|

시장보고서

상품코드

2027002

의료용 접착제 시장 : 기술별, 수지 유형별, 용도별, 지역별 - 세계 예측(-2031년)Medical Adhesives Market by Technology (Water-Based, Solvent-Based, Solid & Hot Melt Based), Resin Type (Natural Resin, Synthetic & Semi-Synthetic Resin), Application (Dental, Surgery, Medical Device & Equipment), And Region - Global Forecast To 2031 |

||||||

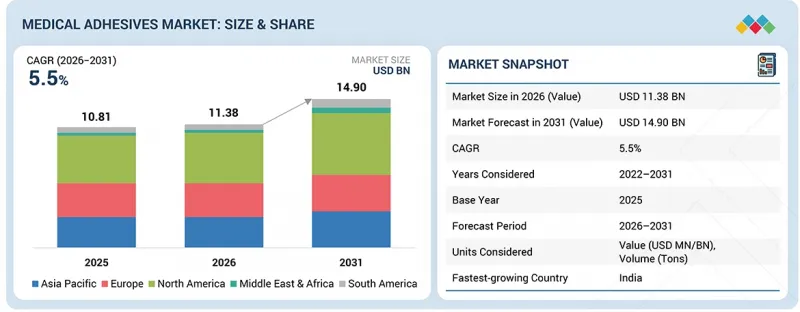

세계의 의료용 접착제 시장 규모는 2026년 113억 8,000만 달러에서 2031년까지 149억 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 5.5%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만 달러, 톤 |

| 부문 | 기술, 수지 유형, 용도, 지역 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

의료용 접착제 시장은 의료시설에서 보다 강력하고 생체적합성이 높으며 내구성이 뛰어난 접착 재료를 필요로 하면서 성장하고 있습니다. 수술 건수의 증가와 더불어 최소침습 수술의 수용이 확대되면서 병원에서 상처 봉합, 조직 봉합, 지혈을 위해 의료용 접착제를 사용하려는 움직임이 활발해지고 있습니다.

웨어러블 의료기기 및 경피 약물전달 시스템의 보급과 함께 장기간 착용이 가능한 피부 친화성이 높은 유연한 접착제에 대한 수요가 증가하고 있습니다. 고령화와 만성 상처 환자의 증가로 인해 접착 드레싱과 실란트를 포함한 첨단 상처 관리 제품에 대한 수요가 증가하고 있습니다. 의료기기 제조 산업에서는 기기 조립 및 고정에 필수적인 고성능 접착제가 요구되고 있습니다. 신흥시장에서의 의료시설의 급속한 발전은 새로운 기회를 열어주고 있습니다. 공급 측면의 지속적인 제품 개선, 실리콘 아크릴 접착제 시스템의 개발, 규제 요건 충족 및 지속가능한 재료 사용에 대한 집중 강화는 제품 성능과 시장 성장을 촉진하고 있습니다.

기술별로 의료용 접착제 시장은 수성 접착제, 솔벤트 기반 접착제, 고체 및 핫멜트 접착제의 세 가지 부문으로 분류됩니다. 수성 접착제는 우수한 생체적합성과 저독성, 휘발성 유기 화합물 배출이 최소화되어 피부 접촉 및 상처 치료 용도에 적합하여 시장을 선도하고 있습니다. 의료용 테이프, 드레싱, 웨어러블 기기에서 환자의 안전과 편안함을 보장하기 위해 이러한 접착제가 사용됩니다. 용제계 접착제의 접착 강도와 내구성은 여전히 높은 수준을 유지하고 있지만, 용제 배출을 규제하는 환경 규제로 인해 시장 성장은 계속 둔화되고 있습니다. 고체 및 핫멜트 접착제는 경화시간이 짧고 가공이 용이하며 다양한 재료에 효과적인 접착이 가능하기 때문에 의료기기 조립 및 위생 용도로 사용이 증가하고 있습니다. 규제 강화로 인해 독성 성분을 포함하지 않는 친환경 제품이 의무화되고, 의료 현장에서는 안전하고 효과적인 솔루션이 요구됨에 따라 수성 접착제 시장이 주도적인 위치를 차지하고 있습니다.

수지 유형별로 의료용 접착제 시장은 피브린계, 콜라겐계, 기타 의료용 접착제 제품의 3가지 카테고리로 구분됩니다. 피브린계 접착제는 생체적합성이 우수하고 체내 자연치유 과정에서 천연 성분으로 작용하기 때문에 가장 큰 시장 점유율을 유지하고 있습니다. 인간 또는 동물의 혈장 성분에서 추출한 피브린계 접착제는 완벽한 혈액 응고 시스템을 형성하여 외과 의사가 지혈, 조직 봉합, 상처 봉합에 이용합니다. 의료 현장에서는 심혈관 수술, 정형외과 수술, 일반 외과 수술에서 출혈을 억제하고 건강에 미치는 악영향의 위험을 줄이면서 환자의 치유 속도를 높일 수 있기 때문에 이 제품들이 사용되고 있습니다. 콜라겐계 접착제는 특히 상처 치료 및 재생의료에서 세포의 증식을 돕는 우수한 조직적합성을 제공하기 때문에 인기가 높아지고 있습니다. 강한 접착력과 제어된 분해가 요구되는 특수 용도에는 합성 접착제가 사용되며, 시아노아크릴레이트나 폴리에틸렌 글리콜(PEG) 계열의 제제가 선호되는 수지 유형입니다. 피브린 접착제는 안전한 사용과 응급 의료 현장에서의 효과적인 결과, 그리고 현대 의료에서 생체 유래 의료 솔루션에 대한 수요가 증가함에 따라 선호되는 선택이 되고 있습니다.

지역별로는 아시아태평양이 의료용 접착제 시장에서 가장 빠르게 성장하고 있습니다. 이는 중국, 인도, 동남아시아의 의료시설이 빠르게 발전하는 한편, 인구수와 의료비 지출 패턴이 지속적으로 개선되고 있기 때문입니다. 만성 질환 환자의 증가와 고령화로 인해 고급 상처 관리 솔루션 및 수술 치료에 대한 수요가 증가하고 있으며, 그 결과 의료용 접착제의 소비가 증가하고 있습니다. 이 지역에서는 낮은 비용, 지원적인 정부 규제, 그리고 해외 투자 증가로 인해 의료기기 제조가 강력한 성장세를 보이고 있습니다. 병원, 진료소, 외래 수술 센터가 사업을 계속 확장함에 따라 제품 사용량도 증가하고 있습니다. 최소침습적 수술법에 대한 지식의 향상과 최신 치료 솔루션으로 인해 우수한 접착 제품에 대한 시장의 요구가 증가하고 있습니다. 아시아태평양의 의료용 접착제 시장이 빠르게 성장하고 있는 이유는 현지 제조 자원과 해외 기업들이 이 지역에 생산기지를 설립하여 공급 유통 및 업무 효율성이 향상되고 있기 때문입니다.

세계의 의료용 접착제 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제6장 규제 상황과 지속가능성에 대한 대처

제7장 고객 상황과 구매 행동

제8장 의료용 접착제 시장 : 수지 유형별

제9장 의료용 접착제 시장 : 기술별

제10장 의료용 접착제 시장 : 용도별

제11장 의료용 접착제 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

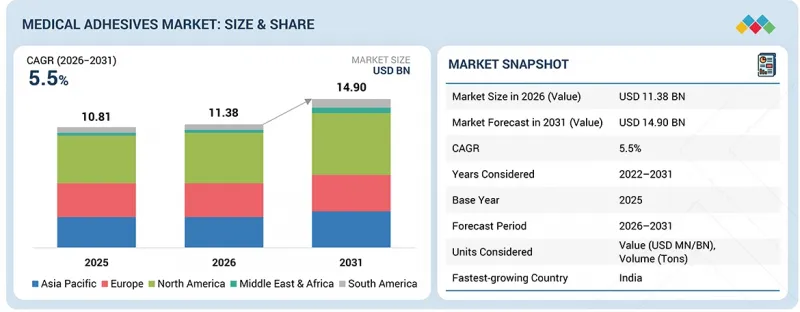

KSM 26.05.20The medical adhesives market is projected to grow from USD 11.38 billion in 2026 to USD 14.90 billion by 2031, at a CAGR of 5.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Tons) |

| Segments | By Technology, Resin Type, Application, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The medical adhesives market is growing as healthcare facilities need stronger, biocompatible, and durable bonding materials. The rising number of surgical procedures, together with the growing acceptance of minimally invasive procedures, is driving hospitals to use medical adhesives for wound closure, tissue sealing, and hemostasis.

The increasing use of wearable medical devices, together with transdermal drug delivery systems, creates a higher demand for skin-compatible flexible adhesives that can be worn for extended periods. The combination of growing elderly populations and rising chronic wound cases drives higher demand for advanced wound care products, including adhesive dressings and sealants. The medical device manufacturing industry requires high-performance adhesives, which are essential for assembling and fixing devices. The rapid development of healthcare facilities in emerging markets opens new business opportunities. Product performance and market growth receive boosts from ongoing supply-side product advances, the development of silicone and acrylic adhesive systems, and increased dedication to meeting regulatory requirements and using sustainable materials.

Based on technology, the medical adhesives market is divided into three segments: water-based adhesives, solvent-based adhesives, and solid & hot melt adhesives. Water-based adhesives lead the market because they provide excellent biocompatibility and low toxicity and produce minimal volatile organic compound emissions, making them suitable for skin-contact and wound care applications. Medical tapes, dressings, and wearable devices use these adhesives to ensure patient safety and comfort. The bonding strength and durability of solvent-based adhesives remain strong, yet their market growth continues to decline because of environmental regulations that restrict solvent emissions. Solid and hot-melt adhesives are now seeing increased use in medical device assembly and hygiene applications because they provide fast curing times, simple processing, and effective adhesion to multiple materials. The water-based adhesive market is the dominant force because rising regulations mandate environmentally friendly products without toxic components and because healthcare demands require both safe and effective solutions.

Based on resin type, the medical adhesives market is divided into three categories: fibrin, collagen, and other medical adhesive products. Fibrin-based adhesives maintain the largest market share because they provide better biocompatibility and function as natural components of the body healing process. Fibrin adhesives, which derive from human or animal plasma components, create a complete blood coagulation system that surgeons use for hemostasis, tissue sealing, and wound closure. The medical community uses these products because they help patients heal faster while controlling blood loss and reducing the risk of adverse health effects during cardiovascular, orthopedic, and general surgical operations. Collagen-based adhesives are becoming more popular because they provide excellent tissue compatibility, which helps cells grow, especially in wound care and regenerative medicine. Specialized applications that need strong bonding and controlled degradation use synthetic adhesives, which include cyanoacrylates and polyethylene glycol (PEG)-based formulations as their preferred resin types. Fibrin adhesives represent the preferred choice because they provide safe usage, effective results in emergency medical situations, and growing demand for biologically based medical solutions in contemporary healthcare.

Based on region, Asia Pacific represents the fastest expanding market for medical adhesives because healthcare facilities in China, India, and Southeast Asia experience rapid development while their population numbers and healthcare spending patterns continue to rise. The increasing number of chronic disease cases, together with the expanding elderly population, creates a greater need for advanced wound care solutions and surgical treatments, which results in higher consumption of medical adhesives. The region experiences strong growth in medical device manufacturing due to lower costs, supportive government regulations, and rising foreign investment. Product usage increases as hospitals, clinics, and ambulatory care centers continue to expand their operations. Rising knowledge of minimally invasive surgical methods, together with modern treatment solutions, creates a market need for superior adhesive products. The medical adhesives market in Asia Pacific experiences rapid growth because local manufacturing resources and foreign companies establishing production centers in the area enhance supply distribution and operational efficiency.

Major players operating in the market include Solventum (US), Henkel AG & Co. KGaA (Germany), H.B. Fuller Company (US), Scapa Healthcare (US), Johnson & Johnson (US), Permabond (UK), Chemence Medical, Inc (US), Artivion, Inc (US), Dymax (Ireland), and Bostik (France). These companies have dependable manufacturing facilities across the Asia Pacific region, as well as robust distribution networks. They have a well-established portfolio that includes reliable goods and services, a strong market presence, and effective business plans. These businesses also hold a sizable portion of the market, offer a broader range of products with more applications, and use cases spanning more geographic regions.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MEDICAL ADHESIVES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MEDICAL ADHESIVES MARKET

- 3.2 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY AND REGION

- 3.3 MEDICAL ADHESIVES MARKET, BY RESIN TYPE

- 3.4 MEDICAL ADHESIVES MARKET, BY APPLICATION

- 3.5 MEDICAL ADHESIVES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for minimally invasive surgeries

- 4.2.1.2 Growth in wearable and portable medical devices

- 4.2.1.3 Advancements in biocompatible and light-curable technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent regulatory requirement

- 4.2.2.2 Risk of skin irritation and biocompatibility issues

- 4.2.2.3 Availability of alternative wound closure methods

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth in home healthcare and remote diagnostics

- 4.2.3.2 Innovations in advanced adhesive technologies

- 4.2.3.3 Integration with smart and minimally invasive surgical solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Compatibility with new medical devices

- 4.2.4.2 Technological complexity in product development

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MEDICAL ADHESIVES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

- 4.6 PORTER'S FIVE FORCES ANALYSIS

- 4.6.1 THREAT OF NEW ENTRANTS

- 4.6.2 THREAT OF SUBSTITUTES

- 4.6.3 BARGAINING POWER OF SUPPLIERS

- 4.6.4 BARGAINING POWER OF BUYERS

- 4.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.7 VALUE CHAIN ANALYSIS

- 4.8 ECOSYSTEM

- 4.9 PRICING ANALYSIS

- 4.9.1 AVERAGE SELLING PRICE, BY REGION

- 4.9.2 AVERAGE SELLING PRICE, BY TECHNOLOGY

- 4.9.3 AVERAGE SELLING PRICE, BY APPLICATION

- 4.10 MACROECONOMIC INDICATORS

- 4.10.1 GLOBAL GDP TRENDS

- 4.11 IMPACT OF 2025 US TARIFFS ON MEDICAL ADHESIVES MARKET

- 4.11.1 INTRODUCTION

- 4.11.2 KEY TARIFF RATES

- 4.11.3 PRICE IMPACT ANALYSIS

- 4.11.4 IMPACT ON COUNTRIES/REGIONS

- 4.11.4.1 US

- 4.11.4.2 Europe

- 4.11.4.3 Asia Pacific

- 4.11.5 IMPACT ON END-USE INDUSTRIES

- 4.12 TRADE ANALYSIS

- 4.12.1 IMPORT SCENARIO (HS CODE 300590)

- 4.12.2 EXPORT SCENARIO (HS CODE 300590)

- 4.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.14 INVESTMENT AND FUNDING SCENARIO

- 4.15 CASE STUDIES

- 4.15.1 BIOCOMPATIBLE EPOXY ENCAPSULANTS IN MEDICAL DEVICE MANUFACTURING

- 4.15.2 SILICONE ADHESIVES FOR LONG-WEAR WEARABLE DEVICES

- 4.15.3 CYANOACRYLATE ADHESIVES FOR SURGICAL WOUND CLOSURE

- 4.16 KEY CONFERENCES & EVENTS

5 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 5.1 TECHNOLOGY ANALYSIS

- 5.1.1 KEY TECHNOLOGIES

- 5.1.1.1 Solids hot melt adhesives

- 5.1.1.2 UV curable adhesives

- 5.1.2 COMPLEMENTARY TECHNOLOGIES

- 5.1.2.1 Water-based (emulsion) adhesives

- 5.1.2.2 Silicone-based adhesives

- 5.1.3 ADJACENT TECHNOLOGIES

- 5.1.3.1 Medical sealants & hemostats

- 5.1.1 KEY TECHNOLOGIES

- 5.2 TECHNOLOGY/PRODUCT ROADMAP

- 5.2.1 SHORT TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 5.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 5.2.3 LONG TERM (2030-2030+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.3 PATENT ANALYSIS

- 5.3.1 LEGAL STATUS OF PATENTS

- 5.3.2 JURISDICTION ANALYSIS

- 5.4 FUTURE APPLICATIONS

- 5.4.1 WEARABLE & REMOTE MONITORING DEVICES

- 5.4.2 MINIMALLY INVASIVE & ROBOTIC SURGERIES

- 5.4.3 IMPLANTABLE MEDICAL DEVICES

- 5.4.4 ADVANCED WOUND CARE & REGENERATIVE MEDICINE

- 5.4.5 TRANSDERMAL DRUG DELIVERY SYSTEMS

- 5.5 IMPACT OF AI/GEN AI ON MEDICAL ADHESIVES MARKET

- 5.5.1 TOP USE CASES AND MARKET POTENTIAL

- 5.5.2 BEST PRACTICES IN MEDICAL ADHESIVES PROCESSING

- 5.5.3 CASE STUDIES OF AI IMPLEMENTATION IN MEDICAL ADHESIVES MARKET

- 5.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MEDICAL ADHESIVES MARKET

6 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 INDUSTRY STANDARDS

- 6.2 IMPACT OF REGULATORY POLICIES AND SUSTAINABILITY INITIATIVES

- 6.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 INTRODUCTION

- 7.2 DECISION-MAKING PROCESS

- 7.3 KEY STAKEHOLDERS AND BUYING CRITERIA

- 7.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.3.2 BUYING CRITERIA

- 7.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.5 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.6 MARKET PROFITABILITY

- 7.6.1 REVENUE POTENTIAL

- 7.6.2 COST DYNAMICS

- 7.6.3 MARGIN OPPORTUNITIES IN KEY END-USE INDUSTRIES

8 MEDICAL ADHESIVES MARKET, BY RESIN TYPE

- 8.1 INTRODUCTION

- 8.2 NATURAL RESIN

- 8.2.1 GROWING PREFERENCE FOR BIOCOMPATIBLE AND BIO-BASED SOLUTIONS DRIVING ADOPTION

- 8.2.2 FIBRIN

- 8.2.2.1 Rising surgical procedures boosting adoption of fibrin-based medical adhesives

- 8.2.3 COLLAGEN

- 8.2.3.1 Expanding advanced wound care applications driving demand

- 8.2.4 OTHER NATURAL RESINS

- 8.3 SYNTHETIC & SEMI-SYNTHETIC RESIN

- 8.3.1 RISING DEMAND FOR HIGH-PERFORMANCE AND DURABLE BONDING SOLUTIONS DRIVING MARKET GROWTH

- 8.3.2 ACRYLIC

- 8.3.2.1 Growing adoption of wearable medical devices driving demand

- 8.3.3 SILICONE

- 8.3.3.1 Increasing demand for gentle, skin-friendly adhesion driving adoption

- 8.3.4 CYANOACRYLATE

- 8.3.4.1 Rising preference for sutureless wound closure to support market growth

- 8.3.5 EPOXY

- 8.3.5.1 Demand for high-strength bonding in medical device assembly to drive growth

- 8.3.6 POLYURETHANE

- 8.3.6.1 Need for flexible and durable medical materials fueling demand

- 8.3.7 OTHER SYNTHETIC & SEMI-SYNTHETIC RESINS

9 MEDICAL ADHESIVES MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 WATER-BASED

- 9.2.1 RISING DEMAND FOR BIOCOMPATIBLE AND SKIN-FRIENDLY SOLUTIONS DRIVING ADOPTION

- 9.3 SOLVENT-BASED

- 9.3.1 HIGH BOND STRENGTH AND DURABILITY DRIVING DEMAND FOR SOLVENT-BASED MEDICAL ADHESIVES

- 9.4 SOLID & HOT MELT-BASED

- 9.4.1 FAST PROCESSING AND SOLVENT-FREE FORMULATION DRIVING ADOPTION OF HOT MELT MEDICAL ADHESIVES

10 MEDICAL ADHESIVES MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 DENTAL

- 10.2.1 RISING DEMAND FOR COSMETIC AND RESTORATIVE DENTISTRY DRIVING MARKET GROWTH

- 10.3 SURGERY

- 10.3.1 GROWING SHIFT TOWARD MINIMALLY INVASIVE PROCEDURES DRIVING ADOPTION

- 10.3.2 INTERNAL

- 10.3.2.1 Increasing complex surgical procedures driving demand for internal medical adhesives

- 10.3.3 EXTERNAL

- 10.3.3.1 Rising preference for sutureless skin closure driving external adhesives demand

- 10.4 MEDICAL DEVICE & EQUIPMENT

- 10.4.1 RAPID GROWTH OF WEARABLE AND MINIATURIZED DEVICES DRIVING DEMAND

- 10.5 OTHER APPLICATIONS

11 MEDICAL ADHESIVES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Rising surgical volumes and advanced healthcare infrastructure driving demand

- 11.2.2 CANADA

- 11.2.2.1 Growing surgical procedures and aging population fueling demand

- 11.2.3 MEXICO

- 11.2.3.1 Expanding medical device manufacturing and healthcare infrastructure driving market growth

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 Massive healthcare expansion and government support driving demand

- 11.3.2 INDIA

- 11.3.2.1 Expanding healthcare coverage and rising surgical volumes fueling market growth

- 11.3.3 JAPAN

- 11.3.3.1 Rapidly aging population driving demand for advanced medical adhesives

- 11.3.4 SOUTH KOREA

- 11.3.4.1 Presence of advanced medical device industry driving medical adhesives demand

- 11.3.5 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Strong healthcare infrastructure and high surgical volumes driving demand

- 11.4.2 FRANCE

- 11.4.2.1 Advanced healthcare systems and rising surgical procedures fueling market growth

- 11.4.3 UK

- 11.4.3.1 E-commerce sales to drive market expansion

- 11.4.4 ITALY

- 11.4.4.1 Rapidly aging population fueling demand for advanced wound care and surgical adhesives

- 11.4.5 SPAIN

- 11.4.5.1 Growing aging population and chronic disease burden driving demand

- 11.4.6 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Vision 2030 healthcare investments accelerating market growth

- 11.5.1.2 Rest of GCC

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Rising chronic disease burden and healthcare expansion supporting market growth

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Expanding public healthcare system driving medical adhesives demand

- 11.6.2 ARGENTINA

- 11.6.2.1 Rising chronic disease burden accelerating demand

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Overall company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Technology footprint

- 12.7.5.4 Resin type footprint

- 12.7.5.5 Application footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHERS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 SOLVENTUM (3M)

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Others

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 HENKEL AG & CO, KGAA

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 H.B. FULLER COMPANY

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 SCAPA HEALTHCARE

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 JOHNSON & JOHNSON (MEDTECH COMPANY)

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 PERMABOND

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.7 B. BRAUN SE

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 MnM view

- 13.1.8 CHEMENCE MEDICAL, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Others

- 13.1.8.4 MnM view

- 13.1.9 ARTIVION, INC.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 DYMAX

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 MnM view

- 13.1.11 BOSTIK

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Deals

- 13.1.11.4 MnM view

- 13.1.1 SOLVENTUM (3M)

- 13.2 OTHER PLAYERS

- 13.2.1 MEDTRONIC

- 13.2.2 DENTSPLY SIRONA

- 13.2.3 MASTERBOND INC.

- 13.2.4 ASHLAND

- 13.2.5 ADVANCED MEDICAL SOLUTIONS GROUP PLC

- 13.2.6 HOENLE AG

- 13.2.7 BECTON, DICKINSON AND COMPANY (BD)

- 13.2.8 VIVOSTAT A/S

- 13.2.9 OCULAR THERAPEUTIX, INC.

- 13.2.10 GLAXOSMITHKLINE PLC

- 13.2.11 NITTO DENKO CORPORATION

- 13.2.12 BAXTER INTERNATIONAL

- 13.2.13 CARTELL CHEMICAL CO., LTD.

- 13.2.14 BIOSEAL INC.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 List of key secondary sources

- 14.1.1.2 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 List of primary interview participants-demand and supply side

- 14.1.2.3 Key industry insights

- 14.1.2.4 Breakdown of interviews with experts

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.2 TOP-DOWN APPROACH

- 14.3 FORECAST NUMBER CALCULATION

- 14.4 DATA TRIANGULATION

- 14.5 FACTOR ANALYSIS

- 14.6 ASSUMPTIONS

- 14.7 LIMITATIONS & RISKS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS