|

시장보고서

상품코드

2041525

의약품 약물전달 시장 : 투여 경로별, 용도별, 시설 이용별, 지역별 - 세계 예측(-2031년)Pharmaceutical Drug Delivery Market By Administration Route (Oral, Injectable, Topical, Ocular, Nasal, Transmucosal & Implantable, Pulmonary, Transdermal Patch), Application (Cancer, Diabetes, Cardiovascular), Facility of Use - Global Forecast to 2031 |

||||||

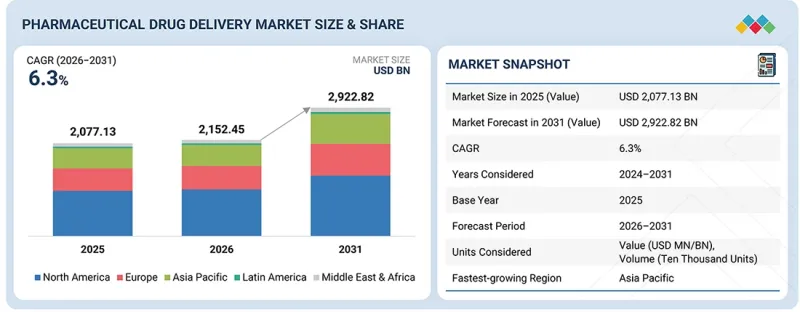

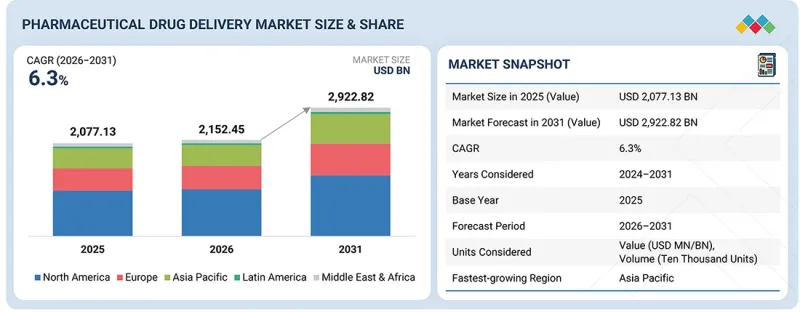

의약품 약물전달 시장 규모는 예측 기간 동안 CAGR 6.3%로 확대되어 2026년 2조 1,524억 5,000만 달러에서 2031년에는 2조 9,228억 2,000만 달러에 달할 것으로 전망됩니다.

전 세계 만성질환의 증가와 바이오의약품, 바이오시밀러, 첨단 치료법의 보급으로 시장은 견조한 속도로 성장하고 있습니다. 환자 친화적인 치료법과 자가 투여 요법으로의 전환으로 선진국과 신흥국에서 새로운 주사제, 흡입제, 경피제, 표적 전달 시스템 등 새로운 주사제, 흡입제, 경피제, 표적 전달 시스템의 채택이 증가하고 있습니다. 고분자 의약품의 추세에 따라 지질 나노입자, 장시간 지속형 디포제제, 서방형 제제, 웨어러블 주사기 등 첨단 전달 매체에 대한 투자가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 투여 경로별, 용도별, 시설 이용별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

한편, 디지털 및 커넥티드 의약품 및 의료기기 기술은 치료의 정확성 향상, 환자의 복약 순응도 및 환자의 원격 모니터링을 촉진하고 있습니다. 시장 성장은 장치 공학, 자동화, 생물학적 제제 안정화 분야의 혁신에 의해 뒷받침되고 있습니다. 그럼에도 불구하고, 업계는 여전히 높은 제품 개발 및 제조 비용, 엄격한 세계 규제 요건, 공급망 및 무균성 관련 복잡성 등의 과제에 직면해 있습니다. 그러나 지속적인 혁신과 홈케어 및 환자 중심 치료로의 큰 전환은 여전히 세계 의약품 약물전달 시장의 강력한 성장을 견인하고 있습니다.

"2025년에는 주사제 전달 부문이 가장 큰 시장 점유율을 차지했습니다."

투여 경로별로 보면 주사제 전달 부문이 전 세계 의약품 약물전달 시장을 독점하고 있습니다. 이는 선진국과 개발도상국의 만성질환 유병률 증가와 더불어 경구 생체 이용률이 낮고 분해 문제로 인해 비경구 투여만 가능한 바이오의약품, 바이오시밀러, 펩타이드, 올리고뉴클레오티드, 세포 및 유전자 치료제가 전 세계적으로 확산되고 있는 추세와 관련이 있습니다. 관련되어 있습니다. 또한, 프리필드 시린지, 오토인젝터, 웨어러블 인젝터, 바늘, 프리젯 인젝터, 피하 급속 주입 시스템, 마이크로/나노 캐리어 플랫폼의 기술 혁신은 약물 투여의 안전성, 편의성, 편리성을 향상시켰으며, 주사제 투여의 주사제 투여의 양상이 달라졌습니다. 이러한 기술적 진보로 인해 병원 밖에서 자가 투약이 크게 증가하여 세계 시장에서 주사제 투여 시스템의 보급이 크게 가속화되었습니다.

"2025년 제제 시장에서 병원 부문이 가장 큰 점유율을 차지했습니다."

2025년 세계 의약품 약물전달 시장에서 병원 부문이 가장 큰 점유율을 차지했습니다. 이 병원은 고도의 인프라와 숙련된 임상 인력을 바탕으로 정확한 투여와 지속적인 모니터링이 필요한 생물학적 제제, 단클론항체, 방사성의약품, 기타 특수 치료제를 관리할 수 있는 능력을 갖추고 있습니다. 병원은 이러한 치료를 할 수 있는 최적의 환경을 제공하고 있습니다. 고분자 의약품의 사용 증가는 수액 펌프, 장시간 지속형 주사제, 나노입자 제제, 디포형 임플란트 등 첨단 병원용 투약 시스템에 대한 수요 확대에 기여하고 있습니다. 이러한 혁신적인 약물전달 기기 및 방법은 약물의 안정성을 유지하고 정확한 투여를 보장하여 치료 효과를 크게 향상시킵니다. 세계 각국의 규제 당국은 병원에서 투여되는 약물전달 플랫폼과 관련하여 안전성, 의료기기, 약물 적합성 및 인적 요소의 성능을 최우선 과제로 삼고 있습니다. 따라서 규정을 충족하기 위해 기업은 설계, 테스트 및 품질 관리를 강화해야 합니다. 병원은 첨단 비경구 요법이나 의료기기를 보조하는 치료를 필요로 하는 경우가 점점 더 많아지고 있기 때문에 전 세계 약물전달 분야에서 여전히 가장 중요한 사용 시설로 남아있습니다.

"2025년, 북미가 의약품 약물전달 시장을 독점했습니다."

2025년 북미가 가장 큰 시장 점유율을 차지했으며, 이는 선진화된 의료 인프라, 바이오의약품 및 전문 의약품의 보급, 활발한 연구개발 활동에 기인하는 것으로 보입니다. 이 지역은 만성질환 유병률이 높고 자가투약에 대한 수요가 높아 자동주사기, 프리필드 시린지, 웨어러블 주사기, 커넥티드 의약품 및 디바이스 플랫폼이 채택되고 있습니다. 이 지역에는 새로운 제형 기술, 고정밀 주사 시스템, 나노입자 기반 플랫폼 및 서방형 메커니즘을 지속적으로 모색하고 있는 대형 제약사 및 제약-의료기기 기업들이 위치하고 있습니다. 규제 프레임워크, 특히 미국 FDA의 규제 프레임워크는 매우 지원적이기 때문에 복합제 및 생물학적 제제 전달 시스템이 북미의 우위를 유지하는 데 도움이 되고 있습니다. 또한, 강력한 바이오테크놀러지 클러스터, 연구기관 및 CDMO도 매우 혁신적인 약물전달 생태계를 구축하는 데 기여하고 있습니다.

이 보고서는 투여 경로, 용도, 사용 시설, 지역별로 의약품 약물전달 시장을 조사하고 있습니다. 또한, 시장 성장에 영향을 미치는 요인(촉진요인, 억제요인, 성장기회, 과제)을 분석하고, 시장 리더들의 경쟁 상황에 대한 상세한 정보를 제공하고 있습니다. 또한, 개별 성장 동향과 관련하여 마이크로 마켓을 분석하고 있습니다. 5개 주요 지역(및 해당 지역 내 국가)에 대한 시장 부문별 수익 예측을 제공합니다.

이 보고서를 구매해야 하는 이유

본 보고서는 기존 기업뿐만 아니라 신규 진입 기업 및 중소기업에게도 시장 동향을 파악하고 시장 점유율을 확대하는 데 도움이 될 것입니다. 이 보고서를 구매한 기업은 시장에서의 입지를 강화하기 위해 다음 전략 중 하나 또는 그 조합을 활용할 수 있습니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인, 제약요인, 기회, 도전과제 분석

- 시장 침투 : 의약품 약물전달 시장의 주요 기업들이 제공하는 제품 포트폴리오에 대한 종합적인 정보

- 제품 개발 및 혁신 : 의약품 약물전달 시장의 미래 동향, R&D 활동 및 신제품 출시에 대한 심층적인 인사이트

- 시장 개발 : 수익성 높은 신흥 지역에 대한 종합적인 정보

- 시장 다각화 : 의약품 약물전달 시장의 신제품, 성장 지역 및 최근 동향에 대한 종합적인 정보

- 경쟁 분석 : 시장 세분화, 성장 전략, 수익 분석 및 주요 시장 기업의 제품에 대한 심층 평가

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 의약품 약물전달 시장(투여 경로별)

제10장 의약품 약물전달(용도별)

제11장 의약품 약물전달 시장(시설 이용별)

제12장 의약품 약물전달 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.01The pharmaceutical drug delivery market is projected to grow from USD 2,152.45 billion in 2026 to USD 2,922.82 billion by 2031, at a CAGR of 6.3% during the forecast period. The market is growing at a healthy pace due to an increase in chronic diseases globally and the use of biologics, biosimilars, and advanced therapies. The shift towards patient-friendly and self-administration therapies is facilitating the adoption of new injectable, inhalation, transdermal, and targeted delivery systems in the developed and emerging economies. The trend of prescribing large-molecule drugs has led to a rise in investments in cutting-edge delivery vehicles such as lipid nanoparticles, long-acting depots, controlled-release formulations, and wearable injectors.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Route of Administration, Application, Facility of Use, Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

Meanwhile, digital and connected drug-device technologies are facilitating greater treatment precision, patient adherence, and remote monitoring of patients. Market growth is enabled by innovations in device engineering, automation, and biologic stabilization. Nevertheless, the industry is still grappling with issues such as high costs of developing and manufacturing products, more stringent global regulatory requirements, and complexities related to the supply chain and sterility. However, continuous innovation and a significant move towards home-based and patient-centric care are still fueling strong growth in the global pharmaceutical drug delivery market.

"Injectable drug delivery segment accounted for the largest market share in 2025"

Based on route of administration, the injectable drug delivery segment dominates the pharmaceutical drug delivery market at a global level. This is linked to the growing incidence of chronic diseases both in developed and developing countries, as well as the worldwide trend of using biologics, biosimilars, peptides, oligonucleotides, and cell & gene therapies that are only parenterally administered due to low oral bioavailability and degradation issues. Moreover, innovations in prefilled syringes, autoinjectors, wearable injectors, needles, free jet injectors, subcutaneous rapid infusion systems, and micro/nanocarrier platforms have changed the injectable drug delivery landscape completely by making drug delivery safer, more comfortable, and easier to use. These technological advances have led to a huge increase in self-administration out of the hospital and have pushed the penetration of injectable drug delivery systems in the global market much quicker.

"Hospitals segment captured the largest share of the market for formulations in 2025"

The hospital segment accounted for the largest share of the global pharmaceutical drug delivery market in 2025. Hospitals are supported by advanced infrastructure, trained clinical staff, and have the capability to manage biologics, monoclonal antibodies, radiopharmaceuticals, and other specialty treatments that require precise dosing and continuous monitoring. They offer the perfect setting for such treatments. An increased usage of large-molecule drugs has contributed to a rise in demand for sophisticated hospital-based delivery systems such as infusion pumps, long-acting injectables, nanoparticle formulations, and depot implants. Such innovative drug delivery devices and methods assist in keeping the drugs stable, ensure accurate administration, and thereby, significantly enhance the effectiveness of therapies. Worldwide regulatory bodies keep safety, device, drug compatibility, and human factor performance at the top of their priorities when it comes to hospital-administered delivery platforms. Therefore, to meet the regulations, the companies have to reinforce design, testing, and quality controls. Hospitals continue to be the most important Facility of Use in the global drug delivery landscape, as they handle more and more cases that need advanced parenteral and device-assisted therapies.

"In 2025, North America dominated the pharmaceutical drug delivery market"

North America held the largest market share in 2025, which can be attributed to an advanced healthcare infrastructure, strong uptake of biologics and specialty medicines, and extensive R&D activity. Autoinjectors, prefilled syringes, wearable injectors, and connected drug, device platforms are adopted as a result of high chronic disease prevalence and a growing demand for self-administration in the region. The area is home to major pharmaceutical and drug, device companies that are constantly looking for new formulation technologies, high-precision injection systems, nanoparticle-based platforms, and controlled-release mechanisms. The regulatory pathways, especially the US FDA's ones, are very supportive, and thus, combination products and biologic delivery systems help to maintain North America's dominant position. Besides that, strong biotech clusters, research institutions, and CDMOs are also helping to create a highly innovative drug delivery ecosystem.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

By End User:

Hospitals (59%), Ambulatory Surgery Centers/Clinics (16%), Home Care Settings (15%), Diagnostic Centers (6%), and Other Facilities of Use (4%)

By Designation:

Physicians (47%), Hospital Directors and Managers (22%), Home-Care & Ambulatory Care Professionals (15%), and Other Designations (16%)

By Region:

North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and Middle East & Africa (15%)

Research Coverage

This report studies the pharmaceutical drug delivery market based on route of administration, application, facility of use, and region. The report also studies factors (drivers, restraints, opportunities, and challenges) affecting market growth and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micro markets with respect to their individual growth trends. It forecasts the revenue of the market segments with respect to five major regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies for strengthening their market presence.

This report provides insights into the following pointers:

- Analysis of Key Drivers, Restraints, Opportunities, Challenges

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the pharmaceutical drug delivery market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the pharmaceutical drug delivery market

- Market Development: Comprehensive information on lucrative emerging regions

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the pharmaceutical drug delivery market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 MAJOR STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PHARMACEUTICAL DRUG DELIVERY MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PHARMACEUTICAL DRUG DELIVERY MARKET OVERVIEW

- 3.2 ASIA PACIFIC: PHARMACEUTICAL DRUG DELIVERY MARKET, BY ROUTE OF ADMINISTRATION & COUNTRY (2025)

- 3.3 PHARMACEUTICAL DRUG DELIVERY MARKET: REGIONAL MIX

- 3.4 PHARMACEUTICAL DRUG DELIVERY MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.5 PHARMACEUTICAL DRUG DELIVERY MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Advancements in drug delivery technologies

- 4.2.1.2 Rising burden of chronic diseases and aging population

- 4.2.1.3 Growing adoption of biologics and biosimilars

- 4.2.1.4 Growing emphasis on patient convenience

- 4.2.1.5 Increasing investments in pharmaceutical R&D

- 4.2.2 RESTRAINTS

- 4.2.2.1 Infections associated with needlestick injuries

- 4.2.2.2 Stringent government regulations

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Geographic expansion into emerging markets

- 4.2.3.2 Integration with digital health & remote monitoring

- 4.2.4 CHALLENGES

- 4.2.4.1 Pricing pressure by governing bodies

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN PHARMACEUTICAL DRUG DELIVERY MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL PHARMACEUTICAL DRUG DELIVERY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF PHARMACEUTICAL DRUG DELIVERY PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.5.1.1 Average selling price trend of injectable drug delivery products, by key player, 2023-2025

- 5.5.1.2 Average selling price trend of oral drug delivery products, by key player, 2023-2025

- 5.5.1.3 Average selling price trend of topical drug delivery products, by key player, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF PHARMACEUTICAL DRUG DELIVERY PRODUCTS, BY REGION, 2023-2025

- 5.5.2.1 Average selling price trend of injectable drug delivery products, by region, 2023-2025

- 5.5.2.2 Average selling price trend of oral drug delivery products, by region, 2023-2025

- 5.5.2.3 Average selling price trend of topical drug delivery products, by region, 2023-2025

- 5.5.2.4 Average selling price trend of pulmonary drug delivery products, by region, 2023-2025

- 5.5.2.5 Average selling price trend of ocular drug delivery products, by region, 2023-2025

- 5.5.2.6 Average selling price trend of nasal drug delivery products, by region, 2023-2025

- 5.5.1 AVERAGE SELLING PRICE TREND OF PHARMACEUTICAL DRUG DELIVERY PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 TRADE DATA FOR HS CODE 3004

- 5.6.1.1 Import data for HS Code 3004

- 5.6.1.2 Export data for HS Code 3004

- 5.6.2 TRADE DATA FOR HS CODE 9018

- 5.6.2.1 Import data for HS Code 9018

- 5.6.2.2 Export data for HS Code 9018

- 5.6.1 TRADE DATA FOR HS CODE 3004

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 REIMBURSEMENT ANALYSIS

- 5.11 PIPELINE ANALYSIS

- 5.12 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 5.12.1 MEDTRONIC - INSULIN PUMP DRUG DELIVERY SYSTEM

- 5.12.2 YPSOMED - SMARTPILOT CONNECTED DRUG DELIVERY

- 5.12.3 ENABLE INJECTIONS - ENFUSE CLINICAL PERFORMANCE

- 5.13 IMPACT OF US TARIFFS-PHARMACEUTICAL DRUG DELIVERY MARKET

- 5.13.1 INTRODUCTION

- 5.13.2 KEY TARIFF RATES

- 5.13.3 PRICE IMPACT ANALYSIS

- 5.13.4 IMPACT ON COUNTRIES/REGIONS

- 5.13.5 IMPACT ON END-USE INDUSTRIES

- 5.13.5.1 Impact on end-use industries: formulations

- 5.13.5.1.1 Hospitals

- 5.13.5.1.2 Ambulatory surgical centers/clinics

- 5.13.5.1.3 Home care settings

- 5.13.5.2 Impact on end-use industries: devices

- 5.13.5.2.1 Pharmaceutical companies

- 5.13.5.2.2 Biotechnology companies

- 5.13.5.2.3 Contract development and manufacturing organizations (CDMOs) & contract research organizations (CROs)

- 5.13.5.1 Impact on end-use industries: formulations

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Nanotechnology-based drug delivery

- 6.1.1.2 Smart/connected drug delivery devices

- 6.1.1.3 Needle-free injection systems and microneedle patches

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 3D printed & personalized drug delivery

- 6.1.2.2 AI/ML in drug delivery & formulation

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Smart monitoring, IoT, and data-driven control

- 6.1.3.2 Cell & gene delivery vectors

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 NEAR-TERM (2025-2027)

- 6.2.2 MID-TERM (2028-2030)

- 6.2.3 LONG-TERM (2030+)

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR PHARMACEUTICAL DRUG DELIVERY MARKET

- 6.3.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 PATIENT-CENTRIC DRUG DELIVERY SYSTEMS

- 6.4.2 MINIMALLY INVASIVE AND SELF-ADMINISTERED DELIVERY

- 6.4.3 LONG-ACTING AND BIOLOGIC DRUG DELIVERY SYSTEMS

- 6.4.4 DIGITAL AND AI-ENABLED DRUG DELIVERY

- 6.5 IMPACT OF AI/GENERATIVE AI ON PHARMACEUTICAL DRUG DELIVERY MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 MARKET POTENTIAL IN PHARMACEUTICAL DRUG DELIVERY ECOSYSTEM

- 6.5.3 AI USE CASES

- 6.5.4 KEY COMPANIES IMPLEMENTING AI IN PHARMACEUTICAL DRUG DELIVERY MARKET

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 ENERGY-EFFICIENT MANUFACTURING & CARBON REDUCTION IN PHARMACEUTICAL DRUG DELIVERY

- 7.3 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS (DEVICES)

- 8.1.2 KEY STAKEHOLDERS IN BUYING PROCESS (FORMULATIONS)

- 8.1.3 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 PHARMACEUTICAL DRUG DELIVERY MARKET, BY ROUTE OF ADMINISTRATION

- 9.1 INTRODUCTION

- 9.2 INJECTABLE DRUG DELIVERY

- 9.2.1 DEVICES

- 9.2.1.1 Conventional injection devices

- 9.2.1.1.1 Rising incidence of chronic diseases and low cost of manufacturing to drive the market

- 9.2.1.1.2 Global Volume Analysis of Conventional Injection Devices, 2024-2031(Ten Thousand Units)

- 9.2.1.1.3 By material

- 9.2.1.1.3.1 Glass

- 9.2.1.1.3.2 Plastic

- 9.2.1.1.4 By usability

- 9.2.1.1.4.1 Reusable

- 9.2.1.1.4.2 Disposable

- 9.2.1.1.5 By type

- 9.2.1.1.5.1 Fillable syringes

- 9.2.1.1.6 Prefilled syringes

- 9.2.1.2 Self-injection devices

- 9.2.1.2.1 Global Volume Analysis of Self-Injection Devices, 2024-2031(Ten Thousand Units)

- 9.2.1.2.2 Needle-free injectors

- 9.2.1.2.3 Autoinjectors

- 9.2.1.2.4 Pen injectors

- 9.2.1.2.5 Wearable injectors

- 9.2.1.3 Other injectable devices

- 9.2.1.1 Conventional injection devices

- 9.2.1 DEVICES

- 9.3 FORMULATIONS

- 9.3.1 BY TYPE

- 9.3.1.1 Conventional drug delivery formulations

- 9.3.1.2 Novel drug delivery formulations

- 9.3.1.3 long-acting injectable formulations

- 9.3.2 BY FORMULATION PACKAGING

- 9.3.2.1 Ampoules

- 9.3.2.1.1 Helps maintain the stability of drugs, thereby enhancing efficacy

- 9.3.2.2 Vials

- 9.3.2.2.1 Ability to store drug formulations for extensive periods

- 9.3.2.3 Cartridges

- 9.3.2.3.1 Offers higher dose accuracy and patient convenience

- 9.3.2.4 Bottles

- 9.3.2.4.1 Easy storage of solutions and emulsions drives demand

- 9.3.2.1 Ampoules

- 9.3.1 BY TYPE

- 9.4 ORAL DRUG DELIVERY

- 9.4.1 SOLID ORAL DRUGS

- 9.4.1.1 Tablets

- 9.4.1.1.1 Development of mini-tablets is a key trend in this market segment

- 9.4.1.2 Capsules

- 9.4.1.2.1 Easy absorption of drugs and decreased irritation in GI tract drive use of capsules

- 9.4.1.3 Powders

- 9.4.1.3.1 Powders are taken by patients who are unable to swallow oral dosage forms

- 9.4.1.4 Granules

- 9.4.1.4.1 Increasing adoption of modified-release and pediatric-friendly formulations driving granules market growth

- 9.4.1.5 Lozenges

- 9.4.1.5.1 Prolonged drug release and localized action enhancing adoption of lozenges

- 9.4.1.1 Tablets

- 9.4.2 LIQUID ORAL DRUGS

- 9.4.2.1 Syrups

- 9.4.2.1.1 Easy administration to patients with swallowing difficulties

- 9.4.2.2 Solutions

- 9.4.2.2.1 Geriatric and pediatric patients generally prefer solutions

- 9.4.2.3 Emulsions

- 9.4.2.3.1 Emulsions offer enhanced solubility and stability with ease of administration

- 9.4.2.4 Suspensions

- 9.4.2.4.1 Increasing demand for pediatric and geriatric-friendly formulations is driving the oral suspension market growth

- 9.4.2.5 Elixirs

- 9.4.2.5.1 Elixirs are a preferred choice for the pediatric population

- 9.4.2.1 Syrups

- 9.4.3 SEMI-SOLID ORAL DRUGS

- 9.4.3.1 Gels

- 9.4.3.1.1 Gels are used for controlled drug release

- 9.4.3.2 Pastes

- 9.4.3.2.1 Microemulsions offer protection against oxidation and enzymatic hydrolysis

- 9.4.3.1 Gels

- 9.4.1 SOLID ORAL DRUGS

- 9.5 TOPICAL DRUG DELIVERY

- 9.5.1 SEMI-SOLID FORMULATIONS

- 9.5.1.1 Ointments

- 9.5.1.1.1 Ointments are widely used in analgesic indications

- 9.5.1.2 Creams

- 9.5.1.2.1 Creams are either water-in-oil or oil-in-water emulsions

- 9.5.1.3 Lotions

- 9.5.1.3.1 Easy administration of lotions to drive demand among end users

- 9.5.1.4 Gels

- 9.5.1.4.1 Faster drug release and greater patient acceptability to drive the market for topical gels

- 9.5.1.5 Pastes

- 9.5.1.5.1 Topical pastes are widely used for the treatment and prevention of skin irritation

- 9.5.1.1 Ointments

- 9.5.2 LIQUID FORMULATIONS

- 9.5.2.1 Suspensions

- 9.5.2.1.1 Higher rate of bioavailability and controlled onset of action to drive market

- 9.5.2.2 Emulsions

- 9.5.2.2.1 Improved spreadability, stability, and controlled release of active ingredients

- 9.5.2.3 Solutions

- 9.5.2.3.1 Uniform & rapid drug delivery to boost demand

- 9.5.2.1 Suspensions

- 9.5.3 SOLID FORMULATIONS

- 9.5.3.1 Powders

- 9.5.3.1.1 Powders have a very fine particle size that covers a large surface area per unit weight

- 9.5.3.2 Suppositories

- 9.5.3.2.1 Suppositories require a suitable base to ensure the compatibility and stability of the drug

- 9.5.3.1 Powders

- 9.5.4 FILMS

- 9.5.4.1 Next-generation advancements to boost demand

- 9.5.5 TRANSDERMAL FORMULATIONS

- 9.5.5.1 Transdermal patches

- 9.5.5.1.1 Transdermal patches prevent premature metabolization of drugs through the liver

- 9.5.5.1 Transdermal patches

- 9.5.6 TRANSDERMAL GELS

- 9.5.6.1 Rapid release of drugs to fuel uptake

- 9.5.7 TRANSDERMAL SPRAYS

- 9.5.7.1 Targeted approach to boost demand

- 9.5.1 SEMI-SOLID FORMULATIONS

- 9.6 OCULAR DRUG DELIVERY

- 9.6.1 LIQUID FORMULATIONS

- 9.6.1.1 Eye drops

- 9.6.1.1.1 Rising prevalence of cataracts and other eye diseases to drive the market growth

- 9.6.1.2 Liquid sprays

- 9.6.1.2.1 Liquid sprays to help in overcoming drawbacks associated with traditional eye drops

- 9.6.1.1 Eye drops

- 9.6.2 SEMI-SOLID FORMULATIONS

- 9.6.2.1 Gels

- 9.6.2.1.1 High viscosity of drugs, prolonged drug release, and ease of drug administration contribute to market growth

- 9.6.2.2 Eye ointments

- 9.6.2.2.1 Eye ointments are safe to use and help in improving ocular contact time with the drug

- 9.6.2.1 Gels

- 9.6.3 OCULAR DEVICES

- 9.6.3.1 Drug-coated contact lenses

- 9.6.3.1.1 Better eyesight offered by lenses and high compliance to drive the market for drug-coated contact lenses

- 9.6.3.2 Ocular inserts

- 9.6.3.2.1 Ocular inserts to help in the sustained release of drugs in the eye

- 9.6.3.1 Drug-coated contact lenses

- 9.6.1 LIQUID FORMULATIONS

- 9.7 PULMONARY DRUG DELIVERY

- 9.7.1 PULMONARY DRUG DELIVERY DEVICE

- 9.7.1.1 Metered-dose Inhalers

- 9.7.1.2 Metered-dose inhalers overcome the problem of poor coordination between inhaler actuation and patient breath

- 9.7.1.2.1 Global Volume Analysis of Metered Dose Inhalers, By Region, 2024-2031 (Ten thousand units)

- 9.7.1.3 Dry Powder Inhalers

- 9.7.1.3.1 Dry powder inhaler formulations are chemically more stable than their counterparts

- 9.7.1.3.2 Global Volume Analysis of Dry Powder Inhalers, By Region, 2024-2031 (Ten thousand units)

- 9.7.1.4 Nebulizers

- 9.7.1.4.1 Global Volume Analysis of Nebulizers, By Region, 2024-2031 (Ten thousand units)

- 9.7.1.4.2 Jet nebulizers

- 9.7.1.4.2.1 Jet nebulizers account for the largest share of the nebulizers market

- 9.7.1.4.3 Ultrasonic nebulizers

- 9.7.1.4.3.1 Ultrasonic nebulizers are easy to use and comfortable to handle

- 9.7.1.4.4 Soft mist nebulizers

- 9.7.1.4.4.1 Soft mist nebulizers are preferred for the treatment of severe COPD

- 9.7.2 PULMONARY DRUG DELIVERY FORMULATION

- 9.7.2.1 Suspension Aerosol

- 9.7.2.2 Suspension Aerosols Enable Delivery of Insoluble Drug Formulations

- 9.7.2.3 Solution Aerosol

- 9.7.2.3.1 Solution Aerosols Support Uniform Drug Distribution and Formulation Flexibility

- 9.7.3 DRY POWDER FORMULATIONS

- 9.7.1 PULMONARY DRUG DELIVERY DEVICE

- 9.8 NASAL DRUG DELIVERY

- 9.8.1 NASAL DROPS & LIQUIDS

- 9.8.1.1 Nasal drops are considered more efficient than nasal sprays

- 9.8.2 NASAL SPRAYS

- 9.8.2.1 Nasal sprays to help in relieving nasal congestion, runny nose, itchy nose, and sneezing

- 9.8.3 NASAL POWDERS

- 9.8.3.1 Absence of preservatives and superior stability of formulations are some advantages associated with nasal powders

- 9.8.1 NASAL DROPS & LIQUIDS

- 9.9 TRANSMUCOSAL DRUG DELIVERY

- 9.9.1 ORAL FORMULATIONS

- 9.9.1.1 Buccal drug delivery

- 9.9.1.1.1 Buccal drug delivery system is suitable for local and systemic therapies

- 9.9.1.2 Sublingual drug delivery

- 9.9.1.2.1 Higher rate of drug absorption compared to oral route drives adoption

- 9.9.1.1 Buccal drug delivery

- 9.9.2 OTHER TRANSMUCOSAL DRUG DELIVERY TECHNOLOGIES

- 9.9.2.1 Rectal transmucosal drug delivery

- 9.9.2.1.1 Enhanced bioavailability and bypassing first-pass metabolism

- 9.9.2.2 Vaginal transmucosal drug delivery

- 9.9.2.2.1 Higher permeability and direct access to target systems drive adoption

- 9.9.2.1 Rectal transmucosal drug delivery

- 9.9.1 ORAL FORMULATIONS

- 9.10 IMPLANTABLE DRUG DELIVERY

- 9.10.1 ACTIVE IMPLANTABLE DRUG DELIVERY

- 9.10.1.1 Active implantable devices are used for diagnostic monitoring, body fluid transportation, and ionizing radiation

- 9.10.2 PASSIVE IMPLANTABLE DRUG DELIVERY

- 9.10.2.1 Passive implantable drug delivery systems offer a means to achieve targeted drug delivery

- 9.10.1 ACTIVE IMPLANTABLE DRUG DELIVERY

- 9.11 OTIC DRUG DELIVERY

- 9.11.1 EAR DROPS

- 9.11.1.1 Increasing prevalence of ear infections and demand for localized treatment are driving ear drops segment growth

- 9.11.2 OTIC SPRAYS

- 9.11.2.1 Growing demand for uniform drug distribution and improved patient convenience driving adoption

- 9.11.1 EAR DROPS

10 PHARMACEUTICAL DRUG DELIVERY, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 INJECTABLE DRUG DELIVERY

- 10.2.1 METABOLIC DISORDERS (DIABETES, OBESITY)

- 10.2.1.1 Rising burden of diabetes and obesity driving strong adoption of injectable drug delivery

- 10.2.2 CANCER

- 10.2.2.1 Rising prevalence of cancer and growing availability of therapeutics to drive market

- 10.2.3 IMMUNOLOGICAL & AUTOIMMUNE DISEASES

- 10.2.3.1 Increased focus on early-stage diagnosis and treatment to propel segment growth

- 10.2.4 INFECTIOUS DISEASES

- 10.2.4.1 Increasing use of liposomes to aid segment growth

- 10.2.5 OTHER INJECTABLE DRUG DELIVERY APPLICATIONS

- 10.2.1 METABOLIC DISORDERS (DIABETES, OBESITY)

- 10.3 ORAL DRUG DELIVERY

- 10.3.1 CARDIOVASCULAR DISEASES

- 10.3.1.1 High prevalence of CVDs and widespread use of oral therapies drive market

- 10.3.2 METABOLIC DISORDERS (DIABETES, OBESITY)

- 10.3.2.1 Growing preference for self-injection devices over traditional syringes to augment market growth

- 10.3.3 CNS DISORDERS

- 10.3.3.1 Chronic nature of CNS disorders and long-term therapy needs driving oral drug delivery adoption

- 10.3.4 INFECTIOUS DISEASES

- 10.3.4.1 High global infection burden and outpatient treatment trends driving oral drug delivery adoption

- 10.3.5 ONCOLOGY (ORAL THERAPIES)

- 10.3.5.1 Shift toward targeted therapies and at-home treatment driving oral drug delivery in oncology

- 10.3.6 OTHER ORAL DRUG DELIVERY APPLICATIONS

- 10.3.1 CARDIOVASCULAR DISEASES

- 10.4 TOPICAL DRUG DELIVERY

- 10.4.1 DERMATOLOGICAL DISORDERS

- 10.4.1.1 High prevalence of skin disorders driving strong demand for topical drug delivery

- 10.4.2 PAIN MANAGEMENT

- 10.4.2.1 Localized relief and reduced systemic side-effects driving topical drug delivery in pain management

- 10.4.3 WOUND CARE

- 10.4.3.1 Rising incidence of chronic wounds and surgical procedures driving topical drug delivery in wound care

- 10.4.1 DERMATOLOGICAL DISORDERS

- 10.5 OCULAR DRUG DELIVERY

- 10.5.1 RETINAL DISORDERS

- 10.5.1.1 Rising prevalence of retinal diseases and biologics adoption driving growth in the retinal disorders segment

- 10.5.2 GLAUCOMA

- 10.5.2.1 High prevalence and lifelong therapy requirements driving ocular drug delivery in glaucoma

- 10.5.3 EYE INFECTIOUS DISEASES

- 10.5.3.1 High incidence of ocular infections and need for rapid localized therapy driving eye infectious diseases segment

- 10.5.4 OTHER OCULAR DRUG DELIVERY APPLICATIONS

- 10.5.1 RETINAL DISORDERS

- 10.6 PULMONARY DRUG DELIVERY

- 10.6.1 ASTHMA

- 10.6.1.1 High global asthma prevalence and lifelong inhalation therapy driving pulmonary drug delivery demand

- 10.6.2 CHRONIC OBSTRUCTIVE PULMONARY DISEASE (COPD)

- 10.6.2.1 Chronic disease burden and high reliance on inhalation therapies driving pulmonary drug delivery in COPD

- 10.6.3 PULMONARY INFECTIONS

- 10.6.3.1 High burden of respiratory infections and need for rapid drug action driving pulmonary drug delivery in pulmonary infections

- 10.6.4 OTHER PULMONARY DRUG DELIVERY APPLICATIONS

- 10.6.1 ASTHMA

- 10.7 NASAL DRUG DELIVERY

- 10.7.1 ALLERGIC RHINITIS

- 10.7.1.1 High prevalence of allergic conditions driving nasal drug delivery in allergic rhinitis

- 10.7.2 SINUSITIS

- 10.7.2.1 High prevalence of sinus infections and need for targeted therapy driving nasal drug delivery in sinusitis

- 10.7.3 OTHER NASAL DRUG DELIVERY APPLICATIONS

- 10.7.1 ALLERGIC RHINITIS

- 10.8 TRANSMUCOSAL DRUG DELIVERY

- 10.8.1 PAIN MANAGEMENT

- 10.8.1.1 Rapid onset and improved patient compliance driving transmucosal drug delivery in pain management

- 10.8.2 HORMONE THERAPY

- 10.8.2.1 Need for controlled hormone delivery and long-term therapy driving transmucosal drug delivery in hormonal therapy

- 10.8.3 INFECTIOUS DISEASES

- 10.8.3.1 Targeted local therapy and improved patient compliance driving transmucosal drug delivery in infectious diseases

- 10.8.4 OTHER TRANSMUCOSAL DRUG DELIVERY APPLICATIONS

- 10.8.1 PAIN MANAGEMENT

- 10.9 IMPLANTABLE DRUG DELIVERY

- 10.9.1 HORMONAL THERAPY/CONTRACEPTION

- 10.9.1.1 Long-acting reversible contraceptives and sustained hormone delivery driving market

- 10.9.2 CANCER

- 10.9.2.1 Targeted therapy and sustained drug release driving implantable drug delivery in cancer

- 10.9.3 OTHER IMPLANTABLE DRUG DELIVERY APPLICATIONS

- 10.9.1 HORMONAL THERAPY/CONTRACEPTION

- 10.10 OTIC DRUG DELIVERY

- 10.10.1 EAR INFECTIONS

- 10.10.1.1 High incidence of otitis and pediatric burden driving otic drug delivery in ear infections

- 10.10.2 CERUMEN REMOVAL

- 10.10.2.1 Growing demand for ear hygiene and non-invasive treatments driving otic drug delivery in cerumen removal

- 10.10.3 OTHER OTIC DRUG DELIVERY APPLICATIONS

- 10.10.1 EAR INFECTIONS

11 PHARMACEUTICAL DRUG DELIVERY MARKET, BY FACILITY OF USE

- 11.1 INTRODUCTION

- 11.2 FORMULATIONS, BY FACILITY OF USE

- 11.2.1 HOSPITALS

- 11.2.1.1 Increased hospital demand for complex drug delivery boosts market uptake

- 11.2.2 HOME CARE SETTINGS

- 11.2.2.1 Rising preference for self-administration of medicine to drive market

- 11.2.3 AMBULATORY SURGERY CENTERS/CLINICS

- 11.2.3.1 Shift toward cost-effective outpatient care driving adoption of drug delivery systems

- 11.2.4 DIAGNOSTIC CENTERS

- 11.2.4.1 Rising prevalence of chronic diseases to support market growth

- 11.2.5 LONG-TERM CARE SETTINGS

- 11.2.5.1 Growing elderly population and chronic disease burden to drive market

- 11.2.6 OTHER FACILITIES OF USE

- 11.2.1 HOSPITALS

- 11.3 DEVICES, BY FACILITY OF USE

- 11.3.1 PHARMACEUTICAL COMPANIES

- 11.3.1.1 Increasing focus on advanced drug delivery systems driving market growth

- 11.3.2 BIOTECHNOLOGY COMPANIES

- 11.3.2.1 Enabling complex biologics delivery and decentralized care

- 11.3.3 CONTRACT RESEARCH ORGANIZATIONS (CROS) & CONTRACT DEVELOPMENT AND MANUFACTURING ORGANIZATIONS (CDMOS)

- 11.3.3.1 Fueling innovation through cost-effective and scalable manufacturing solutions

- 11.3.1 PHARMACEUTICAL COMPANIES

12 PHARMACEUTICAL DRUG DELIVERY MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 12.2.2 NORTH AMERICA: VOLUME ANALYSIS, BY PHARMACEUTICAL DRUG DELIVERY DEVICES, 2024-2031

- 12.2.3 US

- 12.2.3.1 US to dominate North American pharmaceutical drug delivery market

- 12.2.4 CANADA

- 12.2.4.1 Government support for research and the prevalence of chronic diseases to drive the market in Canada

- 12.3 EUROPE

- 12.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 12.3.2 EUROPE: VOLUME ANALYSIS, BY PHARMACEUTICAL DRUG DELIVERY DEVICES, 2024-2031

- 12.3.3 GERMANY

- 12.3.3.1 Growing focus of pharmaceutical companies on the development of various drug delivery products to drive market

- 12.3.4 UK

- 12.3.4.1 NHS support and growing access to cost-effective pen needles to drive the market

- 12.3.5 FRANCE

- 12.3.5.1 Presence of leading pharmaceutical companies, along with the increasing prevalence of chronic diseases, to drive market growth in France

- 12.3.6 ITALY

- 12.3.6.1 Increasing focus on clinical research and growing popularity of branded drugs to drive demand for pharmaceutical drug manufacturing

- 12.3.7 DENMARK

- 12.3.7.1 Strong R&D ecosystem, biologics innovation, and export-driven pharmaceutical manufacturing to drive demand for pharmaceutical drug delivery

- 12.3.8 SWEDEN

- 12.3.8.1 Strong life sciences ecosystem, biologics innovation, and government-backed healthcare system to drive demand for pharmaceutical drug delivery

- 12.3.9 SPAIN

- 12.3.9.1 Increase in biologics production to support market growth

- 12.3.10 NETHERLANDS

- 12.3.10.1 Enhancing patient care through innovation and collaboration to drive market growth

- 12.3.11 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 ASIA PACIFIC: VOLUME ANALYSIS, BY PHARMACEUTICAL DRUG DELIVERY DEVICES, 2024-2031

- 12.4.3 CHINA

- 12.4.3.1 A high diabetic population and rising prevalence of chronic diseases contribute to China's large demand

- 12.4.4 JAPAN

- 12.4.4.1 Favorable government initiatives and increased geriatric population to drive market growth in Japan

- 12.4.5 INDIA

- 12.4.5.1 Growing generic demand and rising government initiatives to drive market

- 12.4.6 AUSTRALIA

- 12.4.6.1 Rising investment and a favorable tax environment to support growth

- 12.4.7 SOUTH KOREA

- 12.4.7.1 Strong government support and investments in healthcare & biopharmaceuticals to propel growth

- 12.4.8 NEW ZEALAND

- 12.4.8.1 Strong public healthcare system, rising biologics adoption, and focus on advanced therapies to drive demand

- 12.4.9 THAILAND

- 12.4.9.1 Regulatory reforms and healthcare initiatives to fuel market growth

- 12.4.10 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 FAVORABLE COST STRUCTURE AND GOVERNMENT INVESTMENTS TO DRIVE PHARMACEUTICAL PRODUCTION IN LATAM

- 12.5.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 12.5.3 LATIN AMERICA: VOLUME ANALYSIS, BY PHARMACEUTICAL DRUG DELIVERY DEVICES, 2024-2031

- 12.5.4 BRAZIL

- 12.5.4.1 Brazil attracting multinational pharmaceutical companies

- 12.5.5 MEXICO

- 12.5.5.1 Growth and diversification in Mexico's pharmaceutical exports

- 12.5.6 ARGENTINA

- 12.5.6.1 Expanding domestic pharmaceutical production, increasing chronic disease burden, and growing biologics adoption to drive demand

- 12.5.7 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 12.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY PHARMACEUTICAL DRUG DELIVERY DEVICES, 2024-2031

- 12.6.3 GCC COUNTRIES

- 12.6.3.1 Kingdom of Saudi Arabia (KSA)

- 12.6.3.1.1 Healthcare reforms and global partnerships fuel pharmaceutical market growth

- 12.6.3.2 United Arab Emirates (UAE)

- 12.6.3.2.1 Government supports and growing local manufacturing to drive market growth

- 12.6.3.3 Rest of GCC Countries

- 12.6.3.1 Kingdom of Saudi Arabia (KSA)

- 12.6.4 REST OF MIDDLE EAST & AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2023-2025

- 13.3.1 PHARMACEUTICAL DRUG DELIVERY DEVICE MANUFACTURERS

- 13.3.2 PHARMACEUTICAL DRUG DELIVERY FORMULATION MANUFACTURERS

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 GLOBAL INJECTABLE DRUG DELIVERY MANUFACTURERS

- 13.4.1.1 Global Injectable Drug Delivery Device Manufacturers

- 13.4.1.2 GLOBAL INJECTABLE DRUG DELIVERY FORMULATION MANUFACTURERS

- 13.4.1.2.1 US Injectable Drug Delivery Formulation Manufacturers

- 13.4.1.3 Europe Injectable drug delivery formulation manufacturers

- 13.4.2 GLOBAL ORAL DRUG DELIVERY MANUFACTURERS

- 13.4.2.1 US oral drug delivery formulation manufacturers

- 13.4.2.2 Europe oral drug delivery manufacturers

- 13.4.3 GLOBAL TOPICAL DRUG DELIVERY MANUFACTURERS

- 13.4.3.1 US Topical Drug Delivery Formulation Manufacturers

- 13.4.3.2 Europe Topical Drug Delivery Manufacturers

- 13.4.1 GLOBAL INJECTABLE DRUG DELIVERY MANUFACTURERS

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 R&D EXPENDITURE OF KEY PLAYERS

- 13.7 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7.1 COMPANY VALUATION

- 13.7.2 FINANCIAL METRICS

- 13.8 COMPANY EVALUATION MATRIX: PHARMACEUTICAL DRUG DELIVERY DEVICE MANUFACTURERS, 2025

- 13.8.1 STARS

- 13.8.2 EMERGING LEADERS

- 13.8.3 PERVASIVE PLAYERS

- 13.8.4 PARTICIPANTS

- 13.8.5 COMPANY FOOTPRINT: PHARMACEUTICAL DRUG DELIVERY DEVICE MANUFACTURERS, 2025

- 13.8.5.1 Company footprint

- 13.8.5.2 Region footprint

- 13.8.5.3 Product type footprint

- 13.8.5.4 Usability footprint

- 13.9 COMPANY EVALUATION MATRIX: PHARMACEUTICAL DRUG DELIVERY FORMULATION MANUFACTURERS, 2025

- 13.9.1 STARS

- 13.9.2 EMERGING LEADERS

- 13.9.3 PERVASIVE PLAYERS

- 13.9.4 PARTICIPANTS

- 13.9.5 COMPANY FOOTPRINT: PHARMACEUTICAL DRUG DELIVERY FORMULATION MANUFACTURERS, 2025

- 13.9.5.1 Company footprint

- 13.9.5.2 Region footprint

- 13.9.5.3 Route of administration footprint

- 13.9.5.4 Therapeutic application footprint

- 13.10 COMPANY EVALUATION MATRIX: PHARMACEUTICAL DRUG DELIVERY FORMULATION STARTUPS/SMES, 2025

- 13.10.1 PROGRESSIVE COMPANIES

- 13.10.2 DYNAMIC COMPANIES

- 13.10.3 STARTING BLOCKS

- 13.10.4 RESPONSIVE COMPANIES

- 13.10.5 COMPETITIVE BENCHMARKING: PHARMACEUTICAL DRUG DELIVERY FORMULATION STARTUPS/SMES, 2025

- 13.10.5.1 Detailed list of key startups/SMEs

- 13.10.5.2 Competitive benchmarking of startups/SMEs

- 13.11 COMPETITIVE SCENARIO

- 13.11.1 PRODUCT APPROVALS AND LAUNCHES

- 13.11.2 DEALS

- 13.11.3 EXPANSIONS

- 13.11.4 OTHER DEVELOPMENTS

14 COMPANYPROFILES

- 14.1 PHARMACEUTICALDRUGDELIVERYFORMULATIONMANUFACTURERS

- 14.1.1 JOHNSON&JOHNSON

- 14.1.1.1 Businessoverview

- 14.1.1.2 Productsoffered

- 14.1.1.3 Recentdevelopments

- 14.1.1.3.1 Productapprovals

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.3.4 Otherdevelopments

- 14.1.1.4 MnMview

- 14.1.1.4.1 Righttowin

- 14.1.1.4.2 Strategicchoices

- 14.1.1.4.3 Weaknessesandcompetitivethreats

- 14.1.2 NOVARTISAG

- 14.1.2.1 Businessoverview

- 14.1.2.2 Productsoffered

- 14.1.2.3 Recentdevelopments

- 14.1.2.3.1 Productlaunches&approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.3.4 Otherdevelopments

- 14.1.2.4 MnMview

- 14.1.2.4.1 Righttowin

- 14.1.2.4.2 Strategicchoices

- 14.1.2.4.3 Weaknessesandcompetitivethreats

- 14.1.3 F.HOFFMANN-LAROCHELTD

- 14.1.3.1 Businessoverview

- 14.1.3.2 Productsoffered

- 14.1.3.3 Recentdevelopments

- 14.1.3.3.1 Productlaunches&approvals

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.3.4 Otherdevelopments

- 14.1.3.4 MnMview

- 14.1.3.4.1 Righttowin

- 14.1.3.4.2 Strategicchoices

- 14.1.3.4.3 Weaknessesandcompetitivethreats

- 14.1.4 PFIZERINC.

- 14.1.4.1 Businessoverview

- 14.1.4.2 Productsoffered

- 14.1.4.3 Recentdevelopments

- 14.1.4.3.1 Productlaunches&approvals

- 14.1.4.3.2 Deals

- 14.1.4.4 MnMview

- 14.1.4.4.1 Righttowin

- 14.1.4.4.2 Strategicchoices

- 14.1.4.4.3 Weaknessesandcompetitivethreats

- 14.1.5 ELILILLYANDCOMPANY

- 14.1.5.1 Businessoverview

- 14.1.5.2 Productsoffered

-

14.1.5.3Recentdevelopments

- 14.1.5.3.1 Productlaunches&approvals

- 14.1.5.3.2 Deals

- 14.1.5.3.3 Expansions

- 14.1.6 GSKPLC.

- 14.1.6.1 Businessoverview

- 14.1.6.2 Productsoffered

- 14.1.6.3 Recentdevelopments

- 14.1.6.3.1 Productlaunches&approvals

- 14.1.6.3.2 Deals

- 14.1.6.3.3 Otherdevelopments

- 14.1.7 ABBVIEINC.

- 14.1.7.1 Businessoverview

- 14.1.7.2 Productsoffered

- 14.1.7.3 Recentdevelopments

- 14.1.7.3.1 Productapprovals

- 14.1.7.3.2 Deals

- 14.1.7.3.3 Expansions

- 14.1.7.3.4 Otherdevelopments

- 14.1.8 MERCK&CO.,INC.

- 14.1.8.1 Businessoverview

- 14.1.8.2 Productsoffered

- 14.1.8.3 Recentdevelopments

- 14.1.8.3.1 Productlaunches&approvals

- 14.1.8.3.2 Deals

- 14.1.8.3.3 Expansions

- 14.1.8.3.4 Otherdevelopments

- 14.1.9 BAUSCHHEALTHCOMPANIESINC.

- 14.1.9.1 Businessoverview

- 14.1.9.2 Productsoffered

- 14.1.9.3 Recentdevelopments

- 14.1.9.3.1 Productlaunches&approvals

- 14.1.9.3.2 Deals

- 14.1.10 BAYERAG

- 14.1.10.1 Businessoverview

- 14.1.10.2 Productsoffered

- 14.1.10.3 Recentdevelopments

- 14.1.10.3.1 Productlaunches&approvals

- 14.1.10.3.2 Deals

- 14.1.10.3.3 Expansions

- 14.1.10.3.4 Otherdevelopments

- 14.1.11 AMGENINC.

- 14.1.11.1 Businessoverview

- 14.1.11.2 Productsoffered

- 14.1.11.3 Recentdevelopments

- 14.1.11.3.1 Productlaunches&approvals

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Expansions

- 14.1.12 ASTRAZENECA

- 14.1.12.1 Businessoverview

- 14.1.12.2 Productsoffered

- 14.1.12.3 Recentdevelopments

- 14.1.12.3.1 Productlaunches&approvals

- 14.1.12.3.2 Deals

- 14.1.12.3.3 Expansions

- 14.1.12.3.4 Otherdevelopments

- 14.1.13 BOEHRINGERINGELHEIMINTERNATIONALGMBH

- 14.1.13.1 Businessoverview

- 14.1.13.2 Productsoffered

- 14.1.13.3 Recentdevelopments

- 14.1.13.3.1 Productlaunches&approvals

- 14.1.13.3.2 Deals

- 14.1.13.4 Recentdevelopments

- 14.1.13.4.1 Expansions

- 14.1.1 JOHNSON&JOHNSON

- 14.2 OTHERPLAYERS

- 14.2.1 SANOFI

- 14.2.2 NOVONORDISKA/S

- 14.2.3 GLENMARKPHARMACEUTICALSLTD.

- 14.2.4 VIATRISINC

- 14.2.5 BRISTOL-MYERSSQUIBBCOMPANY

- 14.2.6 RUSANPHARMALTD.

- 14.2.7 CMPPHARMA,INC.

- 14.2.8 XERISPHARMACEUTICALS,INC.

- 14.2.9 ADHEXPHARMA

- 14.3 PHARMACEUTICALDRUGDELIVERYDEVICEMANUFACTURERS

- 14.3.1 BD

- 14.3.1.1 Businessoverview

- 14.3.1.2 Productsoffered

- 14.3.1.3 Recentdevelopments

- 14.3.1.3.1 Deals

- 14.3.1.3.2 Expansions

- 14.3.1.3.3 Otherdevelopments

- 14.3.1.4 MnMview

- 14.3.1.4.1 Righttowin

- 14.3.1.4.2 Strategicchoices

- 14.3.1.4.3 Weaknessesandcompetitivethreats

- 14.3.2 CARDINALHEALTH

- 14.3.2.1 Businessoverview

- 14.3.2.2 Productsoffered

- 14.3.2.3 Recentdevelopments

- 14.3.2.3.1 Expansions

- 14.3.2.4 MnMview

- 14.3.2.4.1 Righttowin

- 14.3.2.4.2 Strategicchoices

- 14.3.2.4.3 Weaknessesandcompetitivethreats

- 14.3.3 B.BRAUNSE

- 14.3.3.1 Businessoverview

- 14.3.3.2 Productsoffered

- 14.3.4 TERUMOCORPORATION

- 14.3.4.1 Businessoverview

- 14.3.4.2 Productsoffered

-

14.3.4.3Recentdevelopments

- 14.3.4.3.1 Productlaunches&approvals

- 14.3.4.3.2 Expansions

- 14.3.5 NIPRO

- 14.3.5.1 Businessoverview

- 14.3.5.2 Productsoffered

- 14.3.5.3 Recentdevelopments

- 14.3.5.3.1 Expansions

- 14.3.6 STEVANATOGROUP

- 14.3.6.1 Businessoverview

- 14.3.6.2 Productsoffered

- 14.3.6.3 Recentdevelopments

- 14.3.6.3.1 Productlaunches&approvals

- 14.3.6.3.2 Deals

- 14.3.6.3.3 Expansions

- 14.3.6.3.4 Otherdevelopments

- 14.3.7 GERRESHEIMERAG

- 14.3.7.1 Businessoverview

- 14.3.7.2 Productsoffered

- 14.3.7.3 Recentdevelopments

- 14.3.7.3.1 Productlaunches&approvals

- 14.3.7.3.2 Deals

- 14.3.7.3.3 Expansions

- 14.3.8 WESTPHARMACEUTICALSERVICES,INC.

- 14.3.8.1 Businessoverview

- 14.3.8.2 Productsoffered

- 14.3.8.3 Recentdevelopments

- 14.3.8.3.1 Productlaunches&approvals

- 14.3.8.3.2 Deals

- 14.3.8.3.3 Expansions

- 14.3.9 YPSOMED

- 14.3.9.1 Businessoverview

- 14.3.9.2 Productsoffered

- 14.3.9.3 Recentdevelopments

- 14.3.9.3.1 Productlaunches

- 14.3.9.3.2 Deals

- 14.3.9.3.3 Expansions

- 14.3.10 SHLMEDICALAG

- 14.3.10.1 Businessoverview

- 14.3.10.2 Productsoffered

- 14.3.10.3 Recentdevelopments

- 14.3.10.3.1 Productlaunches

- 14.3.10.3.2 Deals

- 14.3.10.3.3 Expansions

- 14.3.1 BD

15 RESEARCHMETHODOLOGY

- 15.1 RESEARCHDATA

- 15.1.1 SECONDARYDATA

- 15.1.1.1 Keysecondarysources

- 15.1.2 PRIMARYDATA

- 15.1.2.1 Primarysources

- 15.1.2.2 Keydatafromprimarysources

- 15.1.2.3 Keyindustryinsights

- 15.1.2.4 Breakdownofprimaries

- 15.1.1 SECONDARYDATA

- 15.2 MARKETSIZEESTIMATION

- 15.2.1 APPROACH1:COMPANYREVENUEANALYSISAPPROACH

- 15.2.2 APPROACH2:CUSTOMER-BASEDMARKETESTIMATION

- 15.2.3 APPROACH3:TOP-DOWNAPPROACH

- 15.2.4 APPROACH4:BOTTOM-UPAPPROACH

- 15.2.5 APPROACH4:PRIMARYINTERVIEWS

- 15.2.6 APPROACH5:DEMAND-SIDEAPPROACH

- 15.2.7 APPROACH6:VOLUMEDATAANALYSIS

- 15.3 DATATRIANGULATIONANDMARKETBREAKDOWN

- 15.4 MARKETSHAREASSESSMENT

- 15.5 RESEARCHASSUMPTIONS

- 15.5.1 STUDYASSUMPTIONS

- 15.5.2 GROWTHRATEASSUMPTIONS

- 15.6 RISKASSESSMENT

- 15.6.1 RESEARCHLIMITATIONS

16 APPENDIX

- 16.1 DISCUSSIONGUIDE

- 16.2 KNOWLEDGESTORE:MARKETSANDMARKETS'SUBSCRIPTIONPORTAL

- 16.3 CUSTOMIZATIONOPTIONS

- 16.3.1 PRODUCTANALYSIS

- 16.3.2 COMPANYINFORMATION

- 16.3.3 GEOGRAPHICANALYSIS

- 16.3.4 COUNTRY-LEVELVOLUMEANALYSISBYPRODUCT

- 16.3.5 BYROUTEOFADMINISTRATIONMARKETSHAREANALYSIS(TOP5PLAYERS)

- 16.3.6 ANYCONSULT/CUSTOMREQUIREMENTSASPERCLIENTREQUESTS

- 16.4 RELATEDREPORTS

- 16.5 AUTHORDETAILS