|

시장보고서

상품코드

2027001

클라우드 전문 서비스 시장 : 클라우드 환경별, 서비스 유형별, 서비스 모델별, 조직 규모별, 업계별, 지역별 - 세계 예측(-2031년)Cloud Professional Services Market by Cloud Environment, Service Type, Service Model - Forecast to 2031 |

||||||

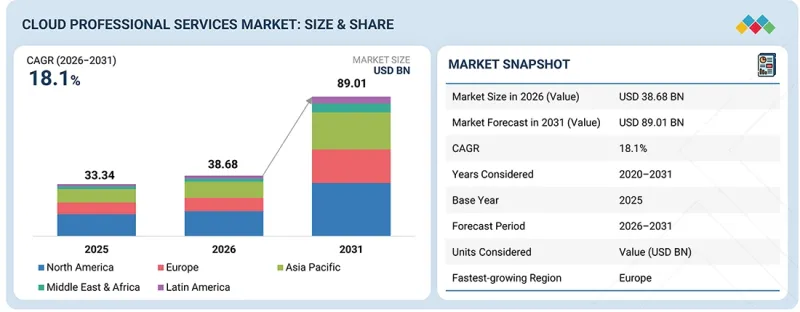

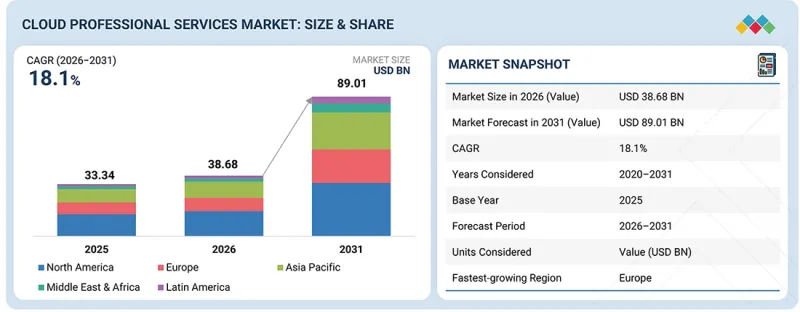

클라우드 전문 서비스 시장 규모는 빠르게 성장하고 있으며, 2025년 386억 8,000만 달러에서 2031년까지 890억 1,000만 달러로, CAGR 18.1%로 성장할 것으로 예측됩니다.

클라우드 지출이 IT 예산에서 중요한 비중을 차지함에 따라 기업들은 클라우드 비용 최적화를 점점 더 중요하게 여기고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 클라우드 환경별, 서비스 유형별, 서비스 모델별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 라틴아메리카 |

기업이 여러 플랫폼과 서비스에 걸쳐 클라우드 사용을 확대함에 따라 비용 관리, 사용량 추적, 비효율성 방지 등이 중요한 과제로 떠오르고 있습니다. 이에 따라 사용 패턴 가시화, 사업부 간 비용 배분, 리소스 사용 최적화를 실현하는 FinOps 중심의 클라우드 전문 서비스에 대한 수요가 증가하고 있습니다.

전문 서비스 제공업체는 비용 모니터링 도구 도입, 재무 거버넌스 프레임워크 구축, 클라우드 사용과 비즈니스 목표의 조정을 통해 조직을 지원합니다. 이러한 서비스는 저활용 리소스 식별, 가격 모델 최적화, 예산 책정 정확도 향상에 도움이 됩니다. 또한, 종량제 요금제로의 전환은 지속적인 모니터링과 최적화가 필요하며, 이는 수요를 더욱 촉진하고 있습니다. 기업이 성능과 비용 효율성의 균형을 맞추기 위해 노력하는 가운데, FinOps 기능은 클라우드 전략의 필수 요소로 자리 잡고 있으며, 클라우드 전문 서비스의 성장에 기여하고 있습니다.

"서비스 유형별로는 AI 및 생성형 AI 도입 지원 서비스가 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

조직이 AI 기반 사용 사례를 실험 단계에서 대규모 도입으로 전환함에 따라, 클라우드 전문 서비스 시장에서 AI 및 생성형 AI 도입 지원 서비스가 가장 빠르게 성장할 것으로 예상됩니다. 기업들은 고객 지원, 콘텐츠 생성, 소프트웨어 개발, 의사결정 인텔리전스 등의 기능에 생성형 AI를 통합하고 있으며, 이러한 움직임에는 강력한 클라우드 기반 인프라와 전문적인 도입 노하우가 필요합니다. 이러한 성장은 AI 지원 아키텍처 설계, 대규모 데이터 파이프라인 관리, 클라우드 환경 내 모델 도입, 모니터링 및 거버넌스 보장에 대한 필요성에 의해 주도되고 있습니다. 또한, 조직은 AI 도입을 보안, 컴플라이언스, 윤리적 프레임워크와 일치시키는 데 도움이 필요합니다. AI 모델을 기존 엔터프라이즈 시스템에 통합하는 복잡성은 전문 서비스에 대한 의존도를 더욱 높이고 있습니다. 그 결과, AI 전략, 모델 통합, 플랫폼 엔지니어링, 라이프사이클 관리에 이르는 기능에 대한 수요가 업계 전반에서 가속화되고 있습니다.

"서비스 모델별로 보면 예측 기간 동안 SaaS 부문이 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

SaaS(Software-as-a-Service)는 기업들이 업무 효율성을 높이고 온프레미스 소프트웨어에 대한 의존도를 낮추기 위해 즉시 사용 가능한 클라우드 기반 애플리케이션을 점점 더 많이 채택함에 따라 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 기업들은 CRM, ERP, HR, 협업 등 핵심 기능에서 SaaS 솔루션을 활용하고 있으며, 이를 통해 보다 빠른 도입, 초기 비용 절감 및 유지보수 간소화를 실현하고 있습니다. 이러한 광범위한 도입으로 인해 기존 IT 환경 내에서 SaaS 플랫폼의 도입, 커스터마이징, 통합 및 지속적인 최적화와 관련된 전문 서비스에 대한 수요가 증가하고 있습니다. 조직은 SaaS 애플리케이션을 비즈니스 프로세스에 맞게 조정하고, 데이터 마이그레이션을 보장하며, 다른 클라우드 시스템 및 레거시 시스템과의 상호 운용성을 확보하기 위해 지원을 필요로 하는 경우가 많습니다. 또한, 확장성, 원격 액세스, 구독형 모델에 대한 관심이 높아지면서 SaaS 도입을 더욱 촉진하고 있으며, 이는 전체 클라우드 전문 서비스 시장의 시장 가치에 대한 주요 기여 요인으로 작용하고 있습니다.

"예측 기간 동안 북미가 클라우드 전문 서비스 시장을 주도할 것으로 예상합니다."

북미는 기업 및 공공 부문 조직에서 클라우드 기술을 조기에 대규모로 도입하여 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이 지역에는 레거시 시스템 현대화, 업무 효율성 향상, 데이터 기반 비즈니스 모델 지원을 위해 클라우드 혁신에 적극적으로 투자하고 있는 디지털 성숙도가 높은 기업들의 탄탄한 기반이 있습니다. 하이브리드 및 멀티 클라우드 전략이 확산되고 있는 것도 컨설팅, 마이그레이션, 매니지드 서비스에 대한 수요를 더욱 촉진하고 있습니다.

첨단 IT 인프라, 주요 클라우드 플랫폼, 성숙한 파트너 생태계가 지속적인 혁신과 대규모 도입을 뒷받침하고 있습니다. 또한 AI, 애널리틱스, 클라우드 네이티브 애플리케이션 개발에 대한 투자 확대로 전문 서비스 범위도 넓어지고 있습니다. 규제 요건, 사이버 보안에 대한 우려, 그리고 업계 전반에서 진행 중인 현대화 이니셔티브도 수요 지속에 기여하고 있으며, 북미를 지역 시장의 선두주자로 자리매김하게 하고 있습니다.

이 보고서에는 클라우드 전문 서비스 시장에서 활동하는 주요 기업들에 대한 상세한 조사가 포함되어 있습니다. 이번 조사에 포함된 주요 시장 진입 기업으로는 Accenture(아일랜드), Deloitte(영국), PWC(영국), IBM(미국), EY(영국), TCS(인도), Wipro(인도), Capgemini(프랑스), HCL Tech(인도), NTT Data(일본), ATOS SE(프랑스), T-Systems(독일), Infosys(인도), Cognizant(미국), HPE(미국), Fujitsu(일본), Rackspace Technology(미국), OVHcloud(프랑스), Mphasis(인도), SoftwareOne(스위스), LTIMindtree(인도), KPMG(런던), Google(미국), AWS(미국), Hitachi Digital Services(일본), Dell(미국), CloudThat Technologies Private Limited(인도), Mission Cloud Services Inc.(미국), Cloudar(벨기에), Cloud Temple(프랑스), StackOverdrive.io LLC(미국), Lambert Labs(영국), Emergent Software(미국) 등이 있습니다.

조사 범위

클라우드 전문 서비스 시장을 클라우드 환경(표준 클라우드 환경, 국가/규제 클라우드 환경), 서비스 유형(클라우드 자문 및 전환 서비스, 클라우드 기반 및 아키텍처 서비스, 클라우드 마이그레이션 서비스, 애플리케이션 현대화 서비스, 클라우드 데이터 및 분석 서비스, AI 및 GenAI 활성화 서비스, 기타), 서비스 모델(IaaS, PaaS, SaaS), 조직 규모(대기업, 중소기업), 산업분야(IT 및 ITeS, BFSI, 유통, 소비재, 헬스케어, 금융, 소비재, 소매) 소비재, 헬스케어/생명과학, 미디어/엔터테인먼트, 제조, 통신, 에너지/공공, 정부/공공부문, 기타 업종), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)을 기준으로 분류하고 있습니다.

이 보고서의 범위에는 클라우드 전문 서비스 시장의 성장에 영향을 미치는 주요 요인에 대한 자세한 정보가 포함되어 있으며, 여기에는 클라우드 전문 서비스 시장의 성장에 영향을 미치는 촉진요인, 제약요인, 과제, 기회 등이 포함되어 있습니다. 주요 서비스 제공업체에 대한 사업 전략, 서비스 포트폴리오, 클라우드 기능 및 기술 제공에 대한 종합적인 분석을 제공합니다. 또한 이 보고서는 파트너십, 제휴, 서비스 혁신, 인수합병, 클라우드 전문 서비스 생태계 전반의 최근 동향을 포함한 전략적 노력에 대해서도 살펴봅니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 클라우드 전문 서비스 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 인사이트를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 자사 서비스를 보다 유리한 위치에 놓아 효과적인 시장 진입 전략을 수립할 수 있는 실용적인 인사이트를 얻을 수 있습니다. 또한, 이 보고서는 클라우드 전문 서비스 시장을 형성하는 주요 촉진요인, 저해요인, 과제 및 기회에 대한 자세한 정보를 제공하여 이해관계자들이 시장 동향과 역학을 평가하는 데 도움이 될 것입니다.

본 보고서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 이 보고서는 클라우드 전문 서비스 시장을 형성하는 주요 촉진요인, 제약요인, 기회 및 과제에 대한 인사이트를 제공합니다. 주요 촉진요인으로는 클라우드 전문 서비스 도입을 가속화하는 AI 기반 수요, 클라우드 서비스 사용을 촉진하는 기업 현대화 미해결 과제, 디지털 전환 및 현대화 프로그램 등이 있습니다. 제약요인으로는 멀티 클라우드의 상호운용성 및 거버넌스 문제, 레거시 시스템 통합의 복잡성, 조직 변화에 대한 저항 등이 있습니다. 기회 요인으로는 소버린 클라우드에 대한 수요, 고부가가치 전문 서비스 범위 확대, 장기적인 클라우드 서비스 수익 기회를 창출하는 AI 기반 현대화 등을 꼽을 수 있습니다. 주요 이슈로는 클라우드 서비스 제공 효율성에 영향을 미치는 레거시 시스템의 복잡성, 클라우드 서비스 실행을 방해하는 보안 및 비용 가시성 격차 등을 들 수 있습니다.

- 서비스 개발 및 혁신 : 클라우드 전문 서비스 시장의 미래 기술, R&D 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트 제공

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 클라우드 전문 서비스 시장을 분석합니다.

- 시장 다각화 : 클라우드 전문 서비스 시장의 새로운 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁사 분석 : Accenture(아일랜드), Deloitte(영국), PWC(영국), IBM(미국), EY(영국), TCS(인도), Wipro(인도), Capgemini(프랑스), HCL Tech(인도), NTT Data(일본)의 시장 점유율, 성장 전략, 클라우드 서비스 제공에 대한 상세한 평가. 성장 전략 및 클라우드 서비스 제공 내용에 대한 상세한 평가. 또한, 이 보고서는 주요 촉진요인, 제약요인, 도전과제 및 기회에 대한 정보를 제공함으로써 이해관계자들이 클라우드 전문 서비스 시장을 이해하는 데 도움이 될 것입니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제8장 규제 상황

제9장 클라우드 전문 서비스 시장(클라우드 환경별)

제10장 클라우드 전문 서비스 시장(서비스 유형별)

제11장 클라우드 전문 서비스 시장(서비스 모델별)

제12장 클라우드 전문 서비스 시장(조직 규모별)

제13장 클라우드 전문 서비스 시장(업계별)

제14장 클라우드 전문 서비스 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.05.20The cloud professional services market is expanding rapidly, with the market projected to grow from USD 38.68 billion in 2025 to USD 89.01 billion by 2031, at a CAGR of 18.1%. Organizations are increasingly prioritizing cloud cost optimization as cloud spending becomes a significant component of IT budgets.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Cloud Environment, Service Type, Organization Size, Vertical and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, Latin America |

As enterprises scale their cloud usage across multiple platforms and services, managing costs, tracking usage, and avoiding inefficiencies have become critical challenges. This has led to growing demand for FinOps-driven cloud professional services that provide visibility into consumption patterns, enable cost allocation across business units, and optimize resource utilization.

Professional service providers support organizations by implementing cost monitoring tools, establishing financial governance frameworks, and aligning cloud usage with business objectives. These services help identify underutilized resources, optimize pricing models, and improve budgeting accuracy. Additionally, the shift toward consumption-based pricing models requires continuous monitoring and optimization, further driving demand. As enterprises aim to balance performance with cost efficiency, FinOps capabilities are becoming an essential component of cloud strategy, contributing to the growth of cloud professional services.

"By service type, AI & GenAI enablement services are expected to register the highest growth during the forecast period."

AI and generative AI enablement services are expected to witness the fastest growth in the cloud professional services market as organizations increasingly move from experimentation to scaled deployment of AI-driven use cases. Enterprises are integrating generative AI into functions such as customer support, content generation, software development, and decision intelligence, a move that requires robust cloud-based infrastructure and specialized implementation expertise. This growth is driven by the need to design AI-ready architectures, manage large-scale data pipelines, and ensure model deployment, monitoring, and governance within cloud environments. Additionally, organizations require support in aligning AI adoption with security, compliance, and ethical frameworks. The complexity of integrating AI models with existing enterprise systems further increases reliance on professional services. As a result, demand for capabilities spanning AI strategy, model integration, platform engineering, and lifecycle management is accelerating across industries.

"By service model, the SaaS segment is expected to account for the largest market share during the forecast period."

Software-as-a-Service (SaaS) is expected to account for the largest market share as organizations increasingly adopt ready-to-use, cloud-based applications to streamline business operations and reduce reliance on on-premises software. Enterprises are leveraging SaaS solutions for critical functions such as CRM, ERP, HR, and collaboration, enabling faster deployment, lower upfront costs, and simplified maintenance. This widespread adoption drives demand for professional services related to implementation, customization, integration, and ongoing optimization of SaaS platforms within existing IT environments. Organizations often require support to align SaaS applications with business processes, ensure data migration, and enable interoperability with other cloud and legacy systems. Additionally, the growing focus on scalability, remote accessibility, and subscription-based models further strengthens SaaS adoption, making it a key contributor to overall market value in the cloud professional services landscape.

"North America leads the cloud professional services market during the forecast period."

North America is expected to account for the largest market share due to early, large-scale adoption of cloud technologies across enterprises and public-sector organizations. The region has a strong base of digitally mature enterprises that are actively investing in cloud transformation to modernize legacy systems, enhance operational efficiency, and support data-driven business models. High adoption of hybrid and multi-cloud strategies further drives demand for consulting, migration, and managed services.

The presence of advanced IT infrastructure, leading cloud platforms, and a mature partner ecosystem supports continuous innovation and large-scale deployments. Additionally, increasing investments in AI, analytics, and cloud-native application development are expanding the scope of professional services. Regulatory requirements, cybersecurity concerns, and ongoing modernization initiatives across industries also contribute to sustained demand, positioning North America as the leading regional market.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the cloud professional services market.

- By Company: Tier I - 35%, Tier II - 45%, and Tier III - 20%

- By Designation: Directors - 35%, Managers -25%, and Others - 40%

- By Region: North America - 25%, Europe - 45%, Asia Pacific - 25%, Middle East & Africa - 3%, and Latin America - 2%.

The report includes a detailed study of key players operating in the cloud professional services market. The major market participants covered in the study include Accenture (Ireland), Deloitte (UK), PWC (UK), IBM (US), EY (UK), TCS (India), Wipro (India), Capgemini (France), HCL Tech (India), NTT Data (Japan), ATOS SE (France), T-Systems (Germany), Infosys (India), Cognizant (US), HPE (US), Fujitsu (Japan), Rackspace Technology (US), OVHcloud (France), Mphasis (India), SoftwareOne (Switzerland), LTIMindtree (India), KPMG (London), Google (US), AWS (US), Hitachi Digital Services (Japan), Dell (US), CloudThat Technologies Private Limited (India), Mission Cloud Services Inc. (US), Cloudar (Belgium), Cloud Temple (France), StackOverdrive.io LLC (US), Lambert Labs (UK), and Emergent Software (US).

Research Coverage

This research report categorizes the cloud professional services market based on cloud environment (standard cloud environments, sovereign/regulated cloud environment), service type (cloud advisory & transformation services, cloud foundation & architecture services, cloud migration services, application modernization services, cloud data & analytics services, AI & GenAI enablement services, others), services model (IaaS, Paas, SaaS), organization size (large enterprises, SMEs), vertical (IT & ITeS, BFSI, retail & consumer goods, healthcare & life sciences, media & entertainment, manufacturing, telecommunications, energy & utilities, government & public sector, other verticals ), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope includes detailed information on the key factors influencing the cloud professional services market, including drivers, restraints, challenges, and opportunities that shape its growth. It provides a comprehensive analysis of leading service providers, covering their business strategies, service portfolios, cloud capabilities, and technology offerings. The report also examines strategic initiatives, including partnerships, collaborations, service innovations, mergers and acquisitions, and recent developments across the cloud professional services ecosystem.

Reason to Buy this Report

The report provides market leaders and new entrants with insights into the closest estimates of revenue for the overall cloud professional services market and its subsegments. It enables stakeholders to understand the competitive landscape and gain actionable insights to better position their offerings and develop effective go-to-market strategies. Additionally, the report helps stakeholders assess market trends and dynamics by providing detailed information on key drivers, restraints, challenges, and opportunities shaping the cloud professional services market.

The report provides insights into the following points:

- The report provides insights into key drivers, restraints, opportunities, and challenges shaping the cloud professional services market. Major drivers include AI-led demand accelerating cloud professional services adoption, enterprise modernization backlog driving cloud services engagement, digital transformation, and modernization programs. Restraints include multi-cloud interoperability and governance challenges, the complexity of legacy system integration, and resistance to organizational change. Opportunities include sovereign cloud demand, an expanding scope of high-value professional services, and AI-driven modernization, creating long-term cloud services revenue opportunities. Key challenges include legacy system complexity that impacts cloud service delivery efficiency, and security and cost visibility gaps that hinder cloud service execution.

- Services Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the cloud professional services market

- Market Development: Comprehensive information about lucrative markets - the report analyses the cloud professional services market across varied regions

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the cloud professional services market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and cloud services offerings of leading players such as Accenture (Ireland), Deloitte (UK), PWC (UK), IBM (US), EY (UK), TCS (India), Wipro (India), Capgemini (France), HCL Tech (India), and NTT Data (Japan). The report also helps stakeholders understand the cloud professional services market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN CLOUD PROFESSIONAL SERVICES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CLOUD PROFESSIONAL SERVICES MARKET

- 3.2 CLOUD PROFESSIONAL SERVICES MARKET, BY CLOUD ENVIRONMENT

- 3.3 CLOUD PROFESSIONAL SERVICES MARKET, BY SERVICE MODEL

- 3.4 CLOUD PROFESSIONAL SERVICES MARKET, BY VERTICAL

- 3.5 CLOUD PROFESSIONAL SERVICES MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 AI-based production accelerating demand for AI, data, and cloud architecture services

- 4.2.1.2 Enterprise shift from legacy to hybrid-cloud architectures driving recurring modernization services demand

- 4.2.1.3 Rising cyber risks and resilience requirements increasing demand for secure cloud architecture and remediation services

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited visibility of measurable cloud value slowing enterprise spending on transformation services

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising sovereign cloud demand creating high-value global professional services opportunity

- 4.2.3.2 Marketplace-led service offerings enabling scalable and repeatable consulting models

- 4.2.3.3 Cloud-native application development driving demand for re-platforming and advisory services

- 4.2.4 CHALLENGES

- 4.2.4.1 Multi-team ownership and governance layers slowing cloud project delivery and increasing effort

- 4.2.4.2 Complexity in integrating multi-vendor ecosystems across hybrid and sovereign environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CLOUD PROFESSIONAL SERVICES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Cloud Professional Service Business Models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECASTS

- 5.2.3 TRENDS IN GLOBAL CLOUD COMPUTING INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DIGITAL TRANSFORMATION INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 IBM CONSULTING ENABLED WATER CORPORATION TO MODERNIZE SAP ARCHITECTURE ON AWS CLOUD

- 5.7.2 GOOGLE CLOUD ENABLED MILLENNIUM BCP TO DRIVE DATA-DRIVEN DIGITAL BANKING TRANSFORMATION

- 5.7.3 DELOITTE ENABLED SANA TO BUILD SOVEREIGN CLOUD PLATFORM WITH STACKIT FOR HEALTHCARE TRANSFORMATION

- 5.8 IMPACT OF 2025 US TARIFF - CLOUD PROFESSIONAL SERVICES MARKET

- 5.8.1 INTRODUCTION

- 5.8.2 KEY TARIFF RATES

- 5.8.3 PRICE IMPACT ANALYSIS

- 5.8.4 IMPACT ON COUNTRY/REGION

- 5.8.4.1 US

- 5.8.4.2 Europe

- 5.8.4.3 Asia Pacific

- 5.8.5 IMPACT ON VERTICALS

- 5.8.5.1 IT & ITeS

- 5.8.5.2 BFSI

- 5.8.5.3 Retail & Consumer Goods

- 5.8.5.4 Healthcare & Life Sciences

- 5.8.5.5 Media & Entertainment

- 5.8.5.6 Manufacturing

- 5.8.5.7 Telecommunications

- 5.8.5.8 Energy & Utilities

- 5.8.5.9 Government & Public Sector

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 6.5 MARKET PROFITABILITY

- 6.5.1 REVENUE POTENTIAL

- 6.5.2 COST DYNAMICS

- 6.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 7.1 TECHNOLOGY ANALYSIS

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.1.1.1 Infrastructure as Code (IaC)

- 7.1.1.2 Kubernetes-based Container Orchestration

- 7.1.1.3 Cloud Automation & Orchestration Platforms

- 7.1.2 COMPLEMENTARY TECHNOLOGIES

- 7.1.2.1 Cloud Observability Platforms

- 7.1.2.2 Cloud Security Posture Management (CSPM)

- 7.1.2.3 API Management Platforms

- 7.1.3 ADJACENT TECHNOLOGIES

- 7.1.3.1 Edge Computing Platforms

- 7.1.3.2 Serverless Computing (Function-as-a-Service)

- 7.1.3.3 Digital Twin Technology

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.2 TECHNOLOGY/PRODUCT ROADMAP

- 7.2.1 SHORT-TERM (2026-2028) | AUTOMATION-FIRST & CLOUD STANDARDIZATION

- 7.2.1.1 Focus Areas:

- 7.2.1.1.1 Technology Development

- 7.2.1.1.2 Product/Service Innovations

- 7.2.1.1.3 Market Adoption

- 7.2.1.1 Focus Areas:

- 7.2.2 MID-TERM (2028-2031) | PLATFORM ENGINEERING & SOVEREIGN MULTI-CLOUD ECOSYSTEMS

- 7.2.2.1 Focus Areas

- 7.2.2.1.1 Technology Development

- 7.2.2.1.2 Product/Service Innovations

- 7.2.2.1.3 Market Adoption

- 7.2.2.1 Focus Areas

- 7.2.3 LONG-TERM (2031-2035+) | AUTONOMOUS CLOUD OPERATIONS & POLICY-DRIVEN CLOUD ECOSYSTEMS

- 7.2.3.1 Focus Areas

- 7.2.3.1.1 Technology Development

- 7.2.3.1.2 Product/Service Innovations

- 7.2.3.1.3 Market Adoption

- 7.2.3.1 Focus Areas

- 7.2.1 SHORT-TERM (2026-2028) | AUTOMATION-FIRST & CLOUD STANDARDIZATION

- 7.3 PATENT ANALYSIS

- 7.4 FUTURE APPLICATIONS

- 7.4.1 INDUSTRY-SPECIFIC CLOUD MODERNIZATION (VERTICALIZED CLOUD TRANSFORMATION)

- 7.4.2 MULTI-CLOUD PLATFORM ENGINEERING AND CLOUD-NATIVE APPLICATION SERVICES

- 7.4.3 CLOUD SECURITY, SOVEREIGNTY, AND ZERO TRUST ARCHITECTURE SERVICES

- 7.4.4 CLOUD-BASED DATA FABRIC AND AI-READY DATA MODERNIZATION SERVICES

- 7.5 IMPACT OF AI/GENERATIVE AI ON CLOUD PROFESSIONAL SERVICES MARKET

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

- 7.5.2 BEST PRACTICES IN CLOUD PROFESSIONAL SERVICES

- 7.5.3 CASE STUDY OF AI IMPLEMENTATION IN CLOUD PROFESSIONAL SERVICES MARKET

- 7.5.3.1 Enabling Secure Hybrid and Multi-cloud Transformation for Financial Services Through AI-driven Cloud Innovation Frameworks

- 7.5.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 7.5.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN CLOUD PROFESSIONAL SERVICES MARKET

- 7.5.6 ACCENTURE: AI REFINERY PLATFORM

- 7.5.7 IBM: WATSONX

8 REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS, BY REGION

- 8.1.2.1 North America

- 8.1.2.2 Europe

- 8.1.2.3 Asia Pacific

- 8.1.2.4 Middle East & Africa

- 8.1.2.5 Latin America

9 CLOUD PROFESSIONAL SERVICES MARKET, BY CLOUD ENVIRONMENT

- 9.1 INTRODUCTION

- 9.1.1 CLOUD ENVIRONMENT: CLOUD PROFESSIONAL SERVICES MARKET DRIVERS

- 9.2 STANDARD CLOUD ENVIRONMENTS

- 9.2.1 SHIFT TOWARD AI-DRIVEN CLOUD OPTIMIZATION AND PLATFORM ENGINEERING ACCELERATES DEMAND BEYOND MIGRATION-LED SERVICES

- 9.3 SOVEREIGN CLOUD ENVIRONMENTS

- 9.3.1 RISING DATA SOVEREIGNTY MANDATES DRIVE COMPLEX, COMPLIANCE-LED CLOUD TRANSFORMATIONS AND LONG-TERM PROFESSIONAL SERVICES DEMAND

10 CLOUD PROFESSIONAL SERVICES MARKET, BY SERVICE TYPE

- 10.1 INTRODUCTION

- 10.1.1 SERVICE TYPE: CLOUD PROFESSIONAL SERVICES MARKET DRIVERS

- 10.2 AI & GENAI ENABLEMENT SERVICES

- 10.2.1 ENTERPRISE SHIFT FROM AI EXPERIMENTATION TO PRODUCTION-SCALE DEPLOYMENT DRIVING DEMAND FOR INTEGRATED AI AND CLOUD ENABLEMENT SERVICES

- 10.3 CLOUD ADVISORY & TRANSFORMATION SERVICES

- 10.3.1 SHIFT FROM STRATEGY-ONLY ADVISORY TO OUTCOME-LINKED TRANSFORMATION PROGRAMS DRIVEN BY AI, FINOPS, AND PLATFORM OPERATING MODELS

- 10.4 CLOUD DATA & ANALYTICS SERVICES

- 10.4.1 SHIFT TOWARD UNIFIED DATA PLATFORMS AND REAL-TIME ANALYTICS DRIVING DEMAND FOR ADVANCED CLOUD DATA ENGINEERING AND TRANSFORMATION SERVICES

- 10.5 CLOUD FOUNDATION & ARCHITECTURE SERVICES

- 10.5.1 RISING MULTI-CLOUD COMPLEXITY AND AI INFRASTRUCTURE NEEDS DRIVE DEMAND FOR ADVANCED ARCHITECTURE AND PLATFORM ENGINEERING SERVICES

- 10.6 APPLICATION MODERNIZATION SERVICES

- 10.6.1 ENTERPRISE SHIFT TO CLOUD-NATIVE ARCHITECTURES IS ACCELERATING DEMAND FOR LARGE-SCALE, ENGINEERING-INTENSIVE APPLICATION MODERNIZATION PROGRAMS

- 10.7 CLOUD MIGRATION SERVICES

- 10.7.1 SHIFT TOWARD SELECTIVE, VALUE-DRIVEN CLOUD MIGRATION AS LARGE-SCALE LIFT-AND-SHIFT PROGRAMS REACH MATURITY

- 10.8 OTHER SERVICE TYPES

- 10.8.1 INCREASING NEED FOR OPERATIONAL CONTROL AND RESILIENCE DRIVING DEMAND FOR SECURITY, OBSERVABILITY, AND GOVERNANCE-FOCUSED CLOUD SERVICES

11 CLOUD PROFESSIONAL SERVICES MARKET, BY SERVICE MODEL

- 11.1 INTRODUCTION

- 11.1.1 SERVICE MODEL: CLOUD PROFESSIONAL SERVICES MARKET DRIVERS

- 11.2 SOFTWARE-AS-A-SERVICE (SAAS)

- 11.2.1 EXPANSION OF ENTERPRISE SAAS ECOSYSTEMS AND DATA INTEGRATION NEEDS DRIVING DEMAND FOR SAAS-FOCUSED CLOUD PROFESSIONAL SERVICES

- 11.3 INFRASTRUCTURE-AS-A-SERVICE (IAAS)

- 11.3.1 AI INFRASTRUCTURE EXPANSION AND MULTI-CLOUD WORKLOAD DISTRIBUTION INCREASING RELIANCE ON IAAS-LED CLOUD SERVICE MODELS

- 11.4 PLATFORM-AS-A-SERVICE (PAAS)

- 11.4.1 ENTERPRISE SHIFT TOWARD PLATFORM ENGINEERING AND AI-DRIVEN DEVELOPMENT IS INCREASING RELIANCE ON PAAS-LED CLOUD SERVICE MODELS

- 11.5 OTHER SERVICE MODELS

12 CLOUD PROFESSIONAL SERVICES MARKET, BY ORGANIZATION SIZE

- 12.1 INTRODUCTION

- 12.1.1 ORGANIZATION SIZE: CLOUD PROFESSIONAL SERVICES MARKET DRIVERS

- 12.2 LARGE ENTERPRISES

- 12.2.1 LARGE ENTERPRISES DRIVING CLOUD PROFESSIONAL SERVICES DEMAND THROUGH COMPLEX, MULTI-CLOUD, AND AI-LED TRANSFORMATION PROGRAMS

- 12.3 SMES

- 12.3.1 SMES DRIVING CLOUD SERVICES ADOPTION THROUGH SAAS-LED MODELS AND SELECTIVE PLATFORM-BASED MODERNIZATION INITIATIVES

13 CLOUD PROFESSIONAL SERVICES MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 VERTICAL: CLOUD PROFESSIONAL SERVICES MARKET DRIVERS

- 13.2 IT & ITES

- 13.2.1 ACCELERATING PLATFORM-LED TRANSFORMATION AND AI-INTEGRATED CLOUD ENVIRONMENTS TO ENHANCE SCALABILITY, CONTROL, AND DEVELOPER PRODUCTIVITY ACROSS IT & ITES ORGANIZATIONS

- 13.3 BFSI

- 13.3.1 DIGITAL BANKING EXPANSION AND REGULATORY-DRIVEN CLOUD ADOPTION ACCELERATING DEMAND FOR CLOUD PROFESSIONAL SERVICES IN BFSI

- 13.4 HEALTHCARE & LIFE SCIENCES

- 13.4.1 DIGITAL HEALTH EXPANSION AND DATA-DRIVEN CARE MODELS ACCELERATING CLOUD PROFESSIONAL SERVICES DEMAND IN HEALTHCARE & LIFE SCIENCES

- 13.5 MANUFACTURING

- 13.5.1 INDUSTRY 4.0 ADOPTION AND CONNECTED FACTORY MODELS ACCELERATING CLOUD PROFESSIONAL SERVICES DEMAND IN MANUFACTURING

- 13.6 GOVERNMENT & PUBLIC SECTOR

- 13.6.1 NATIONAL SECURITY PRIORITIES AND SOVEREIGN CLOUD ADOPTION DRIVING CLOUD PROFESSIONAL SERVICES DEMAND IN GOVERNMENT AND PUBLIC SECTOR

- 13.7 ENERGY & UTILITIES

- 13.7.1 GEOPOLITICAL RISKS, GRID DIGITALIZATION, AND RENEWABLE INTEGRATION DRIVING DEMAND FOR SECURE AND SOVEREIGN CLOUD TRANSFORMATION IN ENERGY AND UTILITIES

- 13.8 RETAIL & CONSUMER GOODS

- 13.8.1 OMNICHANNEL EXPANSION AND DATA-DRIVEN COMMERCE MODELS ACCELERATING CLOUD PROFESSIONAL SERVICES DEMAND IN RETAIL AND CONSUMER GOODS

- 13.9 TELECOMMUNICATIONS

- 13.9.1 5G ROLLOUT AND NETWORK VIRTUALIZATION DRIVING CLOUD PROFESSIONAL SERVICES DEMAND ACROSS TELECOM OPERATORS AND DIGITAL SERVICE PROVIDERS

- 13.10 MEDIA & ENTERTAINMENT

- 13.10.1 STREAMING EXPANSION AND DIGITAL CONTENT PLATFORMS ACCELERATING CLOUD PROFESSIONAL SERVICES DEMAND IN MEDIA & ENTERTAINMENT

- 13.11 OTHER VERTICALS

14 CLOUD PROFESSIONAL SERVICES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Cloud services demand accelerating through AI adoption, regulated environments, and large-scale enterprise transformation initiatives

- 14.2.2 CANADA

- 14.2.2.1 Cloud services demand accelerating through domestic adoption, AI integration, public-sector transformation, and sovereignty-led control and infrastructure expansion

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Cloud services demand driven by public-cloud-first adoption, strong governance frameworks, and increasing focus on AI, compliance, and operational control

- 14.3.2 GERMANY

- 14.3.2.1 Sovereign cloud adoption accelerating through strict regulatory controls, public-sector modernization programs, and multi-platform cloud deployments

- 14.3.3 FRANCE

- 14.3.3.1 National sovereign cloud platforms driving high-value services demand through qualification-led migration, modernization, and compliance execution

- 14.3.4 ITALY

- 14.3.4.1 Public-sector driven cloud adoption accelerating through centralized platforms, compliance-led transformation, and controlled workload modernization programs

- 14.3.5 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Industrial AI scale-up and domestic cloud ecosystems driving high-value services demand through large-scale infrastructure and regulated digital transformation

- 14.4.2 JAPAN

- 14.4.2.1 Cloud services demand advancing through government-led standardization, enterprise AI adoption, and domestic cloud infrastructure expansion

- 14.4.3 INDIA

- 14.4.3.1 Cloud services demand accelerating through enterprise-scale transformation, AI adoption, and expanding digital infrastructure across key industries

- 14.4.4 AUSTRALIA & NEW ZEALAND

- 14.4.4.1 Cloud services demand expanding through government-led governance frameworks, AI adoption, and secure local-region infrastructure development

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC COUNTRIES

- 14.5.1.1 Saudi Arabia

- 14.5.1.1.1 AI-led national programs and hyperscale infrastructure expansion driving high-value cloud services demand across regulated and sovereign environments

- 14.5.1.2 United Arab Emirates (UAE)

- 14.5.1.2.1 AI-driven cloud adoption and sovereign public cloud models accelerating high-value services demand across advanced digital infrastructure ecosystems

- 14.5.1.3 Other GCC countries

- 14.5.1.1 Saudi Arabia

- 14.5.2 SOUTH AFRICA

- 14.5.2.1 Cloud services demand strengthening through in-country infrastructure expansion, enterprise modernization, and emerging AI-driven transformation

- 14.5.3 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC COUNTRIES

- 14.6 LATIN AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Cloud services demand accelerating due to strong in-country hyperscaler expansion, rising enterprise AI adoption, and increasing public-sector digital transformation programs

- 14.6.2 MEXICO

- 14.6.2.1 Cloud services demand accelerating due to in-country hyperscaler expansion, rising enterprise digital transformation, and increasing adoption of AI-enabled applications

- 14.6.3 REST OF LATIN AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 15.3 REVENUE ANALYSIS, 2020-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 SERVICE COMPARISON, 2026

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025 (CLOUD PROFESSIONAL SERVICES MARKET)

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Region footprint

- 15.6.5.3 Cloud environment footprint

- 15.6.5.4 Service type footprint

- 15.6.5.5 Service model footprint

- 15.6.5.6 Organization size footprint

- 15.6.5.7 Vertical footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 EVALUATION MATRIX FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- 15.7.2 PROGRESSIVE COMPANIES

- 15.7.3 RESPONSIVE COMPANIES

- 15.7.4 DYNAMIC COMPANIES

- 15.7.5 STARTING BLOCKS

- 15.7.6 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7.6.1 Detailed list of key startups/SMEs

- 15.7.6.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 15.8.1 COMPANY VALUATION OF KEY VENDORS

- 15.8.2 FINANCIAL METRICS OF KEY VENDORS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS

- 16.2.1 ACCENTURE

- 16.2.1.1 Business overview

- 16.2.1.2 Products/Solutions/Services offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Service launches and enhancements

- 16.2.1.3.2 Deals

- 16.2.1.4 MnM view

- 16.2.1.4.1 Right to win

- 16.2.1.4.2 Strategic choices

- 16.2.1.4.3 Weaknesses and competitive threats

- 16.2.2 DELOITTE

- 16.2.2.1 Business overview

- 16.2.2.2 Products/Solutions/Services offered

- 16.2.2.3 Recent developments

- 16.2.2.3.1 Service launches and enhancements

- 16.2.2.3.2 Deals

- 16.2.2.3.3 Expansions

- 16.2.2.4 MnM view

- 16.2.2.4.1 Right to win

- 16.2.2.4.2 Strategic choices

- 16.2.2.4.3 Weaknesses and competitive threats

- 16.2.3 IBM

- 16.2.3.1 Business overview

- 16.2.3.2 Products/Solutions/Services offered

- 16.2.3.3 Recent developments

- 16.2.3.3.1 Service launches and enhancements

- 16.2.3.3.2 Deals

- 16.2.3.4 MnM view

- 16.2.3.4.1 Right to win

- 16.2.3.4.2 Strategic choices

- 16.2.3.4.3 Weaknesses and competitive threats

- 16.2.4 PWC

- 16.2.4.1 Business overview

- 16.2.4.2 Products/Solutions/Services offered

- 16.2.4.3 Recent developments

- 16.2.4.3.1 Service launches and enhancements

- 16.2.4.3.2 Deals

- 16.2.4.4 MnM view

- 16.2.4.4.1 Right to win

- 16.2.4.4.2 Strategic choices

- 16.2.4.4.3 Weaknesses and competitive threats

- 16.2.5 EY

- 16.2.5.1 Business overview

- 16.2.5.2 Products/Solutions/Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Service launches & enhancements

- 16.2.5.3.2 Deals

- 16.2.5.4 MnM view

- 16.2.5.4.1 Right to win

- 16.2.5.4.2 Strategic choices

- 16.2.5.4.3 Weaknesses and competitive threats

- 16.2.6 TATA CONSULTANCY SERVICES (TCS)

- 16.2.6.1 Business overview

- 16.2.6.2 Products/Solutions/Services offered

- 16.2.6.3 Recent developments

- 16.2.6.3.1 Service launches & enhancements

- 16.2.6.3.2 Deals

- 16.2.7 WIPRO

- 16.2.7.1 Business overview

- 16.2.7.2 Products/Solutions/Services offered

- 16.2.7.3 Recent developments

- 16.2.7.3.1 Service launches and enhancements

- 16.2.7.3.2 Deals

- 16.2.8 CAPGEMINI

- 16.2.8.1 Business overview

- 16.2.8.2 Products/Solutions/Services offered

- 16.2.8.3 Recent developments

- 16.2.8.3.1 Service launches and enhancements

- 16.2.8.3.2 Deals

- 16.2.9 HCLTECH

- 16.2.9.1 Business overview

- 16.2.9.2 Products/Solutions/Services offered

- 16.2.9.3 Recent developments

- 16.2.9.3.1 Service launches & enhancements

- 16.2.9.3.2 Deals

- 16.2.10 NTT DATA

- 16.2.10.1 Business overview

- 16.2.10.2 Products/Solutions/Services offered

- 16.2.10.3 Recent developments

- 16.2.10.3.1 Service launches and enhancements

- 16.2.10.3.2 Deals

- 16.2.11 ATOS SE

- 16.2.12 T-SYSTEMS

- 16.2.13 INFOSYS

- 16.2.14 COGNIZANT

- 16.2.15 HEWLETT PACKARD ENTERPRISE (HPE)

- 16.2.16 FUJITSU

- 16.2.17 RACKSPACE TECHNOLOGY

- 16.2.18 OVHCLOUD

- 16.2.19 MPHASIS

- 16.2.20 SOFTWAREONE

- 16.2.21 LTIMINDTREE

- 16.2.22 KPMG

- 16.2.23 HITACHI DIGITAL SERVICES

- 16.2.24 DELL INC.

- 16.2.25 CLOUDTHAT TECHNOLOGIES PRIVATE LIMITED

- 16.2.26 MISSION CLOUD SERVICES INC.

- 16.2.27 CLOUDAR

- 16.2.28 CLOUD TEMPLE

- 16.2.29 STACKOVERDRIVE.IO

- 16.2.30 LAMBERT LABS

- 16.2.31 EMERGENT SOFTWARE

- 16.2.1 ACCENTURE

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Data & List of Key Secondary Sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakdown of primary interviews

- 17.1.3 MARKET SIZE ESTIMATION

- 17.1.4 DATA TRIANGULATION

- 17.1.5 FACTOR ANALYSIS

- 17.1.6 RESEARCH ASSUMPTIONS

- 17.1.1 SECONDARY DATA

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS