast period."

The healthcare segment is projected to grow at the highest CAGR in the AI-driven predictive maintenance market, driven by the increasing adoption of AI to improve equipment reliability and patient care. Healthcare industries are increasingly using AI to monitor critical medical equipment such as imaging systems, diagnostic devices, and hospital infrastructure, helping detect potential issues early and reduce unplanned downtime. The growing use of connected devices and digital systems is generating large volumes of data, enabling more accurate and timely maintenance planning through real-time insights. In addition, the need to ensure continuous operations, reduce maintenance costs, and improve asset utilization is encouraging the adoption of predictive maintenance solutions across healthcare facilities. The integration of IoT and advanced analytics is further supporting this shift toward proactive maintenance strategies. As healthcare providers continue to focus on operational efficiency, service quality, and patient safety, the demand for AI-driven predictive maintenance solutions is expected to increase significantly during the forecast period.

"The Asia Pacific is expected to grow at the highest CAGR during the forecast period."

The Asia Pacific is expected to grow at the highest CAGR in the AI-driven predictive maintenance market, driven by rapid digital transformation and increasing AI adoption across industries. Countries such as China, Japan, South Korea, and India are investing in smart manufacturing, industrial automation, and digital infrastructure, driving demand for predictive maintenance solutions. Governments across the region are supporting technology adoption through initiatives focused on Industry 4.0, smart factories, and the development of the digital economy. The growing use of connected equipment and IoT devices is generating large volumes of operational data, enabling organizations to adopt AI-based solutions for real-time monitoring and early fault detection.

Extensive primary interviews were conducted with key industry experts in the AI-driven predictive maintenance to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is provided below:

The study includes insights from industry experts, ranging from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-40%, Tier 2-25%, and Tier 3-25%

- By Designation: C-level-40%, Directors-45%, and Others-15%

- By Region: North America-26%, Europe-28%, Asia Pacific-41%, and RoW-5%

The report profiles key players in the AI-driven predictive maintenance market, including their respective market rankings. Prominent players profiled in this report are IBM (US), Siemens (Germany), SAP SE (Germany), GE Vernova (US), C3.ai (US), ABB (Switzerland), Schneider Electric (France), Hitachi, Ltd. (Japan), Uptake Technologies Inc. (US), among others.

KONE (Finland), PTC (US), Emerson Electric Co. (US), Honeywell International Inc. (US), Augury Ltd. (US), Nanoprecise (Canada), Oracle (US), SKF AB (Sweden), Falkonry (US), Capgemini (France), Hexagon AB (Sweden), Dynamox (Brazil), Bosch Global Software Technologies Private Limited (India), eMaint (US), and Rockwell Automation (US) are among the few other companies in the market.

Research Coverage:

This research report categorizes the AI-driven predictive maintenance market based on offering, solution, deployment mode, organization size, technique, industry, and region. The report describes the major drivers, restraints, challenges, and opportunities for the market and forecasts them through 2032. Apart from this, the report includes leadership mapping and analysis of all companies in the ecosystem.

Key Benefits of Buying the Report

The report will help market leaders/new entrants in this market by providing information on the closest approximations of the numbers for the overall market and its subsegments. This report will help stakeholders understand the competitive landscape and gain additional insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of Key Drivers (increasing demand for real-time condition monitoring systems, increasing demand to reduce unplanned equipment downtime, growing adoption of Industry 4.0 and smart manufacturing, expansion of IoT-enabled connected assets and sensors)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product launches in the market

- Market Development: Comprehensive information about lucrative markets-the report analyzes the market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading market players, such as IBM (US), Siemens (Germany), SAP SE (Germany), GE Vernova (US), and C3.ai (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI-DRIVEN PREDICTIVE MAINTENANCE MARKET

- 3.2 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY OFFERING

- 3.3 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY SOLUTION

- 3.4 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY DEPLOYMENT

- 3.5 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY ORGANIZATION SIZE

- 3.6 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY TECHNIQUE

- 3.7 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY INDUSTRY

- 3.8 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for real-time condition monitoring systems

- 4.2.1.2 Need to reduce unplanned equipment downtime

- 4.2.1.3 Growing adoption of Industry 4.0 and smart manufacturing

- 4.2.1.4 Expansion of IoT-enabled connected assets and sensors

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial capital investment for AI infrastructure and sensor deployment

- 4.2.2.2 Cybersecurity risks in connected industrial environments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of predictive maintenance-as-a-service (PdMaaS) models

- 4.2.3.2 Partnerships between AI vendors and industrial OEMs

- 4.2.3.3 Expansion of AI at the edge for low-latency predictive analytics

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of skilled workforce

- 4.2.4.2 Continuous model upgradation

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL AI-DRIVEN PREDICTIVE MAINTENANCE MARKET

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF SOFTWARE, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025 (USD/MONTH)

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847150)

- 5.6.2 EXPORT SCENARIO (HS CODE 847150)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO, 2023-2025

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 KONE AND IBM IMPLEMENT AI-BASED PREDICTIVE MAINTENANCE FOR HUMLEGARDEN, ENHANCING OPERATIONAL EFFICIENCY

- 5.10.2 SIEMENS ENABLES AI-DRIVEN PREDICTIVE MAINTENANCE FOR BLUESCOPE STEEL, IMPROVING MAINTENANCE EFFICIENCY AND DECISION-MAKING

- 5.10.3 IBM ENABLES AI-DRIVEN PREDICTIVE MAINTENANCE FOR KONE, IMPROVING ELEVATOR RELIABILITY AND REDUCING DOWNTIME

- 5.11 IMPACT OF US TARIFFS-AI-DRIVEN PREDICTIVE MAINTENANCE MARKET

- 5.11.1 INTRODUCTION

- 5.11.1.1 Key tariff rates

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT OF COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE INDUSTRIES

- 5.11.1 INTRODUCTION

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 MACHINE LEARNING-BASED ANOMALY DETECTION TECHNOLOGY

- 6.1.2 DIGITAL TWIN AND CONDITION MONITORING TECHNOLOGY

- 6.1.3 EDGE AI-BASED REAL-TIME MONITORING TECHNOLOGY

- 6.1.4 PRESCRIPTIVE ANALYTICS AND REMAINING USEFUL LIFE (RUL) ESTIMATION TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INDUSTRIAL INTERNET OF THINGS (IIOT) AND SENSOR NETWORKS

- 6.2.2 CLOUD COMPUTING AND ENTERPRISE ASSET MANAGEMENT (EAM) INTEGRATION

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

- 7.1.2.1 ISO 55000

- 7.1.2.2 ISO 17359

- 7.1.2.3 IEC 62443

- 7.1.2.4 ISO/IEC 27001

- 7.1.2.5 ISO 14224

- 7.1.2.6 NIST AI Risk Management Framework (AI RMF)

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

9 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 SOFTWARE

- 9.2.1 RISING ADOPTION OF AI-POWERED ASSET ANALYTICS PLATFORMS DRIVING GROWTH OF PREDICTIVE MAINTENANCE SOFTWARE

- 9.3 SERVICES

- 9.3.1 GROWING DEMAND FOR AI IMPLEMENTATION AND INTEGRATION EXPERTISE TO ACCELERATE ADOPTION OF PREDICTIVE MAINTENANCE SERVICES

10 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY SOLUTION

- 10.1 INTRODUCTION

- 10.2 INTEGRATED SOLUTIONS

- 10.2.1 INCREASING DEMAND FOR UNIFIED ASSET MONITORING AND ANALYTICS PLATFORMS TO BOOST ADOPTION

- 10.3 STANDALONE SOLUTIONS

- 10.3.1 NEED FOR SPECIALIZED CONDITION MONITORING TOOLS SUPPORTS UPTAKE OF STANDALONE SOLUTIONS

11 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY DEPLOYMENT MODE

- 11.1 INTRODUCTION

- 11.2 CLOUD-BASED

- 11.2.1 RISING DEMAND FOR REAL-TIME MONITORING AND SCALABLE ANALYTICS TO DRIVE DEMAND FOR CLOUD-BASED PREDICTIVE MAINTENANCE

- 11.3 ON-PREMISES

- 11.3.1 NEED FOR DATA CONTROL AND SECURE INDUSTRIAL INFRASTRUCTURE TO PROPEL MARKET GROWTH

12 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.2 LARGE ENTERPRISES

- 12.2.1 HIGH COST OF DOWNTIME AND NEED FOR ENTERPRISE-WIDE MONITORING ARE ACCELERATING DEMAND

- 12.3 SMALL AND MEDIUM-SIZED ENTERPRISES

- 12.3.1 INCREASING AVAILABILITY OF SCALABLE AND CLOUD-BASED PREDICTIVE MAINTENANCE PLATFORMS TO SUPPORT ADOPTION

13 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY TECHNIQUE

- 13.1 INTRODUCTION

- 13.2 VIBRATION ANALYSIS

- 13.2.1 RISING NEED FOR EARLY DETECTION OF MECHANICAL FAILURES IN ROTATING EQUIPMENT DRIVES MARKET

- 13.3 INFRARED THERMOGRAPHY

- 13.3.1 DEMAND FOR NON-CONTACT AND SAFE INSPECTION METHODS PROPELS ADOPTION OF INFRARED THERMOGRAPHY

- 13.4 ACOUSTIC MONITORING

- 13.4.1 NEED FOR EARLY FAULT DETECTION AND NON-INVASIVE MONITORING TO SUPPORT USAGE

- 13.5 OIL ANALYSIS

- 13.5.1 INCREASING USE OF HEAVY MACHINERY AND CRITICAL ASSETS IN MINING, ENERGY, ETC., BOOSTS DEMAND

- 13.6 MOTOR CIRCUIT ANALYSIS

- 13.6.1 EXPANSION OF AUTOMATED INDUSTRIAL EQUIPMENT PROPELS USE OF MOTOR CIRCUIT ANALYSIS TECHNIQUES

- 13.7 OTHER TECHNIQUES

14 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY INDUSTRY

- 14.1 INTRODUCTION

- 14.2 ENERGY & UTILITIES

- 14.2.1 GROWING NEED FOR CONTINUOUS MONITORING OF CRITICAL ENERGY INFRASTRUCTURE DRIVES PREDICTIVE MAINTENANCE ADOPTION

- 14.3 MANUFACTURING

- 14.3.1 EXPANSION OF SMART MANUFACTURING AND AUTOMATION DRIVING PREDICTIVE MAINTENANCE ADOPTION

- 14.4 TRANSPORTATION

- 14.4.1 INCREASING INFRASTRUCTURE MODERNIZATION AND DEMAND FOR OPERATIONAL RELIABILITY DRIVING PREDICTIVE MAINTENANCE ADOPTION

- 14.5 AEROSPACE & DEFENSE

- 14.5.1 INCREASING EMPHASIS ON MISSION READINESS AND SYSTEM RELIABILITY TO PROPEL MARKET GROWTH

- 14.6 MINING & HEAVY EQUIPMENT

- 14.6.1 RISING FOCUS ON EQUIPMENT UPTIME IN HARSH OPERATING CONDITIONS SUPPORTS ADOPTION

- 14.7 HEALTHCARE

- 14.7.1 CONTINUOUS EQUIPMENT AVAILABILITY BECOMING CRITICAL FOR EFFICIENT HEALTHCARE OPERATION

- 14.8 TELECOMMUNICATIONS

- 14.8.1 GROWING COMPLEXITY OF NETWORK INFRASTRUCTURE TO DRIVE DEMAND

- 14.9 OTHER INDUSTRIES

15 AI-DRIVEN PREDICTIVE MAINTENANCE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Strong presence of highly developed industrial AI and analytics ecosystem to drive demand

- 15.2.2 CANADA

- 15.2.2.1 Growing demand for operational efficiency and regulatory compliance to spur market growth

- 15.2.3 MEXICO

- 15.2.3.1 Expansion of automotive manufacturing and industrial automation supporting adoption

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Leadership in industry 4.0 and advanced manufacturing driving adoption of AI-driven predictive maintenance

- 15.3.2 UK

- 15.3.2.1 Industry 4.0 initiatives and advanced aerospace manufacturing driving adoption of AI-driven predictive maintenance

- 15.3.3 FRANCE

- 15.3.3.1 Accelerating industrial digitalization and aerospace expansion driving market growth

- 15.3.4 ITALY

- 15.3.4.1 Strong industrial machinery sector and manufacturing modernization driving predictive maintenance adoption

- 15.3.5 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Large-scale industrial production and smart factory initiatives driving adoption of AI-driven predictive maintenance

- 15.4.2 JAPAN

- 15.4.2.1 Increasing need to address aging industrial infrastructure and workforce shortages to spur market demand

- 15.4.3 SOUTH KOREA

- 15.4.3.1 Smart manufacturing and industrial automation driving adoption in South Korea

- 15.4.4 INDIA

- 15.4.4.1 Industrial digitalization and expansion of industrial automation supporting predictive maintenance adoption

- 15.4.5 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 REST OF THE WORLD (ROW)

- 15.5.1 MIDDLE EAST & AFRICA

- 15.5.1.1 GCC Countries

- 15.5.1.2 Rest of Middle East & Africa

- 15.5.2 SOUTH AMERICA

- 15.5.2.1 Expansion of industrial production and energy infrastructure supporting predictive maintenance adoption

- 15.5.1 MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS, STRATEGIES/RIGHT TO WIN (2022-2026)

- 16.3 REVENUE ANALYSIS, 2022-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Offering footprint

- 16.7.5.4 Deployment mode footprint

- 16.7.5.5 Application footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 IBM

- 17.1.1.1 Business overview

- 17.1.1.2 Products/solutions/services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/right to win

- 17.1.1.4.2 Strategic choices made

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 SIEMENS

- 17.1.2.1 Business overview

- 17.1.2.2 Products/solutions/services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/right to win

- 17.1.2.4.2 Strategic choices made

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 SAP SE

- 17.1.3.1 Business overview

- 17.1.3.2 Products/solutions/services offered

- 17.1.3.3 MnM view

- 17.1.3.3.1 Key strengths/right to win

- 17.1.3.3.2 Strategic choices made

- 17.1.3.3.3 Weaknesses and competitive threats

- 17.1.4 GE VERNOVA

- 17.1.4.1 Business overview

- 17.1.4.2 Products/solutions/services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/right to win

- 17.1.4.4.2 Strategic choices made

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 C3.AI

- 17.1.5.1 Business overview

- 17.1.5.2 Products/solutions/services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product enhancements

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/right to win

- 17.1.5.4.2 Strategic choices made

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 ABB

- 17.1.6.1 Business overview

- 17.1.6.2 Products/solutions/services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.7 SCHNEIDER ELECTRIC

- 17.1.7.1 Business overview

- 17.1.7.2 Products/solutions/services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.8 HITACHI, LTD.

- 17.1.8.1 Business overview

- 17.1.8.2 Products/solutions/services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.9 L&T TECHNOLOGY SERVICES LIMITED

- 17.1.9.1 Business overview

- 17.1.9.2 Products/solutions/services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Other deals

- 17.1.10 UPTAKE TECHNOLOGIES INC.

- 17.1.10.1 Business overview

- 17.1.10.2 Products/solutions/services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.1 IBM

- 17.2 OTHER PLAYERS

- 17.2.1 KONE

- 17.2.2 PTC

- 17.2.3 EMERSON ELECTRIC CO.

- 17.2.4 HONEYWELL INTERNATIONAL INC.

- 17.2.5 AUGURY LTD.

- 17.2.6 NANOPRECISE

- 17.2.7 ORACLE

- 17.2.8 SKF

- 17.2.9 FALKONRY

- 17.2.10 CAPGEMINI

- 17.2.11 HEXAGON AB

- 17.2.12 DYNAMOX

- 17.2.13 BOSCH GLOBAL SOFTWARE TECHNOLOGIES PRIVATE LIMITED

- 17.2.14 EMAINT

- 17.2.15 ROCKWELL AUTOMATION

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.2 SECONDARY AND PRIMARY RESEARCH

- 18.2.1 SECONDARY DATA

- 18.2.1.1 Key data from secondary sources

- 18.2.1.2 List of key secondary sources

- 18.2.2 PRIMARY DATA

- 18.2.2.1 Key data from primary sources

- 18.2.2.2 List of primary interview participants

- 18.2.2.3 Breakdown of primaries

- 18.2.2.4 Key industry insights

- 18.2.1 SECONDARY DATA

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 BOTTOM-UP APPROACH

- 18.3.2 TOP-DOWN APPROACH

- 18.3.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 18.4 MARKET FORECAST APPROACH

- 18.4.1 BOTTOM-UP APPROACH

- 18.4.2 TOP-DOWN APPROACH

- 18.5 DATA TRIANGULATION

- 18.6 FACTOR ANALYSIS

- 18.7 RESEARCH ASSUMPTIONS

- 18.8 RESEARCH LIMITATIONS

- 18.9 RISK ANALYSIS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS