|

시장보고서

상품코드

2038241

압력 용기 시장 예측(-2031년) : 유형(저장용 용기, 처리용 용기), 재질(강철, 티타늄, 니켈 합금, 알루미늄, 복합재료, 기타), 내압 등급, 최종사용자 산업, 지역별Pressure Vessels Market by Type (Storage Vessels, Processing Vessels), By Material (Steel, Titanium, Nickel Alloys, Aluminium, Composites, Other Pressure Vessels Material), Pressure Rating, End-User Industry and Region - Global Forecast to 2031 |

||||||

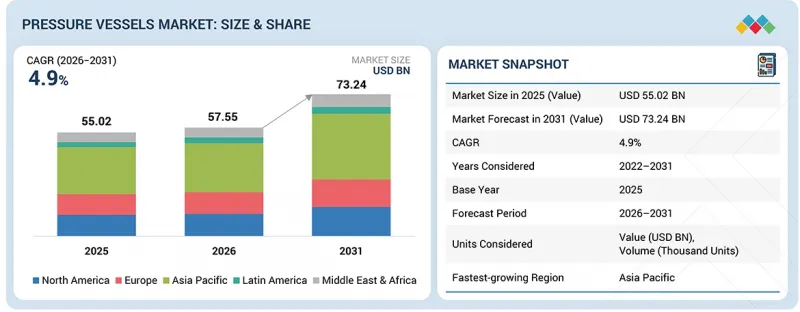

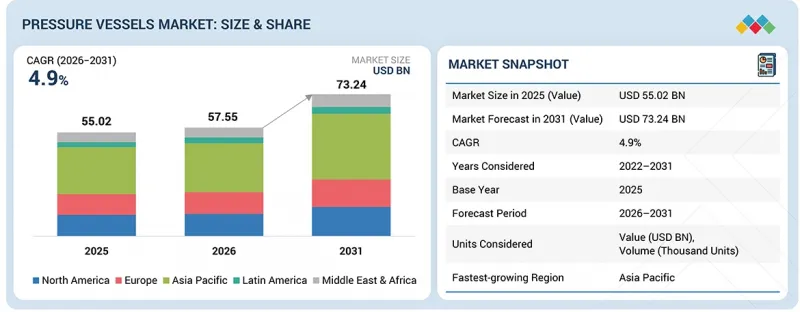

세계의 압력 용기 시장 규모는 2026년 575억 5,000만 달러에서 2031년에는 732억 4,000만 달러로 성장하며, 예측 기간 중 CAGR은 4.9%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) , 수량(유닛) |

| 부문 | 유형, 재질, 내압 등급, 최종사용자 산업, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카 |

세계 화학제품 생산 증가와 에너지 수요 증가가 이 시장의 성장을 주도하고 있습니다.

"유형별로는 저장용기가 2026년 두 번째로 큰 점유율을 차지할 것으로 전망"

저장 용기는 특정 온도와 압력 하에서 액체와 기체를 안전하게 저장하는 데 중요한 역할을 하므로 모든 산업 분야에서 큰 수요가 있습니다. 석유 및 가스, 화학 제조, 발전 등 많은 산업에서 효율적이고 안정적인 운영을 유지하기 위해 저장 용기에 크게 의존하고 있습니다. 신흥 국가에서는 파이프라인, 정유소, 화학공장, 발전소 등 인프라 프로젝트가 빠르게 확대되고 있으며, 저장용기에 대한 수요가 더욱 증가하고 있습니다. 한편, 처리용 용기에는 보일러, 반응기, 분리기, 열교환기, 플래시 드럼 등의 설비가 포함됩니다. 이러한 용기는 온도와 압력을 제어하면서 이루어지는 산업 공정을 지원함으로써 제품 품질 확보와 생산 효율성 향상에 중요한 역할을 하고 있습니다.

"처리용 용기 중에서는 반응기가 예측 기간 중 가장 빠르게 성장할 것으로 전망"

처리용 용기는 다시 보일러, 분리기, 반응기, 기타 압력용기로 분류됩니다. 이 중 반응기는 처리용 용기 중 가장 빠르게 성장하고 있는 분야입니다. 이러한 수요는 혼합, 반응, 분리, 열전달, 상변화 등 제어된 화학 및 산업 공정의 필요성이 증가함에 따라 밀접한 관련이 있습니다. 화학, 제약, 특수소재 등의 산업에서는 효율성, 제품 품질, 공정 제어를 향상시키기 위해 첨단 반응기 시스템에 대한 의존도가 높아지고 있습니다. 동시에 플래시 드럼, 열교환기 등의 장비에 대해서도 특히 증류, 분별, 기화 등의 용도에서 안정적인 수요가 지속되고 있습니다. 이러한 용기는 광범위한 산업 활동을 지원하고 있으며, 화학 공정의 급속한 확장과 반응기 기술 혁신으로 인해 예측 기간 중 반응기 부문의 성장이 더욱 가속화될 것으로 예상됩니다.

"지역별로는 북미가 두 번째로 높은 성장률 보일 전망"

북미는 기술 발전과 인프라 개발에 힘입어 예측 기간 중 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 이 지역은 석유 및 가스, 발전, 화학 등의 산업에서 강력한 존재감을 보이고 있으며, 이들 산업은 모두 안전하고 효율적인 운영을 위해 압력 용기에 크게 의존하고 있습니다. 수소 생산 및 탄소 포집를 포함한 청정 에너지 프로젝트에 대한 급속한 투자도 시장 성장을 더욱 촉진하고 있습니다. 또한 노후화된 산업 인프라의 현대화 및 안전 규제 강화로 인해 기업은 기존 설비를 업데이트하거나 업그레이드해야 하는 상황에 직면해 있습니다. 또한 첨단 제조 및 자동화 기술 도입 확대도 이 지역 전체에서 꾸준한 시장 성장을 지원하고 있습니다.

세계의 압력용기(Pressure Vessel) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 압력 용기 시장 : 유형별

제10장 압력 용기 시장 : 내압 등급별

제11장 압력 용기 시장 : 재질별

제12장 압력 용기 시장 : 최종사용자 산업별

제13장 압력 용기 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.06.01The global pressure vessels market is projected to grow from USD 57.55 billion in 2026 to USD 73.24 billion by 2031, at a CAGR of 4.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion), Volume (Thousand Units) |

| Segments | By Type, Material, Pressure Rating, End-User Industry and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Middle East & Africa |

The rise in chemical production and energy demand worldwide is driving market growth.

"Storage vessels are expected to account for the second-largest share of the pressure vessels market, by type, in 2026."

The pressure vessels market, by type, includes processing vessels and storage vessels. The demand for storage vessels is significant across all industries because these vessels play a major role in storing liquids and gases safely at specific temperatures and pressures. Many industries, such as oil & gas, chemical manufacturing, and power generation, rely heavily on storage vessels to maintain efficient and consistent operations. Emerging economies are driving further demand for storage vessels due to the rapid growth of infrastructure projects such as pipelines, refineries, chemical facilities, and power plants. Processing vessels, on the other hand, include equipment such as boilers, reactors, separators, heat exchangers, and flash drums. These vessels play an important role in meeting manufacturers' demands by completing industrial processes that require maintaining controlled temperature and pressure, thereby ensuring the quality of the final product and efficient production processes.

"Reactors are expected to emerge as the fastest-growing by processing vessels of processing vessels during the forecast period."

By Processing Vessels, the pressure vessels segment is classified into boilers, separators, reactors, and other pressure vessels. Among these, reactors represent the fastest-growing segment within processing vessels. Their demand is closely linked to the growing need for controlled chemical and industrial processes, such as mixing, reaction, separation, heat transfer, and phase change. Industries such as chemicals, pharmaceuticals, and specialty materials are increasingly relying on advanced reactor systems to improve efficiency, product quality, and process control. At the same time, equipment such as flash drums and heat exchangers continues to see steady demand, particularly in applications such as distillation, fractionation, and vaporization. While these vessels support a wide range of industrial operations, the rapid expansion of chemical processing and innovation in reactor technologies is driving stronger growth for the reactor segment during the forecast period.

"North America is expected to be the second-fastest-growing region in the pressure vessels market."

North America is expected to be the second-fastest-growing pressure vessels market during the forecast period, driven by technological advancements and infrastructure development. The region has a strong presence in industries such as oil & gas, power generation, and chemicals, all of which heavily rely on pressure vessels for safe and efficient operations. Rapid investments in clean energy projects, including hydrogen production and carbon capture, are further boosting market growth. Additionally, the modernization of aging industrial infrastructure and the tightening of safety regulations are pushing companies to replace or upgrade existing equipment. The growing adoption of advanced manufacturing and automation technologies is also supporting steady market growth across the region.

In-depth interviews have been conducted with key industry participants, subject-matter experts, C-level executives of major market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3 - 11%

By Designation: C-level Executives - 30%, Directors - 25%, and Others - 45%

By Region: North America - 21%, Europe - 26%, Asia Pacific - 44%, Middle East & Africa - 7%, and South America - 3%

Notes: The tiers of the companies are defined based on their total revenues as of 2025. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million.

Other designations include sales managers, engineers, and regional managers.

Mitsubishi Heavy Industries (Japan), IHI Corporation (Japan), Bharat Heavy Electricals Limited (India) are some of the major players in the pressure vessels market. The study includes an in-depth competitive analysis of these key players, including their company profiles, recent developments, and key market strategies.

Research Coverage:

The report defines, describes, and forecasts the global pressure vessels market, by type, material, pressure rating, end user, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, value-based market estimates, and future trends in the pressure vessels market.

Key Benefits of Buying the Report

- It provides an analysis of key drivers (growth momentum in the chemical manufacturing industry, increasing global electricity demand), restraints (cost-intensive manufacturing and upkeep requirements), opportunities (renrenewable energy expansion, growing focus on nuclear energy deployment), challenges (growing focus on nuclear energy deployment) influencing the growth of the pressure vessels market.

- Market Development: It offers comprehensive information about lucrative markets-the report analyzes the pressure vessels market across varied regions.

- Market Diversification: The report includes exhaustive information about new products and services, untapped geographies, recent developments, and investments in the pressure vessels market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Babcock & Wilcox Enterprises Inc. (US), GE Vernova (US), LARSEN & TOURBO LIMITED (India), Mitsubishi Heavy Industries (Japan), Isgec Hitachi Zosen Ltd. (India), IHI Corporation (Japan), Bharat Heavy Electricals Limited (India), Dongturbo Electric Company Ltd. (China), Samuel, Son & Co. (Canada), Westinghouse Electric Company (US), Halvorsen Company (US), Bosch Industriekessel GmbH (Germany); among others in the pressure vessels market.

- Product Innovation/Development: The pressure vessels market is buzzing with fresh innovations, as companies race to meet demands for better efficiency, top-notch safety, and seamless digital smarts. They are packing vessels with IoT sensors for real-time monitoring of pressure, temperature, and structural health, plus predictive maintenance that cuts downtime, boosts safety, and stretches equipment life. Think hydrogen storage tanks for renewables, rugged designs for extreme industrial conditions, and automation-friendly setups. On top of that, firms are turning to tough, eco-friendly, corrosion-resistant materials, along with modular builds that make upkeep and upgrades a breeze. It is all turning these workhorses into clever, reliable powerhouses across industries such as energy, chemicals, and beyond.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PRESSURE VESSELS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PRESSURE VESSELS MARKET

- 3.2 PRESSURE VESSELS MARKET, BY TYPE AND REGION

- 3.3 PRESSURE VESSELS MARKET SHARE, BY TYPE

- 3.4 PRESSURE VESSELS MARKET SHARE, BY PRESSURE RATING

- 3.5 PRESSURE VESSELS MARKET SHARE, BY MATERIAL

- 3.6 PRESSURE VESSELS MARKET SHARE, BY END-USE INDUSTRY

- 3.7 PRESSURE VESSELS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth momentum in chemical manufacturing industry

- 4.2.1.2 Increasing global electricity demand

- 4.2.2 RESTRAINTS

- 4.2.2.1 Cost-intensive manufacturing and upkeep requirements

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Renewable energy expansion enabling new demand streams for pressure vessels

- 4.2.3.2 Growing focus on nuclear energy deployment

- 4.2.4 CHALLENGES

- 4.2.4.1 Price volatility of raw materials

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL PRESSURE VESSELS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF PRESSURE VESSELS, BY TYPE (2022-2031)

- 5.5.2 AVERAGE SELLING PRICE OF PRESSURE VESSELS, BY REGION (2022-2031)

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8401)

- 5.6.2 EXPORT SCENARIO (HS CODE 8401)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 PRESSURE VESSEL USAGE IN HYDROGEN REFUELING STATION INFRASTRUCTURE

- 5.10.2 INDUSTRIAL PRESSURE VESSEL APPLICATION IN LOW-CARBON HYDROGEN PRODUCTION REACTOR

- 5.10.3 PRESSURE VESSEL FOR HYDROGEN STORAGE INFRASTRUCTURE

- 5.11 IMPACT OF US TARIFF - PRESSURE VESSELS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.4 South America

- 5.11.4.5 Middle East & Africa

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 HYDROGEN STORAGE SYSTEMS

- 6.1.2 CNG STORAGE

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SMART MONITORING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON PRESSURE VESSELS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN PRESSURE VESSELS MARKET

- 6.6.3 CASE STUDIES OF AI/GEN AI IMPLEMENTATION IN PRESSURE VESSELS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI/GEN AI IN PRESSURE VESSELS MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 PRESSURE VESSELS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 STORAGE VESSELS

- 9.2.1 RISING DEMAND FOR SAFELY STORING LIQUIDS AND GASES UNDER CONTROLLED PRESSURE AND TEMPERATURE TO DRIVE ADOPTION

- 9.3 PROCESSING VESSELS

- 9.3.1 BOILERS

- 9.3.1.1 Dependence of developing countries on thermal power plants to produce electricity to drive market

- 9.3.2 REACTORS

- 9.3.2.1 Rising investments in nuclear power generation to drive market

- 9.3.3 SEPARATORS

- 9.3.3.1 Growing oil & gas operations in middle east and Asia Pacific to boost segmental growth

- 9.3.4 OTHER PROCESSING VESSELS

- 9.3.1 BOILERS

10 PRESSURE VESSELS MARKET, BY PRESSURE RATING

- 10.1 INTRODUCTION

- 10.2 0-10 BAR

- 10.2.1 EXPANSION OF FOOD PROCESSING AND PHARMACEUTICAL MANUFACTURING TO DRIVE DEMAND

- 10.3 11-50 BAR

- 10.3.1 GROWING USE IN PROCESS INTENSIFICATION AND ENERGY SYSTEMS TO SUPPORT MARKET GROWTH

- 10.4 51-100 BAR

- 10.4.1 NEED FOR HIGHER EFFICIENCY IN INDUSTRIAL SYSTEMS TO DRIVE ADOPTION

- 10.5 ABOVE 100 BAR

- 10.5.1 GROWING INVESTMENTS IN ENERGY TRANSITION TO DRIVE MARKET

11 PRESSURE VESSELS MARKET, BY MATERIAL

- 11.1 INTRODUCTION

- 11.2 STEEL

- 11.2.1 STRENGTH, VERSATILITY, AND COST EFFICIENCY TO DRIVE ADOPTION

- 11.3 TITANIUM

- 11.3.1 HIGH STRENGTH-TO-WEIGHT RATIO AND SUPERIOR CORROSION RESISTANCE TO SUPPORT MARKET GROWTH

- 11.4 NICKEL ALLOYS

- 11.4.1 EXCELLENT TOUGHNESS AND FLEXIBILITY TO DRIVE MARKET

- 11.5 ALUMINUM

- 11.5.1 LIGHTWEIGHT DESIGN AND HIGH THERMAL CONDUCTIVITY TO DRIVE ADOPTION

- 11.6 COMPOSITES

- 11.6.1 HIGH STRENGTH, LOW WEIGHT, AND SUPERIOR CORROSION RESISTANCE TO PROPEL ADOPTION

- 11.7 OTHER MATERIALS

12 PRESSURE VESSELS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 POWER GENERATION

- 12.2.1 RISING ENERGY DEMAND AND PLANT MODERNIZATION TO DRIVE MARKET GROWTH

- 12.3 OIL & GAS

- 12.3.1 UNCONVENTIONAL RESOURCE DEVELOPMENT AND OFFSHORE EXPANSION TO DRIVE MARKET

- 12.4 FOOD & BEVERAGES

- 12.4.1 FOCUS ON SAFETY, QUALITY, AND EFFICIENT PROCESSING EXPANSION TO DRIVE MARKET

- 12.5 PHARMACEUTICALS

- 12.5.1 EXPANDING PHARMACEUTICAL MANUFACTURING AND EMERGING MARKET DEMAND TO DRIVE ADOPTION

- 12.6 CHEMICALS

- 12.6.1 RISING CHEMICAL DEMAND AND PETROCHEMICAL EXPANSION TO FUEL MARKET GROWTH

- 12.7 OTHER END-USE INDUSTRIES

13 PRESSURE VESSELS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Strong industrial base and energy transition investments to drive market

- 13.2.2 CANADA

- 13.2.2.1 Industrial expansion and clean energy investments to drive market

- 13.2.3 MEXICO

- 13.2.3.1 Expanding industrial activity across oil & gas, chemicals, power generation, and manufacturing sectors to propel market

- 13.2.1 US

- 13.3 ASIA PACIFIC

- 13.3.1 CHINA

- 13.3.1.1 Large-scale industrial capacity, refining expansion, and energy transition to augment market growth

- 13.3.2 INDIA

- 13.3.2.1 Rising industrialization and industrial growth to drive market growth

- 13.3.3 JAPAN

- 13.3.3.1 Process precision, retrofit demand, and hydrogen transition to drive market growth

- 13.3.4 SOUTH KOREA

- 13.3.4.1 Advanced manufacturing demand, hydrogen economy push, and export-oriented engineering to augment market growth

- 13.3.5 MALAYSIA

- 13.3.5.1 LNG infrastructure, downstream processing, and export-oriented energy projects to drive market

- 13.3.6 AUSTRALIA

- 13.3.6.1 Energy export infrastructure, resource processing, and emerging clean energy projects to drive market growth

- 13.3.7 INDONESIA

- 13.3.7.1 Gas utilization, refinery upgrades, and industrial expansion to drive market growth

- 13.3.8 REST OF ASIA PACIFIC

- 13.3.1 CHINA

- 13.4 EUROPE

- 13.4.1 UK

- 13.4.1.1 Rising energy transition and industrial base to accelerate market growth

- 13.4.2 FRANCE

- 13.4.2.1 Nuclear energy dominance, hydrogen transition, and industrial demand to drive market growth

- 13.4.3 GERMANY

- 13.4.3.1 Industrial strength and stringent regulations to drive market growth

- 13.4.4 RUSSIA

- 13.4.4.1 Oil & gas dominance and infrastructure expansion to propel market

- 13.4.5 REST OF EUROPE

- 13.4.1 UK

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Oil & gas expansion, petrochemical investments, and localization initiatives to drive market growth

- 13.5.1.2 SAUDI ARABIA

- 13.5.1.2.1 Oil & gas-led demand and industrial expansion to drive market growth

- 13.5.1.3 UAE

- 13.5.1.3.1 Industrial diversification and energy transition to drive market growth

- 13.5.1.4 Rest of GCC countries

- 13.5.2 ALGERIA

- 13.5.2.1 Gas export infrastructure, refinery modernization, and process industry demand to drive market

- 13.5.3 NIGERIA

- 13.5.3.1 Oil & gas processing, refinery upgrades, and downstream expansion to drive demand

- 13.5.4 SOUTH AFRICA

- 13.5.4.1 Need for infrastructure modernization to propel growth

- 13.5.5 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Industrial expansion, process industry growth, and resource-driven demand to drive market

- 13.6.2 ARGENTINA

- 13.6.2.1 Oil & gas sector expansion to drive demand for pressure vessels in Argentina

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND COMPARISON

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT, KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Pressure rating footprint

- 14.7.5.5 End-use industry footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 BHARAT HEAVY ELECTRICALS LIMITED

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 IHI CORPORATION

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths/Right to win

- 15.1.3.4.2 Strategic choice

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 LARSEN & TOUBRO LIMITED

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.3.2 Expansions

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choice

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 BABCOCK & WILCOX ENTERPRISES, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 GE VERNOVA

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 ISGEC HITACHI ZOSEN LTD.

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.8 DONGTURBO ELECTRIC COMPANY LTD.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.9 SAMUEL, SON & CO.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Expansions

- 15.1.10 WESTINGHOUSE ELECTRIC COMPANY LLC

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 Recent developments

- 15.1.10.4.1 Other developments

- 15.1.11 HALVORSEN COMPANY

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.12 BOSCH INDUSTRIEKESSEL GMBH

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.13 ALAVALAVAL

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Deals

- 15.1.14 GODREJ ENTERPRISES

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.15 KARADANI ENGINEERING PVT. LTD.

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.1 BHARAT HEAVY ELECTRICALS LIMITED

- 15.2 OTHER KEY PLAYERS

- 15.2.1 ALLOY PRODUCTS CORP.

- 15.2.2 KELVION HOLDING GMBH

- 15.2.3 ORNALP UNOZON

- 15.2.4 ZAMIL PROCESS EQUIPMENT COMPANY LIMITED

- 15.2.5 WEIHAI CHEMICAL MACHINERY CO., LTD.

- 15.2.6 MIURA AMERICA CO., LTD.

- 15.2.7 INFINITE COMPOSITES

- 15.2.8 SUN BOILERS PVT. LTD.

- 15.2.9 KAIROS POWER

- 15.2.10 STEELHEAD COMPOSITES, INC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.2 SECONDARY AND PRIMARY RESEARCH

- 16.2.1 SECONDARY DATA

- 16.2.1.1 List of key secondary sources

- 16.2.1.2 Key data from secondary sources

- 16.2.2 PRIMARY DATA

- 16.2.2.1 List of primary interview participants

- 16.2.2.2 Key industry insights

- 16.2.2.3 Breakdown of primaries

- 16.2.2.4 Key data from primary sources

- 16.2.1 SECONDARY DATA

- 16.3 MARKET SIZE ESTIMATION METHODOLOGY

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.3.3 DEMAND-SIDE ANALYSIS

- 16.3.3.1 Demand-side assumptions

- 16.3.3.2 Demand-side calculations

- 16.3.4 SUPPLY-SIDE ANALYSIS

- 16.3.4.1 Supply-side assumptions

- 16.3.4.2 Supply-side calculations

- 16.4 FORECAST

- 16.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ANALYSIS

17 APPENDIX

- 17.1 INSIGHTS FROM INDUSTRY EXPERTS

- 17.2 DISCUSSION GUIDE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS