|

시장보고서

상품코드

2027370

차세대 약물 접합체 시장 : 제품별, 유형별, 표적 리간드별, 페이로드 유형별, 적응증별, 지역별 - 세계 예측(-2035년)Next Generation Drug Conjugates Market by Product (Enhertu, Amvuttra), Type (Antibody-Small Molecule), Target Ligand (Antibody, Peptide), Payload Type (Oligonucleotide, Radionuclide), Indication (Breast Cancer, Prostate Cancer) - Global Forecast to 2035 |

||||||

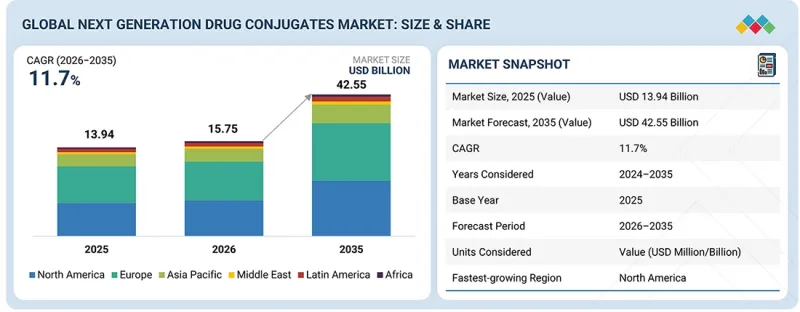

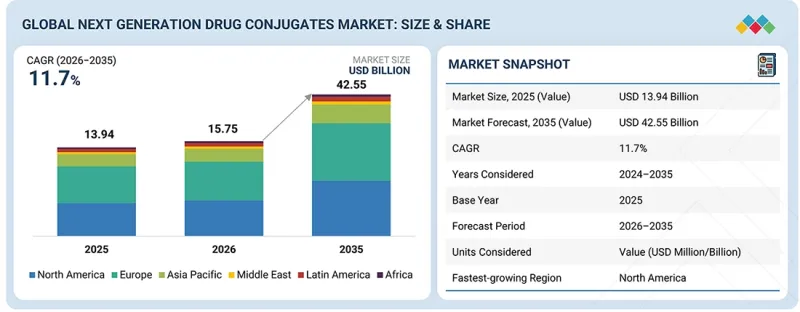

세계의 차세대 약물 접합체 시장 규모는 2026년 157억 5,000만 달러에서 2035년까지 425억 5,000만 달러에 달할 것으로 추정되어 있으며, 2026년에서 2035년까지 예측 기간 동안 CAGR 11.7%를 기록할 것으로 전망됩니다.

세계 차세대 약물 접합체 시장은 표적 치료제 채택 확대, 링커, 페이로드, 표적화 리간드 기술의 지속적인 혁신, 종양학에 초점을 맞춘 의약품 개발에 대한 투자 증가에 힘입어 예측 기간 동안 강력한 성장세를 보일 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2035년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 유형별, 표적 리간드별, 페이로드 유형별, 적응증별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

발표된 업계 정보를 기반으로 한 시장 예측에 따르면, 2034년까지 두 자릿수 성장률을 기록할 것으로 예상되며, 이는 이러한 치료법에 대한 임상적 및 상업적 모멘텀을 반영합니다. 그러나 안전성에 대한 우려, 제조의 복잡성, 그리고 높은 치료비용은 시장의 추가 확장을 억제하는 주요 요인으로 남을 것으로 예상됩니다.

"2025년 차세대 약물 복합제 시장에서 제품별로는 엔허투(Enhertu)가 가장 큰 점유율을 차지했습니다."

제품별로 살펴보면, 차세대 복합제 시장은 엔하투(fam-trastuzumab deruxtecan-nxki), 플루빅토(lutetium Lu 177 vipivotide tetraxetan), 암부트라(vutrisiran), 토로델비(sacituzumab govitecan-hziy), 사시투주맙 틸모테칸, 파트리투주맙 덱스테칸(HER3-DXd), 225Ac-PSMA-617, 기타 시판 중인 제품, 기타 파이프라인 제품으로 크게 나뉩니다. 2025년에는 ENHERTU 부문이 가장 큰 시장 점유율을 차지했습니다. 이러한 선도적 지위는 여러 HER2 발현 종양 유형에 대한 강력한 효능, 전이성 유방암을 넘어 보다 광범위한 고형암 영역으로 빠르게 적응증을 확대한 점, 의사들의 신뢰와 치료 도입률을 높인 독보적인 DXd 페이로드와 바이스탠더 효과 등 여러 요인에 기인하는 것으로 보입니다. 또한, 엔헬츠는 세계 시장 침투 확대, 치료 초기 단계에서의 사용 증가, 아스트라제네카와 다이이찌산쿄의 광범위한 개발 및 상업화 역량을 통해 강력한 지원을 받을 수 있게 되었습니다.

"2025년 차세대 약물 접합체 시장에서 유형별로는 항체-저분자 약물 복합체 부문이 가장 큰 점유율을 차지했습니다."

최종사용자별로 세계 차세대 약물 접합체 시장은 항체-저분자 약물 복합체, 리간드-올리고뉴클레오티드 복합체, 저분자-방사성동위원소 복합체, 펩타이드-방사성동위원소 복합체, 기타 복합체 유형으로 분류됩니다. 2025년에는 항체-저분자 부문이 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이는 주로 항체약물접합체가 표적형 접합체 중 가장 임상적으로 확립되고 상업적으로 발전된 클래스이며, 지속적인 기술 발전으로 여러 종양 유형에서 치료 성적이 개선되고 있기 때문입니다.

"2026년부터 2035년까지 차세대 약물 접합체 시장에서 북미가 가장 높은 CAGR로 성장하고 있습니다."

차세대 약물 접합체 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 구분됩니다. 예측 기간 동안 북미는 가장 높은 CAGR로 성장할 것으로 예상됩니다. 이러한 성장은 이 지역의 바이오의약품 혁신의 집중, 첨단 표적 치료제의 조기 도입, 노바티스, 화이자, 아루니람과 같은 주요 시장 진입자들이 차세대 약물 복합제 개발 및 상용화에 적극적으로 나서고 있기 때문인 것으로 분석됩니다.

본 보고서에 소개된 기업 프로파일 목록

- Alnylam Pharmaceuticals

- Gilead Sciences, Inc.

- Novartis AG

- AstraZeneca

- Daiichi Sankyo Company, Limited

- Ionis Pharmaceuticals, Inc.

- Rakuten Group

- Novo Nordisk

- ADC Therapeutics SA

- Sanofi

- Arrowhead Pharmaceuticals

- Abbvie

- Regeneron Pharmaceuticals, Inc.

- Bicycle therapeutics

- Avidity Biosciences

- Silence Therapeutics

- MediLink Therapeutics

- SystImmune, Inc.

- Actinium Pharmaceuticals

- Alphamab Oncology

- Fusion Pharma

- Orano group

- PepGen Inc

- Tubulis GmbH

- Clarity Pharmaceuticals

조사 범위

본 조사 보고서는 차세대 약물 접합체 시장을 제품별, 유형별, 표적 리간드별, 페이로드 유형별, 적응증별, 지역별로 분석하였습니다.

이 보고서의 조사 범위는 차세대 약물 접합체 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 과제, 기회, 제약 등)에 대한 자세한 정보를 다룹니다. 이 보고서는 주요 업계 진출 기업들에 대한 상세한 분석을 통해 사업 개요, 제품 포트폴리오, 제품 승인 및 출시, 제휴, 파트너십, 사업 확장, 계약 및 차세대 복합제 시장과 관련된 최근 동향과 같은 주요 전략에 대한 인사이트를 제공합니다. 본 보고서는 차세대 약물 접합체 시장 생태계에서 주요 기업 및 신생 스타트업의 경쟁 분석도 다루고 있습니다.

본 보고서 구매의 주요 이점

이 보고서는 전체 차세대 약물 접합체 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 또한, 이해관계자들이 경쟁 상황을 더 깊이 이해하고, 자신의 비즈니스를 적절히 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 이 보고서를 통해 이해관계자들은 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 기회 및 과제에 대한 정보를 얻을 수 있습니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(항체약물접합체의 임상적 성공과 규제 당국의 승인 증가, 링커 화학 및 페이로드 개발의 기술적 진보), 제약요인(복잡한 바이오의약품에 따른 높은 개발 및 제조 비용), 기회(비종양 치료 영역으로의 약물 복합체 확대), 도전 과제(복잡한 임상시험 설계 및 복잡한 임상시험 설계 및 환자 선정 요건)에 대한 분석은 차세대 약물 복합제 시장의 성장에 영향을 미치고 있습니다.

- 제품 개발/혁신 : 차세대 약물 복합제 시장의 신규 출시 제품에 대한 심층 분석

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 차세대 약물 접합체 시장을 분석합니다.

- 시장 다각화 : 차세대 복합제 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보 제공

- 경쟁사 분석 : 차세대 복합제 시장의 주요 기업(Alnylam Pharmaceuticals(미국), Gilead Sciences, Inc. Limited(일본), Ionis Pharmaceuticals, Inc.(미국) 등)의 시장 점유율, 성장 전략, 제품 라인업에 대한 상세 평가

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 차세대 약물 접합체 시장(제품별)

제10장 차세대 약물 접합체 시장(유형별)

제11장 차세대 약물 접합체 시장(표적 리간드별)

제12장 차세대 약물 접합체 시장(페이로드 유형별)

제13장 차세대 약물 접합체 시장(적응증별)

제14장 차세대 약물 접합체 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSMThe global next generation drug conjugates market is estimated to reach USD 42.55 billion by 2035 from USD 15.75 billion in 2026, at a CAGR of 11.7% during the forecast period of 2026 to 2035. The global next generation drug conjugates market is projected to witness strong growth over the forecast period, supported by rising adoption of targeted therapies, continued innovation in linker, payload, and targeting ligand technologies, and increasing investment in oncology-focused drug development.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD billion) |

| Segments | Product, Type, Targeting ligand, Payload type, Indications |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

Market estimates from published industry sources indicate robust double-digit growth through 2034, reflecting strong clinical and commercial momentum for these therapies. However, safety concerns, manufacturing complexity, and high treatment costs are expected to remain key factors restraining broader market expansion.

"The Enhertu product segment accounted for the largest share by product in the next generation drug conjugates market in 2025."

Based on product, the next generation drug conjugates market is broadly segmented into Enhertu (fam-trastuzumab deruxtecan-nxki), Pluvicto (lutetium Lu 177 vipivotide tetraxetan), Amvuttra (vutrisiran), Trodelvy (sacituzumab govitecan-hziy), Sacituzumab tirumotecan, Patritumab Deruxtecan (HER3-DXd), 225Ac-PSMA-617, other commercialized products and other pipeline products. The ENHERTU segment held the largest market share in 2025. This leadership can be attributed to several factors, including its strong efficacy across multiple HER2-expressing tumor types, rapid label expansion beyond metastatic breast cancer into broader solid tumor settings, and its differentiated DXd payload and bystander effect, which have strengthened physician confidence and treatment adoption. In addition, Enhertu has benefited from growing global commercial penetration, increasing use in earlier lines of therapy, and strong backing from AstraZeneca and Daiichi Sankyo's extensive development and commercialization capabilities.

"The antibody-small molecule drug conjugate segment accounted for the largest share by type segment in the next generation drug conjugates market in 2025."

Based on end users, the global next generation drug conjugates market is segmented into antibody-small molecule drug conjugates, ligand-oligonucleotide conjugates, small molecule-radionuclide conjugates, peptide-radionuclide conjugates, and other conjugate types. In 2025, the antibody-small molecule segment accounted for the largest share of the market. This is primarily because antibody-drug conjugates are the most clinically established and commercially advanced class within targeted conjugates, with continued technological progress improving outcomes across multiple tumor types.

"North America is growing at the highest CAGR in the next generation drug conjugates market from 2026 to 2035."

The next generation drug conjugates market is segmented into North America, Europe, Asia Pacific, Latin America, the Middle East and Africa. During the forecast period, the North American region is estimated to grow at the highest CAGR. This growth is expected to be supported by the region's strong concentration of biopharmaceutical innovation, early adoption of advanced targeted therapies and the presence of key market participants, such as Novartis, Pfizer and Alnylam, actively developing and commercializing next generation drug conjugates.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side - 70% and Demand Side - 30%

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: CXOs and Directors - 30%, Managers - 45%, and Others - 25%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Latin America - 10%, and the Middle East - 5%

List of Companies Profiled in the Report

- Alnylam Pharmaceuticals

- Gilead Sciences, Inc.

- Novartis AG

- AstraZeneca

- Daiichi Sankyo Company, Limited

- Ionis Pharmaceuticals, Inc.

- Rakuten Group

- Novo Nordisk

- ADC Therapeutics SA

- Sanofi

- Arrowhead Pharmaceuticals

- Abbvie

- Regeneron Pharmaceuticals, Inc.

- Bicycle therapeutics

- Avidity Biosciences

- Silence Therapeutics

- MediLink Therapeutics

- SystImmune, Inc.

- Actinium Pharmaceuticals

- Alphamab Oncology

- Fusion Pharma

- Orano group

- PepGen Inc

- Tubulis GmbH

- Clarity Pharmaceuticals

Research Coverage

This research report categorizes the next generation drug conjugates market by product (Enhertu [fam-trastuzumab deruxtecan-nxki], Pluvicto [lutetium Lu 177 vipivotide tetraxetan], AMVUTTRA [vutrisiran], TRODELVY [sacituzumab govitecan-hziy], Sacituzumab tirumotecan, Patritumab Deruxtecan [HER3-DXd], 225Ac-PSMA-617, other commercialized products and other pipeline products); by type: antibody-small molecule drug conjugate, ligand-oligonucleotide conjugate, small molecule-radionuclide conjugate, peptide-radionuclide conjugate, and other conjugate types; by targeting ligand: antibody, amino sugar, small molecule and peptide; by payload type: small molecule, oligonucleotide, and radionuclide; by indications: breast cancer, prostate cancer, hATTR with polyneuropathy, primary hyperlipidemia and other indications; and by region (North America, Europe, Asia Pacific, Latin America, Middle East, Africa).

The scope of the report covers detailed information regarding the major factors, such as drivers, challenges, opportunities, and restraints, influencing the growth of the next generation drug conjugates market. A detailed analysis of the key industry players has been done to provide insights into their business overview, product portfolio, key strategies such as product approvals and launches, collaborations, partnerships, expansions, agreements, and recent developments associated with the next generation drug conjugates market. Competitive analysis of top players and upcoming startups in the next generation drug conjugates market ecosystem is covered in this report.

Key Benefits of Buying the Report

The report will help market leaders/new entrants by providing them with the closest approximations of the revenue numbers for the overall next generation drug conjugates market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their business and make suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide them with information on the key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing clinical success and regulatory approvals of antibody-drug conjugates, technological advancements in linker chemistry and payload development), restraints (high development and manufacturing costs associated with complex biologics), opportunities (expansion of drug conjugates into non-oncology therapeutic areas) and challenges (complex clinical trial design and patient selection requirements) are influencing the growth of next generation drug conjugates market

- Product Development/Innovation: Detailed insights on newly launched products of the next generation drug conjugates market

- Market Development: Comprehensive information about lucrative markets - the report analyses the next generation drug conjugates market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the next generation drug conjugates market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players include Alnylam Pharmaceuticals (US), Gilead Sciences, Inc. (US), Novartis AG (Switzerland), AstraZeneca (UK), Daiichi Sankyo Company, Limited (Japan), Ionis Pharmaceuticals, Inc. (US), among others in the next generation drug conjugates market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 NEXT-GENERATION DRUG CONJUGATES MARKET OVERVIEW

- 3.2 NEXT-GENERATION DRUG CONJUGATES MARKET, BY TARGET LIGAND & REGION

- 3.3 NEXT-GENERATION DRUG CONJUGATES MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing clinical success and regulatory approvals of antibody-drug conjugates

- 4.2.1.2 Technological advancements in linker chemistry and payload development

- 4.2.2 RESTRAINTS

- 4.2.2.1 High development and manufacturing costs associated with complex biologics

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of drug conjugates into non-oncology therapeutic areas

- 4.2.3.2 Increasing developments of novel conjugate platforms

- 4.2.4 CHALLENGES

- 4.2.4.1 Concerns related to biocompatibility, safety, and adverse immune responses

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY MOLECULE

- 4.4.2 PHARMACEUTICAL MANUFACTURING SERVICES MARKET FOR SMALL MOLECULES, BY TYPE

- 4.4.3 PHARMACEUTICAL CONTRACT MANUFACTURING MARKET FOR LARGE MOLECULES, BY TYPE

- 4.4.4 BIOCONJUGATION SERVICES MARKET, BY CONJUGATION TYPE

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL NEXT-GENERATION DRUG CONJUGATES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE SELLING PRICE, BY KEY PLAYER, 2025 (USD)

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- 5.5.3 AVERAGE SELLING PRICE RANGE, BY REGION, 2025 (USD)

- 5.6 KEY CONFERENCES & EVENTS

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.8 INVESTMENT & FUNDING ACTIVITY

- 5.9 IMPACT OF US TARIFFS-NEXT-GENERATION DRUG CONJUGATES MARKET

- 5.9.1 INTRODUCTION

- 5.9.2 KEY TARIFF RATES

- 5.9.3 PRICE IMPACT ANALYSIS

- 5.9.4 IMPACT ON COUNTRIES/REGIONS

- 5.9.4.1 North America

- 5.9.4.2 Europe

- 5.9.4.3 Asia Pacific

- 5.9.5 IMPACT ON END-USE INDUSTRIES

- 5.9.5.1 Hospitals

- 5.9.5.2 Specialty clinics and cancer centers

- 5.9.5.3 Other specialty care settings

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 New-generation payload chemistries

- 6.1.1.2 Radioligand/theranostic conjugate engineering

- 6.1.2 ADJACENT TECHNOLOGIES

- 6.1.2.1 Protein engineering/antibody engineering

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.1.3.1 Diagnostic imaging/theranostics workflows

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 FUTURE APPLICATIONS

- 6.4 IMPACT OF AI/GEN AI ON NEXT-GENERATION DRUG CONJUGATES MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 CASE STUDIES OF AI IMPLEMENTATION IN NEXT-GENERATION DRUG CONJUGATES MARKET

- 6.4.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN NEXT-GENERATION DRUG CONJUGATES MARKET

- 6.5 PIPELINE ANALYSIS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK & REIMBURSEMENT

- 7.1.2.1 Reimbursement scenario

- 7.1.3 INDUSTRY STANDARDS

- 7.1.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END USERS

- 8.5 MARKET PROFITABILITY

9 NEXT-GENERATION DRUG CONJUGATES MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 ENHERTU

- 9.2.1 BROAD CLINICAL ADOPTION AND REGULATORY EXPANSION OF TARGETED ADC THERAPIES DRIVE MARKET GROWTH

- 9.3 PLUVICTO

- 9.3.1 EXPANDING USE OF TARGETED RADIOLIGAND THERAPY IN PROSTATE CANCER TO DRIVE MARKET GROWTH

- 9.4 AMVUTTRA

- 9.4.1 ADVANCING RNAI THERAPEUTICS THROUGH DURABLE GENE SILENCING AND EXPANDED INDICATION REACH

- 9.5 TRODELVY

- 9.5.1 RISING GOVERNMENT APPROVALS FOR BREAST CANCER TREATMENTS TO DRIVE MARKET GROWTH

- 9.6 SACITUZUMAB TIRUMOTECAN

- 9.6.1 ADVANCING NEXT-GENERATION ADC PAYLOAD INNOVATION IN NDC MARKET

- 9.7 PATRITUMAB DERUXTECAN

- 9.7.1 ADVANCEMENTS IN HER3-DIRECTED ANTIBODY-DRUG CONJUGATES TO AID GROWTH

- 9.8 225AC-PSMA-617

- 9.8.1 POTENT THERAPEUTIC PROFILE AND EXPANDING CLINICAL VALIDATION TO SUPPORT MARKET GROWTH

- 9.9 OTHER COMMERCIALIZED PRODUCTS

- 9.10 OTHER PIPELINE PRODUCTS

10 NEXT-GENERATION DRUG CONJUGATES MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 ANTIBODY-SMALL MOLECULE CONJUGATES

- 10.2.1 ENHANCED CLINICAL UTILITY AND TECHNOLOGICAL INNOVATION TO DRIVE MARKET

- 10.3 PEPTIDE-RADIONUCLIDE CONJUGATES

- 10.3.1 INNOVATIONS IN PRECISION ONCOLOGY APPLICATIONS AND TECHNOLOGICAL ADVANCEMENTS SUPPORT GROWTH

- 10.4 LIGAND-OLIGONUCLEOTIDE CONJUGATES

- 10.4.1 ENHANCED DELIVERY AND TISSUE TARGETING CAPABILITIES OF LIGAND-OLIGONUCLEOTIDE CONJUGATES DRIVE GROWTH

- 10.5 OTHER DRUG CONJUGATES

11 NEXT-GENERATION DRUG MARKET, BY TARGET LIGAND

- 11.1 INTRODUCTION

- 11.2 ANTIBODIES

- 11.2.1 ADVANCEMENTS IN ANTIBODY ENGINEERING AND EXPANDING TARGET DIVERSITY DRIVE GROWTH

- 11.3 AMINO SUGARS

- 11.3.1 GROWING ADOPTION OF GALNAC-BASED LIVER-TARGETING PLATFORMS DRIVES EXPANSION

- 11.4 SMALL MOLECULES

- 11.4.1 EXPANDING USE OF SMALL-MOLECULE TARGETING LIGANDS IS BROADENING THE NEXT-GENERATION DRUG CONJUGATES MARKET

- 11.5 PEPTIDES

- 11.5.1 EXPANDING CLINICAL PIPELINES AND TUMOR-TARGETING INNOVATIONS PROPEL GROWTH

12 NEXT-GENERATION DRUG CONJUGATES MARKET, BY PAYLOAD TYPE

- 12.1 INTRODUCTION

- 12.2 SMALL-MOLECULE PAYLOADS

- 12.2.1 RISING ADOPTION OF HIGHLY POTENT, NEXT-GENERATION PAYLOADS AND ADVANCED LINKER TECHNOLOGIES IS ACCELERATING GROWTH

- 12.3 OLIGONUCLEOTIDE PAYLOADS

- 12.3.1 RISING ADOPTION OF RNA-BASED GENE-SILENCING THERAPIES AND LONG-ACTING CONJUGATE PLATFORMS TO DRIVE MARKET

- 12.4 RADIONUCLIDE PAYLOADS

- 12.4.1 EXPANDING RADIOLIGAND THERAPY ADOPTION AND ADVANCEMENTS IN ISOTOPE TECHNOLOGIES SUPPORT MARKET GROWTH

13 NEXT-GENERATION DRUG CONJUGATES MARKET, BY INDICATION

- 13.1 INTRODUCTION

- 13.2 BREAST CANCER

- 13.2.1 RISING INCIDENCE AND INCREASING ADOPTION OF TARGETED ADC THERAPIES TO DRIVE MARKET

- 13.3 HATTR WITH POLYNEUROPATHY

- 13.3.1 ADVANCEMENTS IN RNA-BASED GENE-SILENCING THERAPIES AND INCREASING DIAGNOSIS RATES ARE DRIVING GROWTH

- 13.4 PROSTATE CANCER

- 13.4.1 EXPANDING ADOPTION OF PSMA-TARGETED RADIOLIGAND THERAPIES IS DRIVING GROWTH

- 13.5 PRIMARY HYPERLIPIDEMIA

- 13.5.1 INCREASING ADOPTION OF LONG-ACTING RNA-BASED THERAPIES DRIVES MARKET GROWTH

- 13.6 OTHER INDICATIONS

14 NEXT-GENERATION DRUG CONJUGATES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 FDA approvals, expanding clinical pipelines, and strategic collaborations drive market

- 14.2.2 CANADA

- 14.2.2.1 Increasing access to innovative NDC therapies drives growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Access to innovative therapies and strong radioligand infrastructure are driving growth

- 14.3.2 UK

- 14.3.2.1 Rising demand for precision oncology and advanced conjugate technologies drives market expansion

- 14.3.3 FRANCE

- 14.3.3.1 Biopharma presence and global innovation in targeted conjugates support market growth

- 14.3.4 ITALY

- 14.3.4.1 Expanding clinical research to accelerate market growth

- 14.3.5 SPAIN

- 14.3.5.1 Increased focus on research for NDC development to propel market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Strong domestic innovation and expanding oncology demand drive NDC market growth

- 14.4.2 JAPAN

- 14.4.2.1 Growing drug approvals and pharma biotech research initiatives support market growth

- 14.4.3 INDIA

- 14.4.3.1 Expanding biologics capabilities and rising demand for targeted oncology therapies support growth

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Key drug approvals relevant to NDC market to aid growth in South Korea

- 14.4.5 AUSTRALIA

- 14.4.5.1 Strong regulatory framework, clinical innovation, and global partnerships drive market growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Expanding clinical trials and rising demand for targeted oncology therapies drive market growth

- 14.5.2 MEXICO

- 14.5.2.1 Gradual increase in pharmaceutical R&D to support market growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.6.1.1 Integration of genomics, biomarker-driven diagnostics, and personalized treatment to propel market

- 14.6.2 REST OF MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.7 AFRICA

- 14.7.1 RESEARCH COLLABORATIONS AND INFRASTRUCTURAL DEVELOPMENT TO DRIVE MARKET

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Type footprint

- 15.5.5.4 Indication footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 BRAND COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 ASTRAZENECA

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product approvals

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices made

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 DAIICHI SANKYO COMPANY, LIMITED

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Products in pipeline

- 16.1.2.4 Recent developments

- 16.1.2.4.1 Product approvals

- 16.1.2.4.2 Expansions

- 16.1.2.5 MnM view

- 16.1.2.5.1 Key strengths/Right to win

- 16.1.2.5.2 Strategic choices made

- 16.1.2.5.3 Weaknesses and competitive threats

- 16.1.3 NOVARTIS AG

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product approvals

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices made

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 ALNYLAM PHARMACEUTICALS, INC

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product approvals

- 16.1.4.3.2 Deals

- 16.1.4.3.3 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices made

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 GILEAD SCIENCES, INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Expansions

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices made

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 IONIS PHARMACEUTICALS, INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Products in pipeline

- 16.1.6.4 Recent developments

- 16.1.6.4.1 Product approvals

- 16.1.6.4.2 Deals

- 16.1.7 RAKUTEN GROUP, INC.

- 16.1.7.1 Business overview

- 16.1.7.2 Products in pipeline

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Deals

- 16.1.8 NOVO NORDISK

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product approvals

- 16.1.8.3.2 Deals

- 16.1.9 ADC THERAPEUTICS SA

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Products in pipeline

- 16.1.10 SANOFI

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Products in pipeline

- 16.1.10.4 Recent developments

- 16.1.10.4.1 Deals

- 16.1.11 ARROWHEAD PHARMACEUTICALS

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product approvals

- 16.1.12 ABBVIE INC.

- 16.1.12.1 Business overview

- 16.1.12.2 Products in pipeline

- 16.1.13 REGENERON PHARMACEUTICALS INC.

- 16.1.13.1 Business overview

- 16.1.13.2 Products in pipeline

- 16.1.1 ASTRAZENECA

- 16.2 OTHER PLAYERS

- 16.2.1 BICYCLE THERAPEUTICS

- 16.2.2 AVIDITY BIOSCIENCES

- 16.2.3 SILENCE THERAPEUTICS

- 16.2.4 MEDILINK THERAPEUTICS

- 16.2.5 SYSTIMMUNE, INC.

- 16.2.6 ACTINIUM PHARMACEUTICALS

- 16.2.7 ALPHAMAB ONCOLOGY

- 16.2.8 FUSION PHARMA

- 16.2.9 ORANO GROUP

- 16.2.10 PEPGEN INC

- 16.2.11 TUBULIS GMBH

- 16.2.12 CLARITY PHARMACEUTICALS

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.2 PRIMARY DATA

- 17.2 MARKET ESTIMATION METHODOLOGY

- 17.2.1 MARKET SIZE ESTIMATION

- 17.2.2 INSIGHTS OF PRIMARY EXPERTS

- 17.2.3 TOP-DOWN APPROACH

- 17.3 MARKET GROWTH RATE PROJECTIONS

- 17.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS