|

시장보고서

상품코드

2037804

도심 항공 모빌리티(UAM) 시장 예측(-2035년) : 시스템별, 용도별, 인프라별, 항속거리별, 아키텍처별, 지역별Urban Air Mobility (UAM) Market by Systems (Aerostructure, Propulsion, Electrical, Avionics, FCS, Interiors), Application (Passenger, Cargo & Logistics, Medical & Disaster, Private), Infrastructure, Range, Architecture, Region - Global Forecast to 2035 |

||||||

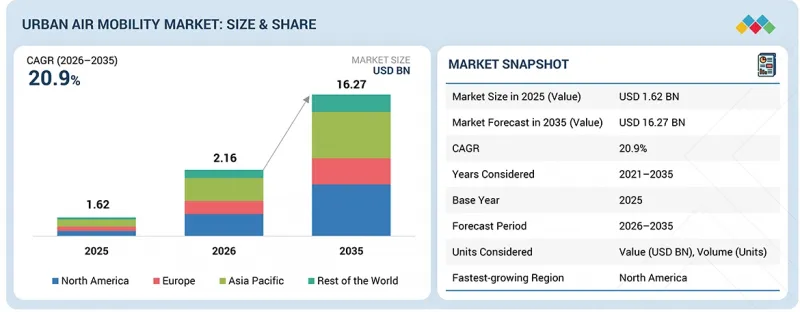

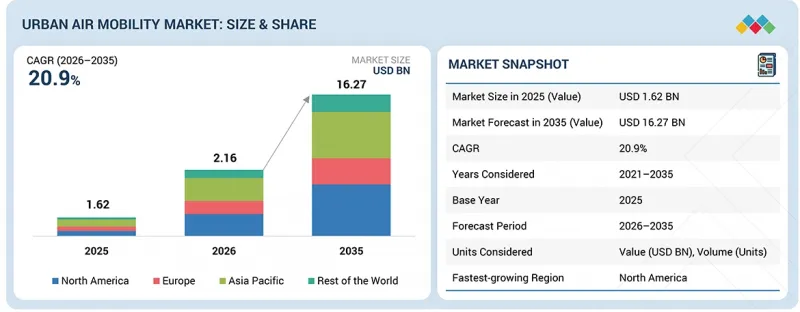

세계의 도심 항공 모빌리티(UAM) 시장 규모는 2026년 21억 6,000만 달러에서 2035년까지 162억 7,000만 달러에 달할 것으로 예측되며, 2031-2035년에 CAGR로 20.9%의 성장이 전망되고 있습니다.

도심의 교통체증 악화로 인해 시장이 확대되고 있습니다. 많은 지역에서 도로 혼잡이 심해지면서 사람들은 더 빠른 이동 수단을 원하고 있습니다. 이러한 수요 증가는 새로운 모빌리티 솔루션에 대한 모색을 촉진하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2035년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 단위 | 10억 달러 |

| 부문 | 시스템, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

도시 인구가 증가함에 따라 시간을 절약할 수 있는 효율적인 지점 간 운송에 대한 요구가 점점 더 중요해지고 있습니다. 전기 추진 시스템과 배터리 시스템의 개선이 계속되고 있으며, 자율 기능의 발전도 진행되고 있습니다. 특히 전기 수직이착륙기(eVTOL) 개발에서 두드러집니다. 정부와 민간 기업 모두 이 분야에 많은 투자를 하고 있으며, 지원적인 규제 또한 도심 항공 모빌리티(UAM) 솔루션의 조기 개발을 촉진하고 있습니다.

"플랫폼 아키텍처별로는 틸트 로터/틸트 윙 부문이 이 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

틸트 로터/틸트 윙 부문의 성장은 효율적인 전진 비행과 함께 수직 이륙을 가능하게 하는 능력에 의해 지원되고 있습니다. 이 설계로 인해 운항 중 높은 속도를 실현하고 있습니다. 또한 다른 구성에 비해 항속거리도 길어집니다. 에너지 사용 효율이 높기 때문에 전반적인 성능이 향상됩니다. 이 항공기는 도시 간 이동에 적합합니다. 지역적 연결성도 중요한 사용 사례 중 하나입니다.

"용도별로는 개인 소유/사용 부문이 2026-2030년 가장 높은 CAGR로 성장할 것으로 예측됩니다. "

개인 소유/사용 부문의 성장은 개인화된 이동 수단에 대한 수요에 의해 촉진되고 있습니다. 부유층은 더 빠른 이동 솔루션을 원하고 있으며, 기업 사용자들도 효율성을 높이기 위해 포인트 투 포인트 이동을 선택하는 경향이 증가하고 있습니다. 이러한 추세로 인해 기존 상업용 운송 네트워크에 대한 의존도가 낮아지고 있습니다. eVTOL(전기 수직이착륙기) 기술의 발전이 성능 향상에 기여하는 한편, 안전 기능의 강화로 사용자의 신뢰가 더욱 높아지고 있습니다. 다양한 시장에서 프리미엄 모빌리티 서비스에 대한 투자가 증가하면서 민간 도심 항공 모빌리티(UAM)에 대한 선택의 폭이 넓어지고 있으며, 이는 이 부문의 보급을 지원하고 있습니다. 그 결과, 유연한 교통 솔루션에 대한 수요는 더욱 증가할 것으로 예상됩니다.

"아시아태평양이 2025년 가장 큰 시장 점유율을 차지할 것으로 보입니다. "

주요 도시의 교통 혼잡이 악화되면서 더 나은 이동성에 대한 수요가 증가하고 있습니다. 중국, 일본, 한국 정부는 파일럿 프로그램을 통해 도심 항공 모빌리티(UAM)의 성장을 지원하고 있습니다. 주요 시장에서는 자금 지원도 증가하고 있습니다. 규제적 노력이 서비스의 조기 출시를 촉진하고 있습니다. 도시 인구도 증가하고 있으며, 교통 시스템에 더 많은 부담을 주고 있습니다. 도시에서는 한정된 공간 내에서 보다 빠른 이동 수단이 요구되고 있습니다. 일부 도시에서는 파일럿 프로젝트가 확대되고 있으며, 현장 테스트가 추진되고 있습니다.

세계의 도심 항공 모빌리티(UAM) 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제8장 지속가능성과 규제 상황

제9장 도심 항공 모빌리티(UAM) 시장 : 플랫폼 시스템별

제10장 도심 항공 모빌리티(UAM) 시장 : 인프라별

제11장 도심 항공 모빌리티(UAM) 시장 : 용도별

제12장 도심 항공 모빌리티(UAM) 시장 : 동작 방식별

제13장 도심 항공 모빌리티(UAM) 시장 : 항속거리별

제14장 도심 항공 모빌리티(UAM) 시장 : 최종사용자별

제15장 도심 항공 모빌리티(UAM) 시장 : 플랫폼 아키텍처별

제16장 도심 항공 모빌리티(UAM) 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSA 26.06.04The global urban air mobility market is projected to grow from USD 2.16 billion in 2026 to reach USD 16.27 billion by 2035, at a CAGR of 20.9% from 2031 to 2035. The market is expanding due to increasing traffic congestion in cities. Many areas are experiencing crowded roads, which drives people to look for faster travel options. This rising demand is fueling the search for new mobility solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By Systems, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

As urban populations grow, the need for efficient point-to-point transportation that saves time becomes even more critical. Improvements in electric propulsion and battery systems are ongoing, and advancements in autonomous features are also progressing, especially in the development of electric vertical take-off and landing (eVTOL) aircraft. Both governments and private companies are making significant investments in this area, and supportive regulations are aiding the early development of urban air mobility (UAM) solutions.

"By platform architecture, the tilt-rotor/tilt-wing segment is expected to grow at the highest CAGR during the period."

The growth of the tilt-rotor/tilt-wing segment is driven by its ability to support vertical take-off with efficient forward flight. This design helps achieve higher speeds during operations. It also supports a longer range compared to other configurations. Energy use is more efficient, which improves overall performance. These aircraft are suitable for intercity travel. Regional connectivity is also a key use case.

"By application, the private ownership/use segment is expected to grow at the highest CAGR from 2026 to 2030."

The growth of the private ownership/use segment is driven by demand for personalized travel options. High-net-worth individuals are seeking faster mobility solutions, and corporate users are increasingly opting for point-to-point travel to enhance efficiency. This trend reduces reliance on traditional commercial transport networks. Advancements in eVTOL (electric vertical take-off and landing) technology are contributing to improved performance, while enhancements in safety features are further building user confidence. As investments in premium mobility services rise across various markets, the availability of private urban air mobility (UAM) options is also expanding, supporting adoption in this sector. Consequently, the demand for flexible transportation solutions is expected to increase even further.

"Asia Pacific captured the largest market share in 2025."

Increasing congestion in major cities is pushing demand for better mobility. Governments in China, Japan, and South Korea are supporting the growth of urban air mobility through pilot programs. Funding support is also increasing in key markets. Regulatory initiatives are helping the early deployment of services. The urban population is also growing, which adds pressure on transport systems. Cities are looking for faster travel options within limited space. Pilot projects are expanding in selected urban areas. This is helping test real-world operations.

The breakdown of profiles for primary participants in the urban air mobility market is provided below:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East& Africa - 10%, Latin America - 5%

Research Coverage:

This market study examines the urban air mobility market across various segments and subsegments. It aims to estimate the market's size and growth potential in different regions. The study also provides a detailed competitive analysis of key market players, including their company profiles, product offerings, recent developments, and strategic market initiatives.

Reasons to buy this report:

The report will assist market leaders and new entrants with estimates of the revenue figures for the overall urban air mobility market. It will also enable stakeholders to understand the competitive landscape better and gain insights to position their businesses more effectively and develop appropriate go-to-market strategies. Additionally, the report will help stakeholders understand the market dynamics and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Rising urban congestion, demand for efficient mobility), Restraints (High certification complexity, evolving regulatory uncertainty), Opportunities (Expansion of UAM applications beyond passenger mobility), Challenges (Airspace integration & traffic management complexity)

- Market Penetration: Comprehensive information on the urban air mobility market is offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the urban air mobility market.

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the urban air mobility market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the urban air mobility market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN URBAN AIR MOBILITY MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN URBAN AIR MOBILITY MARKET

- 3.2 URBAN AIR MOBILITY MARKET, BY PLATFORM

- 3.3 URBAN AIR MOBILITY MARKET, BY OPERATION MODE

- 3.4 URBAN AIR MOBILITY MARKET, BY RANGE

- 3.5 URBAN AIR MOBILITY MARKET, BY END USER

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising urban congestion and demand for efficient mobility

- 4.2.1.2 Advancements in electric propulsion and supportive regulatory frameworks

- 4.2.1.3 Increasing investments and strategic partnerships across ecosystem

- 4.2.2 RESTRAINTS

- 4.2.2.1 High certification complexity and evolving regulatory uncertainty

- 4.2.2.2 Infrastructure limitations and high initial deployment costs

- 4.2.2.3 Public acceptance barriers and safety perception concerns

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of UAM applications beyond passenger mobility

- 4.2.3.2 Integration of UAM into smart cities and multimodal transport networks

- 4.2.3.3 Development of dedicated UAM infrastructure and vertiport networks

- 4.2.4 CHALLENGES

- 4.2.4.1 Airspace integration and traffic management complexity

- 4.2.4.2 Battery limitations and operational performance constraints

- 4.2.4.3 Supply chain constraints and limited production scalability

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 LIMITED AVAILABILITY OF STANDARDIZED AIRSPACE INTEGRATION SYSTEMS FOR URBAN ENVIRONMENTS

- 4.3.2 LIMITED DEVELOPMENT OF HIGH-EFFICIENCY CHARGING AND ENERGY INFRASTRUCTURE

- 4.3.3 LACK OF INTEGRATED DIGITAL PLATFORMS FOR END-TO-END UAM OPERATIONS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CONVERGENCE WITH LOGISTICS, E-COMMERCE, AND SUPPLY CHAIN NETWORKS

- 4.4.2 CONVERGENCE WITH ENERGY, BATTERY, AND ELECTRIC MOBILITY ECOSYSTEMS

- 4.4.3 CONVERGENCE WITH DEFENSE, PUBLIC SAFETY, AND EMERGENCY RESPONSE ECOSYSTEMS

- 4.4.4 CONVERGENCE WITH TELECOMMUNICATIONS, 5G, AND CONNECTIVITY INFRASTRUCTURE

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AVIATION INDUSTRY

- 5.2.4 TRENDS IN GLOBAL URBAN AIR MOBILITY (UAM) INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 R&D ENGINEERS (30%)

- 5.3.2 RAW MATERIAL SUPPLIERS (10%)

- 5.3.3 COMPONENT AND PRODUCT MANUFACTURERS (10%)

- 5.3.4 ASSEMBLERS AND INTEGRATORS (30%)

- 5.3.5 END USERS (20%)

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 MANUFACTURERS

- 5.4.2 SOLUTION AND SERVICE PROVIDERS

- 5.4.3 END USERS

- 5.5 INVESTMENT & FUNDING SCENARIO

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING ANALYSIS OF KEYPLAYERS, BY RANGE (2025-2026)

- 5.6.2 INDICATIVE PRICING ANALYSIS OF KEY PLAYER, BY MTOW

- 5.6.3 INDICATIVE PRICING ANALYSIS OF AIRCRAFT, BY PASSENGER CAPACITY

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8803)

- 5.7.2 EXPORT SCENARIO (HS CODE 8803)

- 5.8 KEY CONFERENCES & EVENTS

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SKYPORTS INFRASTRUCTURE DEPLOYED VERTIPORT SOLUTIONS ACROSS URBAN AND AIRPORT ENVIRONMENTS TO SUPPORT EVTOL AIRCRAFT OPERATIONS

- 5.10.2 FERROVIAL PARTNERED WITH URBAN AIR MOBILITY STAKEHOLDERS TO DEVELOP AIRPORT-CONNECTED VERTIPORT INFRASTRUCTURE DESIGNED FOR EVTOL AIRCRAFT OPERATIONS

- 5.10.3 GROUPE ADP COLLABORATED WITH TECHNOLOGY PROVIDERS, AVIATION COMPANIES, AND INFRASTRUCTURE PARTNERS TO DEVELOP VERTIPORT NETWORKS

- 5.11 IMPACT OF 2025 US TARIFFS

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRY/REGION

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON APPLICATIONS

- 5.11.4.1 Vertiport infrastructure

- 5.11.4.2 Battery and charging systems

- 5.11.4.3 Air traffic management and digital connectivity systems

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYERS, STAKEHOLDERS, AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.4 UNMET NEEDS FROM VARIOUS END-USER INDUSTRIES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 AUTONOMOUS FLIGHT AND ADVANCED FLIGHT CONTROL SYSTEMS

- 7.1.2 UTM-INTEGRATED AIRSPACE MANAGEMENT SYSTEMS

- 7.1.3 ELECTRIC PROPULSION, BATTERY SYSTEMS, AND HIGH-POWER VERTIPORT CHARGING

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 VERTIPORT INFRASTRUCTURE AND ENERGY MANAGEMENT SYSTEMS

- 7.2.2 COMMUNICATION, NAVIGATION, SURVEILLANCE, AND CYBERSECURITY SYSTEMS

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 UNMANNED AIRCRAFT SYSTEMS (UAS)/DRONE DELIVERY PLATFORMS

- 7.3.2 SMART MOBILITY & MULTIMODAL TRANSPORT INTEGRATION PLATFORMS

- 7.4 TECHNOLOGY ROADMAP

- 7.5 PATENT ANALYSIS

- 7.6 FUTURE APPLICATIONS

- 7.7 IMPACT OF AI/ GENERATIVE AI ON URBAN AIR MOBILITY MARKET

- 7.7.1 TOP USE CASES AND MARKET POTENTIAL

- 7.7.2 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN URBAN AIR MOBILITY MARKET

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.2 REGULATORY FRAMEWORK

- 8.3 INDUSTRY STANDARDS

- 8.4 SUSTAINABILITY INITIATIVES

- 8.4.1 ELECTRIFICATION AND ENERGY MANAGEMENT SYSTEMS

- 8.4.2 NOISE REDUCTION AND URBAN COMPLIANCE MEASURES

9 URBAN AIR MOBILITY (UAM) MARKET, BY PLATFORM SYSTEM (MARKET SIZE & FORECAST TO 2035 - USD MILLION)

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 INCREASING INVESTMENTS IN ELECTRIC PROPULSION, LIGHTWEIGHT STRUCTURES, AND ADVANCED AVIONICS TO DRIVE GROWTH

- 9.2.1.1 Use case: Electric propulsion system integration by Joby Aviation

- 9.2.2 AEROSTRUCTURES

- 9.2.2.1 Increasing demand for lightweight composite structures and high-strength materials to drive growth

- 9.2.3 PROPULSION SYSTEMS

- 9.2.3.1 Increasing advancements in electric propulsion technologies and battery efficiency to drive growth

- 9.2.4 AVIONICS

- 9.2.4.1 Increasing integration of advanced flight management, navigation, and safety systems to drive growth

- 9.2.5 ELECTRICAL SYSTEMS

- 9.2.5.1 Increasing demand for high-efficiency power distribution and advanced energy management systems to drive growth

- 9.2.6 FLIGHT CONTROL & SOFTWARE

- 9.2.6.1 Increasing adoption of autonomous flight technologies and digital aircraft management systems to drive growth

- 9.2.7 INTERIORS

- 9.2.7.1 Increasing focus on passenger comfort, lightweight cabin designs, and smart interior systems to drive growth

- 9.2.1 INCREASING INVESTMENTS IN ELECTRIC PROPULSION, LIGHTWEIGHT STRUCTURES, AND ADVANCED AVIONICS TO DRIVE GROWTH

- 9.3 SOFTWARE

- 9.3.1 INCREASING ADOPTION OF DIGITAL FLEET MANAGEMENT, AUTONOMOUS OPERATIONS, AND AIR TRAFFIC INTEGRATION SOFTWARE TO DRIVE GROWTH

- 9.3.1.1 Use case: Autonomous flight software platform by Wisk Aero

- 9.3.1 INCREASING ADOPTION OF DIGITAL FLEET MANAGEMENT, AUTONOMOUS OPERATIONS, AND AIR TRAFFIC INTEGRATION SOFTWARE TO DRIVE GROWTH

10 URBAN AIR MOBILITY MARKET, BY INFRASTRUCTURE (MARKET SIZE & FORECAST TO 2035 - USD MILLION)

- 10.1 INTRODUCTION

- 10.2 GROUND & CHARGING INFRASTRUCTURE

- 10.2.1 INCREASING INVESTMENTS IN VERTIPORT DEVELOPMENT AND ELECTRIC CHARGING NETWORKS TO DRIVE GROWTH

- 10.2.1.1 Use case: Vertiport infrastructure development by Skyports Infrastructure

- 10.2.2 VERTIPORTS/VERTISTOPS

- 10.2.2.1 Increasing development of urban landing infrastructure and passenger mobility hubs to drive growth

- 10.2.3 CHARGING & ENERGY SYSTEMS

- 10.2.3.1 Increasing demand for high-power charging infrastructure and advanced energy management solutions to drive growth

- 10.2.4 HANGARS & MAINTENANCE FACILITIES

- 10.2.4.1 Increasing investments in aircraft maintenance infrastructure and fleet support facilities to drive growth

- 10.2.1 INCREASING INVESTMENTS IN VERTIPORT DEVELOPMENT AND ELECTRIC CHARGING NETWORKS TO DRIVE GROWTH

- 10.3 AIRSPACE & TRAFFIC INFRASTRUCTURE

- 10.3.1 INCREASING NEED FOR SAFE AIRSPACE INTEGRATION AND REAL-TIME TRAFFIC MANAGEMENT TO DRIVE GROWTH

- 10.3.1.1 Use case: Digital airspace management platform by Frequentis

- 10.3.2 UTM SYSTEMS

- 10.3.2.1 Growing need for automated low-altitude traffic coordination to support scalable eVTOL operations

- 10.3.3 ATM INTEGRATION SYSTEMS

- 10.3.3.1 Increasing focus on integrating eVTOL operations with existing air traffic networks to drive adoption

- 10.3.4 COMMUNICATION, NAVIGATION, AND SURVEILLANCE SYSTEMS

- 10.3.4.1 Rising need for real-time aircraft connectivity and operational visibility to support urban airspace operations

- 10.3.5 FLEET MANAGEMENT SOFTWARE

- 10.3.5.1 Increasing need for real-time operational control and digital fleet optimization to support eVTOL scalability

- 10.3.1 INCREASING NEED FOR SAFE AIRSPACE INTEGRATION AND REAL-TIME TRAFFIC MANAGEMENT TO DRIVE GROWTH

11 URBAN AIR MOBILITY (UAM) MARKET, BY APPLICATION (MARKET SIZE & FORECAST TO 2035-USD MILLION)

- 11.1 INTRODUCTION

- 11.2 PASSENGER TRANSPORT

- 11.2.1 RISING DEMAND FOR FAST, SUSTAINABLE, AND CONGESTION-FREE URBAN TRANSPORTATION TO ACCELERATE ADOPTION

- 11.2.1.1 Use case: eVTOL platform development by Archer Aviation

- 11.2.1 RISING DEMAND FOR FAST, SUSTAINABLE, AND CONGESTION-FREE URBAN TRANSPORTATION TO ACCELERATE ADOPTION

- 11.3 CARGO & LOGISTICS

- 11.3.1 INCREASING DEMAND FOR AUTONOMOUS CARGO AIRCRAFT PLATFORMS AND HIGH-EFFICIENCY URBAN DELIVERY INFRASTRUCTURE TO DRIVE TECHNOLOGY DEVELOPMENT

- 11.3.1.1 Use case: Autonomous cargo eVTOL platform by Elroy Air

- 11.3.1 INCREASING DEMAND FOR AUTONOMOUS CARGO AIRCRAFT PLATFORMS AND HIGH-EFFICIENCY URBAN DELIVERY INFRASTRUCTURE TO DRIVE TECHNOLOGY DEVELOPMENT

- 11.4 MEDICAL & DISASTER RESPONSE

- 11.4.1 INCREASING FOCUS ON RAPID-DEPLOYMENT EVTOL PLATFORMS AND EMERGENCY AVIATION TECHNOLOGIES TO SUPPORT CRITICAL RESPONSE INFRASTRUCTURE

- 11.4.1.1 Use case: Autonomous eVTOL platform development by EHang

- 11.4.1 INCREASING FOCUS ON RAPID-DEPLOYMENT EVTOL PLATFORMS AND EMERGENCY AVIATION TECHNOLOGIES TO SUPPORT CRITICAL RESPONSE INFRASTRUCTURE

- 11.5 PRIVATE OWNERSHIP/USE

- 11.5.1 GROWING INTEREST IN PERSONAL EVTOL AIRCRAFT AND PREMIUM URBAN AVIATION TECHNOLOGIES TO SUPPORT MARKET

- 11.5.1.1 Use case: Personal eVTOL platform development by Jetson

- 11.5.1 GROWING INTEREST IN PERSONAL EVTOL AIRCRAFT AND PREMIUM URBAN AVIATION TECHNOLOGIES TO SUPPORT MARKET

12 URBAN AIR MOBILITY (UAM) MARKET, BY OPERATION MODE (MARKET SIZE & FORECAST TO 2035-USD MILLION)

- 12.1 INTRODUCTION

- 12.2 PILOTED

- 12.2.1 EARLY-STAGE COMMERCIALIZATION AND REGULATORY CERTIFICATION ACTIVITIES TO SUPPORT MARKET ADOPTION

- 12.2.1.1 Use case: Piloted eVTOL platform development by Joby Aviation

- 12.2.1 EARLY-STAGE COMMERCIALIZATION AND REGULATORY CERTIFICATION ACTIVITIES TO SUPPORT MARKET ADOPTION

- 12.3 REMOTELY OPERATED /SEMI-AUTONOMOUS

- 12.3.1 INCREASING INVESTMENTS IN FLIGHT AUTOMATION AND REMOTE OPERATION TECHNOLOGIES TO SUPPORT SCALABLE EVTOL OPERATIONS

- 12.3.1.1 Use case: Semi-autonomous eVTOL flight system by Wisk Aero

- 12.3.1 INCREASING INVESTMENTS IN FLIGHT AUTOMATION AND REMOTE OPERATION TECHNOLOGIES TO SUPPORT SCALABLE EVTOL OPERATIONS

- 12.4 FULLY AUTONOMOUS

- 12.4.1 ADVANCEMENTS IN ARTIFICIAL INTELLIGENCE AND AUTONOMOUS FLIGHT SYSTEMS TO ACCELERATE NEXT-GENERATION EVTOL DEVELOPMENT

- 12.4.1.1 Use case: Fully autonomous eVTOL platform by EHang

- 12.4.1 ADVANCEMENTS IN ARTIFICIAL INTELLIGENCE AND AUTONOMOUS FLIGHT SYSTEMS TO ACCELERATE NEXT-GENERATION EVTOL DEVELOPMENT

13 URBAN AIR MOBILITY (UAM) MARKET, BY RANGE (MARKET SIZE & FORECAST TO 2035-USD MILLION)

- 13.1 INTRODUCTION

- 13.2 SHORT RANGE (< 50 KM)

- 13.2.1 INCREASING FOCUS ON HIGH-FREQUENCY URBAN EVTOL OPERATIONS AND COMPACT AIRCRAFT ARCHITECTURES TO DRIVE MARKET GROWTH

- 13.2.1.1 Use case: Short-range eVTOL platform development by Archer Aviation

- 13.2.1 INCREASING FOCUS ON HIGH-FREQUENCY URBAN EVTOL OPERATIONS AND COMPACT AIRCRAFT ARCHITECTURES TO DRIVE MARKET GROWTH

- 13.3 MEDIUM RANGE (50-200 KM)

- 13.3.1 ADVANCEMENTS IN BATTERY PERFORMANCE AND AIRCRAFT EFFICIENCY TO SUPPORT EXTENDED EVTOL OPERATIONS

- 13.3.1.1 Use case: Medium-range eVTOL platform development by Eve Air Mobility

- 13.3.1 ADVANCEMENTS IN BATTERY PERFORMANCE AND AIRCRAFT EFFICIENCY TO SUPPORT EXTENDED EVTOL OPERATIONS

- 13.4 LONG RANGE (> 200 KM)

- 13.4.1 INCREASING DEVELOPMENT OF HIGH-ENDURANCE EVTOL PLATFORMS AND ADVANCED ENERGY SYSTEMS TO SUPPORT EXTENDED AIR MOBILITY OPERATIONS

- 13.4.1.1 Use case: Long-range electric aircraft platform by BETA Technologies

- 13.4.1 INCREASING DEVELOPMENT OF HIGH-ENDURANCE EVTOL PLATFORMS AND ADVANCED ENERGY SYSTEMS TO SUPPORT EXTENDED AIR MOBILITY OPERATIONS

14 URBAN AIR MOBILITY (UAM) MARKET, BY END USER (MARKET SIZE & FORECAST TO 2035-USD MILLION)

- 14.1 INTRODUCTION

- 14.2 COMMERCIAL FLEET OPERATORS

- 14.2.1 INCREASING FLEET SCALABILITY REQUIREMENTS AND DIGITAL OPERATIONAL INFRASTRUCTURE TO DRIVE MARKET EXPANSION

- 14.2.1.1 Use case: Integrated fleet management ecosystem by Eve Air Mobility

- 14.2.1 INCREASING FLEET SCALABILITY REQUIREMENTS AND DIGITAL OPERATIONAL INFRASTRUCTURE TO DRIVE MARKET EXPANSION

- 14.3 INSTITUTIONAL/GOVERNMENT

- 14.3.1 INCREASING GOVERNMENT SUPPORT FOR ADVANCED AIR MOBILITY INFRASTRUCTURE AND AIRSPACE MODERNIZATION TO DRIVE MARKET DEVELOPMENT

- 14.3.1.1 Use case: Advanced air mobility airspace integration program by Federal Aviation Administration (FAA)

- 14.3.1 INCREASING GOVERNMENT SUPPORT FOR ADVANCED AIR MOBILITY INFRASTRUCTURE AND AIRSPACE MODERNIZATION TO DRIVE MARKET DEVELOPMENT

- 14.4 PRIVATE/INDIVIDUAL USERS

- 14.4.1 GROWING INTEREST IN PERSONAL AVIATION TECHNOLOGIES AND USER-CENTRIC EVTOL PLATFORMS TO SUPPORT MARKET EXPANSION

- 14.4.1.1 Use case: Personal eVTOL aircraft platform by Doroni Aerospace

- 14.4.1 GROWING INTEREST IN PERSONAL AVIATION TECHNOLOGIES AND USER-CENTRIC EVTOL PLATFORMS TO SUPPORT MARKET EXPANSION

15 URBAN AIR MOBILITY (UAM) MARKET, BY PLATFORM ARCHITECTURE (MARKET SIZE & FORECAST TO 2035-USD MILLION)

- 15.1 INTRODUCTION

- 15.2 MULTIROTOR

- 15.2.1 INCREASING DEMAND FOR SIMPLE AIRCRAFT ARCHITECTURES AND HIGH-STABILITY LOW-ALTITUDE OPERATIONS TO DRIVE GROWTH

- 15.2.1.1 Use case: Autonomous multirotor eVTOL platform by EHang

- 15.2.1 INCREASING DEMAND FOR SIMPLE AIRCRAFT ARCHITECTURES AND HIGH-STABILITY LOW-ALTITUDE OPERATIONS TO DRIVE GROWTH

- 15.3 LIFT + CRUISE

- 15.3.1 INCREASING FOCUS ON BALANCING VERTICAL LIFT PERFORMANCE WITH EXTENDED FLIGHT EFFICIENCY TO SUPPORT GROWTH

- 15.3.1.1 Use case: Lift + cruise eVTOL platform by Archer Aviation

- 15.3.1 INCREASING FOCUS ON BALANCING VERTICAL LIFT PERFORMANCE WITH EXTENDED FLIGHT EFFICIENCY TO SUPPORT GROWTH

- 15.4 TILT-ROTOR/TILT-WING

- 15.4.1 INCREASING DEMAND FOR HIGH-SPEED EVTOL PLATFORMS AND ADVANCED AERODYNAMIC PERFORMANCE TO DRIVE MARKET DEVELOPMENT

- 15.4.1.1 Use case: Tilt-rotor eVTOL platform by Hyundai Supernal

- 15.4.1 INCREASING DEMAND FOR HIGH-SPEED EVTOL PLATFORMS AND ADVANCED AERODYNAMIC PERFORMANCE TO DRIVE MARKET DEVELOPMENT

16 URBAN AIR MOBILITY MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 FAA rules and pilot programs to drive market

- 16.2.2 CANADA

- 16.2.2.1 Regional access needs and airspace planning to drive market

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 UK

- 16.3.1.1 Policy milestones and funding programs to drive growth

- 16.3.2 GERMANY

- 16.3.2.1 Growth in industrial capability to drive market

- 16.3.3 FRANCE

- 16.3.3.1 Controlled route testing to drive practical market buildout

- 16.3.4 ITALY

- 16.3.4.1 Airport-led trials and vertiport rules to drive market development

- 16.3.5 SPAIN

- 16.3.5.1 Airspace testing and airport network planning to drive market

- 16.3.6 REST OF EUROPE

- 16.3.1 UK

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Low-altitude economy policy and certification progress drive market

- 16.4.2 JAPAN

- 16.4.2.1 Expo demonstrations and airline participation to drive market

- 16.4.3 SOUTH KOREA

- 16.4.3.1 Government test programs and digital infrastructure to drive market

- 16.4.4 SINGAPORE

- 16.4.4.1 Controlled deployment and standards leadership to drive market

- 16.4.5 AUSTRALIA

- 16.4.5.1 Regional mobility needs and regulatory roadmaps to drive growth

- 16.4.6 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 REST OF THE WORLD

- 16.5.1 LATIN AMERICA

- 16.5.1.1 Demand for better urban and suburban connectivity to drive market

- 16.5.2 MIDDLE EAST & AFRICA

- 16.5.2.1 Air taxi programs and urban infrastructure gaps to drive market readiness

- 16.5.1 LATIN AMERICA

17 COMPETITIVE LANDSCAPE

- 17.1 INTRODUCTION

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 17.3 REVENUE ANALYSIS, 2021-2025

- 17.4 MARKET SHARE ANALYSIS, 2026

- 17.5 BRAND/PRODUCT COMPARISON

- 17.6 COMPANY VALUATION AND FINANCIAL METRICS

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT

- 17.7.6 COMPANY FOOTPRINT

- 17.7.7 REGION FOOTPRINT

- 17.7.8 PLATFORM SYSTEM FOOTPRINT

- 17.7.9 INFRASTRUCTURE FOOTPRINT

- 17.7.10 APPLICATION FOOTPRINT

- 17.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING

- 17.8.5.1 List of startups/SMEs

- 17.8.5.2 Competitive benchmarking of startups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

- 17.9.3 OTHER DEVELOPMENTS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 JOBY AERO, INC.

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Deals

- 18.1.1.3.2 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 EHANG

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions offered

- 18.1.2.3 Recent development

- 18.1.2.3.1 Deals

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 ARCHER AVIATION INC.

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Deals

- 18.1.3.3.2 Other developments

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 SKYPORTS INFRASTRUCTURE LIMITED

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Deals

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 BETA TECHNOLOGIES, INC.

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Deals

- 18.1.5.3.2 Other developments

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 VERTICAL AEROSPACE

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches/Developments

- 18.1.6.3.2 Deals

- 18.1.7 EVE HOLDING, INC.

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions offered

- 18.1.7.3 Recent developments

- 18.1.7.4 Recent developments

- 18.1.7.5 Other developments

- 18.1.7.5.1 Other developments

- 18.1.8 AIRBUS

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Product launches/developments

- 18.1.8.3.2 Deals

- 18.1.9 TEXTRON INC.

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions offered

- 18.1.9.3 Recent developments

- 18.1.9.4 Recent developments

- 18.1.9.4.1 Deals

- 18.1.10 WISK AERO

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Services offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches/developments

- 18.1.10.3.2 Deals

- 18.1.10.3.3 Other developments

- 18.1.11 AUTOFLIGHT

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches/Developments

- 18.1.11.4 Recent developments

- 18.1.11.4.1 Deals

- 18.1.11.4.2 Other developments

- 18.1.12 FERROVIAL

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Other developments

- 18.1.13 URBANV

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.14 AEROPORTS DE PARIS

- 18.1.14.1 Business overview

- 18.1.14.2 Products/Solutions offered

- 18.1.14.3 Recent developments

- 18.1.14.3.1 Deals

- 18.1.15 THALES

- 18.1.15.1 Business overview

- 18.1.15.2 Products/Solutions offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 deals

- 18.1.15.3.2 Other developments

- 18.1.16 HONEYWELL INTERNATIONAL, INC.

- 18.1.16.1 Business overview

- 18.1.16.2 Products/Solutions offered

- 18.1.16.3 Recent developments

- 18.1.16.3.1 Deals

- 18.1.17 FREQUENTIS AG

- 18.1.17.1 Business overview

- 18.1.17.2 Products/Solutions offered

- 18.1.17.3 Recent developments

- 18.1.17.3.1 deals

- 18.1.17.3.2 Other developments

- 18.1.1 JOBY AERO, INC.

- 18.2 OTHER PLAYERS

- 18.2.1 TCAB TECH

- 18.2.2 SKYWAY TECHNOLOGIES, CORP

- 18.2.3 UNIFLY

- 18.2.4 DRONEUP LLC

- 18.2.5 OVERAIR, INC.

- 18.2.6 ASCENDANCE FLIGHT TECHNOLOGIES S.A.S.

- 18.2.7 ELECTRA.AERO

- 18.2.8 SKYDRIVE INC.

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Primary interview participants

- 19.1.2.2 Key data from primary sources

- 19.1.2.3 Breakdown of primary interviews

- 19.1.2.4 Key industry insights

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 BOTTOM-UP APPROACH

- 19.2.2 TOP-DOWN APPROACH

- 19.2.3 BASE NUMBER CALCULATION

- 19.3 DATA TRIANGULATION

- 19.4 FACTOR ANALYSIS

- 19.4.1 SUPPLY-SIDE INDICATORS

- 19.4.2 DEMAND-SIDE INDICATORS

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ASSESSMENT

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 ANNEXURE

- 20.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.4 CUSTOMIZATION OPTIONS

- 20.5 RELATED REPORTS

- 20.6 AUTHOR DETAILS