|

시장보고서

상품코드

2029911

오토인젝터 시장 예측(-2031년) : 유형별, 사용법별, 작동 기구별, 투여 경로별, 치료 영역별, 약제 유형별, 용량별, 최종사용자별, 지역별Autoinjectors Market by Type (Devices, Finished Formulation), Usage (Disposable, Reusable), Actuation Mechanism (Mechanical, Electronic), Therapy (Rheumatoid Arthritis, Obesity, Diabetes), ROA (SC, IM), Volume (< 3ml, > 3ml) - Global Forecast to 2031 |

||||||

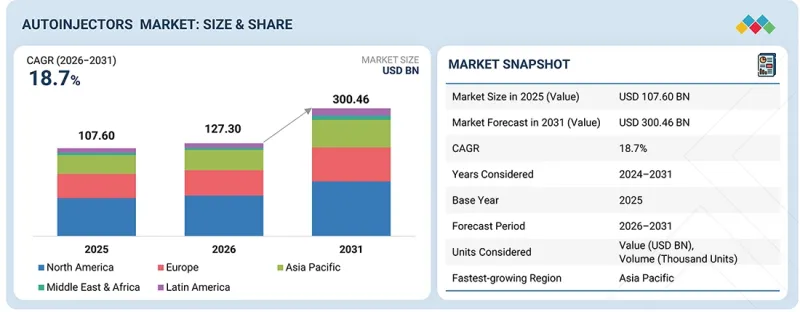

세계의 오토인젝터 시장 규모는 2026년 1,273억 달러에서 2031년까지 3,004억 6,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR은 18.7%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 사용법별, 작동 기구별, 투여 경로별, 치료 영역별, 약제 유형별, 용량별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

만성질환 및 자가면역질환의 유병률 증가와 세계 인구 증가를 배경으로 자동주사기 수요는 꾸준히 성장하고 있습니다. 장기 치료에서 오토인젝터의 채용 확대와 더불어 재택 치료로의 전환이 진행되고 있는 것이 제품 사용을 촉진하고 있습니다. 환자들은 정확한 약물 투여와 안전성을 보장하기 위해 고품질의 안전하고 사용하기 쉬운 자동주사기를 원하고 있습니다. 무침 자동 인젝터, 스마트 커넥티드 디바이스, 내장 센서 등의 기술 발전은 시장의 보급을 더욱 촉진하고 있습니다. 또한 신흥 국가의 의료 인프라 확충과 현대 의료를 장려하는 정부 지원책으로 인해 향후 수년간 시장은 강력한 성장세를 유지할 것으로 예상됩니다.

"의약품 유형별로는 바이오의약품 부문이 큰 시장점유율을 차지할 것으로 예상됩니다. "

약물 유형별로는 류마티스 관절염, 다발성 경화증, 당뇨병과 같은 만성질환 및 자가면역질환 치료에 대한 사용 증가에 힘입어 생물제제가 오토인젝터 시장에서 지배적인 부문를 차지하고 있습니다. 또한 생명공학 및 바이오시밀러 개발에 대한 투자 확대와 더불어 생물제제에 대한 규제 당국의 승인 증가도 수요를 더욱 촉진하고 있습니다. 많은 바이오의약품은 비경구 투여가 필요하므로 오토인젝터와 궁합이 잘 맞습니다. 또한 모노클로널 항체 및 기타 주사제 바이오의약품의 파이프라인이 확대되고 있는 것도 수요를 가속화하고 있습니다.

"투여 경로별로는 피하투여 부문이 2025년 가장 큰 비중을 차지할 것으로 예상됩니다. "

투여 경로별로는 피하투여가 오토인젝터 시장에서 가장 큰 점유율을 차지하고 있습니다. 이는 피하 투여가 근육내 투여에 비해 침투 깊이가 얕아 투여시 통증이 적기 때문입니다. 피하 투여는 약물의 흡수가 안정적이고 환자의 순응도가 높아 생물제제 요법에서 피하 투여가 선호되고 있습니다. 만성 및 급성 질환의 유병률 증가와 입원 환자 수 증가에 따라 장기 치료에 대한 수요가 지속적으로 증가하고 있으며, 이는 오토인젝터에 대한 수요를 더욱 증가시키고 있습니다.

2025년 지역별로는 북미가 자동 인젝터 시장에서 가장 큰 점유율을 차지했습니다.

자동 인젝터 시장은 북미, 유럽, 라틴아메리카, 아시아태평양, 중동 및 아프리카로 분류됩니다. 북미는 전 세계 자동 인젝터 시장을 독점하고 있습니다. 이러한 선도적 지위는 높은 만성질환 유병률, 잘 구축된 의료 인프라, 그리고 첨단 의료기술의 빠른 보급에 기인합니다. 또한 주요 시장 기업의 강력한 존재감, 의료비 증가, 병원 및 재택 의료 현장에서의 첨단 주입 시스템에 대한 수요 증가는 모두 이 지역의 시장 지배적 지위를 지원하고 있습니다.

자동 인젝터 장비 시장의 주요 기업으로는 Becton, Dickinson and Company(미국), SHL Medical(스위스), Ypsomed(스위스) 등이 있습니다. 한편, 자동주입기용 제제 시장의 주요 기업으로는 Novo Nordisk(덴마크), Eli Lilly and Company(미국), AbbVie(미국) 등을 꼽을 수 있습니다.

조사 범위

이 보고서는 유형, 용도, 작동 메커니즘, 투여 경로, 치료 영역, 약물 유형, 용량, 최종사용자 및 지역을 기준으로 자동 인젝터 시장을 분석합니다. 또한 시장 성장에 영향을 미치는 요인에 대해 논의하고, 다양한 기회와 과제를 분석하며, 시장 리더들의 경쟁 상황에 대한 세부 정보를 제공합니다. 또한 이 보고서는 개별 동향의 관점에서 마이크로 시장을 분석하고 5개 주요 지역(및 해당 지역내 국가)의 시장 세분화 매출을 예측하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 대기업부터 중소기업에 이르기까지 시장을 더 깊이 이해하고 시장 점유율을 확대하는 데 도움이 될 것입니다. 이 보고서를 구매한 기업은 다음 전략을 단독으로 또는 조합하여 시장에서의 입지를 강화할 수 있습니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

주요 촉진요인(만성질환 유병률 증가, 규제당국의 승인 증가, 바이오시밀러 및 바이오의약품에 대한 높은 수요, 자가투여 의약품의 보급 확대, 정부 지원 및 유리한 상환 정책), 제약요인(바늘 없는 약물전달 시스템에 대한 관심 및 바늘 공포증 확산), 기회요인(생물학적 분자의 특허 만료 임박, 기술적으로 진보된 자동주입기 출시, 미개발 기회) 만료 임박, 기술적으로 진보된 오토인젝터 출시, 신흥 시장의 미개발 기회), 도전과제(다양한 약물 점도에 대응하는 오토인젝터 개발, 기기 오작동 및 리콜 위험) 등 오토인젝터 시장의 성장에 영향을 미치는 요인 분석

- 시장 침투도: 자동 인젝터 시장의 주요 기업이 제공하는 제품 포트폴리오에 대한 포괄적인 정보

- 제품 개발/혁신: 오토인젝터 시장의 미래 동향, R&D 활동 및 제품 개발에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 수익성 높은 신흥 지역에 대한 종합적인 정보

- 시장 다각화: 자동 인젝터 시장의 신제품, 성장 지역 및 최근 동향에 대한 포괄적인 정보

- 경쟁 분석: 시장 세분화, 성장 전략, 매출 분석 및 주요 시장 진입 기업의 제품에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 고객 상황과 구매 행동

제8장 규제 상황과 지속가능성 구상

제9장 오토인젝터 시장(유형별)

제10장 오토인젝터 시장(사용법별)

제11장 오토인젝터 시장(작동 기구별)

제12장 오토인젝터 시장(투여 경로별)

제13장 오토인젝터 시장(치료 영역별)

제14장 오토인젝터 시장(약제 유형별)

제15장 오토인젝터 시장(용량별)

제16장 오토인젝터 시장(최종사용자별)

제17장 오토인젝터 시장(지역별)

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSA 26.05.21The global autoinjectors market is projected to reach USD 300.46 billion by 2031 from USD 127.30 billion in 2026, at a CAGR of 18.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Usage, Actuation Mechanism, Route of Administration, Therapy Area, Drug type, Volume, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

The demand for autoinjectors is experiencing steady growth, fueled by the increasing prevalence of chronic and autoimmune diseases and the growing global population. The rising adoption of autoinjectors for long-term treatments, along with the shift toward home-based care, is boosting product use. Patients are seeking high-quality, safe, and easy-to-use autoinjectors to ensure accurate drug delivery and safety. Technological advances such as needle-free autoinjectors, smart connected devices, and built-in sensors are further increasing market adoption. Additionally, expanding healthcare infrastructure in emerging economies and supportive government initiatives promoting modern healthcare are expected to maintain strong market growth in the coming years.

"By drug type, the biologics segment is projected to capture a significant market share."

Based on drug type, biologics are the dominant segment in the autoinjectors market, driven by their increased use in treating chronic and autoimmune diseases such as rheumatoid arthritis, multiple sclerosis, and diabetes. Furthermore, growing investments in biotechnology and biosimilar development, along with increasing regulatory approvals for biologics, are further boosting demand. Many biologics require parenteral administration, making them compatible with autoinjectors. The expanding pipeline of monoclonal antibodies and other biologic injectables is also accelerating demand.

"By route of administration, the subcutaneous route of administration segment is expected to register the largest share in 2025."

By route of administration, the subcutaneous route holds the largest share in the autoinjectors market because it allows drugs to be delivered with less pain than the intramuscular route, due to reduced penetration depth. The subcutaneous route is favored for biologic therapies because it provides consistent drug absorption and better patient compliance. The increasing prevalence of chronic and acute diseases, along with more hospital admissions, continues to boost demand for long-term treatments, which further increases the demand for autoinjectors.

In 2025, North America accounted for the largest share of the autoinjectors market by region.

The autoinjectors market is divided into North America, Europe, Latin America, Asia Pacific, and the Middle East & Africa. North America dominates the global autoinjectors market; this leadership is due to the high prevalence of chronic diseases, an established healthcare infrastructure, and rapid adoption of advanced medical technologies. Moreover, the strong presence of key market players, increased healthcare spending, and rising demand for advanced infusion systems in hospitals and home healthcare settings all support the region's dominant market position.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-40%, Tier 2-35%, and Tier 3- 25%

- By Designation: Directors-23%, Managers-30%, and Others-47%

- By Region: North America-25%, Europe-35%, Asia Pacific-20%, Latin America- 13%, and the Middle East & Africa- 7%

The prominent players in the autoinjector devices market include Becton, Dickinson and Company (US), SHL Medical (Switzerland), and Ypsomed (Switzerland). However, prominent players in the autoinjector finished formulation market include Novo Nordisk (Denmark), Eli Lilly and Company (US), and AbbVie (US).

Research Coverage

This report examines the autoinjectors market based on type, usage, actuation mechanism, route of administration, therapy area, drug type, volume, end user, and region. It also discusses the factors influencing market growth, analyzes various opportunities and challenges, and provides details about the competitive landscape for market leaders. Additionally, the report analyzes micro markets in terms of their individual growth trends and forecasts the revenue of market segments across five main regions (and the respective countries within these regions).

Reasons to Buy the Report

The report will help both established and smaller firms understand the market better, which, in turn, will assist them in gaining a larger market share. Companies purchasing the report can use one or a combination of the strategies below to strengthen their market position.

This report provides insights into the following pointers:

Analysis of key drivers (rising prevalence of chronic diseases, Increasing regulatory approvals, high demand for biosimilars and biologics, growing adoption of self-administered medicines, government support and favorable reimbursement policies), restraints (focus on needle-free drug delivery systems and prevalence of needle phobia), opportunities (impending patent expiry of biological molecules, launch of technologically advanced autoinjectors, untapped opportunities in emerging markets), and challenges (development of autoinjectors for multiple drug viscosities, risk of device malfunctions and recalls) influencing the growth of autoinjectors market

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the autoinjectors market

- Product Development/Innovation: Detailed insights into the upcoming trends, R&D activities, and product developments in the autoinjectors market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the autoinjectors market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 SEGMENTS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AUTOINJECTORS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 AUTOINJECTORS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: AUTOINJECTOR DEVICES MARKET, BY COUNTRY AND USAGE

- 3.3 ASIA PACIFIC: FINISHED FORMULATION AUTOINJECTORS MARKET, BY COUNTRY AND ACTUATION MECHANISM

- 3.4 GEOGRAPHIC SNAPSHOT OF AUTOINJECTOR DEVICES MARKET

- 3.5 GEOGRAPHIC SNAPSHOT OF FINISHED FORMULATION AUTOINJECTORS MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising prevalence of chronic and autoimmune diseases

- 4.2.1.2 Increasing regulatory approvals for autoinjectors

- 4.2.1.3 High demand for biosimilars and biologics

- 4.2.1.4 Growing adoption of self-administered medicines

- 4.2.1.5 Government support and favorable reimbursement policies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Focus on needle-free drug delivery systems and prevalence of needle phobia

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Impending patent expiry of biological molecules

- 4.2.3.2 Launch of technologically advanced autoinjectors

- 4.2.3.3 Untapped opportunities in emerging markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Development of autoinjectors for multiple drug viscosities

- 4.2.4.2 Risk of device malfunctions and recalls

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN AUTOINJECTORS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 MARKET ECOSYSTEM

- 5.5.1 AUTOINJECTORS MARKET PROVIDERS

- 5.5.2 END USERS

- 5.5.3 REGULATORY BODIES

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE, BY KEY PLAYER, 2025 (USD)

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025 (USD)

- 5.6.2.1 Rheumatoid arthritis

- 5.6.2.2 Anaphylaxis

- 5.6.2.3 Diabetes

- 5.6.2.4 Obesity

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 901890

- 5.7.2 EXPORT DATA FOR HS CODE 901890

- 5.8 REIMBURSEMENT SCENARIO

- 5.8.1 KEY CONFERENCES & EVENTS (2025-2026)

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF US TARIFFS-AUTOINJECTORS MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Asia Pacific

- 5.12.4.3 Europe

- 5.12.4.4 Latin America

- 5.12.5 IMPACT ON END-USE SEGMENTS

- 5.13 DEVICES FOR LARGE-VOLUME FORMULATIONS

- 5.14 DEVICES FOR HIGHLY VISCOUS FORMULATIONS

- 5.15 INSIGHTS ON FUTURE AREAS OF FOCUS IN AUTOINJECTORS MARKET

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INJECTION MECHANISM TECHNOLOGY

- 6.1.2 ELECTRONIC AND CONNECTIVITY SOLUTIONS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 POWER ASSISTANCE MECHANISMS

- 6.2.2 ADVANCED NEEDLE TECHNOLOGY

- 6.2.3 DRUG CONTAINER AND CARTRIDGE TECHNOLOGIES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 WEARABLE DRUG DELIVERY DEVICES

- 6.3.2 IMPLANTABLE DRUG DELIVERY SYSTEMS

- 6.3.3 NEEDLE-FREE INJECTION TECHNOLOGY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 NEAR TERM (2025-2027)

- 6.4.2 MID-TERM (2028-2030)

- 6.4.3 LONG TERM (2030+)

- 6.5 PATENT ANALYSIS

- 6.5.1 JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-ENABLED PERSONALIZED DRUG DELIVERY

- 6.6.2 COMBINATION THERAPY DELIVERY

- 6.6.3 REUSABLE AUTOINJECTOR PLATFORMS

- 6.7 IMPACT OF AI/GEN AI ON AUTOINJECTORS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 TOP USE CASES AND MARKET POTENTIAL

- 6.7.3 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN AUTOINJECTORS MARKET

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 7.5 MARKET PROFITABILITY

8 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 REGULATORY FRAMEWORK

- 8.1.2.1 North America

- 8.1.2.2 Europe

- 8.1.2.3 Asia Pacific

- 8.1.2.4 Latin America

- 8.1.2.5 Middle East & Africa

- 8.1.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 8.1.4 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 REUSABLE AUTOINJECTOR PLATFORMS

- 8.2.2 USE OF BIO-BASED POLYMERS

- 8.2.3 CIRCULAR DEVICE DESIGN AND RECYCLABILITY

9 AUTOINJECTORS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 FINISHED FORMULATION AUTOINJECTORS

- 9.2.1 READY-TO-USE DESIGN AND PATIENT CONVENIENCE DRIVE MARKET LEADERSHIP

- 9.3 AUTOINJECTOR DEVICES

- 9.3.1 FLEXIBILITY AND PLATFORM-BASED INTEGRATION SUPPORT MARKET ADOPTION

10 AUTOINJECTORS MARKET, BY USAGE

- 10.1 INTRODUCTION

- 10.2 DISPOSABLE AUTOINJECTORS

- 10.2.1 EASE OF USE AND REDUCED RISK OF NEEDLESTICK INJURIES TO PROPEL MARKET GROWTH

- 10.3 REUSABLE AUTOINJECTORS

- 10.3.1 COST-EFFECTIVENESS, ADAPTABILITY, AND SUSTAINABILITY TO DRIVE MARKET EXPANSION

11 AUTOINJECTORS MARKET, BY ACTUATION MECHANISM

- 11.1 INTRODUCTION

- 11.2 MECHANICAL (SPRING-BASED) AUTOINJECTORS

- 11.2.1 USER-FRIENDLY DESIGN AND INCREASED PATIENT CONTROL TO AUGMENT MARKET GROWTH

- 11.3 ELECTRONIC AUTOINJECTORS

- 11.3.1 EASE OF ACCURATE DOCUMENTATION AND COMPREHENSIVE PATIENT RECORDS TO SUPPORT MARKET GROWTH

12 AUTOINJECTORS MARKET, BY ROUTE OF ADMINISTRATION

- 12.1 INTRODUCTION

- 12.2 SUBCUTANEOUS ADMINISTRATION

- 12.2.1 EASE OF USE, RAPID ABSORPTION, AND SUITABILITY FOR SELF-ADMINISTRATION TO AID MARKET GROWTH

- 12.3 INTRAMUSCULAR ADMINISTRATION

- 12.3.1 NEED FOR PRECISE DOSE DELIVERY IN EMERGENCY CLINICAL SETTINGS TO DRIVE MARKET

13 AUTOINJECTORS MARKET, BY THERAPY AREA

- 13.1 INTRODUCTION

- 13.2 RHEUMATOID ARTHRITIS

- 13.2.1 HIGH DISEASE PREVALENCE AND NEED FOR FREQUENT DOSING TO DRIVE MARKET

- 13.3 DIABETES

- 13.3.1 LARGE DIABETIC POPULATION AND EASE OF ADMINISTRATION TO STIMULATE DEMAND

- 13.4 ANAPHYLAXIS

- 13.4.1 REQUIREMENT FOR PROMPT INITIAL TREATMENT FOR PATIENTS WITH FOOD ALLERGIES TO FUEL MARKET GROWTH

- 13.5 MULTIPLE SCLEROSIS

- 13.5.1 AVAILABILITY OF COST-EFFECTIVE GENERIC ORAL MULTIPLE SCLEROSIS DRUGS TO LIMIT MARKET GROWTH

- 13.6 OBESITY

- 13.6.1 INCREASING FOCUS ON WEIGHT MANAGEMENT TO BOOST MARKET GROWTH

- 13.7 OTHER THERAPY AREAS

14 AUTOINJECTORS MARKET, BY DRUG TYPE

- 14.1 INTRODUCTION

- 14.2 BIOLOGICS

- 14.2.1 INCREASING USE IN INJECTABLE THERAPIES AND SELF-ADMINISTRATION TO DRIVE MARKET

- 14.3 BIOSIMILARS

- 14.3.1 COST-EFFECTIVE ALTERNATIVES ACCELERATING MARKET EXPANSION

- 14.4 SMALL MOLECULES

- 14.4.1 CRITICAL ROLE IN SELECTIVE INJECTABLES AND EMERGENCY USE CASES

15 AUTOINJECTORS MARKET, BY VOLUME

- 15.1 INTRODUCTION

- 15.2 UP TO 3ML

- 15.2.1 RISING PREVALENCE OF AUTOIMMUNE DISORDERS AND LONG-TERM CHRONIC DISEASES TO PROPEL MARKET GROWTH

- 15.3 ABOVE 3ML

- 15.3.1 INCREASING FOCUS ON COMPLEX TREATMENTS WITH HIGH-VISCOSITY DRUGS TO DRIVE THE MARKET

16 AUTOINJECTORS MARKET, BY END USER

- 16.1 AUTOINJECTOR DEVICE END USERS

- 16.1.1 PHARMACEUTICAL & BIOTECH COMPANIES

- 16.1.1.1 Expanding pipelines, advancements, and rising patient adherence to propel market

- 16.1.2 CONTRACT DEVELOPMENT & MANUFACTURING ORGANIZATIONS

- 16.1.2.1 Growing trend of outsourcing and demand for specialized drug-device manufacturing capabilities support growth

- 16.1.1 PHARMACEUTICAL & BIOTECH COMPANIES

- 16.2 FINISHED FORMULATION AUTOINJECTOR END USERS

- 16.2.1 HOME CARE SETTINGS

- 16.2.1.1 Cost-effectiveness and increased availability of home care support services to propel market growth

- 16.2.2 HOSPITALS & CLINICS

- 16.2.2.1 Technological advancements and availability of real-time patient data to support market growth

- 16.2.3 AMBULATORY CARE CENTERS

- 16.2.3.1 Growing demand for outpatient services to fuel market growth

- 16.2.4 OTHER END USERS

- 16.2.1 HOME CARE SETTINGS

17 AUTOINJECTORS MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 17.2.2 US

- 17.2.2.1 US holds largest share in North American

- 17.2.3 CANADA

- 17.2.3.1 Aging population and increasing prevalence of allergies to propel market growth

- 17.3 EUROPE

- 17.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 17.3.2 GERMANY

- 17.3.2.1 Growing investments and increasing government spending on healthcare to drive market

- 17.3.3 UK

- 17.3.3.1 Increase in prevalence of lifestyle diseases and allergies supports demand growth

- 17.3.4 FRANCE

- 17.3.4.1 Favorable reimbursement policies and increased investment to drive market growth

- 17.3.5 ITALY

- 17.3.5.1 Rising elderly population pool to drive the market

- 17.3.6 SPAIN

- 17.3.6.1 Favorable reimbursement scenario and prevalence of chronic disease

- 17.3.7 NETHERLANDS

- 17.3.7.1 Strong healthcare system and aging population drive market growth

- 17.3.8 REST OF EUROPE

- 17.4 ASIA PACIFIC

- 17.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 17.4.2 JAPAN

- 17.4.2.1 High healthcare expenditure, favorable reimbursement, and insurance coverage to support market growth

- 17.4.3 CHINA

- 17.4.3.1 Increase in prevalence of lifestyle diseases and allergies drives market growth

- 17.4.4 INDIA

- 17.4.4.1 Increasing burden of diabetes and cardiovascular diseases to spur market growth

- 17.4.5 AUSTRALIA

- 17.4.5.1 Growing older population and rising prevalence of target diseases to propel market

- 17.4.6 SOUTH KOREA

- 17.4.6.1 Rising obesity and chronic disease burden propel market growth

- 17.4.7 THAILAND

- 17.4.7.1 Rising geriatric population and chronic disease burden driving autoinjectors market growth

- 17.4.8 VIETNAM

- 17.4.8.1 Aging population and healthcare expansion aiding autoinjectors market growth in Vietnam

- 17.4.9 REST OF ASIA PACIFIC

- 17.5 LATIN AMERICA

- 17.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 17.5.2 BRAZIL

- 17.5.2.1 Rising obesity to stimulate market growth

- 17.5.3 MEXICO

- 17.5.3.1 Rising disease burden to support market growth

- 17.5.4 REST OF LATIN AMERICA

- 17.6 MIDDLE EAST & AFRICA

- 17.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 17.6.2 GCC COUNTRIES

- 17.6.2.1 Kingdom of Saudi Arabia (KSA)

- 17.6.2.1.1 Strong public investments and rising trend of home care to propel market

- 17.6.2.2 United Arab Emirates

- 17.6.2.2.1 Favorable government strategies for health and infrastructure driving market growth

- 17.6.2.3 Other GCC Countries

- 17.6.2.1 Kingdom of Saudi Arabia (KSA)

- 17.6.3 REST OF MIDDLE EAST & AFRICA

18 COMPETITIVE LANDSCAPE

- 18.1 INTRODUCTION

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 18.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN AUTOINJECTORS MARKET

- 18.3 REVENUE ANALYSIS, 2023-2025

- 18.3.1 REVENUE ANALYSIS: AUTOINJECTOR DEVICES MARKET

- 18.3.2 REVENUE ANALYSIS: FINISHED FORMULATION AUTOINJECTORS MARKET

- 18.4 MARKET SHARE ANALYSIS, 2025

- 18.4.1 MARKET SHARE ANALYSIS: AUTOINJECTOR DEVICES MARKET

- 18.4.2 MARKET SHARE ANALYSIS: FINISHED FORMULATION AUTOINJECTORS MARKET

- 18.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.5.1 AUTOINJECTOR DEVICES MARKET

- 18.5.1.1 Stars

- 18.5.1.2 Emerging leaders

- 18.5.1.3 Pervasive players

- 18.5.1.4 Participants

- 18.5.1.5 Company footprint: key players, 2025

- 18.5.1.5.1 Company footprint

- 18.5.1.5.2 Region footprint

- 18.5.1.5.3 Usage footprint

- 18.5.1.5.4 Volume footprint

- 18.5.1.5.5 Route of administration footprint

- 18.5.2 FINISHED FORMULATION AUTOINJECTORS MARKET

- 18.5.2.1 Stars

- 18.5.2.2 Emerging leaders

- 18.5.2.3 Pervasive players

- 18.5.2.4 Participants

- 18.5.2.5 Company footprint: key players, 2025

- 18.5.2.5.1 Company footprint

- 18.5.2.5.2 Region footprint

- 18.5.2.5.3 Usage footprint

- 18.5.2.5.4 Volume footprint

- 18.5.2.5.5 Route of administration footprint

- 18.5.1 AUTOINJECTOR DEVICES MARKET

- 18.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.6.1 AUTOINJECTOR DEVICES MARKET

- 18.6.1.1 Progressive companies

- 18.6.1.2 Responsive companies

- 18.6.1.3 Dynamic companies

- 18.6.1.4 Starting blocks

- 18.6.1.5 Competitive benchmarking: Startups/SMEs, 2025

- 18.6.1.6 Competitive benchmarking of key startup/SME players

- 18.6.2 FINISHED FORMULATION AUTOINJECTORS MARKET

- 18.6.2.1 Progressive companies

- 18.6.2.2 Responsive companies

- 18.6.2.3 Dynamic companies

- 18.6.2.4 Starting blocks

- 18.6.2.5 Competitive benchmarking: startups/SMEs, 2025

- 18.6.2.6 Competitive benchmarking of key startup/SME players

- 18.6.1 AUTOINJECTOR DEVICES MARKET

- 18.7 COMPANY VALUATION AND FINANCIAL METRICS

- 18.7.1 FINANCIAL METRICS

- 18.7.2 COMPANY VALUATION

- 18.8 BRAND COMPARISON

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES & APPROVALS

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

- 18.9.4 PRODUCT LAUNCHES & APPROVALS

- 18.9.5 DEALS

- 18.9.6 EXPANSIONS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS: AUTOINJECTOR DEVICES MARKET

- 19.1.1 SHL MEDICAL AG

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Expansions

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 YPSOMED AG

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Expansions

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 WEST PHARMACEUTICAL SERVICES, INC.

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Expansions

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 BECTON, DICKINSON AND COMPANY (BD)

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Deals

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 PHILLIPS-MEDISIZE

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Expansions

- 19.1.6 HALOZYME, INC.

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.7 OWEN MUMFORD

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches

- 19.1.7.3.2 Deals

- 19.1.1 SHL MEDICAL AG

- 19.2 KEY PLAYERS: FINISHED FORMULATION AUTOINJECTORS MARKET

- 19.2.1 ELI LILLY AND COMPANY

- 19.2.1.1 Business overview

- 19.2.1.2 Products offered

- 19.2.1.3 Recent developments

- 19.2.1.3.1 Product approvals

- 19.2.1.3.2 Deals

- 19.2.1.3.3 Expansions

- 19.2.1.4 MnM view

- 19.2.1.4.1 Key strengths

- 19.2.1.4.2 Strategic choices

- 19.2.1.4.3 Weaknesses and competitive threats

- 19.2.2 ABBVIE INC.

- 19.2.2.1 Business overview

- 19.2.2.2 Products offered

- 19.2.2.3 Recent developments

- 19.2.2.3.1 Product approvals

- 19.2.2.3.2 Deals

- 19.2.2.4 MnM view

- 19.2.2.4.1 Key strengths

- 19.2.2.4.2 Strategic choices

- 19.2.2.4.3 Weaknesses and competitive threats

- 19.2.3 SANOFI

- 19.2.3.1 Business overview

- 19.2.3.2 Products offered

- 19.2.3.3 Recent developments

- 19.2.3.3.1 Product approvals

- 19.2.3.4 MnM view

- 19.2.3.4.1 Key strengths

- 19.2.3.4.2 Strategic choices

- 19.2.3.4.3 Weaknesses and competitive threats

- 19.2.4 NOVO NORDISK A/S

- 19.2.4.1 Business overview

- 19.2.4.2 Products offered

- 19.2.4.3 Recent developments

- 19.2.4.3.1 Product approvals

- 19.2.4.3.2 Deals

- 19.2.4.3.3 Expansions

- 19.2.4.3.4 Other developments

- 19.2.5 AMGEN INC.

- 19.2.5.1 Business overview

- 19.2.5.2 Products offered

- 19.2.5.3 Recent developments

- 19.2.5.3.1 Product launches

- 19.2.5.3.2 Expansions

- 19.2.5.3.3 Other developments

- 19.2.6 JOHNSON & JOHNSON

- 19.2.6.1 Business overview

- 19.2.6.2 Products offered

- 19.2.6.3 Recent developments

- 19.2.6.3.1 Product approvals

- 19.2.6.3.2 Other developments

- 19.2.7 GSK PLC

- 19.2.7.1 Business overview

- 19.2.7.2 Products offered

- 19.2.7.3 Recent developments

- 19.2.7.3.1 Product approvals

- 19.2.8 ASTRAZENECA

- 19.2.8.1 Business overview

- 19.2.8.2 Products offered

- 19.2.8.3 Recent developments

- 19.2.8.3.1 Product approvals

- 19.2.8.3.2 Deals

- 19.2.8.3.3 Expansions

- 19.2.8.3.4 Other developments

- 19.2.1 ELI LILLY AND COMPANY

- 19.3 OTHER PLAYERS

- 19.3.1 GERRESHEIMER AG

- 19.3.2 HASELMEIER GMBH

- 19.3.3 SMC LTD

- 19.3.4 KALEO, INC.

- 19.3.5 SOLTEAM INCORPORATION CO., LTD.

- 19.3.6 ELCAM DRUG DELIVERY DEVICES

- 19.3.7 CROSSJECT

- 19.3.8 JABIL, INC.

- 19.3.9 CONGRUENCE MEDICAL SOLUTIONS LLC

- 19.3.10 MIDAS PHARMA GMBH

- 19.3.11 XERIS PHARMACEUTICALS, INC.

- 19.3.12 WINDGAP MEDICAL, INC

- 19.3.13 ALTAVIZ

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.2 RESEARCH METHODOLOGY DESIGN

- 20.2.1 SECONDARY DATA

- 20.2.1.1 Key data from secondary sources

- 20.2.2 PRIMARY DATA

- 20.2.2.1 Key industry insights

- 20.2.1 SECONDARY DATA

- 20.3 MARKET SIZE ESTIMATION: AUTOINJECTOR DEVICES

- 20.4 MARKET SIZE ESTIMATION: FINISHED FORMULATIONS

- 20.4.1 SEGMENTAL MARKET ESTIMATION (TOP-DOWN APPROACH)

- 20.5 MARKET GROWTH RATE PROJECTIONS

- 20.6 DATA TRIANGULATION

- 20.7 MARKET SHARE ANALYSIS

- 20.8 RESEARCH ASSUMPTIONS

- 20.8.1 GROWTH RATE ASSUMPTIONS

- 20.9 RISK ASSESSMENT

- 20.10 LIMITATIONS

- 20.10.1 METHODOLOGY-RELATED LIMITATIONS

- 20.10.2 SCOPE-RELATED LIMITATIONS

- 20.11 RISK ANALYSIS

21 APPENDIX

- 21.1 DISCUSSION GUIDE

- 21.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.3 CUSTOMIZATION OPTIONS

- 21.3.1 COMPANY INFORMATION

- 21.3.2 GEOGRAPHIC ANALYSIS

- 21.3.3 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 21.3.4 COUNTRY-LEVEL VOLUME ANALYSIS

- 21.3.5 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 21.4 RELATED REPORTS

- 21.5 AUTHOR DETAILS