|

시장보고서

상품코드

2029905

메틸 메타크릴레이트계 접착제 시장 예측(-2030년) : 기재별, 경화 속도별, 시스템 유형별, 최종 용도 산업별, 지역별Methyl Methacrylate Adhesives Market by System Type, Substrate, Cure Speed, End-use Industry, and Region - Global Forecast to 2030 |

||||||

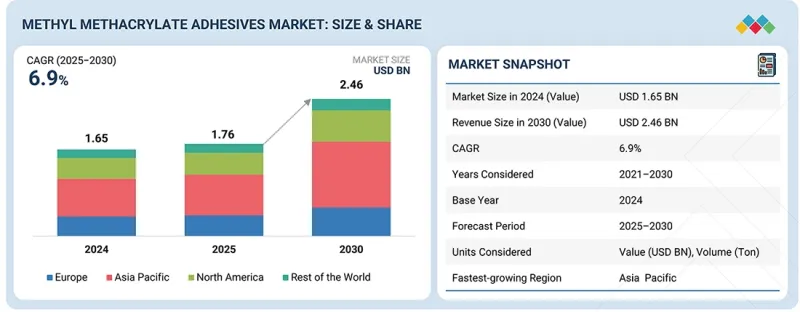

세계의 메틸 메타크릴레이트계 접착제 시장 규모는 2025년 17억 6,000만 달러에서 2030년까지 24억 6,000만 달러로 성장하며, 예측 기간 중 CAGR 6.9%를 기록할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 산정 단위 | 금액(100만/10억 달러), 톤 |

| 부문 | 기재별, 경화 속도별, 시스템 유형별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 세계의 기타 지역 |

메틸 메타크릴레이트계 접착제 시장은 최근 수년간 지속적으로 성장하고 있습니다. 이는 주로 고강도, 내구성, 빠른 경화형 접착제에 대한 수요 증가에 기인합니다. 자동차, 풍력발전, 건설, 선박 등 다양한 분야에서 다용도한 구조물에 경량 소재를 사용하는 추세가 강화되고 있는 것이 메틸메타크릴레이트계 접착제의 성장에 기여하고 있습니다. 메틸 메타크릴레이트계 접착제는 금속, 복합재료, 플라스틱에 우수한 접착력을 나타내며, 표면처리를 최소화할 수 있습니다. 전기자동차 및 풍력 터빈 블레이드 제조를 포함한 재생에너지 기술 개발도 메틸 메타크릴레이트계 접착제 시장의 성장에 기여하고 있습니다. 또한 건축 및 건설 분야에서도 메틸 메타크릴레이트계 접착제에 대한 수요가 증가하고 있습니다. 아시아태평양은 메틸 메타크릴레이트 접착제 시장 성장의 주요 견인차 역할을 하고 있습니다. 이는 주로 아시아태평양의 급속한 산업화에 기인합니다.

"시스템 유형별로는 2액형 프리믹스(2K) 부문이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

2액형 프리믹스(2K) 시스템은 까다로운 산업 응용 분야에서 성능, 신뢰성 및 사용 편의성의 최적의 균형을 제공함으로써 메틸 메타크릴레이트 접착제 시장을 독점하고 있습니다. 2K 시스템은 노맥스 활성화제계 접착제 시스템이나 UV/광경화형 아크릴계 접착제 시스템과 달리 수지와 경화제 간의 화학반응 과정이 빛이나 표면 활성화 등의 환경적 요인에 영향을 받지 않고 진행되므로 신뢰성 높은 경화를 실현합니다. 2액형 프리믹스(2K) 시스템은 금속, 복합재료, 플라스틱 등 다양한 표면에 사용할 수 있으며, 폭넓은 적응성을 보여줍니다. 이 시스템은 강력한 구조적 접착력을 생성하고 우수한 틈새 충진 성능과 높은 내충격성을 제공하므로 자동차, 건설, 선박 산업에 적합합니다. 프리믹스 포장을 통해 작업자는 실수를 줄이고 작업을 완료할 수 있습니다. 2액형 프리믹스(2K)는 내구성, 높은 생산성, 그리고 간편한 시공 공정을 제공할 수 있다는 장점으로 인해 제조업체들의 선택을 받아 세계 시장에서 선도적인 위치를 차지하고 있습니다.

최종 사용 산업별로는 육상 운송(자동차, 트럭, 철도, 버스) 부문이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

육상운송(자동차, 트럭, 철도, 버스) 부문은 메틸 메타크릴레이트계 접착제 시장에서 가장 큰 점유율을 차지했습니다. 이는 가볍고 견고한 영구 접착 솔루션에 대한 수요가 높기 때문입니다. 자동차, 상업용 트럭, 철도 운송 등의 산업에서 기존의 기계식 패스너나 용접을 대체할 수 있는 메틸 메타크릴레이트 접착제에 대한 의존도가 높아지고 있습니다. 이 접착제는 강한 충격으로부터 완벽하게 보호하고 반복적인 사이클에도 강도를 유지하여 지속적인 진동과 가혹한 작동 조건에 노출되는 차량에 이상적입니다. 메틸 메타크릴레이트 접착제를 사용하면 생산 공정이 빨라지고 생산 비용이 절감되는 동시에 현대적인 디자인 옵션이 가능합니다.

"아시아태평양은 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

아시아태평양은 메틸 메타크릴레이트계 접착제의 가장 큰 시장입니다. 이 지역은 탄탄한 제조 인프라와 급속한 산업화로 인해 메틸 메타크릴레이트 접착제 산업에서 엄청난 성장 기회를 제공하고 있습니다. 아시아태평양에서 메틸 메타크릴레이트 접착제 시장의 성장에 기여하는 주요 국가는 중국, 인도, 일본, 그리고 한국입니다. 이 지역의 각국에서는 자동차, 건설, 선박, 풍력발전, 전자기기 등 다양한 산업에서 메틸메타크릴레이트계 접착제에 대한 수요가 증가하고 있습니다. 메틸 메타크릴레이트계 접착제는 우수한 접착 강도, 빠른 접착 시간, 그리고 금속, 플라스틱, 복합재료 등 다양한 재료를 접착할 수 있는 특성으로 인해 널리 사용되고 있습니다. 아시아태평양은 세계 최고의 자동차 산업 거점 중 하나입니다. 이 지역에서는 메틸 메타크릴레이트계 접착제가 경량화 접착 및 구조용 접착에 사용되고 있습니다. 도시화의 진전, 생활수준의 향상, 중산층의 증가로 인해 주거 및 상업용 건축에 대한 수요가 증가하고 있습니다.

메틸 메타크릴레이트 접착제 시장은 3M(미국), Henkel AG & Co. KGaA(독일), H.B. Fuller Company(미국), IPS Corporation(미국), Illinois Tool Works Inc.(미국), Scott Bader Company Ltd.(영국), Huntsman International LLC(미국), Bostik(프랑스), Sika AG(스위스), PARKER HANNIFIN CORP.(US) 등의 주요 기업으로 구성되어 있습니다. 메틸 메타크릴레이트계 접착제 시장의 주요 기업에 대해 기업 개요, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시했습니다.

조사 범위

이 보고서는 메틸 메타크릴레이트 접착제 시장을 시스템 유형, 최종 사용 산업, 기판, 경화 속도, 지역별로 세분화하여 각 지역의 전체 시장 규모를 추정합니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 메틸 메타크릴레이트 접착제 시장과 관련된 사업 개요, 제품 및 서비스, 주요 전략, 사업 확장에 대한 인사이트를 제공합니다.

이 보고서 구매의 주요 이점

이 보고서는 산업 분석(업계 동향), 주요 기업 시장 순위 분석, 기업 개요 등 다각적인 분석에 중점을 두었으며, 이를 종합하여 경쟁 구도, 메틸 메타크릴레이트 접착제 시장의 신흥 및 고성장 부문, 고성장 지역, 시장 촉진요인, 제약요인, 기회, 과제 등을 파악할 수 있도록 했습니다. 시장 촉진요인, 제약요인, 기회, 도전과제를 파악할 수 있습니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 촉진요인 분석:(경량화 및 다재료 접착에 대한 수요, 기존 접착제 시스템 대비 우수한 성능, 재생에너지 도입 가속화에 따른 고성능 메틸 메타크릴레이트 접착제 수요 확대), 제약 요인(도입 장벽 및 운영상의 복잡성, 가격에 민감한 시장에서 메틸 메타크릴레이트 접착제 채택을 제한하는 높은 비용), 기회(전기자동차 및 배터리 시스템의 급속한 확대, 복합재 적용 확대), 도전 과제(시장 상용화를 지연시키는 성능 표준화 및 인증 요건) 가격 민감 시장에서 메틸 메타크릴레이트 접착제의 채택을 제한하는 높은 비용), 기회(전기자동차 및 배터리 시스템의 급속한 확대, 복합재료 응용분야의 확대), 도전과제(시장 상용화를 지연시키는 성능 표준화 및 인증 요건)가 메틸 메타크릴레이트 접착제 시장 성장에 미치는 영향

- 시장 침투: 글로벌 메틸 메타크릴레이트 접착제 시장의 주요 업체들이 제공하는 제품에 대한 종합적인 정보를 제공합니다.

- 제품 개발 및 혁신: 메틸 메타크릴레이트 접착제 시장의 향후 기술 동향, 신제품 출시, 사업 확장 및 인수합병에 대한 상세 분석

- 시장 개발: 수익성 높은 신흥 시장에 대한 종합적인 정보. 이 보고서에서는 지역별 메틸 메타크릴레이트계 접착제 시장을 분석합니다.

- 시장 생산능력: 메틸 메타크릴레이트계 접착제 시장내 각 기업의 생산능력(가용 범위) 및 향후 생산능력 전망

- 경쟁 분석: 메틸 메타크릴레이트 접착제 시장 주요 기업의 시장 점유율, 전략, 제품, 제조 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 메틸 메타크릴레이트계 접착제 시장(기재별)

제10장 메틸 메타크릴레이트계 접착제 시장(경화 속도별)

제11장 메틸 메타크릴레이트계 접착제 시장(시스템 유형별)

제12장 메틸 메타크릴레이트계 접착제 시장(최종 용도 산업별)

제13장 메틸 메타크릴레이트계 접착제 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

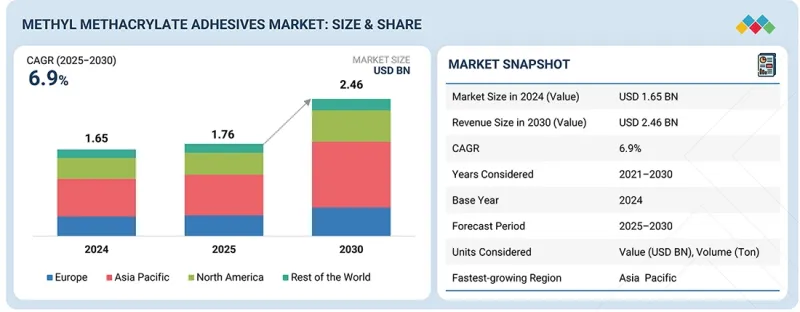

KSA 26.05.21The global methyl methacrylate adhesives market is projected to grow from USD 1.76 billion in 2025 to USD 2.46 billion by 2030, registering a CAGR of 6.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Ton) |

| Segments | Substrate, System Type, Cure Speed, End-use Industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Rest of the World |

The methyl methacrylate adhesives market has been witnessing growth in recent years. This is mainly due to the increasing demand for high-strength, durable, and fast-curing adhesives. The increasing trend of using lightweight materials in multi-material constructions in various sectors, including automotive, wind energy, construction, and marine, is contributing to the growth of methyl methacrylate adhesives. Methyl methacrylate adhesives have good bonding properties with metals, composites, and plastics with low surface preparation. The development of electric vehicles and renewable energy technologies, including wind turbine blade manufacturing, is also contributing to the growth of methyl methacrylate adhesives. The demand for methyl methacrylate adhesives is also increasing in the building & construction sectors. Asia Pacific is the major contributor to the growth of the methyl methacrylate adhesives market. This is mainly due to the rapid industrialization in Asia Pacific.

"By system type, the two-part pre-mix (2K) segment is anticipated to account for the largest market share during the forecast period."

The two-part pre-mix (2K) system dominates the methyl methacrylate adhesives market as it delivers the best balance of performance, reliability, and ease of use for demanding industrial applications. 2K systems provide reliable curing as their chemical reaction process between resin and hardener develops independently from environmental factors such as light and surface activation, unlike the no-mix activator adhesive system and UV/light-cure acrylic adhesive system. Two-part pre-mix (2K) system shows extensive adaptability as it can be used on various surfaces, such as metals, composites, and plastics. This system type serves perfectly for automotive, construction, and marine industries as they create strong structural bonds and provides excellent gap-filling performance and high impact resistance. Pre-mixed packaging enables workers to complete their tasks with fewer mistakes. Two-part pre-mix (2K) continues to dominate the global market as manufacturers choose it for their ability to provide durability, high productivity, and straightforward application processes.

By end-use industry, the land transport (auto, truck, rail, bus) segment is anticipated to account for the largest market share during the forecast period.

The land transport (auto, truck, rail, bus) segment accounted for the largest share of the methyl methacrylate adhesives market. This is attributed to the high demand for their lightweight and strong permanent adhesive solutions. Industries such as the automotive, commercial trucking, and rail transport increasingly rely on methyl methacrylate adhesives to replace traditional mechanical fasteners and welding. These adhesives provide complete protection against strong impacts while sustaining their strength through multiple cycles, which makes them ideal for vehicles that undergo continuous vibrations and intense operational demands. The use of methyl methacrylate adhesives leads to quicker production processes together with decreased production expenses, while enabling contemporary design options.

"Asia Pacific is anticipated to account for the largest market share during the forecast period.

Asia Pacific is the largest market for methyl methacrylate adhesives. The region offers immense growth opportunities in the methyl methacrylate adhesive industry because of the presence of robust manufacturing infrastructure and rapid industrialization. In the Asia Pacific region, the key countries that contribute to the growth of the methyl methacrylate adhesive market are China, India, Japan, and South Korea. Countries in this region have a high demand for methyl methacrylate adhesives in various industries, such as the automotive, construction, marine, wind energy, and electronics. Methyl methacrylate adhesives are widely used because of the superior bonding strength, quick bonding time, and the ability of the product to bond different materials such as metals, plastics, and composite materials. The Asia Pacific region is one of the largest automotive hubs in the world. In this region, methyl methacrylate adhesives are used in lightweight bonding and structural bonding. The rise in urbanization and the growth in the standard of living and middle-class population have led to an increase in demand for residential and commercial construction.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the methyl methacrylate adhesives market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers - 15%, Directors - 20%, and Others - 65%

- By Region: North America - 30%, Europe - 25%, Asia Pacific - 35%, Rest of the World - 15%

The methyl methacrylate adhesives market comprises of major companies, such as 3M (US), Henkel AG & Co. KGaA (Germany), H.B. Fuller Company (US), IPS Corporation (US), Illinois Tool Works Inc. (US), Scott Bader Company Ltd. (UK), Huntsman International LLC (US), Bostik (France), Sika AG (Switzerland), and PARKER HANNIFIN CORP. (US). The study includes in-depth competitive analysis of these key players in the methyl methacrylate adhesives market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for methyl methacrylate adhesives market on the basis of system type, end-use industry, substrate, cure speed, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the methyl methacrylate adhesives market.

Key benefits of buying this report

This research report is focused on various levels of analysis-industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the methyl methacrylate adhesives market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following points:

- Analysis of Drivers: (Lightweighting & multi-material bonding demand, superior performance compared to conventional adhesive systems, Accelerating renewable energy deployment driving demand for high-performance methyl methacrylate adhesives), restraints (Adoption barriers and operational complexity, High cost of methyl methacrylate adhesives limiting adoption in price-sensitive markets), opportunities (Rapid expansion of electrical vehicles and battery systems, Expansion in composite applications), and challenges (Performance standardization and certification requirements delaying market commercialization) influencing the growth of methyl methacrylate adhesives market

- Market Penetration: Comprehensive information on the methyl methacrylate adhesives offered by top players in the global methyl methacrylate adhesives market

- Product Development/Innovation: Detailed insights on upcoming technologies, product launches, expansions, and acquisitions in the methyl methacrylate adhesives market

- Market Development: Comprehensive information about lucrative emerging markets, the report analyzes the markets for methyl methacrylate adhesives across regions.

- Market Capacity: Production capacity of the companies is provided wherever available with upcoming capacities for the methyl methacrylate adhesives market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the methyl methacrylate adhesives market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METHYL METHACRYLATE ADHESIVES MARKET

- 3.2 METHYL METHACRYLATE ADHESIVES MARKET, BY SUBSTRATE AND REGION

- 3.3 METHYL METHACRYLATE ADHESIVES MARKET, BY SYSTEM TYPE

- 3.4 METHYL METHACRYLATE ADHESIVES MARKET, BY CURE SPEED

- 3.5 METHYL METHACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY

- 3.6 METHYL METHACRYLATE ADHESIVES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Lightweighting & multi-material bonding demand

- 4.2.1.2 Superior performance to conventional adhesive systems

- 4.2.1.3 Accelerating renewable energy deployment

- 4.2.2 RESTRAINTS

- 4.2.2.1 Adoption barriers and operational complexity

- 4.2.2.2 High cost limiting adoption in price-sensitive markets

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid expansion of electric vehicles and battery systems

- 4.2.3.2 Expansion in composite applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Performance standardization and certification requirements delaying commercialization

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN METHYL METHACRYLATE ADHESIVES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS (2022-2025)

- 5.4.1 AVERAGE SELLING PRICE TREND OF METHYL METHACRYLATE ADHESIVES, BY REGION (2022-2025)

- 5.4.2 AVERAGE SELLING PRICE TREND OF METHYL METHACRYLATE ADHESIVES, BY SYSTEM TYPE (2022-2025)

- 5.4.3 AVERAGE SELLING PRICE TREND OF METHYL METHACRYLATE ADHESIVES, BY CURE SPEED (2022-2025)

- 5.4.4 AVERAGE SELLING PRICE TREND OF METHYL METHACRYLATE ADHESIVES, BY SUBSTRATE (2022-2025)

- 5.4.5 AVERAGE SELLING PRICE TREND OF METHYL METHACRYLATE ADHESIVES, BY END-USE INDUSTRY (2022-2025)

- 5.4.6 AVERAGE SELLING PRICE OF METHYL METHACRYLATE ADHESIVES AMONG KEY PLAYERS, BY SYSTEM TYPE, 2025

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 291614)

- 5.6.2 EXPORT SCENARIO (HS CODE 291614)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ENABLING ADVANCED STRUCTURAL BONDING SOLUTIONS THROUGH METHYL METHACRYLATE ADHESIVE TECHNOLOGIES

- 5.10.2 ENABLING ENERGY-EFFICIENT BUILDINGS THROUGH METHYL METHACRYLATE ADHESIVE-BASED STRUCTURAL AND PREFABRICATED ASSEMBLIES

- 5.10.3 STRENGTHENING ELECTRONICS DURABILITY AND THERMAL MANAGEMENT THROUGH METHYL METHACRYLATE ADHESIVE-BASED SOLUTIONS

- 5.11 IMPACT OF 2025 US TARIFF - METHYL METHACRYLATE ADHESIVES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 FAST-CURING METHYL METHACRYLATE ADHESIVES (3-10 MIN)

- 6.1.2 HIGH TEMPERATURE RESISTANCE (>150°C)

- 6.1.3 LOW-EMISSION AND SUSTAINABLE METHYL METHACRYLATE ADHESIVES

- 6.1.4 NANOTECHNOLOGY-ENHANCED METHYL METHACRYLATE ADHESIVES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SURFACE TREATMENT AND PRIMER TECHNOLOGIES

- 6.2.2 AUTOMATED DISPENSING AND APPLICATION SYSTEMS

- 6.2.3 CURE MONITORING AND NONDESTRUCTIVE TESTING (NDT) TOOLS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 UV-CURABLE AND LIGHT-ACTIVATED ADHESIVE TECHNOLOGIES

- 6.3.2 HIGH-PERFORMANCE STRUCTURAL EPOXY ADHESIVES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM ROADMAP: PROCESS OPTIMIZATION AND COST RATIONALIZATION

- 6.4.2 MID-TERM ROADMAP: CUSTOMIZATION, APPLICATION-SPECIFIC FORMULATIONS, AND SUSTAINABILITY INTEGRATION

- 6.4.3 LONG-TERM ROADMAP: ADVANCED PERFORMANCE AND SUSTAINABILITY ENABLEMENT

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 GRANTED PATENTS, 2016-2025

- 6.5.2.1 Publication trends for last ten years

- 6.5.3 INSIGHTS

- 6.5.4 LEGAL STATUS

- 6.5.5 JURISDICTION ANALYSIS

- 6.5.6 TOP APPLICANTS

- 6.5.7 LIST OF MAJOR PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 STRUCTURAL BODY BONDING & BATTERY ENCLOSURE ASSEMBLY IN AUTOMOTIVE & EVS

- 6.6.2 FRP PANEL BONDING & STRUCTURAL REINFORCEMENT IN CONSTRUCTION & INFRASTRUCTURE

- 6.6.3 COMPOSITE TURBINE BLADE BONDING & REPAIR IN WIND ENERGY

- 6.6.4 METAL PANEL BONDING & STRUCTURAL ASSEMBLY IN RAIL AND INDUSTRIAL EQUIPMENT

- 6.7 IMPACT OF AI/GEN AI ON METHYL METHACRYLATE ADHESIVES MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN METHYL METHACRYLATE ADHESIVES MANUFACTURING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN METHYL METHACRYLATE ADHESIVES MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN METHYL METHACRYLATE ADHESIVES MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 3M (U.S.): ADVANCED METHYL METHACRYLATE ADHESIVE SOLUTIONS FOR MULTI-MATERIAL BONDING

- 6.8.2 HENKEL AG & CO. KGAA (GERMANY): HIGH-PERFORMANCE METHYL METHACRYLATE ADHESIVES FOR AUTOMOTIVE AND INDUSTRIAL APPLICATIONS

- 6.8.3 SIKA AG (SWITZERLAND): METHYL METHACRYLATE ADHESIVES FOR CONSTRUCTION AND INFRASTRUCTURE APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF METHYL METHACRYLATE ADHESIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRY

- 8.5 MARKET PROFITABILITY

- 8.5.1 VALUE ADDITION AND FUNCTIONAL PREMIUMS

- 8.5.2 FEEDSTOCK AND COST STRUCTURE SENSITIVITY

- 8.5.3 SCALE, CUSTOMIZATION, AND OPERATING LEVERAGE

- 8.5.4 CUSTOMER LOCK-IN AND SWITCHING COSTS

9 METHYL METHACRYLATE ADHESIVES MARKET, BY SUBSTRATE

- 9.1 INTRODUCTION

- 9.2 METALS (STEEL, AL, SS)

- 9.2.1 INCREASING SHIFT FROM WELDING TO ADHESIVE BONDING IN METAL STRUCTURES DRIVING DEMAND

- 9.3 THERMOSET COMPOSITES (FRP/CRP/GRP)

- 9.3.1 RISING ADOPTION OF LIGHTWEIGHT COMPOSITE MATERIALS BOOSTING DEMAND

- 9.4 STANDARD THERMOPLASTICS (ABS, PC, PVC)

- 9.4.1 INCREASING USE OF THERMOPLASTICS IN MULTI-MATERIAL ASSEMBLIES INCREASING ADOPTION

- 9.5 ENGINEERING PLASTICS/LSE (NYLON, PP, PE, TPO)

- 9.5.1 GROWING USE OF LOW SURFACE ENERGY PLASTICS IS INCREASING DEMAND FOR ADVANCED MMA ADHESIVE FORMULATIONS.

- 9.6 CERAMICS/MAGNETS/GLASS

- 9.6.1 RISING DEMAND FOR HIGH-PERFORMANCE BONDING IN ELECTRONICS AND ENERGY SYSTEMS DRIVING DEMAND

10 METHYL METHACRYLATE ADHESIVES MARKET, BY CURE SPEED

- 10.1 INTRODUCTION

- 10.2 ULTRA-FAST (< 3 MIN)

- 10.2.1 INCREASING DEMAND FOR HIGH-THROUGHPUT MANUFACTURING ACCELERATING ADOPTION OF ULTRA-FAST CURING METHYL METHACRYLATE ADHESIVES

- 10.3 FAST (3-10 MIN)

- 10.3.1 NEED FOR BALANCED WORKING TIME AND PRODUCTIVITY DRIVING WIDESPREAD ADOPTION OF FAST-CURING METHYL METHACRYLATE ADHESIVES

- 10.4 EXTENDED (15-60 MIN)

- 10.4.1 INCREASING USE OF LARGE AND COMPLEX ASSEMBLIES BOOSTING DEMAND FOR EXTENDED-CURE METHYL METHACRYLATE ADHESIVES

- 10.5 UV/LIGHT-CURE (1-PART, 1-5 MIN)

- 10.5.1 RISING DEMAND FOR PRECISION BONDING IN ELECTRONICS AND MEDICAL DEVICES DRIVING ADOPTION OF UV/LIGHT-CURE METHYL METHACRYLATE ADHESIVES

11 METHYL METHACRYLATE ADHESIVES MARKET, BY SYSTEM TYPE

- 11.1 INTRODUCTION

- 11.2 TWO-PART PRE-MIX (2K)

- 11.2.1 HIGH DEMAND FOR RELIABLE, HIGH-STRENGTH STRUCTURAL BONDING DRIVING WIDESPREAD ADOPTION OF 2K MMA ADHESIVE SYSTEMS

- 11.3 NO-MIX/ACTIVATOR

- 11.3.1 NEED FOR SIMPLE, EQUIPMENT-FREE BONDING SOLUTIONS ACCELERATING ADOPTION OF NO-MIX MMA ADHESIVE SYSTEMS

- 11.4 UV/LIGHT-CURE ACRYLIC

- 11.4.1 INCREASING DEMAND FOR PRECISION AND CLEAN PROCESSING IN HIGH-TECH INDUSTRIES DRIVING ADOPTION OF UV-CURE METHYL METHACRYLATE ADHESIVE SYSTEMS

12 METHYL METHACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 LAND TRANSPORT (AUTO, TRUCK, RAIL, BUS)

- 12.2.1 VEHICLE LIGHTWEIGHTING AND MULTI-MATERIAL DESIGN TRENDS DRIVING METHYL METHACRYLATE ADHESIVE ADOPTION IN TRANSPORTATION

- 12.3 MARINE (SHIPBUILDING + LEISURE BOATS)

- 12.3.1 DEMAND FOR CORROSION-RESISTANT BONDING IN COMPOSITE MARINE STRUCTURES BOOSTING DEMAND

- 12.4 RENEWABLE ENERGY (WIND, SOLAR FRAMES)

- 12.4.1 EXPANSION OF WIND AND SOLAR INFRASTRUCTURE DRIVING DEMAND FOR METHYL METHACRYLATE ADHESIVES IN ENERGY SYSTEMS

- 12.5 CONSTRUCTION (PANELS, FACADES, GLAZING)

- 12.5.1 RISING ADOPTION OF PREFABRICATED AND MODULAR CONSTRUCTION IS ACCELERATING DEMAND

- 12.6 EV/NEW ENERGY (BATTERY, MOTOR, MAGNETS)

- 12.6.1 RAPID GROWTH OF ELECTRIC MOBILITY DRIVING DEMAND FOR METHYL METHACRYLATE ADHESIVES IN EV COMPONENTS

- 12.7 ELECTRONICS (DEVICES, ENCLOSURES, DISPLAYS)

- 12.7.1 INCREASING MINIATURIZATION AND COMPLEXITY OF ELECTRONIC DEVICES DRIVING METHYL METHACRYLATE ADHESIVE ADOPTION

- 12.8 AEROSPACE & DEFENSE (CERTIFIED GRADES)

- 12.8.1 INCREASING USE OF LIGHTWEIGHT COMPOSITES IN AEROSPACE BOOSTING DEMAND

- 12.9 MEDICAL DEVICES (ISO 10993-QUALIFIED)

- 12.9.1 GROWING DEMAND FOR BIOCOMPATIBLE AND RELIABLE BONDING SOLUTIONS DRIVING DEMAND IN MEDICAL DEVICES

- 12.10 GENERAL INDUSTRIAL/MRO

- 12.10.1 INCREASING FOCUS ON MAINTENANCE EFFICIENCY AND EQUIPMENT LONGEVITY DRIVING METHYL METHACRYLATE ADHESIVE ADOPTION

13 METHYL METHACRYLATE ADHESIVES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Massive growth in EVs, renewable energy, and manufacturing driving large-scale demand

- 13.2.2 JAPAN

- 13.2.2.1 Advanced manufacturing and high-precision electronics sustaining demand

- 13.2.3 INDIA

- 13.2.3.1 Infrastructure expansion and manufacturing growth under government initiatives demand

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Semiconductor-driven manufacturing and offshore wind expansion supporting demand

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 NORTH AMERICA

- 13.3.1 US

- 13.3.1.1 Strong infrastructure spending and advanced manufacturing expansion accelerating demand

- 13.3.2 CANADA

- 13.3.2.1 Infrastructure investment and clean energy expansion driving methyl demand

- 13.3.3 MEXICO

- 13.3.3.1 Rapid nearshoring-led industrialization and automotive expansion fueling demand

- 13.3.1 US

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Energy transition and automotive lightweighting sustaining long-term demand

- 13.4.2 ITALY

- 13.4.2.1 Strong marine manufacturing and construction activity driving demand

- 13.4.3 FRANCE

- 13.4.3.1 Renewable energy expansion and aerospace-driven manufacturing fueling demand

- 13.4.4 UK

- 13.4.4.1 Offshore wind expansion and infrastructure development driving demand

- 13.4.5 SPAIN

- 13.4.5.1 Rapid renewable energy deployment and infrastructure investments driving demand

- 13.4.6 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Mega infrastructure projects and energy diversification under Vision 2030 driving demand

- 13.5.1.2 UAE

- 13.5.1.2.1 Infrastructure expansion and logistics hub development fueling demand

- 13.5.1.3 Rest of GCC Countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 Renewable energy expansion and automotive manufacturing supporting demand

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 ARGENTINA

- 13.6.1.1 Renewable energy development and automotive manufacturing supporting growth

- 13.6.2 BRAZIL

- 13.6.2.1 Renewable energy expansion and construction growth

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 ARGENTINA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS, 2025

- 14.3.1 HENKEL AG & CO. KGAA

- 14.3.2 3M

- 14.3.3 SIKA AG

- 14.3.4 H.B. FULLER COMPANY

- 14.3.5 ILLINOIS TOOL WORKS INC.

- 14.4 REVENUE ANALYSIS, 2021-2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 System type footprint

- 14.5.5.4 End-use industry footprint

- 14.5.5.5 Substrate footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of key startups/SMEs

- 14.7 PRODUCT COMPARISON

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 HENKEL AG & CO. KGAA

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 H.B. FULLER COMPANY

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 IPS CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 MnM view

- 15.1.3.3.1 Key strengths

- 15.1.3.3.2 Strategic choices

- 15.1.3.3.3 Weaknesses and competitive threats

- 15.1.4 ILLINOIS TOOL WORKS INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 SCOTT BADER COMPANY LTD.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 3M

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 MnM view

- 15.1.6.3.1 Right to win

- 15.1.6.3.2 Strategic choices

- 15.1.6.3.3 Weaknesses and competitive threats

- 15.1.7 HUNTSMAN INTERNATIONAL LLC.

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 MnM view

- 15.1.7.3.1 Right to win

- 15.1.7.3.2 Strategic choices

- 15.1.7.3.3 Weaknesses and competitive threats

- 15.1.8 BOSTIK

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Expansions

- 15.1.8.4 MnM view

- 15.1.8.4.1 Right to win

- 15.1.8.4.2 Strategic choices

- 15.1.8.4.3 Weaknesses and competitive threats

- 15.1.9 SIKA AG

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 MnM view

- 15.1.9.3.1 Right to win

- 15.1.9.3.2 Strategic choices

- 15.1.9.3.3 Weaknesses and competitive threats

- 15.1.10 PARKER HANNIFIN CORP

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 MnM view

- 15.1.10.3.1 Key strengths/Right to win

- 15.1.10.3.2 Strategic choices

- 15.1.10.3.3 Weaknesses and competitive threats

- 15.1.1 HENKEL AG & CO. KGAA

- 15.2 OTHER PLAYERS

- 15.2.1 PERMABOND

- 15.2.2 PARSON ADHESIVES, INC.

- 15.2.3 ADVANCED ADHESIVE SYSTEMS

- 15.2.4 ADHESIVE SYSTEMS, INC.

- 15.2.5 DYNAMIC ADHESIVE SOLUTIONS

- 15.2.6 INFINITY BOND ADHESIVES

- 15.2.7 WEICON INC.

- 15.2.8 HERNON MANUFACTURING

- 15.2.9 BONDLOC UK LTD

- 15.2.10 HOENLE AG

- 15.2.11 SUPEX

- 15.2.12 ADINOX

- 15.2.13 KISLING AG

- 15.2.14 NOVACHEM CORPORATION LTD.

- 15.2.15 LOXEAL S.R.L.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary interview participants

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 16.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS