|

시장보고서

상품코드

2034862

전기차 무선 충전 시장 : 충전 시스템별, 충전 유형별, 용도별, 컴포넌트별, 전력 공급 범위별, 추진 방식별, 차량 유형별, 지역별 - 예측(-2032년)Wireless Charging Market for Electric Vehicles by Charging System (Inductive, Capacitive, Magnetic Power Transfer), Propulsion, Charging Type (Stationary, Dynamic Wireless Charging), Component, Power Supply, and Vehicle Type - Global Forecast to 2032 |

||||||

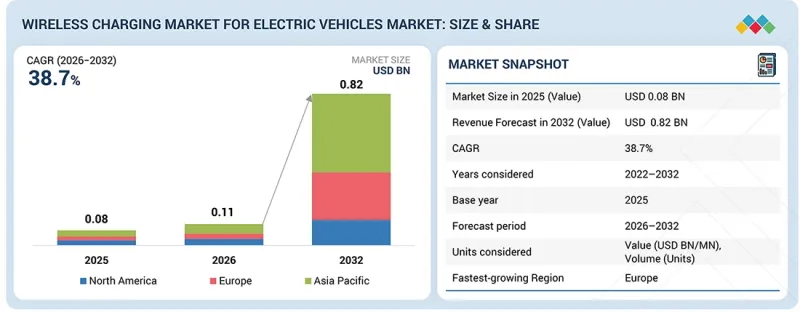

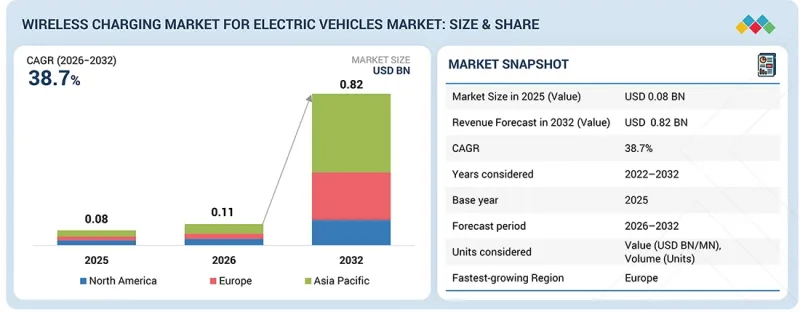

전기차 무선 충전 시장 규모는 2026년 1억 1,000만 달러에서 2032년까지 8억 2,000만 달러에 이를 것으로 예측되며, CAGR은 38.7%를 나타낼 전망입니다.

이러한 성장은 전기차 보급 확대와 충전 편의성 향상에 대한 관심 증가에 힘입은 것입니다. 자동차 제조업체들은 기술 제공업체와의 제휴를 통해 무선 충전을 차량 플랫폼에 통합하는 것을 고려하고 있습니다. 무선 충전은 자동 에너지 전송을 가능하게 하여 케이블에 대한 의존도를 줄이고, 특히 도시 및 차량용 용도에서 편의성을 향상시킵니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 10억 달러 |

| 부문 | 충전 시스템별, 충전 유형별, 용도별, 컴포넌트별, 전력 공급 범위별, 추진 방식별, 차량 유형별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽 |

유도 충전 시스템, 포지셔닝 및 표준화의 발전으로 시스템 성능이 향상되고 초기 단계의 도입이 촉진되고 있습니다. 차량과 인프라 간의 통합이 진행됨에 따라, 무선 충전은 사용 빈도가 높은 이용 사례에서 점차 확산될 것으로 예측됩니다.

"충전 시스템별로는 유도식 전력 전송이 가장 큰 부문이 될 것으로 예측됩니다. "

유도 전력 전송은 EV의 무선 충전에서 가장 널리 채택된 방식입니다. 이는 전자기 유도 원리를 기반으로 하며, 지상의 송신 패드와 차량에 탑재된 수신 패드 사이에 전력이 전송됩니다. 유도식 시스템은 SAE J2954 등의 표준화 노력에 힘입어 주택, 직장, 공공 충전 환경 곳곳에 도입이 진행되고 있습니다. 현대자동차, 볼보그룹, BMW, 도요타 등 자동차 제조업체와 Aptiv, Mahle 등 Tier 1 공급업체들은 차량 플랫폼에 유도 충전을 통합하기 위한 노력을 기울이고 있습니다. 예를 들어, 2026년 3월 Electreon(Electreon)은 미국 미시간 주에서 대중교통 및 차량용 유도 충전의 보급을 확대했습니다. 그 이전인 2025년 6월, ENRX는 볼보 그룹과 협력하여 전기 버스와 트럭을 위한 유도 충전을 전개하고, 기회 충전을 지원했습니다. 유도 전력 전송의 주요 장점은 안정적인 전력 전송, 통합 용이성 및 시스템 복잡성 감소를 포함합니다. 유도 전력 전송의 효율은 보통 90-95% 범위로, 에너지 손실을 줄이고 안정적인 충전 성능을 실현합니다. 이러한 요인들은 유도 전력 전송의 보급을 촉진하고, 시장에서 주요 기술로 자리매김하고 있습니다.

"충전 방식별로는 고정식 무선 충전이 가장 큰 비중을 차지할 것으로 예측됩니다. "

고정식 무선 충전은 주택, 직장, 공공 주차장 환경에서 자동 충전의 실용적인 솔루션으로 주목받고 있습니다. 유도 전력 전송을 기반으로 하는 이 시스템은 지상에 설치된 충전 패드와 차량에 탑재된 수신기 사이에 에너지를 전송합니다. 이를 통해 주차 중에도 수동 조작 없이 충전이 가능하여 편의성을 높이고 플러그인 시스템에 대한 의존도를 낮출 수 있습니다. 이 기술은 일정 시간 동안 차량이 정지되어 있는 승용차 및 차량용 차량에 가장 적합합니다. 이 기술은 안정적인 충전을 지원하고, 사용자 경험을 향상시키며, 물리적 커넥터의 마모와 손상을 줄일 수 있습니다. 자동차 제조업체(OEM)와 무선 충전 제공업체들은 이러한 시스템을 차량 플랫폼과 주차 인프라에 통합하는 데 주력하고 있습니다. 2026년 3월, WiTricity는 지멘스와 협력하여 확장 가능한 인프라 통합에 중점을 두고 주거용 및 차량용 주차 용도에 고정식 무선 충전 솔루션의 배포를 추진했습니다. 시스템의 효율성과 표준화가 진행됨에 따라 고정형 무선 충전은 주요 이용 사례에서 더 널리 채택될 것으로 예측됩니다.

"예측 기간 동안 유럽이 가장 빠르게 성장하는 시장이 될 것으로 예측됩니다. "

유럽 자동차 산업은 유럽연합(EU)의 엄격한 배출가스 규제와 명확한 탈탄소화 목표에 힘입어 무공해 모빌리티로의 강력한 전환이 진행되고 있습니다. 유럽 각국은 인센티브, 인프라 투자, 정책적 지원을 통해 전기차 보급을 적극적으로 추진하고 있으며, 무선 충전 기술에 유리한 환경을 조성하고 있습니다. 무선 충전에 대한 수요는 프리미엄 EV의 부상과 사용자 편의성 및 첨단 차량 기능에 대한 관심이 높아짐에 따라 무선 충전에 대한 수요도 증가하고 있습니다. OEM과 기술 제공업체들은 지역 표준 및 상호운용성 요건을 준수하면서 차세대 차량 플랫폼에 무선 충전을 통합하기 위해 협력하고 있습니다. 이 지역의 주요 기업으로는 독일의 IPT Technology GmbH와 Robert Bosch GmbH, 유럽의 여러 시장에서 사업을 전개하고 있는 Electreon, 노르웨이의 ENRX 등이 있습니다. 2025년 4월, Electreon은 독일에서 무선 충전 도로 프로젝트를 확대하여 대중교통을 위한 유도 충전 인프라 구축을 지원했습니다. 이러한 솔루션은 특히 대중교통 및 차량용 용도에서 파일럿 프로젝트와 초기 상용 프로젝트를 통해 도입이 진행되고 있습니다. 스마트시티와 커넥티드 인프라에 대한 투자가 증가하는 가운데, 유럽은 전기차 무선 충전의 보급을 촉진하는 데 있어 중심적인 역할을 할 것으로 예측됩니다.

전기차 무선충전 시장은 Electreon(이스라엘), Witricity(미국), ENRX(노르웨이), HEVO Inc.(미국), Plugless Power Inc.(미국) 등 기존 업체들이 주도하고 있습니다. 이들 기업은 공장 출하 통합형 시스템부터 고출력 차량용 인프라에 이르기까지 다양한 무선 충전 솔루션을 개발 및 공급하고 있습니다.

조사 범위:

본 조사에서는 전기자동차용 무선충전 시장을 충전 시스템(유도전력전송, 자기전력전송, 전도전력전송), 추진방식(BEV, PHEV), 충전방식(고정형 무선충전, 동적 무선충전), 구성부품(베이스 충전패드, 전력제어장치, 차량용 충전패드), 전력공급(<3.7-7.7 kW, 7.7-7.5 kW, 7.7-11 kW, >7.7-11 kW, >7.7-11 kW, 전력공급(<3.7-7.5 kW) 전력 공급(<3.7 kW, 3.8-7.7 kW, 7.8-11 kW, >3.7 kW, 7.8-11 kW, >3.7 kW)11 kW) 및 차종별(승용차, 상용차)로 분석했습니다. 또한, 무선 충전 생태계의 주요 기업들경쟁 구도와 기업 프로파일에 대해서도 다루고 있습니다.

본 보고서의 주요 장점:

이 보고서는 시장 선도업체와 신규 진입업체에게 전체 전기자동차 무선 충전 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 이해하고, 비즈니스를 보다 효과적으로 포지셔닝하고, 적절한 시장 진출 전략을 수립할 수 있는 인사이트를 얻을 수 있습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 성장 촉진요인, 제약, 과제 및 기회에 대한 정보를 제공함으로써 시장 동향을 파악할 수 있도록 돕습니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(OEM의 무선 충전 생태계 진입 확대, 자동 및 스마트 주차 시스템과의 무선 충전 통합, 무배출 및 지속 가능한 전기 모빌리티에 대한 정부의 강력한 지원), 제약 요인(차량 내 무선 충전 시스템 통합에 따른 높은 비용과 복잡성, 기존 유선 충전 솔루션 대비 낮은 에너지 전송 효율), 기회(스마트 시티 인프라의 무선 충전 채택 확대, 동적 무선 충전 기술에 대한 투자 증가, 고사용 전기자동차 차량 운영 시 시스템 안정성) 기존 유선 충전 솔루션 대비 낮은 에너지 전송 효율), 기회(스마트 시티 인프라에서 무선 충전 채택 확대, 동적 무선 충전 기술에 대한 투자 증가, 전기차 운행 빈도가 높은 차량에서 원활한 충전 가능성), 시장 성장에 영향을 미치는 과제(표준화된 차량 충전 시스템) 시장 성장에 영향을 미치는 과제(표준화된 차량 통합 프레임워크의 부재, 공공 무선 충전 인프라 설치 및 도입 비용의 높은 수준)

- 제품 개발/혁신 : 시장에서의 미래 기술, R&D 활동, 신제품 출시에 대한 상세한 인사이트

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역 시장을 분석합니다.

- 시장 다각화 : 시장 내 신제품, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁사 분석 : Electreon(이스라엘), Witricity(미국), ENRX(노르웨이), HEVO Inc.(미국), Plugless Power Inc.(미국) 등 주요 기업의 시장 점유율, 성장전략, 서비스 제공내용에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 전기차 무선 충전 시장(충전 시스템별)

제6장 전기차 무선 충전 시장(충전 방식별)

제7장 전기차 무선 충전 시장(용도별)

제8장 전기차 무선 충전 시장(컴포넌트별)

제9장 전기차 무선 충전 시장(전력 공급 범위별)

제10장 전기차 무선 충전 시장(추진 방식별)

제11장 전기차 무선 충전 시장(차량 유형별)

제12장 전기차 무선 충전 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

LSH 26.06.01The wireless charging market for electric vehicles is expected to reach USD 0.82 billion by 2032, from USD 0.11 billion in 2026, with a CAGR of 38.7%. This growth is supported by increasing EV adoption and rising focus on improving charging convenience. OEMs are evaluating the integration of wireless charging into vehicle platforms, which is influenced by partnerships with technology providers. Wireless charging enables automated energy transfer, reducing reliance on cables and improving ease of use, especially in urban and fleet applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | USD Billion |

| Segments | Charging Type, Component, Application, Charging System, Propulsion, Power Supply Range, Vehicle Type |

| Regions covered | Asia Pacific, North America, Europe |

Advancements in inductive systems, alignment, and standardization are enhancing system performance and supporting early-stage deployments. As integration across vehicles and infrastructure improves, wireless charging is expected to see gradual adoption in high-utilization use cases.

"Inductive power transfer is expected to be the largest segment by charging system."

Inductive power transfer is the most widely used method for wireless charging of EVs. It operates on the principle of electromagnetic induction, where power is transferred between a transmitter pad on the ground and a receiver pad installed in the vehicle. Inductive systems are being deployed across residential, workplace, and public charging environments, supported by standardization efforts like SAE J2954. OEMs such as Hyundai, Volvo Group, BMW, and Toyota, along with Tier-1 suppliers like Aptiv and Mahle, are working on integrating inductive charging into vehicle platforms. For instance, in March 2026, Electreon expanded its inductive charging deployment in Michigan, US, for public transport and fleet applications. Earlier, in June 2025, ENRX partnered with Volvo Group to deploy inductive charging for electric buses and trucks, supporting opportunity charging. Key advantages of inductive power transfer include stable power transfer, ease of integration, and lower system complexity. The efficiency of inductive power transfer typically ranges between 90-95%, supporting reduced energy losses and consistent charging performance. These factors support widespread adoption of inductive power transfer and position it as the leading technology in the market.

"Stationary wireless charging is expected to be the largest segment by charging type."

Stationary wireless charging is gaining traction as a practical solution for automated charging in residential, workplace, and public parking environments. Based on inductive power transfer, the system enables energy transfer between a ground-based charging pad and a receiver installed in the vehicle. This allows vehicles to charge without manual intervention while parked, improving convenience and reducing reliance on plug-in systems. The technology is well-suited for passenger cars and fleet applications where vehicles remain stationary for defined periods. It supports consistent charging, improves user experience, and reduces wear and tear associated with physical connectors. OEMs and wireless charging providers are focusing on integrating these systems into vehicle platforms and parking infrastructure. In March 2026, WiTricity, in collaboration with Siemens, advanced the deployment of stationary wireless charging solutions across residential and fleet parking applications, focusing on scalable infrastructure integration. As system efficiency and standardization improve, stationary wireless charging is expected to see wider adoption across key use cases.

"Europe is expected to be the fastest-growing market during the forecast period."

The European automotive industry is witnessing a strong shift toward zero-emission mobility, supported by strict emission regulations and clear decarbonization targets set by the European Union. European countries are actively promoting EV adoption through incentives, infrastructure investments, and policy support, creating a favorable environment for wireless charging technologies. Demand for wireless charging is also supported by the growing presence of premium EVs and increasing focus on user convenience and advanced vehicle features. OEMs and technology providers are working together to integrate wireless charging into next-generation vehicle platforms, with alignment toward regional standards and interoperability requirements. Key players in the region include IPT Technology GmbH and Robert Bosch GmbH in Germany, Electreon operating across multiple European markets, and ENRX in Norway. In April 2025, Electreon expanded its wireless charging road projects in Germany, supporting the deployment of inductive charging infrastructure for public transport applications. These solutions are being deployed through pilot and early commercial projects, particularly in public transport and fleet applications. As investments in smart cities and connected infrastructure increase, Europe is expected to play a central role in advancing wireless EV charging adoption.

In-depth interviews were conducted with CXOs, managers, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 24%, Tier 1 - 67%, Tier 2 - 9%,

- By Designation: CXOs - 33%, Managers- 52%, Executives - 15%

- By Region: North America - 32%, Europe - 27 %, Asia Pacific - 41%

The wireless charging market for electric vehicles is dominated by established players such as Electreon (Israel), Witricity (US), ENRX (Norway), HEVO Inc. (US), and Plugless Power Inc. (US). These companies develop and supply wireless charging solutions, ranging from factory-integrated systems to high-power fleet infrastructure.

Research Coverage:

The study analyzes the wireless charging for electric vehicles market by charging system (inductive power transfer, magnetic power transfer, conductive power transfer), propulsion (BEV, PHEV), charging type (stationary wireless charging, dynamic wireless charging), component (base charging pads, power control unit, vehicle charging pads), power supply (<3.7 kW, 3.8-7.7 kW, 7.8-11 kW, >11 kW), and vehicle type (passenger cars, commercial vehicles). It also covers the competitive landscape and company profiles of the major players in the wireless charging ecosystem.

Key Benefits of Report:

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the overall wireless charging market for electric vehicles and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Increased participation of OEMs in wireless charging ecosystem, Integration of wireless charging with automated and smart parking systems, Strong government support for emission free and sustainable electric mobility), restraints (High cost and complexity associated with integrating in vehicle wireless charging systems, Lower energy transfer efficiency compared to conventional wired charging solutions), opportunities (Growing adoption of wireless charging within smart city infrastructure, Rising investments in dynamic wireless charging technology, Potential for seamless charging in high utilization electric fleet operations), and challenges (Lack of standardized vehicle integration frameworks, High setup and installation costs for public wireless charging infrastructure) influencing the growth of market

- Product Development/Innovation: Detailed insights on upcoming technologies, R&D activities, and new product launches in the market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the market across various regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Electreon (Israel), Witricity (US), ENRX (Norway), HEVO Inc. (US), and Plugless Power Inc. (US), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES

- 2.3 HIGH-GROWTH SEGMENTS

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES

- 3.2 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE

- 3.3 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION

- 3.4 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE

- 3.5 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM

- 3.6 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT

- 3.7 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Ability to combine user-centric design with long-term cost efficiency

- 4.2.1.2 Active participation of OEMs in wireless charging ecosystem

- 4.2.1.3 Integration of wireless charging with automated smart parking systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High integration cost and design complexity of in-vehicle wireless charging systems

- 4.2.2.2 Lower energy transfer efficiency compared to conventional wired charging solutions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid adoption of wireless charging within smart city infrastructure

- 4.2.3.2 Rising investments in dynamic wireless charging technologies

- 4.2.3.3 Potential for seamless charging in high-utilization electric fleet operations

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of standardization and interoperability across vehicles and wireless charging infrastructure

- 4.2.4.2 High setup and installation costs for public wireless charging infrastructure

- 4.2.1 DRIVERS

- 4.3 PRICING ANALYSIS

- 4.3.1 AVERAGE SELLING PRICE TREND, BY PROPULSION, 2023-2025

- 4.3.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 4.4 ECOSYSTEM ANALYSIS

- 4.4.1 OEMS

- 4.4.2 WIRELESS EV CHARGING SYSTEM PROVIDERS

- 4.4.3 CHARGING STATION SERVICE PROVIDERS

- 4.4.4 ENERGY SUPPLIERS

- 4.4.5 PAYMENT PROCESSING COMPANIES

- 4.4.6 END USERS

- 4.5 VALUE CHAIN ANALYSIS

- 4.6 CASE STUDY ANALYSIS

- 4.6.1 ELECTREON'S WIRELESS CHARGING ROAD PROJECT

- 4.6.2 WITRICITY'S HALO WIRELESS CHARGING SYSTEM

- 4.6.3 HEVO'S WIRELESS CHARGING PAD

- 4.6.4 ENRX'S INDUCTIVE CHARGING SYSTEM

- 4.6.5 PLUGLESS POWER'S RESIDENTIAL WIRELESS CHARGING SYSTEM

- 4.6.6 WITRICITY'S DRIVE 11 WIRELESS CHARGING TECHNOLOGY

- 4.6.7 PLUGLESS POWER'S WIRELESS LEVEL 2 CHARGING SYSTEM

- 4.6.8 ELECTREON'S DYNAMIC AND STATIONARY EV CHARGING INFRASTRUCTURE

- 4.6.9 HEVO AND VEHYA'S WIRELESS EV CHARGING SOLUTION

- 4.7 INVESTMENT AND FUNDING SCENARIO

- 4.8 PATENT ANALYSIS

- 4.9 TECHNOLOGY ANALYSIS

- 4.9.1 KEY TECHNOLOGIES

- 4.9.1.1 Moving-field inductive power transfer

- 4.9.1.2 Resonant charging

- 4.9.1.3 Dynamic wireless charging

- 4.9.1.4 Power electronics and conversion

- 4.9.2 COMPLEMENTARY TECHNOLOGIES

- 4.9.2.1 Capacitive wireless power transfer

- 4.9.2.2 Thermal management

- 4.9.2.3 Foreign object detection

- 4.9.3 ADJACENT TECHNOLOGIES

- 4.9.3.1 Bidirectional charging

- 4.9.3.2 Renewable energy integration

- 4.9.1 KEY TECHNOLOGIES

- 4.10 MARKET STRUCTURING AND COMPETITIVE PRIORITIES

- 4.10.1 GLOBAL ALIGNMENT OF WIRELESS CHARGING STANDARDS

- 4.10.2 ADOPTION OF WIRELESS EV CHARGING IN PASSENGER AND COMMERCIAL SEGMENTS

- 4.10.3 AUTOMOTIVE OEM POSITIONING IN WIRELESS EV CHARGING ECOSYSTEM

- 4.10.4 TECHNICAL CONSTRAINTS IN WIRELESS POWER TRANSFER

- 4.10.5 INFRASTRUCTURE MATURITY AND COMMERCIALIZATION TIMELINES

- 4.10.6 PUBLIC SECTOR INVESTMENT VS. PRIVATE SECTOR OPERATIONS

- 4.11 WIRELESS EV CHARGING INFRASTRUCTURE AND INTEGRATION DEPENDENCIES

- 4.11.1 SUPPLIER ECOSYSTEM AND TECHNOLOGY DIFFERENTIATION

- 4.11.2 UTILITY COORDINATION AND SMART GRID INTEGRATION

- 4.11.3 WIRELESS CHARGING APPLICATIONS IN HIGH-DUTY FLEET ENVIRONMENTS

- 4.11.4 INFRASTRUCTURE REQUIREMENTS FOR DYNAMIC ON-ROAD WIRELESS EV CHARGING SYSTEMS

- 4.12 INVESTMENT AND CAPEX ANALYSIS

- 4.12.1 CAPITAL EXPENDITURE VS. OPERATIONAL EFFICIENCY MODELS

- 4.12.2 REAL ESTATE AND PARKING PARTNERSHIPS

- 4.12.3 INSURANCE AND WARRANTY CONSIDERATIONS

- 4.13 REGULATORY OVERVIEW

- 4.13.1 NETHERLANDS

- 4.13.2 GERMANY

- 4.13.3 FRANCE

- 4.13.4 UK

- 4.13.5 CHINA

- 4.13.6 US

- 4.13.7 REGULATORY POLICIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 4.14 KEY CONFERENCES AND EVENTS, 2026-2027

- 4.15 GLOBAL EV TRENDS

- 4.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 4.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 4.16.2 BUYING CRITERIA

- 4.17 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.18 OEM ANALYSIS

- 4.18.1 OEM-TECHNOLOGY PARTNER MAPPING FOR WIRELESS CHARGING BY VEHICLE MODEL

- 4.18.2 VALUE PROPOSITION FOR WIRELESS VS. WIRED CHARGING

- 4.18.3 PLAYER INTERRELATIONSHIPS: PLATFORM LEADERS VS. SYSTEM PROVIDERS VS. DYNAMIC CHARGING INNOVATORS

- 4.18.4 OEM READINESS AND INTEGRATION STRATEGY

- 4.18.4.1 Strategic trends in wireless EV charging adoption

- 4.18.4.2 Futuristic strategic insights: Road to 2030

- 4.18.5 DATA MONETIZATION STRATEGIES

5 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING SYSTEM

- 5.1 INTRODUCTION

- 5.1.1 WIRELESS CHARGING SYSTEM OFFERINGS BY KEY PLAYERS

- 5.2 MAGNETIC POWER TRANSFER

- 5.2.1 ADVANTAGES OF MAGNETIC RESONANCE COUPLING TO DRIVE MARKET

- 5.3 INDUCTIVE POWER TRANSFER

- 5.3.1 LOWER COST AND MINIMAL MAINTENANCE REQUIREMENTS TO DRIVE MARKET

- 5.4 CAPACITIVE POWER TRANSFER

- 5.5 PRIMARY INSIGHTS

6 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY CHARGING TYPE

- 6.1 INTRODUCTION

- 6.1.1 COMPARISON BETWEEN WIRELESS CHARGING TYPES

- 6.2 STATIONARY WIRELESS CHARGING

- 6.3 DYNAMIC WIRELESS CHARGING

- 6.4 PRIMARY INSIGHTS

7 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY APPLICATION

- 7.1 INTRODUCTION

- 7.1.1 POWER SUPPLY RANGE OF HOME CHARGING UNITS OFFERED BY LEADING PLAYERS

- 7.2 HOME CHARGING UNITS

- 7.2.1 HEIGHTENED PASSENGER CAR SALES AMID GROWING CONCERNS AROUND EMISSIONS TO DRIVE MARKET

- 7.3 COMMERCIAL CHARGING STATIONS

- 7.4 PRIMARY INSIGHTS

8 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT

- 8.1 INTRODUCTION

- 8.2 BASE CHARGING PADS

- 8.2.1 SIMPLE DESIGN, RELIABLE PERFORMANCE, AND REDUCED NEED FOR USER INTERACTION TO DRIVE MARKET

- 8.3 POWER CONTROL UNITS

- 8.3.1 INCREASED INVESTMENTS IN WIRELESS CHARGING INFRASTRUCTURE TO DRIVE MARKET

- 8.4 VEHICLE CHARGING PADS

- 8.4.1 RAPID DEPLOYMENT INTO NEWER EV MODELS TO DRIVE MARKET

- 8.5 PRIMARY INSIGHTS

9 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY RANGE

- 9.1 INTRODUCTION

- 9.1.1 POWER SUPPLY RANGE OFFERED BY KEY PLAYERS

- 9.2 <3.7 KW

- 9.2.1 LOWER POWER REQUIREMENT TO DRIVE GROWTH

- 9.3 3.7-7.7 KW

- 9.3.1 FOCUS ON INTEGRATING MID-POWER WIRELESS CHARGING SYSTEMS INTO VEHICLE PLATFORMS TO DRIVE MARKET

- 9.4 7.8-11 KW

- 9.4.1 NEED FOR HIGH-POWER WIRELESS CHARGING IN HEAVY-DUTY OPERATIONS TO DRIVE MARKET

- 9.5 >11 KW

- 9.5.1 EXPANSION OF LOGISTICS AND COMMERCIAL FLEETS TO DRIVE MARKET

- 9.6 PRIMARY INSIGHTS

10 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY PROPULSION

- 10.1 INTRODUCTION

- 10.2 BEV

- 10.2.1 EMPHASIS ON ZERO-EMISSION MOBILITY AND IMPROVEMENTS IN DRIVING RANGE AND BATTERY PERFORMANCE TO DRIVE MARKET

- 10.3 PHEV

- 10.3.1 NEED TO IMPROVE CHARGING CONVENIENCE AND SUPPORT REGULAR TOP-UP CHARGING TO DRIVE MARKET

- 10.4 PRIMARY INSIGHTS

11 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE

- 11.1 INTRODUCTION

- 11.2 PASSENGER CARS

- 11.2.1 CONSUMER DEMAND FOR CONVENIENCE, AUTOMATION, AND SEAMLESS USER EXPERIENCE TO DRIVE MARKET

- 11.3 COMMERCIAL VEHICLES

- 11.3.1 INCREASING ELECTRIFICATION OF PUBLIC TRANSPORT SYSTEMS AND LAST-MILE DELIVERY FLEETS TO DRIVE MARKET

- 11.3.2 ELECTRIC BUSES

- 11.3.3 ELECTRIC VANS

- 11.3.4 ELECTRIC PICKUP TRUCKS

- 11.3.5 ELECTRIC TRUCKS

- 11.4 PRIMARY INSIGHTS

12 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Government subsidies for EV adoption to drive market

- 12.2.2 INDIA

- 12.2.2.1 Strong government backing and regulatory push for electrification to drive market

- 12.2.3 JAPAN

- 12.2.3.1 High demand for electric vehicles and focus on clean mobility to drive market

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Emphasis on penetration of electric vehicles and related charging infrastructure to drive market

- 12.2.1 CHINA

- 12.3 EUROPE

- 12.3.1 FRANCE

- 12.3.1.1 Public transport electrification and low-emission targets to drive market

- 12.3.2 GERMANY

- 12.3.2.1 OEM-led innovation to drive market

- 12.3.3 NETHERLANDS

- 12.3.3.1 Focus on increasing charging infrastructure to drive market

- 12.3.4 NORWAY

- 12.3.4.1 Transition toward electric mobility to drive market

- 12.3.5 SPAIN

- 12.3.5.1 National targets and policy measures focused on decarbonization to drive market

- 12.3.6 SWEDEN

- 12.3.6.1 Emphasis on innovation and clean transport to drive market

- 12.3.7 SWITZERLAND

- 12.3.7.1 Pilot projects and early wireless charging deployments to drive market

- 12.3.8 UK

- 12.3.8.1 Government-funded trials and fleet electrification to drive market

- 12.3.1 FRANCE

- 12.4 NORTH AMERICA

- 12.4.1 CANADA

- 12.4.1.1 Targeted fleet applications to drive market

- 12.4.2 US

- 12.4.2.1 Transit and logistics fleet demand to drive market

- 12.4.1 CANADA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.4 REVENUE ANALYSIS, 2021-2025

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Charging system footprint

- 13.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2026

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING

- 13.8.5.1 List of start-ups/SMEs

- 13.8.5.2 Competitive benchmarking of start-ups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 ELECTREON

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Other developments

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 WITRICITY AI TECH, LLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches/developments

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.3.4 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 ENRX

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches/developments

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.3.4 Other developments

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 HEVO INC.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches/developments

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses AND competitive threats

- 14.1.5 PLUGLESS POWER INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches/developments

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 MITSUBISHI ELECTRIC CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.7 TGOOD ELECTRIC CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.8 TOYOTA MOTOR CORPORATION

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.9 ROBERT BOSCH GMBH

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 CONTINENTAL AG

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 TOSHIBA CORPORATION

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.12 HELLA GMBH & CO. KGAA

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.1 ELECTREON

- 14.2 OTHER PLAYERS

- 14.2.1 IDEANOMICS INC.

- 14.2.2 VOLTERIO GMBH

- 14.2.3 MOJO MOBILITY INC.

- 14.2.4 BMW

- 14.2.5 FORTUM CORPORATION

- 14.2.6 HYUNDAI MOTOR COMPANY

- 14.2.7 PULS GMBH

- 14.2.8 DAIHEN CORPORATION

- 14.2.9 VIE GROUP CO., LTD.

- 14.2.10 IPT TECHNOLOGY GMBH

- 14.2.11 EASELINK GMBH

- 14.2.12 MAHLE GMBH

- 14.2.13 NISSAN MOTOR CO., LTD.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Primary interviewees from demand and supply sides

- 15.1.2.2 Breakdown of primary interviews

- 15.1.2.3 List of primary participants

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 DATA TRIANGULATION

- 15.4 FACTOR ANALYSIS

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.3.1 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY POWER SUPPLY, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.2 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY VEHICLE TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.3 WIRELESS CHARGING MARKET FOR ELECTRIC VEHICLES, BY COMPONENT, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 16.3.4 COMPANY INFORMATION

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS