|

시장보고서

상품코드

2029906

홈 오토메이션 시스템 시장 : 제품 유형별, 프로토콜별, 시스템 유형별, 주택 유형별 - 세계 예측(-2032년)Home Automation System Market by Product, By Protocol, By System Type, By Residence Type - Global Forecast to 2032 |

||||||

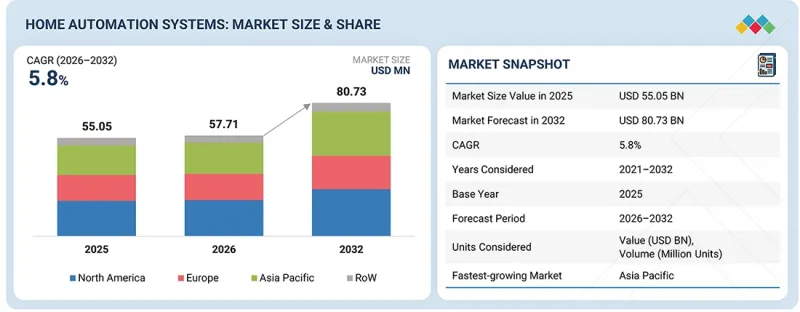

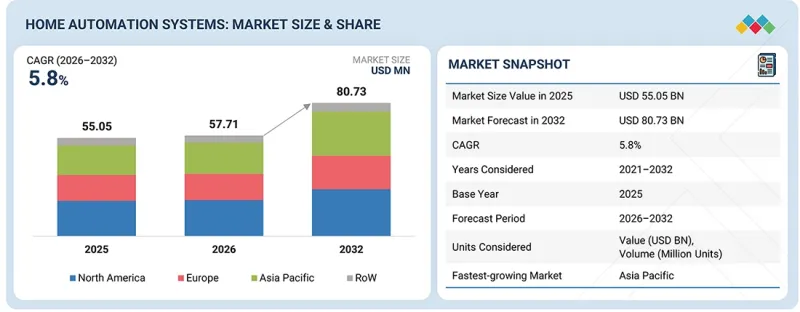

세계의 홈 오토메이션 시스템 시장 규모는 2026년에 577억 1,000만 달러, 2032년에는 807억 3,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR 5.8%로 성장할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제품, 프로토콜, 주택 유형, 시스템 유형, 설치 유형, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

"제품별로는 조명 제어 부문이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상"

조명 제어 부문은 조명 제어 시스템이 에너지 효율을 높이고 개인화된 조명 경험을 제공하는 데 있어 중요한 역할을 하기 때문에 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다. 주거, 상업, 산업 각 분야에서 널리 채택되고 있는 이 시스템은 밝기, 색상, 스케줄 설정을 정밀하게 제어하여 에너지 비용 절감에 기여합니다. 또한, 에너지 절약에 대한 규제 강화와 Zigbee, Bluetooth Mesh와 같은 무선 기술의 발전이 급속한 보급을 촉진하고 있습니다. 또한, 사용자 친화적인 인터페이스, 클라우드 연결, AI를 활용한 자동화를 통해 소규모에서 대규모 설치 환경까지 그 활용 범위가 확대되고 있으며, 조명 제어는 스마트 빌딩 및 홈 오토메이션 시스템의 중요한 구성요소로 자리 잡고 있습니다.

"시스템 유형별로는 예측 기간 동안 '행동 기반' 부문이 시장을 주도할 것으로 예상"

행동 기반 부문은 자동화된 데이터 기반 의사결정을 통해 편의성, 에너지 효율성, 보안을 향상시키기 때문에 예측 기간 동안 시장을 주도할 것으로 예상됩니다. 행동 기반 시스템은 사용자의 재실 상황, 조명 선호도, 온도 설정, 일상 습관 등 사용자의 패턴을 학습하여 수동 개입 없이 자동으로 장치를 조정합니다. 이러한 지능형 자동화를 통해 에너지 소비를 줄이고, 유틸리티 비용을 절감하며, 전반적인 편안함을 향상시킬 수 있습니다. 또한, AI 탑재 어시스턴트, 스마트 온도조절기, 적응형 조명 시스템의 보급이 확산되고 있는 것도 수요를 더욱 부추기고 있습니다. 또한, 매끄럽고 개인화된 생활 경험에 대한 소비자의 선호도가 높아지고 커넥티드 디바이스의 보급률이 높아지면서 주거용 부동산 전반에 걸쳐 행동 기반 자동화 솔루션의 대규모 도입이 촉진되고 있습니다.

"예측 기간 동안 북미가 가장 큰 시장 규모를 차지할 것으로 예상"

예측 기간 동안 북미가 가장 큰 시장 규모를 차지할 것으로 예상됩니다. 이는 높은 스마트홈 보급률, 강력한 구매력, 첨단 디지털 인프라에 기인합니다. 이 지역은 광범위한 광대역 보급, IoT 기술의 조기 도입, 주요 기술 제공업체의 강력한 존재감의 혜택을 누리고 있습니다. 또한, 에너지 효율, 홈 시큐리티, 편의성을 중시하는 소비자들의 인식이 높아지면서 수요가 더욱 가속화되고 있습니다. 주택 신축 및 개보수 프로젝트에서 음성 비서, 커넥티드 보안 시스템, 스마트 조명 솔루션이 통합되고 있는 것도 예측 기간 동안 북미의 우위를 강화하는 요인으로 작용할 것으로 보입니다.

세계의 홈 오토메이션 시스템 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 홈 오토메이션 시스템 시장에서 사용되는 기술

제10장 홈 오토메이션 시스템 시장 : 제품 유형별

제11장 홈 오토메이션 시스템 시장 : 프로토콜·통신 기술별

제12장 홈 오토메이션 시스템 시장 : 주택 유형별

제13장 홈 오토메이션 시스템 시장 : 설치 유형별

제14장 홈 오토메이션 시스템 시장 : 제어 인터페이스별

제15장 홈 오토메이션 시스템 시장 : 용도별

제16장 홈 오토메이션 시스템 시장 : 최종사용자별

제17장 홈 오토메이션 시스템 시장 : 지역별

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSM 26.05.21The global home automation system market is estimated to be valued at USD 57.71 billion in 2026. It is projected to reach USD 80.73 billion by 2032, growing at a CAGR of 5.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Product, Protocol, Residence Type, System Type, Instrallation Type and Region |

| Regions covered | North America, Europe, APAC, RoW |

"By product, the lighting controls segment is projected to witness the highest growth during the forecast period"

The lighting controls segment is projected to witness the highest growth during the forecast period due to the key role of lighting control systems in improving energy efficiency and providing personalized lighting experiences. Widely adopted across residential, commercial, and industrial sectors, these systems offer precise control over brightness, color, and scheduling, helping reduce energy costs. Additionally, increasing regulatory focus on energy conservation and advancements in wireless technologies like Zigbee and Bluetooth Mesh are driving rapid adoption. Moreover, user-friendly interfaces, cloud connectivity, and AI-powered automation expand their use across small and large installations, making lighting controls a vital component of smart building and home automation systems.

"By system type, the behavioral segment is projected to lead market size during the forecast period"

The behavioral segment is projected to lead the market during the forecast period because the system enhances convenience, energy efficiency, and security through automated, data-driven decision-making. Behavioral systems learn user patterns, such as occupancy, lighting preferences, temperature settings, and daily routines, and automatically adjust devices without manual intervention. This intelligent automation reduces energy consumption, lowers utility costs, and improves overall comfort. Additionally, the growing adoption of AI-enabled assistants, smart thermostats, and adaptive lighting systems further strengthens demand. Furthermore, increasing consumer preference for seamless, personalized living experiences and the rising penetration of connected devices are driving large-scale adoption of behavioral automation solutions across residential properties.

"North America is projected to account for the largest market size during forecast period"

North America is projected to account for the largest market size in the home automation system market during the forecast period. This is due to high smart home adoption, strong purchasing power, and advanced digital infrastructure. The region benefits from widespread broadband penetration, early adoption of IoT technologies, and strong presence of leading technology providers. In addition, the growing consumer awareness regarding energy efficiency, home security, and convenience-driven living further accelerates demand. Moreover, the increasing integration of voice assistants, connected security systems, and smart lighting solutions in residential construction and renovation projects also strengthens North America's dominant position during the forecast period.

Extensive primary interviews were conducted with key industry experts in the home automation system market to determine and verify the market size for various segments and subsegments gathered through secondary research.

The breakdown of primary participants for the report is shown below:

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, and RoW - 5%

The home automation system market is dominated by a few globally established players, such as Johnson Controls (Ireland), Schneider Electric (France), Siemens (Germany), Honeywell (US), ASSA ABLOY (Sweden), Apple (US), ABB (Switzerland), Robert Bosch (Germany), Legrand (France), and ADT (US). The study includes an in-depth competitive analysis of these key players in the home automation system market. It also includes their company profiles, recent developments, and key market strategies.

Study Coverage

The report segments the home automation system market. It forecasts it based on product (Lighting controls, security & access control, HVAC controls, entertainment & other controls, smart speakers), protocol (Wired, wireless), residence type (Single-family, multi-family), system type (Behavioral, proactive), and installation type (New, retrofit). It analyzes key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across North America, Europe, Asia Pacific, and the Rest of the World. The study also covers value chain analysis and competitive landscape assessment of leading players operating in the global home automation system ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (Rising demand for convenience and comfort, increasing demand for energy-efficient devices), restraints (High up-front costs, complexity and glitches), opportunities (Favorable government regulations, Adaptive to remote working), challenges (Cybersecurity concerns)

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the home automation system market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the home automation system market

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, including Johnson Controls (Ireland), Schneider Electric (France), Siemens (Germany), Honeywell (US), ASSA ABLOY (Sweden), Apple (US), ABB (Switzerland), Robert Bosch (Germany), Legrand (France), and ADT (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HOME AUTOMATION SYSTEM MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 OPPORTUNITIES FOR PLAYERS IN HOME AUTOMATION SYSTEM MARKET

- 3.2 HOME AUTOMATION SYSTEM MARKET, BY INSTALLATION TYPE

- 3.3 HOME AUTOMATION SYSTEM MARKET, BY CONTROL INTERFACE

- 3.4 HOME AUTOMATION SYSTEM MARKET, BY REGION

- 3.5 HOME AUTOMATION SYSTEM MARKET IN ASIA PACIFIC, BY PRODUCT TYPE AND COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift from device connectivity to system-level orchestration

- 4.2.1.2 Disposable income and expanding middle-class population driving adoption of integrated home automation systems

- 4.2.1.3 Rising demand for real-time home monitoring and remote access to household systems

- 4.2.1.4 Pressing need for energy-efficient home automation solutions

- 4.2.1.5 Growing public emphasis on safety, security, and convenience

- 4.2.1.6 Ongoing advancements in AI- and voice-enabled home automation solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited adoption of home automation solutions due to high costs, data security risks, and connectivity dependence

- 4.2.2.2 Data privacy, security risks, and regulatory compliance challenges

- 4.2.2.3 Dependence on stable internet connectivity and network infrastructure

- 4.2.2.4 Perception of home automation technologies as convenience-driven rather than necessity-driven

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Government regulations and initiatives promoting green buildings and energy-efficient infrastructure

- 4.2.3.2 Integration of IoT-enabled lighting controllers with built-in connectivity

- 4.2.3.3 Incorporation of power line communication technology in home automation

- 4.2.3.4 Expansion of retrofit and renovation opportunities in existing residential infrastructure

- 4.2.4 CHALLENGES

- 4.2.4.1 Interoperability gaps and lack of unified standards in home automation ecosystems

- 4.2.4.2 Risk of device malfunction

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.4.1 STRATEGIC FOCUS AND MOVES CARRIED OUT BY MARKET PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN HOME AUTOMATION SYSTEM MARKET

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF HOME AUTOMATION SYSTEM PRODUCTS, BY KEY PLAYER, 2022-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF HOME AUTOMATION SMART BULBS, BY REGION, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 852872)

- 5.7.2 EXPORT SCENARIO (HS CODE 852872)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 ASSA ABLOY DEPLOYS ACCESS CONTROL SYSTEMS TO REDUCE EMERGENCY RESPONSE TIME

- 5.11.2 JOHNSON CONTROLS PROVIDES FISERV WITH YORK TEMPO CHILLERS TO ACHIEVE ENERGY SAVINGS

- 5.11.3 HONEYWELL OFFERS SECURITY SOLUTIONS TO IMPROVE SECURITY AND VISITOR ACCESS

- 5.12 IMPACT OF US TARIFF ON HOME AUTOMATION SYSTEM MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 VOICE ASSISTANTS

- 6.1.2 WIRELESS COMMUNICATION PROTOCOLS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 5G NETWORKS & ADVANCED BROADBAND INFRASTRUCTURE

- 6.2.2 AUGMENTED REALITY (AR) & MOBILE APP INTERFACES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027): INTEROPERABILITY & AI-ENABLED AUTOMATION

- 6.3.2 MID-TERM (2027-2030): ECOSYSTEM INTEGRATION & EDGE AI EXPANSION

- 6.3.3 LONG-TERM (2030-2035+): AUTONOMOUS HOME AUTOMATION & DIGITAL ECOSYSTEM CONVERGENCE

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI ON HOME AUTOMATION SYSTEM MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY COMPANIES IN HOME AUTOMATION SYSTEM MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN HOME AUTOMATION SYSTEM MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT AI IN HOME AUTOMATION SYSTEM MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 LAWS AND DIRECTIVES

- 7.2 INDUSTRY STANDARDS

- 7.2.1 SMART HVAC STANDARDS

- 7.2.2 ENTERTAINMENT & CONTROL SYSTEM STANDARDS

- 7.2.3 ACCESS CONTROL & SECURITY STANDARDS

- 7.3 REGIONAL REGULATIONS

- 7.3.1 US

- 7.3.2 EUROPE

- 7.3.3 CHINA

- 7.3.4 JAPAN

- 7.3.5 INDIA

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS

9 TECHNOLOGIES USED IN HOME AUTOMATION SYSTEM MARKET

- 9.1 INTRODUCTION

- 9.2 IOT CONNECTIVITY

- 9.3 AI & MACHINE LEARNING

- 9.4 VOICE RECOGNITION

- 9.5 COMPUTER VISION

- 9.6 EDGE COMPUTING

10 HOME AUTOMATION SYSTEM MARKET, BY PRODUCT TYPE

- 10.1 INTRODUCTION

- 10.2 SMART LIGHTING SOLUTIONS

- 10.2.1 HARDWARE

- 10.2.1.1 Luminaires & smart lights

- 10.2.1.1.1 Proficiency in creating dynamic lighting environments tailored to specific activities or moods to spur demand

- 10.2.1.2 Lighting controls

- 10.2.1.2.1 Relays

- 10.2.1.2.1.1 System-level automation through centralized control, sensor integration, and seamless retrofitting to drive segment growth

- 10.2.1.2.2 Occupancy sensors

- 10.2.1.2.2.1 Real-time, sensor-driven automation and energy optimization to drive segment growth

- 10.2.1.2.3 Daylight sensors

- 10.2.1.2.3.1 Adaptive, energy-efficient lighting through real-time daylight integration to drive segment growth

- 10.2.1.2.4 Timers

- 10.2.1.2.4.1 Schedule-driven automation and system-level orchestration to drive segment growth

- 10.2.1.2.5 Dimmers

- 10.2.1.2.5.1 Enhancing adaptive lighting control and energy optimization to support segment growth

- 10.2.1.2.6 Switches

- 10.2.1.2.6.1 Seamless human-to-system interaction and hybrid control to drive segment growth

- 10.2.1.2.7 Other lighting control types

- 10.2.1.2.1 Relays

- 10.2.1.1 Luminaires & smart lights

- 10.2.2 SOFTWARE & SERVICES

- 10.2.2.1 Potential to provide centralized control interface, data analytics, and remote access capabilities to drive segmental growth

- 10.2.1 HARDWARE

- 10.3 SMART SECURITY & ACCESS CONTROL SYSTEMS

- 10.3.1 VIDEO SURVEILLANCE SOLUTIONS

- 10.3.1.1 Hardware

- 10.3.1.1.1 Cameras

- 10.3.1.1.1.1 Analog cameras

- 10.3.1.1.1.1.1 Rising use in budget-sensitive or retrofit residential applications to support segmental growth

- 10.3.1.1.1.2 IP cameras

- 10.3.1.1.1.2.1 Superior scalability and ultra-high-definition video quality to contribute to segmental growth

- 10.3.1.1.1.1 Analog cameras

- 10.3.1.1.2 Storage devices

- 10.3.1.1.2.1 Pressing need for storage equipment to store crucial data to foster segmental growth

- 10.3.1.1.3 Monitors

- 10.3.1.1.3.1 Ability to display highly detailed images needed to make security decisions to spur demand

- 10.3.1.1.4 Other accessories

- 10.3.1.1.1 Cameras

- 10.3.1.2 Software & services

- 10.3.1.2.1 Incorporation of artificial intelligence and data analytics to ensure safety & security to fuel demand

- 10.3.1.1 Hardware

- 10.3.2 ACCESS CONTROL SYSTEMS

- 10.3.2.1 Hardware

- 10.3.2.1.1 Tags

- 10.3.2.1.1.1 Temporary access provisioning, time-based restrictions, and remote credential management features to drive adoption

- 10.3.2.1.2 Readers

- 10.3.2.1.2.1 Card-based readers

- 10.3.2.1.2.1.1 Simplicity, scalability, and compatibility with existing infrastructure to accelerate demand

- 10.3.2.1.2.2 Biometrics readers

- 10.3.2.1.2.2.1 Increasing privacy and security concerns to boost adoption

- 10.3.2.1.2.2.2 Fingerprint

- 10.3.2.1.2.2.3 Palm recognition

- 10.3.2.1.2.2.4 Iris recognition

- 10.3.2.1.2.2.5 Face recognition

- 10.3.2.1.2.2.6 Voice recognition

- 10.3.2.1.2.3 Multi-technology readers

- 10.3.2.1.2.3.1 Ability to unify multiple access methods into single interface to support implementation

- 10.3.2.1.2.1 Card-based readers

- 10.3.2.1.3 Smart locks

- 10.3.2.1.3.1 Smart deadbolt locks

- 10.3.2.1.3.1.1 Elevating demand for robust and reliable front-door security to fuel segmental growth

- 10.3.2.1.3.2 Smart lever & knob locks

- 10.3.2.1.3.2.1 Suitability for high-frequency usage areas such as bedrooms, offices, and utility rooms to escalate demand

- 10.3.2.1.3.3 Smart door handle sets

- 10.3.2.1.3.3.1 Easy installation and intuitive access control interfaces to drive demand

- 10.3.2.1.3.4 Smart mortise locks

- 10.3.2.1.3.4.1 Durability, advanced functionality, and sophisticated design features to stimulate segmental growth

- 10.3.2.1.3.5 Smart cam locks

- 10.3.2.1.3.5.1 Need to safeguard valuables, sensitive documents, and restricted household items to foster segmental growth

- 10.3.2.1.3.6 Smart garage door locks & controllers

- 10.3.2.1.3.6.1 Ability to provide automated access to vehicle entry and perimeter security to boost demand

- 10.3.2.1.3.1 Smart deadbolt locks

- 10.3.2.1.4 Controllers

- 10.3.2.1.4.1 Focus on improving access system coordination through communication-enabled control panels to drive market

- 10.3.2.1.5 Alarm systems

- 10.3.2.1.5.1 Elevating demand for real-time threat detection and responsive security activation to support market growth

- 10.3.2.1.6 Other access control hardware types

- 10.3.2.1.1 Tags

- 10.3.2.2 Software & services

- 10.3.2.2.1 Surging demand for intelligent, adaptive, and future-ready smart home security systems to support segmental growth

- 10.3.2.1 Hardware

- 10.3.1 VIDEO SURVEILLANCE SOLUTIONS

- 10.4 SMART HVAC SOLUTIONS

- 10.4.1 HARDWARE

- 10.4.1.1 HVAC systems

- 10.4.1.1.1 Intelligent thermal management capabilities to boost demand

- 10.4.1.2 HVAC controls

- 10.4.1.2.1 Smart thermostats

- 10.4.1.2.1.1 Strong focus on achieving energy efficiency to fuel demand

- 10.4.1.2.2 Sensors

- 10.4.1.2.2.1 Constant need to capture environmental and operational data in real time to facilitate adoption

- 10.4.1.2.3 Control valves

- 10.4.1.2.3.1 Strong focus on reducing energy wastage to drive demand

- 10.4.1.2.4 Dampers

- 10.4.1.2.4.1 Proficiency in offering balanced airflow distribution and enhancing occupant comfort to elevate demand

- 10.4.1.2.5 Actuators

- 10.4.1.2.5.1 High reliability and low power consumption to offer growth opportunities

- 10.4.1.2.6 Smart vents

- 10.4.1.2.6.1 Inclination toward room-level airflow optimization for personalized comfort and energy efficiency to drive segmental growth

- 10.4.1.2.1 Smart thermostats

- 10.4.1.1 HVAC systems

- 10.4.2 SOFTWARE & SERVICES

- 10.4.2.1 Need to remotely manage temperature settings, schedules, and system performance in real time to stimulate segmental growth

- 10.4.1 HARDWARE

- 10.5 SMART ENTERTAINMENT & OTHER SYSTEMS

- 10.5.1 AUDIO

- 10.5.1.1 Smart speakers

- 10.5.1.1.1 Integration of smart speakers as voice-enabled interfaces for scenario-based control to drive adoption

- 10.5.1.2 Voice-enabled devices

- 10.5.1.2.1 Expanding role of natural language interfaces as access layers for scenario-based control in home automation systems to drive growth

- 10.5.1.1 Smart speakers

- 10.5.2 VIDEO

- 10.5.2.1 Smart TVs

- 10.5.2.1.1 Superior picture quality, enhanced contrast, and improved color accuracy contribute to increased demand

- 10.5.2.2 Smart streaming devices

- 10.5.2.2.1 Surging demand for flexible, scalable, and user-centric home entertainment solutions to fuel segmental growth

- 10.5.2.1 Smart TVs

- 10.5.3 CONTROLS

- 10.5.3.1 Entertainment controls

- 10.5.3.1.1 Competency in managing and synchronizing multiple audio-visual devices to propel demand

- 10.5.3.1.2 Audio & volume controls

- 10.5.3.1.3 Home theater system controls

- 10.5.3.1.4 Touchscreen & keypad interfaces

- 10.5.3.2 Other controls

- 10.5.3.2.1 Smart meters

- 10.5.3.2.2 Smart plugs

- 10.5.3.2.3 Smart hubs

- 10.5.3.2.4 Smoke detectors

- 10.5.3.1 Entertainment controls

- 10.5.1 AUDIO

11 HOME AUTOMATION SYSTEM MARKET, BY PROTOCOL & COMMUNICATION TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 WIRED

- 11.2.1 STRONG PRESENCE IN STRUCTURED DEPLOYMENTS AND PREMIUM RESIDENTIAL PROJECTS TO SUPPORT MARKET GROWTH

- 11.2.2 DALI

- 11.2.3 KNX

- 11.2.4 DMX

- 11.2.5 LONWORKS

- 11.2.6 ETHERNET

- 11.2.7 MODBUS

- 11.2.8 BACNET

- 11.2.9 POWER LINE COMMUNICATION

- 11.3 WIRELESS

- 11.3.1 FLEXIBILITY, SCALABILITY, COST-EFFICIENCY, AND INTEROPERABILITY TO DRIVE ADOPTION

- 11.3.2 ZIGBEE

- 11.3.3 MATTER

- 11.3.4 Z-WAVE

- 11.3.5 WI-FI

- 11.3.6 BLUETOOTH

- 11.3.7 ENOCEAN

- 11.3.8 THREAD

12 HOME AUTOMATION SYSTEM MARKET, BY RESIDENCE TYPE

- 12.1 INTRODUCTION

- 12.2 SINGLE-FAMILY HOMES

- 12.2.1 GREATER OWNERSHIP CONTROL TO SUPPORT ADOPTION OF ADVANCED AND CUSTOMIZED HOME AUTOMATION SOLUTIONS

- 12.3 MULTI-FAMILY BUILDINGS

- 12.3.1 DEVELOPER-LED INTEGRATION AND SMART APARTMENT TRENDS TO DRIVE LARGE-SCALE ADOPTION

- 12.4 VILLAS/LUXURY HOMES

- 12.4.1 RISING DEMAND FOR PREMIUM LIVING AND PERSONALIZED AUTOMATION TO DRIVE ADOPTION OF HIGH-END SOLUTIONS

13 HOME AUTOMATION SYSTEM MARKET, BY INSTALLATION TYPE

- 13.1 INTRODUCTION

- 13.2 NEW INSTALLATION

- 13.2.1 FOCUS OF BUILDERS ON MEETING EVOLVING CONSUMER DEMAND FOR CONNECTED LIVING TO ACCELERATE DEPLOYMENT

- 13.3 RETROFIT INSTALLATION

- 13.3.1 AVAILABILITY OF USER-FRIENDLY, SUSTAINABLE, AND DIY INSTALLATION OPTIONS TO SPUR DEMAND

14 HOME AUTOMATION SYSTEM MARKET, BY CONTROL INTERFACE

- 14.1 INTRODUCTION

- 14.2 SMARTPHONE/TABLET APPLICATIONS

- 14.2.1 ABILITY TO MONITOR AND MANAGE CONNECTED DEVICES FROM ANY LOCATION TO DRIVE DEMAND

- 14.3 VOICE ASSISTANTS

- 14.3.1 PROFICIENCY IN MANAGING SMART HOME DEVICES WITHOUT PHYSICAL INTERACTION TO PROPEL DEMAND

- 14.4 WALL PANELS & SWITCHES

- 14.4.1 COMMERCIALIZATION OF ADVANCED WALL PANELS WITH TOUCHSCREEN AND CUSTOMIZABLE CONTROLS TO SUPPORT SEGMENTAL GROWTH

- 14.5 WEARABLES

- 14.5.1 POTENTIAL TO OFFER QUICK AND CONVENIENT ACCESS TO ESSENTIAL FUNCTIONS TO PROPEL SEGMENTAL GROWTH

15 HOME AUTOMATION SYSTEM MARKET, BY APPLICATION

- 15.1 INTRODUCTION

- 15.2 SAFETY & SECURITY

- 15.2.1 INCREASING CONCERNS AROUND RESIDENTIAL SAFETY, ASSET PROTECTION, AND PERSONAL WELL-BEING TO DRIVE DEMAND

- 15.3 COMFORT & CONVENIENCE

- 15.3.1 SIGNIFICANT FOCUS ON IMPROVING QUALITY OF LIFE THROUGH AUTOMATION AND INTELLIGENT CONTROL SYSTEMS TO SUPPORT MARKET GROWTH

- 15.4 ENERGY MANAGEMENT

- 15.4.1 CONSIDERABLE FOCUS ON MONITORING, CONTROLLING, AND OPTIMIZING ENERGY USAGE TO ENCOURAGE ADOPTION

- 15.5 ENTERTAINMENT

- 15.5.1 INTEGRATION OF AUDIO-VISUAL ECOSYSTEMS TO CREATE PERSONALIZED ENTERTAINMENT ENVIRONMENT TO PROPEL MARKET GROWTH

- 15.6 OTHER APPLICATIONS

16 HOME AUTOMATION SYSTEM MARKET, BY END USER

- 16.1 INTRODUCTION

- 16.2 INDIVIDUAL HOMEOWNERS

- 16.2.1 INCREASING ENVIRONMENTAL AWARENESS TO SPUR DEMAND FOR ENERGY-EFFICIENT SMART HOME SOLUTIONS

- 16.3 RESIDENTIAL BUILDERS & DEVELOPERS

- 16.3.1 RISING FOCUS ON MEETING SUSTAINABILITY STANDARDS AND ENHANCING PROPERTY VALUE TO DRIVE ADOPTION

- 16.4 RENTAL HOUSING OWNERS & OPERATORS

- 16.4.1 GREATER EMPHASIS ON IMPROVING TENANT EXPERIENCE TO PROPEL DEMAND

17 HOME AUTOMATION SYSTEM MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Strong presence of companies offering robust security and surveillance solutions to drive market

- 17.2.2 CANADA

- 17.2.2.1 Favorable government policies promoting installation of safety and security products to support market growth

- 17.2.3 MEXICO

- 17.2.3.1 Rapid penetration of connected devices due to increasing disposable incomes to contribute to market growth

- 17.2.1 US

- 17.3 EUROPE

- 17.3.1 UK

- 17.3.1.1 Stringent fire safety rules for building occupants to support market growth

- 17.3.2 GERMANY

- 17.3.2.1 High standard of living and preference for comfort and security to create growth opportunities

- 17.3.3 FRANCE

- 17.3.3.1 Government mandates and incentives for energy-efficient renovations to fuel market growth

- 17.3.4 ITALY

- 17.3.4.1 Government energy efficiency policies to boost demand

- 17.3.5 SPAIN

- 17.3.5.1 Strong focus on renewable energy integration to stimulate market growth

- 17.3.6 NETHERLANDS

- 17.3.6.1 Increasing adoption of advanced smart metering and AI-based energy optimization platforms to propel market

- 17.3.7 NORDICS

- 17.3.7.1 Strong environmental awareness and government support for renewable energy-powered solutions to drive market

- 17.3.8 REST OF EUROPE

- 17.3.1 UK

- 17.4 ASIA PACIFIC

- 17.4.1 CHINA

- 17.4.1.1 Strong government support for digital infrastructure to foster market growth

- 17.4.2 JAPAN

- 17.4.2.1 Greater emphasis on reducing energy consumption in residential buildings to elevate demand

- 17.4.3 SOUTH KOREA

- 17.4.3.1 Development of energy-efficient lighting controls to propel market

- 17.4.4 INDIA

- 17.4.4.1 Availability of local language-based and cost-effective voice assistants to fuel market growth

- 17.4.5 SINGAPORE

- 17.4.5.1 Smart Nation initiative to expedite adoption of smart home solutions

- 17.4.6 AUSTRALIA

- 17.4.6.1 High consumer awareness and demand for energy-efficient living to support market growth

- 17.4.7 SOUTHEAST ASIA

- 17.4.7.1 Increasing smartphone penetration to drive market

- 17.4.8 REST OF ASIA PACIFIC

- 17.4.1 CHINA

- 17.5 SOUTH AMERICA

- 17.5.1 BRAZIL

- 17.5.1.1 Large-scale investments in digital infrastructure and e-commerce expansion to accelerate demand

- 17.5.2 ARGENTINA

- 17.5.2.1 Expansion of e-commerce platforms to create growth opportunities

- 17.5.3 REST OF SOUTH AMERICA

- 17.5.1 BRAZIL

- 17.6 MIDDLE EAST & AFRICA

- 17.6.1 SOUTH AFRICA

- 17.6.1.1 Growing need for energy-efficient and secure residential solutions to fuel market growth

- 17.6.2 GCC COUNTRIES

- 17.6.2.1 Rising government initiatives and construction growth to drive adoption of energy-efficient home automation systems

- 17.6.3 REST OF MIDDLE EAST & AFRICA

- 17.6.1 SOUTH AFRICA

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 18.3 MARKET SHARE ANALYSIS, 2025

- 18.4 REVENUE ANALYSIS, 2021-2025

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.5.1 HOME AUTOMATION SYSTEM MARKET: COMPANY VALUATION

- 18.5.2 HOME AUTOMATION SYSTEM MARKET: FINANCIAL METRICS

- 18.6 BRAND COMPARISON

- 18.6.1 SCHNEIDER ELECTRIC (FRANCE)

- 18.6.2 HONEYWELL INTERNATIONAL INC. (US)

- 18.6.3 SIEMENS (GERMANY)

- 18.6.4 JOHNSON CONTROLS (IRELAND)

- 18.6.5 ABB (SWITZERLAND)

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Protocol & communication technology footprint

- 18.7.5.4 Product type footprint

- 18.7.5.5 Installation type footprint

- 18.7.5.6 Application footprint

- 18.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 18.8.5.1 Detailed list of key startups/SMEs

- 18.8.5.2 Competitive benchmarking of key startups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 18.9.2 DEALS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 JOHNSON CONTROLS

- 19.1.1.1 Business overview

- 19.1.1.2 Products/Solutions/Services offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches/enhancements

- 19.1.1.3.2 Other developments

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths/Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses/Competitive threats

- 19.1.2 SCHNEIDER ELECTRIC

- 19.1.2.1 Business overview

- 19.1.2.2 Products/Solutions/Services offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches/enhancements

- 19.1.2.3.2 Deals

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths/Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses/Competitive threats

- 19.1.3 SIEMENS

- 19.1.3.1 Business overview

- 19.1.3.2 Products/Solutions/Services offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches/enhancements

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths/Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses/Competitive threats

- 19.1.4 HONEYWELL INTERNATIONAL INC.

- 19.1.4.1 Business overview

- 19.1.4.2 Products/Solutions/Services offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches/enhancements

- 19.1.4.3.2 Deals

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths/Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses/Competitive threats

- 19.1.5 ASSA ABLOY

- 19.1.5.1 Business overview

- 19.1.5.2 Products/Solutions/Services offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches/enhancements

- 19.1.5.3.2 Deals

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths/Right to win

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses/Competitive threats

- 19.1.6 ADT

- 19.1.6.1 Business overview

- 19.1.6.2 Products/Solutions/Services offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches/enhancements

- 19.1.6.3.2 Deals

- 19.1.7 ROBERT BOSCH GMBH

- 19.1.7.1 Business overview

- 19.1.7.2 Products/Solutions/Services offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches/enhancements

- 19.1.7.3.2 Deals

- 19.1.8 ABB

- 19.1.8.1 Business overview

- 19.1.8.2 Products/Solutions/Services offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product launches/enhancements

- 19.1.8.3.2 Deals

- 19.1.9 APPLE INC.

- 19.1.9.1 Business overview

- 19.1.9.2 Products/Solutions/Services offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches/enhancements

- 19.1.9.3.2 Deals

- 19.1.10 AMAZON.COM, INC.

- 19.1.10.1 Business overview

- 19.1.10.2 Products/Solutions/Services offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Product launches/enhancements

- 19.1.10.3.2 Deals

- 19.1.11 SIGNIFY HOLDING

- 19.1.11.1 Business overview

- 19.1.11.2 Products/Solutions/Services offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches/enhancements

- 19.1.11.3.2 Deals

- 19.1.12 ACUITY INC.

- 19.1.12.1 Business overview

- 19.1.12.2 Products/Solutions/Services offered

- 19.1.12.3 Recent developments

- 19.1.12.3.1 Product launches/enhancements

- 19.1.12.3.2 Deals

- 19.1.13 LEGRAND

- 19.1.13.1 Business overview

- 19.1.13.2 Products/Solutions/Services offered

- 19.1.13.3 Recent developments

- 19.1.13.3.1 Product launches/enhancements

- 19.1.14 DAIKIN INDUSTRIES LTD.

- 19.1.14.1 Business overview

- 19.1.14.2 Products/Solutions/Services offered

- 19.1.14.3 Recent developments

- 19.1.14.3.1 Product launches/enhancements

- 19.1.14.3.2 Deals

- 19.1.15 CARRIER

- 19.1.15.1 Business overview

- 19.1.15.2 Products/Solutions/Services offered

- 19.1.15.3 Recent developments

- 19.1.15.3.1 Product launches/enhancements

- 19.1.1 JOHNSON CONTROLS

- 19.2 OTHER PLAYERS

- 19.2.1 PANASONIC HOLDINGS CORPORATION

- 19.2.2 ZUMTOBEL GROUP

- 19.2.3 EMERSON ELECTRIC CO.

- 19.2.4 AMS-OSRAM AG

- 19.2.5 RESIDEO TECHNOLOGIES INC.

- 19.2.6 SAMSUNG

- 19.2.7 SONY GROUP CORPORATION

- 19.2.8 OOMA, INC.

- 19.2.9 WOZART TECHNOLOGIES PRIVATE LIMITED

- 19.2.10 AXIS COMMUNICATIONS AB

- 19.2.11 COMCAST

- 19.2.12 ECOBEE

- 19.2.13 CRESTRON ELECTRONICS, INC.

- 19.2.14 SIMPLISAFE, INC.

- 19.2.15 SAVANT SYSTEMS, INC.

- 19.2.16 SMARTFROG LTD.

- 19.2.17 LG ELECTRONICS

- 19.2.18 LUTRON

- 19.2.19 HANGZHOU HIKVISION DIGITAL TECHNOLOGY CO., LTD.

- 19.2.20 WIPRO LIGHTING

- 19.2.21 INTER IKEA SYSTEMS B.V.

- 19.2.22 LENNOX INTERNATIONAL INC.

- 19.2.23 U-TEC GROUP INC.

- 19.2.24 ALARM.COM

- 19.2.25 HAVELLS INDIA LTD.

20 RESEARCH METHODOLOGY

- 20.1 INTRODUCTION

- 20.2 RESEARCH DATA

- 20.2.1 SECONDARY DATA

- 20.2.1.1 List of key secondary sources

- 20.2.1.2 Key data from secondary sources

- 20.2.2 PRIMARY DATA

- 20.2.2.1 Breakdown of primary interviews

- 20.2.2.2 Key data from primary sources

- 20.2.2.3 Key industry insights

- 20.2.2.4 List of primary interview participants

- 20.2.1 SECONDARY DATA

- 20.3 MARKET SIZE ESTIMATION

- 20.3.1 BOTTOM-UP APPROACH

- 20.3.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 20.3.2 TOP-DOWN APPROACH

- 20.3.2.1 Approach to estimate market size using top-down analysis (supply side)

- 20.3.1 BOTTOM-UP APPROACH

- 20.4 MARKET FORECAST APPROACH

- 20.4.1 MARKET SIZE ESTIMATION: DEMAND-SIDE ANALYSIS

- 20.5 DATA TRIANGULATION

- 20.6 RESEARCH ASSUMPTIONS

- 20.6.1 ASSUMPTIONS CONSIDERED DURING RESEARCH

- 20.6.2 GROWTH PROJECTION AND FORECAST-RELATED ASSUMPTIONS

- 20.7 RESEARCH LIMITATIONS

- 20.8 RISK ASSESSMENT

21 APPENDIX

- 21.1 DISCUSSION GUIDE

- 21.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.3 CUSTOMIZATION OPTIONS

- 21.4 RELATED REPORTS

- 21.5 AUTHOR DETAILS