|

시장보고서

상품코드

2022835

장섬유 강화 열가소성 수지 시장 예측(-2031년) : 섬유 유형별, 수지 유형별, 제조 프로세스별, 최종 용도 산업별, 지역별Long Fiber Thermoplastics Market by Fiber Type (Glass, Carbon), Resin Type (PA, PP, PEEK, PPA), Manufacturing Process (Pultrusion, Direct-LFT (D-LFT)), End-use Industry, and Region - Global Forecast to 2031 |

||||||

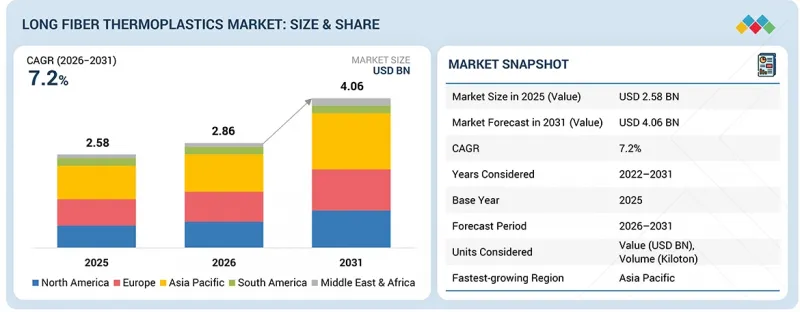

장섬유 강화 열가소성 수지 시장 규모는 2026년에 28억 6,000만 달러로 추정되고 있으며, 2031년까지 40억 6,000만 달러에 달할 것으로 예측됩니다.

이는 예측 기간 중 CAGR이 7.2%임을 나타냅니다. 유리섬유 강화 열가소성 수지는 탄소섬유에 비해 상대적으로 저렴하면서도 강도, 강성, 내충격성을 겸비하여 자동차, 전기-전자 및 산업 분야에서 널리 사용되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 섬유 유형별, 수지 유형별, 제조 프로세스별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

이 부문은 특히 비용 대비 성능 최적화가 필수적인 대량 생산 애플리케이션에서 안정적인 수요가 지속되고 있습니다. 유리섬유의 배합 및 가공 기술의 지속적인 발전으로 재료 특성이 향상되고 그 응용 범위가 확대되고 있습니다. 탄소섬유에 비해 유리섬유 강화 열가소성 수지의 성능은 떨어지지만, 하이엔드 소재로의 전환이 진행됨에 따라 성장률이 약간 둔화되어 빠르게 성장하는 부문에 뒤쳐지고 있습니다.

"2025년 기준, PA 수지 유형 부문은 전체 장섬유 강화 열가소성 수지 시장에서 두 번째 점유율을 차지했습니다. "

폴리아미드(PA) 수지 부문은 기계적 성능과 가공성의 우수한 균형에 힘입어 2025년 장섬유 강화 열가소성 수지 시장에서 두 번째 점유율을 차지할 것으로 예상됩니다. PA계 장섬유 강화 열가소성 수지는 높은 강도, 우수한 내마모성 및 내스크래치성, 우수한 열 안정성으로 인해 자동차, 산업, 전기 및 전자 분야의 가혹한 용도에 널리 사용되고 있습니다. 구조적 무결성을 유지하면서 금속 부품을 대체할 수 있는 이 소재의 특성은 그 보급을 더욱 촉진하고 있습니다. 잘 구축된 공급망, 광범위한 제품 가용성 및 다양한 보강재와의 호환성이 시장 점유율을 높이는 데 기여하고 있지만, 신흥 고성능 수지도 특수 응용 분야에서 점차 그 존재감을 드러내고 있습니다.

"금액 기준으로는 풀트러젼 공정 분야가 예측 기간 중 두 번째로 높은 성장률을 기록할 것으로 예상됩니다. "

금액 기준으로는 풀루션 프로세스 분야가 예측 기간 중 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 이는 일관된 품질과 높은 구조적 성능을 갖춘 연속 섬유 강화 프로파일을 생산할 수 있는 능력에 의해 지원됩니다. 풀루션은 우수한 강도, 강성, 치수 안정성을 갖춘 부품 제조가 가능하며, 건설, 인프라, 전기 시스템 분야에서의 적용에 적합합니다. 이 공정은 재료의 낭비를 최소화하면서 길고 균일한 부품을 생산하는 데 매우 효율적이며, 대규모 생산에서 비용 최적화를 돕습니다. 내구성, 내식성, 경량성을 갖춘 구조부재에 대한 수요 증가로 인해 풀루젼 방식의 장섬유 강화 열가소성 수지의 채택이 가속화되고 있으며, 이 부문은 시장의 주요 성장 분야로 자리매김하고 있습니다.

"금액 기준으로는 스포츠 용품 부문이 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다. "

금액 기준으로는 고급 스포츠 용품의 고성능 경량 소재에 대한 수요가 증가함에 따라 스포츠 용품 부문이 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다. 장섬유 강화 열가소성 수지는 우수한 강도 대 중량비, 내충격성, 내구성이 뛰어나 자전거, 라켓, 헬멧, 보호구 등의 제품에 점점 더 많이 사용되고 있습니다. 이러한 소재는 안전성과 제품의 내구성을 보장하는 동시에 선수의 퍼포먼스를 향상시킵니다. 피트니스 및 레크리에이션 활동에 대한 소비자의 관심 증가와 스포츠 용품의 고급화 추세는 첨단 복합소재의 채택을 촉진하며 이 부문의 강력한 성장세를 지원하고 있습니다.

"2025년 유럽은 전체 장섬유 강화 열가소성 수지 시장에서 두 번째 점유율을 차지했습니다. "

2025년 유럽은 장섬유 강화 열가소성 수지 시장에서 두 번째 점유율을 차지했습니다. 이는 탄탄한 자동차 및 산업 기반과 더불어 첨단 소재에 대한 강한 집중력을 바탕으로 한 것입니다. 이 지역에는 폭스바겐 AG, BMW AG, Stellantis N.V. 등 주요 자동차 제조업체들이 소재하고 있으며, 경량화 및 연비 효율 향상을 위해 장섬유 강화 열가소성 수지의 채용을 확대하고 있습니다. LFT 소재는 강도와 안전 기준을 유지하면서 차량 중량을 줄이기 위해 프런트 엔드 모듈, 차체 하부 차폐, 구조 부품 등에 널리 사용되고 있습니다. 유럽 전역의 엄격한 환경 규제와 지속가능성 목표가 재활용 가능하고 가벼운 소재의 사용을 촉진하고 있습니다. 독일, 프랑스, 이탈리아 등의 국가들은 자동차, 전기 및 전자, 산업 분야에서 고성능 열가소성 수지를 가장 먼저 도입하고 있습니다. 이러한 탄탄한 산업 생태계와 규제적 지원은 유럽의 큰 시장 점유율에 기여하고 있습니다.

이 보고서에서는 다음 기업에 대한 종합적인 분석을 제공합니다. :

이 시장의 주요 기업으로는 Celanese Corporation(미국), SABIC(사우디아라비아), Avient Corporation(미국), Daicel Corporation(일본), RTP Company(미국), Lotte Chemical Corporation(한국), Syensqo(벨기에), BASF SE(독일), Mitsubishi Chemical Group Corporation(일본), Asahi Kasei Corporation(일본), KINGFA(중국), Toray Industries, Inc.(일본), Xiamen LFT Composite Plastic(중국), BGF Group(중국), Lehmann&Voss&Co. KG(독일) 등을 들 수 있습니다.

조사 범위

장섬유 열가소성 수지 시장을 섬유 유형(유리, 탄소), 수지 유형(PA, PP, PEEK, PPA), 제조 공정(풀트러션, 다이렉트 LFT), 최종 용도 산업(자동차, 전기-전자, 스포츠용품, 소비재), 지역(북미, 유럽, 아시아태평양, 중동, 아시아태평양, 남미, 아프리카, 중동, 유럽, 아시아태평양, 남미) 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류하고 있습니다. 이 보고서의 연구 범위에는 장섬유 강화 열가소성 수지 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 포괄적인 조사를 통해 사업 개요, 솔루션 및 서비스, 주요 전략, 장섬유 강화 열가소성 수지 시장의 최근 동향에 대한 인사이트를 제공합니다. 또한 이 보고서에는 장섬유 강화 열가소성 수지 시장 생태계에서 신생 스타트업 기업의 경쟁 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 장섬유 강화 열가소성 수지 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 자신의 비즈니스를 더 나은 위치에 놓고 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인 및 과제에 대한 정보를 제공함으로써 시장 동향을 파악할 수 있도록 지원합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(경량 및 연비 효율 차량에 대한 수요 증가, 전기화 및 EV 생산 증가), 제약 요인(복잡한 제조 공정, 열경화성 복합재 및 금속과의 경쟁), 기회 요인(금속 대체 응용 분야에서의 채택 확대), 도전 과제(전체 시스템 비용 절감 필요) 분석은 장섬유 강화 열가소성 수지 시장의 성장에 영향을 미치고 있습니다. 의 성장에 영향을 미치고 있습니다.

- 제품 개발/혁신: 장섬유 열가소성 수지 시장의 미래 기술, 연구개발 활동 및 신제품 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 다양한 지역의 장섬유 강화 열가소성 수지 시장을 분석합니다.

- 시장 다각화: 장섬유 열가소성 수지 시장의 서비스, 미개발 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁 분석 : Celanese Corporation(미국), SABIC(사우디아라비아), Avient Corporation(미국), Daicel Corporation(일본), RTP Company(미국), Lotte Chemical Corporation(한국), Syensqo(벨기에), BASF SE(독일), Mitsubishi Chemical Group Corporation(일본), Asahi Kasei Corporation(일본), KINGFA(중국), Toray Industries, Inc.(일본), Xiamen LFT Composite Plastic(중국), BGF Group(중국), Lehmann&Voss&Co. KG(독일) 등 주요 기업의 시장점유율, 성장전략, 제품 라인업에 대한 상세 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 장섬유 강화 열가소성 수지 시장(섬유 유형별)

제10장 장섬유 강화 열가소성 수지 시장(수지 유형별)

제11장 장섬유 강화 열가소성 수지 시장(제조 프로세스별)

제12장 장섬유 강화 열가소성 수지 시장(용도별)

제13장 장섬유 강화 열가소성 수지 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

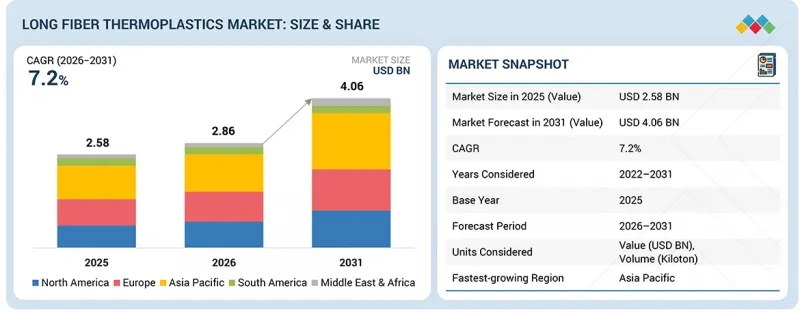

KSA 26.05.14The long fiber thermoplastics market is estimated at USD 2.86 billion in 2026 and is projected to reach USD 4.06 billion by 2031, reflecting a CAGR of 7.2% over the forecast period. Glass-fiber-reinforced thermoplastics offer a favorable combination of strength, stiffness, and impact resistance at a relatively lower cost than carbon fiber, making them widely adopted across automotive, electrical & electronics, and industrial applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | By fiber type, resin type, manufacturing process, end-use industry, and region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, South America |

The segment continues to see steady demand, particularly in high-volume applications where cost-performance optimization is critical. Ongoing advancements in glass-fiber formulations and processing technologies are enhancing material properties and expanding their application scope. Compared with carbon fiber, glass-fiber-reinforced thermoplastics deliver lower performance, and the ongoing shift toward high-end materials slightly moderates their growth rate, positioning them behind faster-growing segments.

"PA resin type segment accounted for second-largest share of the overall long fiber thermoplastics market in 2025."

The polyamide (PA) resin segment accounted for the second-largest share of the long fiber thermoplastics market in 2025, driven by its strong balance of mechanical performance and processability. PA-based long fiber thermoplastics are widely used for their high strength, excellent wear and abrasion resistance, and good thermal stability, making them suitable for demanding applications in the automotive, industrial, and electrical & electronics sectors. The material's ability to replace metal components while maintaining structural integrity has further supported its widespread adoption. The established supply chain, broad product availability, and compatibility with various reinforcement types contribute to its significant market share, although emerging high-performance resins are gradually gaining traction in specialized applications.

"In terms of value, the pultrusion process segment is expected to register the second fastest growth during the forecast period."

In terms of value, the pultrusion process segment is expected to be the second-fastest-growing during the forecast period, driven by its ability to produce continuous fiber-reinforced profiles with consistent quality and high structural performance. Pultrusion enables the manufacturing of components with excellent strength, stiffness, and dimensional stability, making it suitable for applications in construction, infrastructure, and electrical systems. The process is highly efficient for producing long, uniform parts with minimal material waste, supporting cost optimization in large-scale production. The increasing demand for durable, corrosion-resistant, and lightweight structural components is accelerating the adoption of pultrusion-based long-fiber thermoplastics, positioning it as a key growth segment in the market.

"In terms of value, the sporting goods segment is expected to register the highest CAGR during the forecasted period."

In terms of value, the sporting goods segment is expected to post the highest CAGR over the forecast period, driven by rising demand for high-performance, lightweight materials in advanced sports equipment. Long-fiber thermoplastics are increasingly used in products such as bicycles, rackets, helmets, and protective gear because of their superior strength-to-weight ratio, impact resistance, and durability. These materials enhance athlete performance while ensuring safety and product longevity. Growing consumer interest in fitness and recreational activities, along with increasing premiumization in sports equipment, is boosting adoption of advanced composite materials, supporting strong growth in this segment.

"Europe accounted for the second-largest share of the overall long fiber thermoplastics market in 2025."

Europe accounted for the second-largest share of the long fiber thermoplastics market in 2025, supported by its well-established automotive and industrial base and a strong focus on advanced materials. The region is home to leading automotive manufacturers such as Volkswagen AG, BMW AG, and Stellantis N.V., which are increasingly adopting long fiber thermoplastics for lightweighting and improved fuel efficiency. LFT materials are widely used in front-end modules, underbody shields, and structural components to reduce vehicle weight while maintaining strength and safety standards. Stringent environmental regulations and sustainability targets across Europe are encouraging the use of recyclable and lightweight materials. Countries such as Germany, France, and Italy are at the forefront of adopting high-performance thermoplastics in automotive, electrical & electronics, and industrial applications. This strong industrial ecosystem and regulatory support contribute to Europe's significant market share.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 40%, Tier 2 - 33%, and Tier 3 - 27%

- By Designation: C-level - 50%, Director-level - 30%, and Managers - 20%

- By Region: North America - 15%, Europe - 50%, Asia Pacific - 20%, the Middle East & Africa - 10%, and South America - 5%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market include Celanese Corporation (US), SABIC (Saudi Arabia), Avient Corporation (US), Daicel Corporation (Japan), RTP Company (US), Lotte Chemical Corporation (South Korea), Syensqo (Belgium), BASF SE (Germany), Mitsubishi Chemical Group Corporation (Japan), Asahi Kasei Corporation (Japan), KINGFA (China), Toray Industries, Inc. (Japan), Xiamen LFT Composite Plastic Co., Ltd. (China), BGF Group (China), Lehmann&Voss&Co. KG (Germany), and others.

Research Coverage

This research report categorizes the long fiber thermoplastics market by fiber type (glass, carbon), resin type (PA, PP, PEEK, PPA), manufacturing process (pultrusion, direct-LFT), end-use industry (automotive, electrical & electronics, sporting goods, consumer goods), and region (North America, Europe, Asia Pacific, Middle East & Africa, South America). The scope of the report includes detailed information on the major factors influencing the growth of the long fiber thermoplastics market, such as drivers, restraints, challenges, and opportunities. A comprehensive examination of key industry players is conducted to provide insights into their business overview, solutions and services, key strategies, and recent developments in the long fiber thermoplastics market. This report also includes a competitive analysis of upcoming startups in the long fiber thermoplastics market ecosystem.

Reasons to buy this report

The report will provide market leaders and new entrants with the closest approximations of revenue for the overall long fiber thermoplastics market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Growing demand for lightweight and fuel-efficient vehicles, and rising electrification and EV production), restraints (complex manufacturing processes, competition from thermoset composites and metals), opportunities (increasing adoption in metal replacement applications), and challenges (need to reduce overall system cost) are influencing the growth of the long fiber thermoplastics market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the long fiber thermoplastics market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the long fiber thermoplastics market across varied regions

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the long fiber thermoplastics market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players such as Celanese Corporation (US), SABIC (Saudi Arabia), Avient Corporation (US), Daicel Corporation (Japan), RTP Company (US), Lotte Chemical Corporation (South Korea), Syensqo (Belgium), BASF SE (Germany), Mitsubishi Chemical Group Corporation (Japan), Asahi Kasei Corporation (Japan), KINGFA (China), Toray Industries, Inc. (Japan), Xiamen LFT Composite Plastic Co., Ltd. (China), BGF Group (China), Lehmann&Voss&Co. KG (Germany), and others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LONG FIBER THERMOPLASTICS MARKET

- 3.2 LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY AND REGION

- 3.3 LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 3.4 LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 3.5 LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand for lightweight and fuel-efficient vehicles

- 4.2.1.2 Rising electrification and EV production

- 4.2.1.3 Superior mechanical performance over short fiber thermoplastics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Higher material and processing costs than conventional plastics

- 4.2.2.2 Complex manufacturing processes

- 4.2.2.3 Competition from thermoset composites and metals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing adoption in metal replacement applications

- 4.2.3.2 Growing demand for recyclable and sustainable composite materials

- 4.2.3.3 Expansion into new applications such as EV battery systems, infrastructure, and industrial automation components

- 4.2.4 CHALLENGES

- 4.2.4.1 Need to reduce overall system cost

- 4.2.4.2 High R&D and qualification timelines

- 4.2.4.3 Maintaining consistent fiber distribution and performance during processing

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN LONG FIBER THERMOPLASTICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN ELECTRIC & ELECTRONICS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF LONG FIBER THERMOPLASTICS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY

- 5.5.2 AVERAGE SELLING PRICE TREND OF LONG FIBER THERMOPLASTICS, BY REGION

- 5.6 TRADE ANALYSIS, 2021-2025

- 5.6.1 IMPORT SCENARIO (HS CODE 7019)

- 5.6.2 EXPORT SCENARIO (HS CODE 7019)

- 5.6.3 IMPORT SCENARIO (HS CODE 681511)

- 5.6.4 EXPORT SCENARIO (HS CODE 681511)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CELANESE: FRONT-END MODULE CARRIER FOR AUTOMOTIVE LIGHTWEIGHTING

- 5.10.2 SABIC: ELECTRIC VEHICLE BATTERY ENCLOSURE STRUCTURES

- 5.10.3 RTP COMPANY: INDUSTRIAL PALLETS & LOGISTICS LOAD CARRIERS

- 5.11 IMPACT OF 2025 US TARIFF ON LONG FIBER THERMOPLASTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.4 Middle East & Africa

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DIRECT LONG FIBER THERMOPLASTICS (D-LFT) PROCESSING TECHNOLOGY

- 6.1.2 LONG FIBER THERMOPLASTICS IN ADDITIVE MANUFACTURING (LFRT 3D PRINTING)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 HYBRID METAL THERMOPLASTIC STRUCTURES (OVERMOLDING TECHNOLOGY)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2028) | FOUNDATION & INCREMENTAL COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2031) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2031-2036+) | SYSTEM-LEVEL OPTIMIZATION & NETWORK INTELLIGENCE

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPES

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 TOP 10 PATENT OWNERS (US) IN LAST 5 YEARS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 STRUCTURAL EV BATTERY INTEGRATION (CELL-TO-PACK / CELL-TO-CHASSIS)

- 6.5.2 HYBRID COMPOSITE AUTOMOTIVE PLATFORMS

- 6.5.3 ADVANCED MODULAR CONSTRUCTION SYSTEMS

- 6.5.4 HIGH-PERFORMANCE DATA CENTER STRUCTURES

- 6.5.5 NEXT-GENERATION MOBILITY (UAVS, EVTOLS, LIGHTWEIGHT TRANSPORT)

- 6.6 IMPACT OF AI/GEN AI ON LONG FIBER THERMOPLASTICS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN LONG FIBER THERMOPLASTICS MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN LONG FIBER THERMOPLASTICS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN LONG FIBER THERMOPLASTICS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 CELANESE: AUTOMOTIVE STRUCTURAL LIGHTWEIGHT COMPONENTS

- 6.7.2 SABIC: EV BATTERY STRUCTURAL MATERIALS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF LONG FIBER THERMOPLASTICS

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF LONG FIBER THERMOPLASTICS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 9.1 INTRODUCTION

- 9.2 GLASS FIBER

- 9.2.1 COST-DRIVEN DOMINANCE IN HIGH-VOLUME STRUCTURAL APPLICATIONS

- 9.3 CARBON FIBER

- 9.3.1 RISING ADOPTION IN HIGH-PERFORMANCE AUTOMOTIVE AND MOBILITY APPLICATIONS

- 9.4 OTHER FIBER TYPES

10 LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 10.1 INTRODUCTION

- 10.2 POLYPROPYLENE (PP)

- 10.2.1 DOMINANT RESIN DRIVEN BY COST EFFICIENCY AND HIGH-VOLUME APPLICATIONS

- 10.2.2 PP: LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 10.3 POLYAMIDE (PA)

- 10.3.1 HIGH-PERFORMANCE RESIN ENABLING UNDER-THE-HOOD LIGHTWEIGHTING

- 10.3.2 PA: LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 10.4 POLYETHER ETHER KETONE (PEEK)

- 10.4.1 HIGH PERFORMANCE RESIN FOR METAL REPLACEMENT AND NICHE STRUCTURAL APPLICATIONS

- 10.4.2 PEEK: LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 10.5 POLYPHTHALAMIDE (PPA)

- 10.5.1 HIGH-TEMPERATURE METAL REPLACEMENT RESIN FOR ELECTRICAL AND POWERTRAIN APPLICATIONS

- 10.5.2 PPA: LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 10.6 OTHER RESIN TYPES

- 10.6.1 POLYBUTYLENE TEREPHTHALATE (PBT)

- 10.6.2 POLYPHENYLENE SULFIDE (PPS)

- 10.6.3 OTHER RESIN TYPES: LONG FIBER THERMOPLASTICS MARKET, BY REGION

11 LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 11.1 INTRODUCTION

- 11.2 PULTRUSION

- 11.2.1 HIGHLY AUTOMATED, COST-EFFICIENT PROCESS DRIVEN BY AUTOMOTIVE LIGHTWEIGHTING AND EV APPLICATIONS

- 11.2.2 PULTRUSION: LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 11.3 DIRECT-LFT (D-LFT)

- 11.3.1 INLINE COMPOUNDING PROCESS ENABLING SUPERIOR PROPERTY CONTROL AND HIGH-VOLUME AUTOMOTIVE APPLICATIONS

- 11.3.2 D-LFT: LONG FIBER THERMOPLASTICS MARKET, BY REGION

12 LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 AUTOMOTIVE

- 12.2.1 USED IN HOODS, SUNROOF FRAMES, SEATS, DOORS, AND LUGGAGE COMPARTMENTS

- 12.2.2 INTERIOR COMPONENTS

- 12.2.3 EXTERIOR COMPONENTS

- 12.2.4 LONG FIBER THERMOPLASTICS MARKET IN AUTOMOTIVE INDUSTRY, BY REGION

- 12.3 ELECTRICAL & ELECTRONICS

- 12.3.1 GROWING ELECTRIFICATION AND MINIATURIZATION DRIVING DEMAND FOR HIGH PERFORMANCE LFT COMPONENTS

- 12.3.2 LONG FIBER THERMOPLASTICS MARKET IN ELECTRICAL & ELECTRONICS, BY REGION

- 12.4 CONSUMER GOODS

- 12.4.1 RISING DEMAND FOR DURABLE, LIGHTWEIGHT, AND COST-OPTIMIZED MATERIALS IN CONSUMER PRODUCTS

- 12.4.2 LONG FIBER THERMOPLASTICS MARKET IN CONSUMER GOODS, BY REGION

- 12.5 SPORTING GOODS

- 12.5.1 PERFORMANCE-DRIVEN MATERIAL SHIFT TOWARD LIGHTWEIGHT AND HIGH STRENGTH COMPOSITES IN SPORTS EQUIPMENT

- 12.5.2 LONG FIBER THERMOPLASTICS MARKET IN SPORTING GOODS, BY REGION

- 12.6 OTHER END-USE INDUSTRIES

- 12.6.1 MARINE

- 12.6.2 AEROSPACE

- 12.6.3 CONSTRUCTION

- 12.6.4 MEDICAL

- 12.6.5 LONG FIBER THERMOPLASTICS MARKET IN OTHER END-USE INDUSTRIES, BY REGION

13 LONG FIBER THERMOPLASTICS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 13.2.2 NORTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 13.2.3 NORTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 13.2.4 NORTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 13.2.5 NORTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

- 13.2.5.1 US

- 13.2.5.1.1 Regulatory push and EV transition driving LFT demand

- 13.2.5.2 Canada

- 13.2.5.2.1 EV policies and aerospace manufacturing driving long fiber thermoplastic demand

- 13.2.5.3 Mexico

- 13.2.5.3.1 Automotive production shift and nearshoring driving long fiber thermoplastic demand

- 13.2.5.1 US

- 13.3 EUROPE

- 13.3.1 EUROPE: LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 13.3.2 EUROPE: LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 13.3.3 EUROPE: LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 13.3.4 EUROPE: LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 13.3.5 EUROPE: LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

- 13.3.5.1 Germany

- 13.3.5.1.1 Automotive innovation and lightweighting strategies driving long fiber thermoplastic demand

- 13.3.5.2 France

- 13.3.5.2.1 EV transition and lightweighting initiatives drive long fiber thermoplastic demand

- 13.3.5.3 UK

- 13.3.5.3.1 Advanced composites adoption across automotive, aerospace, and industrial sectors driving long fiber thermoplastic demand

- 13.3.5.4 Italy

- 13.3.5.4.1 Automotive export base and performance engineering driving long fiber thermoplastic demand

- 13.3.5.5 Spain

- 13.3.5.5.1 Automotive production and supply chain localization driving long fiber thermoplastic demand

- 13.3.5.6 Rest of Europe

- 13.3.5.1 Germany

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 13.4.2 ASIA PACIFIC: LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 13.4.3 ASIA PACIFIC: LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 13.4.4 ASIA PACIFIC: LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 13.4.5 ASIA PACIFIC: LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

- 13.4.5.1 China

- 13.4.5.1.1 EV scale and localized supply chains accelerating LFT market expansion

- 13.4.5.2 Japan

- 13.4.5.2.1 Advanced material innovation and hybrid vehicle production driving demand

- 13.4.5.3 South Korea

- 13.4.5.3.1 EV export strength and advanced composites driving long fiber thermoplastic demand

- 13.4.5.4 India

- 13.4.5.4.1 Infrastructure expansion and automotive localization driving long fiber thermoplastic demand

- 13.4.5.5 Rest of Asia Pacific

- 13.4.5.1 China

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 13.5.2 MIDDLE EAST & AFRICA: LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 13.5.3 MIDDLE EAST & AFRICA: LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 13.5.4 MIDDLE EAST & AFRICA: LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 13.5.5 MIDDLE EAST & AFRICA: LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

- 13.5.6 GCC COUNTRIES

- 13.5.6.1 Saudi Arabia

- 13.5.6.1.1 Automotive localization and industrial investments drive long fiber thermoplastic demand

- 13.5.6.2 UAE

- 13.5.6.2.1 Urban development and industrial expansion fueling long fiber thermoplastic adoption

- 13.5.6.3 Rest of GCC Countries

- 13.5.6.1 Saudi Arabia

- 13.5.7 SOUTH AFRICA

- 13.5.7.1 Automotive exports and mining applications driving long fiber thermoplastic demand in South Africa

- 13.5.8 REST OF MIDDLE EAST & AFRICA

- 13.6 SOUTH AMERICA

- 13.6.1 SOUTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY FIBER TYPE

- 13.6.2 SOUTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY MANUFACTURING PROCESS

- 13.6.3 SOUTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY RESIN TYPE

- 13.6.4 SOUTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY END-USE INDUSTRY

- 13.6.5 SOUTH AMERICA: LONG FIBER THERMOPLASTICS MARKET, BY COUNTRY

- 13.6.5.1 Brazil

- 13.6.5.1.1 Automotive base and aerospace manufacturing supporting demand

- 13.6.5.2 Argentina

- 13.6.5.2.1 Manufacturing recovery and material substitution supporting long fiber thermoplastic uptake

- 13.6.5.3 Rest of South America

- 13.6.5.1 Brazil

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 BRAND COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Fiber type footprint

- 14.6.5.4 Resin type footprint

- 14.6.5.5 Manufacturing process type footprint

- 14.6.5.6 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY COMPANIES

- 15.1.1 CELANESE CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 SABIC

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 BASF SE

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 MITSUBISHI CHEMICAL GROUP CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 AVIENT CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 DAICEL CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.4 MnM view

- 15.1.6.4.1 Right to win

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses and competitive threats

- 15.1.7 ASAHI KASEI CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.4 MnM view

- 15.1.7.4.1 Right to win

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 RTP COMPANY, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 MnM view

- 15.1.8.3.1 Right to win

- 15.1.8.3.2 Strategic choices

- 15.1.8.3.3 Weaknesses and competitive threats

- 15.1.9 SYENSQO

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.9.4 MnM view

- 15.1.9.4.1 Right to win

- 15.1.9.4.2 Strategic choices

- 15.1.9.4.3 Weaknesses and competitive threats

- 15.1.10 TORAY INDUSTRIES, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Expansions

- 15.1.10.4 MnM view

- 15.1.10.4.1 Right to win

- 15.1.10.4.2 Strategic choices

- 15.1.10.4.3 Weaknesses and competitive threats

- 15.1.11 LOTTE CHEMICAL CORPORATION

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.3.2 Deals

- 15.1.11.3.3 Expansions

- 15.1.11.3.4 Other developments

- 15.1.11.4 MnM view

- 15.1.11.4.1 Right to win

- 15.1.11.4.2 Strategic choices

- 15.1.11.4.3 Weaknesses and competitive threats

- 15.1.12 KINGFA SCIENCE & TECHNOLOGY CO., LTD.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 MnM view

- 15.1.12.3.1 Right to win

- 15.1.12.3.2 Strategic choices

- 15.1.12.3.3 Weaknesses and competitive threats

- 15.1.13 XIAMEN LFT COMPOSITE PLASTIC CO., LTD.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 MnM view

- 15.1.13.3.1 Right to win

- 15.1.13.3.2 Strategic choices

- 15.1.13.3.3 Weaknesses and competitive threats

- 15.1.14 BGF GROUP

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 MnM view

- 15.1.14.3.1 Right to win

- 15.1.14.3.2 Strategic choices

- 15.1.14.3.3 Weaknesses and competitive threats

- 15.1.15 LEHMANN&VOSS&CO.

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 MnM view

- 15.1.15.3.1 Right to win

- 15.1.15.3.2 Strategic choices

- 15.1.15.3.3 Weaknesses and competitive threats

- 15.1.1 CELANESE CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 TECHNOCOMPOUND GMBH

- 15.2.2 POLYRAM GROUP

- 15.2.3 AKRO-PLASTIC GMBH

- 15.2.4 GS CALTEX CORPORATION

- 15.2.5 SUMITOMO CHEMICAL CO., LTD.

- 15.2.6 PRET ADVANCED MATERIALS (SHANGHAI PRET)

- 15.2.7 ZHEJIANG JUNER NEW MATERIALS CO., LTD.

- 15.2.8 SUZHOU SUNWAY POLYMER CO., LTD

- 15.2.9 INDORE COMPOSITE PVT. LTD.

- 15.2.10 DIEFFENBACHER GMBH MASCHINEN- UND ANLAGENBAU

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary interview participants

- 16.1.2.3 Breakdown of interviews with experts

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 16.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 16.4 FORECAST NUMBER CALCULATION

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS