|

시장보고서

상품코드

2042501

수소 센서 시장(-2032년) : 기술(전기화학식, 촉매식, 열전도식, MOS/고체식, 광학식), 감지 범위(1000ppm 미만, 1000-10000ppm, 10000ppm 이상), 용도(누설 감지, 프로세스&배출 가스 감시)Hydrogen Sensor Market by Technology (Electrochemical Catalytic, Thermal Conductivity, MOS/Solid-state, Optical), Detection Range (<1000, 1000-10000, > 10000 PPM), Application (Leak Detection, Process & Emission Monitoring) - Global Forecast to 2032 |

||||||

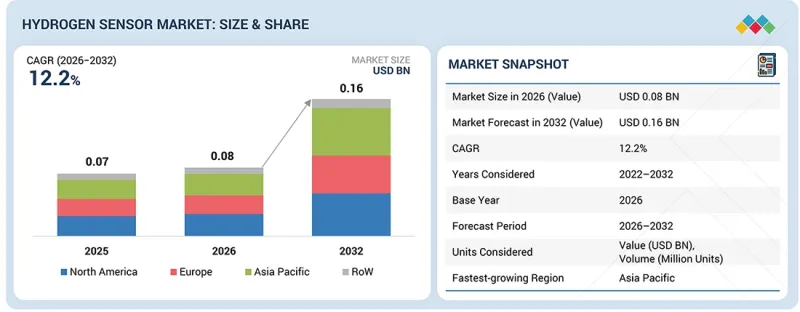

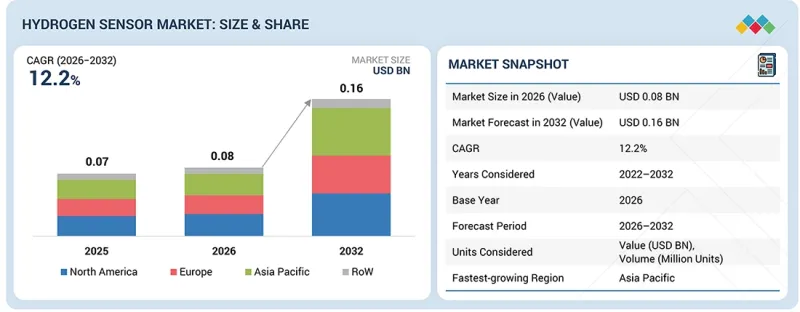

수소 시장 규모는 2026년 8,000만 달러에서 2032년에는 1억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 12.2%를 나타낼 전망입니다.

수소 센서 시장은 에너지, 산업, 모빌리티 분야에서의 수소 활용 확대에 힘입어 예측 기간 동안 강력한 성장세를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 금액(달러) |

| 부문 | 기술, 용도, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

수소는 인화성이 매우 높아 엄격한 안전 조치가 필요하기 때문에 각 산업계에서는 실시간 누출 감지 및 지속적인 모니터링을 실현하는 첨단 센싱 솔루션을 우선적으로 도입하고 있습니다. 안전 시스템에 필수적인 수소 센서는 사고 예방과 규제 준수에 있어 매우 중요한 역할을 하고 있습니다. 이에 따라 각 제조업체들은 감도 향상, 응답 시간 단축, IoT 및 AI 기반 모니터링 플랫폼과의 통합을 실현한 고성능 센서를 개발하고 있습니다.

이러한 발전은 안전 관리 향상, 다운타임 감소, 운영 효율성 향상에 기여하고 있습니다. 또한, 수소 인프라, 청정 에너지에 대한 노력, 탈탄소화 목표에 대한 투자 확대도 수소 센서의 도입을 가속화하고 있습니다. 수소 센서는 안전, 신뢰성, 컴플라이언스 향상으로 인한 장기적인 이점으로 인해 에너지, 석유 및 가스, 화학, 자동차 등의 산업에서 필수적인 투자 대상이 되고 있습니다.

"기술별로는 예측 기간 동안 금속 산화물 반도체(MOS) 부문이 두 번째 시장 점유율을 차지할 것으로 예측됩니다."

MOS 수소 센서는 견고성, 긴 수명, 열악한 산업 환경에 대한 적응성으로 인해 예측 기간 동안 상당한 성장이 예상됩니다. 이 센서는 내구성과 지속적인 모니터링이 필수적인 석유 및 가스, 화학 처리, 수소 인프라 등의 분야에서 널리 사용되고 있습니다. 광범위한 온도 범위에서 작동하고 다양한 수소 농도를 감지할 수 있는 능력으로 높은 범용성을 발휘합니다. 또한, 낮은 제조 비용과 산업 안전 시스템에 쉽게 통합할 수 있다는 점도 채택을 촉진하고 있습니다. 신뢰할 수 있고 비용 효율적인 센싱 솔루션에 대한 수요 증가는 수소 센서 시장에서 MOS 부문의 성장을 더욱 뒷받침하고 있습니다.

"검출 범위별로는 0-1,000ppm 범위가 예측 기간 동안 큰 비중을 차지할 것으로 예상"

0-1,000ppm 범위에서 작동하는 센서는 저농도의 수소를 감지하여 조기 누출을 감지할 수 있는 중요한 역할을 하기 때문에 큰 시장 점유율을 차지할 것으로 예측됩니다. 이 센서는 고감도가 필수적인 연료전지, 실험실, 밀폐된 산업 환경 등에서 널리 사용되고 있습니다. 정확한 실시간 모니터링 기능을 제공함으로써 안전성을 향상시키고 규제 준수를 보장합니다. 고정밀 감지에 대한 수요 증가와 센서 기술의 발전은 수소 관련 응용 분야에서 이러한 센서의 채택을 더욱 촉진하고 있습니다.

"예측 기간 동안 아시아태평양은 수소 센서 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다."

아시아태평양은 수소 인프라의 급속한 확장과 주요 최종 사용자 산업의 강력한 성장으로 인해 예측 기간 동안 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 중국, 일본, 한국, 인도 등의 국가에서 에너지, 운송, 산업 분야에서 수소의 채택이 확대되면서 수소 센서 수요를 크게 견인하고 있습니다. 청정 에너지 프로젝트에 대한 투자 증가, 정부 지원 정책, 국가의 수소 전략이 시장 성장을 더욱 가속화시키고 있습니다. 또한, 비용 경쟁력을 갖춘 제조업체의 존재와 산업 안전 및 규제 준수에 대한 관심이 높아진 것도 시장 침투를 촉진하고 있습니다. 실시간 모니터링, 안전 시스템, 확장 가능한 수소 도입에 대한 관심 확대는 아시아태평양의 수소 센서 시장의 강력한 성장을 지속적으로 뒷받침하고 있습니다.

세계의 수소 센서(Hydrogen Sensor) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 수소 센서 응용

제10장 수소 센서 시장 : 기술별

제11장 수소 센서 시장 : 감지 범위별

제12장 수소 센서 시장 : 산업별

제13장 수소 센서 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSHAccording to MarketsandMarkets, the hydrogen market is projected to reach USD 0.16 billion by 2032 from USD 0.08 billion in 2026, at a CAGR of 12.2% during the forecast period. The hydrogen sensor market is projected to witness strong growth during the forecast period, driven by the increasing adoption of hydrogen across energy, industrial, and mobility applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

As hydrogen is highly flammable and requires strict safety measures, industries are prioritizing advanced sensing solutions for real-time leak detection and continuous monitoring. Hydrogen sensors, being integral to safety systems, play a critical role in preventing accidents and ensuring regulatory compliance. As a result, manufacturers are developing high-performance sensors with improved sensitivity, faster response times, and integration with IoT and AI-based monitoring platforms.

These advancements enable better safety management, reduced downtime, and enhanced operational efficiency. Additionally, growing investments in hydrogen infrastructure, clean energy initiatives, and decarbonization goals are accelerating adoption. The long-term benefits of improved safety, reliability, and compliance make hydrogen sensors a critical investment across industries such as energy, oil & gas, chemicals, and automotive.

"By technology, the metal oxide semiconductor segment will capture the second-largest market share throughout the forecast period."

MOS (Metal Oxide Semiconductor) hydrogen sensors are expected to witness significant growth during the forecast period due to their robustness, long operational life, and suitability for harsh industrial environments. These sensors are widely used in applications such as oil & gas, chemical processing, and hydrogen infrastructure, where durability and continuous monitoring are critical. Their ability to operate across a wide temperature range and detect varying hydrogen concentrations makes them highly versatile. Additionally, lower manufacturing costs and ease of integration into industrial safety systems are driving their adoption. Increasing demand for reliable and cost-efficient sensing solutions is further supporting the growth of the MOS segment in the hydrogen sensor market.

"By detection range, 0-1,000 ppm is expected to capture the significant share during the forecast period."

Sensors operating in the 0-1,000 ppm range are expected to capture a significant market share due to their critical role in detecting low concentrations of hydrogen and enabling early leak detection. These sensors are widely used in applications such as fuel cells, laboratories, and enclosed industrial environments where high sensitivity is essential. Their ability to provide accurate, real-time monitoring ensures enhanced safety and regulatory compliance. Increasing demand for precision detection and advancements in sensor technologies are further driving their adoption across hydrogen applications.

"Asia Pacific is likely to be the fastest-growing region in the hydrogen sensor market during the forecast period."

Asia Pacific is likely to be the fastest-growing region in the hydrogen sensor market during the forecast period due to the rapid expansion of hydrogen infrastructure and strong growth across key end-use industries. Increasing adoption of hydrogen in energy, transportation, and industrial applications in countries such as China, Japan, South Korea, and India is significantly driving demand for hydrogen sensors. Rising investments in clean energy projects, supportive government policies, and national hydrogen strategies are further accelerating market growth. Additionally, the presence of cost-competitive manufacturers and a growing focus on industrial safety and regulatory compliance are enhancing market penetration. Increasing emphasis on real-time monitoring, safety systems, and scalable hydrogen deployment continues to support the strong growth trajectory of the Asia Pacific hydrogen sensor market.

Breakdown of Primaries

A variety of executives from key organizations operating in the hydrogen sensor market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 38%, Tier 2 - 28%, and Tier 3 - 34%

- By Designation: C-level Executives - 40%, Directors - 30%, and Others - 30%

- By Region: North America - 35%, Europe - 35, Asia Pacific - 20%, and RoW - 10%

Note: The RoW region includes the Middle East, Africa, and South America. Other designations include product, sales, and marketing managers. Three tiers of companies have been defined based on their total revenues: Tier 3: revenue less than USD 100 million; Tier 2: revenue between USD 100 million and USD 1 billion; and Tier 1: revenue more than USD 1 billion.

Major players profiled in this report are as follows: Major players operating in hydrogen sensor market include Amphenol Corporation (US) Honeywell International Inc. (US), Nissha Co., Ltd (Japan), Schaeffler AG (US), Figaro Engineering Inc. (Japan), Valeo (France), Membrapor AG (Switzerland), Zhengzhou Winsen Electronics Technology Co., Ltd. (China), and Posifa Technologies, INC. (Us), among others.

These companies compete by continuously enhancing hydrogen sensor performance, focusing on improved sensitivity, faster response times, and higher accuracy for leak detection across diverse applications. Strategic emphasis is placed on developing advanced sensing technologies, including electrochemical, MOS, and optical sensors, along with integration with IoT and AI-based monitoring systems. Market participants prioritize scalable and reliable solutions tailored for industries such as energy, oil & gas, chemicals, and automotive. Strong focus is also placed on ensuring regulatory compliance, operational safety, and ease of integration with existing infrastructure. Continued investments in advanced materials, miniaturization, and smart sensing technologies, along with collaborations with industrial players and technology providers, are expected to sustain competition and accelerate adoption across the global hydrogen sensor market.

The study provides a detailed competitive analysis of these key players in the hydrogen sensor market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the hydrogen sensor market presents a detailed analysis based on technology, detection range, application, end-use industry, and region. By technology, the market is segmented into electrochemical, metal oxide semiconductor, catalytic, optical, and other technologies. By detection range, it is categorized into 0-1,000 ppm, 1,000-10,000 ppm, and above 10,000 ppm. By end-use industry, the market covers energy & power, oil & gas, chemicals, automotive & transportation, and other end-use industries. The regional analysis includes North America, Europe, Asia Pacific, and RoW, enabling evaluation of demand patterns, growth drivers, and industry trends.

Reasons to Buy the Report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the hydrogen sensor market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (rapid expansion of the hydrogen economy and clean energy transition, increasing adoption of fuel cell electric vehicles (FCEVs)); restraints (high cost of advanced hydrogen sensing technologies, sensor poisoning, and cross-sensitivity issues); opportunities (integration with IoT-based industrial safety systems, advancements in nanomaterial-based hydrogen sensors); and challenges (achieving high selectivity and ultra-low detection limits, reliability in harsh industrial environments) influencing the growth of the hydrogen sensor market

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the hydrogen sensor market

- Market Development: Comprehensive information about lucrative markets by analyzing the hydrogen sensor market across varied regions

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the hydrogen sensor market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Amphenol Corporation (US), Honeywell International Inc. (US), Nissha Co., Ltd. (Japan), Schaeffler AG (US), AMETEK, Inc. (US), Figaro Engineering Inc. (Japan), Valeo (France), Membrapor AG (Switzerland), Zhengzhou Winsen Electronics Technology Co., Ltd. (China), and Posifa Technologies, Inc. (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING HYDROGEN SENSOR MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HYDROGEN SENSOR MARKET

- 3.2 HYDROGEN SENSOR MARKET, BY TECHNOLOGY

- 3.3 HYDROGEN SENSOR MARKET, BY DETECTION RANGE

- 3.4 HYDROGEN SENSOR MARKET, BY INDUSTRY

- 3.5 HYDROGEN SENSOR MARKET IN ASIA PACIFIC, BY INDUSTRY AND COUNTRY

- 3.6 HYDROGEN SENSOR MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid shift toward low-carbon energy systems

- 4.2.1.2 Mounting adoption of fuel cell electric vehicles to support low-emission transportation

- 4.2.1.3 Rising implementation of stringent safety standards for hydrogen storage, handling, and transportation

- 4.2.1.4 Increasing investment in hydrogen refueling infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 High development and production costs of advanced hydrogen sensing technologies

- 4.2.2.2 Sensor poisoning and cross-sensitivity issues

- 4.2.2.3 Limited standardization of multiple technologies

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising integration of hydrogen sensors with Internet of Things platforms

- 4.2.3.2 Growing popularity of nanomaterial-based hydrogen sensors

- 4.2.3.3 High emphasis on industrial decarbonization in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Complexities in achieving high selectivity and ultra-low detection limits

- 4.2.4.2 Issues in maintaining consistent performance in harsh industrial environments

- 4.2.4.3 Complexities in integrating hydrogen sensors into existing industrial systems

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL OIL & GAS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF HYDROGEN SENSORS, BY KEY PLAYER, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF HYDROGEN SENSORS, BY TECHNOLOGY, 2022-2025

- 5.5.3 AVERAGE SELLING PRICE TREND OF HYDROGEN SENSORS, BY REGION, 2022-2025

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (902710)

- 5.7.2 EXPORT SCENARIO (902710)

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 US-BASED AUTOMOTIVE MANUFACTURER DEPLOYS H2SCAN'S HYDROGEN SENSORS TO ELIMINATE CROSS-SENSITIVITY ISSUES AND IMPROVE OPERATIONAL EFFICIENCY

- 5.10.2 MANUFACTURING FACILITIES IN NORTH AMERICA USE GAO TEK'S HYDROGEN GAS DETECTORS TO MAINTAIN SAFE WORKING ENVIRONMENTS

- 5.10.3 UTILITY & POWER INFRASTRUCTURE OPERATORS ADOPT H2SCAN'S SOLID-STATE HYDROGEN SENSOR TO ENABLE EARLY FAULT DETECTION AND REDUCE DOWNTIME

- 5.10.4 HYDROGEN PRODUCTION AND STORAGE ENVIRONMENTS ACHIEVE ENHANCED SAFETY AND REGULATORY COMPLIANCE USING HONEYWELL'S HYDROGEN SENSORS

- 5.11 IMPACT OF US TARIFFS - HYDROGEN SENSOR MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 NANOMATERIAL-BASED HYDROGEN SENSORS

- 6.1.2 MEMS-BASED HYDROGEN SENSORS

- 6.1.3 OPTICAL FIBER HYDROGEN SENSORS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF THINGS-ENABLED GAS MONITORING PLATFORMS

- 6.2.2 ARTIFICIAL INTELLIGENCE/MACHINE LEARNING-BASED PREDICTIVE GAS DETECTION ANALYTICS

- 6.2.3 WIRELESS SAFETY MONITORING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYDROGEN FUEL CELL MONITORING SYSTEMS

- 6.3.2 INDUSTRIAL GAS DETECTION SYSTEMS

- 6.3.3 HYDROGEN STORAGE & LEAK DETECTION SYSTEMS

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON HYDROGEN SENSOR MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN HYDROGEN SENSOR MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN HYDROGEN SENSOR MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED HYDROGEN SENSORS

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

9 APPLICATIONS OF HYDROGEN SENSORS

- 9.1 INTRODUCTION

- 9.2 SAFETY & LEAK DETECTION

- 9.3 PROCESS CONTROL & MONITORING

- 9.3.1 HYDROGEN GAS CONCENTRATION MONITORING

- 9.3.2 ELECTRICAL STACK MONITORING

- 9.4 QUALITY ASSURANCE

- 9.5 EMISSION MONITORING

10 HYDROGEN SENSOR MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 ELECTROCHEMICAL

- 10.2.1 NEED TO ACCURATELY DETECT HYDROGEN AT LOW-CONCENTRATION LEVELS TO BOLSTER SEGMENTAL GROWTH

- 10.3 MOS

- 10.3.1 COST-EFFECTIVENESS, SIMPLICITY, AND LONG OPERATIONAL LIFE TO ACCELERATE SEGMENTAL GROWTH

- 10.4 THERMAL CONDUCTIVITY

- 10.4.1 USE TO MEASURE HIGH HYDROGEN CONCENTRATIONS IN INDUSTRIAL APPLICATIONS TO FUEL SEGMENTAL GROWTH

- 10.5 CATALYTIC

- 10.5.1 ABILITY TO DETECT HYDROGEN CONCENTRATIONS NEAR EXPLOSIVE LIMITS TO EXPEDITE SEGMENTAL GROWTH

- 10.6 OTHER TECHNOLOGIES

11 HYDROGEN SENSOR MARKET, BY DETECTION RANGE

- 11.1 INTRODUCTION

- 11.2 BELOW 1,000 PPM

- 11.2.1 SURGING ADOPTION OF HIGH-SENSITIVITY SENSORS FOR EARLY LEAK DETECTION TO FOSTER SEGMENTAL GROWTH

- 11.3 1,000-10,000 PPM

- 11.3.1 GROWING FOCUS ON INDUSTRIAL SAFETY AND INFRASTRUCTURE MONITORING TO ACCELERATE SEGMENTAL GROWTH

- 11.4 ABOVE 10,000 PPM

- 11.4.1 INCREASING USE IN PROCESS CONTROL AND EFFICIENCY OPTIMIZATION APPLICATIONS TO DRIVE MARKET

12 HYDROGEN SENSOR MARKET, BY INDUSTRY

- 12.1 INTRODUCTION

- 12.2 OIL & GAS

- 12.2.1 INCREASING INVESTMENT IN LOW-CARBON FUEL PROJECTS TO BOOST SEGMENTAL GROWTH

- 12.2.2 REFINERIES

- 12.2.3 PETROCHEMICAL PLANTS

- 12.2.4 PIPELINE MONITORING

- 12.2.5 OFFSHORE PLATFORMS

- 12.3 AUTOMOTIVE

- 12.3.1 RAPID COMMERCIALIZATION OF HYDROGEN FUEL CELL ELECTRIC VEHICLES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 12.3.2 FUEL CELL ELECTRIC VEHICLES

- 12.3.3 HYDROGEN STORAGE SYSTEMS

- 12.3.4 REFUELING STATIONS

- 12.3.5 SAFETY MONITORING SYSTEMS

- 12.4 CHEMICALS

- 12.4.1 GROWING EMPHASIS ON HIGH ACCURACY, CHEMICAL RESISTANCE, AND CALIBRATION STABILITY TO EXPEDITE SEGMENTAL GROWTH

- 12.4.2 PRODUCTION FACILITIES

- 12.4.3 PROCESS MONITORING

- 12.4.4 LEAK DETECTION SYSTEMS

- 12.5 MANUFACTURING

- 12.5.1 STRONG FOCUS ON MEETING CLEANROOM OR FOOD-SAFE COMPATIBILITY REQUIREMENTS TO AUGMENT SEGMENTAL GROWTH

- 12.5.2 METAL PROCESSING

- 12.5.3 ELECTRONICS MANUFACTURING

- 12.5.4 GLASS PRODUCTION

- 12.5.5 FOOD PROCESSING

- 12.6 POWER & ENERGY

- 12.6.1 INCREASING NEED FOR QUALITY ASSURANCE AND PROCESS OPTIMIZATION TO BOLSTER SEGMENTAL GROWTH

- 12.6.2 HYDROGEN POWER PLANTS

- 12.6.3 COMBINED HEAT AND POWER

- 12.6.4 BACKUP POWER SYSTEMS

- 12.6.5 HYDROGEN PRODUCTION FACILITIES

- 12.6.6 ELECTROLYZERS

- 12.6.7 STORAGE FACILITIES

- 12.6.8 DISTRIBUTION NETWORKS

- 12.7 OTHER INDUSTRIES

- 12.7.1 RESEARCH & LABORATORY

- 12.7.1.1 Academic institutions

- 12.7.1.2 R&D centers

- 12.7.1.3 Testing facilities

- 12.7.2 AEROSPACE & DEFENSE

- 12.7.2.1 Aircraft fuel systems

- 12.7.2.2 Space

- 12.7.2.3 Military vehicles

- 12.7.1 RESEARCH & LABORATORY

13 HYDROGEN SENSOR MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Rising hydrogen infrastructure development and low-carbon energy transition to boost market growth

- 13.2.2 CANADA

- 13.2.2.1 Increasing investment in hydrogen production facilities and fuel cell technologies to foster market growth

- 13.2.3 MEXICO

- 13.2.3.1 Growing emphasis on clean energy adoption and industrial modernization to augment market growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Strong focus on green hydrogen production, carbon capture integration, and industrial decarbonization to drive market

- 13.3.2 GERMANY

- 13.3.2.1 Strategic investments in green energy projects to contribute to market growth

- 13.3.3 FRANCE

- 13.3.3.1 Growing emphasis on sustainability and energy transition to accelerate market growth

- 13.3.4 ITALY

- 13.3.4.1 Increasing hydrogen initiatives and industrial transition to fuel market growth

- 13.3.5 SPAIN

- 13.3.5.1 Large-scale green hydrogen production projects to expedite market growth

- 13.3.6 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rapid expansion of hydrogen refueling stations to drive market

- 13.4.2 JAPAN

- 13.4.2.1 Long-term clean energy transition strategies to accelerate market growth

- 13.4.3 INDIA

- 13.4.3.1 Government-led initiatives to support decarbonization to foster market growth

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Strong hydrogen economy roadmap and industrial investments to expedite market growth

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 ROW

- 13.5.1 SOUTH AMERICA

- 13.5.1.1 Increasing focus on hydrogen infrastructure development and energy diversification to bolster market growth

- 13.5.2 MIDDLE EAST

- 13.5.2.1 High investment in large-scale green and blue hydrogen projects to contribute to market growth

- 13.5.3 AFRICA

- 13.5.3.1 Rising emphasis on safe operations across production, storage, and transportation infrastructure to drive market

- 13.5.1 SOUTH AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2022-2026

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND COMPARISON

- 14.6.1 SGX SENSORTECH (SWITZERLAND)

- 14.6.2 FIGARO ENGINEERING INC. (JAPAN)

- 14.6.3 AMETEK (US)

- 14.6.4 HONEYWELL (US)

- 14.6.5 NISSHA CO., LTD. (JAPAN)

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Technology footprint

- 14.7.5.4 Detection range footprint

- 14.7.5.5 Industry footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AMPHENOL CORPORATION

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths/Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses/Competitive threats

- 15.1.2 HONEYWELL INTERNATIONAL INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths/Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses/Competitive threats

- 15.1.3 AMETEK, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 MnM view

- 15.1.3.3.1 Key strengths/Right to win

- 15.1.3.3.2 Strategic choices

- 15.1.3.3.3 Weaknesses/Competitive threats

- 15.1.4 FIGARO ENGINEERING INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths/Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses/Competitive threats

- 15.1.5 NISSHA CO., LTD.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths/Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses/Competitive threats

- 15.1.6 ZHENGZHOU WINSEN ELECTRONICS TECHNOLOGY CO., LTD.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 MnM view

- 15.1.6.3.1 Key strengths/Right to win

- 15.1.6.3.2 Strategic choices

- 15.1.6.3.3 Weaknesses/Competitive threats

- 15.1.7 MARQUARDT MANAGEMENT SE

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.4 MnM view

- 15.1.7.4.1 Key strengths/Right to win

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses/Competitive threats

- 15.1.8 VALEO

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 SCHAEFFLER AG

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 CUBIC SENSOR AND INSTRUMENT CO., LTD.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Expansions

- 15.1.11 POSIFA TECHNOLOGIES, INC.

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.3.2 Deals

- 15.1.11.3.3 Expansions

- 15.1.1 AMPHENOL CORPORATION

- 15.2 OTHER PLAYERS

- 15.2.1 SENSIDYNE, LP.

- 15.2.2 SHENZHEN PROSENSE TECHNOLOGIES CO., LTD.

- 15.2.3 SENSORIX GMBH

- 15.2.4 SEMEATECH INC.

- 15.2.5 SENSIRION AG

- 15.2.6 UNIPHOS

- 15.2.7 SHANGHAI SANGBAY SENSOR TECHNOLOGY CO., LTD.

- 15.2.8 WEATHERALL EQUIPMENT & INSTRUMENTS LTD

- 15.2.9 MAKEL ENGINEERING, INC.

- 15.2.10 SENKO CO., LTD.

- 15.2.11 DYNAMENT

- 15.2.12 MEMBRAPOR

- 15.2.13 AEROQUAL

- 15.2.14 KIMO ELECTRONIC PVT. LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY AND PRIMARY RESEARCH

- 16.1.2 SECONDARY DATA

- 16.1.2.1 List of key secondary sources

- 16.1.2.2 Key data from secondary sources

- 16.1.3 PRIMARY DATA

- 16.1.3.1 List of primary interview participants

- 16.1.3.2 Key data from primary sources

- 16.1.3.3 Key industry insights

- 16.1.3.4 Breakdown of primary interviews

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 16.3 MARKET FORECAST APPROACH

- 16.3.1 SUPPLY-SIDE

- 16.3.2 DEMAND-SIDE

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS