|

시장보고서

상품코드

2038239

혈액 분석기 및 시약 시장 예측(-2031년) : 제품 및 서비스, 가격대(고, 중, 저), 용도(감염증, 혈액암), 최종사용자별(병원, CTL, 정부계 실험실)Hematology Analyzers and Reagents Market by Product & Service, Price (High, Mid, Low), Application (Infectious Diseases, Blood Cancer), End User (Hospital, CTL, Govt Lab) - Global Forecast to 2031 |

||||||

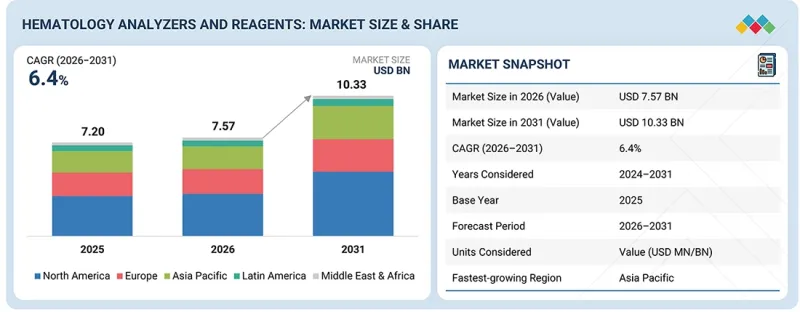

세계의 혈액 분석기 및 시약 시장 규모는 2026년 75억 7,000만 달러에서 2031년에는 103억 3,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 6.4%로 성장할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 제품·서비스, 가격대, 용도, 사용 형태, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

혈액 분석기 및 시약의 기술 발전은 향후 수년간 시장 성장의 주요 촉진제가 될 것으로 예상됩니다. 그러나 한편으로는 혈액 분석기 및 시약의 높은 비용, 신흥 국가의 숙련된 전문가 부족, 이들 지역의 첨단 혈액 검사 장비 도입 지연이 시장 성장을 저해할 수 있습니다.

"제품&서비스별로는 혈액학 부문이 2025년 가장 큰 점유율을 보일 것"

이 부문은 다시 장비, 시약, 소모품, 서비스 등으로 세분화됩니다. 성장을 촉진하는 요인으로는 검사 건수 증가, 혈액질환 유병률 증가, 5분류 및 6분류 백혈구 분획기, 유세포분석, AI 도입 등 기술 발전이 꼽힙니다.

"가격대별로는 저가형 부문이 2025년 가장 큰 점유율을 보일 것"

시장은 예측 기간 중도 저가형 혈액 분석기 부문이 시장을 주도할 것으로 예상됩니다. 이 부문의 우위가 예상되는 배경에는 비용 효율성이 높고, 소규모 연구소나 진단센터 등 자원이 부족한 환경에서도 우수한 성능을 발휘할 수 있다는 점이 있습니다. 이 장비는 3성분 백혈구 분획 기능을 갖추고 있으며, 컴팩트한 크기, 적은 검체량, 간편한 조작이 가능합니다.

세계의 혈액 분석기 및 시약 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 혈액 분석기 및 시약 시장 : 가격별

제10장 혈액 분석기 및 시약 시장 : 사용 형태별

제11장 혈액 분석기 및 시약 시장 : 제품·서비스별

제12장 혈액 분석기 및 시약 시장 : 용도별

제13장 혈액 분석기 및 시약 시장 : 최종사용자별

제14장 혈액 분석기 및 시약 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

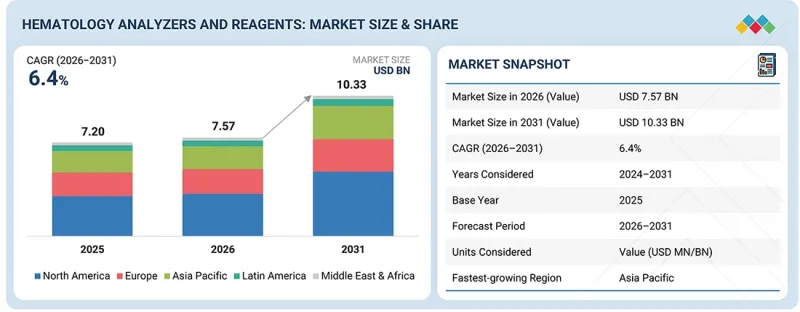

KSA 26.06.01The global hematology analyzers and reagents market is projected to reach USD 10.33 billion by 2031 from USD 7.57 billion in 2026, growing at a CAGR of 6.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product and Service, Price Range, Application, Usage Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Advancements in hematology analyzers and reagents are expected to be a primary driver of market growth in the coming years. However, the high costs of hematology analyzers and reagents, the shortage of skilled experts in emerging nations, and the slow adoption of advanced hematology devices in these regions could hinder growth in the hematology analyzers and reagents market.

"The hematology products and services segment held the largest share of the market in 2025."

The global market for hematology analyzers and reagents, by product and service, is segmented into hematology products & services, hemostasis products & services, and immunohematology products & services. Hematology products & services hold a dominant position in the global market for hematology analyzers and reagents. This segment is further divided into: instruments, reagents, consumables, and services. Factors driving growth include higher test volumes, rising prevalence of hematological conditions, and technological advancements such as the introduction of five- and six-part differential analyzers, flow cytometry, and artificial intelligence.

"The low-range hematology analyzers segment held the largest share of the market in 2025."

Based on price range, the hematology analyzers and reagents market is segmented into high-range hematology analyzers, mid-range hematology analyzers, and low-range hematology analyzers. It is anticipated that the market will be led by the low-range hematology analyzers segment throughout the forecast period. The anticipation of the dominance of the low-range hematology analyzer segment stems from its cost-effectiveness and ability to perform well in limited-resource environments, such as small labs and diagnostic centers. They come with a 3-part differential, small in size, smaller sample volumes, and are easy to operate.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1-40%, Tier 2-30%, and Tier 3- 30%

- By Designation: C-level-27%, Director-level-18%, and Others-55%

- By Region: North America-40%, Europe-32%, Asia Pacific-20%, Latin America-5%, and the Middle East & Africa-3%

The prominent players in the hematology analyzers and reagents market are F. Hoffmann-La Roche Ltd (Switzerland), Abbott Laboratories (US), Danaher Corporation (US), Diatron (Hungary), Drew Scientific (US), Siemens Healthineers (Germany), Sysmex Corporation (Japan), Bio-Rad Laboratories, Inc. (US), Horiba Ltd. (Japan), Nihon Kohden Corporation (Japan), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), BioSystems (Spain), and QuidelOrtho Corporation (US), among others.

Research Coverage

This report studies the hematology analyzers and reagents market based on product and service, price range, application, end user, and region. It also covers the factors driving market growth, analyzes the opportunities and challenges in the market, and provides details on the competitive landscape for market leaders. Furthermore, the report analyzes micro markets by their individual growth trends and forecasts revenue for the market segments across five main regions (and the respective countries within these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

- Analysis of key drivers (rapid integration of AI technology for increased accuracy of diagnosis and optimized hematology analysis workflows, advanced parameters and multi-functionality behind increasing use of hematology analyzers, growing requirements for affordable and efficient tests with first-pass yield and less reagents usage), restraints (expensive advanced hematology analyzer instruments hampering their implementation in healthcare institutions and limited accuracy of digital morphology analyzers in identifying abnormal cells), opportunities (expanding use of AI-based telehematology solutions and precision diagnostics offering advanced cell analysis and rare cell detection capabilities), and challenges (Increased complexity of data management and analysis due to the advent of next-generation hematology analyzers and laboratory shortages affecting workflow efficiency of hematology) influencing the growth of the contrast media market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in hematology analyzers and reagents market

- Market Development: Comprehensive information about lucrative markets-the report analyses the hematology analyzers and reagents market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the hematology analyzers and reagents market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 3.2 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY REGION

- 3.3 HEMATOLOGY ANALYZERS AND REAGENTS MARKET IN ASIA PACIFIC, BY END USER AND COUNTRY

- 3.4 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid integration of AI to enhance diagnostic accuracy and optimize hematology workflows

- 4.2.1.2 Growing preference for high-parameter and multi-functional testing

- 4.2.1.3 Mounting demand for cost-efficient hematology analyzers

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of advanced hematology analyzers

- 4.2.2.2 Limited accuracy of digital morphology analyzers in detecting rare and complex cell abnormalities

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of AI-enabled tele-hematology and remote diagnostics

- 4.2.3.2 Adoption of precision diagnostics enabling advanced cell profiling, rare cell detection, and early disease identification

- 4.2.4 CHALLENGES

- 4.2.4.1 Complexity in managing and interpreting data generated by next-generation hematology analyzers

- 4.2.4.2 Shortage of laboratory workforce

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 THREAT OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 5.2.3 MACROECONOMIC OUTLOOK FOR EUROPE

- 5.2.4 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 5.2.5 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 5.2.6 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 5.2.7 TRENDS IN GLOBAL IN-VITRO DIAGNOSTICS (IVD) INDUSTRY

- 5.2.8 TRENDS IN GLOBAL POINT-OF-CARE (POC) DIAGNOSTICS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING TREND OF HEMATOLOGY INSTRUMENTS, BY REGION, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE OF HEMATOLOGY ANALYZERS AND REAGENTS, BY PRICE RANGE, 2025

- 5.6 TRADE DATA ANALYSIS

- 5.6.1 IMPORT DATA (HS CODE 902780)

- 5.6.2 EXPORT DATA (HS CODE 902780)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 DETECTION OF ABNORMAL WBC POPULATIONS IN HIGH WBC COUNT CASES USING XN-SERIES AUTOMATED HEMATOLOGY ANALYZER

- 5.10.2 MONITORING AND DETECTION OF ACUTE MYELOBLASTIC LEUKEMIA (AML-M1) USING ADVANCED HEMATOLOGY ANALYZERS

- 5.10.3 DETECTION OF MICROCYTIC ANEMIA WITH THROMBOCYTOSIS THROUGH ADVANCED SCATTERGRAM ANALYSIS

- 5.11 IMPACT OF US TARIFFS - HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 FLOW CYTOMETRY

- 6.1.2 DIGITAL MORPHOLOGY ANALYZERS

- 6.1.3 MICROFLUIDICS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 LABORATORY INFORMATION SYSTEMS

- 6.2.2 CLOUD & REMOTE DIAGNOSTICS

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES FOLLOWED BY COMPANIES IN HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 6.5.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN HEMATOLOGY ANALYZERS AND REAGENTS MARKET

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT AI/GEN AI-INTEGRATED HEMATOLOGY ANALYZERS AND REAGENTS

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY TRENDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS

9 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY PRICE RANGE

- 9.1 INTRODUCTION

- 9.2 LOW-RANGE HEMATOLOGY ANALYZERS

- 9.2.1 LOW OPERATING EXPENSES TO ACCELERATE SEGMENTAL GROWTH

- 9.3 HIGH-RANGE HEMATOLOGY ANALYZERS

- 9.3.1 HIGH ACCURACY AND MULTI-PARAMETER APPROACH TO FUEL SEGMENTAL GROWTH

- 9.4 MID-RANGE HEMATOLOGY ANALYZERS

- 9.4.1 INTEGRATION WITH QUALITY CONTROL SOFTWARE TO SUPPORT SEGMENTAL GROWTH

10 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY USAGE TYPE

- 10.1 INTRODUCTION

- 10.2 STANDALONE ANALYZERS

- 10.2.1 INCREASING DEMAND FOR HIGH-THROUGHPUT AND AUTOMATED LABORATORY WORKFLOWS TO FOSTER SEGMENTAL GROWTH

- 10.3 POINT-OF-CARE ANALYZERS

- 10.3.1 SHIFTING PREFERENCE TOWARD DECENTRALIZED AND RAPID DIAGNOSTICS TO EXPEDITE SEGMENTAL GROWTH

11 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY PRODUCT & SERVICE

- 11.1 INTRODUCTION

- 11.2 HEMATOLOGY PRODUCTS & SERVICES

- 11.2.1 REAGENTS & CONSUMABLES

- 11.2.1.1 Hematology reagents

- 11.2.1.1.1 Growing preference for rental business models to drive market

- 11.2.1.2 Hematology consumables

- 11.2.1.2.1 Requirement for accurate and efficient blood analysis in laboratory workflows to spur demand

- 11.2.1.3 Controls & calibrators

- 11.2.1.3.1 Ability to monitor multiple parameters to boost segmental growth

- 11.2.1.4 Slide stainers & makers

- 11.2.1.4.1 Detailed visualization of cellular morphology to augment segmental growth

- 11.2.1.1 Hematology reagents

- 11.2.2 INSTRUMENTS

- 11.2.2.1 5-part & 6-part fully automated hematology analyzers

- 11.2.2.1.1 Identification and classification of WBCs to drive market

- 11.2.2.2 3-part fully automated hematology analyzers

- 11.2.2.2.1 Low maintenance costs to contribute to segmental growth

- 11.2.2.3 Point-of-care & semi-automated testing hematology analyzers

- 11.2.2.3.1 Shift toward decentralized, rapid, and multi-parameter hematology testing to spur demand

- 11.2.2.1 5-part & 6-part fully automated hematology analyzers

- 11.2.3 SERVICES

- 11.2.3.1 High adoption of diagnostic techniques to boost segmental growth

- 11.2.1 REAGENTS & CONSUMABLES

- 11.3 HEMOSTASIS PRODUCTS & SERVICES

- 11.3.1 HEMOSTASIS REAGENTS & CONSUMABLES

- 11.3.1.1 Expanding use in comprehensive coagulation testing and specialized diagnostics to fuel segmental growth

- 11.3.2 HEMOSTASIS INSTRUMENTS

- 11.3.2.1 High productivity with low complexities to drive market

- 11.3.3 HEMOSTASIS SERVICES

- 11.3.3.1 Advancements in hemostasis diagnostic techniques to support segmental growth

- 11.3.1 HEMOSTASIS REAGENTS & CONSUMABLES

- 11.4 IMMUNOHEMATOLOGY PRODUCTS & SERVICES

- 11.4.1 IMMUNOHEMATOLOGY REAGENTS & CONSUMABLES

- 11.4.1.1 Use to ensure accurate transfusion testing and enhance blood safety to bolster segmental growth

- 11.4.2 IMMUNOHEMATOLOGY INSTRUMENTS

- 11.4.2.1 Growing automation in immunohematology labs to foster segmental growth

- 11.4.3 SERVICES

- 11.4.3.1 Provision of customer-focused care to support segmental growth

- 11.4.1 IMMUNOHEMATOLOGY REAGENTS & CONSUMABLES

12 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 HEMORRHAGIC CONDITIONS

- 12.2.1 INCREASING DEMAND FOR DECENTRALIZED AND FREQUENT MONITORING TO EXPEDITE SEGMENTAL GROWTH

- 12.3 INFECTIOUS DISEASES

- 12.3.1 NEED FOR RAPID SCREENING TO ACCELERATE SEGMENTAL GROWTH

- 12.4 IMMUNE SYSTEM DISORDERS

- 12.4.1 FOCUS ON ADVANCED BLOOD PROFILING TO FACILITATE SEGMENTAL GROWTH

- 12.5 BLOOD CANCER

- 12.5.1 ABILITY TO IDENTIFY ABNORMAL BLOOD CELLS AND MORPHOLOGICAL ABNORMALITIES TO DRIVE MARKET

- 12.6 ANEMIA

- 12.6.1 SHIFT TOWARD ADVANCED RBC PARAMETER ANALYSIS TO BOOST SEGMENTAL GROWTH

- 12.7 OTHER APPLICATIONS

13 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 COMMERCIAL SERVICE PROVIDERS

- 13.2.1 HIGH EMPHASIS ON HIGH-VOLUME ROUTINE TESTING, PREVENTIVE SCREENING, AND ADVANCED DIAGNOSTICS TO DRIVE MARKET

- 13.3 HOSPITAL LABORATORIES

- 13.3.1 RISING NEED FOR REAL-TIME PATIENT DIAGNOSIS AND EMERGENCY TESTING TO EXPEDITE SEGMENTAL GROWTH

- 13.4 GOVERNMENT REFERENCE LABORATORIES

- 13.4.1 INCREASING NEED FOR LARGE-SCALE DISEASE SURVEILLANCE, SCREENING, AND DIAGNOSTIC STANDARDIZATION TO SPUR DEMAND

- 13.5 RESEARCH & ACADEMIC INSTITUTES

- 13.5.1 GROWING FOCUS ON ADVANCED DISEASE PROFILING, BIOMARKER DISCOVERY, AND TRANSLATIONAL RESEARCH TO BOOST SEGMENTAL GROWTH

14 HEMATOLOGY ANALYZERS AND REAGENTS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Rising incidence of anemia and hemophilia to drive market

- 14.2.2 CANADA

- 14.2.2.1 Mounting demand for accurate blood diagnostics to bolster market growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Increasing prevalence of anemia to contribute to market growth

- 14.3.2 FRANCE

- 14.3.2.1 Rising adoption of automated and high-throughput hematology analyzers to support market growth

- 14.3.3 UK

- 14.3.3.1 High incidence of blood-related disorders to expedite market growth

- 14.3.4 ITALY

- 14.3.4.1 Growing acceptance of hematology-based diagnostics to boost market growth

- 14.3.5 SPAIN

- 14.3.5.1 Rising preference for automated and high-throughput hematology systems to augment market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Large target patient population to expedite market growth

- 14.4.2 JAPAN

- 14.4.2.1 Rising cases of influenza to support market growth

- 14.4.3 INDIA

- 14.4.3.1 Government-led procurement initiatives and expanding diagnostic infrastructure to fuel market growth

- 14.4.4 AUSTRALIA

- 14.4.4.1 Increasing prevalence of celiac disease to drive market

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Strong focus on advanced diagnostics and automation to contribute to market growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Increasing burden of anemia and infectious diseases to expedite market growth

- 14.5.2 MEXICO

- 14.5.2.1 Mounting demand for diagnostic testing to accelerate market growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 HIGH DISEASE AWARENESS, IMPROVING HEALTHCARE INFRASTRUCTURE, AND ADVANCED TREATMENT OPTIONS TO DRIVE MARKET

- 14.6.2 GCC COUNTRIES

- 14.6.3 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYERS COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 MARKET RANKING, 2025

- 15.6 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7 PRODUCT COMPARISON

- 15.8 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.8.1 STARS

- 15.8.2 EMERGING LEADERS

- 15.8.3 PERVASIVE PLAYERS

- 15.8.4 PARTICIPANTS

- 15.8.5 COMPETITIVE FOOTPRINT: KEY PLAYERS, 2025

- 15.8.5.1 Company footprint

- 15.8.5.2 Region footprint

- 15.8.5.3 Product & service footprint

- 15.8.5.4 Application footprint

- 15.8.5.5 End user footprint

- 15.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.9.1 PROGRESSIVE COMPANIES

- 15.9.2 RESPONSIVE COMPANIES

- 15.9.3 DYNAMIC COMPANIES

- 15.9.4 STARTING BLOCKS

- 15.9.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.9.5.1 Detailed list of key startups/SMEs

- 15.9.5.2 Competitive benchmarking of key startups/SMEs

- 15.10 COMPETITIVE SCENARIO

- 15.10.1 PRODUCT LAUNCHES AND APPROVALS

- 15.10.2 DEALS

- 15.10.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 SYSMEX CORPORATION

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Expansions

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 ABBOTT

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches and approvals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 DANAHER CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 SIEMENS HEALTHINEERS AG

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches and approvals

- 16.1.4.3.2 Deals

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches and approvals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 DIATRON

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Expansions

- 16.1.7 DREW SCIENTIFIC

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 BIO-RAD LABORATORIES, INC.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches and approvals

- 16.1.9 HORIBA

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches and approvals

- 16.1.10 NIHON KOHDEN CORPORATION

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Expansions

- 16.1.11 EKF DIAGNOSTICS HOLDINGS PLC

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches and approvals

- 16.1.12 BOULE

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches and approvals

- 16.1.12.3.2 Deals

- 16.1.13 F. HOFFMANN-LA ROCHE LTD

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.14 BIOSYSTEMS DIAGNOSTICS

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.1 SYSMEX CORPORATION

- 16.2 OTHER PLAYERS

- 16.2.1 DRUCKER DIAGNOSTICS

- 16.2.2 ACCUREX

- 16.2.3 STRECK

- 16.2.4 NEOMEDICA

- 16.2.5 EVERLIFE CPC

- 16.2.6 MERIL

- 16.2.7 SHENZHEN DYMIND BIOTECHNOLOGY CO., LTD.

- 16.2.8 PZ CORMAY S.A.

- 16.2.9 PIXCELL MEDICAL

- 16.2.10 RAYTO LIFE AND ANALYTICAL SCIENCES CO.,LTD.

- 16.2.11 ANALYTICON BIOTECHNOLOGIES GMBH

17 RESEARCH METHODOLOGY

- 17.1 INTRODUCTION

- 17.2 RESEARCH DATA

- 17.2.1 SECONDARY DATA

- 17.2.1.1 List of key secondary sources

- 17.2.1.2 Key data from secondary sources

- 17.2.2 PRIMARY RESEARCH

- 17.2.2.1 Key data from primary sources

- 17.2.2.2 Primary research objectives

- 17.2.2.3 Key industry insights

- 17.2.2.4 Breakdown of primaries

- 17.2.2.5 List of primary interview participants

- 17.2.1 SECONDARY DATA

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.2 TOP-DOWN APPROACH

- 17.4 GROWTH FORECAST

- 17.5 DATA TRIANGULATION

- 17.6 MARKET SHARE ASSESSMENT

- 17.7 RESEARCH ASSUMPTIONS

- 17.8 RESEARCH LIMITATIONS

- 17.9 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS