|

시장보고서

상품코드

2037092

글리세릴 글루코사이드 시장 예측(-2031년) : 유형, 기능, 최종사용자 산업, 형태, 원료, 농도/유효 성분, 지역별Glyceryl Glucoside Market By Type, Functionality, End-use Industry, Form; Source, Concentration/Active, and Region - Global Forecast to 2031 |

||||||

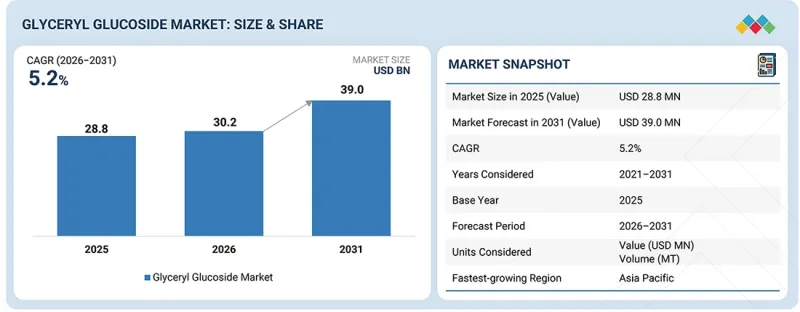

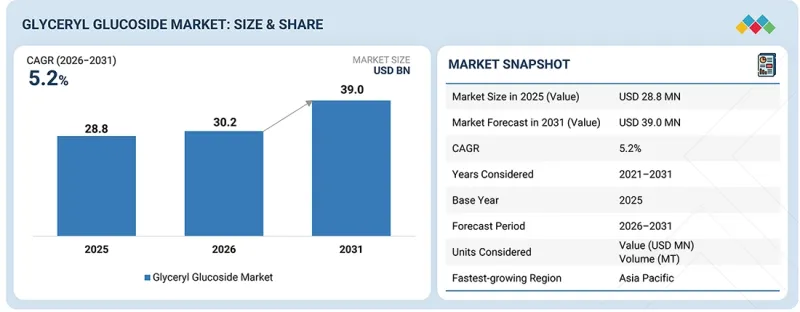

글리세릴 글루코사이드 시장 규모는 2026년 3,020만 달러에서 2031년에는 3,900만 달러에 달할 것으로 예측되고 있으며, 2026-2031년까지 CAGR은 5.2%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(달러) 및 톤 |

| 부문 | 유형, 기능, 최종사용자 산업, 형태, 원료, 농도/유효 성분, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

글리세릴 글루코사이드 시장은 2026년까지는 비교적 틈새 시장에 머물 것으로 예상되지만, 2031년까지 화장품 및 퍼스널 케어 분야에서 고성능 바이오 기반 보습제에 대한 수요 증가에 힘입어 안정적인 성장을 지속할 것으로 예상됩니다. 이 시장은 첨단 제품 제형 기술, 생명공학 기반 원료 개발, 데이터베이스 스킨케어 솔루션의 도입으로 변화하고 있습니다. BASF SE 및 Evonik Industries AG와 같은 주요 기업은 이 진화하는 시장에 전략적으로 집중하고 있습니다. 최근 혁신 기술로는 피부 침투력을 향상시키고, 지속적인 보습 효과를 제공하며, 클린 라벨 및 지속가능한 제품에 대한 수요를 충족시키기 위해 특별히 고안된 고순도 글리세릴글루코사이드가 있습니다. 각 업체들은 천연 화장품과 더마슈티컬에 대한 소비자 지향에 대응하기 위해 바이오 기반 생산 기술과 그린 케미스트리에 대한 투자를 확대하고 있습니다. 그 결과, 특히 럭셔리 더모코스메틱과 더마슈티컬에 대한 소비자의 관심 증가 등이 글리세릴글루코사이드를 포함한 고순도 및 프리미엄급 화장품에 대한 수요를 견인하며 글로벌 성장과 용도 확대를 견인할 것으로 예상됩니다.

기회와 디스럽션: 이 시장은 개인 맞춤형 뷰티 및 클린 뷰티 동향과 밀접한 관련이 있으며, 화장품 제조업체와 원료 공급업체 모두에게 큰 성장 잠재력을 보여주고 있습니다. 화장품 제조업체에게 글리세릴 글루코사이드는 특히 프리미엄 스킨케어 분야에서 고성능성 보습제, 안티에이징 제품, 장벽 기능 회복 솔루션의 배합을 가능하게 합니다. 원료 공급업체는 다기능적이고 지속가능한 유효성분 제공, 용도에 특화된 제형 개발, 생명공학을 통한 생산 모색을 통해 제품 라인업을 확장할 수 있는 다양한 기회를 얻게 되었습니다. 동시에 시장에서는 큰 변화가 일어나고 있습니다. 그 주요 요인으로는 생명공학 유래 원료의 급속한 보급, 화장품 제형에 대한 규제 심사 강화, 투명성과 지속가능성에 대한 소비자의 요구 등을 들 수 있습니다. 또한 최소한의 성분으로 과학적으로 입증된 제제를 찾는 움직임과 같은 시장 역학이 경쟁 구도를 크게 바꾸고 있습니다.

AI를 활용한 성분 최적화: 퍼스널 케어 및 화장품 업계에서는 성분 배합 최적화, 성분 적합성 예측, 성능 어필 강화를 위해 AI와 머신러닝이 점점 더 많이 활용되고 있습니다. 예를 들어 글리세릴 글루코사이드의 경우, 이러한 기술은 표적화된 제제 개발을 가능하게 하고, 유효성 시험을 개선하며, 혁신 주기를 가속화할 수 있습니다.

첨단 제형 기술은 복잡한 화장품 및 퍼스널 케어 제품의 제형에서 성분의 안정성, 생체 이용률 및 전반적인 성능을 향상시키는 데 중점을 두고 있습니다. 가공 기술에는 마이크로캡슐화, 리포좀 마이크로캡슐화, 대체 전달 시스템이 포함되며, 종종 히알루론산, 펩티드, 세라마이드와 같은 다른 활성 성분과 함께 배합하여 실현되는 경우가 많습니다.

원료별로는 천연 유래 부문이 주요 카테고리입니다.

이러한 선도적 지위는 퍼스널 케어 및 화장품 제품에서 바이오 기반 친환경 성분에 대한 소비자 수요가 증가하고 있기 때문입니다. 일반적으로 식물성 포도당과 글리세롤로 제조되는 천연 유래 글리세릴글루코사이드는 건강하고 환경 친화적인 화장품에 대한 소비자의 선호도가 높아짐에 따라 천연 유래 글리세릴글루코사이드의 수요가 증가하고 있습니다. 프리미엄 화장품 브랜드들이 이 성분을 적극적으로 채택하고, 규제 당국의 그린 케미스트리 추진과 더불어 천연 유래 부문의 급속한 성장을 촉진하고 있습니다. 또한 천연 성분의 건강 및 환경적 이점에 대한 인식이 높아짐에 따라 제조업체들은 재생하고 생분해 가능한 원료로 전환하고 있습니다.

세계의 글리세릴글루코사이드(Glyceryl Glucoside) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 글리세릴 글루코사이드 시장 : 유형별

제10장 글리세릴 글루코사이드 시장 : 기능별

제11장 글리세릴 글루코사이드 시장 : 원료별

제12장 글리세릴 글루코사이드 시장 : 형태별

제13장 글리세릴 글루코사이드 시장 : 농도별

제14장 글리세릴 글루코사이드 시장 : 용도별

제15장 글리세릴 글루코사이드 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 인접 시장 및 관련 시장

제20장 부록

KSA 26.05.29The glyceryl glucoside market is projected to reach USD 39.0 million by 2031 from USD 30.2 million in 2026, at a CAGR of 5.2% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD) and Volume (Metric Tons) |

| Segments | Type, Functionality, End-use Industry, Form, Source, Concentration / Active, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The glyceryl glucoside market is estimated to remain a relatively niche segment by 2026, with expectations of steady growth through 2031 due to a rising demand for high-performance, bio-based moisturizing agents in cosmetics and personal care applications. The market is witnessing a transformation driven by the adoption of advanced product formulation technologies, the development of biotechnology-based ingredients, and the implementation of data-driven skincare solutions. Key players such as BASF SE and Evonik Industries AG are focusing strategically on this evolving market. Recent innovations include specially formulated high-purity glyceryl glucosides designed to improve skin delivery, provide long-lasting hydration, and meet the demand for clean-label, sustainable products. Companies are increasingly investing in bio-based production techniques and green chemistry to align with the consumer trend towards natural cosmetics and dermaceuticals. Consequently, the growing consumer interest in "luxury" dermo-cosmetics and dermaceuticals, among other factors, is expected to drive the demand for high-purity and premium-grade cosmetics containing glyceryl glucosides, supporting consistent global growth and application.

Opportunities and disruptions: This market is closely tied to the increasing trend of personalized and clean beauty, showcasing significant growth potential for both cosmetics manufacturers and ingredient suppliers. For cosmetics companies, glyceryl glucoside enables the formulation of highly effective moisturizers, anti-aging products, and barrier-repair solutions, particularly in the premium skincare segment. Ingredient suppliers are presented with various opportunities to expand their product offerings by providing multifunctional and sustainable actives, developing application-specific formulations, and exploring biotech production. At the same time, the marketplace is undergoing substantial changes, highlighted by the swift adoption of biotech-based ingredients, stricter regulatory scrutiny of cosmetic formulations, and a consumer demand for transparency and sustainability. Additionally, market dynamics, such as the push for minimal and scientifically backed formulations, are significantly reshaping the competitive landscape.

AI-driven nutrient optimization: AI and machine learning are increasingly being used in the personal care and cosmetics industry to optimize ingredient blends, predict ingredient compatibility, and enhance performance claims. For instance, with glyceryl glucoside, these technologies enable targeted formulation development, improve efficacy testing, and accelerate innovation cycles.

Regarding advanced formulation technologies, the focus is on enhancing the stability, bioavailability, and overall performance of ingredients in complex cosmetic and personal care formulations. Processing technologies include microencapsulation, liposomal microencapsulation, and alternative delivery systems, often achieved through co-formulation with other active ingredients such as hyaluronic acid, peptides, and ceramides.

The natural segment is the leading category within the source segment of the glyceryl glucoside market.

This leadership can be attributed to the increasing consumer demand for bio-based and environmentally friendly ingredients in personal care and cosmetic products. Naturally derived glyceryl glucoside, typically produced from plant-sourced glucose and glycerol, aligns with consumers' growing preference for healthy, eco-conscious, and composition-friendly cosmetic products. The strong adoption of this ingredient by premium cosmetic brands, coupled with the advocacy for green chemistry from regulatory bodies, has fueled the rapid growth of the natural segment. Additionally, heightened awareness regarding the health and environmental benefits of natural ingredients is encouraging manufacturers to shift toward renewable and biodegradable raw material sources.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the glyceryl glucoside market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) -10%

Prominent companies in the market include BASF SE (Germany), Evonik Industries AG (Germany), YR Chemspec (China), Beiersdorf AG (Germany), Puri Pharma (China), Storm Chemical (China), Incospharm (South Korea), Nanjing DASF Biotechnology Co., Ltd. (China), Seebio Biotech (Shanghai) Co., Ltd. (China), Woosung CNT Co., Ltd. (South Korea), Sino Lion Chemical Co., Ltd. (China), Soho Aneco Chemical Co., Ltd. (China), Creative Biogene (US), DKSH (Switzerland), and Shandong Zhishang Chemical (China).

Research Coverage:

Global Glyceryl Glucoside Market by Type (Mono-glyceryl Glucosides, Di-glyceryl Glucosides, Tri-glyceryl/Higher Glycosides, Mixed Glycosides); By Functionality (Humectants & Moisturizing Agents, Emollients & Conditioning Agents, Texture, Stability & Processing Aids, Solubility & Compatibility Enhancers, Others); By End-use Industry (Personal Care & Cosmetics, Pharmaceuticals, Food & Beverages, Industrial, Others); By Form (Liquid Solutions, Powder, Formulated Blends, Others); By Source (Natural, Synthetic); By Concentration/Active Content (Low-concentration Grades <=45%, Mid-low Concentration Grades 45-55%, Mid-high Concentration Grades 55-65%, High-concentration Grades 65-85%+).and Region - Global Forecast to 2031

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the global glyceryl glucoside market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. Competitive analysis of upcoming startups in the global glyceryl glucoside market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue figures for the overall glyceryl glucoside market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

1. In-depth Segmentation across Type, Functionality, End-use Industry, Form, Source and Concentration/ Active Content: The study examines key drivers (rising demand for advanced skincare ingredients, increasing focus on hydration and anti-aging products, growing R&D and innovation in bio-based and specialty chemical ingredients, shift toward bio-based and sustainable ingredients), restraints (high production and formulation costs, limited awareness among small and mid-scale manufacturers, availability of substitute ingredients (e.g., hyaluronic acid, glycerin)), opportunities (expansion in premium and dermatological skincare segments, rising demand in Asia Pacific markets, Innovation in bio-catalysis and formulation technologies, Growing use in multifunctional cosmetic products), and challenges (regulatory compliance across regions, price sensitivity in developing markets, supply chain and raw material dependency, strong competition from established moisturizing ingredients)

2. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across the Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. It evaluates regional demand patterns, irrigation penetration, regulatory policies related to glyceryl glucoside, and investment trends in the glyceryl glucoside market, offering strategic guidance for expansion and localization initiatives.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, Deere & Company (US), AGCO Corporation (US), CNH Industrial N.V. (UK), Vaderstad AB (Sweden), Kinze Manufacturing (US), are profiled in detail. The report covers recent product launches, capacity expansions, strategic partnerships, and investments shaping the competitive dynamics of the global glyceryl glucoside market.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the global sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.8 RECESSION IMPACT

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN GLYCERYL GLUCOSIDE MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GLYCERYL GLUCOSIDE MARKET

- 3.2 GLYCERYL GLUCOSIDE MARKET, BY CONCENTRATION AND REGION

- 3.3 GLYCERYL GLUCOSIDE MARKET, BY SOURCE

- 3.4 GLYCERYL GLUCOSIDE MARKET, BY FUNCTIONALITY

- 3.5 GLYCERYL GLUCOSIDE MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for advanced skincare ingredients

- 4.2.1.2 Increasing focus on hydration and anti-aging products

- 4.2.1.3 Growing R&D and innovation in bio-based and specialty chemical ingredients

- 4.2.1.4 Shift toward bio-based and sustainable ingredients

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production and formulation costs

- 4.2.2.2 Limited awareness among small and mid-scale manufacturers

- 4.2.2.3 Availability of substitute ingredients

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion in premium and dermatological skincare segments

- 4.2.3.2 Rising demand in Asia Pacific markets

- 4.2.3.3 Innovation in bio-catalysis and formulation technologies

- 4.2.3.4 Growing use in multifunctional cosmetic products

- 4.2.4 CHALLENGES

- 4.2.4.1 Regulatory compliance across regions

- 4.2.4.2 Price sensitivity in developing markets

- 4.2.4.3 Supply chain and raw material dependency

- 4.2.4.4 Strong competition from established moisturizing ingredients

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN GLYCERYL GLUCOSIDE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 RETAIL SALES INDICATOR FOR PERSONAL CARE MARKET DEMAND

- 5.2.2 RAW MATERIAL PRICE MOVEMENT INDICATOR FOR GLYCERYL GLUCOSIDE PRODUCTION COST STRUCTURE

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 INTERMEDIATE PROCESSING & INGREDIENT MANUFACTURING

- 5.3.3 FORMULATION & PRODUCT DEVELOPMENT

- 5.3.4 CUSTOMIZATION & BRANDING

- 5.3.5 DISTRIBUTION & SUPPLY NETWORK

- 5.3.6 END USERS & POST-SALES SUPPORT

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY CONCENTRATION

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE TREND, BY FORM

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO OF HS CODE 2938

- 5.6.2 IMPORT SCENARIO OF HS CODE 2938

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 BASF SE LEVERAGES AI-DRIVEN FORMULATION PLATFORMS TO ACCELERATE BIO-BASED INGREDIENT INNOVATION

- 5.9.2 EVONIK INDUSTRIES AG UTILIZES AI AND COMPUTATIONAL BIOLOGY TO OPTIMIZE GLYCOSIDE PRODUCTION AND PERFORMANCE

- 5.9.3 BEIERSDORF AG APPLIES AI-POWERED SKIN RESEARCH TO ENHANCE EFFICACY OF ADVANCED SKINCARE INGREDIENTS

- 5.10 IMPACT OF 2026 US TARIFF - GLYCERYL GLUCOSIDE MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 China (Asia Pacific)

- 5.10.4.2 European Union

- 5.10.4.3 South Korea

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ENZYMATIC BIOCATALYSIS & PRECISION FERMENTATION

- 6.1.2 ADVANCED PROCESS PATENTS FOR STABILITY & FUNCTIONAL ENHANCEMENT

- 6.1.3 AI-DRIVEN FORMULATION & INGREDIENT OPTIMIZATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MICROENCAPSULATION & CONTROLLED-RELEASE DELIVERY SYSTEMS

- 6.2.2 GREEN CHEMISTRY & BIO-BASED FEEDSTOCK INTEGRATION

- 6.2.3 MULTI-FUNCTIONAL ACTIVE BLENDING & SYNERGISTIC FORMULATION TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 SYNTHETIC BIOLOGY & METABOLIC PATHWAY ENGINEERING

- 6.3.2 SKIN MICROBIOME MODULATION & BIO-ACTIVE DELIVERY PLATFORMS

- 6.3.3 DIGITAL SKIN DIAGNOSTICS & PERSONALIZED SKINCARE PLATFORMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 BIO-ENGINEERED HYDRATION ENHANCERS

- 6.6.2 AI-DRIVEN PERSONALIZED FORMULATIONS

- 6.6.3 ADVANCED ENCAPSULATION & DELIVERY SYSTEMS

- 6.6.4 MULTI-FUNCTIONAL INGREDIENT SYSTEMS

- 6.6.5 SUSTAINABLE BIO-BASED PRODUCTION

- 6.7 IMPACT OF GENERATIVE AI ON GLYCERYL GLUCOSIDE MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 USE OF GENERATIVE AI ON GLYCERYL GLUCOSIDE MARKET

- 6.7.3 TOP USE CASES AND MARKET POTENTIAL

- 6.7.4 BEST PRACTICES IN GLYCERYL GLUCOSIDES INDUSTRY

- 6.7.5 CASE STUDIES OF AI IMPLEMENTATION IN GLYCERYL GLUCOSIDE MARKET

- 6.7.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.8 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN GLYCERYL GLUCOSIDE MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.4.1 REGION-WISE LABELING STANDARDS

- 7.4.1.1 North America

- 7.4.1.2 Europe

- 7.4.1.3 Asia Pacific

- 7.4.1.4 South America

- 7.4.1.5 Rest of the World (RoW)

- 7.4.1 REGION-WISE LABELING STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIER AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USER/END-USE INDUSTRIES

- 8.4.1 PERSONAL CARE & COSMETICS INDUSTRY

- 8.4.2 DERMATOLOGY & PHARMACEUTICAL INDUSTRY

- 8.4.3 BIOTECHNOLOGY & LIFE SCIENCES INDUSTRY

- 8.4.4 FOOD & NUTRACEUTICAL INDUSTRY

- 8.5 MARKET PROFITABILITY

9 GLYCERYL GLUCOSIDE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 MONO-GLYCERYL GLUCOSIDES

- 9.2.1 DRIVING VOLUME GROWTH THROUGH COST-EFFICIENT HYDRATION ACTIVES

- 9.3 DI-GLYCERYL GLUCOSIDES

- 9.3.1 PREMIUMIZATION LEVER THROUGH ENHANCED MOISTURE RETENTION AND BARRIER FUNCTIONALITY

- 9.4 TRI-GLYCERYL/HIGHER GLYCOSIDES

- 9.4.1 ADVANCING HIGH-PERFORMANCE ACTIVES FOR LONG-LASTING HYDRATION AND BARRIER ENGINEERING

- 9.5 MIXED GLYCOSIDES

- 9.5.1 OPTIMIZING FORMULATION FLEXIBILITY THROUGH MULTI-FUNCTIONAL GLYCOSIDE BLENDS

10 GLYCERYL GLUCOSIDE MARKET, BY FUNCTIONALITY

- 10.1 INTRODUCTION

- 10.2 HUMECTANTS & MOISTURIZING AGENTS

- 10.2.1 STRENGTHENING CORE DEMAND THROUGH BIOLOGICALLY ACTIVE HYDRATION SYSTEMS

- 10.3 EMOLLIENTS & CONDITIONING AGENTS

- 10.3.1 ENHANCING SENSORY PERFORMANCE AND BARRIER CONDITIONING IN ADVANCED FORMULATIONS

- 10.4 TEXTURE, STABILITY, & PROCESSING AIDS

- 10.4.1 ENABLING FORMULATION EFFICIENCY THROUGH MULTIFUNCTIONAL STABILIZATION SYSTEMS

- 10.5 SOLUBILITY & COMPATIBILITY ENHANCERS

- 10.5.1 FACILITATING ACTIVE INTEGRATION IN COMPLEX, MULTI-PHASE FORMULATIONS

- 10.6 OTHERS

11 GLYCERYL GLUCOSIDE MARKET, BY SOURCE

- 11.1 INTRODUCTION

- 11.2 NATURAL

- 11.2.1 DRIVING PREMIUM POSITIONING THROUGH BIO-BASED AND TRACEABLE INGREDIENT SYSTEMS

- 11.3 SYNTHETIC

- 11.3.1 ENSURING COST EFFICIENCY AND SCALABLE SUPPLY THROUGH CONTROLLED CHEMICAL SYNTHESIS

12 GLYCERYL GLUCOSIDE MARKET, BY FORM

- 12.1 INTRODUCTION

- 12.2 LIQUID SOLUTIONS

- 12.2.1 MAXIMIZING FORMULATION EFFICIENCY THROUGH READY-TO-USE AQUEOUS SYSTEMS

- 12.3 POWDER

- 12.3.1 ENABLING HIGH PURITY, CONCENTRATED FORMATS FOR PRECISION FORMULATION AND SUPPLY CHAIN EFFICIENCY

- 12.4 FORMULATED BLENDS & OTHERS

- 12.4.1 ACCELERATING TIME-TO-MARKET THROUGH PRE-OPTIMIZED MULTIFUNCTIONAL SYSTEMS

13 GLYCERYL GLUCOSIDE MARKET, BY CONCENTRATION

- 13.1 INTRODUCTION

- 13.2 LOW-CONCENTRATION GRADES (<=45%)

- 13.2.1 OPTIMIZING PERFORMANCE WITH LOW-CONCENTRATION GLYCERYL GLUCOSIDE SOLUTIONS

- 13.3 MID-LOW CONCENTRATION GRADES (45-55%)

- 13.3.1 ENHANCING FORMULATION EFFICIENCY WITH MID-LOW CONCENTRATION GLYCERYL GLUCOSIDE GRADES

- 13.4 MID-HIGH CONCENTRATION GRADES (55-65%)

- 13.4.1 MAXIMIZING FUNCTIONAL IMPACT WITH MID-HIGH CONCENTRATION GLYCERYL GLUCOSIDE GRADES

- 13.5 HIGH-CONCENTRATION GRADES (65-85%+)

- 13.5.1 DRIVING PREMIUM PERFORMANCE WITH HIGH-CONCENTRATION GLYCERYL GLUCOSIDE GRADES

14 GLYCERYL GLUCOSIDE MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 PERSONAL CARE & COSMETICS

- 14.2.1 ACCELERATING DEMAND THROUGH BIOACTIVE HYDRATION AND CLEAN-LABEL FORMULATIONS

- 14.3 PHARMACEUTICALS

- 14.3.1 EXPANDING UTILITY AS FUNCTIONAL EXCIPIENT IN DERMATOLOGICAL AND TOPICAL THERAPIES

- 14.4 FOOD & BEVERAGES

- 14.4.1 EXPLORING NICHE FUNCTIONAL ROLES IN CLEAN-LABEL AND STABILITY-DRIVEN FORMULATIONS

- 14.5 INDUSTRIAL & OTHERS

- 14.5.1 LEVERAGING PROCESS EFFICIENCY AND COMPATIBILITY IN SPECIALTY INDUSTRIAL APPLICATIONS

15 GLYCERYL GLUCOSIDE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Demand for advanced dermaceutical innovation and premium skincare to drive market

- 15.2.2 CANADA

- 15.2.2.1 Clean beauty and regulatory-driven innovation to support glyceryl glucoside uptake

- 15.2.3 MEXICO

- 15.2.3.1 Expanding mid-market skincare and manufacturing base to drive glyceryl glucoside demand

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Advanced chemical manufacturing and sustainable skincare innovation to drive market

- 15.3.2 FRANCE

- 15.3.2.1 Luxury skincare leadership and formulation excellence to drive market

- 15.3.3 UK

- 15.3.3.1 Science-backed skincare and regulatory transparency to drive market

- 15.3.4 ITALY

- 15.3.4.1 Premium formulation craftsmanship and natural ingredient integration to drive market

- 15.3.5 SPAIN

- 15.3.5.1 Growing dermo-cosmetic demand and export-oriented manufacturing to drive market

- 15.3.6 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Technology-led skincare expansion and domestic manufacturing strength to drive market

- 15.4.2 INDIA

- 15.4.2.1 Rising domestic personal care demand and cost-effective formulation trends to drive market

- 15.4.3 JAPAN

- 15.4.3.1 Advanced skincare innovation and high-purity formulation standards to drive market

- 15.4.4 AUSTRALIA & NEW ZEALAND

- 15.4.4.1 Clean beauty leadership and premium skincare demand to drive market

- 15.4.5 SOUTH KOREA

- 15.4.5.1 Advanced K-beauty innovation and functional skincare leadership to drive market

- 15.4.6 INDONESIA

- 15.4.6.1 Expanding mass-market skincare and halal-compliant formulation trends to drive market

- 15.4.7 THAILAND

- 15.4.7.1 Growing dermo-cosmetic demand and tourism-driven skincare market to support glyceryl glucoside adoption

- 15.4.8 MALAYSIA

- 15.4.8.1 Southeast Asia export hub and clean beauty shift to drive glyceryl glucoside demand

- 15.4.9 VIETNAM

- 15.4.9.1 Emerging skincare market and rapid urbanization to drive glyceryl glucoside demand

- 15.4.10 PHILIPPINES

- 15.4.10.1 Rising mass-premium transition and climate-driven skincare needs to drive market

- 15.4.11 SINGAPORE

- 15.4.11.1 Regional innovation gateway and high-value skincare ecosystem to accelerate glyceryl glucoside demand

- 15.4.12 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.5.1.1 Expanding local production and premium skincare development to drive market

- 15.5.2 ARGENTINA

- 15.5.2.1 Strengthening domestic formulation capabilities and import substitution to drive market

- 15.5.3 REST OF SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.6 REST OF THE WORLD

- 15.6.1 AFRICA

- 15.6.1.1 Gradual premiumization and climate-driven skincare need to support market growth

- 15.6.2 MIDDLE EAST

- 15.6.2.1 Premium skincare demand and climate-specific formulation needs to drive market

- 15.6.1 AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 16.3 REVENUE ANALYSIS, 2021-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.4.1 BASF SE (GERMANY)

- 16.4.2 WOOSUNG CNT CO., LTD. (SOUTH KOREA)

- 16.4.3 BITOP AG (GERMANY)

- 16.5 PRODUCT COMPARISON

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6.5.1 Company footprint

- 16.6.5.2 Type footprint

- 16.6.5.3 Functionality footprint

- 16.6.5.4 End-use industry footprint

- 16.6.5.5 Source footprint

- 16.6.5.6 Form footprint

- 16.6.5.7 Concentration footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPETITIVE SCENARIO

- 16.8.1 DEALS

- 16.8.2 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 BASF SE

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.3.2 Expansions

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 EVONIK INDUSTRIES AG

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Deals

- 17.1.2.3.2 Expansions

- 17.1.2.3.3 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 YR CHEMSPEC

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 MnM view

- 17.1.3.3.1 Key strengths

- 17.1.3.3.2 Strategic choices

- 17.1.3.3.3 Weaknesses and competitive threats

- 17.1.4 BEIERSDORF AG

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.3.2 Expansions

- 17.1.4.3.3 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 PURI PHARMACEUTICAL CO., LTD

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 STORM CORPORATION

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 MnM view

- 17.1.7 INCOSPHARM

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 MnM view

- 17.1.8 NANJING DASF BIOTECHNOLOGY CO., LTD.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 MnM view

- 17.1.9 SEEBIO BIOTECH (SHANGHAI) CO., LTD

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 MnM view

- 17.1.10 WOOSUNG CNT CO., LTD.

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 MnM view

- 17.1.11 SINO LION CHEMICAL CO., LTD.

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 MnM view

- 17.1.12 SOHO ANECO CHEMICAL CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 MnM view

- 17.1.13 CREATIVE BIOGENE

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 MnM view

- 17.1.14 DKSH

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 MnM view

- 17.1.15 SHANDONG ZHISHANG CHEMICAL CO., LTD.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 MnM view

- 17.1.1 BASF SE

- 17.2 OTHER PLAYERS

- 17.2.1 GENECHEM

- 17.2.1.1 Business overview

- 17.2.1.2 Products offered

- 17.2.1.3 MnM view

- 17.2.2 ECSA CHEMICALS

- 17.2.2.1 Business overview

- 17.2.2.2 Products offered

- 17.2.2.3 MnM view

- 17.2.3 DADIA CHEMICAL INDUSTRIES

- 17.2.3.1 Business overview

- 17.2.3.2 Products offered

- 17.2.3.3 MnM view

- 17.2.4 GIHI CHEMICALS CO., LIMITED

- 17.2.4.1 Business overview

- 17.2.4.2 Products offered

- 17.2.4.3 MnM view

- 17.2.5 BIOTOP AG

- 17.2.5.1 Business overview

- 17.2.5.2 Products offered

- 17.2.5.3 MnM view

- 17.2.6 UNIPROMA

- 17.2.7 SUZHOU GREENWAY BIOTECH CO., LTD.

- 17.2.8 CHEMIPAN CORPORATION CO., LTD.

- 17.2.9 SUZHOU NMT BIOTECH

- 17.2.10 COSROMA

- 17.2.1 GENECHEM

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of major secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Key industry insights

- 18.1.2.3 Breakdown of primaries

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to estimate market size using top-down analysis

- 18.3 DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

19 ADJACENT AND RELATED MARKETS

- 19.1 INTRODUCTION

- 19.2 LIMITATIONS

- 19.3 FOOD EMULSIFIERS MARKET

- 19.3.1 MARKET DEFINITION

- 19.3.2 MARKET OVERVIEW

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS