|

시장보고서

상품코드

2031737

제약·바이오테크놀러지용 웨어러블 디바이스 시장 예측(-2031년) : 제품별, 치료 분야별, 용도별, 최종사용자별, 지역별Wearables in Pharma & Biotech Market by Product, Therapy, Application, End User - Global Forecasts to 2031 |

||||||

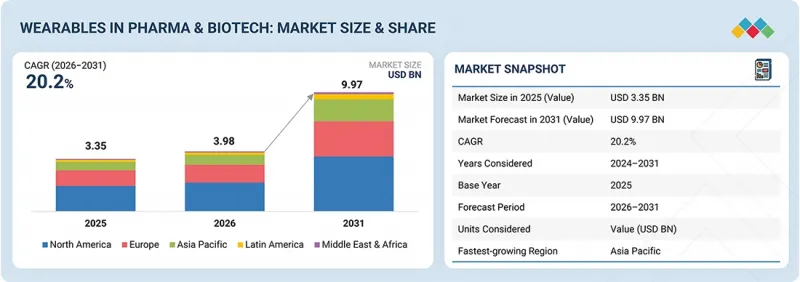

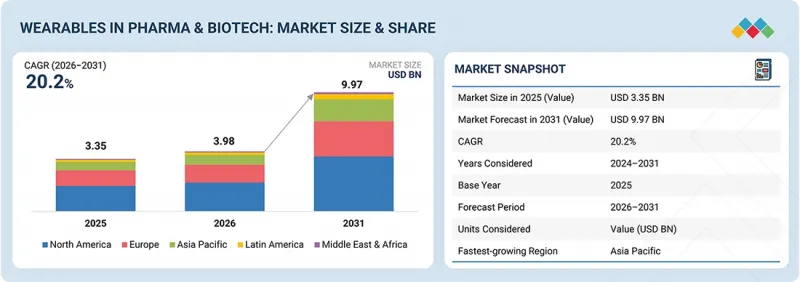

제약·바이오테크놀러지용 웨어러블 디바이스 시장 규모는 2026년 39억 8,000만 달러에서 2031년까지 99억 7,000만 달러에 달할 것으로 예측되고 있으며, CAGR은 20.2%에 달할 전망입니다.

이 시장은 바이오센서, 소형화, 디지털화의 급속한 기술 발전에 의해 주도되고 있습니다. 전 세계 디지털 연결성의 향상도 웨어러블 시장 확대를 촉진하는 중요한 요인 중 하나입니다. 국제전기통신연합(ITU)의 보고서에 따르면 2023년 전 세계 54억 명 이상이 인터넷을 사용한다고 합니다. 이러한 광범위한 연결성을 통해 웨어러블 기기의 데이터를 클라우드 환경에 원활하게 통합할 수 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 치료 분야별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

또한 'All of Us' 연구 프로그램은 50만 명 이상의 참가자를 모집하고 있으며, 그 중 일부는 웨어러블 기기를 통해 활동 수준, 심박수, 수면 패턴 등의 데이터를 제공하고 있습니다. 이는 대규모 생물의학 연구와 정밀의료에서 웨어러블 기술의 역할이 확대되고 있음을 반영합니다. 이러한 성장은 원격 환자 모니터링(RPM)과 디지털 케어 솔루션의 도입 확대에 힘입어 더욱 가속화되고 있습니다. 미국 메디케어-메디케이드 서비스 센터(CMS)는 2022년 정책 확대에 따라 원격 생리적 모니터링 서비스에 대한 상환 청구가 크게 증가했다고 보고했습니다. 이는 의료진들 사이에서 웨어러블 기기를 활용한 진료가 널리 보급되고 있음을 보여줍니다. 또한 센서의 정확도와 다항목 모니터링 기술의 발전으로 웨어러블 기기는 기본적인 바이탈 사인를 넘어 임상적으로 중요한 평가지표를 측정할 수 있게 되었습니다. 이로 인해 의약품의 안전성 및 치료 관련 연구에서 웨어러블 기기의 적용 범위가 확대되고 있습니다.

"제품별로는 지속혈당측정기(CGM) 부문이 가장 큰 시장점유율을 차지하고 있습니다. "

제품 부문은 스마트워치, 피트니스 밴드, 스마트 링, 연속 혈당 측정기(CGM), 패치, 웨어러블 주사기, 기타로 분류됩니다. CGM 부문은 임상 가이드라인의 높은 지지, 적응증 환자군의 확대, 그리고 최첨단 당뇨병 관리 시스템과의 병용이 가능하므로 큰 시장 점유율을 차지하고 있습니다. 미국당뇨병학회는 2024년판 '치료 표준(Standards of Care)'에 따라 광범위한 당뇨병 환자군에 CGM 사용을 권장하고 있으며, 이에 따라 시장 규모가 확대되고 있습니다. 또한 국민보건서비스(NHS)를 통해 수십만 명의 환자들이 급여를 받을 수 있게된 것도 이 지역 시장 확대에 기여하고 있습니다. 또한 미국 식품의약국(FDA)이 인슐린 투여 시스템과 함께 사용할 수 있는 상호 운용 가능한 CGM을 승인한 것도 이 지역 시장 확대에 힘을 실어주고 있습니다. 또한 이 기기들은 하루에 최대 288회까지 혈당 측정이 가능하여 시장에서 매우 높은 가치를 제공하고 있습니다.

"최종사용자별로 보면 2025년 제약 및 생명공학 기업이 가장 큰 시장 점유율을 차지했습니다. "

2025년 제약 및 생명공학 분야의 웨어러블 기기 시장에서는 제약 및 생명공학 기업이 시장 점유율 측면에서 주도적인 위치를 차지했습니다. 이는 주로 임상 시험의 복잡성 때문에 제약 및 생명공학 기업이 데이터 수집을 위해 웨어러블 기술을 필요로 하기 때문입니다. Tufts Center for the Study of Drug Development(Tufts Center for the Study of Drug Development)의 조사에 따르면 현재 임상시험 프로토콜에는 평균 20개 이상의 평가지표가 포함되어 있으며, 데이터 수집의 필요성이 증가하고 있습니다. 이러한 상황에서 웨어러블 기술의 활용은 점점 더 확대되고 있습니다. 또한 영국 바이오뱅크(UK Biobank)와 같은 대규모 연구 구상에서 웨어러블 기술을 성공적으로 활용하여 10만 명 이상의 피험자로부터 데이터를 수집하는 등 제약 연구에서의 웨어러블 기술의 잠재력이 부각되고 있습니다. 이러한 상황을 감안할 때, 제약 및 생명공학 기업은 앞으로도 이 시장의 주요 최종사용자로 남을 것으로 보입니다.

"예측 기간 중 아시아태평양이 가장 높은 성장률을 기록할 것으로 예상"

아시아태평양은 제약 및 바이오 시장내 웨어러블 분야에서 가장 높은 성장률을 기록하고 있습니다. 이러한 성장은 디지털 헬스 인프라의 개선, 임상 연구 활동의 증가, 그리고 충분한 의료 서비스를 받지 못하는 환자의 수가 매우 많다는 점 등 여러 가지 요인에 기인하는 것으로 보입니다. WHO에 따르면 서태평양 지역과 동남아시아 지역을 합친 지역이 전 세계 질병 부담의 상당 부분을 차지하고 있습니다. 국제전기통신연합(ITU)에 따르면 아시아태평양의 인터넷 보급률은 최근 66%에서 70%를 넘어섰습니다. 또한 중국, 인도 등의 국가들이 임상시험의 거점으로 부상하고 있으며, 이들 지역에서는 이미 수천 건의 임상시험이 진행되고 있는 것으로 확인되고 있습니다. 이러한 임상시험의 효율성을 높이기 위해 기술이 도입되고 있습니다. 2024년 9월, Biobeat는 Infinity Pharma와의 제휴를 통해 아르헨티나와 칠레로 사업 확장을 발표했습니다.

Abbott(미국), Dexcom, Inc.(미국), Masimo(미국)는 제약 및 생명공학 분야의 주요 웨어러블 기기 기업 중 일부입니다.

- 제약 및 바이오테크놀러지 시장의 웨어러블 분야 주요 기업에 대해 기업 개요, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 실시했습니다.

조사 범위

본 조사 보고서는 제약 및 바이오테크놀러지 분야의 웨어러블 시장을 제품별, 치료분야별, 용도별, 최종사용자별, 지역별로 분석하고 있습니다. 이 보고서는 제약 및 바이오테크놀러지 분야 웨어러블 디바이스의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전과제, 기회 등)에 대해 상세히 조사하여 정리 정리했습니다. 웨어러블 디바이스(웨어러블 기기)의 주요 기업 개요, 솔루션, 서비스, 주요 전략, 계약, 파트너십, 합의사항, 신제품 및 서비스 출시, 인수합병, 최근 제약 및 바이오테크놀러지의 웨어러블 기기 관련 동향에 대한 인사이트를 제공합니다. 제공하고 있습니다. 이 보고서에서는 시장 생태계내 신생 스타트업의 경쟁 분석도 함께 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 제약 및 생명공학 시장의 웨어러블 및 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 이 시장의 시장 리더와 신규 진입자에게 도움을 줄 수 있습니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 제약, 도전 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(가치 기반 및 환자 중심 의료 모델로의 전환, 지속적인 환자 모니터링이 필요한 만성질환의 유병률 증가, 의료의 급속한 디지털화 및 원격의료 서비스 확대), 제약 요인(의료 제공자의 높은 도입 및 통합 비용, 데이터 프라이버시 및 사이버 보안 우려), 기회(원격 환자 모니터링 및 재택 의료 모델 확대, 첨단 분석 및 맞춤형 의료 통합), 도전 과제(기존 의료 IT 시스템의 상호운용성 제한) 사이버 보안에 대한 우려), 기회(원격 환자 모니터링 및 재택 진료 모델의 확대, 고급 분석 및 맞춤형 의료의 통합), 도전 과제(기존 의료 IT 시스템과의 상호운용성 제한, 낮은 환자 채택률 및 디지털 리터러시 장벽), 제약 및 바이오테크놀러지 분야에서의 제약 및 생명공학 분야에서 웨어러블 디바이스의 성장에 영향을 미치는 요인을 분석합니다.

- 제품 개발 및 혁신: 제약 및 생명공학 시장의 웨어러블 분야, 향후 기술 동향, 연구개발 활동, 신제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보. 이 보고서에서는 다양한 지역의 제약 및 생명공학 분야의 웨어러블 디바이스를 분석합니다.

- 시장 다각화: 제약-바이오 시장의 웨어러블 분야 신제품 및 서비스, 미개발 지역, 최근 동향 및 투자에 대한 포괄적인 정보 제공

- 경쟁사 분석: 제약/바이오테크놀러지 분야 웨어러블 시장에서 BD(미국), Abbott(미국), Masimo(미국), DexCom, Inc. 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 제약·바이오테크놀러지용 웨어러블 디바이스 시장(제품별)

제10장 제약·바이오테크놀러지용 웨어러블 디바이스 시장(치료 분야별)

제11장 제약·바이오테크놀러지용 웨어러블 디바이스 시장(용도별)

제12장 제약·바이오테크놀러지용 웨어러블 디바이스 시장(최종사용자별)

제13장 제약·바이오테크놀러지용 웨어러블 디바이스 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.05.21The wearables in pharma & biotech market is projected to reach USD 9.97 billion by 2031 from USD 3.98 billion in 2026, at a CAGR of 20.2%. The market is driven by rapid technological developments in biosensors, miniaturization, and digitization. Increasing global digital connectivity is another significant facilitator of the expanding wearable market. The International Telecommunication Union reported that over 5.4 billion people worldwide were using the internet in 2023. This widespread connectivity is enabling the seamless integration of data from wearable devices into cloud environments.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Therapeutic Area, Application, End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Additionally, the All of Us Research Program has recruited more than 500,000 participants, some of whom are contributing data from wearables, including activity levels, heart rate, and sleep patterns. This reflects the growing role of wearable technology in large-scale biomedical research and precision medicine. This growth is further supported by the increasing adoption of remote patient monitoring (RPM) and digital care solutions. In the US, the Centers for Medicare & Medicaid Services reported a substantial increase in reimbursement claims for remote physiological monitoring services following the expansion of the policy in 2022. This indicates widespread adoption of wearable-derived care among healthcare providers. In addition, developments in the accuracy of sensors and multi-parameter monitoring are allowing wearables to measure clinically significant endpoints beyond basic vital signs. This is expanding the scope of wearables in drug safety and therapeutic studies.

"By product, continuous glucose monitors (CGMs) segment to account for largest market share"

The product segment is divided into smartwatches, fitness bands, smart rings, continuous glucose monitors (CGMs), patches, wearable injectors, and others. The CGMs segment has a large market share due to the high level of support from clinical guidelines, increasing scope of eligible patients, and the ability of the devices to be used with the most advanced diabetic management systems. The American Diabetes Association recommends the use of CGMs for a broad population of diabetic patients, as per the 2024 Standards of Care, thereby increasing the scope of the market. Furthermore, the availability of reimbursement schemes for hundreds of thousands of patients through the National Health Service has also helped the market expand in the region. In addition, approvals by the Food and Drug Administration for interoperable CGMs used in conjunction with insulin delivery systems have also helped the market expand in the region. The devices also provide up to 288 glucose readings in a day, making them highly valuable in the market .

"By end user, pharmaceutical and biotech companies accounted for largest market share in 2025"

Pharmaceutical and biotech companies dominated the market for wearables in the pharma & biotech market in terms of market share in 2025. This is mainly attributed to the complexity of clinical trials, where pharmaceutical and biotech companies require wearable technologies for data collection. According to a study by the Tufts Center for the Study of Drug Development, clinical trial protocols currently involve more than 20 endpoints on average, thus increasing the requirement for data collection. Wearable technologies are increasingly being used in this context. Furthermore, large-scale research initiatives, such as the UK Biobank, have successfully used wearable technologies for data collection from over 100,000 individuals, thus highlighting the potential of wearable technologies in pharmaceutical research. Considering this, pharmaceutical and biotech companies are likely to remain a dominant end user in this market .

"Asia Pacific to witness highest growth rate during forecast period"

The Asia Pacific (APAC) region is experiencing the highest growth rate in the wearables in pharma & biotech market. This growth can be attributed to several factors, including improvements in digital health infrastructure, a rise in clinical research activities, and a significant number of underserved patients. According to the WHO, the combined Western Pacific and Southeast Asia regions contribute a large share to the world's disease burden. It has been mentioned by the International Telecommunication Union that the penetration of the Internet in the APAC region has surpassed 66% to 70% in recent years. Additionally, it has been observed that countries like China and India are emerging as hubs for clinical trials, with thousands of trials already conducted in these regions. Technology is being adopted to enhance the efficiency of these trials. In September 2024, Biobeat announced its expansion into Argentina and Chile through a partnership with Infinity Pharma.

The breakdown of primary participants is as given below:

- By Company Type - Tier 1: 60%, Tier 2: 30%, and Tier 3: 10%

- By Designation - C-level: 30%, Director-level: 50%, and Others: 20%

- By Region - North America: 45%, Europe: 20%, Asia Pacific: 25%, Rest of the World: 10%.

Abbott (US), Dexcom, Inc. (US), and Masimo (US) are some of the key players in the wearables in pharma & biotech market.

- The study includes an in-depth competitive analysis of these key players in the wearables in pharma & biotech market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the wearables in pharma & biotech market by Product (Smartwatches, Fitness Bands, Smart Rings, Continuous Glucose Monitors (CGM), Patches, Wearable Injectors, Others), Therapeutic Area (cardiovascular (atherosclerotic cardiovascular disease (ASCVD) / secondary prevention, heart failure (HFREF and HFPEF), hypertension, atrial fibrillation (AF) / stroke prevention, pulmonary hypertension, structural heart disease / interventional cardiology), oncology (solid tumors, hematologic malignancies), diabetes, mental health & behavioral health, respiratory disorders, lifestyle & wellness improvement, neurology, musculoskeletal disorders / pain management, women's health & reproductive health, other diseases), Application (drug discovery, clinical trials (phase ii, phase iii, phase iv), medication adherence & behavioral support, chronic disease monitoring, personalized & preventive digital therapeutics), end user (pharmaceutical & biotech companies, healthcare providers & clinicians, other end users), and region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the wearables in pharma & biotech market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, mergers & acquisitions, and recent developments associated with the wearables in pharma & biotech market. Competitive analysis of upcoming startups in the market ecosystem is covered in this report.

Reasons to Buy this Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the wearables in pharma & biotech market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Shift toward value-based and patient-centric healthcare models, Rising prevalence of chronic diseases requiring continuous patient monitoring, Rapid digitalization of healthcare and expansion of telehealth services) restraints (High implementation and integration costs for healthcare providers, Data privacy and cybersecurity concerns) opportunities (Expansion of remote patient monitoring and home-based care models, Integration of advanced analytics and personalized healthcare) and challenges (Interoperability limitations with existing healthcare IT systems, Low patient adoption and digital literacy barriers) influencing the growth of the wearables in pharma & biotech market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the wearables in pharma & biotech market

- Market Development: Comprehensive information about lucrative markets; the report analyses the wearables in pharma & biotech market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the wearables in pharma & biotech market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like BD (US), Abbott (US), Masimo (US), DexCom, Inc. (US), Medtronic (Ireland), among others, in the wearables in pharma & biotech market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING WEARABLES IN PHARMA & BIOTECH MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR WEARABLES IN PHARMA & BIOTECH MARKET

- 3.2 NORTH AMERICA WEARABLES IN PHARMA & BIOTECH MARKET, BY END USER AND COUNTRY

- 3.3 WEARABLES IN PHARMA & BIOTECH MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Shift toward value-based and patient-centric healthcare models

- 4.2.1.2 Prevalence of chronic diseases requiring continuous patient monitoring

- 4.2.1.3 Rapid digitalization of healthcare and expansion of telehealth services

- 4.2.2 RESTRAINTS

- 4.2.2.1 High implementation and integration costs

- 4.2.2.2 Data privacy and cybersecurity concerns

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of remote patient monitoring and home-based care models

- 4.2.3.2 Integration of advanced analytics and personalized healthcare

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited interoperability with existing healthcare IT systems

- 4.2.4.2 Low patient adoption and digital literacy barriers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS (MODERATE)

- 5.1.2 BARGAINING POWER OF BUYERS (MODERATE TO HIGH)

- 5.1.3 THREAT OF SUBSTITUTES (LOW TO MODERATE)

- 5.1.4 THREAT OF NEW ENTRANTS (MODERATE)

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY PRODUCT, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY REGION, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 9018)

- 5.6.2 EXPORT DATA (HS CODE 9018)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.11 IMPACT OF 2025 US TARIFF

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE INDUSTRIES

- 5.11.4.1 Pharmaceutical & biotech companies

- 5.11.4.2 Healthcare providers & clinicians

- 5.11.4.3 Other end users

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ADVANCED BIOSENSING AND MULTI-PARAMETER WEARABLES

- 6.1.2 AI-DRIVEN ANALYTICS AND CLINICAL INTELLIGENCE

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MOBILE HEALTH AND REMOTE PATIENT MONITORING

- 6.2.2 ANALYTICS AND POPULATION-LEVEL HEALTH DATA INTEGRATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INTERNET OF MEDICAL THINGS AND CONNECTED DEVICES

- 6.3.2 CLOUD AND EDGE COMPUTING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS

- 6.5.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE MONITORING AND CLINICAL DECISION SUPPORT

- 6.6.2 CLOSED-LOOP THERAPEUTIC AND DRUG DELIVERY SYSTEMS

- 6.6.3 DECENTRALIZED AND HYBRID CLINICAL TRIAL ENABLEMENT

- 6.6.4 CONTINUOUS DISEASE MANAGEMENT AND PREVENTIVE HEALTHCARE

- 6.6.5 ADVANCED BIOSENSING AND NON-INVASIVE DIAGNOSTICS

- 6.6.6 INTEGRATION WITH DIGITAL THERAPEUTICS AND PERSONALIZED MEDICINE

- 6.7 IMPACT OF AI/GEN AI

- 6.7.1 MARKET POTENTIAL OF AI/GEN AI

- 6.7.2 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.2.1 AI-driven continuous glucose monitoring and diabetes management at Dexcom

- 6.7.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.3.1 Wearable data analytics and AI-driven monitoring platforms

- 6.7.3.2 Digital health platforms, integration, and regulatory infrastructure

- 6.7.3.3 Clinical care, remote monitoring, and personalized therapeutics

- 6.7.4 USER READINESS AND IMPACT ASSESSMENT

- 6.7.4.1 User readiness

- 6.7.4.1.1 User A: Hospitals, clinics, and long-term care providers

- 6.7.4.1.2 User B: Pharma and biotech companies

- 6.7.4.2 Impact assessment

- 6.7.4.2.1 User A: Hospitals, clinics, and long-term care providers

- 6.7.4.2.1.1 Implementation

- 6.7.4.2.1.2 Impact

- 6.7.4.2.2 User B: Pharma and biotech companies

- 6.7.4.2.2.1 Implementation

- 6.7.4.2.2.2 Impact

- 6.7.4.2.1 User A: Hospitals, clinics, and long-term care providers

- 6.7.4.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 8.4.1 UNMET NEEDS

- 8.4.2 END-USER EXPECTATIONS

- 8.5 MARKET PROFITABILITY

9 WEARABLES IN PHARMA & BIOTECH MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 SMARTWATCHES

- 9.2.1 EXPANDING ROLE IN DIGITAL CLINICAL TRIALS AND REMOTE MONITORING

- 9.3 FITNESS BANDS

- 9.3.1 EMPHASIS ON REAL-WORLD EVIDENCE AND PATIENT-CENTRIC TRIAL DESIGNS

- 9.4 SMART RINGS

- 9.4.1 EMERGING CLINICAL-GRADE WEARABLES ENABLING EARLY DISEASE DETECTION AND CONTINUOUS MONITORING

- 9.5 CONTINUOUS GLUCOSE MONITORS

- 9.5.1 TRANSFORMING METABOLIC RESEARCH THROUGH REAL-TIME, HIGH-FREQUENCY DATA

- 9.6 PATCHES

- 9.6.1 CONTINUOUS, CLINICAL-GRADE MONITORING DRIVING ADOPTION IN DECENTRALIZED TRIALS

- 9.7 WEARABLE INJECTORS

- 9.7.1 GROWING DEMAND FOR SELF-ADMINISTRATION OF BIOLOGICS IN CHRONIC DISEASE MANAGEMENT

- 9.8 OTHER PRODUCTS

10 WEARABLES IN PHARMA & BIOTECH MARKET, BY THERAPEUTIC AREA

- 10.1 INTRODUCTION

- 10.2 CARDIOVASCULAR

- 10.2.1 ATHEROSCLEROTIC CARDIOVASCULAR DISEASES/SECONDARY PREVENTION

- 10.2.1.1 Focus on improving endpoint capture and long-term outcomes monitoring

- 10.2.2 HEART FAILURE

- 10.2.2.1 Continuous physiologic monitoring and AI-enabled decompensation prediction

- 10.2.3 HYPERTENSION

- 10.2.3.1 Cuffless monitoring and AI-driven adherence management enabling precision blood pressure control

- 10.2.4 ATRIAL FIBRILLATION/STROKE PREVENTION

- 10.2.4.1 Rapid expansion of AI-powered arrhythmia detection algorithms and regulatory-cleared wearable ECG technologies

- 10.2.5 PULMONARY HYPERTENSION

- 10.2.5.1 Growing use of wearable-enabled remote monitoring and AI analytics to generate objective, real-world functional endpoints

- 10.2.6 STRUCTURAL HEART DISEASES/INTERVENTIONAL CARDIOLOGY

- 10.2.6.1 Wearable-enabled remote recovery monitoring and procedural optimization supporting precision structural heart care

- 10.2.1 ATHEROSCLEROTIC CARDIOVASCULAR DISEASES/SECONDARY PREVENTION

- 10.3 ONCOLOGY

- 10.3.1 SOLID TUMORS

- 10.3.1.1 BREAST CANCER

- 10.3.1.1.1 Continuous wearable-based survivorship monitoring and decentralized oncology trials driving personalized long-term care models

- 10.3.1.2 LUNG CANCER

- 10.3.1.2.1 Constant respiratory monitoring and decentralized trial adoption

- 10.3.1.3 PROSTATE CANCER

- 10.3.1.3.1 Expansion of decentralized oncology trials and long-term survivorship management

- 10.3.1.4 COLORECTAL CANCER

- 10.3.1.4.1 Increasing adoption of decentralized oncology trials and remote post-surgical monitoring

- 10.3.1.5 BRAIN TUMOR

- 10.3.1.5.1 Remote neurologic surveillance and functional recovery tracking accelerating personalized care

- 10.3.1.6 OTHER SOLID TUMORS

- 10.3.1.1 BREAST CANCER

- 10.3.2 HEMATOLOGIC MALIGNANCIES

- 10.3.2.1 LEUKEMIA

- 10.3.2.1.1 Wearable-enabled infection surveillance and treatment resilience monitoring transforming outpatient care

- 10.3.2.2 LYMPHOMA

- 10.3.2.2.1 Shift toward outpatient infusion centers, home-based recovery, and decentralized clinical trials

- 10.3.2.3 MULTIPLE MYELOMA

- 10.3.2.3.1 Real-time toxicity and mobility tracking using wearables in long-term management

- 10.3.2.4 OTHER HEMATOLOGIC MALIGNANCIES

- 10.3.2.1 LEUKEMIA

- 10.3.3 DIABETES

- 10.3.3.1 Critical need for long-term, real-world metabolic monitoring

- 10.3.4 MENTAL HEALTH & BEHAVIORAL HEALTH

- 10.3.4.1 Rising global burden of psychiatric disorders

- 10.3.5 RESPIRATORY DISORDERS

- 10.3.5.1 Early exacerbation detection through continuous monitoring reduces hospitalization

- 10.3.6 LIFESTYLE & WELLNESS IMPROVEMENT

- 10.3.6.1 Continuous tracking for lifestyle optimization and preventive health risk management

- 10.3.7 NEUROLOGY

- 10.3.7.1 Wearable-based monitoring of neurological function and digital clinical endpoints in CNS disorders

- 10.3.8 MUSCULOSKELETAL DISORDERS/PAIN MANAGEMENT

- 10.3.8.1 Wearable-guided functional movement and chronic pain monitoring in musculoskeletal disorders

- 10.3.9 WOMEN'S HEALTH & REPRODUCTIVE HEALTH

- 10.3.9.1 Continuous physiological and reproductive cycle using wearables

- 10.3.10 OTHER DISEASES

- 10.3.1 SOLID TUMORS

11 WEARABLES IN PHARMA & BIOTECH MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 DRUG DISCOVERY

- 11.2.1 RECENT ADVANCES PROMOTE DISCOVERY OF DRUGS THROUGH WEARABLES IN PHARMA & BIOTECH

- 11.3 CLINICAL TRIALS

- 11.3.1 PHASE II

- 11.3.1.1 AI-enabled remote monitoring and adaptive trial designs accelerate adoption

- 11.3.2 PHASE III

- 11.3.2.1 Rapid expansion of decentralized and hybrid global trial models propels growth

- 11.3.3 PHASE IV

- 11.3.3.1 Ability to improve patient engagement and retention in long-duration studies drives market

- 11.3.1 PHASE II

- 11.4 MEDICATION ADHERENCE & BEHAVIORAL SUPPORT

- 11.4.1 CONNECTED REMINDERS, PASSIVE MONITORING, AND PERSONALIZED NUDGES BOOST ADOPTION

- 11.5 CHRONIC DISEASE MONITORING

- 11.5.1 CONTINUOUS PHYSIOLOGICAL TRACKING AND PROACTIVE INTERVENTION CAPABILITIES INCREASE ADOPTION

- 11.6 PERSONALIZED & PREVENTIVE DIGITAL THERAPEUTICS

- 11.6.1 BIOMETRIC SENSING AND AI-DRIVEN COACHING RAISE DEMAND FOR WEARABLES

12 WEARABLES IN PHARMA & BIOTECH MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 PHARMACEUTICAL & BIOTECH COMPANIES

- 12.2.1 CLINICAL DIGITIZATION, REAL-WORLD EVIDENCE GENERATION, AND CONNECTED THERAPY MODELS DRIVE MARKET

- 12.3 HEALTHCARE PROVIDERS & CLINICIANS

- 12.3.1 REMOTE PATIENT MONITORING, PREVENTIVE CARE, AND DATA-DRIVEN CLINICAL DECISION SUPPORT BOOST GROWTH

- 12.4 CONTRACT RESEARCH ORGANIZATIONS

- 12.4.1 DECENTRALIZED TRIALS, WEARABLE DATA INTEGRATION, AND FASTER CLINICAL EXECUTION RAISE DEMAND

- 12.5 OTHER END USERS

13 WEARABLES IN PHARMA & BIOTECH MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 High concentration of clinical research activity, clinical trial inefficiencies, and cost pressures to drive market

- 13.2.2 CANADA

- 13.2.2.1 Clinical research participation, public health burden, and digital health adoption to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Expanding clinical trial activity and regulatory leadership to drive market

- 13.3.2 FRANCE

- 13.3.2.1 Regulatory-first approach to healthcare and clinical innovation to drive market

- 13.3.3 UK

- 13.3.3.1 Real-world data integration and decentralized trial innovation to drive market

- 13.3.4 ITALY

- 13.3.4.1 Evolving clinical trial landscape and regulatory decentralization to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Increasing investment in digital health infrastructure to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Clinical trial expansion and real-world data integration to drive market

- 13.4.2 JAPAN

- 13.4.2.1 Late-stage trial leadership and regulatory precision to drive market

- 13.4.3 INDIA

- 13.4.3.1 High-volume Phase III trial ecosystem and ABDM-driven digital health integration to drive market

- 13.4.4 AUSTRALIA

- 13.4.4.1 Early-phase trial leadership and remote care needs to drive market

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Integrated clinical trial ecosystem and national health data infrastructure to drive market

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Clinical trial leadership and high diabetes burden to drive market

- 13.5.2 MEXICO

- 13.5.2.1 Regulatory reforms and Phase III trial expansion to drive market

- 13.5.3 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC

- 13.6.2 SAUDI ARABIA

- 13.6.2.1 Vision 2030-led digital health transformation to drive market

- 13.6.3 UAE

- 13.6.3.1 Digital health strategy, clinical trial expansion, and high healthcare investment to drive market

- 13.6.4 REST OF GCC

- 13.6.5 SOUTH AFRICA

- 13.6.5.1 Clinical trial leadership and decentralized care models to drive market

- 13.6.6 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2026

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Product footprint

- 14.7.5.4 Therapeutic area footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2025

- 14.8.5.1 List of start-ups/SMEs

- 14.8.5.2 Competitive benchmarking of start-ups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES AND APPROVALS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 DEXCOM, INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches and approvals

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 ABBOTT

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches and approvals

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 MASIMO

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches and approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 BD

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches and approvals

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 APPLE INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches and approvals

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 BOSTON SCIENTIFIC CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 IRHYTHM TECHNOLOGIES, INC.

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches and approvals

- 15.1.7.3.2 Deals

- 15.1.8 KONINKLIJKE PHILIPS N.V.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches and approvals

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Other developments

- 15.1.9 MEDTRONIC

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 BIOINTELLISENSE, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches and approvals

- 15.1.10.3.2 Deals

- 15.1.11 F. HOFFMANN-LA ROCHE LTD

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches and approvals

- 15.1.12 GE HEALTHCARE

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches and approvals

- 15.1.12.3.2 Deals

- 15.1.13 BIOBEAT

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches and approvals

- 15.1.13.3.2 Deals

- 15.1.13.3.3 Other developments

- 15.1.14 EMPATICA INC.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches and approvals

- 15.1.14.3.2 Deals

- 15.1.15 VITALCONNECT

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.15.3.2 Other developments

- 15.1.16 AMETRIS, LLC

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Deals

- 15.1.17 ALIVECOR, INC.

- 15.1.17.1 Business overview

- 15.1.17.2 Products offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Product launches and approvals

- 15.1.17.3.2 Deals

- 15.1.18 WITHINGS

- 15.1.18.1 Business overview

- 15.1.18.2 Products offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Product launches and approvals

- 15.1.18.3.2 Deals

- 15.1.19 VIVALNK, INC.

- 15.1.19.1 Business overview

- 15.1.19.2 Products offered

- 15.1.19.3 Recent developments

- 15.1.19.3.1 Product launches and approvals

- 15.1.20 MEDIBIOSENSE

- 15.1.20.1 Business overview

- 15.1.20.2 Products offered

- 15.1.20.3 Recent developments

- 15.1.20.3.1 Product launches and approvals

- 15.1.1 DEXCOM, INC.

- 15.2 OTHER PLAYERS

- 15.2.1 SIBEL HEALTH, INC.

- 15.2.2 BYTEFLIES

- 15.2.3 STRADOS LABS

- 15.2.4 ONERA TECHNOLOGIES B.V.

- 15.2.5 EPICORE BIOSYSTEMS, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH APPROACH

- 16.1.1 SECONDARY RESEARCH

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY RESEARCH

- 16.1.2.1 Primary sources

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Insights from primary experts

- 16.1.1 SECONDARY RESEARCH

- 16.2 RESEARCH METHODOLOGY DESIGN

- 16.3 MARKET SIZE ESTIMATION

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.6.1 METHODOLOGY-RELATED

- 16.6.2 SCOPE-RELATED

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS