|

시장보고서

상품코드

2034860

지방족 탄화수소 용제 및 희석제 시장 : 유형별, 용도별, 지역별 - 예측(-2032년)Aliphatic Hydrocarbon Solvents and Thinners Market By Type (Varnish Makers´ & Painters´ Naphtha, Mineral Spirits, Hexane), Application (Paints & Coatings, Cleaning & Degreasing, Adhesives, Rubbers & Polymers, Aerosols), Region - Global Forecast to 2032 |

||||||

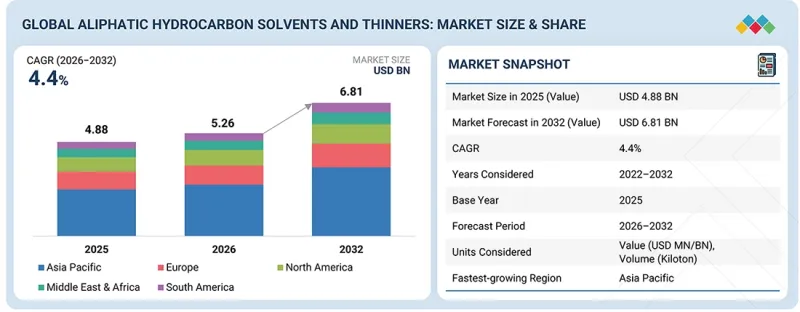

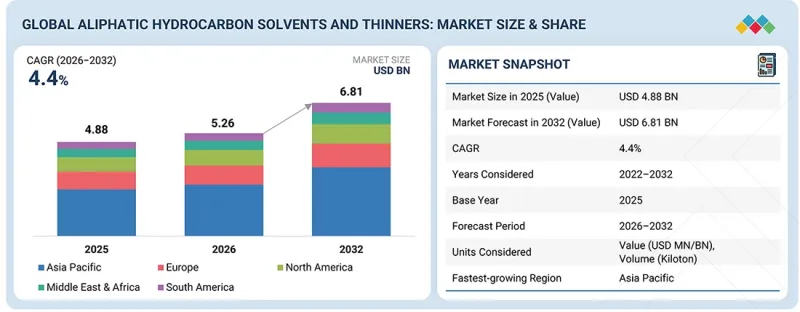

세계의 지방족 탄화수소 용제 및 희석제 시장은 2026년 52억 6,000만 달러에서 예측 기간 중에 CAGR 4.4%로 확대되어 2032년에는 68억 1,000만 달러에 이를 것으로 예측됩니다.

시장 확대는 주로 페인트, 접착제, 산업 유지 보수 등 다양한 산업 분야의 소비 증가에 의해 뒷받침되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(100만/10억 달러) 및 킬로톤 |

| 부문 | 유형, 용도 및 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

자동차 산업이 지속적으로 성장하고 있고, 건설 및 인프라 개발 프로젝트에 대한 자금 투입이 증가함에 따라 솔벤트 기반 솔루션에 대한 수요가 지속적으로 증가하고 있습니다. 산업 공정에서 이러한 용매는 배합 특성 향상, 효과적인 세척 및 매끄러운 마무리를 위해 사용됩니다. 개발도상국에서의 제조 활동이 확대됨에 따라 지방족 탄화수소 용매 및 희석제 시장은 지속적으로 성장하고 있으며, 인쇄 잉크, 에어로졸 및 기타 용도에 대한 수요도 지속적으로 강세를 보이고 있습니다.

"유형별로는 예측 기간 동안 미네랄 스피릿 부문이 금액 기준으로 가장 큰 점유율을 차지할 것으로 추정됩니다. "

유형별로는 미네랄 스피릿, 지방족 탄화수소 용매 및 희석제 부문이 여러 산업 분야에서 널리 사용됨에 따라 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 미네랄 스피릿은 최적의 증발 속도와 뛰어난 용해력을 가지고 있어 페인트 및 코팅의 희석제 역할을 합니다. 세척 및 탈지 작업에서 이러한 제품을 많이 사용하여 높은 소비율로 이어지고 있습니다. 이러한 특정 용매는 낮은 운영 비용과 다양한 제품 혼합물에 대응할 수 있다는 점에서 사용자를 끌어들이고 있습니다. 건설 산업, 자동차 부문 및 유지 보수 작업은 이러한 제품의 지속적인 사용을 주도하고 있습니다. 미네랄 스피릿은 다양한 용도와 신뢰할 수 있는 결과를 제공하는 능력으로 업계 표준으로 자리매김하고 있습니다.

"용도별로는 예측 기간 동안 페인트 및 코팅 분야가 금액 기준으로 가장 큰 점유율을 차지할 것으로 추정됩니다. "

용도별로는 페인트 및 코팅용 지방족 탄화수소 용매 및 희석제 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상되며, 이는 코팅 제조에서 희석제 및 캐리어 재료로 널리 사용되고 있기 때문입니다. 지방족 용매는 점도를 최적화하고 적절한 제품 도포와 균일한 피막 형성을 가능하게 하는 데 중요한 역할을 합니다. 주거, 상업, 산업 건축 프로젝트를 포함한 건설 산업이 페인트 및 코팅에 대한 높은 수요를 주도하고 있습니다. 자동차 생산량 증가와 그 유지보수 업무의 확대로 고성능 코팅에 대한 수요가 증가하고 있습니다. 용매는 건조 시간을 단축하는 동시에 표면 마감의 품질을 향상시킵니다. 이러한 요인으로 인해 예측 기간 동안 페인트 및 코팅 시장에서 지방족 탄화수소계 용매 및 희석제에 대한 수요가 확대될 것으로 예측됩니다.

"예측 기간 동안 아시아태평양이 금액 기준으로 가장 큰 시장 점유율을 차지할 것으로 추정됩니다. "

아시아태평양은 잘 구축된 산업 시설과 다양한 용도의 용매 수요를 모두 갖추고 있어 지방족 탄화수소계 용매 및 희석제 시장에서 가장 큰 규모를 자랑합니다. 이 지역은 대규모 건설 및 인프라 개발에 힘입어 페인트 및 코팅 분야의 견조한 수요의 혜택을 누리고 있습니다. 중국, 인도, 일본 등의 국가에 위치한 주요 제조 거점은 용매에 대한 지속적인 산업 수요를 창출하고 있습니다. 자동차 및 포장 산업은 지속적으로 성장하고 있으며, 이는 지속적인 시장 수요로 이어지고 있습니다. 이 지역은 원자재 가용성과 강력한 석유화학 생산 능력으로 인해 충분한 공급 능력을 갖추고 있습니다. 아시아태평양은 제품 소비량과 제조 생산량 모두에서 다른 지역을 앞서고 있기 때문에 이 지역 시장 지배력은 최고 수준에 도달했습니다.

ExxonMobil Corporation(미국), Shell plc(영국), Phillips 66(미국), SK Geocentric(한국), Calumet, Inc.(미국)는 지방족 탄화수소계 용매 및 희석제 시장의 주요 기업입니다. 이들 기업은 시장 점유율과 사업 수익을 확대하기 위해 제휴, 합작투자, 사업 확장 등 다양한 전략을 채택하고 있습니다.

조사 범위

이 보고서는 지방족 탄화수소 용매 및 희석제 시장을 유형, 용도, 지역별로 정의하고 세분화하여 시장 규모를 예측합니다. 주요 기업의 전략적 프로파일을 작성하고, 시장 점유율과 핵심 경쟁력을 종합적으로 분석합니다. 또한, 시장 내 각 기업의 사업 확장, 계약, 인수 등 경쟁 동향을 추적 및 분석했습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 지방족 탄화수소 용매 및 희석제 시장과 각 부문의 수익에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 시장 진출기업에게 도움이 될 것으로 기대됩니다. 또한, 이 보고서는 이해관계자들이 시장 경쟁 구도를 보다 깊이 이해하고, 비즈니스 입지를 강화하기 위한 귀중한 인사이트를 얻고, 효과적인 시장 진출 전략을 수립하는 데 도움이 될 것으로 기대됩니다. 또한, 이해관계자들이 시장 동향을 파악할 수 있도록 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다.

- 주요 성장 촉진요인(페인트 및 코팅 산업 수요 증가, 건설 및 인프라 활동 확대), 제약 요인(VOC 배출에 대한 엄격한 환경 규제, 수성 및 바이오 대체품에 대한 선호도 증가), 기회(저 VOC 및 무취 용매 배합 개발, 특수 용도 및 고순도 용도로의 확장), 과제(원유 및 석유 원료의 변동, 무용제 공정으로의 기술 전환)에 대한 분석. 과제(원유 및 석유 원료 가격 변동, 무용제 공정으로의 기술적 전환)에 대한 분석. 이는 지방족 탄화수소 용매 및 희석제 시장의 성장에 영향을 미치고 있습니다.

- 제품 개발 및 혁신 : 지방족 탄화수소계 용매 및 희석제 시장의 향후 기술 동향, 연구개발 활동에 대한 심층 분석

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 -이 보고서는 다양한 지역의 지방족 탄화수소 용매 및 희석제 시장을 분석합니다.

- 시장 다각화 : 알킬 탄화수소 용매 및 희석제 시장의 신제품, 다양한 유형, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보

- 경쟁 분석 : 알킬 탄화수소계 용매 및 희석제 시장에서 ExxonMobil Corporation(미국), Shell plc(영국), Phillips 66(미국), SK Geocentric(한국), Calumet, Inc. 성장전략, 제품 라인업에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 지방족 탄화수소 용제 및 희석제 시장(유형별)

제10장 지방족 탄화수소 용제 및 희석제 시장(용도별)

제11장 지방족 탄화수소 용제 및 희석제 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

LSH 26.06.01The global aliphatic hydrocarbon solvents and thinners market is projected to reach USD 6.81 billion by 2032, from USD 5.26 billion in 2026, at a CAGR of 4.4% during the forecast period. Market expansion is primarily supported by rising consumption across various industries, including coatings, adhesives, and industrial maintenance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Million/Billion) and Volume (Kiloton) |

| Segments | Type, Application, and Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

The automotive industry continues to expand, while construction and infrastructure development projects receive increased funding, driving ongoing demand for solvent-based solutions. Industrial processes use these solvents to improve formulation properties, enable effective cleaning, and achieve smooth finishing results. The aliphatic hydrocarbon solvents and thinners market experiences sustained growth as developing regions expand their manufacturing operations, while demand for printing inks, aerosols, and other applications remains strong.

"By type, the mineral spirits segment is estimated to hold the largest share, in terms of value, during the forecast period."

The mineral spirits, aliphatic hydrocarbon solvents and thinners segment by type is expected to hold the largest market share during the forecast period due to its widespread usage across multiple industrial applications. Mineral spirits serve as thinners for paints and coatings because they possess an optimum evaporation rate and exceptional solvent power. The strong usage of these products in cleaning and degreasing tasks leads to high consumption rates. The particular solvents attract users to their lower operational expenses and their ability to work with various product mixtures. The construction industry, the automotive sector, and maintenance work drive the continuous use of these products. Mineral spirits maintain their status as an industry standard because of their multiple applications and their ability to deliver reliable results.

"By application, the paints & coatings segment is estimated to account for the largest share, in terms of value, during the forecast period."

The paints & coatings aliphatic hydrocarbon solvents and thinners segment by application is expected to hold the largest market share during the forecast period, driven by the widespread use of these solvents as thinners and carrier materials in coating production. Aliphatic solvents play a crucial role in optimizing viscosity, enabling proper product application and consistent film development. The construction industry, which includes residential, commercial, and industrial building projects, drives the high demand for paints and coatings. The increasing production of vehicles and their maintenance operations create a rising need for high-performance coatings. The solvents improve drying time while also enhancing the quality of surface finishes. These factors are expected to enhance demand in the paints & coatings market for aliphatic hydrocarbon solvents and thinners during the forecast period.

"Asia Pacific is estimated to hold the largest market share, in terms of value, during the forecast period."

The aliphatic hydrocarbon solvents and thinners market is the largest in the Asia Pacific, as the region has both established industrial facilities and a need for solvents across various applications. The region benefits from strong demand in paints & coatings, supported by large-scale construction and infrastructure development. The major manufacturing centers located in countries such as China, India, and Japan create ongoing industrial demand for solvents. The automotive and packaging industries are experiencing growth, leading to sustained market demand. The region has substantial supply capabilities due to its raw material availability and strong petrochemical production capacity. The market control in the Asia Pacific region reaches its peak because the area leads all others in both product consumption and manufacturing output.

Break-up of primary participants for the report:

- By Company Type: Tier 1 - 20%, Tier 2 - 40%, and Tier 3 - 40%

- By Designation: C-Level Executives - 10%, Directors - 70%, and Others - 20%

- By Region: North America - 45%, Asia Pacific - 25%, Europe - 20%, Middle East & Africa - 5%, and South America - 5%

ExxonMobil Corporation (US), Shell plc (UK), Phillips 66 (US), SK Geocentric Co., Ltd. (South Korea), and Calumet, Inc. (US) are the key players in the aliphatic hydrocarbon solvents and thinners market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage

The report defines, segments, and projects the size of the aliphatic hydrocarbon solvents and thinners market by type, application, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the aliphatic hydrocarbon solvents and thinners market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (growing demand from the paints and coatings industry, expansion of construction and infrastructure activities), restraints (stringent environmental regulations on VOC emissions, rising preference for water-based and bio-based alternatives), opportunities (development of low-VOC and odorless solvent formulations, expansion in specialty and high-purity applications), and challenges (volatility in crude oil and petroleum feedstock prices, technological shift toward solvent-free processes) influencing the growth of the aliphatic hydrocarbon solvents and thinners market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the aliphatic hydrocarbon solvents and thinners market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the aliphatic hydrocarbon solvents and thinners market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the aliphatic hydrocarbon solvents and thinners market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as ExxonMobil Corporation (US), Shell plc (UK), Phillips 66 (US), SK Geocentric Co., Ltd. (South Korea), and Calumet, Inc. (US) in the aliphatic hydrocarbon solvents and thinners market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET

- 3.2 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY TYPE

- 3.3 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY APPLICATION

- 3.4 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY REGION

- 3.5 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand from paints & coatings industry

- 4.2.1.2 Expansion of construction and infrastructure activities

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent environmental regulations on VOC emissions

- 4.2.2.2 Rising preference for water-based and bio-based alternatives

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of low-VOC and odorless solvent formulations

- 4.2.3.2 Expansion in specialty and high-purity applications

- 4.2.4 CHALLENGES

- 4.2.4.1 Volatility in crude oil and petroleum feedstock prices

- 4.2.4.2 Technological shift towards solvent-free processes

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ALIPHATIC HYDROCARBON SOLVENTS & THINNERS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 RAW MATERIAL

- 5.3.3 MANUFACTURING

- 5.3.4 DISTRIBUTION NETWORK

- 5.3.5 END-USE INDUSTRIES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF ALIPHATIC HYDROCARBON SOLVENTS & THINNERS, BY REGION

- 5.5.2 AVERAGE SELLING PRICE TREND OF ALIPHATIC HYDROCARBON SOLVENTS & THINNERS, BY KEY PLAYERS

- 5.6 TRADE DATA

- 5.6.1 IMPORT SCENARIO (HS CODE 381400)

- 5.6.2 EXPORT SCENARIO (HS CODE 381400)

- 5.7 KEY CONFERENCES AND EVENTS

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 US TARIFF IMPACT ON ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET

- 5.9.1 KEY TARIFF RATES IMPACTING THE MARKET

- 5.9.2 PRICE IMPACT ANALYSIS

- 5.9.3 IMPACT ON KEY COUNTRIES/REGIONS

- 5.9.3.1 US

- 5.9.3.2 Europe

- 5.9.3.3 Asia Pacific

- 5.9.4 IMPACT ON END-USE INDUSTRIES OF ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET

- 5.9.4.1 Paints & coatings

- 5.9.4.2 Adhesives & sealants

- 5.9.4.3 Cleaning & degreasing

- 5.9.4.4 Printing inks

- 5.9.4.5 Aerosols & consumer products

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 HYDROPROCESSING (HYDROTREATING & HYDROFINISHING)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 FRACTIONAL DISTILLATION & SOLVENT BLENDING

- 6.2.2 DEAROMATIZATION (AROMATIC REMOVAL TECHNOLOGIES)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | PROCESS EFFICIENCY & QUALITY ENHANCEMENT

- 6.3.2 MID-TERM (2027-2030) | SUSTAINABILITY & SPECIALTY SOLVENT DEVELOPMENT

- 6.3.3 LONG-TERM (2030-2035+) | CIRCULARITY, LOW-EMISSION SOLVENT SYSTEMS

- 6.4 PATENT ANALYSIS

- 6.4.1 METHODOLOGY

- 6.5 FUTURE APPLICATIONS

- 6.5.1 PAINTS & COATINGS: HIGH-PERFORMANCE FORMULATIONS & ADVANCED COATING SYSTEMS

- 6.5.2 CLEANING & DEGREASING: INDUSTRIAL MAINTENANCE & PRECISION CLEANING SOLUTIONS

- 6.5.3 ADHESIVES: ADVANCED BONDING & LIGHTWEIGHT MATERIAL APPLICATIONS

- 6.5.4 RUBBERS & POLYMERS: PROCESSING AIDS & MATERIAL ENHANCEMENT

- 6.6 IMPACT OF GENERATIVE AI ON ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET

- 6.6.1 INTRODUCTION

- 6.6.1.1 Production & process optimization

- 6.6.1.2 Supply chain resilience & demand forecasting

- 6.6.1.3 Quality control & consistency

- 6.6.1.4 Innovation in product development & formulation

- 6.6.1.5 Cost, efficiency & competitive advantage

- 6.6.1.6 Challenges & regulatory considerations

- 6.6.1 INTRODUCTION

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 EXXONMOBIL CORPORATION: ADVANCING INTEGRATED REFINING & CIRCULAR FEEDSTOCK STRATEGIES

- 6.7.2 SHELL PLC: FORMULATING FLEXIBILITY & SUSTAINABILITY

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGULATORY LANDSCAPE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ALIPHATIC HYDROCARBON SOLVENTS & THINNERS

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ALIPHATIC HYDROCARBON SOLVENTS & THINNERS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 VARNISH MAKERS' & PAINTERS' NAPHTHA

- 9.2.1 GROWING DEMAND FROM PAINTS & COATINGS TO DRIVE DEMAND

- 9.3 MINERAL SPIRITS

- 9.3.1 WIDESPREAD USE IN PAINTS, COATINGS, AND INDUSTRIAL CLEANING APPLICATIONS TO DRIVE DEMAND

- 9.4 HEXANE

- 9.4.1 FAST EVAPORATION RATE AND EFFECTIVE SOLVENCY DRIVING DEMAND IN INDUSTRIAL APPLICATIONS

- 9.5 HEPTANE

- 9.5.1 ADOPTION IN PAINTS & COATINGS AND AEROSOL FORMULATIONS TO DRIVE MARKET GROWTH

- 9.6 OTHER TYPES

10 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 PAINTS & COATINGS

- 10.2.1 INCREASING DEMAND FOR HIGH-PERFORMANCE COATINGS AND APPLICATION EFFICIENCY TO DRIVE MARKET

- 10.3 CLEANING & DEGREASING

- 10.3.1 ABILITY TO EFFECTIVELY DISSOLVE OILS, GREASES, AND OTHER CONTAMINANTS FUELING DEMAND

- 10.4 ADHESIVES

- 10.4.1 GROWING DEMAND FOR PACKAGED GOODS AND INDUSTRIAL BONDING SOLUTIONS TO DRIVE DEMAND

- 10.5 AEROSOLS

- 10.5.1 GROWING USE OF CONVENIENCE-BASED PRODUCTS SUCH AS SPRAY PAINTS AND CLEANING SPRAYS TO DRIVE DEMAND

- 10.6 RUBBERS & POLYMERS

- 10.6.1 INCREASING DEMAND FOR RUBBER AND POLYMER-BASED PRODUCTS IN INDUSTRIAL AND CONSUMER APPLICATIONS TO DRIVE DEMAND

- 10.7 PRINTING INKS

- 10.7.1 RISING DEMAND FOR HIGH-QUALITY PRINTING IN PACKAGING AND LABELING APPLICATIONS TO SUPPORT MARKET GROWTH

- 10.8 OTHER APPLICATIONS

11 ALIPHATIC HYDROCARBON SOLVENTS & THINNERS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Industrial expansion and infrastructure development to drive market growth

- 11.2.2 JAPAN

- 11.2.2.1 Growing demand from automotive sector to fuel market growth

- 11.2.3 INDIA

- 11.2.3.1 Expanding industrial base and investment outlook offering significant growth potential

- 11.2.4 SOUTH KOREA

- 11.2.4.1 Growing demand from electronics, automotive, and shipbuilding industries to boost demand

- 11.2.5 INDONESIA

- 11.2.5.1 Increasing investments in infrastructure and construction to fuel demand

- 11.2.6 THAILAND

- 11.2.6.1 Increasing demand for industrial coatings and maintenance solutions to drive steady growth

- 11.2.7 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Well-established coatings and industrial sectors driving consistent demand

- 11.3.2 UK

- 11.3.2.1 Demand from maintenance, repair, and infrastructure-related activities to support market growth

- 11.3.3 FRANCE

- 11.3.3.1 Steady growth in construction and industrial activities fueling demand

- 11.3.4 ITALY

- 11.3.4.1 Strong manufacturing and automotive sectors to drive market growth

- 11.3.5 TURKEY

- 11.3.5.1 Rising demand from paints & coatings sector to fuel demand

- 11.3.6 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 NORTH AMERICA

- 11.4.1 US

- 11.4.1.1 Strong demand from manufacturing and construction sectors driving demand

- 11.4.2 CANADA

- 11.4.2.1 Growth in infrastructure development and maintenance activities to support market growth

- 11.4.3 MEXICO

- 11.4.3.1 Ongoing infrastructure development and rising construction activities to drive market

- 11.4.1 US

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Growth in manufacturing and logistics sectors contributing to market growth

- 11.5.1.2 UAE

- 11.5.1.2.1 Ongoing investments in transportation, real estate, and industrial development supporting demand growth

- 11.5.1.3 Rest of GCC

- 11.5.1.3.1 Strong raw material availability and industrial expansion to enhance demand

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Economic diversification and strengthening industrial output to drive demand

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Growth of automotive sector to boost market expansion

- 11.6.2 ARGENTINA

- 11.6.2.1 Presence of major automotive manufacturers fueling market growth

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.4.1 EXXON MOBIL CORPORATION (US)

- 12.4.2 SK GEOCENTRIC CO., LTD. (SOUTH KOREA)

- 12.4.3 SHELL (UK)

- 12.4.4 TOTALENERGIES (FRANCE)

- 12.4.5 CHEVRON PHILLIPS CHEMICAL COMPANY LLC (US)

- 12.5 BRAND/PRODUCT COMPARISON

- 12.5.1 EXXONMOBIL

- 12.5.2 SHELL

- 12.5.3 TOTALENERGIES

- 12.5.4 SK GEOCENTRIC

- 12.5.5 CHEVRON PHILLIPS CHEMICAL COMPANY

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Type footprint

- 12.7.5.4 Application footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 DEALS

- 12.9.2 EXPANSIONS

13 COMPANY PROFILES

- 13.1 MAJOR PLAYERS

- 13.1.1 EXXON MOBIL CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deal

- 13.1.1.3.2 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 SK GEOCENTRIC CO., LTD.

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 MnM view

- 13.1.2.3.1 Right to win

- 13.1.2.3.2 Strategic choices

- 13.1.2.3.3 Weaknesses and competitive threats

- 13.1.3 SHELL

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 TOTALENERGIES

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 MnM view

- 13.1.4.3.1 Right to win

- 13.1.4.3.2 Strategic choices

- 13.1.4.3.3 Weaknesses and competitive threats

- 13.1.5 CHEVRON PHILLIPS CHEMICAL COMPANY LLC

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 CALUMET, INC.

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.7 KP GROUP

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.8 GOTHAM INDUSTRIES

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.9 GULF CHEMICAL & INDUSTRAL OILS

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.10 RECOCHEM CORPORATION

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.11 HALTERMANN CARLESS GROUP GMBH

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.12 WM BARR

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.13 MEHTA PETRO REFINERIES LTD.

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Solutions/Services offered

- 13.1.14 LYONDELLBASELL INDUSTRIES HOLDINGS B.V.

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Solutions/Services offered

- 13.1.15 GANGA RASAYANIE P. LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Solutions/Services offered

- 13.1.16 GADIV

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Solutions/Services offered

- 13.1.17 SASOL

- 13.1.17.1 Business overview

- 13.1.17.2 Products/Solutions/Services offered

- 13.1.18 GANDHAR OIL REFINERY (INDIA) LIMITED

- 13.1.18.1 Business overview

- 13.1.18.2 Products/Solutions/Services offered

- 13.1.19 BASF

- 13.1.19.1 Business overview

- 13.1.19.2 Products/Solutions/Services offered

- 13.1.20 PHILLIPS 66 COMPANY

- 13.1.20.1 Business overview

- 13.1.20.2 Products/Solutions/Services offered

- 13.1.1 EXXON MOBIL CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 PON PURE CHEMICALS GROUP

- 13.2.2 CRYSTAL CLEAN, INC.

- 13.2.3 RB PRODUCTS, INC.

- 13.2.4 SAFRA COMPANY LIMITED

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 List of key secondary sources

- 14.1.1.2 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 List of primary interview participants (demand and supply sides)

- 14.1.2.3 Key industry insights

- 14.1.2.4 Breakdown of interviews with experts

- 14.1.1 SECONDARY DATA

- 14.2 DEMAND-SIDE ANALYSIS

- 14.3 SUPPLY-SIDE ANALYSIS

- 14.3.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 14.4 MARKET SIZE ESTIMATION

- 14.4.1 BOTTOM-UP APPROACH

- 14.4.2 TOP-DOWN APPROACH

- 14.5 GROWTH FORECAST

- 14.6 DATA TRIANGULATION

- 14.7 FACTOR ANALYSIS

- 14.8 RESEARCH ASSUMPTIONS

- 14.9 RESEARCH LIMITATIONS

- 14.10 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS