|

시장보고서

상품코드

2024209

데이터센터용 칩 시장 : 구성요소별, 데이터센터 규모별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2032년)Data Center Chip Market by Component (Processors, Memory, Network, Sensors, Power Management, Analog & Mixed-Signal ICS), Application (AI, General-purpose Computing), Data Center Size, & End User - Global Forecast to 2032 |

||||||

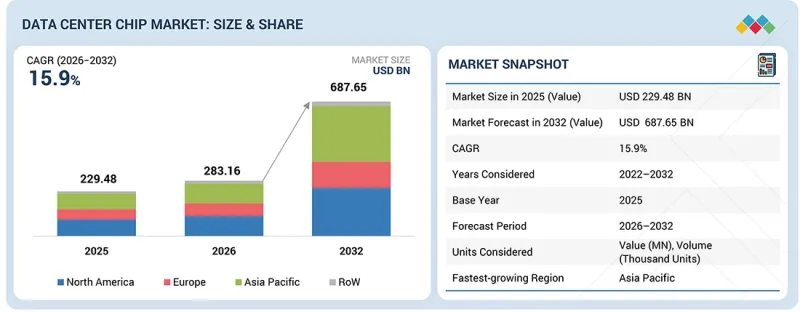

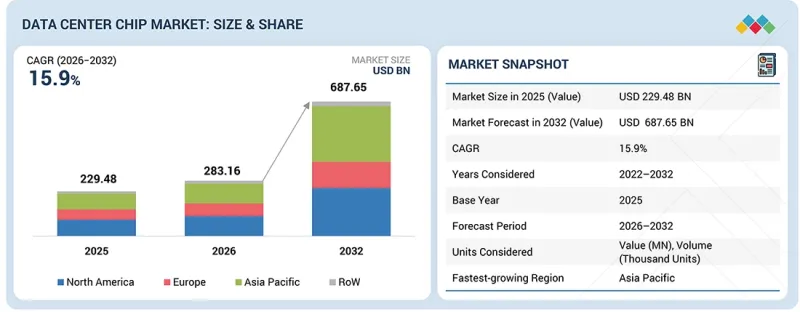

데이터센터용 칩 시장 규모는 2026년 2,831억 6,000만 달러에서 2032년까지 6,876억 5,000만 달러로 성장할 것으로 예상되며, 이 기간 동안 연평균 성장률(CAGR)은 15.9%에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 구성요소별, 데이터센터 규모별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

AI, 생성형 AI 및 데이터 집약적 워크로드에 대한 수요가 증가함에 따라 시장은 크게 성장할 것으로 예상됩니다. 이들은 처리 속도 향상과 지연 감소를 위해 고급 프로세서, 메모리 및 전용 가속기를 필요로 합니다. 또한, 하이퍼스케일 데이터센터의 확대와 칩렛 아키텍처 및 이기종 컴퓨팅과 같은 기술의 발전은 확장 가능하고 에너지 효율적이며 고성능의 칩 솔루션에 대한 수요를 촉진하고 있습니다.

"2025년 기준, 최종사용자로서 클라우드 서비스 제공업체가 가장 큰 시장 점유율을 차지했습니다."

클라우드 서비스 제공업체는 하이퍼스케일 데이터센터의 광범위한 구축과 AI, 스토리지, 컴퓨팅 서비스를 지원하기 위한 클라우드 인프라의 지속적인 확장으로 인해 2025년 데이터센터용 칩 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이들 업체들은 다양한 데이터 집약적 워크로드를 관리하기 위해 CPU, GPU, 커스텀 액셀러레이터를 포함한 대량의 고급 칩을 필요로 하는 방대한 서버 네트워크를 운영하고 있습니다. 또한, 풍부한 자금력을 바탕으로 차세대 반도체 기술로의 잦은 업그레이드와 성능 및 비용 효율성 향상을 위한 맞춤형 실리콘에 대한 투자가 가능해졌습니다. 그 결과, 클라우드 운영의 규모, 집중도 및 지속적인 성장으로 인해 다른 최종사용자에 비해 칩 소비량이 크게 증가하여 시장에서의 지배적 지위를 확고히 하고 있습니다.

"중규모 데이터센터는 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다."

데이터 인프라의 분산화와 분산형 컴퓨팅 모델로의 전환이 진행됨에 따라, 예측 기간 동안 중규모 데이터센터는 데이터센터용 칩 시장에서 가장 높은 CAGR을 보일 것으로 예상됩니다. 조직이 대기 시간을 줄이고 데이터 처리 효율을 높이기 위해 너무 크지도 작지도 않은 지역 밀착형 및 로컬 데이터센터를 구축해야 할 필요성이 커지고 있습니다. 중간 규모의 시설은 엣지 지원 워크로드, 콘텐츠 전송, 지역 클라우드 서비스를 지원한다는 점에서 이러한 목적에 이상적입니다. 이러한 추세는 단순한 업그레이드가 아닌 인프라에 대한 신규 투자를 촉진하고, 최신 고성능 칩에 대한 수요를 증가시키고 있습니다. 또한, 통신, 의료, 스마트 인프라 등 산업별 애플리케이션에서 중형 데이터센터가 점점 더 많이 채택되고 있으며, 이는 예측 기간 동안 칩 소비량 증가로 이어져 성장을 더욱 가속화할 것으로 보입니다.

"아시아태평양은 예측 기간 동안 가장 높은 CAGR을 보일 것으로 예상됩니다."

아시아태평양은 디지털 경제의 급속한 성장, 인터넷 보급률 증가, 신흥 시장 전반의 데이터 생성량 증가로 인해 예측 기간 동안 데이터센터용 칩 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. 이 지역에서는 클라우드 서비스, AI, E-Commerce, 모바일 애플리케이션에 대한 수요 증가에 대응하기 위해 새로운 데이터센터 도입이 가속화되고 있습니다. 반도체 제조에 대한 투자 확대와 지역 내 칩 생태계 강화를 위한 정부 지원책이 수요와 공급을 모두 끌어올리고 있습니다. 아시아태평양 클라우드 제공업체들의 존재감 증가와 세계 하이퍼스케일 기업들의 아시아태평양 진출은 첨단 고성능 데이터센터용 칩에 대한 수요를 더욱 견인하고 있으며, 다른 지역에 비해 시장 성장을 가속화하고 있습니다.

2차 조사를 통해 수집된 다양한 부문 및 하위 부문의 시장 규모를 확인하고 검증하기 위해 데이터센터용 칩 솔루션을 제공하는 주요 업계 전문가를 대상으로 광범위한 1차 인터뷰를 실시했습니다. 본 보고서의 1차 인터뷰 대상자 내역은 다음과 같습니다:

본 보고서에서는 데이터센터용 칩 시장의 주요 기업들을 소개하고 시장 순위를 제시합니다. 주요 대상 기업으로는 NVIDIA Corporation(미국), Advanced Micro Devices, Inc.(미국), SAMSUNG(한국), SK HYNIX INC.(한국), Micron Technology, Inc.(미국) 등이 있습니다.

Google(미국), Amazon Web Services, Inc.(미국), Monolithic Power Systems, Inc. Microsoft(미국), Altera Corporation(미국) 등이 데이터센터용 칩 시장의 주요 업체로 꼽힙니다.

조사 범위:

본 조사 보고서는 데이터센터용 칩 시장을 카테고리, 데이터센터 규모, 용도, 지역별로 분류하고 있습니다. 본 보고서는 데이터센터용 칩 시장과 관련된 주요 시장 촉진요인, 저해요인, 도전과제, 기회요인을 개괄하고 2032년까지의 예측을 제시합니다. 또한, 이 보고서에는 데이터센터용 칩 시장 생태계 내 모든 기업의 리더십 매핑 및 분석이 포함되어 있습니다.

본 보고서 구매의 주요 이점

이 보고서는 데이터센터용 칩 시장 전체와 그 하위 부문에 대한 대략적인 수치를 제공함으로써 시장 리더와 신규 진입자들에게 도움을 줄 수 있습니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 효과적인 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한, 주요 시장 촉진요인, 제약요인, 도전 과제, 기회 등 시장 동향을 파악하는 데 도움이 될 것입니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(하이퍼스케일 데이터센터의 급속한 확장, AI 및 머신러닝 워크로드 도입 증가, 저지연 및 고처리 컴퓨팅에 대한 수요 증가, GPU 및 TPU와 같은 AI 가속기에 대한 수요 증가), 제약요인(고급 GPU 및 AI 가속기의 높은 비용 및 공급 제한, 고급 반도체 제조 역량 집중), 기회(국가 주도의 AI 인프라 이니셔티브 부상, FPGA 및 커스텀 가속기 채택 증가) 높은 비용과 공급 제한, 첨단 반도체 제조 역량 집중), 기회(국가 주도 AI 인프라 구상의 부상, 데이터센터 내 FPGA 및 커스텀 가속기 채택 확대), 도전과제(데이터센터 인프라의 높은 에너지 소비, 컴퓨팅 시스템 하드웨어 보안 취약성)가 있습니다. 하드웨어 보안 취약점, 숙련된 반도체 및 AI 엔지니어의 부족)에 대해 설명합니다.

- 제품 개발 및 혁신 : 데이터센터 칩 시장의 미래 기술, R&D 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 동향 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 데이터센터용 칩 시장을 분석합니다.

- 시장 다각화 : 데이터센터 칩 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보 제공

- 경쟁 분석 : 데이터센터용 칩 시장의 주요 기업(NVIDIA Corporation(미국), Advanced Micro Devices, Inc.(미국), SAMSUNG(한국), SK HYNIX INC.(한국), Micron Technology, Inc.(미국) 등)의 시장 점유율, 성장 전략 및 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 데이터센터용 칩 시장(구성요소별)

제10장 데이터센터용 칩 시장(데이터센터 규모별)

제11장 데이터센터용 칩 시장(용도별)

제12장 데이터센터용 칩 시장(최종사용자별)

제13장 데이터센터용 칩 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.05.19The data center chip market is projected to grow from USD 283.16 billion in 2026 to USD 687.65 billion by 2032, at a CAGR of 15.9% during this period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Component, Application, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

The market is expected to see significant growth due to increasing demand for AI, generative AI, and data-intensive workloads, which require advanced processors, memory, and specialized accelerators for faster processing and lower latency. Furthermore, the expansion of hyperscale data centers and technological advancements such as chiplet architectures and heterogeneous computing are fueling the need for scalable, energy-efficient, and high-performance chip solutions.

"Cloud service providers, as end users, held the largest market share in 2025."

Cloud service providers held the largest share in the data center chip market in 2025 due to their widespread deployment of hyperscale data centers and ongoing expansion of cloud infrastructure to support AI, storage, and computing services. These providers operate vast server networks that require high volumes of advanced chips, including CPUs, GPUs, and custom accelerators, to manage diverse and data-intensive workloads. Additionally, their strong financial resources enable frequent upgrades to next-generation semiconductor technologies and investments in custom silicon for better performance and cost efficiency. As a result, the scale, intensity, and continuous growth of cloud operations lead to significantly higher chip consumption compared to other end users, solidifying their dominant market position.

"Medium-sized data centers are projected to record the highest CAGR during the forecast period."

Medium-sized data centers are projected to have the highest CAGR in the data center chip market during the forecast period due to the growing decentralization of data infrastructure and the shift toward distributed computing models. As organizations seek to reduce latency and enhance data processing efficiency, there is an increasing need to deploy regional and localized data centers that are neither too large nor too small. Medium-sized facilities are ideal for this purpose, supporting edge-compliant workloads, content delivery, and regional cloud services. This trend is prompting new investments in infrastructure rather than just upgrades, leading to greater demand for modern, high-performance chips. Furthermore, medium-sized data centers are increasingly adopted for industry-specific applications such as telecom, healthcare, and smart infrastructure, which further accelerates their growth and results in higher chip consumption during the forecast period.

"Asia Pacific will exhibit the highest CAGR during the forecast period."

Asia Pacific is expected to experience the highest CAGR in the data center chip market during the forecast period due to the rapid growth of digital economies, increasing internet penetration, and strong data generation growth across emerging markets. The region is seeing accelerated deployment of new data centers to meet rising demand for cloud services, AI, e-commerce, and mobile applications. Growing investments in semiconductor manufacturing and supportive government initiatives aimed at strengthening local chip ecosystems are fueling both supply and demand. The increasing presence of regional cloud providers and the expansion of global hyperscale companies into Asia Pacific are further driving the need for advanced, high-performance data center chips, leading to faster market growth compared to other regions.

Extensive primary interviews were conducted with key industry experts providing data center chip solutions to identify and verify the market size for various segments and subsegments collected through secondary research. The breakdown of primary participants for the report is listed below:

The study includes insights from a range of industry experts, from component suppliers to Tier 1 companies and OEMs. The distribution of the primaries is as follows:

- By Company Type: Tier 1-40%, Tier 2-35%, and Tier 3-25%

- By Designation: C-level-40%, Directors-45%, and Others-15%

- By Region: North America-41%, Europe-26%, Asia Pacific-28%, and RoW-5%

The report highlights key players in the data center chip market and provides their market rankings. The prominent companies included are NVIDIA Corporation (US), Advanced Micro Devices, Inc. (US), SAMSUNG (South Korea), SK HYNIX INC. (South Korea), and Micron Technology, Inc. (US).

Google (US), Amazon Web Services, Inc. (US), Monolithic Power Systems, Inc. (US), Texas Instruments Incorporated (US), Analog Devices, Inc. (US), Microsoft (US), Altera Corporation (US), among others, are other companies in the data center chip market.

Research Coverage:

This research report classifies the data center chip market by category, data center size, application, and region. The report outlines the key drivers, restraints, challenges, and opportunities related to the data center chip market and provides forecasts through 2032. Additionally, the report includes leadership mapping and analysis of all companies within the data center chip market ecosystem.

Key Benefits of Buying the Report

The report will assist market leaders and new entrants by providing approximate figures for the overall data center chip market and its subsegments. This report helps stakeholders understand the competitive landscape and gain insights to better position their businesses and develop effective go-to-market strategies. It also gives stakeholders a pulse on the market, including key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (rapid expansion of hyperscale data centers, increasing deployment of AI and machine learning workloads, rising demand for low-latency and high-throughput computing, growing demand for AI accelerators such as GPUs and TPUs), restraints (high cost and limited supply of advanced GPUs and AI accelerators, concentration of advanced semiconductor manufacturing capacity), opportunities (emergence of sovereign AI infrastructure initiatives, increasing adoption of FPGA and custom accelerators in data centers), and challenges (high energy consumption of data center infrastructure, hardware security vulnerabilities in computing systems, shortage of skilled semiconductor and AI engineers) of the data center chip market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the data center chip market

- Market Development: Comprehensive information about lucrative markets-the report analyzes the data center chip market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center chip market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players, such as NVIDIA Corporation (US), Advanced Micro Devices, Inc. (US), SAMSUNG (South Korea), SK HYNIX INC. (South Korea), and Micron Technology, Inc. (US) in the data center chip market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIONS SHAPING DATA CENTER CHIP MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER CHIP MARKET

- 3.2 DATA CENTER CHIP MARKET, BY COMPONENT

- 3.3 DATA CENTER CHIP MARKET, BY DATA CENTER SIZE

- 3.4 DATA CENTER CHIP MARKET, BY END USER

- 3.5 DATA CENTER CHIP MARKET, BY APPLICATION

- 3.6 DATA CENTER CHIP MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid expansion of hyperscale data centers

- 4.2.1.2 Increasing deployment of AI and ML technologies

- 4.2.1.3 Rising need for low-latency and high-throughput computing

- 4.2.1.4 Mounting demand for AI accelerators

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost and limited supply of advanced AI accelerators

- 4.2.2.2 Concentration risks in advanced semiconductor manufacturing for data centers

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of sovereign AI infrastructure initiatives

- 4.2.3.2 Increasing adoption of FPGA and custom accelerators in data centers

- 4.2.4 CHALLENGES

- 4.2.4.1 High energy consumption in data centers

- 4.2.4.2 Computing hardware security vulnerabilities

- 4.2.4.3 Shortage of skilled semiconductor and AI engineers

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL DATA CENTER INDUSTRY

- 5.3.4 TRENDS IN GLOBAL AI CHIP INDUSTRY

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 PRICING RANGE OF AI PROCESSORS OFFERED BY KEY PLAYERS, BY TYPE, 2025

- 5.6.2 PRICING RANGE OF AI PROCESSORS, BY TYPE, 2021-2025

- 5.6.3 AVERAGE SELLING PRICE TREND OF AI PROCESSORS, BY REGION, 2021-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 854231)

- 5.7.2 EXPORT SCENARIO (HS CODE 854231)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 STMICROELECTRONICS DEPLOYS HPE SERVERS AND MICROSOFT AZURE CLOUD INSTANCES POWERED BY AMD EPYC PROCESSORS TO IMPROVE DATA CENTER PERFORMANCE

- 5.11.2 JOCDN ADOPTS AMD EPYC PROCESSORS TO IMPROVE BROADCAST VIDEO STREAMING CAPABILITIES

- 5.11.3 DBS BANK LEVERAGES AMD EPYC PROCESSOR-POWERED DELL SERVERS TO TRANSFORM DATA CENTER INFRASTRUCTURE

- 5.12 IMPACT OF 2025 US TARIFF - DATA CENTER CHIP MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT OF COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI ACCELERATORS (ASICS/GPUS/TPUS)

- 6.1.2 DATA PROCESSING UNITS (DPUS)/SMARTNICS

- 6.1.3 ADVANCED PACKAGING (2.5D/3D/CHIPLETS)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CHIP DESIGN TOOLS

- 6.2.2 DATA CENTER POWER MANAGEMENT AND COOLING SYSTEMS

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI/GEN AI ON DATA CENTER CHIP MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY COMPANIES IN DATA CENTER CHIP MARKET

- 6.5.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN DATA CENTER CHIP MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT AI/GEN AI-INTEGRATED DATA CENTER CHIPS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS

9 DATA CENTER CHIP MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 PROCESSORS

- 9.2.1 AI PROCESSORS

- 9.2.1.1 GPU

- 9.2.1.1.1 Rising AI workloads and hyperscale investments to fuel segmental growth

- 9.2.1.2 CPU

- 9.2.1.2.1 Increasing demand for AI-oriented workload management to boost segmental growth

- 9.2.1.3 FPGA

- 9.2.1.3.1 Growing need for efficient parallel processing and low-latency execution in data centers to drive market

- 9.2.1.4 ASIC

- 9.2.1.4.1 Increasing demand for workload-specific optimization to augment market growth

- 9.2.1.4.2 DOJO & FSD

- 9.2.1.4.3 Trainium & Inferentia

- 9.2.1.4.4 Athena

- 9.2.1.4.5 T-Head

- 9.2.1.4.6 MTIA

- 9.2.1.4.7 LPU

- 9.2.1.4.8 Ascend

- 9.2.1.4.9 TPU

- 9.2.1.4.10 Other ASICs

- 9.2.1.1 GPU

- 9.2.2 GENERAL-PURPOSE COMPUTING PROCESSORS

- 9.2.2.1 CPU

- 9.2.2.1.1 High processing capability through multiple cores and clock speeds to foster segmental growth

- 9.2.2.2 FPGA

- 9.2.2.2.1 Emergence as flexible and reconfigurable solution for data center workloads to expedite segmental growth

- 9.2.2.1 CPU

- 9.2.1 AI PROCESSORS

- 9.3 MEMORY

- 9.3.1 DDR

- 9.3.1.1 Increasing deployment of high-performance server memory to support data center workload expansion to drive market

- 9.3.2 HBM

- 9.3.2.1 Increasing demand for ultra-high memory bandwidth to support AI and accelerated computing workloads to spur demand

- 9.3.1 DDR

- 9.4 NETWORK INTERFACES/INTERCONNECTS

- 9.4.1 NICS/NETWORK ADAPTERS

- 9.4.1.1 InfiniBand

- 9.4.1.1.1 Ability to deliver ultra-low latency and high data throughput in data center environments to bolster segmental growth

- 9.4.1.2 Ethernet

- 9.4.1.2.1 Scalability, reliability, and cost efficiency in supporting large-scale computing infrastructure to drive market

- 9.4.1.3 Other NICs/network adapters

- 9.4.1.1 InfiniBand

- 9.4.2 INTERCONNECTS

- 9.4.2.1 Growing complexity of AI models and high-performance computing workloads to fuel segmental growth

- 9.4.1 NICS/NETWORK ADAPTERS

- 9.5 SENSORS

- 9.5.1 TEMPERATURE SENSORS

- 9.5.1.1 Ability to maintain optimal operating temperatures for servers and storage systems to foster segmental growth

- 9.5.2 HUMIDITY SENSORS

- 9.5.2.1 Need for real-time environmental data to contribute to segmental growth

- 9.5.3 AIRFLOW SENSORS

- 9.5.3.1 Focus on maintaining balanced airflow and hotspot prevention to augment segmental growth

- 9.5.4 OTHER SENSORS

- 9.5.1 TEMPERATURE SENSORS

- 9.6 POWER MANAGEMENT SOLUTIONS

- 9.6.1 MULTIPHASE CONTROLLERS

- 9.6.1.1 Focus on receiving adequate power while minimizing energy losses and heat generation to foster segmental growth

- 9.6.2 POINT-OF-LOAD (DC/DC CONVERTERS)

- 9.6.2.1 Use to provide fast response to changing load conditions and maintain stable voltage delivery to drive market

- 9.6.3 LOW DROPOUT

- 9.6.3.1 Ability to provide stable and low-noise output voltage to accelerate segmental growth

- 9.6.4 48V INTERMEDIATE BUS CONVERTERS

- 9.6.4.1 Rising deployment of power-intensive processors in data centers to expedite segmental growth

- 9.6.5 HOT SWAP CONTROLLERS/EFUSES

- 9.6.5.1 Use to minimize downtime, improve operational efficiency, and maintain system reliability to boost segmental growth

- 9.6.6 POWER SEQUENCERS

- 9.6.6.1 Need for controlled power initialization to accelerate segmental growth

- 9.6.7 BASEBOARD MANAGEMENT CONTROLLERS (BMCS)

- 9.6.7.1 Proactive maintenance and faster troubleshooting attributes to drive market

- 9.6.1 MULTIPHASE CONTROLLERS

- 9.7 ANALOG & MIXED-SIGNAL ICS

- 9.7.1 MULTICHANNEL ADCS/DACS

- 9.7.1.1 Ability to simplify system design, reduce component count, and improve overall signal processing efficiency to drive market

- 9.7.2 SWITCHES

- 9.7.2.1 Need for optimized data routing, reduced network congestion, and scalable communication support to spur demand

- 9.7.3 MUXES

- 9.7.3.1 Focus on managing signal routing between various subsystems to augment segmental growth

- 9.7.4 CURRENT SENSOR AMPLIFIERS

- 9.7.4.1 Use to accurately measure electrical parameters to contribute to segmental growth

- 9.7.5 SUPERVISORY ICS

- 9.7.5.1 Need to protect sensitive components from voltage fluctuations to expedite segmental growth

- 9.7.6 FAN CONTROLLERS

- 9.7.6.1 Demand for centralized or automated thermal management to boost segmental growth

- 9.7.7 CLOCK ICS

- 9.7.7.1 Ability to maintain reliable high-speed data transfer and prevent errors to contribute to segmental growth

- 9.7.1 MULTICHANNEL ADCS/DACS

10 DATA CENTER CHIP MARKET, BY DATA CENTER SIZE

- 10.1 INTRODUCTION

- 10.2 SMALL

- 10.2.1 RISING ADOPTION OF EDGE COMPUTING AND DISTRIBUTED DIGITAL SERVICES TO ACCELERATE SEGMENTAL GROWTH

- 10.3 MEDIUM

- 10.3.1 INCREASING NEED TO SUPPORT ENTERPRISE APPLICATIONS, DATA PROCESSING, AND CLOUD SERVICES TO DRIVE MARKET

- 10.4 LARGE

- 10.4.1 MOUNTING DEMAND FOR LARGE-SCALE COMPUTING INFRASTRUCTURE TO FUEL SEGMENTAL GROWTH

11 DATA CENTER CHIP MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 ARTIFICIAL INTELLIGENCE

- 11.2.1 GENERATIVE AI

- 11.2.1.1 Rule-based models

- 11.2.1.1.1 Increasing need for explainable decision-making systems to facilitate segmental growth

- 11.2.1.2 Statistical models

- 11.2.1.2.1 Growing need for data-driven prediction and pattern analysis to bolster segmental growth

- 11.2.1.3 Deep learning

- 11.2.1.3.1 Increasing computational intensity of neural networks to expedite segmental growth

- 11.2.1.4 Generative adversarial networks (GANs)

- 11.2.1.4.1 Rising emphasis on high-performance computing to support segmental growth

- 11.2.1.5 Autoencoders

- 11.2.1.5.1 Increasing need for efficient data representation and compression to drive market

- 11.2.1.6 Convolutional neural networks (CNNs)

- 11.2.1.6.1 Mounting demand for image and video processing to contribute to segmental growth

- 11.2.1.7 Transformer models

- 11.2.1.7.1 Rising adoption of large language models to accelerate segmental growth

- 11.2.1.1 Rule-based models

- 11.2.2 MACHINE LEARNING

- 11.2.2.1 Increasing deployment of predictive analytics and intelligent automation to boost segmental growth

- 11.2.3 NATURAL LANGUAGE PROCESSING

- 11.2.3.1 Burgeoning demand for real-time language understanding to fuel segmental growth

- 11.2.4 COMPUTER VISION

- 11.2.4.1 Increasing requirement for visual data analytics to foster segmental growth

- 11.2.1 GENERATIVE AI

- 11.3 GENERAL-PURPOSE COMPUTING

- 11.3.1 RISING ENTERPRISE WORKLOADS AND DIGITAL TRANSFORMATION TO EXPEDITE SEGMENTAL GROWTH

12 DATA CENTER CHIP MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 CLOUD SERVICE PROVIDERS

- 12.2.1 INCREASING AI-DRIVEN CLOUD WORKLOADS TO ACCELERATE SEGMENTAL GROWTH

- 12.3 ENTERPRISES

- 12.3.1 HEALTHCARE

- 12.3.1.1 Increasing adoption of AI-driven healthcare applications to bolster segmental growth

- 12.3.2 BFSI

- 12.3.2.1 Strong focus on real-time fraud detection and risk management to facilitate segmental growth

- 12.3.3 AUTOMOTIVE

- 12.3.3.1 Rising integration of AI in autonomous and connected vehicles to augment segmental growth

- 12.3.4 RETAIL & E-COMMERCE

- 12.3.4.1 Expanding digital commerce ecosystems and real-time transaction to fuel segmental growth

- 12.3.5 MEDIA & ENTERTAINMENT

- 12.3.5.1 Real-time analysis of viewer preferences and demographic information to augment segmental growth

- 12.3.6 OTHER ENTERPRISES

- 12.3.1 HEALTHCARE

- 12.4 GOVERNMENT ORGANIZATIONS

- 12.4.1 INCREASING ADOPTION OF DATA-DRIVEN GOVERNANCE AND DIGITAL PUBLIC SERVICES TO ACCELERATE SEGMENTAL GROWTH

13 DATA CENTER CHIP MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Accelerated AI chip innovation and hyperscale investments to drive market

- 13.2.2 CANADA

- 13.2.2.1 AI workload expansion and sustainable infrastructure to bolster market growth

- 13.2.3 MEXICO

- 13.2.3.1 Expansion of digital infrastructure and edge data centers to augment market growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Increasing AI adoption and hyperscale data center expansion to drive market

- 13.3.2 UK

- 13.3.2.1 Growing cloud adoption and AI workloads to support market expansion

- 13.3.3 FRANCE

- 13.3.3.1 Strong government support and AI data center expansion to fuel market growth

- 13.3.4 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Large-scale data infrastructure expansion and AI adoption to drive market

- 13.4.2 JAPAN

- 13.4.2.1 Increasing demand for high-reliability computing and advanced connectivity to expedite market growth

- 13.4.3 INDIA

- 13.4.3.1 Government-led digital infrastructure expansion and AI adoption to boost market growth

- 13.4.4 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 ROW

- 13.5.1 MIDDLE EAST & AFRICA

- 13.5.1.1 Rising demand for high-performance computing and data processing to drive market

- 13.5.1.2 GCC countries

- 13.5.1.3 Rest of Middle East & Africa

- 13.5.2 SOUTH AMERICA

- 13.5.2.1 Rising digital workloads and cloud adoption to accelerate market growth

- 13.5.1 MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND/PRODUCT COMPARISON

- 14.6.1 NVIDIA CORPORATION

- 14.6.2 ADVANCED MICRO DEVICES, INC.

- 14.6.3 INTEL CORPORATION

- 14.6.4 SAMSUNG

- 14.6.5 SK HYNIX INC.

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Component footprint

- 14.7.5.4 Application footprint

- 14.7.5.5 Data center size footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 NVIDIA CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 ADVANCED MICRO DEVICES, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 SAMSUNG

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses/Competitive threats

- 15.1.4 SK HYNIX INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 MICRON TECHNOLOGY, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 INTEL CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches

- 15.1.6.3.2 Deals

- 15.1.7 GOOGLE

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.8 AMAZON WEB SERVICES, INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.9 MONOLITHIC POWER SYSTEMS, INC

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 TEXAS INSTRUMENTS INCORPORATED

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Other developments

- 15.1.11 ANALOG DEVICES, INC.

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Expansions

- 15.1.12 MICROSOFT

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.12.3.2 Deals

- 15.1.1 NVIDIA CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 IMAGINATION TECHNOLOGIES

- 15.2.2 GRAPHCORE

- 15.2.3 CEREBRAS

- 15.2.4 TESLA

- 15.2.5 STMICROELECTRONICS

- 15.2.6 SENSIRION AG

- 15.2.7 AKCP

- 15.2.8 BOSCH SENSORTEC GMBH

- 15.2.9 RENESAS ELECTRONICS CORPORATION

- 15.2.10 INFINEON TECHNOLOGIES AG

- 15.2.11 DIODES INCORPORATED

- 15.2.12 MICROCHIP TECHNOLOGY INC.

- 15.2.13 HUAWEI TECHNOLOGIES CO., LTD.

- 15.2.14 T-HEAD

- 15.2.15 TENSTORRENT

- 15.2.16 TAALAS

- 15.2.17 REBELLIONS INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 SECONDARY AND PRIMARY RESEARCH

- 16.2.1 SECONDARY DATA

- 16.2.1.1 Key data from secondary sources

- 16.2.1.2 List of key secondary sources

- 16.2.2 PRIMARY DATA

- 16.2.2.1 Key data from primary sources

- 16.2.2.2 List of primary interview participants

- 16.2.2.3 Breakdown of primaries

- 16.2.2.4 Key industry insights

- 16.2.1 SECONDARY DATA

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.3.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS

- 16.9 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS