|

시장보고서

상품코드

2031738

메탄올 엔진 시장 예측(-2035년) : 선박 유형별, 사용법별, 출력별, 건조 형태별, 지역별Methanol Engines Market By Usage, Power, Ship Type, Build, and Region - Global Forecast to 2035 |

||||||

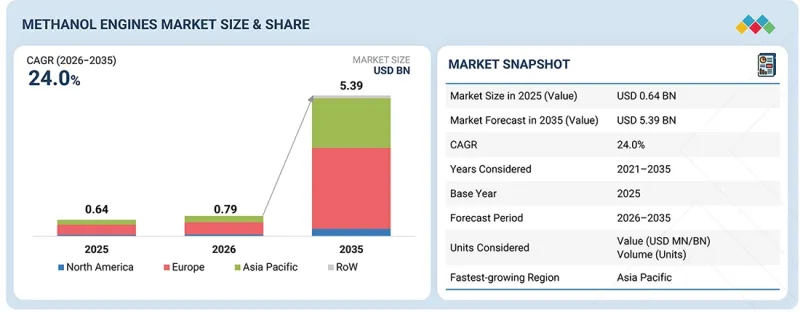

메탄올 엔진 시장 규모는 예측 기간 중 CAGR 24.0%로 확대하며, 2026년 7억 9,000만 달러에서 2035년에는 53억 9,000만 달러에 달할 것으로 전망되고 있습니다.

이 시장의 성장은 해운업계의 장기적인 탈탄소화 목표를 지원하는 연료 유연성 엔진 솔루션의 도입과 배기가스 배출량 감축의 필요성에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2035년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 선박 유형별, 사용법별, 출력별, 건조 형태별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

컨테이너선, 유조선 등 주요 선종에서 메탄올 연료 선박의 수주 증가가 시장 성장을 촉진하고 있습니다. 국제해사기구(IMO)의 배출량 목표, 지역별 정책 등 규제 압력이 높아지면서 도입이 더욱 가속화되고 있습니다. 또한 메탄올 연료 보급 인프라의 개선과 그린 메탄올의 공급 확대로 인해 메탄올 연료는 대규모 도입을 위한 보다 현실적인 선택이 되고 있습니다. 듀얼 연료 엔진 기술의 발전과 레트로핏 솔루션의 확대도 시장 보급 확대에 기여하고 있습니다.

"건조 형태별로는 신조선 부문이 예측 기간 중 가장 큰 비중을 차지할 것으로 예상됩니다. "

신조선 부문은 예측 기간 중 계속해서 주요 부문이 될 것으로 예상됩니다. 이는 메탄올 엔진 도입의 대부분이 처음부터 대체연료 사용을 염두에 두고 설계된 선박과 관련되어 있기 때문입니다. 신조선 프로젝트에서 선주는 개조 전환에 비해 메탄올 저장 설비, 연료 시스템 및 엔진 구성을 보다 효율적으로 통합할 수 있습니다. 이를 통해 특히 운용 수명이 긴 대형 상선에서는 실용성을 높일 수 있습니다. 또한 메탄올 대응 선박 및 메탄올 연료 선박의 수주 증가는 이 부문의 견고한 지위를 지속적으로 지원하고 있습니다.

"용도별로는 발전기 엔진 부문이 2026-2035년까지 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

선주들이 메탄올의 사용 범위를 주 추진에서 선내 보조 동력으로 점차 확대함에 따라 발전기 엔진 부문은 향후 수년간 가장 높은 성장률을 보일 것으로 예상됩니다. 선박의 연료 통합이 진행됨에 따라 메탄올 기반 발전기는 전반적인 탈탄소화를 촉진하고 기존 선박 연료에 대한 의존도를 줄이는 데 있으며, 점점 더 중요한 역할을 하고 있습니다. 또한 정박 및 기타 선내 작업에서 청정 발전에 대한 수요도 그 도입을 촉진하고 있습니다.

"예측 기간 중 유럽이 주요 시장 점유율을 차지할 것으로 예상됩니다. "

유럽은 엄격한 환경 규제와 명확한 탈탄소화 목표에 힘입어 저배출 해운의 선구자 역할을 해왔으며, 2035년까지 메탄올 엔진 시장의 주요 점유율을 차지할 것으로 예상됩니다. 메탄올 전략을 적극적으로 전개하고 있는 많은 주요 선주, 기술 제공업체, 엔진 개발 업체들이 유럽에 기반을 두고 있으며, 이는 수요와 공급의 균형을 유지하는 데 도움이 되고 있습니다. 또한 이 지역에서는 그린 시핑 코리도(Green Shipping Corridor), 항만 정비, 대체연료 인프라 구축 등에서도 활발한 움직임을 보이고 있습니다. 이 모든 것이 유럽이 메탄올 엔진 도입에 있으며, 선도적인 위치를 유지하는 데 기여하고 있습니다.

조사 범위:

이 시장 조사는 다양한 부문 및 하위 부문에 걸친 메탄올 엔진 시장을 대상으로 합니다. 이 조사는 지역 및 분야별 시장 규모와 성장 잠재력을 추정하는 것을 목표로 하고 있습니다. 또한 시장내 주요 업체들의 상세한 경쟁 분석, 기업 개요, 제품 및 사업 제공에 대한 주요 관찰 사항, 최근 동향, 주요 시장 전략에 대해서도 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 시장 리더와 신규 진입자에게 전체 메탄올 엔진 시장 매출에 대한 가장 정확한 추정치를 제공합니다. 또한 이해관계자들이 경쟁 상황을 이해하고, 자신의 비즈니스를 더 나은 위치에 놓고, 적절한 시장 진입 전략을 수립하기 위한 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 시장 촉진요인(배출가스 규제 강화에 따른 청정 선박용 연료로의 전환 가속화, 메탄올 대응 엔진 기술 상용화의 진전), 제약 요인(기존 엔진 대비 높은 초기 비용, 그린 메탄올 연료 공급 부족 및 높은 비용), 기회(기존 선박 개조시 높은 잠재력, 유지보수 및 서비스 매출 증가), 과제(메탄올 연료 취급 및 안전 요구사항, 항만 벙커링 부족) 유지보수 및 서비스 매출 증가), 과제(메탄올 연료 취급 및 안전 요구사항, 항만내 벙커링 인프라 부족)

- 시장 침투도: 시장을 선도하는 주요 기업이 제공하는 메탄올 엔진에 대한 포괄적인 정보

- 제품 개발 및 혁신: 메탄올 엔진 시장의 미래 기술, R&D 활동 및 신제품 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보를 제공합니다.

- 시장 다각화: 메탄올 엔진 시장의 신제품, 미개발 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁 분석: 메탄올 엔진 시장 주요 기업의 시장 점유율, 성장 전략, 제품 및 제조 능력에 대한 상세 분석

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 메탄올 엔진 시장(선박 유형별)

제10장 메탄올 엔진 시장(사용법별)

제11장 메탄올 엔진 시장(출력별)

제12장 메탄올 엔진 시장(건조 형태별)

제13장 메탄올 엔진 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

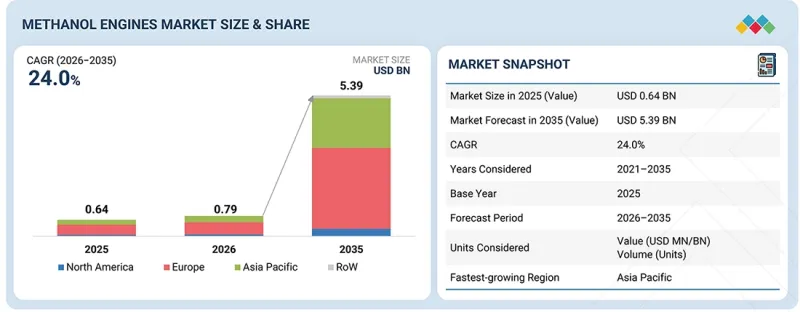

KSA 26.05.21The methanol engines market is anticipated to grow from USD 0.79 billion in 2026 to USD 5.39 billion in 2035, at a CAGR of 24.0% during the forecast period. The market is driven by the need to reduce emissions while adopting fuel-flexible engine solutions that support long-term decarbonization goals in the shipping industry.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By Usage, Power, Ship Type and Region |

| Regions covered | North America, Europe, APAC, RoW |

Growth is supported by the rising number of methanol-fueled vessel orders across key segments, such as container ships and tankers. Increasing regulatory pressure, including IMO emission targets and regional policies, is further accelerating adoption. In addition, improving methanol bunkering infrastructure and growing availability of green methanol are making the fuel more viable for large-scale deployment. Advancements in dual-fuel engine technologies and the expansion of retrofit solutions are also contributing to wider market adoption.

"By build, the newbuild segment is projected to be the most dominant during the forecast period"

Newbuild is expected to remain the leading build segment during the forecast period, as most of the methanol engine adoption is linked to vessels designed from the start for alternative fuel use. Newbuild projects allow shipowners to integrate methanol storage, fuel systems, and engine setup in a more efficient way compared with retrofit conversions. This makes it more practical, especially for large commercial vessels with long operating lives. Additionally, increasing orders for methanol-ready and methanol-fueled vessels are continuing to support the strong position of this segment.

"By usage, the generator engine segment is likely to grow at the highest CAGR from 2026 to 2035"

The generator engine segment is expected to grow at the highest rate over the coming years as shipowners are slowly extending the use of methanol beyond main propulsion and into onboard auxiliary power. As vessels move toward wider fuel integration, methanol-based generators are becoming more relevant for improving overall decarbonization and reducing dependence on conventional marine fuels. Their adoption is also supported by the need for cleaner power generation during hoteling and other onboard operations.

"Europe is projected to capture a major market share during the forecast period"

Europe is expected to hold a major share of the methanol engines market through 2035 as the region has been an early mover in low-emission shipping, which is supported by strong environmental rules and clear decarbonization targets. Many leading shipowners, technology providers, and engine developers with active methanol strategies are based in Europe, which helps in keeping demand and supply aligned. The region is also seeing more activity in green shipping corridors, port readiness, and alternative fuel infrastructure. All of this is helping Europe continue its lead in methanol engine adoption.

The breakdown of profiles for primary participants in the methanol engines market is provided below:

- By Company Type: Tier 1 - 30%, Tier 2 - 45%, and Tier 3 - 25%

- By Designation: Directors - 20%, Managers - 10%, and Others - 70%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 40%, RoW - 10%

Research Coverage:

This market study covers the methanol engines market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall methanol engines market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Stringent emission regulations accelerating shift toward cleaner marine fuel, Growing commercial availability of methanol-ready engine technologies), Restraints (High upfront cost compared with conventional engines, Limited supply and high cost of green methanol fuel), Opportunities (Strong potential to retrofit existing ships, Increasing revenue from maintenance and services), Challenges (Handling and safety requirements for methanol fuel, Limited bunkering infrastructure across ports)

- Market Penetration: Comprehensive information on methanol engines offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the methanol engines market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the methanol engines market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the methanol engines market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 DISRUPTIVE TRENDS SHAPING MARKET

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

- 2.6 BUSINESS MODELS

- 2.6.1 SUPPLY OF ENGINES FOR NEWLY BUILT VESSELS

- 2.6.2 RETROFIT AND CONVERSION MODEL

- 2.6.3 LIFECYCLE SERVICES AND AFTERMARKET SUPPORT

- 2.6.4 TECHNOLOGY LICENSING AND DISTRIBUTED MANUFACTURING

- 2.6.5 INTEGRATED METHANOL POWERTRAIN AND FUEL SYSTEM SOLUTIONS

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN METHANOL ENGINES MARKET

- 3.2 METHANOL ENGINES MARKET, BY USAGE

- 3.3 METHANOL ENGINES MARKET, BY POWER

- 3.4 METHANOL ENGINES MARKET, BY BUILD

- 3.5 METHANOL ENGINES MARKET, BY SHIP TYPE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Stringent emission regulations accelerating shift toward cleaner marine fuel

- 4.2.1.2 Growing commercial availability of methanol-ready engine technologies

- 4.2.1.3 Rising orderbook for methanol-powered vessels supporting market adoption

- 4.2.2 RESTRAINTS

- 4.2.2.1 High upfront cost compared to conventional engines

- 4.2.2.2 Limited supply and high cost of green methanol fuel

- 4.2.2.3 Additional storage requirements due to low energy density of methanol

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Strong potential to retrofit existing ships

- 4.2.3.2 Growing revenue from maintenance and services

- 4.2.3.3 Expansion into diverse ship types and marine segments

- 4.2.4 CHALLENGES

- 4.2.4.1 Handling and safety requirements for methanol fuel

- 4.2.4.2 Limited bunkering infrastructure across ports

- 4.2.4.3 Lack of trained workforce and support ecosystem

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 SCALABLE AND COST-COMPETITIVE GREEN METHANOL SUPPLY

- 4.3.2 STANDARDIZED BUNKERING AND FUEL HANDLING INFRASTRUCTURE

- 4.3.3 FUEL QUALITY CONSISTENCY AND STANDARDIZATION ACROSS SUPPLIERS

- 4.3.4 PROVEN LONG-TERM OPERATIONAL DATA AND PERFORMANCE BENCHMARKS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 MARINE FUEL AND BUNKERING INFRASTRUCTURE MARKET

- 4.4.2 MARINE ENGINE AND SHIPBUILDING MARKET

- 4.4.3 CARBON CAPTURE, UTILIZATION, AND STORAGE (CCUS) MARKET

- 4.4.4 SHIP RETROFIT AND CONVERSION MARKET

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 ECOSYSTEM ANALYSIS

- 5.1.1 ENGINE MANUFACTURERS

- 5.1.2 METHANOL FUEL SUPPLIERS

- 5.1.3 END USERS

- 5.2 VALUE CHAIN ANALYSIS

- 5.2.1 CONCEPT & RESEARCH

- 5.2.2 COMPONENT & MATERIAL DEVELOPMENT

- 5.2.3 ENGINE MANUFACTURING

- 5.2.4 SYSTEM INTEGRATION & VALIDATION

- 5.2.5 POST-DEPLOYMENT SERVICE

- 5.3 TRADE ANALYSIS

- 5.3.1 IMPORT SCENARIO (HS CODE 290511)

- 5.3.2 EXPORT SCENARIO (HS CODE 290511)

- 5.4 CASE STUDY ANALYSIS

- 5.4.1 GREEN MARITIME METHANOL PROJECT: RETROFITTING OF MV EEMSBORG FOR METHANOL PROPULSION

- 5.4.2 STENA LINE: METHANOL RETROFITTING OF STENA GERMANICA FERRY FOR EMISSION REDUCTION

- 5.4.3 CMA CGM: DEPLOYMENT OF METHANOL-FUELED CONTAINER SHIPS FOR DECARBONIZED SHIPPING

- 5.5 KEY CONFERENCES & EVENTS, 2026

- 5.6 INVESTMENT & FUNDING SCENARIO

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 OPERATIONAL DATA

- 5.9 TOTAL COST OF OWNERSHIP (TCO)

- 5.10 MACROECONOMIC OUTLOOK

- 5.10.1 INTRODUCTION

- 5.10.2 GDP TRENDS AND FORECAST

- 5.10.3 TRENDS IN GLOBAL METHANOL ENGINE INDUSTRY

- 5.10.4 TRENDS IN GLOBAL MARINE INDUSTRY

- 5.11 VOLUME DATA

- 5.12 BILL OF MATERIALS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 DUAL-FUEL ENGINE TECHNOLOGY

- 6.1.2 METHANOL FUEL STORAGE AND HANDLING SYSTEMS

- 6.1.3 ADVANCED COMBUSTION AND EMISSION CONTROL TECHNOLOGIES

- 6.1.4 DIGITAL MONITORING, AI, AND ENERGY MANAGEMENT SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 HYBRID PROPULSION AND ENERGY MANAGEMENT SYSTEMS

- 6.2.2 FUEL SYSTEM AUTOMATION, SAFETY AND MONITORING TECHNOLOGIES

- 6.2.3 DIGITAL OPTIMIZATION, ROUTE ANALYTICS, AND SMART SHIPPING SYSTEMS

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GENERATIVE AI

- 6.6.1 IMPLEMENTATION OF AI IN METHANOL ENGINES MARKET: TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 IMPLEMENTATION OF AI IN METHANOL ENGINES MARKET: CASE STUDIES

- 6.6.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.4 CLIENTS' READINESS TO ADOPT AI/GENERATIVE AI

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 ORGANIZATIONS

- 7.1.2 KEY REGULATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT REDUCTION

- 7.2.2 ECO-APPLICATIONS

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 BUYING EVALUATION CRITERIA

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

9 METHANOL ENGINES MARKET, BY SHIP TYPE

- 9.1 INTRODUCTION

- 9.1.1 CONTAINER VESSELS

- 9.1.1.1 Large-scale fleet decarbonization and high fuel consumption to drive adoption of methanol engines in container vessels

- 9.1.2 BULK CARRIERS

- 9.1.2.1 Cost sensitivity and operational efficiency to influence gradual adoption of methanol engines in bulk carriers

- 9.1.3 CHEMICAL TANKERS

- 9.1.3.1 Cargo compatibility and safe fuel integration to drive adoption

- 9.1.4 CAR CARRIERS

- 9.1.4.1 Pressure for emission reduction from automotive supply chains to drive growth

- 9.1.5 OTHER OFFSHORE VESSELS

- 9.1.1 CONTAINER VESSELS

10 METHANOL ENGINES MARKET, BY USAGE

- 10.1 INTRODUCTION

- 10.2 MAIN ENGINE

- 10.2.1 HIGH POWER REQUIREMENTS AND NEED FOR EXTENDED OPERATIONS TO DRIVE ADOPTION OF METHANOL IN MAIN ENGINES

- 10.3 AUXILIARY ENGINE

- 10.3.1 DEMAND FOR LOW-EMISSION ONBOARD POWER SYSTEMS TO SUPPORT GROWTH

- 10.4 GENERATION ENGINE

- 10.4.1 INCREASING ELECTRIFICATION OF MARINE PROPULSION SYSTEMS TO DRIVE DEMAND

11 METHANOL ENGINES MARKET, BY POWER

- 11.1 INTRODUCTION

- 11.2 UP TO 300 KW

- 11.2.1 DEMAND FOR LOW-POWER METHANOL ENGINES TO DRIVE MARKET

- 11.3 301-600 KW

- 11.3.1 EXPANDING USE OF METHANOL ENGINES IN MEDIUM-SIZED VESSELS TO SUPPORT GROWTH

- 11.4 601-900 KW

- 11.4.1 INCREASING DEPLOYMENT OF METHANOL ENGINES IN FERRIES AND WORKBOATS TO DRIVE GROWTH

- 11.5 901-1,200 KW

- 11.5.1 RISING DEMAND FOR HIGH-PERFORMANCE MED-POWER ENGINES TO SUPPORT GROWTH

- 11.6 1,201-1,500 KW

- 11.6.1 RISING USE OF LARGE FERRIES AND SPECIALIZED VESSELS TO DRIVE GROWTH

- 11.7 1,501-1,800 KW

- 11.7.1 DEPLOYMENT OF METHANOL ENGINES IN HEAVY-DUTY MARINE APPLICATIONS TO SUPPORT GROWTH

- 11.8 1,801-2,100 KW

- 11.8.1 DEMAND FOR HIGH-POWER METHANOL ENGINES TO BOOST GROWTH

- 11.9 ABOVE 2,100 KW

- 11.9.1 DOMINANCE OF LARGE CARGO AND OCEAN VESSELS TO DRIVE DEMAND

12 METHANOL ENGINES MARKET, BY BUILD

- 12.1 INTRODUCTION

- 12.2 NEW BUILD

- 12.2.1 EARLY INTEGRATION OF METHANOL SYSTEMS TO MEET FUTURE COMPLIANCE NEEDS TO DRIVE MARKET

- 12.3 RETROFIT

- 12.3.1 NEED FOR COST-EFFECTIVE REDUCTION IN EMISSIONS IN EXISTING FLEET TO BOOST GROWTH

13 METHANOL ENGINES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 PORT-LEVEL DECARBONIZATION EFFORTS AND FLEET TRANSITION STRATEGIES TO SUPPORT ADOPTION OF METHANOL ENGINES

- 13.3 EUROPE

- 13.3.1 FRANCE

- 13.3.1.1 Strong maritime decarbonization policies and industrial capabilities to support demand

- 13.3.2 GERMANY

- 13.3.2.1 Strong marine engineering base and clean fuel transition to reinforce demand

- 13.3.3 DENMARK

- 13.3.3.1 Leadership in green shipping and early adoption of methanol propulsion to accelerate market growth

- 13.3.4 SWEDEN

- 13.3.4.1 Strong environmental regulations and ferry transition to support demand for methanol engines

- 13.3.5 NORWAY

- 13.3.5.1 Advanced maritime decarbonization ecosystem and alternative fuel adoption to drive deployment of methanol engines

- 13.3.6 NETHERLANDS

- 13.3.6.1 Development of infrastructure and bunkering to support adoption of methanol engines

- 13.3.7 SWITZERLAND

- 13.3.7.1 Global shipping exposure and decarbonization commitments to support adoption of methanol engines

- 13.3.1 FRANCE

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Large-scale shipbuilding capacity and fuel ecosystem development to accelerate adoption of methanol engines

- 13.4.2 SOUTH KOREA

- 13.4.2.1 Advanced shipbuilding expertise and dual-fuel engine development to drive demand

- 13.4.3 JAPAN

- 13.4.3.1 Focus on efficient propulsion technologies and clean fuel transition to support demand

- 13.4.4 SOUTH ASIA

- 13.4.4.1 Growing inland waterway development and policy support to drive demand for methanol engines

- 13.4.5 SOUTHEAST ASIA

- 13.4.5.1 Singapore

- 13.4.5.1.1 Regulatory clarity and bunkering readiness to support adoption of methanol engines

- 13.4.5.2 Taiwan

- 13.4.5.2.1 Export-driven shipping activity and initial decarbonization efforts to support exploration of methanol engines

- 13.4.5.1 Singapore

- 13.4.1 CHINA

- 13.5 REST OF THE WORLD

- 13.5.1 MIDDLE EAST

- 13.5.1.1 Strong methanol production base and emerging maritime decarbonization initiatives to support growth

- 13.5.2 SOUTH AMERICA

- 13.5.2.1 Brazil's export-driven shipping and fuel integration potential to anchor adoption of methanol engines

- 13.5.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- 14.3 MARKET SHARE ANALYSIS, 2026

- 14.4 MARKET SHARE ANALYSIS, 2030

- 14.5 MARKET SHARE ANALYSIS, 2035

- 14.6 BRAND/PRODUCT COMPARISON

- 14.7 COMPANY VALUATION AND FINANCIAL METRICS

- 14.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 PERVASIVE PLAYERS

- 14.8.4 PARTICIPANTS

- 14.8.5 COMPANY FOOTPRINT

- 14.8.5.1 Company footprint

- 14.8.5.2 Region footprint

- 14.8.5.3 Usage footprint

- 14.8.5.4 Ship type footprint

- 14.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.9.1 PROGRESSIVE COMPANIES

- 14.9.2 RESPONSIVE COMPANIES

- 14.9.3 DYNAMIC COMPANIES

- 14.9.4 STARTING BLOCKS

- 14.9.5 COMPETITIVE BENCHMARKING

- 14.9.5.1 List of startups/SMEs

- 14.9.5.2 Competitive benchmarking of startups/SMEs

- 14.10 COMPETITIVE SCENARIO

- 14.10.1 PRODUCT LAUNCHES

- 14.10.2 DEALS

- 14.10.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 EVERLLENCE SE

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 WARTSILA

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches/developments

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 ROLLS-ROYCE

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 MnM view

- 15.1.3.3.1 Right to win

- 15.1.3.3.2 Strategic choices

- 15.1.3.3.3 Weaknesses and competitive threats

- 15.1.4 YANMAR HOLDINGS CO., LTD.

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 MnM view

- 15.1.4.3.1 Right to win

- 15.1.4.3.2 Strategic choices

- 15.1.4.3.3 Weaknesses and competitive threats

- 15.1.5 ANGLO BELGIAN CORPORATION NV

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches/developments

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 BERGEN ENGINES AS

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Other developments

- 15.1.7 HD HYUNDAI HEAVY INDUSTRIES

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Other developments

- 15.1.7.4 MnM view

- 15.1.7.4.1 Right to win

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 CATERPILLAR

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 CUMMINS INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Other developments

- 15.1.10 VOLVO PENTA

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.11 SCANIA

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 CHINA YUCHAI INTERNATIONAL LIMITED

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Other developments

- 15.1.13 MITSUI E&S CO., LTD.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Other developments

- 15.1.14 HANWHA ENGINE CO., LTD.

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.15 WINGD LTD.

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.15.3.2 Other developments

- 15.1.16 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Other developments

- 15.1.1 EVERLLENCE SE

- 15.2 OTHER PLAYERS

- 15.2.1 WEICHAI HOLDING GROUP CO., LTD.

- 15.2.2 SANDFIRDEN TECHNICS

- 15.2.3 SCANDINAOS AB

- 15.2.4 HANSHIN DIESEL WORKS LTD.

- 15.2.5 CSSC-MES DIESEL CO., LTD.

- 15.2.6 CSSC MARINE POWER CO., LTD.

- 15.2.7 DALIAN MARINE DIESEL CO., LTD

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Primary interviewees

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 FACTOR ANALYSIS

- 16.2.1 INTRODUCTION

- 16.2.2 DEMAND-SIDE INDICATORS

- 16.2.3 SUPPLY-SIDE INDICATORS

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.1.1 Market size estimation methodology: Demand side

- 16.3.2 TOP-DOWN APPROACH

- 16.3.1 BOTTOM-UP APPROACH

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS