|

시장보고서

상품코드

2011925

보호 필름 시장 예측(-2031년) : 유형별, 재료별, 최종 용도 산업별, 지역별Protective Films Market by Type, Material, End-use Industry (Automotive & Transportation, Building & Construction), and Region - Global Forecast To 2031 |

||||||

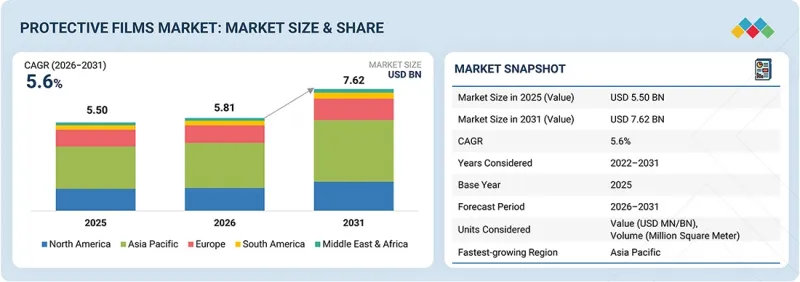

세계의 보호 필름 시장 규모는 2026년 58억 1,000만 달러에서 2031년까지 76억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 5.6%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만 달러, 100만 평방미터 |

| 부문 | 유형, 재료, 최종 용도 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

건설, 제조, 설치 과정에서 표면 보호가 필요한 인프라 및 산업 프로젝트가 증가함에 따라 보호 필름 시장은 확대될 것으로 예상됩니다. 유리, 금속, 바닥재에 코팅은 일반적으로 취급시 긁힘, 먼지, 손상을 방지하기 위해 사용됩니다. 또한 전기자동차 생산이 증가함에 따라 도장된 차체 부품, 디스플레이, 배터리 부품에 대한 보호필름의 사용도 확대되고 있습니다.

"감압성 접착제(PSA) 필름 부문이 2031년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

감압성 접착제(PSA) 필름 부문은 열, 용제, 기타 장비가 필요 없고 사용이 매우 간편하므로 2031년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. PSA 필름은 높은 효과를 가지면서도 일시적인 접착력을 발휘하며, 잔여물을 남기지 않고 쉽게 떼어낼 수 있습니다. 자동차, 전자, 가전, 건설 산업에서 일시적인 표면 보호용으로 널리 활용되고 있습니다. 다용도하고 다양한 기판에 사용할 수 있는 특성으로 인해 가장 널리 사용되는 보호 필름 유형입니다.

"폴리에틸렌(PE) 부문이 2031년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

폴리에틸렌(PE) 부문은 표면 보호용 PE 필름의 뛰어난 유연성, 내구성, 저렴한 가격으로 인해 2031년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이 필름은 습기, 먼지, 마모에 강하고 제조, 보관, 운송의 각 단계에서 재료를 보호하는 데 사용할 수 있습니다. PE 보호 필름은 다양한 산업 분야에서 금속, 플라스틱, 유리, 도장면 등에 널리 사용되고 있습니다. 그 인기와 대부분의 응용 분야에서 사용의 유연성으로 인해 시장에서 지배적인 위치를 차지하고 있습니다.

"자동차 및 운송 부문이 2031년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

자동차 및 운송 부문은 자동차 생산량 증가와 표면 보호 제품에 대한 수요 증가로 인해 2031년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 도장된 차체 부품, 인테리어 트림, 디스플레이, 섬세한 부품은 제조 및 운송 중 긁힘이나 손상을 방지하기 위해 보호 필름을 부착합니다. 전기자동차의 이용이 급증하고 있는 것도 배터리 시스템 및 전자 스크린용 보호필름의 수요 증가로 이어지고 있습니다. 이러한 추세로 인해 자동차 산업에서 보호 코팅의 사용이 증가할 것으로 예상됩니다.

"아시아태평양의 보호 필름 시장은 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

아시아태평양의 보호 필름 시장은 급속한 산업화, 도시화 및 인프라 개발로 인해 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다. 중국, 인도, 일본, 한국은 자동차, 전자, 건설 부문의 강력한 제조국입니다. 표면 보호 필름에 대한 수요는 소비자 전자제품, 자동차, 건축자재 제조의 확대에 의해 촉진되고 있습니다. 또한 제조 및 인프라 개발에 대한 투자 증가도 이 지역의 시장 성장에 기여하고 있습니다.

세계의 보호필름 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 보호 필름 시장 : 유형별

제10장 보호 필름 시장 : 재료별

제11장 보호 필름 시장 : 용도별

제12장 보호 필름 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.05.04The protective films market is projected to grow from USD 5.81 billion in 2026 to USD 7.62 billion by 2031, at a CAGR of 5.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Million Square Meter) |

| Segments | Type, Material, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The protective films market will expand as infrastructure and industrial projects requiring surface protection during construction, fabrication, and installation increase. Coatings on glass, metal, and flooring materials are commonly used to ensure that they are not scratched, dusty, or damaged when being handled. Moreover, the rising manufacture of electric cars is raising the application of protective films on the painted body parts, displays, and battery parts.

"Pressure-sensitive adhesive (PSA) films segment is projected to capture the largest market share in 2031."

The pressure-sensitive adhesive (PSA) films segment is expected to get the highest market share in 2031 because the films do not require heat, solvents, or other equipment to be used and are very easy to apply. PSA films are highly effective but temporary adhesives and can be readily cleaned off without any residue. They find large applications in automotive, electronics, appliances, and construction industries in temporary surface protection. They are the most popular type of protective film due to their versatility and ability to use several substrates.

"The polyethylene (PE) segment is projected to capture the largest market share in 2031."

The polyethylene (PE) segment is expected to hold the largest market share in 2031 due to the superior flexibility, longevity, and affordability of PE films for surface protection. The films are resistant to moisture, dust, and abrasion and can be used to protect materials in the manufacturing, storage, and transportation stages. PE protective films are widely applied on metals, plastics, glass, and painted surfaces in a variety of industries. Their popularity and flexibility in use in most applications make them dominant in the market.

"The automotive and transportation segment is projected to capture the largest market share in 2031."

The automotive & transportation segment will hold the largest market share in 2031, driven by rising vehicle production and demand for surface protection products. Painted body parts, interior trims, displays, and sensitive parts are coated with protective films to ensure that they are not scratched and damaged during manufacture and transportation. The surge in the use of electric vehicles is also creating more demand for protective films in battery systems and electronic screens. Such trends are likely to drive increased use of protective coating in the automobile industry.

"Asia Pacific protective films market is projected to grow at the highest CAGR during the forecast period."

The Asia Pacific protective films market is expected to have the highest CAGR over the forecast period, as the region is undergoing rapid industrialization, urbanization, and infrastructure development. China, India, Japan, and South Korea are strong manufacturing countries in the automotive, electronics, and construction sectors. The demand for protective films on surfaces is fueled by the growing manufacturing of consumer electronics, vehicles, and building materials. Also, increasing investments in manufacturing and infrastructure initiatives are contributing towards market growth in the region.

Companies Covered: Nitto Denko Corporation (Japan), 3M (US), POLIFILM (Germany), Eastman Chemical Company (US), and XPEL (US), among other companies, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the protective films market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the protective films market based on type [pressure-sensitive adhesive (PSA) films, non-adhesive/cling films, and specialty removable/clean-peel films], material [polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polyethylene terephthalate (PET), polyurethane (PU), polycarbonate (PC), and other materials] end-use industry [building & construction, automotive & transportation, electronics & electrical, industrial manufacturing/metal processing, packaging & logistics, furniture & interior, medical & pharmaceutical, and other end-use industries], and region [Asia Pacific, North America, Europe, South America, and the Middle East & Africa]. The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the protective films market. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, product offerings, and key strategies, including product launches, expansions, acquisitions, and agreements, associated with the protective films market. This report covers a competitive analysis of upcoming startups in the protective films market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with information on the closest approximations of revenue for the overall protective films market and its subsegments. This report will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses, and plan effective go-to-market strategies. The report will help stakeholders understand the market and provide them with information on key market drivers, restraints, challenges, and opportunities. The report provides insights into the following points:

- Analysis of key drivers (increased demand in the transportation industry), restraints (difficulty in recycling polymer plastics), opportunities (growing demand for sustainable protective films), and challenges (stringent environmental regulations)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the protective films market

- Market Development: Comprehensive information about profitable markets-the report analyzes the protective films market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the protective films market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Nitto Denko Corporation (Japan), 3M (US), POLIFILM (Germany), Eastman Chemical Company (US), XPEL (US), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

- 1.4 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING PROTECTIVE FILMS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: ASIA PACIFIC MARKET SIZE AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN THE PROTECTIVE FILMS MARKET

- 3.2 PROTECTIVE FILMS MARKET, BY TYPE AND REGION

- 3.3 PROTECTIVE FILMS MARKET, BY MATERIAL

- 3.4 PROTECTIVE FILMS MARKET, BY END-USE INDUSTRY

- 3.5 PROTECTIVE FILMS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased demand in transportation

- 4.2.1.2 Growth in building & construction

- 4.2.1.3 Rising demand in e-commerce

- 4.2.2 RESTRAINTS

- 4.2.2.1 Difficulty in recycling polymer plastics

- 4.2.2.2 Volatility in raw material prices

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand in pharmaceutical & medical applications

- 4.2.3.2 Rising demand for sustainable protective films

- 4.2.3.3 Advancements in smart and functional protective films

- 4.2.4 CHALLENGES

- 4.2.4.1 Stringent environmental regulations

- 4.2.4.2 Limited awareness in developing markets

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PROTECTIVE FILMS MARKET

- 4.3.1.1 Growing need for high-performance and application-specific protective film solutions

- 4.3.1.2 Need for more sustainable and fully recyclable protective films

- 4.3.1.3 Lack of standardization across applications and industries

- 4.3.1.4 Demand for residue-free and surface-compatible adhesive technologies

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Expansion into high-growth and underserved end-use segments

- 4.3.2.2 Growth in aftermarket and maintenance applications

- 4.3.2.3 Digital integration, traceability, and smart packaging solutions

- 4.3.1 UNMET NEEDS IN PROTECTIVE FILMS MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING EXPANSION AND PRODUCT INNOVATION

- 4.5.1.1 POLIFILM-strategic acquisition to expand protective film distribution network

- 4.5.1.2 Avery Dennison Corporation-product innovation in paint protection films

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING EXPANSION AND PRODUCT INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN GLOBAL ELECTRONICS & ELECTRICAL INDUSTRY

- 5.2.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER (2025) (USD/ SQUARE METER)

- 5.5.2 AVERAGE SELLING PRICE, BY REGION (2022-2026) (USD/SQUARE METER)

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 391990)

- 5.6.2 IMPORT SCENARIO (HS CODE 391990)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SS CUSTOMS RELIES ON AVERY DENNISON GRAPHICS SOLUTIONS AUTOMOTIVE FILMS

- 5.11 IMPACT OF US TARIFFS-PROTECTIVE FILMS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Asia Pacific

- 5.11.4.3 Europe

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 SELF-HEALING PROTECTIVE FILM TECHNOLOGY

- 6.1.2 MULTILAYER COEXTRUSION FILM TECHNOLOGY

- 6.1.3 THERMOPLASTIC POLYURETHANE (TPU) PROTECTIVE FILMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ADVANCED ADHESIVE INTEGRATION TECHNOLOGY

- 6.2.2 UV-RESISTANT AND NON-YELLOWING FILM TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INDUSTRIAL SURFACE PROTECTION SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | MATURITY & SUSTAINABLE SURFACE PROTECTION SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 PROTECTIVE FILMS MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 INTEGRATION OF PROTECTIVE FILMS IN ADVANCED AND HIGH-PERFORMANCE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON PROTECTIVE FILMS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN PROTECTIVE FILMS MARKET

- 6.7.3 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PROTECTIVE FILMS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 PREGIS POLYMASK PROTECTIVE FILM SUPPORTS AUTOMOTIVE FENDER PROTECTION DURING MANUFACTURING AND TRANSPORT

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF PROTECTIVE FILMS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF PROTECTIVE FILMS

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.6 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 PROTECTIVE FILMS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 PRESSURE-SENSITIVE ADHESIVE (PSA) FILMS

- 9.2.1 HIGH VERSATILITY AND COMPATIBILITY WITH MULTIPLE SUBSTRATES TO DRIVE DEMAND

- 9.3 NON-ADHESIVE/CLING FILMS

- 9.3.1 INCREASING USE FOR TEMPORARY COVERING IN CONSTRUCTION AND RENOVATION APPLICATIONS TO PROPEL DEMAND

- 9.4 SPECIALTY REMOVABLE/CLEAN-PEEL FILMS

- 9.4.1 RISING DEMAND FOR RESIDUE-FREE AND EASY-PEEL SURFACE PROTECTION IN MANUFACTURING TO AUGMENT DEMAND

10 PROTECTIVE FILMS MARKET, BY MATERIAL

- 10.1 INTRODUCTION

- 10.2 POLYETHYLENE (PE)

- 10.2.1 WIDE APPLICATION ACROSS MULTIPLE INDUSTRIES TO DRIVE DEMAND

- 10.3 POLYPROPYLENE (PP)

- 10.3.1 GROWING USE IN SURFACE PROTECTION APPLICATIONS TO DRIVE DEMAND

- 10.4 POLYVINYL CHLORIDE (PVC)

- 10.4.1 HIGH DURABILITY AND SUITABILITY FOR INDUSTRIAL AND OUTDOOR APPLICATIONS TO PROPEL MARKET

- 10.5 POLYETHYLENE TEREPHTHALATE (PET)

- 10.5.1 INCREASING DEMAND FROM ELECTRONICS AND DISPLAY INDUSTRY TO AUGMENT MARKET GROWTH

- 10.6 POLYURETHANE (PU)

- 10.6.1 INCREASING DEMAND FOR PAINT PROTECTION FILMS IN AUTOMOTIVE APPLICATIONS TO DRIVE MARKET

- 10.7 POLYCARBONATE (PC)

- 10.7.1 HIGH IMPACT RESISTANCE AND MECHANICAL STRENGTH TO AUGMENT DEMAND

- 10.8 OTHER MATERIALS

11 PROTECTIVE FILMS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 BUILDING & CONSTRUCTION

- 11.2.1 RAPID EXPANSION OF CONSTRUCTION ACTIVITIES AND URBAN DEVELOPMENT TO DRIVE DEMAND

- 11.3 AUTOMOTIVE & TRANSPORTATION

- 11.3.1 GROWTH IN AUTOMOTIVE PRODUCTION AND EXPORT ACTIVITIES TO AUGMENT DEMAND

- 11.4 ELECTRONICS & ELECTRICAL

- 11.4.1 RISING DEMAND FOR CONSUMER ELECTRONICS AND SMART DEVICES TO PROPEL MARKET GROWTH

- 11.5 INDUSTRIAL MANUFACTURING/ METAL PROCESSING

- 11.5.1 INCREASING PROCESSING OF STAINLESS STEEL AND METAL COMPONENTS TO DRIVE MARKET

- 11.6 PACKAGING & LOGISTICS

- 11.6.1 GROWTH IN E-COMMERCE AND ONLINE RETAIL ACTIVITIES TO SUPPORT ADOPTION

- 11.7 FURNITURE & INTERIOR

- 11.7.1 GROWTH IN FURNITURE MANUFACTURING AND RISING CONSUMER DEMAND TO SUPPORT MARKET GROWTH

- 11.8 MEDICAL & PHARMACEUTICAL

- 11.8.1 RISING MEDICAL DEVICE MANUFACTURING TO PROPEL DEMAND

- 11.9 OTHER END-USE INDUSTRIES

12 PROTECTIVE FILMS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Rapid expansion of China's electronics manufacturing sector to propel the market

- 12.2.2 JAPAN

- 12.2.2.1 Adoption of energy-efficient building standards to drive the market

- 12.2.3 INDIA

- 12.2.3.1 Rapid expansion of electric vehicle adoption and automotive manufacturing to drive market

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Renovation and modernization of aging building infrastructure to augment market growth

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Growing automotive production and electric vehicle adoption to propel market growth

- 12.3.2 CANADA

- 12.3.2.1 Growing adoption of zero-emission vehicles (ZEVs) to drive the market

- 12.3.3 MEXICO

- 12.3.3.1 Large-scale housing and industrial construction projects to drive the market

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Strong automotive manufacturing and export leadership to propel the market

- 12.4.2 UK

- 12.4.2.1 Adoption of energy-efficient building standards to drive the market

- 12.4.3 FRANCE

- 12.4.3.1 Government investments under the France 2030 Plan to drive the market

- 12.4.4 ITALY

- 12.4.4.1 Strong automotive manufacturing and component supply chain to augment the market

- 12.4.5 SPAIN

- 12.4.5.1 Renovation and modernization of aging building infrastructure to augment the market

- 12.4.6 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Strong automotive investments and rising electric vehicle adoption to propel the market

- 12.5.2 ARGENTINA

- 12.5.2.1 High healthcare spending and rising imports of medical devices to drive the market

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

- 12.6.1.1 Saudi Arabia

- 12.6.1.1.1 Large-scale infrastructure and construction projects under Vision 2030 to support market growth

- 12.6.1.2 UAE

- 12.6.1.2.1 Rising real estate development and large-scale construction projects to drive market

- 12.6.1.3 Rest of GCC countries

- 12.6.1.1 Saudi Arabia

- 12.6.2 SOUTH AFRICA

- 12.6.2.1 Expansion of construction and infrastructure development to propel the market

- 12.6.3 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.5.1 COMPANY VALUATION

- 13.5.2 FINANCIAL METRICS

- 13.6 BRAND COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Material footprint

- 13.7.5.4 Type footprint

- 13.7.5.5 End-use Industry footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 AVERY DENNISON CORPORATION

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 NITTO DENKO CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 SAINT-GOBAIN

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Key strengths

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 3M

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Key strengths

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 COMPAGNIE CHARGEURS INVEST

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 POLIFILM

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Expansions

- 14.1.6.4 MnM view

- 14.1.6.4.1 Key strengths

- 14.1.7 DUPONT

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.4 MnM view

- 14.1.8 EASTMAN CHEMICAL COMPANY

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.4 MnM view

- 14.1.9 XPEL

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches

- 14.1.9.4 MnM view

- 14.1.10 TORAY INDUSTRIES, INC.

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 MnM view

- 14.1.1 AVERY DENNISON CORPORATION

- 14.2 OTHER PLAYERS

- 14.2.1 PREGIS LLC

- 14.2.2 ECOPLAST LTD

- 14.2.3 LINTEC CORPORATION

- 14.2.4 BISCHOF+KLEIN SE & CO. KG

- 14.2.5 PRESTO TAPE

- 14.2.6 MT TAPES S.R.O.

- 14.2.7 KAO-CHIA PLASTICS CO., LTD.

- 14.2.8 LAMIN-X

- 14.2.9 DUNMORE

- 14.2.10 ECHOTAPE

- 14.2.11 COVERTEC SRL.

- 14.2.12 HAINING HUANAN NEW MATERIAL TECHNOLOGY CO., LTD.

- 14.2.13 REEDEE

- 14.2.14 SHANDONG JIARUN NEW MATERIALS CO., LTD.

- 14.2.15 GARWARE HI-TECH FILMS

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 TOP-DOWN APPROACH

- 15.2.2 BOTTOM-UP APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 DEMAND-SIDE APPROACH

- 15.3.2 SUPPLY-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 GROWTH RATE ASSUMPTIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 CUSTOMIZATION OPTIONS

- 16.3 RELATED REPORTS

- 16.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.5 AUTHOR DETAILS