|

시장보고서

상품코드

2029865

산업용 교반기 시장 예측(-2032년) : 출력 정격별, 모델 유형별, 컴포넌트별, 설치 방식별, 형상별, 업계별, 지역별Industrial Agitators Market by Model Type, Rating, Mounting, Form, Component - Global Forecast to 2032 |

||||||

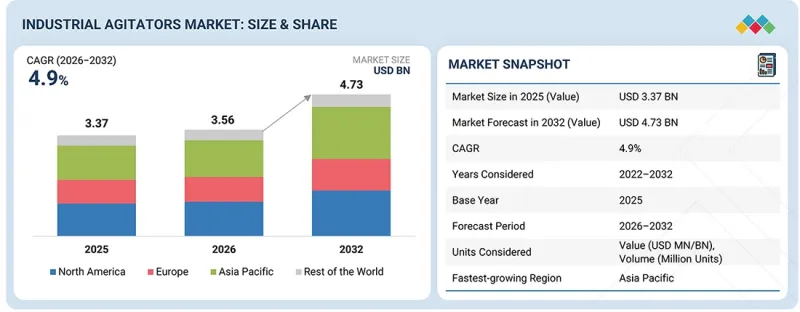

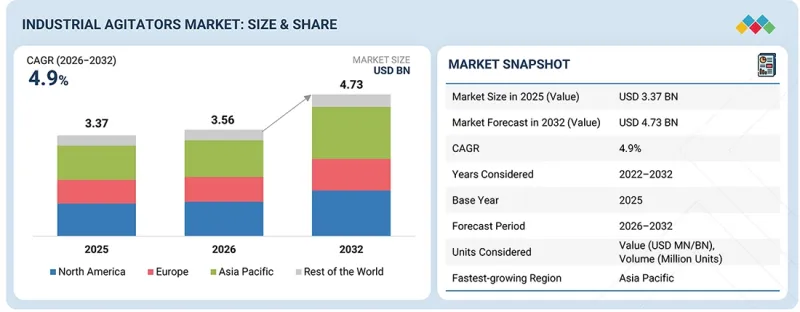

산업용 교반기 시장 규모는 2026년 35억 6,000만 달러에서 2032년에는 47억 3,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 4.9%에 달할 전망입니다.

에너지 비용 상승과 지속가능성에 대한 압박이 커지면서 각 산업계는 에너지 효율이 높은 설비의 도입에 점점 더 많은 관심을 기울이고 있습니다. 연속 처리 공정에 필수적인 산업용 교반기는 전체 에너지 소비에 크게 기여하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 출력 정격별, 모델 유형별, 컴포넌트별, 설치 방식별, 형상별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

그 결과, 각 제조업체들은 교반 성능의 저하 없이 전력 소비를 줄이기 위해 최적화된 임펠러 설계, 가변 주파수 드라이브, 고효율 모터를 갖춘 첨단 교반기를 채택하고 있습니다. 이러한 혁신은 더 나은 유동 패턴, 토크 요구 사항 감소, 공정 출력 향상 및 운영 비용 절감으로 이어집니다. 또한 각 기업은 탄소발자국을 최소화하고 환경 규제에 대응하기 위해 노력하고 있으며, 이로 인해 에너지 효율이 높은 시스템으로의 전환이 더욱 가속화되고 있습니다. 장기적인 비용 절감과 더불어 생산성 향상 및 지속가능성의 이점이 결합된 최신 교반기는 화학, 식품 가공, 제약 및 기타 산업 분야에서 매력적인 투자 대상입니다.

"모델 유형별로는 휴대용 교반기 부문이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

휴대용 교반기는 유연성, 비용 효율성, 다양한 응용 분야에 쉽게 도입할 수 있는 장점으로 인해 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이 교반기는 중소기업뿐만 아니라 임시 또는 이동식 혼합 솔루션이 필요한 업계에서 널리 선호되고 있습니다. 다양한 크기의 탱크에 쉽게 설치, 이동, 조작할 수 있으며, 범용성이 매우 높은 것이 특징입니다. 수처리, 식품가공, 특수화학 분야의 수요 증가는 그 보급을 더욱 촉진하고 있습니다. 또한 모듈식 및 분산형 생산 시스템으로 전환하는 추세가 강화되고 있는 것도 휴대용 장비에 대한 수요를 촉진하고 있습니다. 고정식 시스템에 비해 설비투자 및 유지보수 부담이 적은 점도 보급에 기여하고 있으며, 시장에서의 우위를 강화하고 있습니다.

"설치 유형별로는 탑마운트형이 예측 기간 중 가장 큰 시장점유율을 차지할 것으로 예상됩니다. "

탑마운트형 교반기는 광범위한 적용 가능성과 대규모 혼합 작업에서 우수한 성능으로 산업용 교반기 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 시스템은 대용량 탱크, 혼합, 분산, 화학 반응 등 다양한 혼합 요구사항에 대응하는 데 적합합니다. 이러한 설계는 효율적인 동력 전달과 최적의 유동 패턴을 실현하여 일관된 제품 품질을 보장합니다. 화학, 제약, 식품 및 음료 등의 산업에서는 확장성과 사용자 정의가 가능하므로 탑마운트형 구성이 점점 더 선호되고 있습니다. 또한 유지보수의 용이성, 우수한 실링 성능, 자동화 기술과의 호환성으로 인해 그 채택이 더욱 확대되고 있습니다. 전 세계 산업 가공 시설의 지속적인 확장은 탑마운트형 교반기에 대한 수요를 지속적으로 견인하고 있습니다.

"아시아태평양은 산업용 교반기 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. "

아시아태평양은 급속한 산업화와 주요 최종 사용 산업의 강력한 성장으로 인해 산업용 교반기 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. 중국, 인도, 동남아시아 국가 등에서 화학, 제약, 식품 및 음료, 광업 부문의 확장은 효율적인 혼합 솔루션에 대한 수요를 크게 증가시키고 있습니다. 제조 인프라에 대한 투자 증가와 더불어 정부의 지원 정책 및 산업 개발 구상이 결합되어 시장 성장을 더욱 가속화시키고 있습니다. 또한 세계 생산기지가 이 지역으로 이동하고, 비용 경쟁력을 갖춘 현지 제조업체의 존재가 시장 침투를 촉진하고 있습니다. 공정 효율성, 에너지 최적화, 대규모 생산 능력에 대한 관심이 높아지면서 아시아태평양 시장의 강력한 성장세를 지원하고 있습니다.

이 보고서에서 다루고 있는 주요 기업 - 산업용 교반기 시장에서 사업을 운영하고 있는 주요 기업으로는 SPX FLOW(미국), Xylem(미국), EKATO Holding GmbH(독일), NOV(미국), Suzler(스위스), Ingersoll Rand(미국), Dynamix Agitators(캐나다), Mixer Direct(미국), Silverson(영국), Statifio Group(영국) 및 Tacmia Corporation(일본) 등을 들 수 있습니다.

이들 기업은 혼합 효율 향상, 임펠러 설계 최적화, 에너지 효율 향상, 다양한 응용 분야에서 복잡한 고점도 유체 처리 능력에 중점을 두고 산업용 교반기의 성능을 지속적으로 향상시켜 경쟁하고 있습니다. 전략적인 초점은 견고하고 사용자 정의 가능한 시스템 설계, 자동화 및 공정 제어 시스템과의 통합, 화학, 제약, 식품 및 음료, 광업, 수처리 등의 산업을 위한 애플리케이션 특화 솔루션 개발에 맞춰져 있습니다. 시장 진입 기업은 기존 처리 설비와의 원활한 통합을 최우선 과제로 삼고, 신뢰성, 내구성 및 유지보수 용이성을 보장합니다. 또한 운영 비용 절감, 프로세스 일관성 향상, 장비, 엔지니어링, 애프터마켓 서비스를 결합한 종합적인 솔루션 제공에 중점을 두고 있습니다. 첨단 소재, 디지털 모니터링 기술, 고효율 모터에 대한 지속적인 투자와 최종사용자 및 엔지니어링 기업과의 협력으로 글로벌 산업용 교반기 시장에서의 경쟁이 유지되고 도입이 가속화될 것으로 예상됩니다.

산업용 교반기 시장의 주요 기업에 대해 상세히 조사했으며, 각 기업의 기업 개요, 최근 동향, 주요 시장 전략에 대해 조사 분석하여 전해드립니다.

조사 범위

이 산업용 교반기 시장 보고서는 출력 등급, 모델 유형, 구성 요소, 장착 방식, 형태, 산업 분야, 지역별로 상세한 분석을 제시합니다. 출력 등급별로 시장은 50마력 미만, 50마력-200마력, 200마력 이상 등 3개 부문로 분류됩니다. 모델 유형별로는 대형 탱크용 교반기, 휴대용 교반기, 드럼용 교반기, 기타로 분류됩니다. 구성품별로는 헤드/동력장치, 실링 시스템, 임펠러, 기타 등이 있습니다. 장착 방식에 따라 탑마운트형, 사이드마운트형, 바텀마운트형으로 구분됩니다. 형태별로는 고체-고체, 고체-액체, 액체-기체, 액체-기체, 액체-액체 혼합물 등이 있습니다. 산업별로는 화학, 제약, 페인트/코팅, 광업, 식품/음료, 화장품, 기타를 다루고 있습니다. 지역별 분석에는 북미, 유럽, 아시아태평양 및 기타 지역이 포함되어 수요 패턴, 성장 요인 및 산업 동향을 평가할 수 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 전체 시장 및 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 이 시장의 리더와 신규 진입자에게 도움을 줄 수 있습니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 산업용 교반기 시장 동향을 이해하는 데 도움이 되며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서 구매의 주요 이점

- 주요 촉진요인(효율적인 폐수 처리 방법의 도입에 대한 수요 증가, 에너지 효율성, 유량 극대화, 빠른 혼합 및 폐기물 감소에 대한 수요 증가, 공정 산업 및 제조 산업의 강력한 성장, 맞춤형 산업용 교반기에 대한 수요 증가, 자동화 및 스마트 기술 발전, 식품 및 음료 산업의 확대), 제약 요인(높은 유지보수 및 수리 비용, 맞춤형 장비의 긴 리드 타임). 식품 및 음료 산업의 확대와 위생 기준 준수 필요성), 제약 요인(높은 유지보수 및 수리 비용, 맞춤형 장비의 긴 리드타임), 기회(다양한 응용 분야에서 교반 기술 활용 확대, 예지보전을 위한 로트 및 데이터 분석의 통합), 도전 과제(엄격한 정부 안전 기준 및 제품 엄격한 정부 안전 기준 및 제품 컴플라이언스 기준, 고비용 및 저사용 교반기/믹서 장비의 임대라는 새로운 동향, 저비용 제조업체와의 경쟁 심화) 등 산업용 교반기 시장의 성장에 영향을 미치는 요인에 대해 분석했습니다.

- 제품 개발 및 혁신: 산업용 교반기 시장의 미래 기술, 연구개발 활동 및 신제품 출시에 대한 자세한 인사이트.

- 시장 개발: 수익성 높은 시장에 대한 포괄적인 정보 - 이 보고서는 다양한 지역의 산업용 교반기 시장을 분석합니다.

- 시장 다각화: 산업용 교반기 시장의 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보를 제공합니다.

- 경쟁 분석 : SPX FLOW(미국), Xylem(미국), EKATO Holding GmbH(독일), NOV(미국), Suzler(스위스), Ingersoll Rand(미국), Dynamix Agitators(캐나다), Mixer Direct(미국), Silverson(영국), Statifio Group(영국), Tacmia Corporation(일본) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 관한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 그리고 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 산업용 교반기의 응용

제10장 산업용 교반기 유통 채널

제11장 산업용 교반기에 사용되는 재료

제12장 산업용 교반기 시장(출력 정격별)

제13장 산업용 교반기 시장(모델 유형별)

제14장 산업용 교반기 시장(컴포넌트별)

제15장 산업용 교반기 시장(설치 방식별)

제16장 산업용 교반기 시장(형상별)

제17장 산업용 교반기 시장(업계별)

제18장 산업용 교반기 시장(지역별)

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 부록

KSA 26.05.21According to MarketsandMarkets, the industrial agitators market is projected to reach USD 4.73 billion by 2032 from USD 3.56 billion in 2026, registering a CAGR of 4.9% during the forecast period. Industries are increasingly prioritizing energy-efficient equipment as energy costs and sustainability pressures continue to rise. Industrial agitators, being integral to continuous processing operations, contribute significantly to overall energy consumption.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Component, Model Type, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

As a result, manufacturers are adopting advanced agitators with optimized impeller designs, variable frequency drives, and high-efficiency motors to reduce power usage without compromising mixing performance. These innovations enable better flow patterns, reduced torque requirements, and improved process output, leading to lower operational costs. Additionally, companies are focusing on minimizing carbon footprints and meeting environmental regulations, further accelerating the shift toward energy-efficient systems. The long-term cost savings, coupled with enhanced productivity and sustainability benefits, make modern agitators an attractive investment across industries such as chemicals, food processing, and pharmaceuticals.

"By model type, the portable agitators segment is expected to capture the largest market share during the forecast period."

Portable agitators are expected to capture the largest market share during the forecast period due to their flexibility, cost-effectiveness, and ease of deployment across multiple applications. These agitators are widely preferred by small and medium-sized enterprises, as well as industries requiring temporary or mobile mixing solutions. Their ability to be easily installed, relocated, and operated in varying tank sizes makes them highly versatile. Increasing demand from water treatment, food processing, and specialty chemicals sectors is further supporting adoption. Additionally, the growing trend toward modular and decentralized production systems is boosting the need for portable equipment. Lower capital investment and maintenance requirements compared to fixed systems also contribute to their widespread use, strengthening their dominant position in the market.

"By mounting type, the top-mounted segment is expected to capture the largest market share during the forecast period."

Top-mounted agitators are expected to capture the largest share of the industrial agitators market due to their wide applicability and superior performance in large-scale mixing operations. These systems are ideal for handling high-volume tanks and diverse mixing requirements, including blending, dispersion, and chemical reactions. Their design allows for efficient power transmission and optimal flow patterns, ensuring consistent product quality. Industries such as chemical, pharmaceutical, and food & beverage increasingly prefer top-mounted configurations for their scalability and customization capabilities. Moreover, ease of maintenance, better sealing options, and compatibility with automation technologies further enhance their adoption. The ongoing expansion of industrial processing facilities globally continues to drive demand for top-mounted agitators.

"Asia Pacific is estimated to emerge as the fastest-growing region in the industrial agitators market."

Asia Pacific is projected to be the fastest-growing regional market for industrial agitators due to rapid industrialization and strong growth across key end-use industries in the region. Expanding chemical, pharmaceutical, food & beverage, and mining sectors in countries such as China, India, and Southeast Asian nations are significantly increasing demand for efficient mixing solutions. Rising investments in manufacturing infrastructure, coupled with favorable government policies and industrial development initiatives, are further accelerating market growth. Additionally, the shift of global production bases to the region and the presence of cost-competitive local manufacturers are enhancing market penetration. Increasing focus on process efficiency, energy optimization, and large-scale production capabilities continues to support the strong growth trajectory of the Asia Pacific market.

Breakdown of primaries

A variety of executives from key organizations operating in the industrial agitators market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 -40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level Executives - 48%, Directors - 33%, and Others - 19%

- By Region: North America - 35%, Europe - 18, Asia Pacific - 40%, and Rest of the World (RoW) - 7%

Note: The RoW region includes the Middle East, Africa, and South America. Other designations include product, sales, and marketing managers. Three tiers of companies have been defined based on their total revenues: tier 3: revenue less than USD 100 million; tier 2: revenue between USD 100 million and USD 1 billion; and tier 1: revenue more than USD 1 billion.

Major players profiled in this report: Major players operating in the industrial agitators market include SPX FLOW (US), Xylem (US), EKATO Holding GmbH (Germany), NOV (US), Suzler (Switzerland), Ingersoll Rand (US), Dynamix Agitators (Canada), Mixer Direct (US), Silverson (UK), Statifio Group (UK), and Tacmia Corporation (Japan).

These companies compete by continuously enhancing industrial agitator performance, focusing on improved mixing efficiency, optimized impeller designs, higher energy efficiency, and the ability to handle complex and high-viscosity fluids across diverse applications. Strategic emphasis is placed on robust and customizable system designs, integration with automation and process control systems, and the development of application-specific solutions for industries such as chemical, pharmaceutical, food & beverage, mining, and water treatment. Market participants prioritize seamless integration with existing processing equipment, ensuring reliability, durability, and ease of maintenance. Strong focus is also placed on reducing operational costs, enhancing process consistency, and offering complete solutions combining equipment, engineering, and aftermarket services. Continued investments in advanced materials, digital monitoring technologies, energy-efficient motors, and collaborations with end users and engineering firms are expected to sustain competition and accelerate adoption across the global industrial agitators market.

The study provides a detailed competitive analysis of the key players in the industrial agitators market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the industrial agitators market presents a detailed analysis based on power rating, model type, component, mounting type, form, industry, and region. By power rating, the market is segmented into less than 50 HP, 50 HP to 200 HP, and more than 200 HP. By model type, it is segmented into large tank agitators, portable agitators, drum agitators, and others. By component, the market includes heads/power units, sealing systems, impellers, and others. By mounting type, it is segmented into top-mounted, side-mounted, and bottom-mounted agitators. By form, it includes solid-solid, solid-liquid, liquid-gas, and liquid-liquid mixtures. By industry, the market covers chemical, pharmaceutical, paints & coatings, mining, food & beverage, cosmetics, and others. The regional analysis includes North America, Europe, Asia Pacific, and the Rest of the World, enabling evaluation of demand patterns, growth drivers, and industry trends.

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the industrial agitators market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (Increasing need for efficient implementation of wastewater treatment practices, Rising demand for energy efficiency, flow maximization, rapid mixing, and waste reduction, Strong growth of process and manufacturing industries, Increasing demand for customized industrial agitators, Advancements in automation and smart technologies, Expansion of food & beverage industry and need for hygiene compliance), restraints (High cost of maintenance and repair, Lengthy lead times for custom equipment), opportunities (Growing use of mixing technologies in multiple applications, Integration of lot and data analytics for predictive maintenance), and challenges (Stringent government safety norms and product compliance standards, Emerging trend of agitators/mixer equipment leasing due to high cost or limited usage, Increasing competition from low-cost manufacturers) influencing the growth of the industrial agitators market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the industrial agitators market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the industrial agitators market across varied regions.

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the industrial agitators market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like SPX FLOW (US), Xylem (US), EKATO Holding GmbH (Germany), NOV (US), Suzler (Switzerland), Ingersoll Rand (US), Dynamix Agitators (Canada), Mixer Direct (US), Silverson (UK), Statifio Group (UK), Tacmia Corporation (Japan), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN INDUSTRIAL AGITATORS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL AGITATORS MARKET

- 3.2 INDUSTRIAL AGITATORS MARKET, BY MODEL TYPE

- 3.3 INDUSTRIAL AGITATORS MARKET, BY MOUNTING TYPE

- 3.4 INDUSTRIAL AGITATORS MARKET, BY FORM

- 3.5 INDUSTRIAL AGITATORS MARKET, BY COMPONENT

- 3.6 INDUSTRIAL AGITATORS MARKET, BY POWER RATING

- 3.7 INDUSTRIAL AGITATORS MARKET, BY INDUSTRY

- 3.8 INDUSTRIAL AGITATORS MARKET IN NORTH AMERICA, BY INDUSTRY AND COUNTRY

- 3.9 INDUSTRIAL AGITATORS MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising implementation of efficient wastewater treatment practices

- 4.2.1.2 Growing emphasis on energy optimization, waste reduction, and regulatory compliance

- 4.2.1.3 Thriving process and manufacturing industries

- 4.2.1.4 High demand for customization to meet specific process requirements

- 4.2.1.5 Rising deployment of automation and smart technologies

- 4.2.1.6 Increasing need for hygiene compliance and safety in food & beverages industry

- 4.2.2 RESTRAINTS

- 4.2.2.1 Elevated maintenance and repair costs

- 4.2.2.2 Lengthy lead times for custom equipment

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Mounting adoption of advanced mixing technologies in multiple applications

- 4.2.3.2 Rising integration of IoT and data analytics for predictive maintenance

- 4.2.3.3 Shifting preference toward modular and micro-factory manufacturing models

- 4.2.4 CHALLENGES

- 4.2.4.1 Stringent safety norms and product compliance standards

- 4.2.4.2 Emerging trend of agitator/mixer equipment leasing

- 4.2.4.3 Increasing competition from low-cost manufacturers

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL PHARMACEUTICALS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL FOOD & BEVERAGES INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF INDUSTRIAL AGITATORS OFFERED BY KEY PLAYERS, BY MOUNTING TYPE, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF INDUSTRIAL AGITATORS, BY REGION, 2021-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847982)

- 5.6.2 EXPORT SCENARIO (HS CODE 847982)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SULZER LTD IMPLEMENTS SCABA AGITATORS TO REDUCE EXPENSES AND MAINTAIN HIGH PROCESS RELIABILITY

- 5.10.2 SPX FLOW'S MMR PROGRAM REDUCES UNPLANNED DOWNTIME AND INCREASES PRODUCTIVITY BY MODERNIZING MIXERS

- 5.10.3 XYLEM HELPS MINING COMPANY ACHIEVE STABLE PRODUCTION AND SIMPLIFIED WASTE DISPOSAL USING FLYGT 4650 HARD IRON MIXERS

- 5.11 IMPACT OF US TARIFFS - INDUSTRIAL AGITATORS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 TURBINE AGITATORS

- 6.1.2 PADDLE AGITATORS

- 6.1.3 ANCHOR AND GATE AGITATORS

- 6.1.4 HELICAL RIBBON AND SCREW AGITATORS

- 6.1.5 HIGH SHEAR MIXERS AND DISPERSERS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.2.2 IOT AND SMART SENSORS

- 6.2.3 DIGITAL TWINS AND SIMULATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 MIXING AND BLENDING SYSTEMS

- 6.3.2 HEAT TRANSFER AND JACKETED VESSELS

- 6.3.3 PROCESS AUTOMATION AND CONTROL

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON INDUSTRIAL AGITATORS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS IN INDUSTRIAL AGITATORS MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN INDUSTRIAL AGITATORS MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED INDUSTRIAL AGITATORS

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 IEC TS 62832-1: 2020

- 7.1.2.2 ISO/IEC TR 63306-1:2020

- 7.1.2.3 ISO 55001: 2014

- 7.1.2.4 ISO/IEC 21823-2

- 7.1.2.5 IEC 60870-5-101/104

- 7.1.2.6 IEC 61850

- 7.1.2.7 Distributed Network Protocol 3 (DNP3)

- 7.1.2.8 IEC 61508

- 7.1.3 REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 APPLICATIONS OF INDUSTRIAL AGITATORS

- 9.1 INTRODUCTION

- 9.2 HOMOGENIZATION

- 9.3 SUSPENSION

- 9.4 CRYSTALLIZATION

- 9.5 EMULSIFICATION

- 9.6 DISPERSION

- 9.7 NEUTRALIZATION

- 9.8 FERMENTATION

- 9.9 OTHER APPLICATIONS

10 DISTRIBUTION CHANNELS FOR INDUSTRIAL AGITATORS

- 10.1 INTRODUCTION

- 10.2 DIRECT

- 10.3 INDIRECT

11 MATERIALS USED IN INDUSTRIAL AGITATORS

- 11.1 INTRODUCTION

- 11.2 STAINLESS STEEL

- 11.3 HASTELLOY/HIGH-ALLOY METALS

- 11.4 TITANIUM

- 11.5 POLYPROPYLENE & POLYVINYLIDENE FLUORIDE

- 11.6 RUBBER-LINED & PTFE-COATED MATERIALS

- 11.7 DUPLEX & SUPER DUPLEX STEELS

12 INDUSTRIAL AGITATORS MARKET, BY POWER RATING

- 12.1 INTRODUCTION

- 12.2 LESS THAN 50 HP

- 12.2.1 ENERGY EFFICIENCY, SCALABILITY, AND ABILITY TO WITHSTAND CHALLENGING INDUSTRIAL ENVIRONMENTS TO SPUR DEMAND

- 12.3 50-100 HP

- 12.3.1 OPTIMIZED MIXING PERFORMANCE AND ENERGY CONSUMPTION IN LARGE-SCALE OPERATIONS TO FUEL SEGMENTAL GROWTH

- 12.4 MORE THAN 100 HP

- 12.4.1 HIGH-TORQUE REQUIREMENTS FOR MASSIVE TANKS IN GOLD AND COPPER EXTRACTION TO AUGMENT SEGMENTAL GROWTH

13 INDUSTRIAL AGITATORS MARKET, BY MODEL TYPE

- 13.1 INTRODUCTION

- 13.2 PORTABLE AGITATORS

- 13.2.1 FOCUS ON MEETING RAPID DEPLOYMENT AND DURABILITY REQUIREMENTS TO BOLSTER SEGMENTAL GROWTH

- 13.3 LARGE TANK AGITATORS

- 13.3.1 ABILITY TO SUPPORT CONTINUOUS OPERATION UNDER HEAVY LOADS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 13.4 DRUM AGITATORS

- 13.4.1 REQUIREMENT FOR QUALITY CONTROL DEVICES TO ENSURE PRODUCT UNIFORMITY TO FUEL SEGMENTAL GROWTH

- 13.5 OTHER MODELS

14 INDUSTRIAL AGITATORS MARKET, BY COMPONENT

- 14.1 INTRODUCTION

- 14.2 HEADS

- 14.2.1 ABILITY TO FACILITATE COMPLIANCE WITH REGULATORY STANDARDS FOR PRODUCT PURITY AND CONSISTENCY TO DRIVE MARKET

- 14.3 SEALING SYSTEMS

- 14.3.1 USE TO PREVENT LEAKAGE OF HAZARDOUS MATERIALS DURING MIXING OPERATIONS TO EXPEDITE SEGMENTAL GROWTH

- 14.4 IMPELLERS

- 14.4.1 DEMAND FOR APPLICATION-SPECIFIC AND EFFICIENT TECHNOLOGIES TO AUGMENT SEGMENTAL GROWTH

- 14.5 OTHER COMPONENTS

15 INDUSTRIAL AGITATORS MARKET, BY MOUNTING TYPE

- 15.1 INTRODUCTION

- 15.2 TOP-MOUNTED

- 15.2.1 HIGH PROCESS RELIABILITY, EFFICIENCY, LOW OPERATING COSTS, AND MINIMAL ENVIRONMENTAL STRESS TO BOOST SEGMENTAL GROWTH

- 15.3 SIDE-MOUNTED

- 15.3.1 INCREASING USE FOR LARGE-SCALE STORAGE OF LOW-VISCOSITY LIQUIDS TO ACCELERATE SEGMENTAL GROWTH

- 15.4 BOTTOM-MOUNTED

- 15.4.1 LIGHTWEIGHT AND EASE OF INSTALLATION AND OPERATION TO CONTRIBUTE TO SEGMENTAL GROWTH

16 INDUSTRIAL AGITATORS MARKET, BY FORM

- 16.1 INTRODUCTION

- 16.2 SOLID-SOLID MIXTURE

- 16.2.1 ABILITY TO ENHANCE BATCH CONSISTENCY, PRODUCTION THROUGHPUT, AND OPERATIONAL SAFETY TO SPUR DEMAND

- 16.3 SOLID-LIQUID MIXTURE

- 16.3.1 NEED TO PREVENT QUALITY VARIATION, LOSS OF RAW MATERIALS, AND IMPROPER HOMOGENEITY TO FOSTER SEGMENTAL GROWTH

- 16.4 LIQUID-GAS MIXTURE

- 16.4.1 HIGH EMPHASIS ON DECARBONIZATION AND RESOURCE EFFICIENCY TO ACCELERATE SEGMENTAL GROWTH

- 16.5 LIQUID-LIQUID MIXTURE

- 16.5.1 LIGHTWEIGHT AND CONVENIENCE IN MIXING OPERATIONS TO EXPEDITE SEGMENTAL GROWTH

17 INDUSTRIAL AGITATORS MARKET, BY INDUSTRY

- 17.1 INTRODUCTION

- 17.2 CHEMICALS & PETROCHEMICALS

- 17.2.1 OIL & GAS

- 17.2.1.1 Use to maintain viscosity, specific gravity, and chemical composition to bolster segmental growth

- 17.2.1.2 Emulsification

- 17.2.1.3 Crude oil processing

- 17.2.1.4 Liquid & gas blending

- 17.2.1.5 Gas dispersion & absorption

- 17.2.2 PETROCHEMICALS

- 17.2.2.1 Need to maintain stability and reaction efficiency of complex hydrocarbon mixtures to augment segmental growth

- 17.2.2.2 Blending

- 17.2.2.3 Desulfurization

- 17.2.2.4 Heat transfer

- 17.2.3 WATER & WASTEWATER TREATMENT

- 17.2.3.1 Requirement for continuous processes enabling fluid homogenization and pollutant removal to drive market

- 17.2.3.2 Gas dispersion & absorption

- 17.2.3.3 Washing & leaching

- 17.2.1 OIL & GAS

- 17.3 MINING

- 17.3.1 FOCUS ON MINIMIZING EROSION AND MATERIAL WEAR FROM MINERAL RECOVERY AND REFINING PROJECTS TO FUEL SEGMENTAL GROWTH

- 17.3.2 LEACHING

- 17.3.3 SLURRY MIXING

- 17.3.4 ORE BENEFICIATION

- 17.3.5 FLOTATION

- 17.3.6 CYANIDATION

- 17.3.7 PRECIPITATION

- 17.3.8 CARBON-IN-PULP (CIP) & CARBON-IN-LEACH (CIL) PROCESSES

- 17.4 FOOD & BEVERAGES

- 17.4.1 ABILITY TO MAINTAIN HIGH VOLUME PRODUCTION AND ADHERE TO STRICT SAFETY STANDARDS TO EXPEDITE SEGMENTAL GROWTH

- 17.4.2 MIXING & BLENDING

- 17.4.3 FERMENTATION

- 17.4.4 HOMOGENIZATION

- 17.4.5 DISSOLVING SUGAR & SALTS

- 17.4.6 AERATION

- 17.4.7 FLAVORING & ADDITIVE MIXING

- 17.5 PHARMACEUTICALS

- 17.5.1 FOCUS ON REDUCING RISKS AND ACCELERATING TIME-TO-MARKET FOR NEW DRUG FORMULATIONS TO FUEL SEGMENTAL GROWTH

- 17.5.2 ACTIVE PHARMACEUTICAL INGREDIENT PROCESSING

- 17.5.3 LIQUID DOSAGE FORM PREPARATION

- 17.5.4 VACCINE PRODUCTION

- 17.5.5 ANTIBIOTIC PRODUCTION

- 17.5.6 CONTROLLED RELEASE FORMULATION

- 17.5.7 STERILE MIXING

- 17.6 COSMETICS

- 17.6.1 ABILITY TO CREATE ULTRA-FINE PARTICLE DISPERSIONS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 17.6.2 COLORANT DISPERSION

- 17.6.3 AEROSOL PROPELLANT MIXING

- 17.6.4 VISCOSITY CONTROL

- 17.6.5 SUSPENSION OF SOLID INGREDIENTS

- 17.6.6 COSMETIC INGREDIENT ACTIVATION

- 17.6.7 TOPICAL FORMULATION MIXING

- 17.6.8 FILLING & PACKAGING ASSISTANCE

- 17.7 PAINTS & COATINGS

- 17.7.1 EMPHASIS ON HIGH CONSISTENCY AND DIGITAL PRECISION TO BOOST SEGMENTAL GROWTH

- 17.7.2 EMULSION FORMATION

- 17.7.3 VISCOSITY CONTROL

- 17.7.4 POLYMERIZATION

- 17.7.5 SOLVENT MIXING

- 17.7.6 FILLER INCORPORATION

- 17.7.7 POWDER COATING MIXING

- 17.7.8 SPRAY COATING PREPARATION

- 17.7.9 PAINT RECYCLING

- 17.7.10 CHEMICAL REACTION MANAGEMENT

- 17.7.11 BATCH MIXING

- 17.7.12 ADDITIVE MIXING

- 17.8 OTHER INDUSTRIES

18 INDUSTRIAL AGITATORS MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 18.2.2 US

- 18.2.2.1 Increasing export of chemical products to accelerate market growth

- 18.2.3 CANADA

- 18.2.3.1 Expanding petrochemical manufacturing facility and oil and gas processing to drive market

- 18.2.4 MEXICO

- 18.2.4.1 Mounting demand for materials supporting critical industrial manufacturing processes to foster market growth

- 18.3 EUROPE

- 18.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 18.3.2 UK

- 18.3.2.1 Increasing investment in chemical and pharmaceutical R&D to expedite market growth

- 18.3.3 GERMANY

- 18.3.3.1 Growing emphasis on wastewater and sustainable water management to contribute to market growth

- 18.3.4 FRANCE

- 18.3.4.1 Strong presence of coal mines and hydroelectricity to bolster market growth

- 18.3.5 ITALY

- 18.3.5.1 High emphasis on meeting strict climate neutrality targets to fuel market growth

- 18.3.6 REST OF EUROPE

- 18.4 ASIA PACIFIC

- 18.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 18.4.2 CHINA

- 18.4.2.1 Rising production and export of rare metals to expedite market growth

- 18.4.3 JAPAN

- 18.4.3.1 Increasing investment in advanced manufacturing technologies to boost market growth

- 18.4.4 INDIA

- 18.4.4.1 High availability of raw materials and industrial resources to accelerate market growth

- 18.4.5 REST OF ASIA PACIFIC

- 18.5 ROW

- 18.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 18.5.2 SOUTH AMERICA

- 18.5.2.1 Rising import of agricultural goods and demand for advanced processing systems to drive market

- 18.5.3 MIDDLE EAST

- 18.5.3.1 Increasing extraction and refining of petroleum to bolster market growth

- 18.5.3.2 GCC

- 18.5.3.3 Rest of Middle East

- 18.5.4 AFRICA

- 18.5.4.1 Rapid industrialization and focus on enhancing processing and refining capabilities to foster market growth

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 19.3 REVENUE ANALYSIS, 2021-2025

- 19.4 MARKET SHARE ANALYSIS, 2025

- 19.5 COMPANY VALUATION AND FINANCIAL METRICS

- 19.6 BRAND/PRODUCT COMPARISON

- 19.6.1 EKATO (GERMANY)

- 19.6.2 SPX FLOW (US)

- 19.6.3 XYLEM INC. (US)

- 19.6.4 SULZER LTD (SWITZERLAND)

- 19.6.5 NOV INC. (US)

- 19.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 19.7.5.1 Company footprint

- 19.7.5.2 Region footprint

- 19.7.5.3 Power rating footprint

- 19.7.5.4 Model type footprint

- 19.7.5.5 Component footprint

- 19.7.5.6 Mounting type footprint

- 19.7.5.7 Industry footprint

- 19.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 19.8.1 PROGRESSIVE COMPANIES

- 19.8.2 RESPONSIVE COMPANIES

- 19.8.3 DYNAMIC COMPANIES

- 19.8.4 STARTING BLOCKS

- 19.8.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2025

- 19.8.5.1 Detailed list of key startups/SMEs

- 19.8.5.2 Competitive benchmarking of key startups/SMEs

- 19.9 COMPETITIVE SCENARIO

- 19.9.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 19.9.2 DEALS

- 19.9.3 EXPANSIONS

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- 20.1.1 SPX FLOW

- 20.1.1.1 Business overview

- 20.1.1.2 Products/Solutions/Services offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches/enhancements

- 20.1.1.3.2 Deals

- 20.1.1.3.3 Expansions

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths/Right to win

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses/Competitive threats

- 20.1.2 XYLEM

- 20.1.2.1 Business overview

- 20.1.2.2 Products/Solutions/Services offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Deals

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths/Right to win

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses/Competitive threats

- 20.1.3 EKATO HOLDING GMBH

- 20.1.3.1 Business overview

- 20.1.3.2 Products/Solutions/Services offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Deals

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths/Right to win

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses/Competitive threats

- 20.1.4 NOV

- 20.1.4.1 Business overview

- 20.1.4.2 Products/Solutions/Services offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Product launches/enhancements

- 20.1.4.3.2 Deals

- 20.1.4.3.3 Expansions

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths/Right to win

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses/Competitive threats

- 20.1.5 SULZER LTD

- 20.1.5.1 Business overview

- 20.1.5.2 Products/Solutions/Services offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Product launches/enhancements

- 20.1.5.3.2 Deals

- 20.1.5.3.3 Expansions

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths/Right to win

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses/Competitive threats

- 20.1.6 INGERSOLL RAND

- 20.1.6.1 Business overview

- 20.1.6.2 Products/Solutions/Services offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches/enhancements

- 20.1.6.3.2 Deals

- 20.1.6.4 MnM view

- 20.1.6.4.1 Key strengths/Right to win

- 20.1.6.4.2 Strategic choices

- 20.1.6.4.3 Weaknesses/Competitive threats

- 20.1.7 DYNAMIX AGITATORS INC.

- 20.1.7.1 Business overview

- 20.1.7.2 Products/Solutions/Services offered

- 20.1.8 MIXER DIRECT

- 20.1.8.1 Business overview

- 20.1.8.2 Products/Solutions/Services offered

- 20.1.9 SILVERSON

- 20.1.9.1 Business overview

- 20.1.9.2 Products/Solutions/Services offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Product launches/enhancements

- 20.1.10 STATIFLO GROUP

- 20.1.10.1 Business overview

- 20.1.10.2 Products/Solutions/Services offered

- 20.1.11 TACMINA CORPORATION

- 20.1.11.1 Business overview

- 20.1.11.2 Products/Services/Solutions offered

- 20.1.1 SPX FLOW

- 20.2 OTHER PLAYERS

- 20.2.1 ALFA LAVAL

- 20.2.2 DE DIETRICH SAS

- 20.2.3 EUROMIXERS LTD

- 20.2.4 FAWCETT CO., INC.

- 20.2.5 MIXEL AGITATEURS

- 20.2.6 PRG GMBH

- 20.2.7 PROQUIP INC.

- 20.2.8 SAVINO BARBERA SRL

- 20.2.9 SHARPE MIXERS

- 20.2.10 SHUANGLONG GROUP CO., LTD.

- 20.2.11 SUMA RUHRTECHNIK GMBH

- 20.2.12 TERALBA INDUSTRIES

- 20.2.13 TIMSA

- 20.2.14 WOODMAN AGITATOR

- 20.2.15 ZHEJIANG GREATWALL MIXERS CO.

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY AND PRIMARY RESEARCH

- 21.1.2 SECONDARY DATA

- 21.1.2.1 List of key secondary sources

- 21.1.2.2 Key data from secondary sources

- 21.1.3 PRIMARY DATA

- 21.1.3.1 List of primary interview participants

- 21.1.3.2 Breakdown of primary interviews

- 21.1.3.3 Key data from primary sources

- 21.1.3.4 Key industry insights

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 BOTTOM-UP APPROACH

- 21.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 21.2.2 TOP-DOWN APPROACH

- 21.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 21.2.1 BOTTOM-UP APPROACH

- 21.3 MARKET FORECAST APPROACH

- 21.3.1 SUPPLY SIDE

- 21.3.2 DEMAND SIDE

- 21.4 DATA TRIANGULATION

- 21.5 RESEARCH ASSUMPTIONS

- 21.6 RESEARCH LIMITATIONS

- 21.7 RISK ANALYSIS

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS