|

시장보고서

상품코드

2029871

OCP 랙 시장 예측(-2030년) : 최종사용자별, 용도별, 지역별OCP Rack Market By Application (AI, High-performance computing, Data Management, Enterprise Apps & Others), End User (Retail Colocation, Enterprise, Neocloud Providers, Others - Hyperscalers/Wholesale Colocation) - Global Forecast to 2030 |

||||||

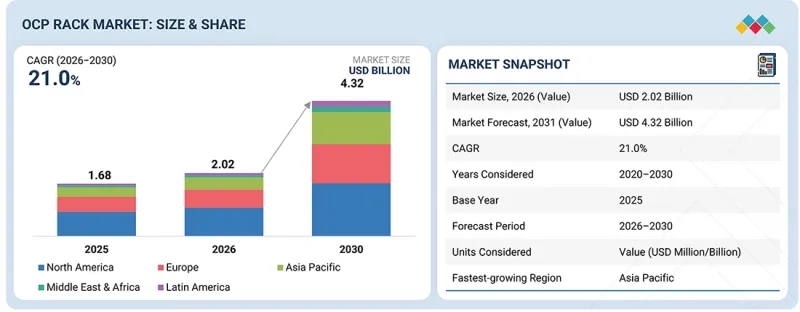

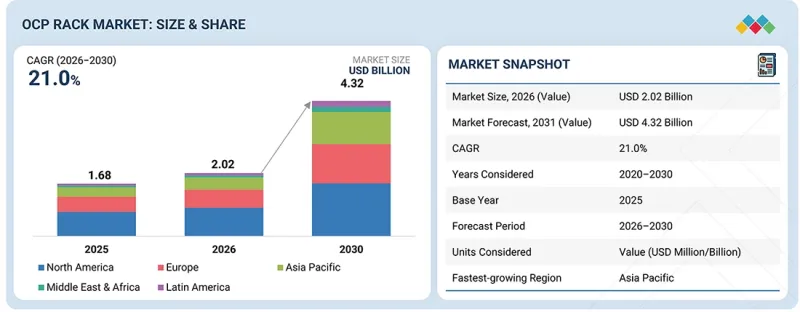

OCP 랙 시장 규모는 급속히 확대하고 있으며, 시장 규모는 2025년 16억 8,000만 달러에서 2030년까지 43억 2,000만 달러로, CAGR 21.0%로 성장할 것으로 예측됩니다.

데이터 처리가 최종사용자와 디바이스에 가까워짐에 따라 엣지 컴퓨팅의 확장은 OCP 랙 시장의 뚜렷한 촉진요인으로 부상하고 있습니다. 엣지 시설은 일반적으로 공간의 제약이 있고, 컴팩트하고 효율적이며 쉽게 도입할 수 있는 인프라를 필요로 합니다. Open Compute Project에서 개발된 OCP 랙의 설계는 단순화된 기계 구조, 모듈식 구성 및 효율적인 전력 분배를 통해 이러한 요구 사항을 충족합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2030년 |

| 대상 단위 | 금액(100만/10억 달러) |

| 부문 | 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카 및 라틴아메리카 |

대규모 하이퍼스케일 환경과 달리 엣지 환경 도입 시에는 신속한 설치와 분산된 여러 거점에서의 일관된 운영이 중요하게 고려되는 경우가 많습니다. OCP 기반 랙은 최소한의 커스터마이징으로 복제 가능한 표준화된 설계를 구현하여 도입 기간과 통합의 복잡성을 줄여줍니다. 또한 더 작은 설치 공간에서 높은 컴퓨팅 밀도를 구현할 수 있다는 점은 공간과 전력 공급이 제한적인 엣지 환경의 요구사항에 부합합니다. 통신, 컨텐츠 전송, 산업용 애플리케이션 등 엣지 사용 사례가 확대됨에 따라 유연하고 확장 가능한 랙 솔루션에 대한 수요가 증가하면서 OCP 아키텍처의 채택이 확대될 것으로 예상됩니다.

"용도별로 보면 예측 기간 중 시장에서 두 번째로 높은 성장률을 보일 것으로 예상되는 분야는 고성능 컴퓨팅(HPC)입니다. "

고성능 컴퓨팅(HPC)은 연구, 기업 및 산업 사용 사례에서 컴퓨팅 집약적인 워크로드에 대한 수요 증가에 힘입어 OCP 랙 시장에서 두 번째로 빠르게 성장하는 애플리케이션이 될 것으로 예측됩니다. HPC 환경은 높은 전력 밀도, 저 지연 네트워크, 효율적인 열 관리를 갖춘 긴밀하게 통합된 시스템을 요구합니다. OCP 랙 아키텍처는 더 높은 랙 전력 용량을 지원하고 액체 냉각을 포함한 고급 냉각 솔루션을 가능하게 함으로써 이러한 요구 사항을 충족합니다. 이를 통해 운영자는 시설의 제약 없이 고밀도 컴퓨팅 클러스터를 구축할 수 있습니다. 또한 HPC 워크로드에는 반복성과 확장성을 갖춘 인프라 설계가 필요한 경우가 많으며, 이는 OCP 랙의 표준화된 접근 방식과 일치합니다. 조직이 시뮬레이션, 모델링 및 AI 지원 컴퓨팅 기능을 확장함에 따라 효율적이고 확장 가능한 HPC 인프라에 대한 요구가 증가하고 있으며, 이는 OCP 기반 랙 시스템 도입을 가속화하고 있습니다.

"최종사용자별로 보면 예측 기간 중 '기타' 부문이 가장 큰 시장 규모를 차지할 것으로 예상됩니다. "

하이퍼스케일러와 홀세일 코로케이션 제공업체로 구성된 '기타' 부문은 인프라 구축 규모와 표준화로 인해 OCP 랙 시장에서 가장 큰 시장 규모를 차지할 것으로 예상됩니다. 이들 사업자들은 통일되고 재현 가능한 아키텍처를 전제로 대규모 데이터센터 캠퍼스를 구축 및 운영하고 있으며, Open Compute Project 표준을 준수하는 OCP 랙은 효율성과 확장성 측면에서 분명한 이점을 제공합니다. 하이퍼스케일러는 특히 AI 및 클라우드 서비스를 위한 고밀도 워크로드를 지원하기 위해 OCP 기반 시스템을 도입하고 있으며, 홀세일 코로케이션 제공업체는 대규모 테넌트의 요구사항을 충족하기 위해 유사한 설계를 채택하고 있습니다. 대용량 전력 공급 및 액체 냉각 인프라를 포함한 맞춤형 시설 설계에 대한 투자 능력도 OCP의 채택을 더욱 촉진하고 있습니다. 또한 이러한 플레이어들은 일반적으로 장기적인 계획 기간과 많은 자본 예산을 가지고 사업을 운영하고 있으며, 새로운 랙 아키텍처를 조기에 도입할 수 있습니다. 이러한 규모, 표준화, 인프라 구축의 시너지 효과로 인해 이 부문은 OCP 랙 수요의 가장 큰 견인차 역할을 하고 있습니다.

"예측 기간 중 OCP 랙 시장을 주도하는 것은 북미 지역입니다. "

북미는 하이퍼스케일 용량 집중, 개방형 하드웨어 표준의 조기 채택, AI 인프라에 대한 지속적인 투자로 인해 OCP 랙 시장에서 가장 큰 시장 규모를 차지할 것으로 예상됩니다. 이 지역에는 대규모 클라우드 제공업체를 비롯해 OCP(Open Compute Project) 생태계의 주요 기여자들이 존재하며, 이들은 OCP 기반 아키텍처를 대규모로 설계 및 배포하고 있습니다. 이들 사업자들은 이미 인프라의 상당 부분을 21인치 오픈 랙 설계로 전환하여 높은 전력 밀도, 효율적인 열 관리, 그리고 여러 캠퍼스에서 표준화된 배포를 가능하게 하고 있습니다.

AI 훈련 및 추론 클러스터의 급속한 확장이 시장을 주도하고 있습니다. 이는 특히 액체 냉각 및 대용량 부스바 시스템의 채택이 증가함에 따라 전력 공급 및 냉각을 위한 랙 레벨의 최적화가 필요하기 때문입니다. 이와 함께 북미의 홀세일 코로케이션 제공업체들이 하이퍼스케일 테넌트를 지원하기 위해 신규 시설 건설을 OCP 요구사항에 맞추면서 수요가 더욱 강화되고 있습니다. 또한 이 지역에서는 컴퓨팅, 네트워크, 냉각을 개별 구성요소가 아닌 미리 통합된 시스템으로 도입하는 '랙 스케일 통합'의 진전도 계속되고 있습니다. 이를 통해 도입 기간을 단축하고 운영상의 복잡성을 줄일 수 있습니다. OEM, ODM, 인프라 벤더를 아우르는 강력한 공급망과 함께 이러한 요인들은 북미를 OCP 랙 도입의 주요 시장으로 자리매김하고 있습니다.

이 보고서에는 OCP 랙 시장에서 사업을 운영하는 주요 기업에 관한 상세한 조사가 포함되어 있습니다. 본 조사에서 다루어진 주요 시장 참여 기업에는 Rittal(독일), Dell Technologies(미국), Sanmina Corporation(미국), Legrand(프랑스), Vertiv(미국), Eaton(아일랜드), Belden(미국), Wiwynn Corporation(대만), Lite-on Cloud Infrastructure(대만), Cheval Group, Gigabyte(대만), Chatsworth Product(미국) 등이 포함됩니다.

조사 범위

OCP 랙 시장을 용도별(AI(트레이닝 및 추론), 고성능 컴퓨팅(HPC), 데이터 관리, 기업 애플리케이션 및 기타), 최종사용자별(소매 코로케이션 제공업체, 기업, 클라우드 제공업체, 기타(하이퍼스케일러/홀세일 코로케이션 제공업체)), 지역별(북미, 유럽, 아시아태평양, 중동 및 기타(하이퍼스케일러/홀세일 코로케이션 제공업체)), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)로 분류하고 있습니다.

이 보고서의 범위에는 OCP 랙 시장의 성장에 영향을 미치는 주요 요인(동인, 제약, 도전 과제, 기회 등)에 대한 자세한 인사이트가 포함되어 있습니다. 또한 주요 벤더의 제품 포트폴리오, 랙 스케일 기능 및 OCP(Open Compute Project)가 정의한 표준 준수 여부에 대한 포괄적인 분석을 제공합니다. 또한 하이퍼스케일러 및 ODM과의 파트너십, OCP 생태계 전반의 협력, 랙 설계의 제품 혁신, 전력 및 냉각 통합과 같은 전략적 노력과 더불어, OCP 랙 시장의 시장 상황에 영향을 미치는 인수합병 및 최근 동향에 대해서도 살펴봅니다. 검증하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 OCP 랙 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 인사이트를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 자사 제품 및 서비스를 보다 효과적으로 포지셔닝하고, 효과적인 시장 진입 전략을 수립할 수 있는 실용적인 인사이트를 얻을 수 있습니다. 또한 이 보고서는 OCP 랙 시장을 형성하는 주요 촉진요인, 저해요인, 과제 및 기회에 대한 상세한 분석을 제공하여 이해 관계자가 시장 동향과 역학을 평가하는 데 도움이 될 것입니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 이 보고서는 OCP 랙 시장을 형성하는 주요 촉진요인, 제약 요인, 기회 및 과제에 대한 인사이트를 제공합니다. 주요 촉진요인으로는 OCP 채택을 촉진하는 AI 랙의 전력 밀도 향상, 컴포넌트 레벨 도입을 대체하는 랙 스케일 통합 인프라, 하이퍼스케일러가 주도하는 표준화된 다른 세계의 OCP 채택 가속화 등을 들 수 있습니다. 제약 요인으로는 기존 19인치 랙 인프라와의 호환성이 낮고, 시설의 전력 및 냉각 시스템에서 초기 재설계 비용이 높다는 점을 들 수 있습니다. 기회로는 랙 설계에 액체 냉각(D2C 및 액침냉각) 통합, 하이퍼스케일 및 네오 클라우드 사업자를 위한 AI 지원 사전 구성된 랙 솔루션 등을 들 수 있습니다. 주요 과제로는 멀티 벤더 OCP 생태계의 상호운용성 문제와 도입 효율성에 영향을 미치는 레거시 시스템의 복잡성을 꼽을 수 있습니다.

- 서비스 개발 및 혁신: OCP 랙 시장의 향후 기술, R&D 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발 : 수익성 높은 시장에 대한 포괄적 인 정보 -이 보고서는 다양한 지역의 OCP 랙 시장을 분석합니다.

- 시장 다각화: OCP 랙 시장의 새로운 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보

- 경쟁 분석 : Rittal(독일), Dell Technologies(미국), Sanmina Corporation(미국), Legrand(프랑스), Vertiv(미국), Eaton(아일랜드), Belden(미국), Wiwynn Corporation(대만), Lite-on Cloud Infrastructure(대만), Cheval Group, Gigabyte(대만), Chatsworth Product(미국) 등 주요 기업의 시장 점유율, 성장 전략, OCP 랙 제품에 대한 상세한 평가. 또한 이 보고서는 주요 시장 촉진요인, 제약 조건, 과제 및 기회에 대한 정보를 제공함으로써 이해 관계자가 OCP 랙 시장을 이해하는 데 도움이 될 것입니다.

자주 묻는 질문

목차

제1장 서론

제2장 시장 개요

제3장 21 인치 OCP 랙 시장(최종사용자별)

제4장 21 인치 OCP 랙 시장(용도별)

제5장 21 인치 OCP 랙 시장(지역별)

제6장 기업 개요

KSA 26.05.21The OCP rack market is expanding rapidly, with the market projected to grow from USD 1.68 billion in 2025 to USD 4.32 billion by 2030, at a CAGR of 21.0%. The expansion of edge computing is emerging as a distinct driver for the OCP rack market, as data processing increasingly shifts closer to end users and devices. Edge facilities are typically space-constrained and require compact, efficient, and easily deployable infrastructure. OCP rack designs, developed under the Open Compute Project, support these requirements through simplified mechanical structures, modular configurations, and efficient power distribution.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2025 |

| Forecast Period | 2026-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Application, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America |

Unlike large hyperscale environments, edge deployments often prioritize rapid installation and operational consistency across multiple distributed sites. OCP-based racks enable standardized designs that can be replicated with minimal customization, reducing deployment time and integration complexity. In addition, the ability to support higher compute density within a smaller footprint aligns with edge requirements where real estate and power availability are limited. As edge use cases expand across telecom, content delivery, and industrial applications, demand for flexible and scalable rack solutions is expected to support increased adoption of OCP architectures.

"By application, the high-performance computing (HPC) is projected to be the second-fastest-growing in the market during the forecast period."

High-performance computing (HPC) is projected to be the second fastest-growing application in the OCP rack market, supported by increasing demand for compute-intensive workloads across research, enterprise, and industrial use cases. HPC environments require tightly integrated systems with high power density, low-latency networking, and efficient thermal management. OCP rack architectures address these requirements by supporting higher rack power capacities and enabling advanced cooling solutions, including liquid cooling. This allows operators to deploy dense compute clusters without exceeding facility constraints. In addition, HPC workloads often require repeatable and scalable infrastructure designs, which aligns with the standardized approach of OCP racks. As organizations expand simulation, modeling, and AI-assisted computing capabilities, the need for efficient and scalable HPC infrastructure is increasing, contributing to the accelerated adoption of OCP-based rack systems.

"By end user, the others segment is expected to hold the largest market value during the forecast period."

The "others" segment, comprising hyperscalers and wholesale colocation providers, is expected to hold the largest market value in the OCP rack market due to the scale and standardization of their infrastructure deployments. These operators build and operate large data center campuses designed for uniform, repeatable architectures, where OCP racks aligned with Open Compute Project standards provide clear advantages in terms of efficiency and scalability. Hyperscalers deploy OCP-based systems to support high-density workloads, particularly for AI and cloud services, while wholesale colocation providers adopt similar designs to meet the requirements of large tenants. Their ability to invest in custom facility design, including high-capacity power and liquid cooling infrastructure, further supports OCP adoption. Additionally, these players typically operate with long planning horizons and large capital budgets, enabling early adoption of new rack architectures. This combination of scale, standardization, and infrastructure readiness positions the segment as the largest contributor to OCP rack demand.

"North America leads the OCP rack market during the forecast."

North America is expected to hold the largest market value in the OCP rack market due to its concentration of hyperscale capacity, early adoption of open hardware standards, and continued investment in AI infrastructure. The region hosts major contributors to the Open Compute Project ecosystem, including large cloud providers that design and deploy OCP-based architectures at scale. These operators have already transitioned significant portions of their infrastructure to 21-inch Open Rack designs, enabling higher power density, efficient thermal management, and standardized deployments across multiple campuses.

The rapid expansion of AI training and inference clusters is driving the market as it requires rack-level optimization for power delivery and cooling, particularly with the increasing adoption of liquid cooling and high-capacity busbar systems. In parallel, wholesale colocation providers in North America are aligning new facility builds with OCP requirements to support hyperscale tenants, further reinforcing demand. The region is also seeing continued advancement in rack-scale integration, where compute, networking, and cooling are deployed as pre-integrated systems rather than discrete components. This reduces deployment timelines and operational complexity. Combined with strong supply chain presence across OEMs, ODMs, and infrastructure vendors, these factors position North America as the leading market for OCP rack deployments.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the OCP rack market.

- By Company: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: Directors - 35%, Managers - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 45%, Asia Pacific - 25%, Middle East & Africa - 3%, and Latin America - 2%.

The report includes a detailed study of key players operating in the OCP rack market. The major market participants covered in the study include Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US).

Research Coverage

This research report categorizes the OCP rack market based on applications By Applications (AI (training & inference), high performance computing (HPC), data management and enterprise apps & others)), By end users (retail colocation providers, enterprise, necloud providers and others (hyperscalers/ wholesale colocation providers) and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope encompasses detailed insights into the key factors influencing the OCP rack market, including drivers, restraints, challenges, and opportunities shaping its growth. It provides a comprehensive analysis of leading vendors, covering their product portfolios, rack-scale capabilities, and alignment with standards defined by the Open Compute Project. The report also examines strategic initiatives such as partnerships with hyperscalers and ODMs, collaborations across the OCP ecosystem, product innovations in rack design, power and cooling integration, as well as mergers, acquisitions, and recent developments impacting the OCP rack market landscape.

Reason to Buy this Report

The report provides market leaders and new entrants with insights into the closest estimations of revenue for the overall OCP rack market and its subsegments. It enables stakeholders to understand the competitive landscape and gain actionable insights to better position their offerings and develop effective go-to-market strategies. Additionally, the report helps stakeholders assess market trends and dynamics by providing a detailed analysis of key drivers, restraints, challenges, and opportunities shaping the OCP rack market.

The report provides insights into the following points:

- The report provides insights into key drivers, restraints, opportunities, and challenges shaping the OCP rack market. Major drivers include AI rack power density exceeding driving OCP adoption, rack-scale integrated infrastructure replacing component-level deployments, and hyperscaler-led standardization accelerating global OCP adoption. Restraints include limited compatibility with legacy 19-inch rack infrastructure and high upfront redesign costs for facility power and cooling systems. Opportunities include integration of liquid cooling (D2C and immersion) within rack designs, pre-configured AI-ready rack solutions for hyperscale and neo-cloud players. Key challenges include interoperability issues in multi-vendor OCP ecosystems and legacy system complexity impacting deployment efficiency.

- Services Development/Innovation: Detailed insight into upcoming technologies, research & development activities, and new product & service launches in the OCP rack market

- Market Development: Comprehensive information about lucrative markets - the report analyses the OCP rack market across varied regions

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the OCP rack market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and OCP rack offerings of leading players such as Rittal (Germany), Dell Technologies (US), Sanmina Corporation (US), Legrand (France), Vertiv (US), Eaton (Ireland), Belden (US), Wiwynn Corporation (Taiwan), Lite-on Cloud Infrastructure (Taiwan), Cheval Group, Gigabyte (Taiwan), and Chatsworth Product (US). The report also helps stakeholders understand the OCP rack market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

2 MARKET OVERVIEW

- 2.1 INTRODUCTION

- 2.2 MARKET DYNAMICS

- 2.2.1 DRIVERS

- 2.2.1.1 Adoption in high-density data center environments driven by AI rack power density

- 2.2.1.2 Rack-scale integration across high-density deployments

- 2.2.1.3 Hyperscale standardization

- 2.2.2 RESTRAINTS

- 2.2.2.1 Legacy 19-inch infrastructure limits broader OCP rack adoption in existing data centers

- 2.2.2.2 High facility redesign costs constrain OCP rack adoption in retrofit data center environments

- 2.2.3 OPPORTUNITIES

- 2.2.3.1 Liquid cooling integration to improve adoption opportunity in high-density AI infrastructure

- 2.2.3.2 Pre-configured AI rack systems among hyperscale and neocloud operators

- 2.2.4 CHALLENGES

- 2.2.4.1 Multi-vendor interoperability gaps increase deployment complexity in OCP environments

- 2.2.4.2 Thermal constraints at ultra-high rack densities challenge OCP scalability

- 2.2.1 DRIVERS

- 2.3 CASE STUDY ANALYSIS

- 2.3.1 MODERNIZED ENTERPRISE INFRASTRUCTURE WITH OCP-BASED PRIVATE CLOUD DEPLOYMENT

- 2.3.2 REDUCED DATA CENTER COST AND IMPROVED FLEXIBILITY WITH OPEN BRIDGE RACK ADOPTION

- 2.3.3 STRENGTHENED SCALABLE PRIVATE CLOUD DELIVERY WITH OCP-BASED INTEGRATED INFRASTRUCTURE

- 2.4 ANALYSIS: DOES RISING RACK POWER DENSITY STRUCTURALLY REDUCE RACK COUNTS?

- 2.5 ANALYSIS OF KW EVOLUTION OF 21" OCP RACKS BY 2030

- 2.5.1 LEGACY TO EARLY OCP FOUNDATION (PRE-2015 -> 2020 | 5-15 KW)

- 2.5.2 PHASE 2: CLOUD SCALING & EARLY AI TRANSITION (2020 -> 2023 | 15-40 KW)

- 2.5.3 PHASE 3: STANDARDIZED HIGH-DENSITY ORV3 ERA (2023 -> 2025 | 50-130 KW)

- 2.5.4 PHASE 4: ORV3 STRETCH PHASE (2025 -> 2026 | 130-200 KW+)

- 2.5.5 PHASE 5: TRANSITION TO HIGH-VOLTAGE ARCHITECTURES (2027 -> 2028 | 200-500 KW)

- 2.5.6 PHASE 6: ULTRA-HIGH-DENSITY AI RACKS (2028 -> 2030 | 500 KW-1 MW)

- 2.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 2.7 PRICING ANALYSIS

- 2.7.1 AVERAGE SELLING PRICE

- 2.7.2 INDICATIVE PRICING, BY VENDOR

3 21-INCH OCP RACK MARKET, BY END USER

- 3.1 INTRODUCTION

- 3.1.1 21 INCH OCP RACK, BY END USER: MARKET DRIVERS

- 3.2 RETAIL COLOCATION PROVIDERS

- 3.2.1 ABILITY TO SUPPORT HIGH-DENSITY DEPLOYMENTS IN SHARED DATA CENTER ENVIRONMENTS TO PROPEL GROWTH

- 3.3 ENTERPRISE (ON-PREMISES)

- 3.3.1 DRIVING ENTERPRISE INFRASTRUCTURE TRANSFORMATION THROUGH OCP ADOPTION TO FUEL GROWTH

- 3.4 NEOCLOUD PROVIDERS

- 3.4.1 ACCELERATING NEOCLOUD GROWTH THROUGH MODULAR OCP INFRASTRUCTURE TO DRIVE ADOPTION

- 3.5 OTHER END USERS

4 21-INCH OCP RACK MARKET, BY APPLICATION

- 4.1 INTRODUCTION

- 4.1.1 21 INCH OCP RACK, BY APPLICATION: MARKET DRIVERS

- 4.2 AI (TRAINING & INFERENCES)

- 4.2.1 ENABLING AI-SCALE TRAINING WITH HIGH-DENSITY OCP RACK ARCHITECTURES TO DRIVE GROWTH

- 4.3 HIGH-PERFORMANCE COMPUTING (HPC)

- 4.3.1 ENHANCING HPC EFFICIENCY WITH ADVANCED COOLING AND POWER SYSTEMS TO PROPEL GROWTH

- 4.4 DATA MANAGEMENT

- 4.4.1 SUPPORTING REAL-TIME DATA PROCESSING WITH OCP RACK SOLUTIONS TO DRIVE ADOPTION

- 4.5 ENTERPRISE APPS AND OTHERS

5 21-INCH OCP RACK MARKET, BY REGION

- 5.1 INTRODUCTION

- 5.2 NORTH AMERICA

- 5.2.1 US

- 5.2.1.1 Accelerating OCP rack adoption through hyperscale and AI expansion to boost market growth

- 5.2.2 CANADA

- 5.2.2.1 Growing emphasis on building scalable AI infrastructure through ecosystem collaboration to support market growth

- 5.2.1 US

- 5.3 EUROPE

- 5.3.1 UK

- 5.3.1.1 Enabling high-density AI workloads through 21-inch OCP rack deployments to propel growth

- 5.3.2 GERMANY

- 5.3.2.1 Leveraging OCP architectures to support liquid cooling and higher rack powers

- 5.3.3 FRANCE

- 5.3.3.1 Supporting gigawatt-scale AI data centers with high-density rack architectures to fuel growth

- 5.3.4 ITALY

- 5.3.4.1 Expanding data center investments to support OCP rack adoption in Italy

- 5.3.5 SPAIN

- 5.3.5.1 Increase in hyperscale activity, including large AI-focused deployments, to drive demand for high-density and scalable infrastructure

- 5.3.6 REST OF EUROPE

- 5.3.1 UK

- 5.4 ASIA PACIFIC

- 5.4.1 CHINA

- 5.4.1.1 Public cloud expansion supporting open rack deployment to propel growth

- 5.4.2 JAPAN

- 5.4.2.1 Japan strengthens OCP rack adoption through AI infrastructure design

- 5.4.3 INDIA

- 5.4.3.1 India supports OCP rack adoption through local infrastructure demand

- 5.4.4 REST OF ASIA PACIFIC

- 5.4.1 CHINA

- 5.5 MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.5.1.1 Saudi Arabia

- 5.5.1.1.1 Saudi data center expansion to drive OCP rack demand

- 5.5.1.2 UAE

- 5.5.1.2.1 UAE hyperscale growth to increase OCP adoption potential

- 5.5.1.3 Rest of GCC

- 5.5.1.1 Saudi Arabia

- 5.5.2 SOUTH AFRICA

- 5.5.2.1 Improving rack power density and cooling efficiency with OCP designs to drive growth

- 5.5.3 REST OF MIDDLE EAST & AFRICA

- 5.5.1 GCC

- 5.6 LATIN AMERICA

- 5.6.1 BRAZIL

- 5.6.1.1 Brazil to strengthen open infrastructure with domestic OCP manufacturing

- 5.6.2 MEXICO

- 5.6.2.1 Mexico to standardize next-generation rack infrastructure for AI workloads

- 5.6.3 REST OF LATIN AMERICA

- 5.6.1 BRAZIL

6 COMPANY PROFILES

- 6.1 INTRODUCTION

- 6.2 KEY PLAYERS

- 6.2.1 SANMINA CORPORATION

- 6.2.1.1 Business overview

- 6.2.1.2 Products/Solutions/Services offered

- 6.2.1.3 Recent developments

- 6.2.1.3.1 Product launches and enhancements

- 6.2.1.3.2 Deals

- 6.2.1.4 MnM view

- 6.2.1.4.1 Right to win

- 6.2.1.4.2 Strategic choices

- 6.2.1.4.3 Weaknesses and competitive threats

- 6.2.2 DELL TECHNOLOGIES

- 6.2.2.1 Business overview

- 6.2.2.2 Products/Solutions/Services offered

- 6.2.2.2.1 Product launches and enhancements

- 6.2.2.3 MnM view

- 6.2.2.3.1 Right to win

- 6.2.2.3.2 Strategic choices

- 6.2.2.3.3 Weaknesses and competitive threats

- 6.2.3 WIWYNN

- 6.2.3.1 Business overview

- 6.2.3.2 Products/Solutions/Services offered

- 6.2.3.3 Recent developments

- 6.2.3.3.1 Product launches and enhancements

- 6.2.3.3.2 Deals

- 6.2.3.4 MnM view

- 6.2.3.4.1 Right to win

- 6.2.3.4.2 Strategic choices

- 6.2.3.4.3 Weaknesses and competitive threats

- 6.2.4 GIGABYTE

- 6.2.4.1 Business overview

- 6.2.4.2 Products/Solutions/Services offered

- 6.2.4.3 Recent developments

- 6.2.4.3.1 Product launches and enhancements

- 6.2.4.4 MnM view

- 6.2.4.4.1 Right to win

- 6.2.4.4.2 Strategic choices

- 6.2.4.4.3 Weaknesses and competitive threats

- 6.2.5 EATON

- 6.2.5.1 Business overview

- 6.2.5.2 Products/Solutions/Services offered

- 6.2.5.3 Recent developments

- 6.2.5.3.1 Product launches and enhancements

- 6.2.5.4 MnM view

- 6.2.5.4.1 Right to win

- 6.2.5.4.2 Strategic choices

- 6.2.5.4.3 Weaknesses and competitive threats

- 6.2.6 RITTAL

- 6.2.6.1 Business overview

- 6.2.6.2 Products/Solutions/Services offered

- 6.2.6.3 Recent developments

- 6.2.6.3.1 Product launches and enhancements

- 6.2.6.3.2 Deals

- 6.2.7 LEGRAND

- 6.2.7.1 Business overview

- 6.2.7.2 Products/Solutions/Services offered

- 6.2.7.3 Recent developments

- 6.2.7.3.1 Product launches and enhancements

- 6.2.8 RACK RENEW

- 6.2.8.1 Business overview

- 6.2.8.2 Products/Solutions/Services offered

- 6.2.8.3 Recent developments

- 6.2.8.3.1 Product launches and enhancements

- 6.2.9 BELDEN

- 6.2.9.1 Business overview

- 6.2.9.2 Products/Solutions/Services offered

- 6.2.10 CHEVAL GROUP

- 6.2.10.1 Business overview

- 6.2.10.2 Products/Solutions/Services offered

- 6.2.1 SANMINA CORPORATION