|

시장보고서

상품코드

2041527

전력 모니터링 시장 : 구성요소별, 용도별, 최종 용도별, 지역별 - 세계 예측(-2031년)Power Monitoring Market by Component (Hardware, Software, Services), Application (Energy Management, Industrial Automation, Building Automation, Transportation), End-Use, and Region - Global Forecast to 2031 |

||||||

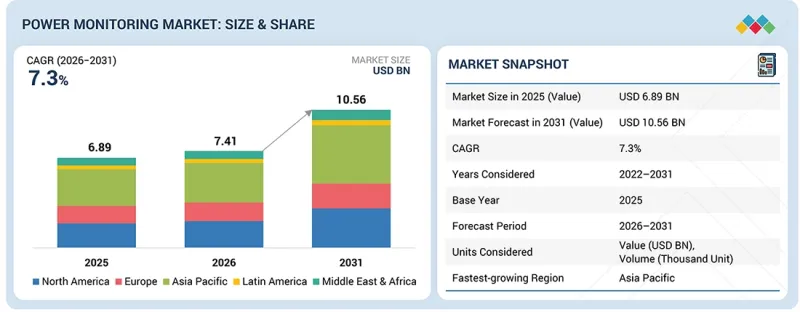

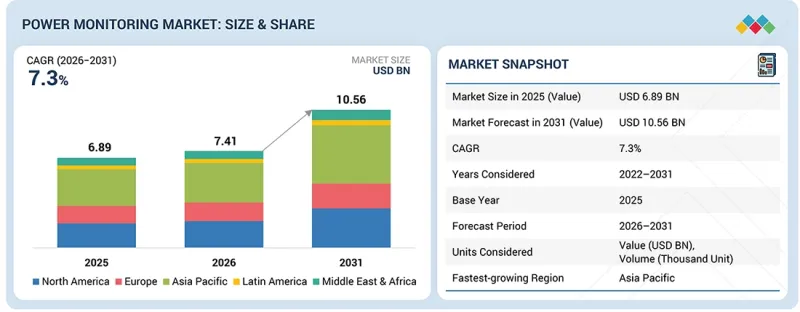

전력 모니터링 시장 규모는 예측 기간 동안 CAGR 7.3%로 확대되어 2026년 74억 1,000만 달러에서 2031년에는 105억 6,000만 달러에 달할 것으로 추정됩니다.

주요 경제권에서 데이터센터, 의료 시설, 통신 인프라, 제조 공장 및 상업용 빌딩의 급속한 확장은 노후화된 전력망에 큰 부담을 주고 있으며, 실시간 가시성, 전력 품질 보장 및 에너지 최적화를 위한 첨단 전력 모니터링 솔루션에 대한 수요를 증가시키고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 10억 달러 |

| 부문 | 구성요소별, 용도별, 최종 용도별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 라틴아메리카 |

전력 모니터링 시스템은 산업시설, 상업시설, 데이터센터, 유틸리티, 재생에너지 발전소 및 중요 인프라 프로젝트에서 지속적인 모니터링을 위해 적극적으로 도입되고 있습니다. 이러한 최종 용도 애플리케이션에는 스마트 미터링, 전력 품질 분석기, IoT 지원 센서, 고급 분석, 고조파 감소, 부하 관리, SCADA, BMS, 클라우드 플랫폼과의 완벽한 통합 등이 포함됩니다. 예지보전, 자동 경보, 원격 진단 등의 기능을 갖춘 전력 모니터링 시스템은 현대 에너지 관리, 전력망 안정성 및 운영 효율성의 핵심적인 역할을 담당하고 있습니다.

미국, 중국, 인도 및 기타 선진국과 신흥 경제국의 주요 인프라 확충, 급속한 도시화, 무정전 전원 공급에 대한 수요는 스마트 그리드 도입, 에너지 효율화 프로그램, 재생에너지 통합, 디지털 전환 촉진에 초점을 맞춘 지원 정책에 의해 가속화되고 있습니다. 이를 통해 IoT 연결, AI 기반 분석, 엣지 컴퓨팅, 하이브리드 시스템과의 호환성을 갖춘 차세대 전력 모니터링 기술의 보급을 촉진하고 있습니다. 유럽, 아시아태평양 및 기타 지역에서는 인프라 확장, 산업화, 잦은 전력 품질 문제 및 이상 기후에 대한 우려로 인해 주거, 상업, 산업 및 유틸리티 규모의 시장에서 더 큰 수요를 창출하고 있습니다. 이러한 모든 추세는 운영 탄력성, 비즈니스 연속성, 에너지 비용 절감 및 지속가능성 목표 달성을 가능하게 하며, 이는 전력 모니터링 시장이 전 세계 인프라와 경제 성장을 뒷받침하는 데 있어 핵심적인 역할을 하고 있습니다.

"예측 기간 동안 빌딩 자동화 부문은 전력 모니터링 시장에서 가장 큰 애플리케이션 부문이 될 것으로 예상됩니다."

빌딩 자동화 부문은 주로 상업시설, 오피스 빌딩, 병원, 호텔, 호텔, 교육기관, 소매점, 대규모 주택 개발에서 광범위하게 사용됨에 따라 예측 기간 동안 전력 모니터링 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 전력 모니터링 시스템은 일반적으로 에너지 소비, 전력 품질 및 전기적 매개 변수에 대한 실시간 가시성을 확보하여 최적의 에너지 관리, 비용 관리 및 중요 장비 보호를 보장하는 데 사용됩니다. 이러한 시스템은 지속적인 모니터링, 이상 징후에 대한 자동 경고, 역률 보정 지원, 부하 관리 및 빌딩 관리 시스템, HVAC 제어, 조명 시스템 및 기타 자동화 플랫폼과의 원활한 통합을 제공하기 때문에 현대 스마트 빌딩에 특히 적합합니다. 또한, 지능형 빌딩 기술의 보급 확대, 에너지 효율화 의무화, LEED 및 BREEAM과 같은 녹색건축 인증 획득이 이 부문의 성장을 촉진하고 있습니다. 또한, 빌딩 자동화 분야는 상업시설 및 공공시설의 신축 및 개보수 공사에서의 도입 확대에 따른 수혜를 받고 있습니다. 이러한 시설의 경우, 전기료 상승, 지속가능성 목표, 입주자의 편안함에 대한 요구가 높아지면서 수요가 증가하고 있습니다. 이 부문의 전력 모니터링 솔루션은 쉬운 통합, 사용하기 쉬운 대시보드, 상세한 에너지 보고서, 중공업 시스템 대비 낮은 복잡성 등의 이점을 제공합니다. 이를 통해 시설 관리자는 큰 혼란 없이 에너지 사용을 최적화하고, 운영 비용을 절감하며, 에너지 규제를 준수하고, 민감한 전자기기 및 일상 업무에 필요한 안정적인 전력 품질을 보장할 수 있습니다.

"최종사용자별로 보면 예측 기간 동안 데이터센터 부문이 전력 모니터링 시장에서 가장 빠른 성장을 기록할 것으로 예상됩니다."

세계 하이퍼스케일 및 코로케이션 시설, 클라우드 컴퓨팅 인프라, 인공지능(AI) 워크로드, 디지털 전환(DX) 이니셔티브의 폭발적인 성장에 힘입어 데이터센터 부문은 예측 기간 동안 전력 모니터링 시장에서 가장 빠른 성장세를 보일 것으로 예상됩니다. 전력 모니터링 시장에서 가장 빠르게 성장하는 최종사용자가 될 것으로 예상됩니다. 비즈니스 연속성, 운영 탄력성을 보장하고 서버 중단 및 장비 손상을 유발할 수 있는 사소한 전력 품질 문제, 전압 강하, 고조파, 과도 현상으로부터 보호하기 위해 데이터센터 운영자는 점점 더 많은 고급 전력 모니터링 솔루션을 도입하고 있습니다. 이 시스템은 매우 높은 전력 밀도를 지원하고, 전기적 파라미터에 대한 실시간 가시성을 제공하며, 매우 신뢰할 수 있는 전력 품질을 보장하도록 개발되었습니다. 이 시스템들은 고정밀 측정, 지속적인 고조파 분석, 이벤트 기록, 예지보전 경보, 부하 프로파일링, 빌딩 관리 시스템, SCADA, DCIM 플랫폼과의 완벽한 통합과 같은 고급 기능을 갖추고 있습니다. 최신 전력 모니터링 시스템 덕분에 전력 소비를 효율적으로 모니터링하고 비효율적인 부분을 파악하여 전체 시설의 성능을 최적화할 수 있게 되었습니다. 이 시스템들은 모듈식 아키텍처, 원격 진단, 클라우드 기반 대시보드, AI를 활용한 분석 기능을 특징으로 합니다. 또한, 데이터센터 내 재생에너지원, 배터리 저장 시스템(BESS) 및 백업 전원 인프라의 통합이 진행됨에 따라 고급 전력 모니터링 솔루션의 도입이 더욱 가속화되고 있습니다.

"지역별로는 예측 기간 동안 북미가 두 번째로 큰 시장 점유율을 차지할 것으로 추정됩니다."

북미는 예측 기간 동안 전력 모니터링 시스템의 두 번째 시장이 될 것으로 예상됩니다. 이러한 추세는 인프라의 고도화된 현대화, 데이터센터 및 상업 시설의 급속한 확장, 미국과 캐나다의 빈번한 전력망 장애, 노후화된 전력 인프라 및 전력 수요 증가를 배경으로 고급 전력 품질 관리에 대한 전반적인 요구로 인해 더욱 가속화되고 있습니다. 이 지역에서는 현재도 대규모 전력사업 프로젝트, 하이퍼스케일 데이터센터 건설, 반도체 제조시설, 의료시설 확장, 통신 인프라 및 산업의 국내 회귀(리쇼어링) 이니셔티브가 잇따르고 있습니다. 이 모든 과정에서 실시간 가시성, 전력 품질 준수 및 운영상의 신뢰성을 보장하기 위해 고급 전력 모니터링 시스템이 필요합니다. '인프라 투자 및 고용법'과 '인플레이션 억제법'에 따른 인센티브, 에너지 효율화에 대한 세액공제, 주정부 차원의 전력망 복원력 프로그램 등 유리한 정책적 지침이 스마트 모니터링 기술에 대한 투자를 촉진하고 있습니다. 또한, 북미의 전력회사와 최종사용자는 간헐적 재생에너지(IBR)의 높은 보급률로 인해 발생하는 전압 변동, 고조파 왜곡, 주파수 변동, 신속한 감지 및 대응 능력의 필요성 등 다양한 문제를 해결하기 위해 보다 스마트하고 효율적인 전력 모니터링 솔루션으로 전환하고 있습니다. 중요 업무의 안정성과 탄력성을 확보해야 하는 상황에서 IoT 지원 센서, AI 기반 분석, 클라우드 기반 대시보드, 고정밀 계측, 자동 경보, 기존 SCADA 및 빌딩 관리 시스템과의 원활한 통합 등 첨단 기능을 갖춘 최신 전력 모니터링 시스템 도입이 진행되고 있습니다.

Schneider Electric(프랑스), Siemens(독일), ABB(스위스), Eaton(미국), Honeywell International Inc.(미국)는 전력 모니터링 시장의 주요 기업 중 일부입니다. 본 조사에서는 이들 주요 기업들에 대한 상세한 경쟁 분석, 기업 프로파일, 최근 동향, 주요 시장 전략 등을 수록하고 있습니다.

조사 범위:

이 보고서는 구성요소, 용도, 최종 용도, 지역별로 세계 전력 모니터링 시장을 정의, 설명, 예측합니다. 또한, 시장에 대한 상세한 정성적, 정량적 분석도 제공하고 있습니다. 이 보고서는 주요 시장 촉진요인, 억제요인, 기회 및 과제를 포괄적으로 검토하고 있습니다. 또한, 시장의 다양한 중요한 측면에 대해서도 다루고 있습니다. 여기에는 경쟁 상황 분석, 시장 역학, 금액 기준 시장 규모 추정, 전력 모니터링 시장의 미래 동향이 포함됩니다.

본 보고서 구매의 주요 이점

- 이 보고서는 전력 모니터링 시장의 성장에 영향을 미치는 주요 촉진요인(엄격한 규정 준수 요건을 충족하기 위한 에너지 효율에 대한 관심 증가, 예측 분석을 가능하게 하는 스마트 그리드에 대한 투자 확대, 급속한 도시화, 전기화, 하이퍼스케일 데이터센터의 확장), 제약요인(고도의 전력 모니터링 시스템의 높은 초기 비용 및 유지보수 비용, 노후화된 전력 인프라 및 레거시 자동화 시스템), 기회(재생에너지 프로젝트 및 마이크로그리드 도입 증가, 정부의 에너지 효율 목표 달성에 대한 관심 증가), 도전과제(고도화된 사이버 위협에 대한 노출) 등 전력 모니터링 시장의 성장에 영향을 미치는 요인에 대한 분석이 포함되어 있습니다.

- 시장 동향 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 전력 모니터링 시장을 분석합니다.

- 시장 다각화 : 전력 모니터링 시장의 신제품 및 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보.

- 경쟁사 분석 : Schneider Electric(프랑스), Siemens(독일), ABB(스위스), Eaton(미국), Honeywell International(미국), Eberle(독일), Bender(독일), Secure Meters(인도), Mikronika(폴란드), Algodue Elettronica(이탈리아), BRR Energy Management(미국), GMC-Instruments(독일), Powerside(독일), GMC Energy Management(미국), GMC Energy Management(미국) MIKRONIKA(폴란드), Algodue Elettronica(이탈리아), KBR Energy Management(독일), GMC-Instruments(독일), Powerside(미국), LUMEL(폴란드), ELMEASURE(인도), Schweitzer Engineering Laboratories(미국), Eberle(독일) Schweitzer Engineering Laboratories(미국), Carlo GAVAZZI(스위스), Janitza electronics(독일), CIRCUTOR.COM(스페인), Accuenergy(캐나다), Elspec(이스라엘), Socomec(프랑스), Elmeasure(인도), Schweitzer Engineering Laboratories(미국) Socomec(프랑스), SATEC GROUP(이스라엘), LOVATO ELECTRIC(이탈리아), Rayleigh Instruments(영국), JIANGSU ELECNOVA ELECTRIC(중국), Entes(튀르키예), Unipower(스웨덴), CET(중국), Eastron Electronic(중국), PQ Plus(독일), CT LAB(남아프리카공화국), KMB Systems(체코) 등이 전력 모니터링 시장에 진출해 있습니다.

- 제품 혁신 및 개발 : 전력 모니터링 시장의 신제품 도입 및 업그레이드가 활발하며, 특히 첨단 IoT 센서, 클라우드 기반 분석 플랫폼, AI를 활용한 예지보전 도구의 통합이 활발하게 진행되고 있습니다. 에너지 절약형 계측기기, 저전력 센서, 그린 빌딩 인증 지원 솔루션 등 지속가능한 개발이 가속화되고 있습니다. 첨단 통신 프로토콜, 엣지 컴퓨팅 기능, 고정밀 전력 품질 분석기, 무선 모니터링 모듈, 모듈식 하드웨어 설계는 산업 플랜트, 데이터센터, 상업용 건물, 유틸리티, 재생에너지 시설, 스마트 시티에서 점점 더 많이 활용되고 있습니다. 디지털 제어의 고도화, 인공지능(AI)을 활용한 이상 감지 및 에너지 최적화, 원격 모니터링 대시보드, SCADA 시스템, 빌딩 관리 시스템, 축전지, 마이크로그리드, 신재생에너지원과의 원활한 통합 등 통합 솔루션의 개발도 빠르게 진행되고 있습니다. 가 실현되고 있습니다. 이러한 혁신은 설치 간소화, 설치 비용 절감, 실시간 의사결정, 전체 에너지 소비 감소, 현대 전력 네트워크의 고조파 감소, 전압 안정성, 고장 감지 및 전체 시스템 신뢰성을 향상시킵니다. 차세대 디바이스는 현재 IEC 61850, Modbus TCP, MQTT 등 다양한 통신 표준을 지원하며, 엄격한 업계 표준을 충족하는 사이버 보안 기능도 갖추고 있습니다. 컴팩트하고 확장성이 높으며, 미래 지향적인 플랫폼으로 시설 확장 및 분산형 에너지 자원 도입에 따라 쉽게 업그레이드 및 확장이 가능합니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 전력 모니터링 시장(구성요소별)

제10장 전력 모니터링 시장(용도별)

제11장 전력 모니터링 시장(용도별)

제12장 전력 모니터링 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.06.01The power monitoring market is estimated to grow from USD 7.41 billion in 2026 to USD 10.56 billion by 2031, at a CAGR of 7.3% during the forecast period. The rapid expansion of data centers, healthcare facilities, telecommunications infrastructure, manufacturing plants, and commercial buildings in large economies is placing significant strain on aging power grids and increasing demand for advanced power monitoring solutions to provide real-time visibility, power quality assurance, and energy optimization.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | USD Billion |

| Segments | By Type, Component, Application, End User, |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, Latin America |

Power monitoring systems are being strongly deployed for continuous monitoring in industrial facilities, commercial complexes, data centers, utilities, renewable energy plants, and critical infrastructure projects. These end-use applications involve smart metering, power quality analyzers, IoT-enabled sensors, advanced analytics, harmonic mitigation, load management, and seamless integration with SCADA, BMS, and cloud platforms. With features such as predictive maintenance, automatic alerts, and remote diagnostics, power monitoring systems are positioned at the center of contemporary energy management, grid stability, and operational efficiency.

The additions to critical infrastructure, rapid urbanization, and the need for an uninterrupted power supply in the US, China, India, and other developed and emerging economies are being accelerated by supportive policies focused on smart grid deployment, energy efficiency programs, renewable energy integration, and digital transformation incentives. This promotes the widespread adoption of next-generation power monitoring technologies with IoT connectivity, AI-driven analytics, edge computing, and hybrid-system compatibility. In Europe, Asia Pacific, and other regions, infrastructure growth, industrialization, and concerns over frequent power quality issues and extreme weather events are driving even greater demand in the residential, commercial, industrial, and utility-scale markets. All these trends are making it possible to achieve greater operational resilience, business continuity, energy cost savings, and sustainability goals, which contribute to the central role of the power monitoring market in supporting global infrastructure and economic growth.

"The building automation segment is expected to be the largest application segment in the power monitoring market during the forecast period."

The building automation segment is expected to hold the largest share of the power monitoring market during the forecast period, primarily due to its widespread use in commercial complexes, office buildings, hospitals, hotels, educational institutions, retail spaces, and large residential developments. Power monitoring systems in this application are commonly used to deliver real-time visibility into energy consumption, power quality, and electrical parameters, ensuring optimal energy management, cost control, and protection of critical equipment. These systems are especially suitable for modern smart buildings because they provide continuous monitoring, automatic anomaly alerts, power factor correction support, load management, and seamless integration with building management systems, HVAC controls, lighting systems, and other automation platforms. Moreover, this segment is strengthening due to the growing adoption of intelligent building technologies, energy-efficiency mandates, and green building certifications such as LEED and BREEAM. The building automation category also benefits from expanding installations in both new construction and retrofits across commercial and institutional facilities, where rising electricity costs, sustainability targets, and occupant comfort requirements are driving demand. Power monitoring solutions in this segment offer the advantages of easy integration, user-friendly dashboards, detailed energy reporting, and lower complexity than heavy industrial-grade systems. They enable facility managers to optimize energy use, reduce operational costs, maintain compliance with energy codes, and ensure reliable power quality for sensitive electronic equipment and daily operations, all without major disruptions.

"By end user, the data center segment is projected to register the fastest growth in the power monitoring market during the forecast period."

The data center segment is expected to be the fastest-growing end user in the power monitoring market throughout the forecast period as a result of the explosive expansion of hyperscale and colocation facilities, cloud computing infrastructure, artificial intelligence workloads, and digital transformation initiatives worldwide. To achieve business continuity, operational resilience, and protection against even minor power quality issues, voltage sags, harmonics, or transients that can cause server outages or equipment damage, data center operators are increasingly adopting advanced power monitoring solutions. These systems are developed to accommodate extremely high power densities, deliver real-time visibility into electrical parameters, and ensure ultra-reliable power quality. They come with advanced features, including high-precision metering, continuous harmonic analysis, event recording, predictive maintenance alerts, load profiling, and seamless integration with building management systems, SCADA, and DCIM platforms. The ability to efficiently monitor power consumption, identify inefficiencies, and optimize the performance of an entire facility is now possible thanks to modern power monitoring systems. These systems feature modular architectures, remote diagnostics, cloud-based dashboards, and AI-driven analytics. Additionally, the increasing integration of renewable energy sources, battery energy storage systems (BESS), and backup power infrastructure in data centers is further encouraging the adoption of advanced power monitoring solutions.

"By region, North America is estimated to account for the second-largest market share during the forecast period."

North America is expected to become the second-largest market for power monitoring systems during the forecast period. The development is encouraged by the high level of infrastructure modernization, rapid expansion of data centers and commercial facilities, and the overall need for advanced power quality management amid frequent grid disturbances, aging power infrastructure, and rising electricity demand in both the US and Canada. The region is still experiencing a significant influx of utility-scale projects, hyperscale data center construction, semiconductor manufacturing facilities, healthcare expansions, telecommunications infrastructure, and industrial reshoring initiatives. All of these require sophisticated power monitoring systems to ensure real-time visibility, power-quality compliance, and operational reliability. Favorable policy guidelines, such as incentives under the Infrastructure Investment and Jobs Act and the Inflation Reduction Act, tax credits for energy efficiency, and state-level grid resilience programs, are boosting investment in smart monitoring technologies. In addition, utilities and end users in North America are moving toward smarter, more efficient power monitoring solutions to address the challenges posed by high penetration of intermittent renewable resources (IBRs), including voltage fluctuations, harmonic distortion, frequency variations, and the need for rapid detection and response capabilities. The need to ensure the reliability and resilience of critical operations is driving the use of modern power monitoring systems with advanced features such as IoT-enabled sensors, AI-driven analytics, cloud-based dashboards, high-precision metering, automatic alerts, and seamless integration with existing SCADA and building management systems.

In-depth interviews have been conducted with key industry participants, subject-matter experts, C-level executives of leading market players, and industry consultants, among others, to obtain and verify critical qualitative and quantitative information and to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1 - 45%, Tier 2 - 30%, and Tier 3 - 25%

By Designation: C-level Executives - 35%, Directors - 25%, and Others - 40%

By Region: Asia Pacific - 60%, Europe - 15%, North America - 10%, Middle East & Africa - 10%, and Latin America - 5%

Notes: The tiers of the companies are defined based on their total revenues as of 2025. Tier 1: > USD 1 billion, Tier 2: USD 500 million to USD 1 billion, and Tier 3: < USD 500 million.

Other designations include sales managers, engineers, and regional managers.

Schneider Electric (France), Siemens (Germany), ABB (Switzerland), Eaton (US) and Honeywell International Inc. (US) are some of the major players in the power monitoring market. The study includes an in-depth competitive analysis of these key players, including their company profiles, recent developments, and key market strategies.

Research Coverage:

The report defines, describes, and forecasts the global power monitoring market by component, application, end use, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in the power monitoring market.

Key Benefits of Buying the Report

- It provides an analysis of key drivers (growing emphasis on energy efficiency to meet strict compliance requirements, increasing investment in smart grids to enable predictive analytics, rapid urbanization, electrification, and hyperscale data center expansion), restraints (high upfront and maintenance costs of advanced power monitoring systems, aging electrical infrastructure and legacy automation systems), opportunities (increasing renewable energy projects and microgrid deployments, heightened focus on achieving government-mandated energy efficiency targets), challenges (exposure to sophisticated cyber threats) influencing the growth of the power monitoring market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the power monitoring market across varied regions.

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the power monitoring market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Schneider Electric (France), Siemens (Germany), ABB (Switzerland), Eaton (US), Honeywell International (US), Eberle (Germany), Bender (Germany), Secure Meters (India), MIKRONIKA (Poland), Algodue Elettronica (Italy), KBR Energy Management (Germany), GMC-Instruments (Germany), Powerside (US), LUMEL (Poland), ELMEASURE (India), Schweitzer Engineering Laboratories (US), CARLO GAVAZZI (Switzerland), Janitza electronics (Germany), CIRCUTOR.COM (Spain), Accuenergy (Canada), Elspec (Israel), Socomec (France), SATEC GROUP (Israel), LOVATO ELECTRIC (Italy), Rayleigh Instruments (UK), JIANGSU ELECNOVA ELECTRIC (China), Entes (Turkey), Unipower (Sweden), CET (China), Eastron Electronic (China), PQ Plus (Germany), CT LAB (South Africa), and KMB Systems (Czech Republic), among others, in the power monitoring market.

- Product Innovation/Development: Product introduction and upgrades in the power monitoring market are high, particularly with the integration of advanced IoT sensors, cloud-based analytics platforms, and AI-powered predictive maintenance tools. Sustainable developments, including energy-efficient metering devices, low-power-consumption sensors, and solutions that support green building certifications, are gaining ground. Advanced communication protocols, edge computing capabilities, high-precision power quality analyzers, wireless monitoring modules, and modular hardware designs are increasingly used in industrial plants, data centers, commercial buildings, utilities, renewable energy installations, and smart cities. The development of integrated solutions is also advancing rapidly, with improved digital controls, artificial intelligence (AI)-based anomaly detection and energy optimization, remote monitoring dashboards, and seamless integration with SCADA systems, building management systems, battery storage, microgrids, and renewable energy sources. These innovations simplify deployment, reduce installation costs, enable real-time decision-making, lower overall energy consumption, and improve harmonic mitigation, voltage stability, fault detection, and overall system reliability in modern power networks. New-generation devices now support multiple communication standards, such as IEC 61850, Modbus TCP, and MQTT, as well as cybersecurity features that meet stringent industry standards. Compact, scalable, and future-ready platforms allow easy upgrades and expansion as facilities grow or adopt more distributed energy resources.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN POWER MONITORING MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POWER MONITORING MARKET

- 3.2 POWER MONITORING MARKET, BY COMPONENT AND REGION

- 3.3 POWER MONITORING MARKET, BY COMPONENT

- 3.4 POWER MONITORING MARKET, BY APPLICATION

- 3.5 POWER MONITORING MARKET, BY END USE

- 3.6 POWER MONITORING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing emphasis on energy efficiency to meet strict compliance requirements

- 4.2.1.2 Increasing investment in smart grids to enable predictive analytics

- 4.2.1.3 Rapid urbanization, electrification, and hyperscale data center expansion

- 4.2.2 RESTRAINTS

- 4.2.2.1 High upfront and maintenance costs of advanced power monitoring systems

- 4.2.2.2 Aging electrical infrastructure and legacy automation systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing renewable energy projects and microgrid deployments

- 4.2.3.2 Heightened focus on achieving government-mandated energy efficiency targets

- 4.2.4 CHALLENGES

- 4.2.4.1 Exposure to sophisticated cyber threats

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL UTILITIES INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DATA CENTER INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF POWER MONITORING SYSTEMS, BY HARDWARE TYPE, 2022-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF POWER MONITORING SYSTEMS, BY REGION, 2022-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 903089)

- 5.6.2 EXPORT SCENARIO (HS CODE 903089)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SCHNEIDER ELECTRIC DEPLOYS ECOSTRUXURE POWER MONITORING PLATFORM TO SUPPORT GRID MODERNIZATION AND DER INTEGRATION OF MAJOR EUROPEAN UTILITY

- 5.10.2 ABB INSTALLS ABILITY POWER QUALITY MONITORING SOLUTION TO ENHANCE POWER RELIABILITY IN HYPERSCALE DATA CENTER IN NORTH AMERICA

- 5.10.3 SIEMENS ADOPTS SENTRON POWERMANAGER PLATFORM TO OPTIMIZE ENERGY CONSUMPTION ACROSS AUTOMOTIVE PRODUCTION LINES IN ASIA PACIFIC

- 5.11 IMPACT OF US TARIFFS - POWER MONITORING MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SMART METERS AND ADVANCED METERING INFRASTRUCTURE

- 6.1.2 POWER QUALITY ANALYZERS AND MEASUREMENT DEVICES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CLOUD AND EDGE COMPUTING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON POWER MONITORING MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN POWER MONITORING MARKET

- 6.6.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION IN POWER MONITORING MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI/GEN AI-INTEGRATED POWER MONITORING SYSTEMS

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 SCHNEIDER ELECTRIC: UTILITY-SCALE WIDE-AREA MONITORING WITH AI-DRIVEN PREDICTIVE ANALYTICS

- 6.7.2 ABB: INDUSTRIAL MICROGRID MONITORING AND AUTONOMOUS ENERGY OPTIMIZATION

- 6.7.3 SIEMENS: COMMERCIAL VIRTUAL POWER PLANT WITH AI-ENHANCED SUB-METERING

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF POWER MONITORING SYSTEMS

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USES

- 8.5 MARKET PROFITABILITY

9 POWER MONITORING MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 HARDWARE

- 9.2.1 MONITORING DEVICES

- 9.2.1.1 Rising need for uninterrupted power quality to accelerate segmental growth

- 9.2.2 MEASUREMENT & SENSING DEVICES

- 9.2.2.1 Growing focus on precise capture of electrical and environmental parameters to boost segmental growth

- 9.2.3 COMMUNICATION & DATA ACQUISITION DEVICES

- 9.2.3.1 Rising distributed energy resources, smart metering infrastructure, and remote asset management to spur demand

- 9.2.1 MONITORING DEVICES

- 9.3 SOFTWARE

- 9.3.1 ON-PREMISES

- 9.3.1.1 High customization, seamless integration, and uninterrupted functionality to foster segmental growth

- 9.3.2 CLOUD-HOSTED

- 9.3.2.1 Scalability, automatic updates, low initial costs, and seamless collaborations to expedite segmental growth

- 9.3.3 HYBRID

- 9.3.3.1 Elastic scaling, predictive insights, and multi-site visibility to bolster segmental growth

- 9.3.1 ON-PREMISES

- 9.4 SERVICES

- 9.4.1 INCREASING SYSTEM COMPLEXITY AND NEED FOR DATA SECURITY TO DRIVE MARKET

10 POWER MONITORING MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 ENERGY MANAGEMENT

- 10.2.1 ABILITY TO PROVIDE REAL-TIME VISIBILITY INTO ENERGY USAGE PATTERNS AND DEMAND PROFILES TO BOOST SEGMENTAL GROWTH

- 10.3 INDUSTRIAL AUTOMATION

- 10.3.1 REQUIREMENT FOR PREDICTIVE ANALYTICS, FAULT DETECTION, AND EQUIPMENT HEALTH INSIGHTS TO FUEL SEGMENTAL GROWTH

- 10.4 BUILDING AUTOMATION

- 10.4.1 FOCUS ON DEMAND-SIDE MANAGEMENT, FAULT DETECTION, AND PREDICTIVE MAINTENANCE OF CRITICAL ELECTRICAL ASSETS TO SPUR DEMAND

- 10.5 TRANSPORTATION

- 10.5.1 RELIABILITY, RAPID FAULT DETECTION, AND SEAMLESS INTEGRATION WITH RENEWABLE ENERGY SOURCES TO AUGMENT SEGMENTAL GROWTH

11 POWER MONITORING MARKET, BY END USE

- 11.1 INTRODUCTION

- 11.2 UTILITIES

- 11.2.1 EMPHASIS ON RELIABLE ELECTRICITY SUPPLY, GRID STABILITY, AND COMPLEX POWER FLOW MANAGEMENT TO BOOST SEGMENTAL GROWTH

- 11.3 DATA CENTERS

- 11.3.1 NEED TO MANAGE ENORMOUS AND RAPIDLY INCREASING POWER DENSITIES TO ACCELERATE SEGMENTAL GROWTH

- 11.4 BUILDINGS

- 11.4.1 HOSPITALS

- 11.4.1.1 Requirement for consistent power supply to support critical equipment to expedite segmental growth

- 11.4.2 AIRPORTS

- 11.4.2.1 Focus on monitoring power quality for sensitive avionics and communication equipment to bolster segmental growth

- 11.4.3 GOVERNMENT, DEFENSE & COMMERCIAL OFFICES

- 11.4.3.1 High emphasis on meeting government-mandated sustainability and energy efficiency targets to drive market

- 11.4.4 OTHER BUILDINGS

- 11.4.1 HOSPITALS

- 11.5 INDUSTRIAL

- 11.5.1 FOOD & BEVERAGES

- 11.5.1.1 Focus on preventing costly production stoppages and reducing waste in energy-intensive processes to foster segmental growth

- 11.5.2 AUTOMOTIVE

- 11.5.2.1 High energy intensity and automation levels in vehicle assembly plants to accelerate segmental growth

- 11.5.3 PHARMACEUTICALS

- 11.5.3.1 Requirement for ultra-reliable power monitoring to contribute to segmental growth

- 11.5.4 HEAVY MACHINERY

- 11.5.4.1 Growing emphasis on continuous real-time monitoring to drive market

- 11.5.5 OTHER INDUSTRIES

- 11.5.1 FOOD & BEVERAGES

- 11.6 RENEWABLE ENERGY

- 11.6.1 REQUIREMENT FOR SPECIALIZED POWER MONITORING SYSTEMS TO EXPEDITE SEGMENTAL GROWTH

- 11.7 TELECOM

- 11.7.1 MOUNTING DEMAND FOR ULTRA-RELIABLE POWER MONITORING TO PREVENT BRIEF OUTAGES TO FOSTER SEGMENTAL GROWTH

- 11.8 RAILWAYS & METROS

- 11.8.1 OPERATION UNDER HIGH DYNAMIC LOADS TO AUGMENT SEGMENTAL GROWTH

- 11.9 OTHER END USES

12 POWER MONITORING MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Accelerated transition from coal to renewable power sources to reduce carbon intensity to bolster market growth

- 12.2.2 INDIA

- 12.2.2.1 Rapid urbanization, industrialization, and digitalization to expedite market growth

- 12.2.3 JAPAN

- 12.2.3.1 High emphasis on enhancing grid stability and rapid fault recovery to accelerate market growth

- 12.2.4 SOUTH KOREA

- 12.2.4.1 Rapid expansion of advanced metering infrastructure and digital substations to foster market growth

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Unprecedented hyperscale data center expansion, aging grid infrastructure, and rising renewable energy penetration to drive market

- 12.3.2 CANADA

- 12.3.2.1 Increasing data center investments, clean electricity targets, and grid modernization efforts to fuel market growth

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Growing emphasis on real-time visibility, automated fault isolation, and predictive grid management to drive market

- 12.4.2 UK

- 12.4.2.1 Increasing investment in smart grid and advanced technologies to augment market growth

- 12.4.3 FRANCE

- 12.4.3.1 Rapid modernization of nuclear fleet to contribute to market growth

- 12.4.4 ITALY

- 12.4.4.1 Strong focus on addressing grid congestion and improving reliability to accelerate market growth

- 12.4.5 SPAIN

- 12.4.5.1 Shifting preference toward renewable energy sources to bolster market growth

- 12.4.6 AUSTRIA

- 12.4.6.1 Increasing hydroelectric generation and decarbonization targets to boost market growth

- 12.4.7 NORDICS

- 12.4.7.1 Rising deployment of smart grid technologies to drive market

- 12.4.8 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Shifting preference from fossil fuels to sustainable energy to accelerate market growth

- 12.5.1.2 UAE

- 12.5.1.2.1 Massive investments in renewable energy, smart grid, and digital transformation strategies to fuel market growth

- 12.5.1.3 Rest of GCC

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Rapid expansion of renewable energy to bolster market growth

- 12.5.3 EGYPT

- 12.5.3.1 Population growth, urbanization, and electrification to augment market growth

- 12.5.4 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC

- 12.6 LATIN AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Aging distribution networks and transmission bottlenecks to expedite market growth

- 12.6.2 ARGENTINA

- 12.6.2.1 Renewed mining investments and persistent grid issues to contribute to market growth

- 12.6.3 MEXICO

- 12.6.3.1 Rising need to improve power quality and reliability amid frequent grid disturbances to drive market

- 12.6.4 REST OF LATIN AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2023-2026

- 13.3 MARKET SHARE ANALYSIS, 2025

- 13.4 REVENUE ANALYSIS, 2021-2025

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 PRODUCT COMPARISON

- 13.6.1 SCHNEIDER ELECTRIC (FRANCE)

- 13.6.2 SIEMENS (GERMANY)

- 13.6.3 ABB (SWITZERLAND)

- 13.6.4 EATON (IRELAND)

- 13.6.5 HONEYWELL INTERNATIONAL INC. (US)

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Component footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 End use footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 OTHER DEVELOPMENTS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 SCHNEIDER ELECTRIC

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product/Service launches

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths/Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses/Competitive threats

- 14.1.2 ABB

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Other developments

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths/Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses/Competitive threats

- 14.1.3 SIEMENS

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths/Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses/Competitive threats

- 14.1.4 EATON

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product/Service launches

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Other developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses/Competitive threats

- 14.1.5 HONEYWELL INTERNATIONAL INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product/Service launches

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths/Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses/Competitive threats

- 14.1.6 SOCOMEC

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.7 A. EBERLE GMBH & CO. KG

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.8 CARLO GAVAZZI

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product/Service launches

- 14.1.9 BENDER GMBH & CO. KG

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product/Service launches

- 14.1.10 EASTRON ELECTRONIC CO., LTD.

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.11 PQ PLUS GMBH

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.12 GMC-INSTRUMENTS

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.13 KBR ENERGYMANAGEMENT GMBH

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.14 KMB SYSTEMS, S.R.O

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.15 ELMEASURE

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Solutions/Services offered

- 14.1.16 LUMEL S.A.

- 14.1.16.1 Business overview

- 14.1.16.2 Products/Solutions/Services offered

- 14.1.17 JANITZA ELECTRONICS GMBH

- 14.1.17.1 Business overview

- 14.1.17.2 Products/Solutions/Services offered

- 14.1.18 SCHWEITZER ENGINEERING LABORATORIES, INC.

- 14.1.18.1 Business overview

- 14.1.18.2 Products/Solutions/Services offered

- 14.1.1 SCHNEIDER ELECTRIC

- 14.2 OTHER PLAYERS

- 14.2.1 CIRCUTOR.COM

- 14.2.2 SATEC GROUP

- 14.2.3 ELSPEC LTD

- 14.2.4 POWERSIDE

- 14.2.5 RAYLEIGH INSTRUMENTS LIMITED.

- 14.2.6 JIANGSU ELECNOVA ELECTRIC CO., LTD

- 14.2.7 ALGODUE ELETTRONICA SRL

- 14.2.8 LOVATO ELECTRIC

- 14.2.9 MIKRONIKA SP. Z O.O.

- 14.2.10 CT LAB (PTY) LIMITED

- 14.2.11 UNIPOWER AB

- 14.2.12 ENTES.COM.TR

- 14.2.13 SECURE METERS LTD.

- 14.2.14 CET INC.

- 14.2.15 ACCUENERGY INC.

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.2 SECONDARY AND PRIMARY RESEARCH

- 15.2.1 SECONDARY DATA

- 15.2.1.1 List of key secondary sources

- 15.2.1.2 Key data from secondary sources

- 15.2.2 PRIMARY DATA

- 15.2.2.1 List of primary interview participants

- 15.2.2.2 Key industry insights

- 15.2.2.3 Breakdown of primaries

- 15.2.2.4 Key data from primary sources

- 15.2.1 SECONDARY DATA

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 BOTTOM-UP APPROACH

- 15.3.2 TOP-DOWN APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 DEMAND-SIDE

- 15.4.1.1 Demand-side assumptions

- 15.4.1.2 Demand-side calculations

- 15.4.2 SUPPLY-SIDE

- 15.4.2.1 Supply-side assumptions

- 15.4.2.2 Supply-side calculations

- 15.4.1 DEMAND-SIDE

- 15.5 FORECAST

- 15.6 DATA TRIANGULATION

- 15.7 RESEARCH LIMITATIONS

- 15.8 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS