|

시장보고서

상품코드

2021042

멀치 필름 시장 예측(-2031년) : 유형별, 용도별, 성분별, 지역별Mulch Films Market Report by Type (Clear/Transparent, Black Mulch, Colored Mulch, Photo-selective Mulch, Degradable Mulch), Application (Agricultural and Horticulture), Element (LLDPE, LDPE, HDPE, EVA, PLA, PHA), and Region - Global Forecast to 2031 |

||||||

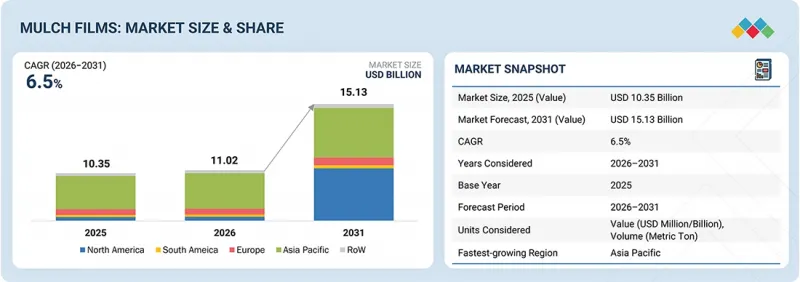

세계의 멀치 필름 시장 규모는 2026년에 추정 110억 2,000만 달러로, 2031년까지 151억 3,000만 달러에 달할 것으로 예측되며, CAGR로 6.5%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 달러, 톤 |

| 부문 | 유형, 성분, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

정밀농업, 보호 재배, 첨단 토양 관리의 채택이 확대됨에 따라 시장은 큰 변화를 보이고 있습니다. 센서식 관개 시스템, 자동 멀칭기, 기후 반응형 필름 등 스마트 농업 기술의 도입으로 제품의 기능은 더욱 향상되고 있습니다. 업계 주요 기업은 토양의 건강 상태를 개선하고 환경에 미치는 악영향을 최소화하며 친환경 농업을 촉진하기 위해 고성능 생분해성 필름과 UV 안정화 필름 개발에 적극 나서고 있습니다. 최근 멀치 필름 업계의 제품 개발은 제품의 내구성, 보온성, 특정 작물용 기능에 대한 집중이 강화되고 있으며, 이는 제품의 성장세가 상승세를 보이고 있음을 보여줍니다.

멀치 필름 산업의 기회와 변화는 주로 지속가능한 농업과 자원 효율적인 농법으로의 급속한 전환과 관련이 있습니다. 작물 수확량 증가, 농산물 품질 향상, 효율적인 물 사용에 대한 수요가 증가함에 따라 멀치 필름은 농업인과 제조업체에게 매우 큰 상업적 잠재력을 가지고 있는 것으로 보입니다. 농업인이 멀치 필름을 사용하면 물의 효율적인 이용, 잡초 억제, 토양 온도 조절, 제초제 사용 감소에 기여하여 농업, 특히 원예 및 고부가가치 작물의 수익성을 향상시킬 수 있습니다. 플라스틱 사용에 대한 환경 규제 강화, 친환경 대체품의 부상, 그리고 지속가능한 재료로의 전환에 따른 업계의 변화로 볼 수 있습니다. 이는 업계에 큰 변화를 가져오고 있으며, 업계 전체에 성장을 위한 과제를 만들어내고 있습니다.

AI를 통한 영양소 최적화: AI와 머신러닝은 멀티필름 시장에서도 유용합니다. 이를 통해 기업은 필름을 생산하기 전에 토양, 날씨, 작물의 상태를 파악할 수 있습니다. 그 결과, 생산해야 할 필름의 두께, 색상, 유형를 정확하게 판단할 수 있습니다. 예를 들어 잡초 방제를 위해 검은색 필름을 사용할 수 있습니다. 한편, 토양을 따뜻하게 하는 목적으로는 투명한 필름을 사용하기도 합니다. 필름의 내구성과 분해에 드는 시간도 AI를 통해 파악할 수 있습니다. 이를 통해 오류 및 비용 발생을 방지할 수 있습니다. 농업인들도 데이터 툴의 혜택을 누릴 수 있습니다. 이를 통해 언제 필름을 사용해야 하는지, 어떤 유형의 필름을 사용해야 하는지 알 수 있습니다. 결과적으로 적절한 계획을 세울 수 있고, 낭비를 줄일 수 있습니다. 이를 통해 농장의 수확량을 증가시킬 수 있습니다.

첨단 배합 기술: 멀티 필름 산업의 주요 중점 분야 중 하나는 재료 개발입니다. 각 업체들은 기존 소재뿐만 아니라 친환경 소재도 개발하고 있습니다. 그러나 폴리에틸렌 필름은 높은 강도와 비용 대비 성능으로 인해 여전히 널리 사용되고 있습니다. 한편, 환경 보호에 대한 규제가 강화됨에 따라 생분해성 필름에 대한 수요도 증가하고 있습니다. 또한 이 업계의 신제품은 자외선 차단 기능이 뛰어나며, 강한 햇볕에도 견딜 수 있습니다. 이들 제품 중 일부는 토양 온도 조절에 탁월하여 작물의 성장을 촉진할 수 있습니다. 또한 물 보존성이 뛰어나 물 사용량을 줄일 수 있는 제품도 있습니다. 이러한 제품 중 일부는 설치 및 사용 중에 찢어지지 않는 제품도 있습니다. 업계에서는 과일, 채소, 꽃 등 작물의 필요에 따라 설계된 작물용 필름도 판매되고 있습니다.

정밀 시비 시스템: 멀치 필름을 깔기 위해 채택된 기술도 현대 기술을 적절히 활용하여 현대화가 진행되고 있습니다. 현대 기술로 인해 농가는 자동멀칭기를 효과적으로 활용할 수 있게 되었습니다. 이를 통해 멀치 필름을 적절하고 균일하게 깔 수 있으며, 시간과 노동력을 절약할 수 있습니다. 토양 수분 센서는 관개에 대한 적절한 지식을 얻는 데 도움이 되고 있습니다. IoT 기술의 도움을 받아 밭의 현황에 대한 적절한 정보를 얻을 수 있습니다. GPS를 활용한 농장 관리 기술은 멀치 필름을 깔 때 적절한 간격 계획을 세우는 데 도움을 주고 있습니다. 이를 통해 멀티 필름을 깔 때 실수를 방지할 수 있습니다. 이러한 실수는 자원 낭비로 이어집니다. 멀티필름의 적절한 활용은 같은 땅에서 얻을 수 있는 효율성과 생산성 향상에 기여하고 있습니다.

세계의 멀티필름 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 채택에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 멀치 필름 시장 : 성분별

제10장 멀치 필름 시장 : 유형별

제11장 멀치 필름 시장 : 용도별

제12장 멀치 필름 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 인접 시장과 관련 시장

제17장 부록

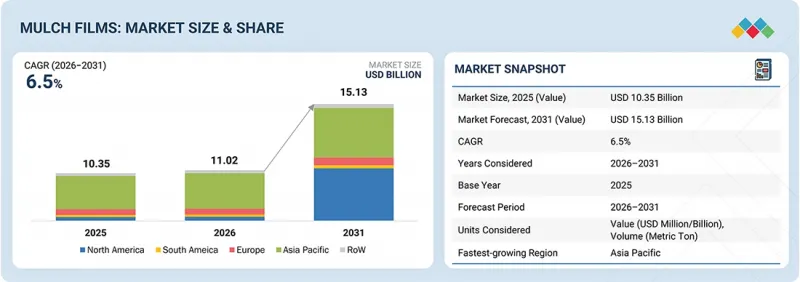

KSA 26.05.13The global mulch films market is estimated at USD 11.02 billion in 2026 and is projected to reach USD 15.13 billion by 2031, at a CAGR of 6.5%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD) and Volume (Metric Tons) |

| Segments | By Type, Element, and Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The market is experiencing significant changes due to the increased adoption of precision agriculture, protected cultivation, and advanced soil management. The incorporation of smart farming technology, such as sensor-based irrigation systems, automatic mulch laying equipment, and climate-responsive films, is further enhancing product capabilities. Major players in the industry are actively working towards developing high-performance biodegradable and UV-stabilized films to improve soil health, minimize environmental damage, and encourage green farming. Recent product developments in the mulch films industry indicate an increased focus on product longevity, moisture retention, and crop-specific capabilities, indicating an upward trend in product growth.

Opportunities and disruption in the mulch films market. The opportunities and disruption in the mulch films industry are largely associated with the rapid shift to sustainable agriculture and resource-efficient farming practices. Mulch films are seen to have tremendous commercial potential for farmers and manufacturers, as the industry is witnessing increased demand for crop yield, better produce quality, and efficient water usage. The use of mulch films by farmers can help in the efficient use of water, reduce weeds, control soil temperature, and reduce the use of herbicides, thereby increasing the profitability of the farming industry, especially in horticulture and high-value crops. The disruption in the industry can be attributed to the increasing environmental regulations on the use of plastic, the rise of eco-friendly alternatives, and the shift to sustainable materials, which are disrupting the industry, thereby creating a challenge for the overall industry to grow.

AI-driven nutrient optimization: Artificial intelligence and machine learning are also useful in the mulch films market. This will help the company understand the soil, the weather, and the crops before they start making the films. They will, therefore, be aware of the thickness, the color, and the type of film to make. For example, the films may be black to control weeds. On the other hand, the transparent ones may be used for warming the soil. The durability of the films and the time taken for them to decompose may also be ascertained using artificial intelligence. This will help prevent failures and costs. The farmers will also benefit from the data tools. This will help them understand when to use the films and the type of film to use. They will, therefore, plan well, and there will be no form of waste. This will result in increased yield from the farms.

Advanced formulation technologies: One of the major areas of focus in the mulch films industry is material development. Companies are developing conventional as well as eco-friendly materials. However, polyethylene films are still in use due to their high strength and cost-effectiveness. At the same time, biodegradable films are also in high demand due to the implementation of stricter rules regarding environmental protection. Additionally, new products in the industry come equipped with better UV protection, allowing them to withstand harsh sun conditions. Some of these products are also better at controlling soil temperature, thereby allowing crops to develop faster. Some of them also provide better moisture retention capabilities, thereby reducing water usage. Some of these products are also tear-resistant during installation as well as usage. Films for crops are also available in the industry, where products are designed according to the needs of crops such as fruits, vegetables, or flowers.

Precision fertigation systems: The techniques that have been adopted for the application of mulch films are also being modernized by making proper use of modern technology. Modern technology has helped farmers in making proper use of automatic mulch laying machines. This helps in the proper and uniform application of mulch films. This has helped in saving time and labor. Soil moisture sensors have helped in acquiring proper knowledge regarding irrigation. With the help of IoT technology, proper knowledge can be obtained regarding the prevailing conditions in the field. GPS-based farm management techniques have helped in proper planning for proper spacing in the application of mulch films. This has helped in avoiding errors in the application of mulch films. Such errors lead to the wastage of resources. Proper techniques for the application of mulch films have helped in increasing efficiency and productivity from the same land.

"Conventional polyolefin-based mulch films stood as the major segment within the form segment of the mulch films market."

The mulch films market indicates that the conventional polyolefin films have the largest market share in the form segment. They include films such as polyethylene, which are commonly used in all farming regions. The films are leading the market due to the ease of production, low cost, and simplicity of use. They are also the preference of the farmers, as they provide good performance in terms of weeds, moisture, and soil temperature. The films are also strong enough to withstand various kinds of weather, making them suitable for repeated use.

These films are easy to store, transport, and apply with the help of standard mulch laying machines. Also, they are available in various colors and thickness levels, making it easy for the farmer to select the product based on the needs of the crop and the climatic conditions. If compared with the other products, the performance of these films is guaranteed, and they are easy to handle. Also, the availability of these films in the market, both in developed and emerging countries, supports the high demand for the product. Furthermore, the low cost and easy supply of the product make it an easy choice for the farmer. Thus, the conventional polyolefin-based mulch films are the market leaders, despite the increasing trend towards biodegradable films.

"Within the application segment, horticulture crops accounted for the largest share."

The mulch films segment indicates that horticulture crops represent the highest share in the application segment. This includes crops such as fruits, vegetables, and flowers, among others. The high share is attributed to factors such as yield, quality, and appearance of crops. Mulch films help in controlling weeds, retaining moisture in the soil, and controlling soil temperature. These factors are crucial in crops that require stable climatic conditions. Mulch films also assist in controlling soil contact, thus making crops clean. Mulch films are used in both greenhouse and field horticulture. They are also helpful in the efficient use of water with the aid of drip irrigation systems. Water loss, herbicides, and labor costs are reduced with the use of these films. They are also helpful in the uniform growth of crops and the yield of crops during different seasons. With the increase in the demand for quality fruits and vegetables, the use of these films is also increasing. This maintains the leading position of the horticulture segment in the market for mulch films. In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the mulch films market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include BASF SE (Germany), Amcor Plc (Switzerland), Dow Inc. (US), Kuraray Co., Ltd. (Japan), and Exxon Mobil Corporation (US). Other important companies include RKW Group (Germany), Intergro, Inc. (United States), Green Maneuver Industries LLP (India), Plastika Kritis S.A. (Greece), and Kothari Group (India). The market also includes Organix Solutions (India), Captain Polyplast Ltd. (India), Sunshine Paper Company (China), Tilak Polypack Pvt. Ltd. (India), and Iris Polymers (India).

Research Coverage:

This research report categorizes the mulch films market by type ( clear/transparent mulch, black mulch, colored mulch, photoselective mulch, degradable mulch, biodegradable mulch, photodegradable mulch, others), element (conventional polyolefin-based mulch films [LLDPE, LDPE, HDPE, EVA], biodegradable & compostable mulch films [PLA, PHA, PBAT], other elements), application (field crop, horticulture crop), and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the global mulch films market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the global mulch films market. Competitive analysis of upcoming startups in the market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leader/new entrants in this market with information on the closest approximations of the revenue numbers for the overall mulch films market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. In-depth Segmentation Based On Type, Element, and Application: Comprehensive analysis across clear/transparent mulch, black mulch, colored mulch, photoselective mulch, degradable mulch, biodegradable mulch, photodegradable mulch, others, conventional polyolefin-based mulch films (LLDPE, LDPE, HDPE, EVA), biodegradable & compostable mulch films (PLA, PHA, PBAT), other elements, application (field crops, horticulture crops). The study examines key drivers (enhancing crop productivity through microclimate management., improving water-use efficiency in irrigated agriculture, promoting protected cultivation via government subsidies, reducing weed pressure and chemical dependency), restraints (addressing agricultural plastic waste accumulation, managing higher costs of biodegradable alternatives, overcoming limited recycling infrastructure in rural areas, improving farmer awareness and technical training), opportunities (increasing adoption of precision irrigation and water management practices, accelerating transition toward sustainable and bio-based films, integrating mulch films with precision irrigation systems), and challenges (navigating regulatory restrictions on plastic usage, mitigating raw material price volatility. ensuring field performance consistency of biodegradable films).

2. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. It evaluates regional demand patterns, irrigation penetration, regulatory policies related to nutrient management, and investment trends in precision agriculture, offering strategic guidance for expansion and localization initiatives.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, BASF SE (Germany), Amcor Plc (Switzerland), Dow Inc. (US), Kuraray Co., Ltd. (Japan), and Exxon Mobil Corporation (US), are profiled in detail. The report covers recent product launches, capacity expansions, strategic partnerships, and investments in specialty nutrient technologies shaping the competitive dynamics of the global mulch market.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for planning investment and market opportunity assessment in the global mulch films sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MULCH FILMS MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MULCH FILMS MARKET

- 3.2 MULCH FILMS MARKET, BY TYPE AND REGION

- 3.3 MULCH FILMS MARKET, BY ELEMENT

- 3.4 MULCH FILMS MARKET, BY ELEMENT

- 3.5 MULCH FILMS MARKET, BY APPLICATION

- 3.6 MULCH FILMS MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Enhancing Crop Productivity Through Microclimate Management

- 4.2.1.2 Improving Water-use Efficiency in Irrigated Agriculture

- 4.2.1.3 Promoting Protected Cultivation via Government Subsidies

- 4.2.1.4 Reducing Weed Pressure and Chemical Dependency

- 4.2.2 RESTRAINTS

- 4.2.2.1 Addressing Agricultural Plastic Waste Accumulation

- 4.2.2.2 Managing Higher Costs of Biodegradable Alternatives

- 4.2.2.3 Limited Recycling Infrastructure in Rural Areas

- 4.2.2.4 Improving Farmer Awareness and Technical Training

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing Adoption of Precision Irrigation and Water Management Practices

- 4.2.3.2 Accelerating Transition Toward Sustainable and Bio-based Films

- 4.2.3.3 Environmental Concerns Related to Plastic Residue Accumulation

- 4.2.4 CHALLENGES

- 4.2.4.1 Navigating Regulatory Restrictions on Plastic Usage

- 4.2.4.2 Mitigating Raw Material Price Volatility

- 4.2.4.3 Ensuring Field Performance Consistency of Biodegradable Films

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MULCH FILMS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 RISE IN POPULATION AND SCARCITY OF ARABLE LAND

- 5.2.2 GLOBAL AGRICULTURAL WATER USE TRENDS IMPACTING MULCH FILMS MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL PROCUREMENT

- 5.3.2 POLYMER PROCESSING AND COMPOUNDING

- 5.3.3 FILM MANUFACTURING (EXTRUSION)

- 5.3.4 PRODUCT CUSTOMIZATION AND PACKAGING

- 5.3.5 DISTRIBUTION AND SALES NETWORK

- 5.3.6 END USE, POST-SALES SUPPORT, AND WASTE MANAGEMENT

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE TREND, BY APPLICATION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO OF HS CODE 392010

- 5.6.2 EXPORT SCENARIO OF HS CODE 392010

- 5.7 KEY CONFERENCES AND EVENTS, 2024-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BASF SE ADVANCED BIODEGRADABLE MULCH FILM PERFORMANCE WITH AI-DRIVEN FIELD ANALYTICS

- 5.9.2 NOVAMONT INTEGRATED AI-BASED AGRONOMIC DATA ANALYTICS FOR BIODEGRADABLE MULCH FILM OPTIMIZATION

- 5.9.3 RKW GROUP IMPLEMENTED AI-ENABLED SMART MULCHING SYSTEM FOR PRECISION HORTICULTURE

- 5.10 IMPACT OF 2025 US TARIFF - MULCH FILMS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 China (Asia Pacific)

- 5.10.4.2 Canada (North America)

- 5.10.4.3 European Union (Europe)

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BIODEGRADABLE AND BIO-BASED MULCH FILMS

- 6.1.2 NANOTECHNOLOGY-ENHANCED MULCH FILMS

- 6.1.3 SMART/SENSOR-INTEGRATED MULCH FILMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DRIP IRRIGATION SYSTEMS

- 6.2.2 PRECISION AGRICULTURE & SOIL MONITORING SENSORS

- 6.2.3 MECHANICAL MULCH FILM LAYING AND RETRIEVAL EQUIPMENT

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIOPLASTICS AND BIOPOLYMER TECHNOLOGY

- 6.3.2 AGRICULTURAL FILM LAYING AND RETRIEVAL MACHINERY

- 6.3.3 SOIL BIODEGRADATION MONITORING & ENVIRONMENTAL TESTING TECHNOLOGIES

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 BIODEGRADABLE AND SOIL-DEGRADABLE MULCH FILM MATERIALS

- 6.5.2 SMART MULCH FILMS WITH SENSOR-INTEGRATED MONITORING

- 6.5.3 PHOTOSELECTIVE AND CLIMATE-ADAPTIVE MULCH FILMS

- 6.5.4 MULTI-LAYER HIGH-PERFORMANCE MULCH FILM STRUCTURES

- 6.5.5 RECYCLABLE AND CIRCULAR ECONOMY-BASED AGRICULTURAL FILMS

- 6.6 IMPACT OF GENERATIVE AI ON MULCH FILMS MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 USE OF GENERATIVE AI ON MULCH FILMS MARKET

- 6.6.3 TOP USE CASES AND MARKET POTENTIAL

- 6.6.4 BEST PRACTICES IN MULCH FILMS INDUSTRY

- 6.6.5 CASE STUDIES OF AI IMPLEMENTATION IN MULCH FILMS MARKET

- 6.6.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MULCH FILMS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.2.3 ADOPTION BARRIER & INTERNAL CHALLENGES

- 8.2.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

- 8.2.4.1 Open-field Crop Farmers (Vegetables, Fruits, Row Crops)

- 8.2.4.2 Greenhouse & Protected Cultivation Operators

- 8.2.4.3 Large Commercial Farms & Contract Farming Operations

- 8.2.4.4 Sustainable & Organic Farming Sector

- 8.2.5 MARKET PROFITABILITY

9 MULCH FILMS MARKET, BY ELEMENT

- 9.1 INTRODUCTION

- 9.2 CONVENTIONAL POLYOLEFIN-BASED MULCH FILMS

- 9.2.1 LLDPE

- 9.2.1.1 Soil temperature regulation to improve crop yields

- 9.2.2 LDPE

- 9.2.2.1 Growth in awareness among farmers led to increased use of LDPE mulch films

- 9.2.3 HDPE

- 9.2.3.1 Extensive use with variegated applications in agriculture

- 9.2.4 EVA

- 9.2.4.1 Increase in awareness of environmental benefits of EVA mulch films

- 9.2.1 LLDPE

- 9.3 BIODEGRADABLE & COMPOSTABLE MULCH FILMS

- 9.3.1 PLA

- 9.3.1.1 Technologically advanced PLA mulch films offer performance with sustainability

- 9.3.2 PHA

- 9.3.2.1 Rise in adoption of sustainable agriculture among farmers

- 9.3.3 PBAT

- 9.3.3.1 Rising adoption of PBAT for high-performance biodegradable mulch films

- 9.3.1 PLA

- 9.4 OTHER ELEMENTS

- 9.4.1 PBS (POLYBUTYLENE SUCCINATE)

- 9.4.1.1 Increasing demand for biodegradable polymers driving adoption of PBS mulch films

- 9.4.2 TPS (THERMOPLASTIC STARCH)

- 9.4.2.1 Expanding use of bio-based materials supporting development of TPS mulch films

- 9.4.3 OXO-PE, SPECIALTY COPOLYMERS, MINOR BLENDS

- 9.4.3.1 Expanding use of bio-based blends

- 9.4.1 PBS (POLYBUTYLENE SUCCINATE)

10 MULCH FILMS MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 CLEAR/TRANSPARENT

- 10.2.1 USE OF CLEAR PLASTIC MULCHES IN COOLER REGIONS

- 10.3 BLACK MULCH

- 10.3.1 INCREASED PRODUCTION OF LEAFY VEGETABLES THAT USE INEXPENSIVE BLACK MULCHES

- 10.4 COLORED MULCH

- 10.4.1 COLORED MULCHES FOR IMPROVED CROP PRODUCTION

- 10.5 PHOTOSELECTIVE MULCH

- 10.5.1 ADOPTION OF PHOTOSELECTIVE MULCH FILMS FOR SUSTAINABLE AGRICULTURE

- 10.6 DEGRADABLE MULCH

- 10.6.1 INCREASE IN USE OF DEGRADABLE MULCH FILMS

- 10.6.2 BIODEGRADABLE MULCH

- 10.6.3 PHOTODEGRADABLE MULCH

- 10.7 OTHER TYPES

11 MULCH FILMS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 FIELD CROPS

- 11.2.1 DEMAND FOR IMPROVED YIELDS OF HIGH-VALUE CROPS

- 11.2.2 CEREALS & GRAINS

- 11.2.3 OILSEEDS & PULSES

- 11.2.4 OTHER FIELD CROPS

- 11.3 HORTICULTURAL CROPS

- 11.3.1 HIGH PREFERENCE FOR COLORED MULCH IN COMMERCIAL HORTICULTURE

- 11.3.2 FRUIT & VEGETABLES

- 11.3.3 FLOWERS & ORNAMENTALS

- 11.3.4 OTHER HORTICULTURE CROPS

12 MULCH FILMS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Rise in demand for mulch films from food and dairy industries

- 12.2.2 CANADA

- 12.2.2.1 Need to reduce water usage, control weed growth, and improve soil quality

- 12.2.3 MEXICO

- 12.2.3.1 Skilled and cost-effective labor force and free trade agreements

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Favorable EU regulations for selecting plastics and new recycling initiatives for mulch films

- 12.3.2 FRANCE

- 12.3.2.1 Over 1 million hectares covered in mulch films, especially black

- 12.3.3 UK

- 12.3.3.1 Need to enhance crop yields, improve crop quality, and reduce weed control costs

- 12.3.4 ITALY

- 12.3.4.1 Adoption of eco-friendly films and various government initiatives to promote mulch films

- 12.3.5 SPAIN

- 12.3.5.1 Implementation of plastic waste recycling, reduction of plastic usage, and landfilling in cooperation

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Massive industrial growth & urbanization, and growth in focus on increasing agricultural output

- 12.4.2 INDIA

- 12.4.2.1 Promotion of agro-textile sector by government and increase in food demand

- 12.4.3 JAPAN

- 12.4.3.1 Advanced crop technologies and need to save labor and time

- 12.4.4 AUSTRALIA & NEW ZEALAND

- 12.4.4.1 Effectiveness of mulch films in promoting growth of avocado trees

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 High adoption of intensive agricultural practices, expansion of irrigated agriculture, and greater demand for high-quality fruits and vegetables

- 12.5.2 ARGENTINA

- 12.5.2.1 Expansion of mulch film adoption driven by export-oriented agriculture

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.6 REST OF THE WORLD (ROW)

- 12.6.1 AFRICA

- 12.6.1.1 Availability of affordable and versatile mulch films

- 12.6.2 MIDDLE EAST

- 12.6.2.1 Need to conserve soil moisture, reduce weed growth, enhance soil fertility, and improve crop yields

- 12.6.1 AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 13.3 REVENUE ANALYSIS, 2020-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Type footprint

- 13.6.5.3 Application footprint

- 13.6.5.4 Type footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPETITIVE SCENARIO

- 13.8.1 PRODUCT LAUNCHES

- 13.8.2 DEALS

- 13.8.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF SE

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 AMCOR PLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 DOW

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 KURARAY

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 EXXON MOBIL CORPORATION

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 RKW GROUP

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 MnM view

- 14.1.7 INTERGRO, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 MnM view

- 14.1.8 GREEN MANEUVER INDUSTRIES LLP

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 MnM view

- 14.1.9 PLASTIKA KRITIS S.A.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 MnM view

- 14.1.10 KOTHARI GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 MnM view

- 14.1.11 ORGANIX SOLUTIONS

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 MnM view

- 14.1.12 CAPTAIN POLYPLAST LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 MnM view

- 14.1.13 SUNSHINE PAPER COMPANY

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 MnM view

- 14.1.14 TILAK POLYPACK PVT. LTD

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 MnM view

- 14.1.15 IRIS POLYMERS

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 MnM view

- 14.1.1 BASF SE

- 14.2 BIODEGRADABLE MULCH FILM MANUFACTURERS

- 14.2.1 EPI (EUROPE) LTD

- 14.2.1.1 Business overview

- 14.2.1.2 Products offered

- 14.2.1.3 MnM view

- 14.2.2 NOVAMONT S.P.A.

- 14.2.2.1 Business overview

- 14.2.2.2 Products offered

- 14.2.2.3 Recent developments

- 14.2.2.4 MnM view

- 14.2.3 ARMANDO ALVAREZ GROUP

- 14.2.3.1 Business overview

- 14.2.3.2 Products offered

- 14.2.3.3 Recent developments

- 14.2.3.4 MnM view

- 14.2.4 ACHILLES CORPORATION

- 14.2.4.1 Business overview

- 14.2.4.2 Products offered

- 14.2.4.3 MnM view

- 14.2.5 WALKI GROUP OY

- 14.2.5.1 Business overview

- 14.2.5.2 Products offered

- 14.2.5.3 MnM view

- 14.2.6 UKHI

- 14.2.7 TURFQUICK AB SWEDEN

- 14.2.8 FILMORGANIC

- 14.2.9 KINGFA SCIENCE & TECHNOLOGY (INDIA) LIMITED

- 14.2.10 GROWIT INDIA PRIVATE LIMITED

- 14.2.1 EPI (EUROPE) LTD

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of major secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 Breakdown of primaries

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.2.2.1 Approach to estimate market size using top-down analysis

- 15.3 DATA TRIANGULATION

- 15.4 RESEARCH ASSUMPTIONS

- 15.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 ADJACENT AND RELATED MARKETS

- 16.1 INTRODUCTION

- 16.2 LIMITATIONS

- 16.3 MULCH FILMS MARKET

- 16.3.1 MARKET DEFINITION

- 16.3.2 MARKET OVERVIEW

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS